Management Accounting Assesment Report

VerifiedAdded on 2022/09/11

|7

|1327

|18

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGEMENT ACCOUNTING

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................3

Answer to question 5:.................................................................................................................4

References and bibliography:.....................................................................................................6

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................3

Answer to question 5:.................................................................................................................4

References and bibliography:.....................................................................................................6

2MANAGEMENT ACCOUNTING

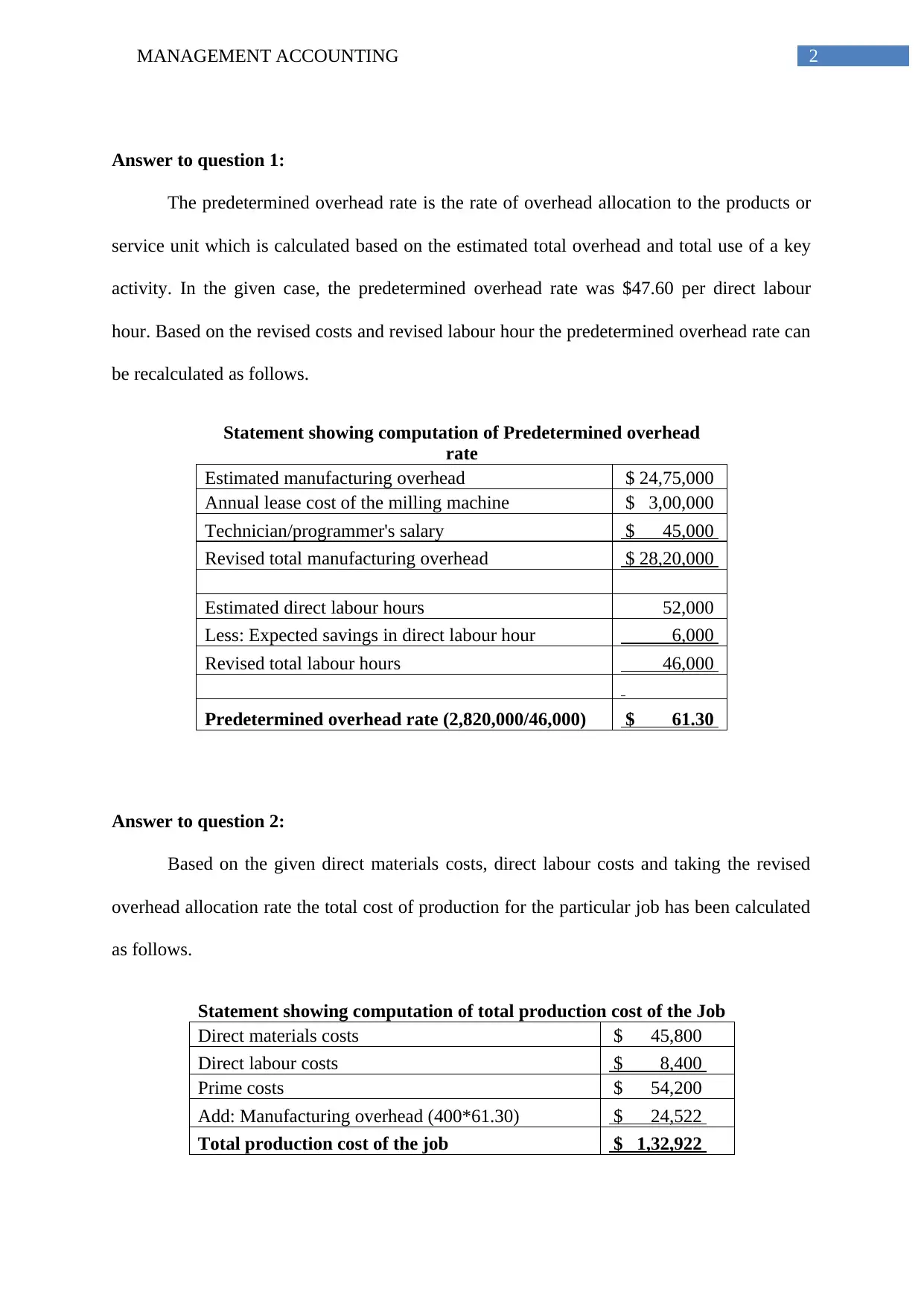

Answer to question 1:

The predetermined overhead rate is the rate of overhead allocation to the products or

service unit which is calculated based on the estimated total overhead and total use of a key

activity. In the given case, the predetermined overhead rate was $47.60 per direct labour

hour. Based on the revised costs and revised labour hour the predetermined overhead rate can

be recalculated as follows.

Statement showing computation of Predetermined overhead

rate

Estimated manufacturing overhead $ 24,75,000

Annual lease cost of the milling machine $ 3,00,000

Technician/programmer's salary $ 45,000

Revised total manufacturing overhead $ 28,20,000

Estimated direct labour hours 52,000

Less: Expected savings in direct labour hour 6,000

Revised total labour hours 46,000

Predetermined overhead rate (2,820,000/46,000) $ 61.30

Answer to question 2:

Based on the given direct materials costs, direct labour costs and taking the revised

overhead allocation rate the total cost of production for the particular job has been calculated

as follows.

Statement showing computation of total production cost of the Job

Direct materials costs $ 45,800

Direct labour costs $ 8,400

Prime costs $ 54,200

Add: Manufacturing overhead (400*61.30) $ 24,522

Total production cost of the job $ 1,32,922

Answer to question 1:

The predetermined overhead rate is the rate of overhead allocation to the products or

service unit which is calculated based on the estimated total overhead and total use of a key

activity. In the given case, the predetermined overhead rate was $47.60 per direct labour

hour. Based on the revised costs and revised labour hour the predetermined overhead rate can

be recalculated as follows.

Statement showing computation of Predetermined overhead

rate

Estimated manufacturing overhead $ 24,75,000

Annual lease cost of the milling machine $ 3,00,000

Technician/programmer's salary $ 45,000

Revised total manufacturing overhead $ 28,20,000

Estimated direct labour hours 52,000

Less: Expected savings in direct labour hour 6,000

Revised total labour hours 46,000

Predetermined overhead rate (2,820,000/46,000) $ 61.30

Answer to question 2:

Based on the given direct materials costs, direct labour costs and taking the revised

overhead allocation rate the total cost of production for the particular job has been calculated

as follows.

Statement showing computation of total production cost of the Job

Direct materials costs $ 45,800

Direct labour costs $ 8,400

Prime costs $ 54,200

Add: Manufacturing overhead (400*61.30) $ 24,522

Total production cost of the job $ 1,32,922

3MANAGEMENT ACCOUNTING

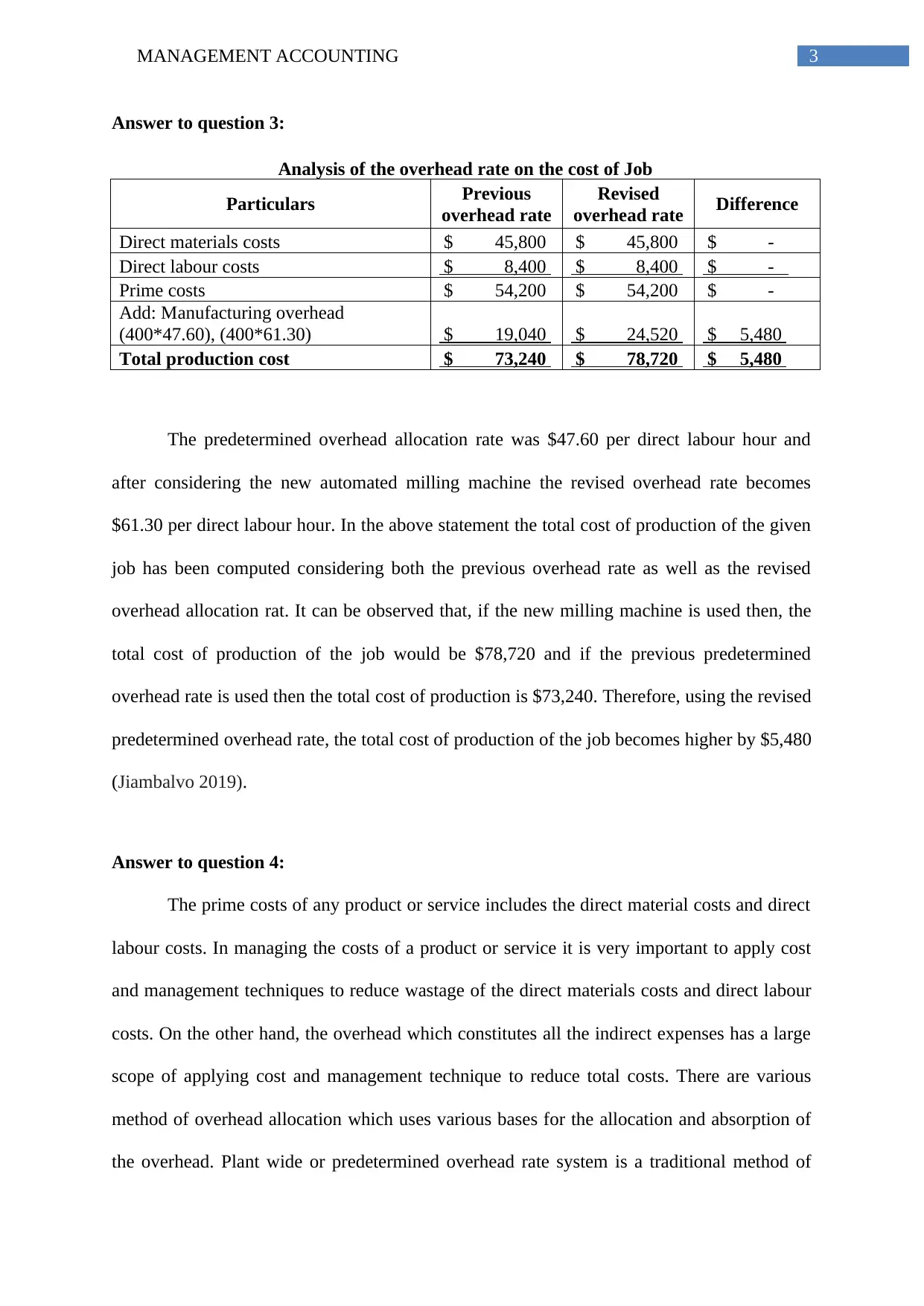

Answer to question 3:

Analysis of the overhead rate on the cost of Job

Particulars Previous

overhead rate

Revised

overhead rate Difference

Direct materials costs $ 45,800 $ 45,800 $ -

Direct labour costs $ 8,400 $ 8,400 $ -

Prime costs $ 54,200 $ 54,200 $ -

Add: Manufacturing overhead

(400*47.60), (400*61.30) $ 19,040 $ 24,520 $ 5,480

Total production cost $ 73,240 $ 78,720 $ 5,480

The predetermined overhead allocation rate was $47.60 per direct labour hour and

after considering the new automated milling machine the revised overhead rate becomes

$61.30 per direct labour hour. In the above statement the total cost of production of the given

job has been computed considering both the previous overhead rate as well as the revised

overhead allocation rat. It can be observed that, if the new milling machine is used then, the

total cost of production of the job would be $78,720 and if the previous predetermined

overhead rate is used then the total cost of production is $73,240. Therefore, using the revised

predetermined overhead rate, the total cost of production of the job becomes higher by $5,480

(Jiambalvo 2019).

Answer to question 4:

The prime costs of any product or service includes the direct material costs and direct

labour costs. In managing the costs of a product or service it is very important to apply cost

and management techniques to reduce wastage of the direct materials costs and direct labour

costs. On the other hand, the overhead which constitutes all the indirect expenses has a large

scope of applying cost and management technique to reduce total costs. There are various

method of overhead allocation which uses various bases for the allocation and absorption of

the overhead. Plant wide or predetermined overhead rate system is a traditional method of

Answer to question 3:

Analysis of the overhead rate on the cost of Job

Particulars Previous

overhead rate

Revised

overhead rate Difference

Direct materials costs $ 45,800 $ 45,800 $ -

Direct labour costs $ 8,400 $ 8,400 $ -

Prime costs $ 54,200 $ 54,200 $ -

Add: Manufacturing overhead

(400*47.60), (400*61.30) $ 19,040 $ 24,520 $ 5,480

Total production cost $ 73,240 $ 78,720 $ 5,480

The predetermined overhead allocation rate was $47.60 per direct labour hour and

after considering the new automated milling machine the revised overhead rate becomes

$61.30 per direct labour hour. In the above statement the total cost of production of the given

job has been computed considering both the previous overhead rate as well as the revised

overhead allocation rat. It can be observed that, if the new milling machine is used then, the

total cost of production of the job would be $78,720 and if the previous predetermined

overhead rate is used then the total cost of production is $73,240. Therefore, using the revised

predetermined overhead rate, the total cost of production of the job becomes higher by $5,480

(Jiambalvo 2019).

Answer to question 4:

The prime costs of any product or service includes the direct material costs and direct

labour costs. In managing the costs of a product or service it is very important to apply cost

and management techniques to reduce wastage of the direct materials costs and direct labour

costs. On the other hand, the overhead which constitutes all the indirect expenses has a large

scope of applying cost and management technique to reduce total costs. There are various

method of overhead allocation which uses various bases for the allocation and absorption of

the overhead. Plant wide or predetermined overhead rate system is a traditional method of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGEMENT ACCOUNTING

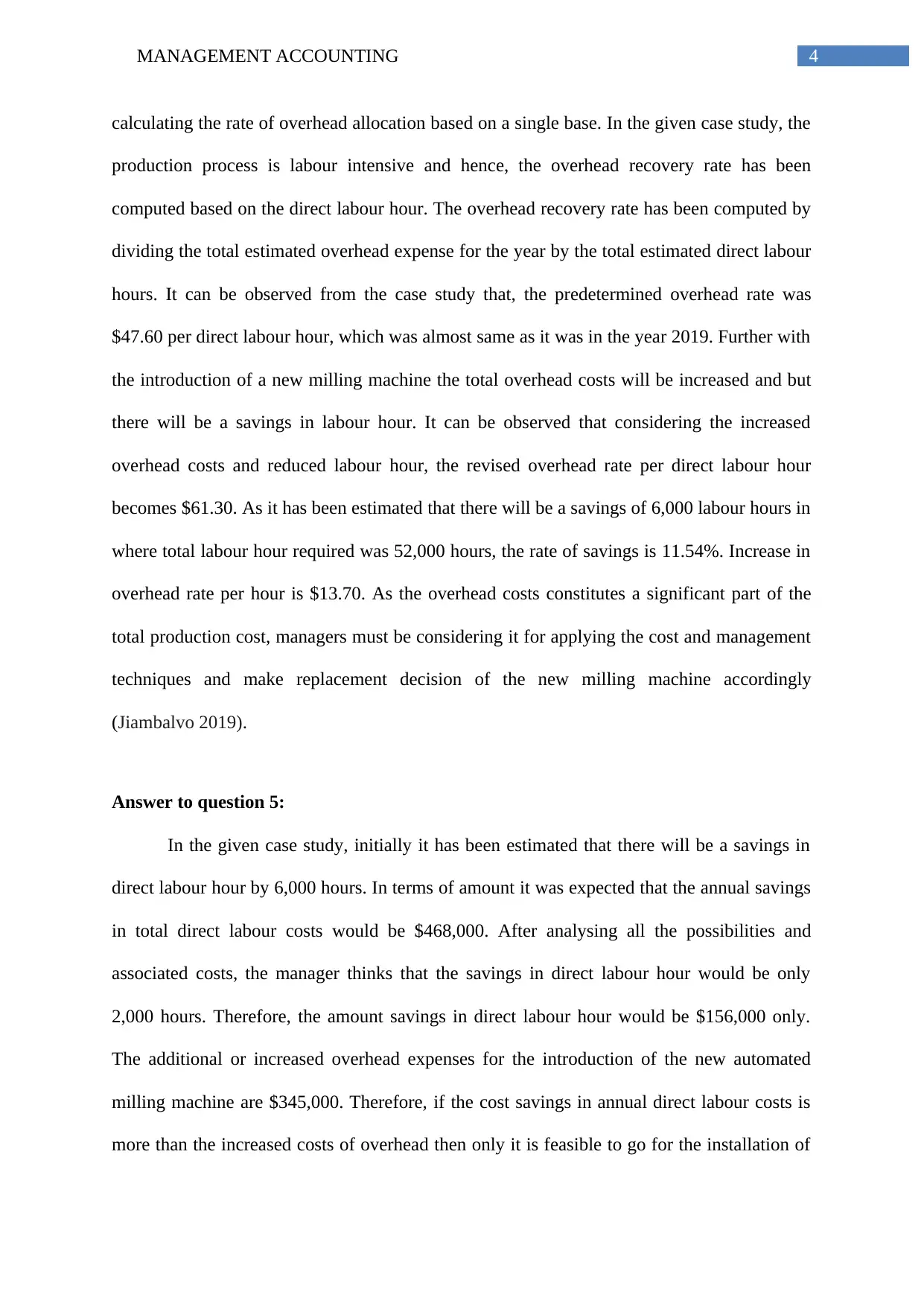

calculating the rate of overhead allocation based on a single base. In the given case study, the

production process is labour intensive and hence, the overhead recovery rate has been

computed based on the direct labour hour. The overhead recovery rate has been computed by

dividing the total estimated overhead expense for the year by the total estimated direct labour

hours. It can be observed from the case study that, the predetermined overhead rate was

$47.60 per direct labour hour, which was almost same as it was in the year 2019. Further with

the introduction of a new milling machine the total overhead costs will be increased and but

there will be a savings in labour hour. It can be observed that considering the increased

overhead costs and reduced labour hour, the revised overhead rate per direct labour hour

becomes $61.30. As it has been estimated that there will be a savings of 6,000 labour hours in

where total labour hour required was 52,000 hours, the rate of savings is 11.54%. Increase in

overhead rate per hour is $13.70. As the overhead costs constitutes a significant part of the

total production cost, managers must be considering it for applying the cost and management

techniques and make replacement decision of the new milling machine accordingly

(Jiambalvo 2019).

Answer to question 5:

In the given case study, initially it has been estimated that there will be a savings in

direct labour hour by 6,000 hours. In terms of amount it was expected that the annual savings

in total direct labour costs would be $468,000. After analysing all the possibilities and

associated costs, the manager thinks that the savings in direct labour hour would be only

2,000 hours. Therefore, the amount savings in direct labour hour would be $156,000 only.

The additional or increased overhead expenses for the introduction of the new automated

milling machine are $345,000. Therefore, if the cost savings in annual direct labour costs is

more than the increased costs of overhead then only it is feasible to go for the installation of

calculating the rate of overhead allocation based on a single base. In the given case study, the

production process is labour intensive and hence, the overhead recovery rate has been

computed based on the direct labour hour. The overhead recovery rate has been computed by

dividing the total estimated overhead expense for the year by the total estimated direct labour

hours. It can be observed from the case study that, the predetermined overhead rate was

$47.60 per direct labour hour, which was almost same as it was in the year 2019. Further with

the introduction of a new milling machine the total overhead costs will be increased and but

there will be a savings in labour hour. It can be observed that considering the increased

overhead costs and reduced labour hour, the revised overhead rate per direct labour hour

becomes $61.30. As it has been estimated that there will be a savings of 6,000 labour hours in

where total labour hour required was 52,000 hours, the rate of savings is 11.54%. Increase in

overhead rate per hour is $13.70. As the overhead costs constitutes a significant part of the

total production cost, managers must be considering it for applying the cost and management

techniques and make replacement decision of the new milling machine accordingly

(Jiambalvo 2019).

Answer to question 5:

In the given case study, initially it has been estimated that there will be a savings in

direct labour hour by 6,000 hours. In terms of amount it was expected that the annual savings

in total direct labour costs would be $468,000. After analysing all the possibilities and

associated costs, the manager thinks that the savings in direct labour hour would be only

2,000 hours. Therefore, the amount savings in direct labour hour would be $156,000 only.

The additional or increased overhead expenses for the introduction of the new automated

milling machine are $345,000. Therefore, if the cost savings in annual direct labour costs is

more than the increased costs of overhead then only it is feasible to go for the installation of

5MANAGEMENT ACCOUNTING

the new automated milling machine. When the, the savings in labour hour is only 2,000

hours, the cost savings is lesser than the increased overhead costs. Hence, it can be

recommended not to go for the installation of the milling machine if it is expected that there

will be only 2,000 hours of savings in direct labour hour (Horngren 2019).

the new automated milling machine. When the, the savings in labour hour is only 2,000

hours, the cost savings is lesser than the increased overhead costs. Hence, it can be

recommended not to go for the installation of the milling machine if it is expected that there

will be only 2,000 hours of savings in direct labour hour (Horngren 2019).

6MANAGEMENT ACCOUNTING

References and bibliography:

Appelbaum, D., Kogan, A., Vasarhelyi, M., & Yan, Z. (2017). Impact of business analytics

and enterprise systems on managerial accounting. International Journal of Accounting

Information Systems, 25, 29-44.

Brewer, P. C., Garrison, R. H., & Noreen, E. W. (2015). Introduction to managerial

accounting. McGraw-Hill Education.

Horngren, C. T. (2019). Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Jiambalvo, J. (2019). Managerial accounting. John Wiley & Sons.

Kim, M., Schmidgall, R. S., & Damitio, J. W. (2017). Key managerial accounting skills for

lodging industry managers: The third phase of a repeated cross-sectional

study. International Journal of Hospitality & Tourism Administration, 18(1), 23-40.

Trkman, P., McCormack, K., De Oliveira, M. P. V., & Ladeira, M. B. (2010). The impact of

business analytics on supply chain performance. Decision Support Systems, 49(3),

318-327.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2018). Financial and Managerial

Accounting. John Wiley & Sons.

Weygandt, J. J., Kimmel, P. D., Kieso, D. E., & Aly, I. M. (2018). Managerial Accounting:

Tools for Business Decision-making. John Wiley & Sons.

References and bibliography:

Appelbaum, D., Kogan, A., Vasarhelyi, M., & Yan, Z. (2017). Impact of business analytics

and enterprise systems on managerial accounting. International Journal of Accounting

Information Systems, 25, 29-44.

Brewer, P. C., Garrison, R. H., & Noreen, E. W. (2015). Introduction to managerial

accounting. McGraw-Hill Education.

Horngren, C. T. (2019). Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Jiambalvo, J. (2019). Managerial accounting. John Wiley & Sons.

Kim, M., Schmidgall, R. S., & Damitio, J. W. (2017). Key managerial accounting skills for

lodging industry managers: The third phase of a repeated cross-sectional

study. International Journal of Hospitality & Tourism Administration, 18(1), 23-40.

Trkman, P., McCormack, K., De Oliveira, M. P. V., & Ladeira, M. B. (2010). The impact of

business analytics on supply chain performance. Decision Support Systems, 49(3),

318-327.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2018). Financial and Managerial

Accounting. John Wiley & Sons.

Weygandt, J. J., Kimmel, P. D., Kieso, D. E., & Aly, I. M. (2018). Managerial Accounting:

Tools for Business Decision-making. John Wiley & Sons.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.