HNC Unit 5: Management Accounting Systems and its Applications

VerifiedAdded on 2023/01/11

|19

|4393

|68

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and their practical applications within an organizational context. It begins by defining management accounting, outlining its essential requirements, and differentiating it from financial accounting. The report then delves into various management accounting methods, including cost accounting, inventory management, and job costing systems, evaluating their benefits and integration within organizational processes. Task 2 focuses on applying management accounting techniques to produce financial statements, including budgeted profit and loss statements using both marginal and absorption costing. The report further analyzes planning tools used in budgetary control, discussing their advantages and disadvantages and evaluating their role in preparing and forecasting budgets. Finally, the report examines how organizations adapt management accounting systems to respond to financial problems, analyzing how these systems can lead to sustainable success.

Management Accounting

Systems and its Applications

Systems and its Applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Explain the concept of Management Accounting and give the essential requirements of

different types of management accounting systems....................................................................3

1.2 Explain different methods used for management accounting reporting................................5

1.3 Evaluate the benefits of management accounting systems and their application within an

organizational context..................................................................................................................6

1.4 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organizational processes...............................................................7

TASK 2............................................................................................................................................7

2.1 Calculate the production cost per unit, total production cost and total cost of sales for

January.........................................................................................................................................7

2.2 Accurately apply the techniques and produce appropriate Budgeted profit or loss statement

for January...................................................................................................................................8

2.3 Difference in budgeted profit and actual profit for January..................................................9

TASK 3..........................................................................................................................................10

3.1 Explain the advantages and disadvantages of different types of planning tools used in

Budgetary Control.....................................................................................................................10

3.2 Analyze the use of different planning tools and their application for preparing and

forecasting budgets....................................................................................................................11

3.3 Evaluate how planning tools for accounting respond appropriately for solving financial

problems to lead organizations to sustainable success..............................................................12

TASK 4..........................................................................................................................................13

4.1 Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Explain the concept of Management Accounting and give the essential requirements of

different types of management accounting systems....................................................................3

1.2 Explain different methods used for management accounting reporting................................5

1.3 Evaluate the benefits of management accounting systems and their application within an

organizational context..................................................................................................................6

1.4 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organizational processes...............................................................7

TASK 2............................................................................................................................................7

2.1 Calculate the production cost per unit, total production cost and total cost of sales for

January.........................................................................................................................................7

2.2 Accurately apply the techniques and produce appropriate Budgeted profit or loss statement

for January...................................................................................................................................8

2.3 Difference in budgeted profit and actual profit for January..................................................9

TASK 3..........................................................................................................................................10

3.1 Explain the advantages and disadvantages of different types of planning tools used in

Budgetary Control.....................................................................................................................10

3.2 Analyze the use of different planning tools and their application for preparing and

forecasting budgets....................................................................................................................11

3.3 Evaluate how planning tools for accounting respond appropriately for solving financial

problems to lead organizations to sustainable success..............................................................12

TASK 4..........................................................................................................................................13

4.1 Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4.2 Analyze how in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................13

4.3 Evaluate how planning tools to accounting respond appropriately for solving financial

problems to lead organizations to sustainable success..............................................................14

CONCLUSION..............................................................................................................................15

REFERENCING............................................................................................................................16

organizations to sustainable success..........................................................................................13

4.3 Evaluate how planning tools to accounting respond appropriately for solving financial

problems to lead organizations to sustainable success..............................................................14

CONCLUSION..............................................................................................................................15

REFERENCING............................................................................................................................16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The main objective of the report is to reveal the administrative accounting requirements

applicable to the business situation, as well as the partnerships operating in that position. The

study of how council accounting implements budget information to help visualize, organize

choices and monitor money within associations. When the unit is successfully completed,

subscribers will be equipped to present budget reports in a work environment and will be able to

assist ranking managers in organizing liquidity. In addition, they will have the skills and

knowledge necessary to move on to the most important stage of learning. The board of directors

accounting helps managers and entrepreneurs to screen the organization's presentation and is set

up through accounting programs as needed. Depending on the type of adventure and the duration

of the information, the director or owner may request reports every day, week by week, month

by month or even quarterly.

TASK 1

1.1 Explain the concept of Management Accounting and give the essential

requirements of different types of management accounting systems

Management accounting refers to the method of measuring data relating to cash, differentiation,

verification, decay and dispatch in achieving the organisation's goals. Cost accounting is also

mentioned. The main difference between cash accounting and transactional accounting is that

council accounting data is programmed to determine leaders in a society, while cash accounting

aims to offer data at meetings outside society. . . The way to prepare management records and

reports is to offer accurate and accurate data of good fortune and related to the money needed by

management to set the daily and short-term options (Appelbaum and Kogan, 2017). There are

reports set up to meet administrative prerequisites.

Accounting is the way to evaluate, recognize and forward financial information to allow

customers to make informed choices and make decisions about information according to the

American Accounting Association (AAA). The administrative accounting frameworks differ in

their application. Each framework is created to adapt management data based on the needs of

The main objective of the report is to reveal the administrative accounting requirements

applicable to the business situation, as well as the partnerships operating in that position. The

study of how council accounting implements budget information to help visualize, organize

choices and monitor money within associations. When the unit is successfully completed,

subscribers will be equipped to present budget reports in a work environment and will be able to

assist ranking managers in organizing liquidity. In addition, they will have the skills and

knowledge necessary to move on to the most important stage of learning. The board of directors

accounting helps managers and entrepreneurs to screen the organization's presentation and is set

up through accounting programs as needed. Depending on the type of adventure and the duration

of the information, the director or owner may request reports every day, week by week, month

by month or even quarterly.

TASK 1

1.1 Explain the concept of Management Accounting and give the essential

requirements of different types of management accounting systems

Management accounting refers to the method of measuring data relating to cash, differentiation,

verification, decay and dispatch in achieving the organisation's goals. Cost accounting is also

mentioned. The main difference between cash accounting and transactional accounting is that

council accounting data is programmed to determine leaders in a society, while cash accounting

aims to offer data at meetings outside society. . . The way to prepare management records and

reports is to offer accurate and accurate data of good fortune and related to the money needed by

management to set the daily and short-term options (Appelbaum and Kogan, 2017). There are

reports set up to meet administrative prerequisites.

Accounting is the way to evaluate, recognize and forward financial information to allow

customers to make informed choices and make decisions about information according to the

American Accounting Association (AAA). The administrative accounting frameworks differ in

their application. Each framework is created to adapt management data based on the needs of

managers, to aid decision making (Blocher, 2016). There are several types of dashboard

frameworks that include inventory management, cost accounting framework, value development

and cost overruns framework all with different objectives, components and accounting

capabilities. However, all the essential components of the accounting frameworks make the

approach normalized to focus on the information that is analyzed, recognized and transferred

(Edmonds and Olds, 2013).

Cost accounting system

A cost containment framework or cost framework is the system that the company has put in

place to calculate the costs of its items for inventory evaluation, productivity analysis and cost

control. In the cost accounting framework, the specification of costs is obtained based on a

function-based cost framework or a standard cost framework. Estimating the cost of items is

critical to the success of skills (Blocher, 2016).

Inventory management

Inventory management refers to the way to control the demand, usage and capacity of the

components that the company puts into creating the products they sell. The inventory

management framework combines the use of custom identification scanners, workspace

programming, cell phones and scanner label printers to facilitate inventory management, such as

supply, products, inventory and supply (Drury, 2015). Similarly, it is the responsibility of

examining and managing the quantities of the total products available for purchase. The

objective of inventory management is to properly understand current stock levels and eliminate

excess weight and default conditions. Through effectively tracking the amounts in the storage

area, administrators will have the experience and be able to adjust for appropriate warehouse

options. Company stock is one of the company's major resources and registrations related to the

sale of articles.

Job costing system

The operating cost system refers to the agreement to assign production costs to the individual

article or piece of articles. It is applied if the processed products are not equal to each other. It

involves gathering information about costs identified by special assistance or creation work. The

frameworks that include inventory management, cost accounting framework, value development

and cost overruns framework all with different objectives, components and accounting

capabilities. However, all the essential components of the accounting frameworks make the

approach normalized to focus on the information that is analyzed, recognized and transferred

(Edmonds and Olds, 2013).

Cost accounting system

A cost containment framework or cost framework is the system that the company has put in

place to calculate the costs of its items for inventory evaluation, productivity analysis and cost

control. In the cost accounting framework, the specification of costs is obtained based on a

function-based cost framework or a standard cost framework. Estimating the cost of items is

critical to the success of skills (Blocher, 2016).

Inventory management

Inventory management refers to the way to control the demand, usage and capacity of the

components that the company puts into creating the products they sell. The inventory

management framework combines the use of custom identification scanners, workspace

programming, cell phones and scanner label printers to facilitate inventory management, such as

supply, products, inventory and supply (Drury, 2015). Similarly, it is the responsibility of

examining and managing the quantities of the total products available for purchase. The

objective of inventory management is to properly understand current stock levels and eliminate

excess weight and default conditions. Through effectively tracking the amounts in the storage

area, administrators will have the experience and be able to adjust for appropriate warehouse

options. Company stock is one of the company's major resources and registrations related to the

sale of articles.

Job costing system

The operating cost system refers to the agreement to assign production costs to the individual

article or piece of articles. It is applied if the processed products are not equal to each other. It

involves gathering information about costs identified by special assistance or creation work. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

data may present cost information to a customer based on the agreement in which the costs are

discounted. Similarly, data is important for determining exactly what the organization's

evaluation logic needs to be equipped to provide cost estimates that allow for significant

payments (Drury, 2015). The data can also be used to adapt tactical costs to prepared articles.

The transaction cost framework must gather the three types of direct data operations, direct

products and above them.

Price optimization systems

Price optimization systems refer to the use of scientific analysis for the organization to determine

how customers manage different costs for their products and campaigns through different

channels (Edmonds and Olds, 2013). Likewise, it is applied to determine the costs that an

organization decides to achieve its goals as a contribution to job performance. Find the choice by

maximizing accessibility or financial savings based on the requirements presented by raising the

desired options and limiting the unwanted ones (Edmonds and Olds, 2013)

1.2 Explain different methods used for management accounting reporting

Management accounting focuses on internal data obtained through cash accounting. Functional

accounting is applied to control, organization, and dynamics. Management accountants are based

on reports on the balance sheet that include cash documents, the payment structure and the

definition of income (Edmonds and Olds, 2013). In any event, they also apply various types of

accounting reports in the organization's data assessment. These can include financial plan cost,

item and execution reports

Cost reports

The board's accounting measures the cost of manufactured items. It is done by taking care of all

the raw materials, costs, labor as well as any extra expenditure in thinking. The integers are then

divided into phases of manufactured goods (Edmonds and Olds, 2013). All the information is

summarized in the expenses report. The report enables managers to view the cost of items

relative to the cost of sales. Helps control clothing and designs net income.

Budgets

discounted. Similarly, data is important for determining exactly what the organization's

evaluation logic needs to be equipped to provide cost estimates that allow for significant

payments (Drury, 2015). The data can also be used to adapt tactical costs to prepared articles.

The transaction cost framework must gather the three types of direct data operations, direct

products and above them.

Price optimization systems

Price optimization systems refer to the use of scientific analysis for the organization to determine

how customers manage different costs for their products and campaigns through different

channels (Edmonds and Olds, 2013). Likewise, it is applied to determine the costs that an

organization decides to achieve its goals as a contribution to job performance. Find the choice by

maximizing accessibility or financial savings based on the requirements presented by raising the

desired options and limiting the unwanted ones (Edmonds and Olds, 2013)

1.2 Explain different methods used for management accounting reporting

Management accounting focuses on internal data obtained through cash accounting. Functional

accounting is applied to control, organization, and dynamics. Management accountants are based

on reports on the balance sheet that include cash documents, the payment structure and the

definition of income (Edmonds and Olds, 2013). In any event, they also apply various types of

accounting reports in the organization's data assessment. These can include financial plan cost,

item and execution reports

Cost reports

The board's accounting measures the cost of manufactured items. It is done by taking care of all

the raw materials, costs, labor as well as any extra expenditure in thinking. The integers are then

divided into phases of manufactured goods (Edmonds and Olds, 2013). All the information is

summarized in the expenses report. The report enables managers to view the cost of items

relative to the cost of sales. Helps control clothing and designs net income.

Budgets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Drawing up spending plans is one of the key components of the board's accounts. Financial plans

are designed by implementing the previous years' spending plans and converting them into future

assumptions. Group financial plans list all expenses and sources of revenue. Companies strive to

achieve their goals and objectives while remaining within their intended amounts (Edmonds and

Olds, 2013). The directors believe that new sellers are used as suppliers of raw materials to set

aside money. Likewise, they are looking for ways to expand their sacrifices while reducing costs.

Performance reports

The executive accountants execute financial plans to compare actual income and expenditure to

expected amounts. The calculated differences are estimated when designing new financial plans

as well as all the data relating to the amounts recorded in the presentation report (Horngreen and

et.al., 2013). These ratios are calculated annually, with the exception of some partnerships that

are built quarterly or month-to-month. The reports help administrators monitor future ongoing

requests and increase costs.

1.3 Evaluate the benefits of management accounting systems and their

application within an organizational context

Benefits of management accounting system:

Increase efficiency: it supports the productivity of the company's activities through a logical

evaluation of performance and coordination with the criterion established by the organization.

Executives make exceptional choices, pay and promote failure to meet agents' expectations of

developing next through the administration's accounting frameworks.

Increasing Net Income: Through budgetary control and a capital utilization model, the company

can restrict labor and capital use together. This also helps the organization to reap huge benefits

by reducing the cost of the item and the cost of the activities.

Make the basic budget summaries: the financial announcement can be complicated to read for

people who still have no place in this area, but through the administration's accounting

frameworks it becomes a direct benefit, an unfortunate interpretation and cash register just by

looking at their final report. It makes it easy for senior management to make decisions in practice

by reading the facts introduced by cash accountants based on budget summaries.

are designed by implementing the previous years' spending plans and converting them into future

assumptions. Group financial plans list all expenses and sources of revenue. Companies strive to

achieve their goals and objectives while remaining within their intended amounts (Edmonds and

Olds, 2013). The directors believe that new sellers are used as suppliers of raw materials to set

aside money. Likewise, they are looking for ways to expand their sacrifices while reducing costs.

Performance reports

The executive accountants execute financial plans to compare actual income and expenditure to

expected amounts. The calculated differences are estimated when designing new financial plans

as well as all the data relating to the amounts recorded in the presentation report (Horngreen and

et.al., 2013). These ratios are calculated annually, with the exception of some partnerships that

are built quarterly or month-to-month. The reports help administrators monitor future ongoing

requests and increase costs.

1.3 Evaluate the benefits of management accounting systems and their

application within an organizational context

Benefits of management accounting system:

Increase efficiency: it supports the productivity of the company's activities through a logical

evaluation of performance and coordination with the criterion established by the organization.

Executives make exceptional choices, pay and promote failure to meet agents' expectations of

developing next through the administration's accounting frameworks.

Increasing Net Income: Through budgetary control and a capital utilization model, the company

can restrict labor and capital use together. This also helps the organization to reap huge benefits

by reducing the cost of the item and the cost of the activities.

Make the basic budget summaries: the financial announcement can be complicated to read for

people who still have no place in this area, but through the administration's accounting

frameworks it becomes a direct benefit, an unfortunate interpretation and cash register just by

looking at their final report. It makes it easy for senior management to make decisions in practice

by reading the facts introduced by cash accountants based on budget summaries.

Company regulatory revenues: the accounting administrator examines sources of liquidity and

its application within the society. They consider restricting unnecessary use of income.

1.4 Critically evaluate how management accounting systems and management

accounting reporting is integrated within organizational processes

Financial accounting records can be used as the primary database for management accounting

techniques (eg item cost or design), naming and approximation. We characterize such a plan,

which is commonly seen in Anglo-American societies, as "coordinated". Two important

favorable situations can be found with the structure of a coordinated accounting framework. First

of all, the officers' accounting data is provided at an incremental cost. Second, internal control

measures and money are actually taken on every level of importance, giving the board a "one-

sided contribution" just like financial experts. This point is particularly important in corporations

that require clear links between the objectives of financial experts and the accounting data of

managers. In addition, the information on cash retention may not be reasonable in all cases for

the purposes of the control of the board of directors, since the hidden accounting guidelines are

not intended for dynamic internal purposes or otherwise might be interested in the main example.

TASK 2

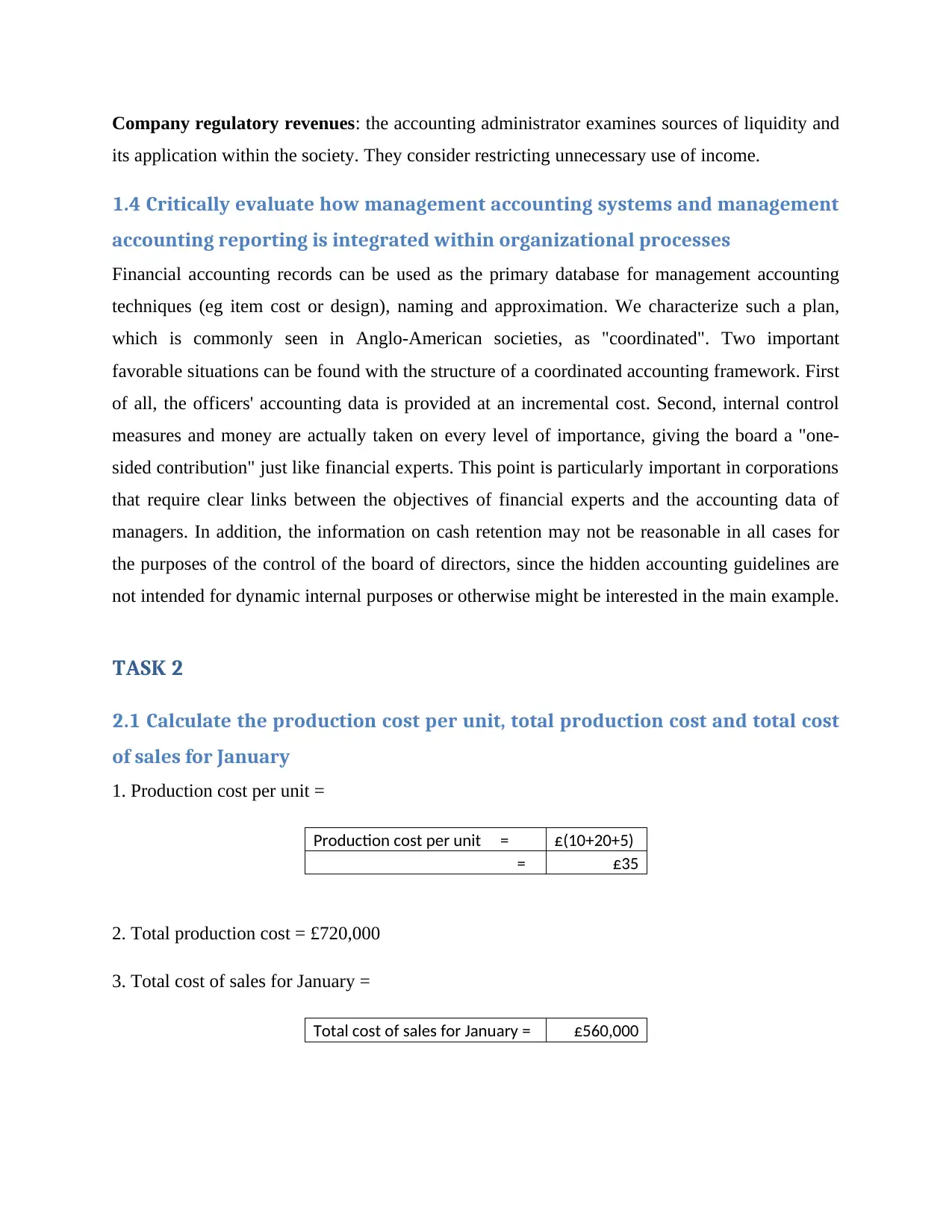

2.1 Calculate the production cost per unit, total production cost and total cost

of sales for January

1. Production cost per unit =

Production cost per unit = £(10+20+5)

= £35

2. Total production cost = £720,000

3. Total cost of sales for January =

Total cost of sales for January = £560,000

its application within the society. They consider restricting unnecessary use of income.

1.4 Critically evaluate how management accounting systems and management

accounting reporting is integrated within organizational processes

Financial accounting records can be used as the primary database for management accounting

techniques (eg item cost or design), naming and approximation. We characterize such a plan,

which is commonly seen in Anglo-American societies, as "coordinated". Two important

favorable situations can be found with the structure of a coordinated accounting framework. First

of all, the officers' accounting data is provided at an incremental cost. Second, internal control

measures and money are actually taken on every level of importance, giving the board a "one-

sided contribution" just like financial experts. This point is particularly important in corporations

that require clear links between the objectives of financial experts and the accounting data of

managers. In addition, the information on cash retention may not be reasonable in all cases for

the purposes of the control of the board of directors, since the hidden accounting guidelines are

not intended for dynamic internal purposes or otherwise might be interested in the main example.

TASK 2

2.1 Calculate the production cost per unit, total production cost and total cost

of sales for January

1. Production cost per unit =

Production cost per unit = £(10+20+5)

= £35

2. Total production cost = £720,000

3. Total cost of sales for January =

Total cost of sales for January = £560,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

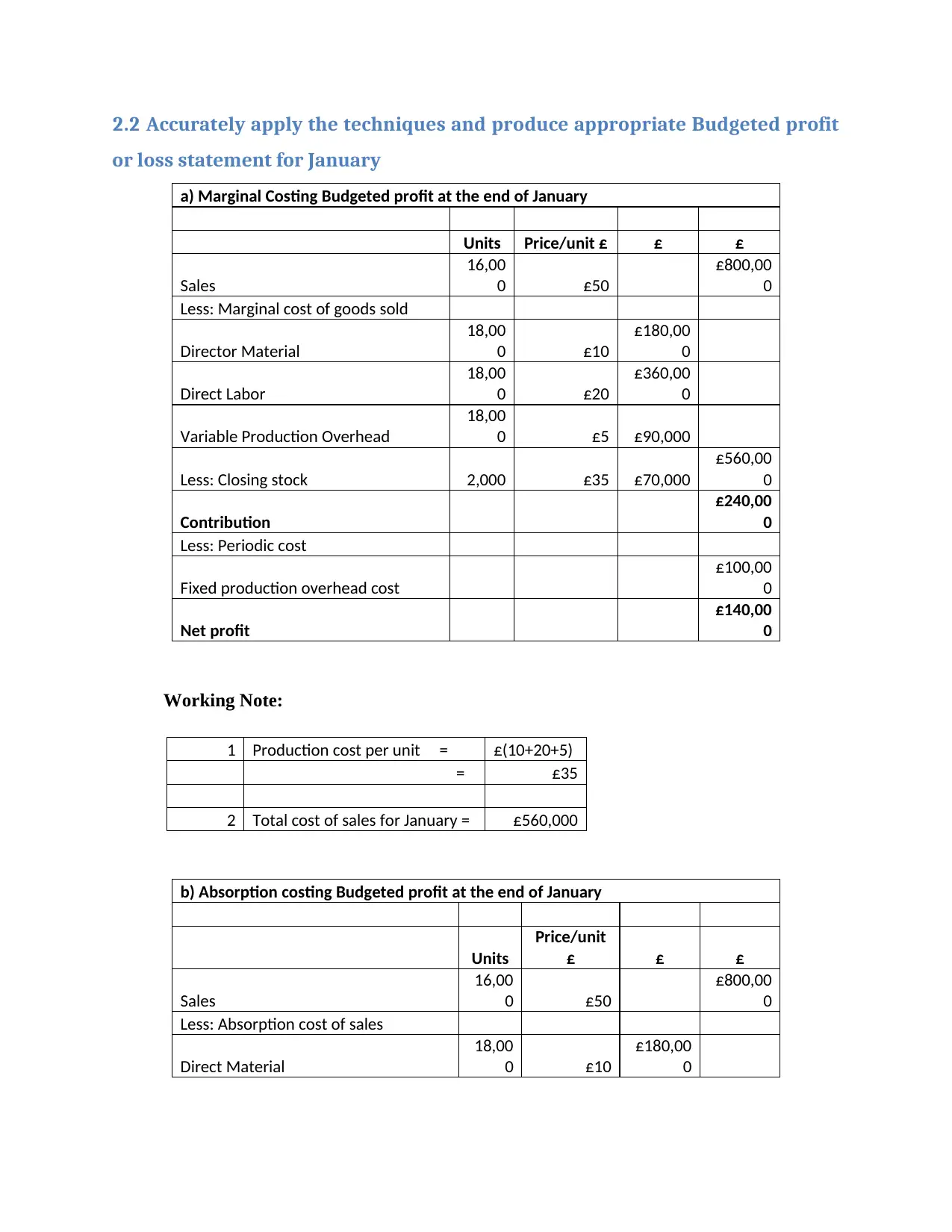

2.2 Accurately apply the techniques and produce appropriate Budgeted profit

or loss statement for January

a) Marginal Costing Budgeted profit at the end of January

Units Price/unit £ £ £

Sales

16,00

0 £50

£800,00

0

Less: Marginal cost of goods sold

Director Material

18,00

0 £10

£180,00

0

Direct Labor

18,00

0 £20

£360,00

0

Variable Production Overhead

18,00

0 £5 £90,000

Less: Closing stock 2,000 £35 £70,000

£560,00

0

Contribution

£240,00

0

Less: Periodic cost

Fixed production overhead cost

£100,00

0

Net profit

£140,00

0

Working Note:

1 Production cost per unit = £(10+20+5)

= £35

2 Total cost of sales for January = £560,000

b) Absorption costing Budgeted profit at the end of January

Units

Price/unit

£ £ £

Sales

16,00

0 £50

£800,00

0

Less: Absorption cost of sales

Direct Material

18,00

0 £10

£180,00

0

or loss statement for January

a) Marginal Costing Budgeted profit at the end of January

Units Price/unit £ £ £

Sales

16,00

0 £50

£800,00

0

Less: Marginal cost of goods sold

Director Material

18,00

0 £10

£180,00

0

Direct Labor

18,00

0 £20

£360,00

0

Variable Production Overhead

18,00

0 £5 £90,000

Less: Closing stock 2,000 £35 £70,000

£560,00

0

Contribution

£240,00

0

Less: Periodic cost

Fixed production overhead cost

£100,00

0

Net profit

£140,00

0

Working Note:

1 Production cost per unit = £(10+20+5)

= £35

2 Total cost of sales for January = £560,000

b) Absorption costing Budgeted profit at the end of January

Units

Price/unit

£ £ £

Sales

16,00

0 £50

£800,00

0

Less: Absorption cost of sales

Direct Material

18,00

0 £10

£180,00

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

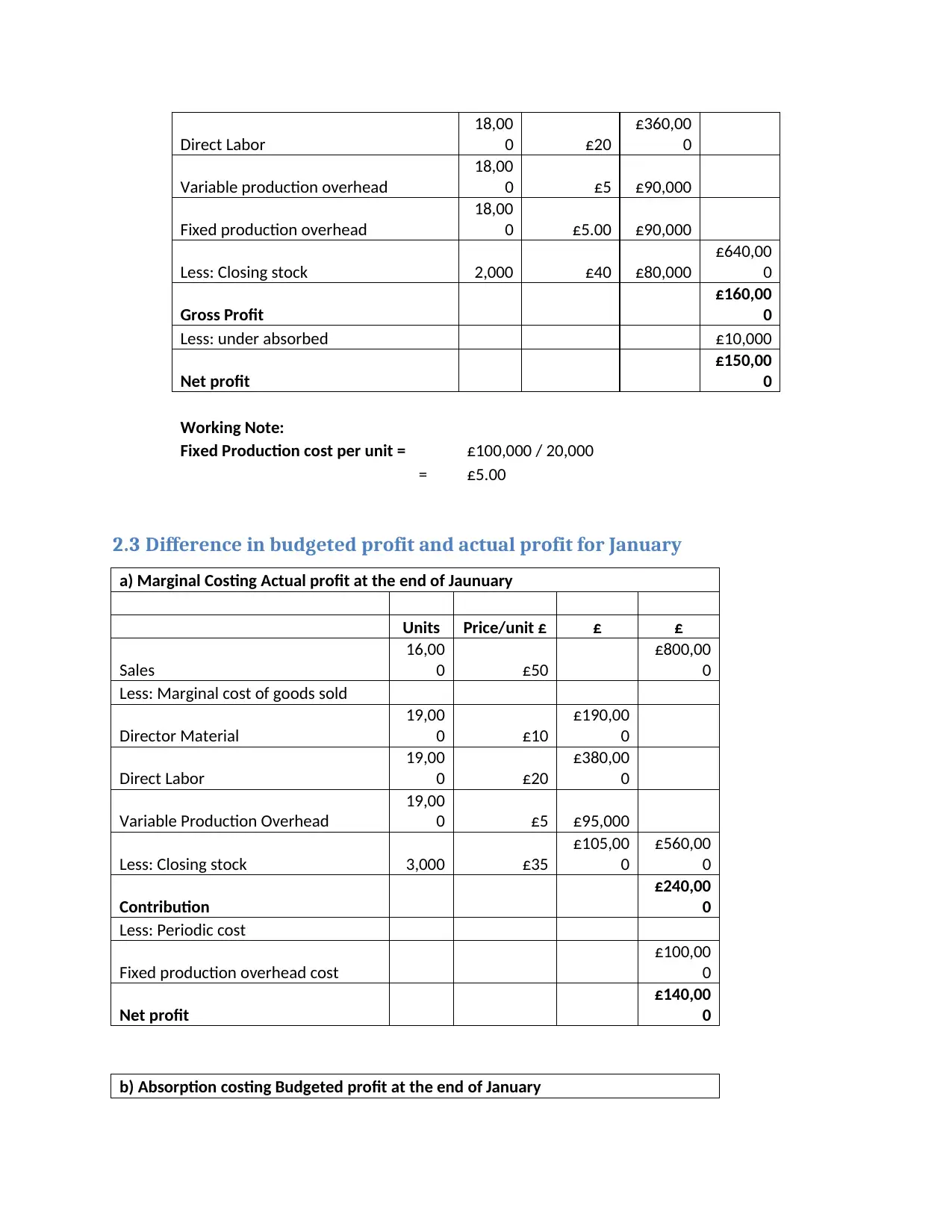

Direct Labor

18,00

0 £20

£360,00

0

Variable production overhead

18,00

0 £5 £90,000

Fixed production overhead

18,00

0 £5.00 £90,000

Less: Closing stock 2,000 £40 £80,000

£640,00

0

Gross Profit

£160,00

0

Less: under absorbed £10,000

Net profit

£150,00

0

Working Note:

Fixed Production cost per unit = £100,000 / 20,000

= £5.00

2.3 Difference in budgeted profit and actual profit for January

a) Marginal Costing Actual profit at the end of Jaunuary

Units Price/unit £ £ £

Sales

16,00

0 £50

£800,00

0

Less: Marginal cost of goods sold

Director Material

19,00

0 £10

£190,00

0

Direct Labor

19,00

0 £20

£380,00

0

Variable Production Overhead

19,00

0 £5 £95,000

Less: Closing stock 3,000 £35

£105,00

0

£560,00

0

Contribution

£240,00

0

Less: Periodic cost

Fixed production overhead cost

£100,00

0

Net profit

£140,00

0

b) Absorption costing Budgeted profit at the end of January

18,00

0 £20

£360,00

0

Variable production overhead

18,00

0 £5 £90,000

Fixed production overhead

18,00

0 £5.00 £90,000

Less: Closing stock 2,000 £40 £80,000

£640,00

0

Gross Profit

£160,00

0

Less: under absorbed £10,000

Net profit

£150,00

0

Working Note:

Fixed Production cost per unit = £100,000 / 20,000

= £5.00

2.3 Difference in budgeted profit and actual profit for January

a) Marginal Costing Actual profit at the end of Jaunuary

Units Price/unit £ £ £

Sales

16,00

0 £50

£800,00

0

Less: Marginal cost of goods sold

Director Material

19,00

0 £10

£190,00

0

Direct Labor

19,00

0 £20

£380,00

0

Variable Production Overhead

19,00

0 £5 £95,000

Less: Closing stock 3,000 £35

£105,00

0

£560,00

0

Contribution

£240,00

0

Less: Periodic cost

Fixed production overhead cost

£100,00

0

Net profit

£140,00

0

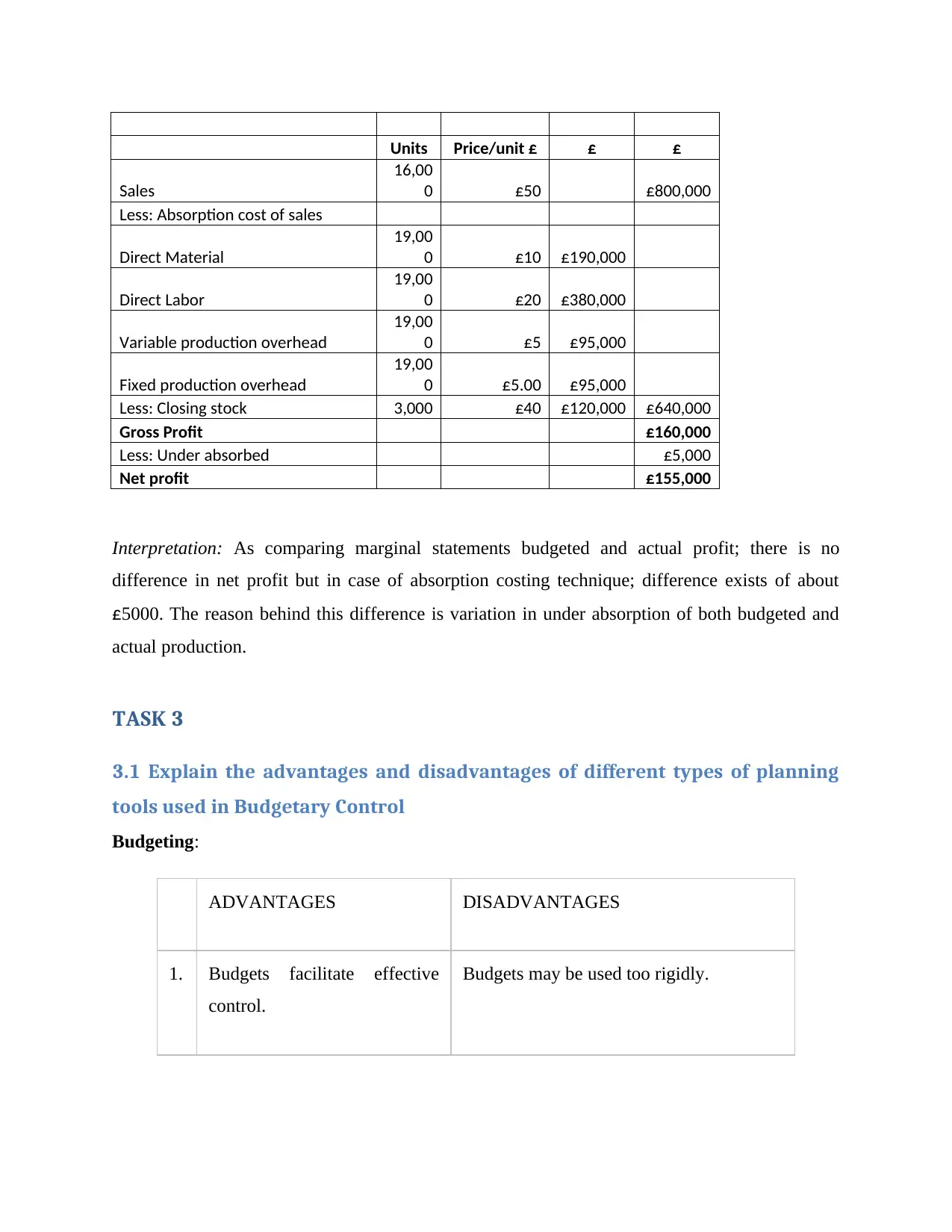

b) Absorption costing Budgeted profit at the end of January

Units Price/unit £ £ £

Sales

16,00

0 £50 £800,000

Less: Absorption cost of sales

Direct Material

19,00

0 £10 £190,000

Direct Labor

19,00

0 £20 £380,000

Variable production overhead

19,00

0 £5 £95,000

Fixed production overhead

19,00

0 £5.00 £95,000

Less: Closing stock 3,000 £40 £120,000 £640,000

Gross Profit £160,000

Less: Under absorbed £5,000

Net profit £155,000

Interpretation: As comparing marginal statements budgeted and actual profit; there is no

difference in net profit but in case of absorption costing technique; difference exists of about

£5000. The reason behind this difference is variation in under absorption of both budgeted and

actual production.

TASK 3

3.1 Explain the advantages and disadvantages of different types of planning

tools used in Budgetary Control

Budgeting:

ADVANTAGES DISADVANTAGES

1. Budgets facilitate effective

control.

Budgets may be used too rigidly.

Sales

16,00

0 £50 £800,000

Less: Absorption cost of sales

Direct Material

19,00

0 £10 £190,000

Direct Labor

19,00

0 £20 £380,000

Variable production overhead

19,00

0 £5 £95,000

Fixed production overhead

19,00

0 £5.00 £95,000

Less: Closing stock 3,000 £40 £120,000 £640,000

Gross Profit £160,000

Less: Under absorbed £5,000

Net profit £155,000

Interpretation: As comparing marginal statements budgeted and actual profit; there is no

difference in net profit but in case of absorption costing technique; difference exists of about

£5000. The reason behind this difference is variation in under absorption of both budgeted and

actual production.

TASK 3

3.1 Explain the advantages and disadvantages of different types of planning

tools used in Budgetary Control

Budgeting:

ADVANTAGES DISADVANTAGES

1. Budgets facilitate effective

control.

Budgets may be used too rigidly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.