Management Accounting Report for Tech - Budget and Strategy

VerifiedAdded on 2020/09/03

|14

|4134

|32

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Tech. It begins with an introduction to management accounting, its essential requirements, and its importance in internal financial reporting and decision-making. The report then delves into the various types of managerial accounting reports used to present financial information, including job cost reports, inventory management reports, and operating budget reports. A key section of the report focuses on the preparation of an income statement for Tech using both absorption and marginal costing methods, comparing and contrasting the results. Furthermore, the report explores the significance of budgeting for planning and controlling purposes, covering financial and operating budgets. Finally, it examines the balance scorecard approach as a tool to address financial challenges within Tech, concluding with a summary of the key findings and recommendations. This report is a valuable resource for understanding financial management and strategic decision-making in a business context.

MANAGEMENT

ACCOUNTING REPORT

FOR TECH

ACCOUNTING REPORT

FOR TECH

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1 Management accounting and essential requirements.............................................................1

P2 Various types of managerial accounting reports to present financial reports........................3

TASK 2............................................................................................................................................4

P3 Income statement using absorption and marginal costing method for Tech.........................4

TASK 3............................................................................................................................................5

P4 Budget for planning and controlling purpose........................................................................5

TASK 4............................................................................................................................................8

P5 Balance scorecard approach to face the financial problems within Tech..............................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

P1 Management accounting and essential requirements.............................................................1

P2 Various types of managerial accounting reports to present financial reports........................3

TASK 2............................................................................................................................................4

P3 Income statement using absorption and marginal costing method for Tech.........................4

TASK 3............................................................................................................................................5

P4 Budget for planning and controlling purpose........................................................................5

TASK 4............................................................................................................................................8

P5 Balance scorecard approach to face the financial problems within Tech..............................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting and budget management will help organisation to manage and

control their cost and resources to respond financial problems in the firm. The report will cover

the management accounting and essential requirements. Income statement of Tech using

marginal and absorption costing method is also assessed with managing the budget in this report.

The balance scorecard approach to respond the financial problems within Tech will be discussed

in this report.

P1 Management accounting and essential requirements

MANAGEMENT ACCOUNTING

It is also known as cost and managerial accounting. Management accounting is useful to

make internal financial reports, accounting and decision making by analysing the costs of

business operations. This will also help management accountants at Tech to prepare costing and

financial data and translate it into useful information. This will help to control and achieve the

better planning for business activities (Armstrong, 2014). It also enhance the value of customers

and shareholders and help managers to use the resources effectively.

Importance of management accounting information for department managers as a decision

making tool: Management accounting information is crucial for managers in order to improve

their decision making for long terms with data driven inputs. For an example, Cost techniques

based on activity, information utilisation and relevant cost analysis etc.

Identify the performance metrics for managers in Tech.

Collect information and data to report the current performance of Tech to manager as

compared to the expectation.

Evaluate the deviation reasons and suggest appropriate measure.

Distinguishing financial accounting from management accounting

BASIS MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

DEFINITION A process which help manager by

providing essential information for

making plans, policies and

strategies.

It prepares financial statements Of

Tech to provide financial information

effectively.

INFORMATION Monetary and Non-monetary Monetary information only.

1

Management accounting and budget management will help organisation to manage and

control their cost and resources to respond financial problems in the firm. The report will cover

the management accounting and essential requirements. Income statement of Tech using

marginal and absorption costing method is also assessed with managing the budget in this report.

The balance scorecard approach to respond the financial problems within Tech will be discussed

in this report.

P1 Management accounting and essential requirements

MANAGEMENT ACCOUNTING

It is also known as cost and managerial accounting. Management accounting is useful to

make internal financial reports, accounting and decision making by analysing the costs of

business operations. This will also help management accountants at Tech to prepare costing and

financial data and translate it into useful information. This will help to control and achieve the

better planning for business activities (Armstrong, 2014). It also enhance the value of customers

and shareholders and help managers to use the resources effectively.

Importance of management accounting information for department managers as a decision

making tool: Management accounting information is crucial for managers in order to improve

their decision making for long terms with data driven inputs. For an example, Cost techniques

based on activity, information utilisation and relevant cost analysis etc.

Identify the performance metrics for managers in Tech.

Collect information and data to report the current performance of Tech to manager as

compared to the expectation.

Evaluate the deviation reasons and suggest appropriate measure.

Distinguishing financial accounting from management accounting

BASIS MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

DEFINITION A process which help manager by

providing essential information for

making plans, policies and

strategies.

It prepares financial statements Of

Tech to provide financial information

effectively.

INFORMATION Monetary and Non-monetary Monetary information only.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information.

TIME FRAME Reports are prepared according to

the needs.

Financial statements are prepared at

the end of year in accounting period

of time.

REPORT Complete and detailed information

for the reports.

Prepare summary report including

financial information at Tech.

Cost accounting system (actual, normal and standard costing): Cost accounting system will

help managers in Tech to evaluate the cost of services and products offered by them. The cost

data will help managers to control and manage the business resources with the help of plans and

strategies for future needs as well. Normal costing, actual costing, direct labour cost and

manufacturing overhead cost are related to the product cost which is used in cost of goods sold.

It will help manager to determine the actual selling cost of a product and service.

Manager can determine the profitability and able to meet the competition.

Identify the product and services cost which helps to manage the resources and decisions

accordingly.

Inventory management system: Inventory is includes the stock of products and resources such

as finished goods, raw materials and work in progress (Chandra, Menon and Mishra, 2016).

Managing the inventory will help manager in Tech to control and manage the resources which

help them to determine the availability, quantity and quality of stock effectively. Inventory cost

also involves cost of storage such as insurance, capital cost, taxes and facilities cost efficiently.

Inventory management system help managers to protect against shortage of resources and

uncertainties.

The system will also help to take advantage of economy scale which support the policies,

plans and strategies efficiently.

Job Casting system: Job casting is a process of cost recording and accumulation in which the

manger identify the present work cost to manage and control it easily and effectively. The system

is mostly used by those organisations where the production of product is 'one off' and also

different for a consumer. It is also used for the special demands of a customer towards a product

or service in a short period of time comparatively and effectively.

2

TIME FRAME Reports are prepared according to

the needs.

Financial statements are prepared at

the end of year in accounting period

of time.

REPORT Complete and detailed information

for the reports.

Prepare summary report including

financial information at Tech.

Cost accounting system (actual, normal and standard costing): Cost accounting system will

help managers in Tech to evaluate the cost of services and products offered by them. The cost

data will help managers to control and manage the business resources with the help of plans and

strategies for future needs as well. Normal costing, actual costing, direct labour cost and

manufacturing overhead cost are related to the product cost which is used in cost of goods sold.

It will help manager to determine the actual selling cost of a product and service.

Manager can determine the profitability and able to meet the competition.

Identify the product and services cost which helps to manage the resources and decisions

accordingly.

Inventory management system: Inventory is includes the stock of products and resources such

as finished goods, raw materials and work in progress (Chandra, Menon and Mishra, 2016).

Managing the inventory will help manager in Tech to control and manage the resources which

help them to determine the availability, quantity and quality of stock effectively. Inventory cost

also involves cost of storage such as insurance, capital cost, taxes and facilities cost efficiently.

Inventory management system help managers to protect against shortage of resources and

uncertainties.

The system will also help to take advantage of economy scale which support the policies,

plans and strategies efficiently.

Job Casting system: Job casting is a process of cost recording and accumulation in which the

manger identify the present work cost to manage and control it easily and effectively. The system

is mostly used by those organisations where the production of product is 'one off' and also

different for a consumer. It is also used for the special demands of a customer towards a product

or service in a short period of time comparatively and effectively.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It helps to establish the cost of planning, controlling and decision making of managers.

The system helps to calculate the product selling cost and also determine the profit and

loss effectively.

P2 Various types of managerial accounting reports to present financial reports

Job cost report: Job cost reports help managers in Tech to identify the cost of a project

or work. The job costing reports are usually combined with estimate revenues that helps

to determine the profitability from work done by employees. The report also help to

evaluate the cost while the work is in progress effectively and efficiently.

Inventory management report: Inventory management system which should be

physical is useful for Tech in order to manage and control the different inventory levels.

The different level which should be evaluated and managed by the manager such as,

quality, quantity and stock availability for products and services effectively and

efficiently.

Operating budget report: The operating budget analysation will help Tech manager to

evaluate the performance of various departments which will help to manage and control

the business operational costs under the budget effectively (Chiwamit, Modell and Yang,

2014). Operating budget is also helpful to provide rewards for the employee for the best

performances.

Accounts receivable ageing report: These reports will help manager to manage the cash

flow in Tech effectively. It is a critical tool that break downs the consumer balance at the

time thwy owned the organisation. It will also help to overlook the Tech previous debts.

Performance report: Performance report will help managers to assess the improvement

of product and services in the market. This will also help to analyse the profitability and

production from different departments. It will help manager to increase the overall

performance of employees to enhance the profits effectively.

IMPORTANCE

Management accounting reports are very useful for the Tech manager in order to make

effective and informed decisions for firm operational activities. Reports provide job cost, cost

and budget, performance and inventory management from which manager is able to take

appropriate decisions to increase the production and profitability. Financial and non-financial

information also help manager to manage and control the cost under the budget. Management

3

The system helps to calculate the product selling cost and also determine the profit and

loss effectively.

P2 Various types of managerial accounting reports to present financial reports

Job cost report: Job cost reports help managers in Tech to identify the cost of a project

or work. The job costing reports are usually combined with estimate revenues that helps

to determine the profitability from work done by employees. The report also help to

evaluate the cost while the work is in progress effectively and efficiently.

Inventory management report: Inventory management system which should be

physical is useful for Tech in order to manage and control the different inventory levels.

The different level which should be evaluated and managed by the manager such as,

quality, quantity and stock availability for products and services effectively and

efficiently.

Operating budget report: The operating budget analysation will help Tech manager to

evaluate the performance of various departments which will help to manage and control

the business operational costs under the budget effectively (Chiwamit, Modell and Yang,

2014). Operating budget is also helpful to provide rewards for the employee for the best

performances.

Accounts receivable ageing report: These reports will help manager to manage the cash

flow in Tech effectively. It is a critical tool that break downs the consumer balance at the

time thwy owned the organisation. It will also help to overlook the Tech previous debts.

Performance report: Performance report will help managers to assess the improvement

of product and services in the market. This will also help to analyse the profitability and

production from different departments. It will help manager to increase the overall

performance of employees to enhance the profits effectively.

IMPORTANCE

Management accounting reports are very useful for the Tech manager in order to make

effective and informed decisions for firm operational activities. Reports provide job cost, cost

and budget, performance and inventory management from which manager is able to take

appropriate decisions to increase the production and profitability. Financial and non-financial

information also help manager to manage and control the cost under the budget. Management

3

accounting reports are necessary to make effective strategies, plans and policies for the firm in

order to manage the performance of employees and organisation effectively and efficiently.

TASK 2

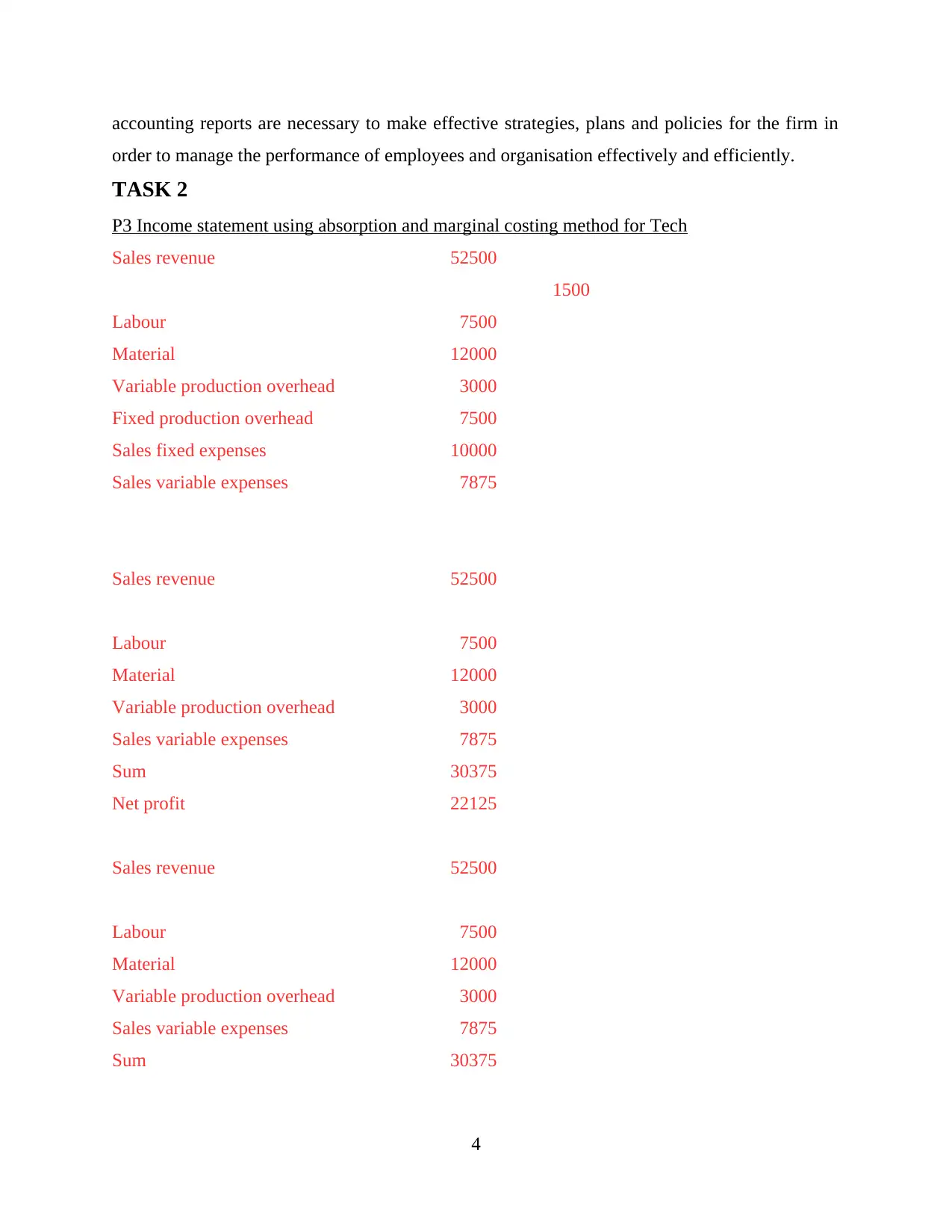

P3 Income statement using absorption and marginal costing method for Tech

Sales revenue 52500

1500

Labour 7500

Material 12000

Variable production overhead 3000

Fixed production overhead 7500

Sales fixed expenses 10000

Sales variable expenses 7875

Sales revenue 52500

Labour 7500

Material 12000

Variable production overhead 3000

Sales variable expenses 7875

Sum 30375

Net profit 22125

Sales revenue 52500

Labour 7500

Material 12000

Variable production overhead 3000

Sales variable expenses 7875

Sum 30375

4

order to manage the performance of employees and organisation effectively and efficiently.

TASK 2

P3 Income statement using absorption and marginal costing method for Tech

Sales revenue 52500

1500

Labour 7500

Material 12000

Variable production overhead 3000

Fixed production overhead 7500

Sales fixed expenses 10000

Sales variable expenses 7875

Sales revenue 52500

Labour 7500

Material 12000

Variable production overhead 3000

Sales variable expenses 7875

Sum 30375

Net profit 22125

Sales revenue 52500

Labour 7500

Material 12000

Variable production overhead 3000

Sales variable expenses 7875

Sum 30375

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed production overhead 7500

Sales fixed expenses 10000

Net profit 4625

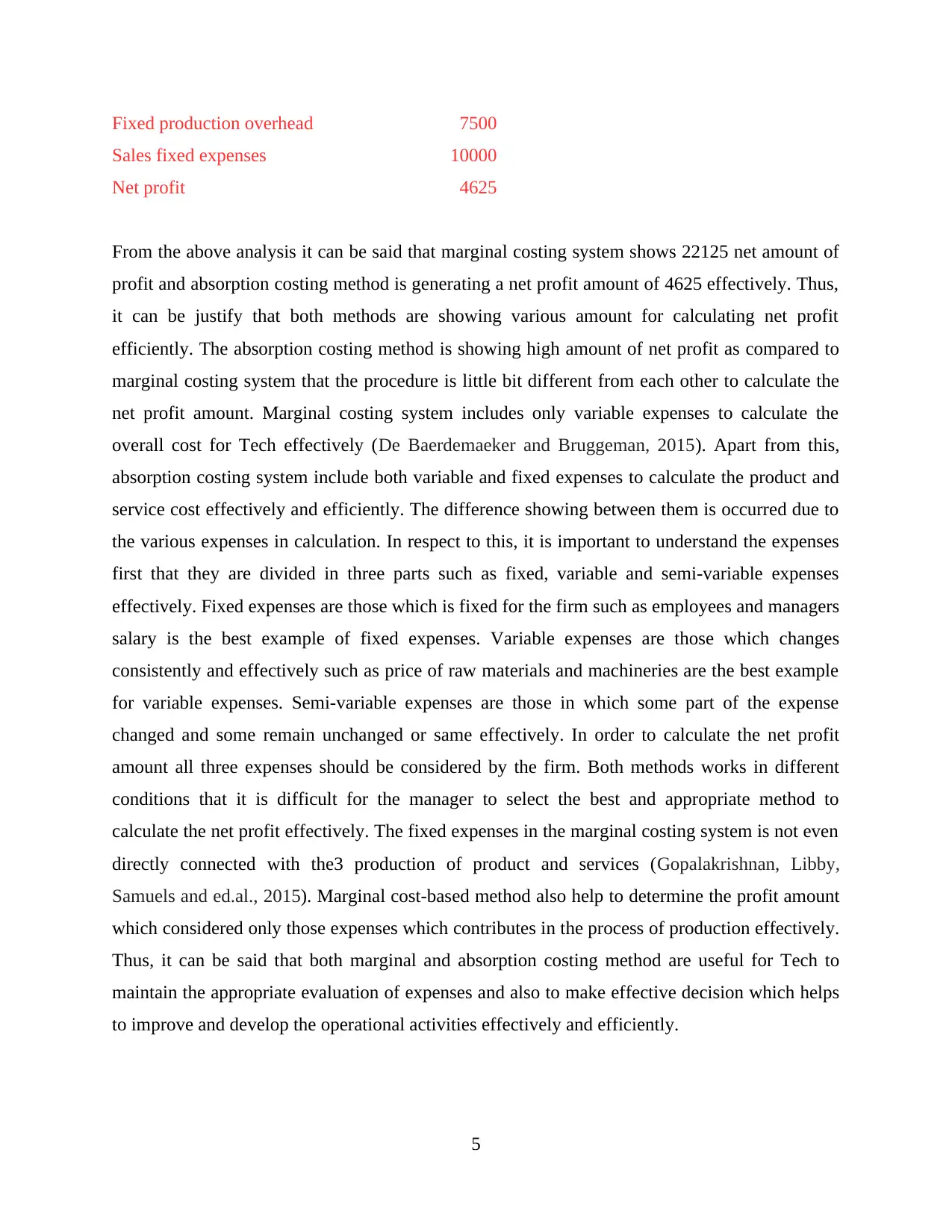

From the above analysis it can be said that marginal costing system shows 22125 net amount of

profit and absorption costing method is generating a net profit amount of 4625 effectively. Thus,

it can be justify that both methods are showing various amount for calculating net profit

efficiently. The absorption costing method is showing high amount of net profit as compared to

marginal costing system that the procedure is little bit different from each other to calculate the

net profit amount. Marginal costing system includes only variable expenses to calculate the

overall cost for Tech effectively (De Baerdemaeker and Bruggeman, 2015). Apart from this,

absorption costing system include both variable and fixed expenses to calculate the product and

service cost effectively and efficiently. The difference showing between them is occurred due to

the various expenses in calculation. In respect to this, it is important to understand the expenses

first that they are divided in three parts such as fixed, variable and semi-variable expenses

effectively. Fixed expenses are those which is fixed for the firm such as employees and managers

salary is the best example of fixed expenses. Variable expenses are those which changes

consistently and effectively such as price of raw materials and machineries are the best example

for variable expenses. Semi-variable expenses are those in which some part of the expense

changed and some remain unchanged or same effectively. In order to calculate the net profit

amount all three expenses should be considered by the firm. Both methods works in different

conditions that it is difficult for the manager to select the best and appropriate method to

calculate the net profit effectively. The fixed expenses in the marginal costing system is not even

directly connected with the3 production of product and services (Gopalakrishnan, Libby,

Samuels and ed.al., 2015). Marginal cost-based method also help to determine the profit amount

which considered only those expenses which contributes in the process of production effectively.

Thus, it can be said that both marginal and absorption costing method are useful for Tech to

maintain the appropriate evaluation of expenses and also to make effective decision which helps

to improve and develop the operational activities effectively and efficiently.

5

Sales fixed expenses 10000

Net profit 4625

From the above analysis it can be said that marginal costing system shows 22125 net amount of

profit and absorption costing method is generating a net profit amount of 4625 effectively. Thus,

it can be justify that both methods are showing various amount for calculating net profit

efficiently. The absorption costing method is showing high amount of net profit as compared to

marginal costing system that the procedure is little bit different from each other to calculate the

net profit amount. Marginal costing system includes only variable expenses to calculate the

overall cost for Tech effectively (De Baerdemaeker and Bruggeman, 2015). Apart from this,

absorption costing system include both variable and fixed expenses to calculate the product and

service cost effectively and efficiently. The difference showing between them is occurred due to

the various expenses in calculation. In respect to this, it is important to understand the expenses

first that they are divided in three parts such as fixed, variable and semi-variable expenses

effectively. Fixed expenses are those which is fixed for the firm such as employees and managers

salary is the best example of fixed expenses. Variable expenses are those which changes

consistently and effectively such as price of raw materials and machineries are the best example

for variable expenses. Semi-variable expenses are those in which some part of the expense

changed and some remain unchanged or same effectively. In order to calculate the net profit

amount all three expenses should be considered by the firm. Both methods works in different

conditions that it is difficult for the manager to select the best and appropriate method to

calculate the net profit effectively. The fixed expenses in the marginal costing system is not even

directly connected with the3 production of product and services (Gopalakrishnan, Libby,

Samuels and ed.al., 2015). Marginal cost-based method also help to determine the profit amount

which considered only those expenses which contributes in the process of production effectively.

Thus, it can be said that both marginal and absorption costing method are useful for Tech to

maintain the appropriate evaluation of expenses and also to make effective decision which helps

to improve and develop the operational activities effectively and efficiently.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

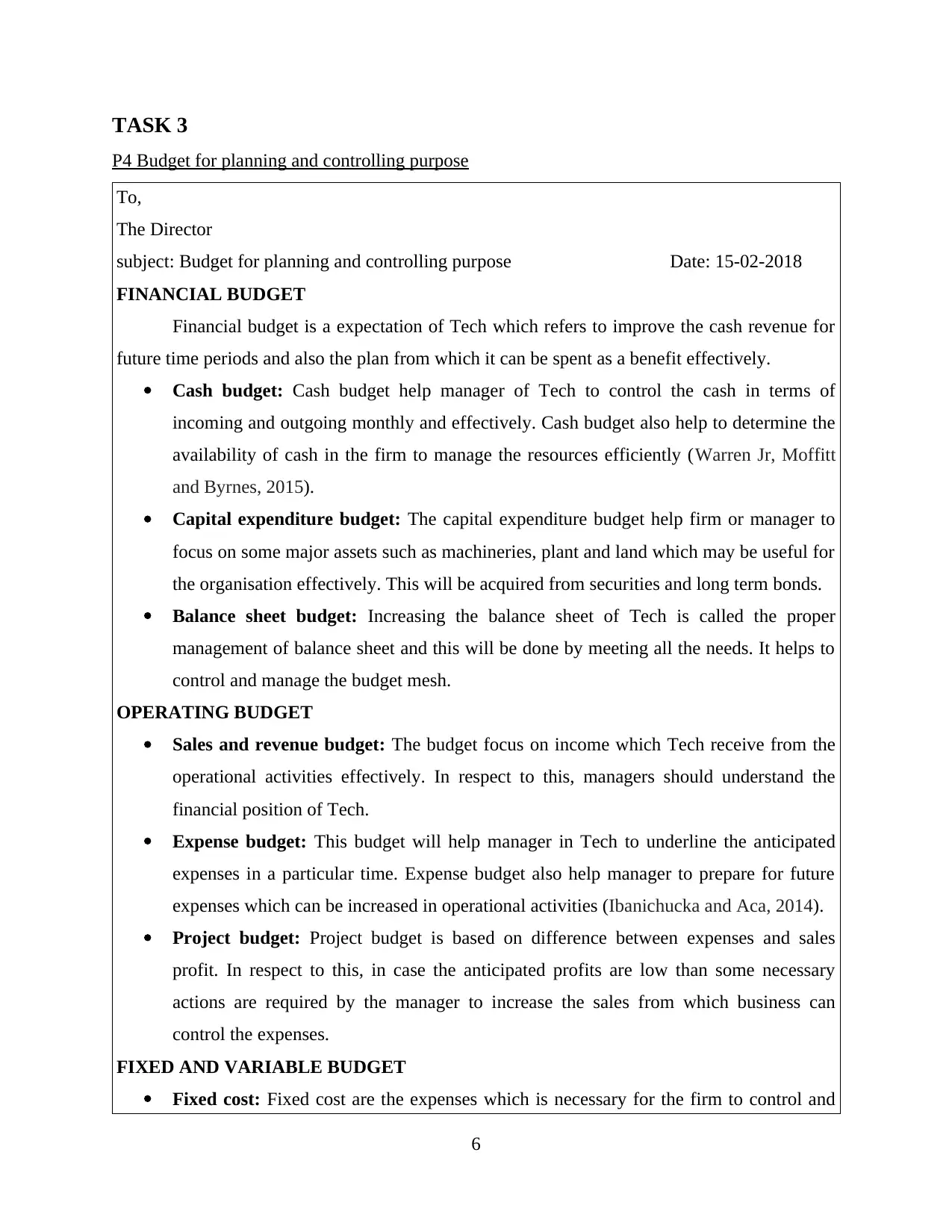

P4 Budget for planning and controlling purpose

To,

The Director

subject: Budget for planning and controlling purpose Date: 15-02-2018

FINANCIAL BUDGET

Financial budget is a expectation of Tech which refers to improve the cash revenue for

future time periods and also the plan from which it can be spent as a benefit effectively.

Cash budget: Cash budget help manager of Tech to control the cash in terms of

incoming and outgoing monthly and effectively. Cash budget also help to determine the

availability of cash in the firm to manage the resources efficiently (Warren Jr, Moffitt

and Byrnes, 2015).

Capital expenditure budget: The capital expenditure budget help firm or manager to

focus on some major assets such as machineries, plant and land which may be useful for

the organisation effectively. This will be acquired from securities and long term bonds.

Balance sheet budget: Increasing the balance sheet of Tech is called the proper

management of balance sheet and this will be done by meeting all the needs. It helps to

control and manage the budget mesh.

OPERATING BUDGET

Sales and revenue budget: The budget focus on income which Tech receive from the

operational activities effectively. In respect to this, managers should understand the

financial position of Tech.

Expense budget: This budget will help manager in Tech to underline the anticipated

expenses in a particular time. Expense budget also help manager to prepare for future

expenses which can be increased in operational activities (Ibanichucka and Aca, 2014).

Project budget: Project budget is based on difference between expenses and sales

profit. In respect to this, in case the anticipated profits are low than some necessary

actions are required by the manager to increase the sales from which business can

control the expenses.

FIXED AND VARIABLE BUDGET

Fixed cost: Fixed cost are the expenses which is necessary for the firm to control and

6

P4 Budget for planning and controlling purpose

To,

The Director

subject: Budget for planning and controlling purpose Date: 15-02-2018

FINANCIAL BUDGET

Financial budget is a expectation of Tech which refers to improve the cash revenue for

future time periods and also the plan from which it can be spent as a benefit effectively.

Cash budget: Cash budget help manager of Tech to control the cash in terms of

incoming and outgoing monthly and effectively. Cash budget also help to determine the

availability of cash in the firm to manage the resources efficiently (Warren Jr, Moffitt

and Byrnes, 2015).

Capital expenditure budget: The capital expenditure budget help firm or manager to

focus on some major assets such as machineries, plant and land which may be useful for

the organisation effectively. This will be acquired from securities and long term bonds.

Balance sheet budget: Increasing the balance sheet of Tech is called the proper

management of balance sheet and this will be done by meeting all the needs. It helps to

control and manage the budget mesh.

OPERATING BUDGET

Sales and revenue budget: The budget focus on income which Tech receive from the

operational activities effectively. In respect to this, managers should understand the

financial position of Tech.

Expense budget: This budget will help manager in Tech to underline the anticipated

expenses in a particular time. Expense budget also help manager to prepare for future

expenses which can be increased in operational activities (Ibanichucka and Aca, 2014).

Project budget: Project budget is based on difference between expenses and sales

profit. In respect to this, in case the anticipated profits are low than some necessary

actions are required by the manager to increase the sales from which business can

control the expenses.

FIXED AND VARIABLE BUDGET

Fixed cost: Fixed cost are the expenses which is necessary for the firm to control and

6

manage the business activities. For an example, salary of managers and employees is a

fixed expense for Tech effectively.

Variable cost: The cost of variable expenses is depended on operations and scope of

Tech effectively. Raw materials in production is the best example for variable cost.

ADVANTAGES DISADVANTAGES

Budget help manager to convert plans and

strategies into action.

Lack of employees participation which produce

demotivation in the firm.

Budget preparation also help manager to keep

record of organisational activities and

operations.

Budget can be also a reason for producing

perceptions of unfairness.

Budget improve and develop the employees

communication level in the firm (MacMillan,

2014).

Budget can make competition for politics and

resources effectively.

Budget help manager to justify all the develop

resources and allocation in the business.

Budget reduce the innovation and initiatives at

lower level if used mechanically or rigidly.

Budget help managers to formulate strategies

and plans to manage the cost under the budget

of firm.

Time consuming and reduce flexibility in plans

and developments.

BUDGET PREPARATION

Obtaining estimates: Obtaining estimates is important for preparing a budget such as

estimate of sales, cost of each department, resource availability and production level etc.

it is the responsibility of manager to provide estimates of future conditions which has an

impact on Tech. Discussion and participation would be informal or formal and the plans

will be reported to the budget department for an approval.

Coordinating estimates: The budget department formulate different plans and

strategies which is provided by various organisations to find the best and appropriate

between them effectively. This will help manager to get an idea of available resources

(Rahimi and Kozak, 2017).

7

fixed expense for Tech effectively.

Variable cost: The cost of variable expenses is depended on operations and scope of

Tech effectively. Raw materials in production is the best example for variable cost.

ADVANTAGES DISADVANTAGES

Budget help manager to convert plans and

strategies into action.

Lack of employees participation which produce

demotivation in the firm.

Budget preparation also help manager to keep

record of organisational activities and

operations.

Budget can be also a reason for producing

perceptions of unfairness.

Budget improve and develop the employees

communication level in the firm (MacMillan,

2014).

Budget can make competition for politics and

resources effectively.

Budget help manager to justify all the develop

resources and allocation in the business.

Budget reduce the innovation and initiatives at

lower level if used mechanically or rigidly.

Budget help managers to formulate strategies

and plans to manage the cost under the budget

of firm.

Time consuming and reduce flexibility in plans

and developments.

BUDGET PREPARATION

Obtaining estimates: Obtaining estimates is important for preparing a budget such as

estimate of sales, cost of each department, resource availability and production level etc.

it is the responsibility of manager to provide estimates of future conditions which has an

impact on Tech. Discussion and participation would be informal or formal and the plans

will be reported to the budget department for an approval.

Coordinating estimates: The budget department formulate different plans and

strategies which is provided by various organisations to find the best and appropriate

between them effectively. This will help manager to get an idea of available resources

(Rahimi and Kozak, 2017).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

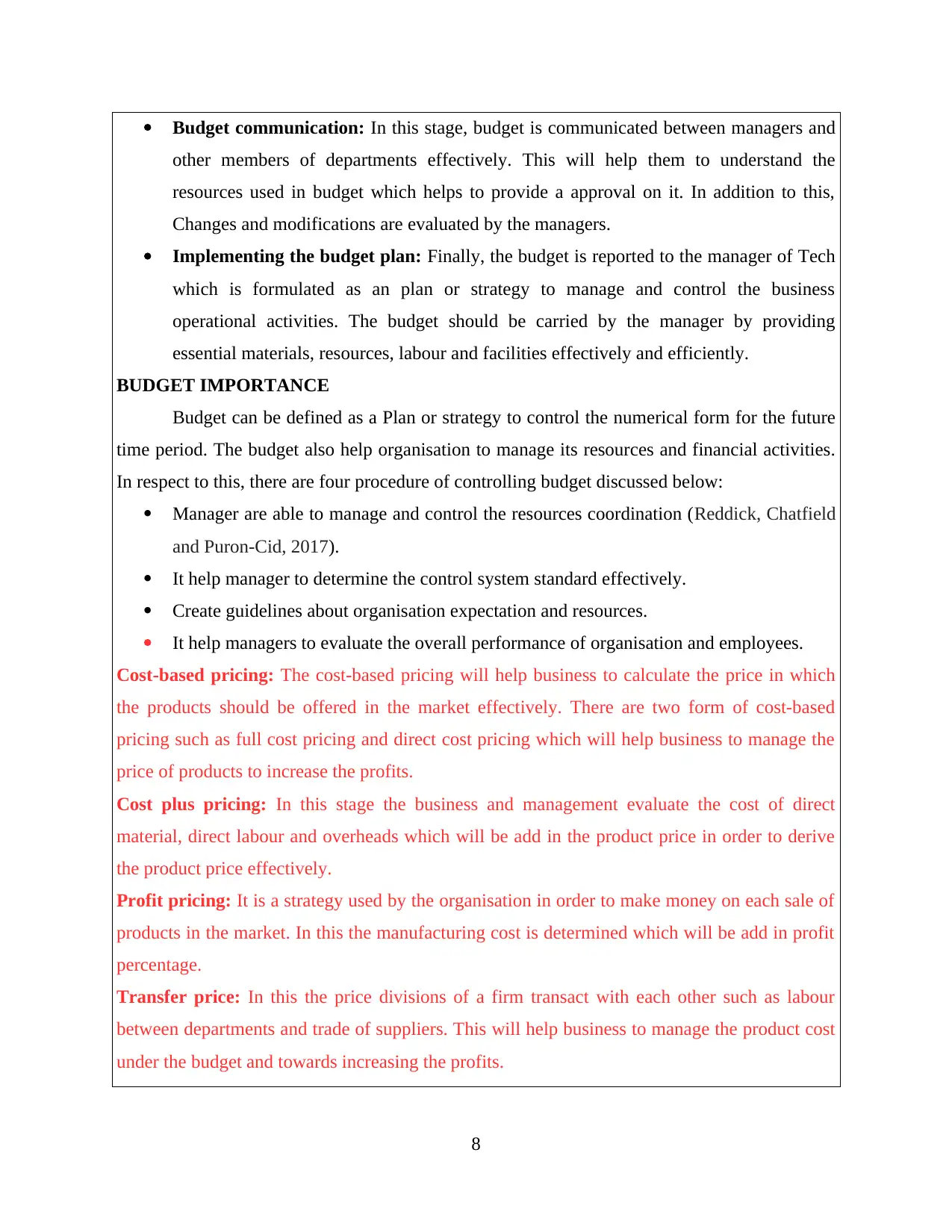

Budget communication: In this stage, budget is communicated between managers and

other members of departments effectively. This will help them to understand the

resources used in budget which helps to provide a approval on it. In addition to this,

Changes and modifications are evaluated by the managers.

Implementing the budget plan: Finally, the budget is reported to the manager of Tech

which is formulated as an plan or strategy to manage and control the business

operational activities. The budget should be carried by the manager by providing

essential materials, resources, labour and facilities effectively and efficiently.

BUDGET IMPORTANCE

Budget can be defined as a Plan or strategy to control the numerical form for the future

time period. The budget also help organisation to manage its resources and financial activities.

In respect to this, there are four procedure of controlling budget discussed below:

Manager are able to manage and control the resources coordination (Reddick, Chatfield

and Puron-Cid, 2017).

It help manager to determine the control system standard effectively.

Create guidelines about organisation expectation and resources.

It help managers to evaluate the overall performance of organisation and employees.

Cost-based pricing: The cost-based pricing will help business to calculate the price in which

the products should be offered in the market effectively. There are two form of cost-based

pricing such as full cost pricing and direct cost pricing which will help business to manage the

price of products to increase the profits.

Cost plus pricing: In this stage the business and management evaluate the cost of direct

material, direct labour and overheads which will be add in the product price in order to derive

the product price effectively.

Profit pricing: It is a strategy used by the organisation in order to make money on each sale of

products in the market. In this the manufacturing cost is determined which will be add in profit

percentage.

Transfer price: In this the price divisions of a firm transact with each other such as labour

between departments and trade of suppliers. This will help business to manage the product cost

under the budget and towards increasing the profits.

8

other members of departments effectively. This will help them to understand the

resources used in budget which helps to provide a approval on it. In addition to this,

Changes and modifications are evaluated by the managers.

Implementing the budget plan: Finally, the budget is reported to the manager of Tech

which is formulated as an plan or strategy to manage and control the business

operational activities. The budget should be carried by the manager by providing

essential materials, resources, labour and facilities effectively and efficiently.

BUDGET IMPORTANCE

Budget can be defined as a Plan or strategy to control the numerical form for the future

time period. The budget also help organisation to manage its resources and financial activities.

In respect to this, there are four procedure of controlling budget discussed below:

Manager are able to manage and control the resources coordination (Reddick, Chatfield

and Puron-Cid, 2017).

It help manager to determine the control system standard effectively.

Create guidelines about organisation expectation and resources.

It help managers to evaluate the overall performance of organisation and employees.

Cost-based pricing: The cost-based pricing will help business to calculate the price in which

the products should be offered in the market effectively. There are two form of cost-based

pricing such as full cost pricing and direct cost pricing which will help business to manage the

price of products to increase the profits.

Cost plus pricing: In this stage the business and management evaluate the cost of direct

material, direct labour and overheads which will be add in the product price in order to derive

the product price effectively.

Profit pricing: It is a strategy used by the organisation in order to make money on each sale of

products in the market. In this the manufacturing cost is determined which will be add in profit

percentage.

Transfer price: In this the price divisions of a firm transact with each other such as labour

between departments and trade of suppliers. This will help business to manage the product cost

under the budget and towards increasing the profits.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

P5 Balance scorecard approach to face the financial problems within Tech

The better financial planning, controlling and management will help business to improve

the cash position in the firm and will decrease the waste cost and lower costs. This will help

business to reduce the financial loss of £1.5m. Customer relationship management will also help

to improve the loyalty of customers, revenues from enhance purchasing by customers, reduce the

return of goods which help management to save their money and improve the financial activities.

Reducing wastage, staff turnover, customer anger and slacks will also help to manage the

financial activities. In addition to this, learning and development of staff will improve the

products quality, creativity, innovations and better process which helps to increase an effective

production to enhance the profitability, which will help to reduce the financial expenses and will

help to solve the financial problem of Tech which is in a loss of £1.5m effectively and

efficiently.

Management of Tech must design a realistic BSC and monitor it to achieve better results

and turn around the loss into profit.

BALANCE SCORECARD APPROACH

Balance scorecard is a approach which helps in strategic management to evaluate and

develop the Tech internal functions. The traditional method of balance scorecard evaluate the

initiative with the help of different perspectives such as financial, growth and learning and

process of organisation. The activities are related with collection, Data, targets, objectives and

analysation. It can be concluded that Tech has a financial loss of £1.5 million at the end of year.

Management accounting will help Tech to solve the financial problems and balance scorecard

method is to respond the financial problem effectively (Rieckhof, Bergmann and Guenther,

2015). The perspectives such as learning and growth in which the manager evaluate the

performance and provide training accordingly which will help to increase the growth effectively.

Profitability and margins will reduce the financial problem that Tech should focus on factors

which enhance the profits and production such as employees performance etc. in respect to this

financial objectives should be made by the manger to achieve them which will help to reduce the

financial problems from the firm. Customer perspective and feedbacks are also important to

develop the organisational activities.

9

P5 Balance scorecard approach to face the financial problems within Tech

The better financial planning, controlling and management will help business to improve

the cash position in the firm and will decrease the waste cost and lower costs. This will help

business to reduce the financial loss of £1.5m. Customer relationship management will also help

to improve the loyalty of customers, revenues from enhance purchasing by customers, reduce the

return of goods which help management to save their money and improve the financial activities.

Reducing wastage, staff turnover, customer anger and slacks will also help to manage the

financial activities. In addition to this, learning and development of staff will improve the

products quality, creativity, innovations and better process which helps to increase an effective

production to enhance the profitability, which will help to reduce the financial expenses and will

help to solve the financial problem of Tech which is in a loss of £1.5m effectively and

efficiently.

Management of Tech must design a realistic BSC and monitor it to achieve better results

and turn around the loss into profit.

BALANCE SCORECARD APPROACH

Balance scorecard is a approach which helps in strategic management to evaluate and

develop the Tech internal functions. The traditional method of balance scorecard evaluate the

initiative with the help of different perspectives such as financial, growth and learning and

process of organisation. The activities are related with collection, Data, targets, objectives and

analysation. It can be concluded that Tech has a financial loss of £1.5 million at the end of year.

Management accounting will help Tech to solve the financial problems and balance scorecard

method is to respond the financial problem effectively (Rieckhof, Bergmann and Guenther,

2015). The perspectives such as learning and growth in which the manager evaluate the

performance and provide training accordingly which will help to increase the growth effectively.

Profitability and margins will reduce the financial problem that Tech should focus on factors

which enhance the profits and production such as employees performance etc. in respect to this

financial objectives should be made by the manger to achieve them which will help to reduce the

financial problems from the firm. Customer perspective and feedbacks are also important to

develop the organisational activities.

9

Determination of vision: Vision of the firm should be placed in the centre of balance

scorecard. The vision is to increase the profitability and revenues from sales to respond

financial problems. The vision also should be clear for employees so that they can also

make contribution for the activities (Smith, 2017).

Add objectives, perspective and measures: The four perspective, organisation process,

customer, financial and growth and learning should be in a circle of vision. Perspectives

should have their objectives, initiatives, measures and targets to make a solution for

financial problems within Tech.

Share and communicate: The balance scorecard method will help to demonstrate action,

short term plans and strategies as well as different initiatives and their contribution for

long term strategies and objectives. Sharing and communicating will help manager of

Tech to measure the long and short term conditions and their contribution.

Just-in-Time JIT: The just-in-time is an strategy towards inventory which helps to increase the

efficiency of workers and also decrease the wastage by receiving goods which are useful for the

firm in the production. This will help Tech to reduce the cost of inventory and the method also

requires the producer to forecast the demand appropriately and effectively.

Apart from this, Balance scorecard is a approach which helps in strategic management to

evaluate and develop the Tech internal functions. The traditional method of balance scorecard

evaluate the initiative with the help of different perspectives such as financial, growth and

learning and process of organisation.

CONCLUSION

It can be concluded from the above report that management accounting is very crucial for

Tech in order to measure and evaluate different factors such as cash, inventory and costs for

products and services effectively. It will also help to manage the financial problems in the firm.

Income statement using marginal and absorption costing method will help firm to account net

profit amount. Budget will also help to reduce financial problems and Balance Scorecard method

to reduce financial problems within Tech which has a financial loss of £1.5m effectively. Thus,

the JIT and Balance scorecard approach will help them to reduce the wastage which will increase

the financial activities such as capital and cash.

10

scorecard. The vision is to increase the profitability and revenues from sales to respond

financial problems. The vision also should be clear for employees so that they can also

make contribution for the activities (Smith, 2017).

Add objectives, perspective and measures: The four perspective, organisation process,

customer, financial and growth and learning should be in a circle of vision. Perspectives

should have their objectives, initiatives, measures and targets to make a solution for

financial problems within Tech.

Share and communicate: The balance scorecard method will help to demonstrate action,

short term plans and strategies as well as different initiatives and their contribution for

long term strategies and objectives. Sharing and communicating will help manager of

Tech to measure the long and short term conditions and their contribution.

Just-in-Time JIT: The just-in-time is an strategy towards inventory which helps to increase the

efficiency of workers and also decrease the wastage by receiving goods which are useful for the

firm in the production. This will help Tech to reduce the cost of inventory and the method also

requires the producer to forecast the demand appropriately and effectively.

Apart from this, Balance scorecard is a approach which helps in strategic management to

evaluate and develop the Tech internal functions. The traditional method of balance scorecard

evaluate the initiative with the help of different perspectives such as financial, growth and

learning and process of organisation.

CONCLUSION

It can be concluded from the above report that management accounting is very crucial for

Tech in order to measure and evaluate different factors such as cash, inventory and costs for

products and services effectively. It will also help to manage the financial problems in the firm.

Income statement using marginal and absorption costing method will help firm to account net

profit amount. Budget will also help to reduce financial problems and Balance Scorecard method

to reduce financial problems within Tech which has a financial loss of £1.5m effectively. Thus,

the JIT and Balance scorecard approach will help them to reduce the wastage which will increase

the financial activities such as capital and cash.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.