Management Accounting: Processes, Tools, and Adaptation to Financial Problems

VerifiedAdded on 2023/01/03

|14

|2511

|42

AI Summary

This document provides an overview of management accounting processes and practices, focusing on the case of Prime Furniture. It covers topics such as cost calculation, different planning tools, and the advantages and disadvantages of these tools. It also explores how organizations adapt their management accounting systems to respond to financial problems. The document offers insights into the importance of management accounting in decision-making and financial governance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Covered in PPT.......................................................................................................................................3

TASK 2..........................................................................................................................................................3

P3. Cost Calculate cost and presentation of different planning tools......................................................3

TASK 3..........................................................................................................................................................9

P4. Explain the advantages and disadvantages of different types of planning tools.................................9

P5. Compare how organizations are adapting management accounting systems to respond to financial

problem.................................................................................................................................................11

CONCLUSION.............................................................................................................................................13

REFERENCES..............................................................................................................................................14

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

Covered in PPT.......................................................................................................................................3

TASK 2..........................................................................................................................................................3

P3. Cost Calculate cost and presentation of different planning tools......................................................3

TASK 3..........................................................................................................................................................9

P4. Explain the advantages and disadvantages of different types of planning tools.................................9

P5. Compare how organizations are adapting management accounting systems to respond to financial

problem.................................................................................................................................................11

CONCLUSION.............................................................................................................................................13

REFERENCES..............................................................................................................................................14

INTRODUCTION

Management Accounting means that organizational processes and responsible actions are

conducted and executed in such a manner as to efficiency meet the commercial intent (Van der

Stede, 2015). In particular, it is used to select the internal motivations that provide financial and

non-fiscal knowledge of the organization. This study addresses topics such as knowing MA

processes and monitoring practices as a growing East London-based company, Prime Furniture.

Calculation of various costs based on successful methods was also carried out. Moreover this

report further explains how distinct forecasting approaches and tools are used in management

accounting and how businesses should use them in addressing financial problems.

TASK 1

Covered in PPT

TASK 2

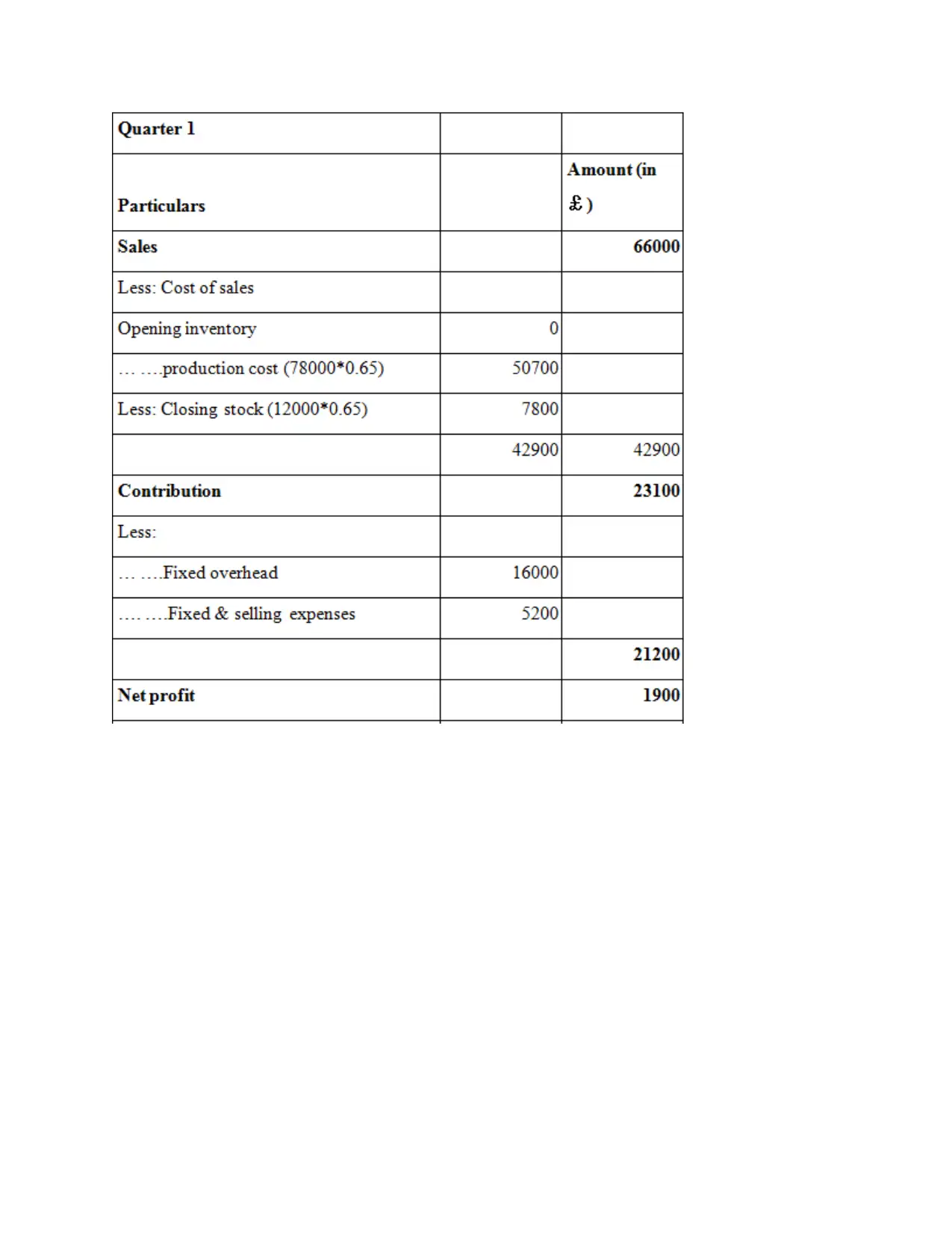

P3. Cost Calculate cost and presentation of different planning tools

Absorption Costing: the critical costing approach is used in estimating commodity costs at the

expense of two basic expenditures, both direct and indirect (Modell, 2014). In estimation the

value of the commodity is measured both implicitly and explicitly. Restricted use of absorption

costs is a major technology in regard to Prime Furniture, with a view to reducing spending and

optimal use of energy.

Management Accounting means that organizational processes and responsible actions are

conducted and executed in such a manner as to efficiency meet the commercial intent (Van der

Stede, 2015). In particular, it is used to select the internal motivations that provide financial and

non-fiscal knowledge of the organization. This study addresses topics such as knowing MA

processes and monitoring practices as a growing East London-based company, Prime Furniture.

Calculation of various costs based on successful methods was also carried out. Moreover this

report further explains how distinct forecasting approaches and tools are used in management

accounting and how businesses should use them in addressing financial problems.

TASK 1

Covered in PPT

TASK 2

P3. Cost Calculate cost and presentation of different planning tools

Absorption Costing: the critical costing approach is used in estimating commodity costs at the

expense of two basic expenditures, both direct and indirect (Modell, 2014). In estimation the

value of the commodity is measured both implicitly and explicitly. Restricted use of absorption

costs is a major technology in regard to Prime Furniture, with a view to reducing spending and

optimal use of energy.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Marginal cost: The cost estimation method is used to measure the manufacturing costs whereby a

fixed cost function is not taken into account in evaluating the gross production costs of the

business. This concentrates on distinct pieces or variants of the budget include production costs,

work costs, operational costs for sells as well as handling (Lavia López and Hiebl, 2015). For the

Prime furniture Limited, additional equipment involved with the manufacture of the commodity

is paid marginal costs.

fixed cost function is not taken into account in evaluating the gross production costs of the

business. This concentrates on distinct pieces or variants of the budget include production costs,

work costs, operational costs for sells as well as handling (Lavia López and Hiebl, 2015). For the

Prime furniture Limited, additional equipment involved with the manufacture of the commodity

is paid marginal costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

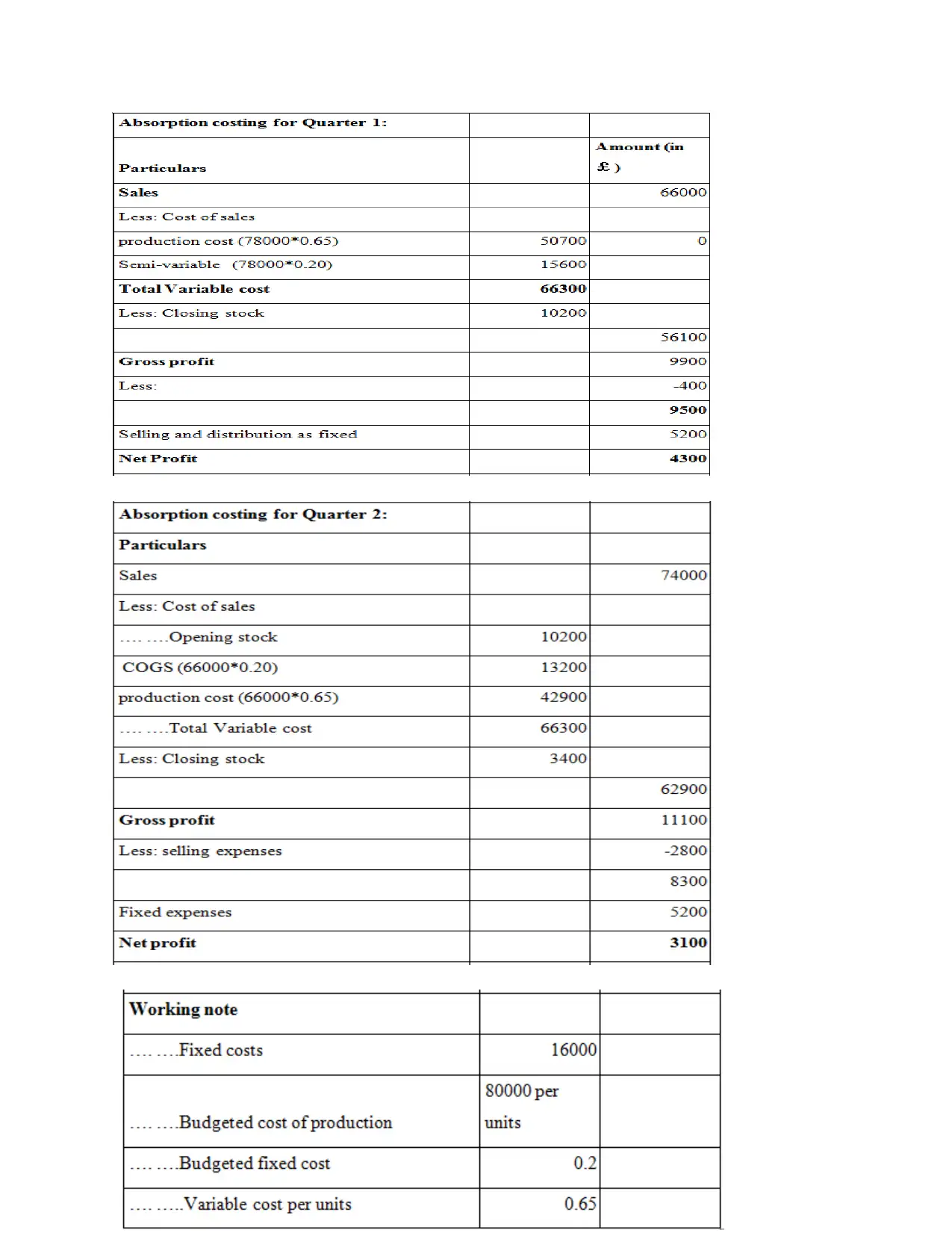

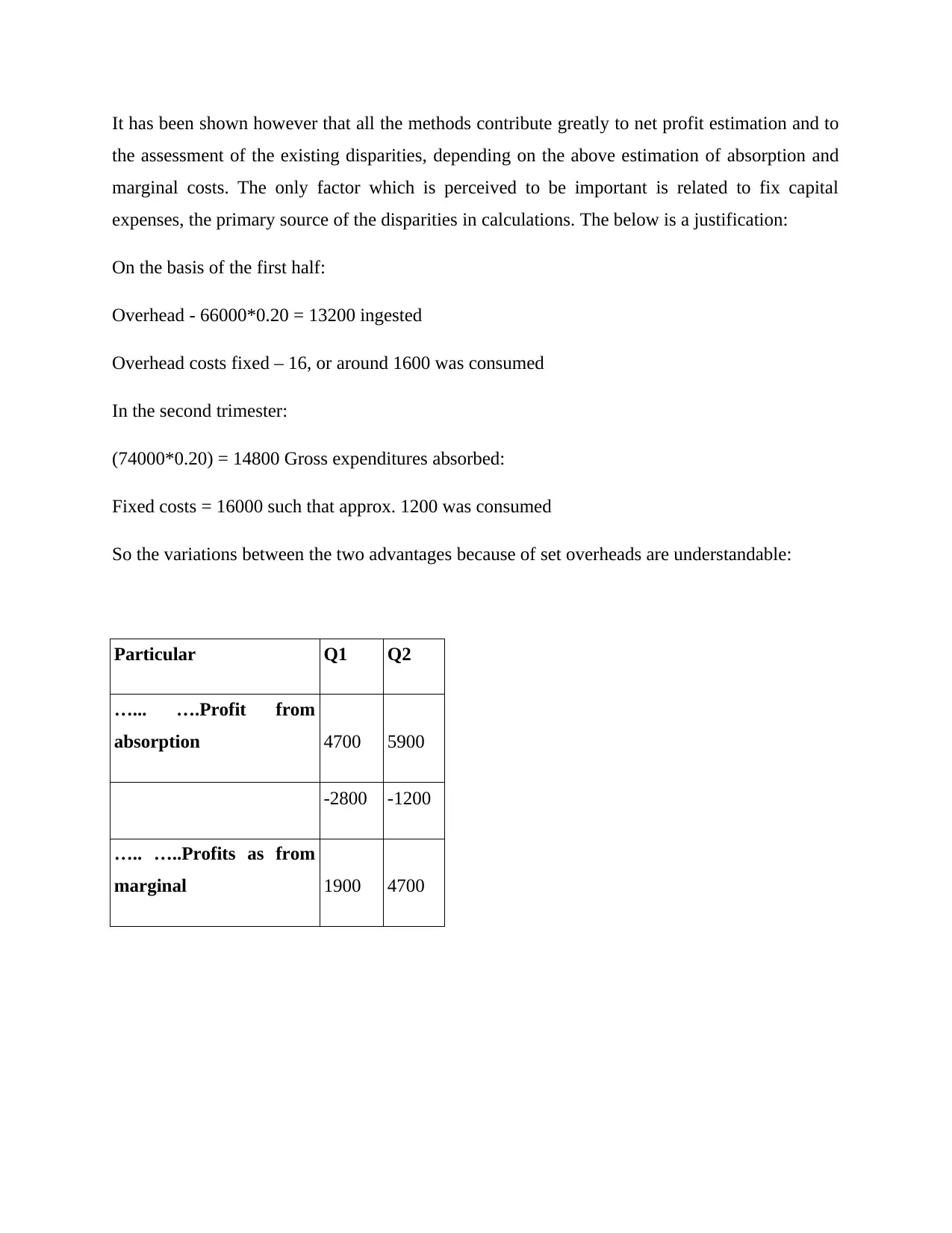

It has been shown however that all the methods contribute greatly to net profit estimation and to

the assessment of the existing disparities, depending on the above estimation of absorption and

marginal costs. The only factor which is perceived to be important is related to fix capital

expenses, the primary source of the disparities in calculations. The below is a justification:

On the basis of the first half:

Overhead - 66000*0.20 = 13200 ingested

Overhead costs fixed – 16, or around 1600 was consumed

In the second trimester:

(74000*0.20) = 14800 Gross expenditures absorbed:

Fixed costs = 16000 such that approx. 1200 was consumed

So the variations between the two advantages because of set overheads are understandable:

Particular Q1 Q2

…... ….Profit from

absorption 4700 5900

-2800 -1200

….. …..Profits as from

marginal 1900 4700

the assessment of the existing disparities, depending on the above estimation of absorption and

marginal costs. The only factor which is perceived to be important is related to fix capital

expenses, the primary source of the disparities in calculations. The below is a justification:

On the basis of the first half:

Overhead - 66000*0.20 = 13200 ingested

Overhead costs fixed – 16, or around 1600 was consumed

In the second trimester:

(74000*0.20) = 14800 Gross expenditures absorbed:

Fixed costs = 16000 such that approx. 1200 was consumed

So the variations between the two advantages because of set overheads are understandable:

Particular Q1 Q2

…... ….Profit from

absorption 4700 5900

-2800 -1200

….. …..Profits as from

marginal 1900 4700

TASK 3

P4. Explain the advantages and disadvantages of different types of planning tools

The budget is to prepare all of the company's costs before a new project is launched. Any

organization makes the Budget planned based on the revenue and expenses so that they can

maximize the usage of capital as well as minimize needless costs of an agency. Different forms

and value of a budget are described below the following are:

Sales Budget—this budget covers unit sales and assists with the measurement of the gain from

those sales of Prime Furniture. Financial plan may be strategies and processes that assist the

business in the manufacture or trading of products and services within a certain time period

(Kamal, 2015).

Benefits - This kind of budget is essential for origin allocation for various goods and services in

order to help to organize projected sales. It also contributes to the framing of distribution

processes so that the organization can meet its designed sales targets and objectives.

Disadvantages – This form of budget requires time and can easily be embraced by the company's

staff. The potential type of behavior cannot be efficiently articulated.

Budget for production—this budget in the corresponding company is a tax schedule composed of

a variety of units generated at a given time. In this business, order to analyze how many units can

be generated by predictable furor needs. The management of the organization will receive

information on the output of products that are required to satisfy customer demands with the aid

of this financial strategy.

Advantages—It is important to manage and to lower the production unit costs and order supplies,

to help run and design the work on raw material, final product as well as stock operation.

Disadvantages: there is a shortage of versatility in this plan as there are multiple covariant in the

control of the efficient phase of organization.

P4. Explain the advantages and disadvantages of different types of planning tools

The budget is to prepare all of the company's costs before a new project is launched. Any

organization makes the Budget planned based on the revenue and expenses so that they can

maximize the usage of capital as well as minimize needless costs of an agency. Different forms

and value of a budget are described below the following are:

Sales Budget—this budget covers unit sales and assists with the measurement of the gain from

those sales of Prime Furniture. Financial plan may be strategies and processes that assist the

business in the manufacture or trading of products and services within a certain time period

(Kamal, 2015).

Benefits - This kind of budget is essential for origin allocation for various goods and services in

order to help to organize projected sales. It also contributes to the framing of distribution

processes so that the organization can meet its designed sales targets and objectives.

Disadvantages – This form of budget requires time and can easily be embraced by the company's

staff. The potential type of behavior cannot be efficiently articulated.

Budget for production—this budget in the corresponding company is a tax schedule composed of

a variety of units generated at a given time. In this business, order to analyze how many units can

be generated by predictable furor needs. The management of the organization will receive

information on the output of products that are required to satisfy customer demands with the aid

of this financial strategy.

Advantages—It is important to manage and to lower the production unit costs and order supplies,

to help run and design the work on raw material, final product as well as stock operation.

Disadvantages: there is a shortage of versatility in this plan as there are multiple covariant in the

control of the efficient phase of organization.

Cash flow budget – In Prime Furniture, all funds and costs that are normal to be created in a

certain period are calculated. This estimation is available on a weekly, quarterly, and annual

basis related to cash receipts and payments.

Advantages—the Company is efficient and tends to assess the weather of the fund that is

maintained and used in many events.

Disadvantages – This form of budget operation needs more effort and is less versatile because of

its consistent commercial position and its introduction to the leadership aspect of the firm.

Operating schedule: The finance officer plans all sales and expenses for a single time area

organizational budget. This plan type encompasses projects that are planned for the company's

profits (Alsharari, Dixon and Youssef, 2015). This plan can be available on a weekly, half-

annual, quarterly and annualized basis. For the Prime furniture limited company, the overall

budget may be adopted to control its output for the short term and to retain continuity of its

market.

Advantages -This leads to recognizing the present strength and vulnerabilities of society for

which actions are intended to recognize and effectively resolve the problem. It allows Prime

Furniture to accomplish its short-term objectives.

Disadvantages – coordination loss is one of the popular issues that can occur in separate sections

during operating plan computation in different sections. Variance research will take time to

conclude the leadership.

Cash Budget: This budget form is used specifically for estimating expense and spending

revenues on the basis of a particular estimate for the term. The Prime furniture company's use of

the cash budget leads to tracking financial transactions as well as to the review of the

corporation's actual status, which assists both different stakeholders.

Advantages - This form of costs allows controlling the company's costs that have lowered the

cost and improved the profit margins. It helps to foresee the financial position of the company by

taking investment decision.

certain period are calculated. This estimation is available on a weekly, quarterly, and annual

basis related to cash receipts and payments.

Advantages—the Company is efficient and tends to assess the weather of the fund that is

maintained and used in many events.

Disadvantages – This form of budget operation needs more effort and is less versatile because of

its consistent commercial position and its introduction to the leadership aspect of the firm.

Operating schedule: The finance officer plans all sales and expenses for a single time area

organizational budget. This plan type encompasses projects that are planned for the company's

profits (Alsharari, Dixon and Youssef, 2015). This plan can be available on a weekly, half-

annual, quarterly and annualized basis. For the Prime furniture limited company, the overall

budget may be adopted to control its output for the short term and to retain continuity of its

market.

Advantages -This leads to recognizing the present strength and vulnerabilities of society for

which actions are intended to recognize and effectively resolve the problem. It allows Prime

Furniture to accomplish its short-term objectives.

Disadvantages – coordination loss is one of the popular issues that can occur in separate sections

during operating plan computation in different sections. Variance research will take time to

conclude the leadership.

Cash Budget: This budget form is used specifically for estimating expense and spending

revenues on the basis of a particular estimate for the term. The Prime furniture company's use of

the cash budget leads to tracking financial transactions as well as to the review of the

corporation's actual status, which assists both different stakeholders.

Advantages - This form of costs allows controlling the company's costs that have lowered the

cost and improved the profit margins. It helps to foresee the financial position of the company by

taking investment decision.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Disadvantages-The outcome decided is impossible to obtain because it does not cover non-

currency expenses and the whole cash reliance is not just the solution for business.

Pricing strategies: pricing schemes help predict the cost and service costs so that current and

future consumers can be drawn to them more and more. Prime Furniture Corporation requires

various forms of price strategies to help company's reputation and sustain profit margins in the

particular financial year. It helps in the enhancement of product performance with respect to the

opponent, so the following are separate methods:

Cost plus pricing: it is an effective mechanism by which good prices are set during output for a

given amount of time. The expense of work includes manufacturing expenses and production

expenses raised by the sale of goods and services.

Full costing pricing: This is known as a constructive approach in which the rate is assigned to

commodity cost with the price taken direct by the retailer over a real span of time.

Differences in budget

This shows the difference between fundamental value and cash price in terms of cost, income,

and real value. It refers to the actual sum for a specific accounting class for the corresponding

business (Quinn, 2014). These variances emerge because they cannot track the coming fund and

productivity in full detail.

Significance of a financial deviation- It allows to monitor expenditures by the monitoring of

budget and true expenses, it helps define or decides the reason for the calculation and oversight

of the material. With the assistance of Prime Furniture, the management can negotiate significant

variances with program managers and make resolutions.

TASK 4

P5. Compare how organizations are adapting management accounting systems to respond to

financial problem

Financial problem: applies to the vital and unnecessary situations that cause difficulties when

undertaking financial operations. There may be fiscal mechanisms and activities that produce

challenges and hurdles to the successful activity of the venture sector (Nielsen, Mitchell and

currency expenses and the whole cash reliance is not just the solution for business.

Pricing strategies: pricing schemes help predict the cost and service costs so that current and

future consumers can be drawn to them more and more. Prime Furniture Corporation requires

various forms of price strategies to help company's reputation and sustain profit margins in the

particular financial year. It helps in the enhancement of product performance with respect to the

opponent, so the following are separate methods:

Cost plus pricing: it is an effective mechanism by which good prices are set during output for a

given amount of time. The expense of work includes manufacturing expenses and production

expenses raised by the sale of goods and services.

Full costing pricing: This is known as a constructive approach in which the rate is assigned to

commodity cost with the price taken direct by the retailer over a real span of time.

Differences in budget

This shows the difference between fundamental value and cash price in terms of cost, income,

and real value. It refers to the actual sum for a specific accounting class for the corresponding

business (Quinn, 2014). These variances emerge because they cannot track the coming fund and

productivity in full detail.

Significance of a financial deviation- It allows to monitor expenditures by the monitoring of

budget and true expenses, it helps define or decides the reason for the calculation and oversight

of the material. With the assistance of Prime Furniture, the management can negotiate significant

variances with program managers and make resolutions.

TASK 4

P5. Compare how organizations are adapting management accounting systems to respond to

financial problem

Financial problem: applies to the vital and unnecessary situations that cause difficulties when

undertaking financial operations. There may be fiscal mechanisms and activities that produce

challenges and hurdles to the successful activity of the venture sector (Nielsen, Mitchell and

Nørreklit, 2015). In Prime Furniture, it may be a lack of funds under which the firm does not

conduct its programs, its operations, and its causes, etc. The monetary benefit that business

entities can suffer from differs. Any of the following questions are discussed:

Disparate cash flow: As a cash flow, the business's market, acquisition and financial operations

require various considerations. In this case the company creates a cash balance that does not fit

the financial operations and creates the financial issue.

Unneeded expenditure: The business is unable, as a result of this problem, to compete with the

sales and business expenditures because it plans to invest more than to produce more. This

unique concern allows the organization to confront the lack of issues when they are unstructured

to handle the company's internal operations.

Key performance indicators: The main performance metric applies to the unit of measurement

that lets the company identify whether this will efficiently or reliably advance for a given period

of time. The boss uses this matrix to track his job productivity and to encourage his or her

performance continuously. The omission of primary success metrics does not resolve and

consistently follow the current performance of the enterprise.

Benchmark: The other success metric by way of its current performance or by review of the

competitive plan is used to set levels of performance for internal stakeholders (Boučková, 2015).

This aims to boost overall job efficiency and job power, contributing to progress and the

productivity of an organization.

Financial governance: Financial governance refers to the collection, oversight, administration

and regulation of all the company's financial data. This helps businesses to conduct or administer

their financing through data monitoring and true reporting. It determines, in essence, the personal

duty of the internal administration to track the consistency of the report and to make financial or

benefit and loss reports efficient.

Comparison

Basis Seatable manufacturing limited Prime furniture limited

Financial Problem The organisation anticipates the The organization is faced with

conduct its programs, its operations, and its causes, etc. The monetary benefit that business

entities can suffer from differs. Any of the following questions are discussed:

Disparate cash flow: As a cash flow, the business's market, acquisition and financial operations

require various considerations. In this case the company creates a cash balance that does not fit

the financial operations and creates the financial issue.

Unneeded expenditure: The business is unable, as a result of this problem, to compete with the

sales and business expenditures because it plans to invest more than to produce more. This

unique concern allows the organization to confront the lack of issues when they are unstructured

to handle the company's internal operations.

Key performance indicators: The main performance metric applies to the unit of measurement

that lets the company identify whether this will efficiently or reliably advance for a given period

of time. The boss uses this matrix to track his job productivity and to encourage his or her

performance continuously. The omission of primary success metrics does not resolve and

consistently follow the current performance of the enterprise.

Benchmark: The other success metric by way of its current performance or by review of the

competitive plan is used to set levels of performance for internal stakeholders (Boučková, 2015).

This aims to boost overall job efficiency and job power, contributing to progress and the

productivity of an organization.

Financial governance: Financial governance refers to the collection, oversight, administration

and regulation of all the company's financial data. This helps businesses to conduct or administer

their financing through data monitoring and true reporting. It determines, in essence, the personal

duty of the internal administration to track the consistency of the report and to make financial or

benefit and loss reports efficient.

Comparison

Basis Seatable manufacturing limited Prime furniture limited

Financial Problem The organisation anticipates the The organization is faced with

issue of the profits that the

management team will easily

present or expend by keeping track

of all cash and non-cash activities.

the dilemma of an insufficient

cash balance due to high costs

and weak financing. This will

impact the company's financial

activities.

System To address the dilemma of the

constant structure of the financial

report, the managerial accounting

method is used. This helps to better

fix the financial issue (Quinn,

Strauss and Kristandl, 2014).

Inventory management system

feature enables address the

challenge by managing cash

balance and processing vast

volumes of refunds and

transactions.

CONCLUSION

From the above analysis, it has been shown that management accounting is an effective

mechanism which provides top management personnel with important information by converting

raw data into these details. The monitoring methods and techniques are used to allow

organizations to respond to financial problems. It is also useful in evaluating the outcomes and

success over a given period of time. Management accounting schemes of various sort exist and

are effective for deciding the firm ’s financial report and for handling the corporation to

administer and for monitoring the company's fiscal operation. Various kinds of forecasting

instruments often benefit the company, helping to schedule numerical value and manage the

company's spending. In the business, there are various kinds of tax problems. The venture should

use diverse accounts so the enterprise can run its operations efficiently and overcome these

financial crises sufficiently to eliminate and alleviate these tensions and uncertainties.

management team will easily

present or expend by keeping track

of all cash and non-cash activities.

the dilemma of an insufficient

cash balance due to high costs

and weak financing. This will

impact the company's financial

activities.

System To address the dilemma of the

constant structure of the financial

report, the managerial accounting

method is used. This helps to better

fix the financial issue (Quinn,

Strauss and Kristandl, 2014).

Inventory management system

feature enables address the

challenge by managing cash

balance and processing vast

volumes of refunds and

transactions.

CONCLUSION

From the above analysis, it has been shown that management accounting is an effective

mechanism which provides top management personnel with important information by converting

raw data into these details. The monitoring methods and techniques are used to allow

organizations to respond to financial problems. It is also useful in evaluating the outcomes and

success over a given period of time. Management accounting schemes of various sort exist and

are effective for deciding the firm ’s financial report and for handling the corporation to

administer and for monitoring the company's fiscal operation. Various kinds of forecasting

instruments often benefit the company, helping to schedule numerical value and manage the

company's spending. In the business, there are various kinds of tax problems. The venture should

use diverse accounts so the enterprise can run its operations efficiently and overcome these

financial crises sufficiently to eliminate and alleviate these tensions and uncertainties.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Van der Stede, W.A., 2015. Management accounting: Where from, where now, where

to?. Journal of Management Accounting Research, 27(1), pp.171-176.

Modell, S., 2014. The societal relevance of management accounting: An introduction to the

special issue. Accounting and Business Research, 44(2), pp.83-103.

Lavia López, O. and Hiebl, M.R., 2015. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research, 27(1), pp.81-119.

Kamal, S., 2015. Historical evolution of management accounting. The cost and

management, 43(4), pp.12-19.

Alsharari, N.M., Dixon, R. and Youssef, M.A.E.A., 2015. Management accounting change:

critical review and a new contextual framework. Journal of Accounting & Organizational

Change.

Quinn, M., 2014. Stability and change in management accounting over time—A century or so of

evidence from Guinness. Management Accounting Research, 25(1), pp.76-92.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and decision

making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No. 1, pp. 66-

82). Taylor & Francis.

Boučková, M., 2015. Management accounting and agency theory. Procedia Economics and

Finance, 25, pp.5-13.

Quinn, M., Strauss, E. and Kristandl, G., 2014. The effects of cloud technology on management

accounting and business decision-making. Financial Management, 10(6), pp.1-12.

Van der Stede, W.A., 2015. Management accounting: Where from, where now, where

to?. Journal of Management Accounting Research, 27(1), pp.171-176.

Modell, S., 2014. The societal relevance of management accounting: An introduction to the

special issue. Accounting and Business Research, 44(2), pp.83-103.

Lavia López, O. and Hiebl, M.R., 2015. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research, 27(1), pp.81-119.

Kamal, S., 2015. Historical evolution of management accounting. The cost and

management, 43(4), pp.12-19.

Alsharari, N.M., Dixon, R. and Youssef, M.A.E.A., 2015. Management accounting change:

critical review and a new contextual framework. Journal of Accounting & Organizational

Change.

Quinn, M., 2014. Stability and change in management accounting over time—A century or so of

evidence from Guinness. Management Accounting Research, 25(1), pp.76-92.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and decision

making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No. 1, pp. 66-

82). Taylor & Francis.

Boučková, M., 2015. Management accounting and agency theory. Procedia Economics and

Finance, 25, pp.5-13.

Quinn, M., Strauss, E. and Kristandl, G., 2014. The effects of cloud technology on management

accounting and business decision-making. Financial Management, 10(6), pp.1-12.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.