Management Accounting Assignment Term 1 2018

VerifiedAdded on 2023/06/12

|9

|2261

|235

AI Summary

This article discusses Management Accounting Assignment Term 1 2018, covering topics such as calculating cost per unit of sewing machines, preparing profit and loss statement, and the benefits and limitations of ABC. It emphasizes the importance of accurate product costing and informed decision making. The article also explains why actual overhead varies from applied overhead. Subject: Management Accounting, Course Code: N/A, Course Name: N/A, College/University: Institution Name

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assignment Term 1 2018

Management Accounting

Assignment Term 1 2018

Institution Name

Student Name

Date

Management Accounting

Assignment Term 1 2018

Institution Name

Student Name

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assignment Term 1 2018

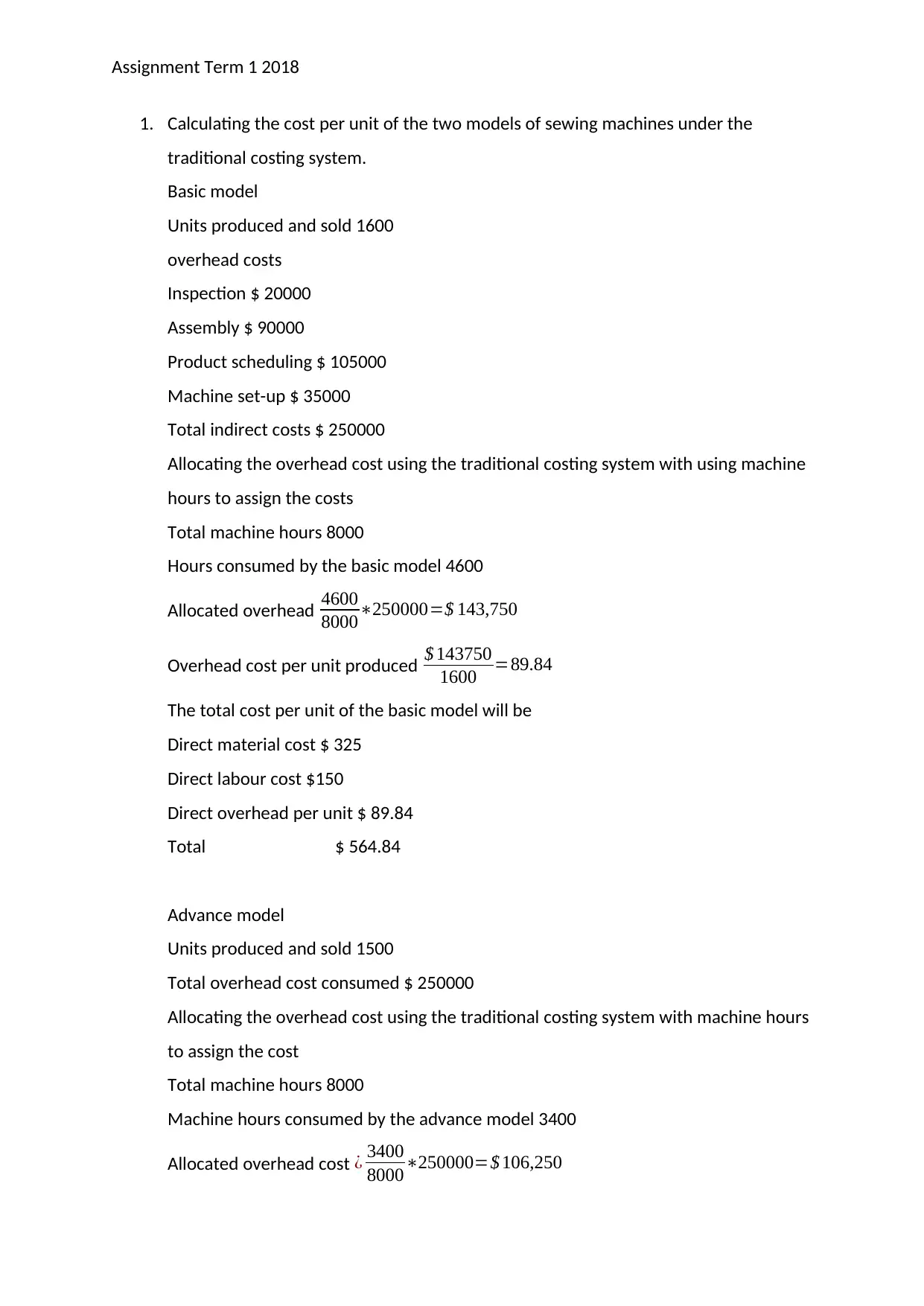

1. Calculating the cost per unit of the two models of sewing machines under the

traditional costing system.

Basic model

Units produced and sold 1600

overhead costs

Inspection $ 20000

Assembly $ 90000

Product scheduling $ 105000

Machine set-up $ 35000

Total indirect costs $ 250000

Allocating the overhead cost using the traditional costing system with using machine

hours to assign the costs

Total machine hours 8000

Hours consumed by the basic model 4600

Allocated overhead 4600

8000∗250000=$ 143,750

Overhead cost per unit produced $ 143750

1600 =89.84

The total cost per unit of the basic model will be

Direct material cost $ 325

Direct labour cost $150

Direct overhead per unit $ 89.84

Total $ 564.84

Advance model

Units produced and sold 1500

Total overhead cost consumed $ 250000

Allocating the overhead cost using the traditional costing system with machine hours

to assign the cost

Total machine hours 8000

Machine hours consumed by the advance model 3400

Allocated overhead cost ¿ 3400

8000∗250000=$ 106,250

1. Calculating the cost per unit of the two models of sewing machines under the

traditional costing system.

Basic model

Units produced and sold 1600

overhead costs

Inspection $ 20000

Assembly $ 90000

Product scheduling $ 105000

Machine set-up $ 35000

Total indirect costs $ 250000

Allocating the overhead cost using the traditional costing system with using machine

hours to assign the costs

Total machine hours 8000

Hours consumed by the basic model 4600

Allocated overhead 4600

8000∗250000=$ 143,750

Overhead cost per unit produced $ 143750

1600 =89.84

The total cost per unit of the basic model will be

Direct material cost $ 325

Direct labour cost $150

Direct overhead per unit $ 89.84

Total $ 564.84

Advance model

Units produced and sold 1500

Total overhead cost consumed $ 250000

Allocating the overhead cost using the traditional costing system with machine hours

to assign the cost

Total machine hours 8000

Machine hours consumed by the advance model 3400

Allocated overhead cost ¿ 3400

8000∗250000=$ 106,250

Assignment Term 1 2018

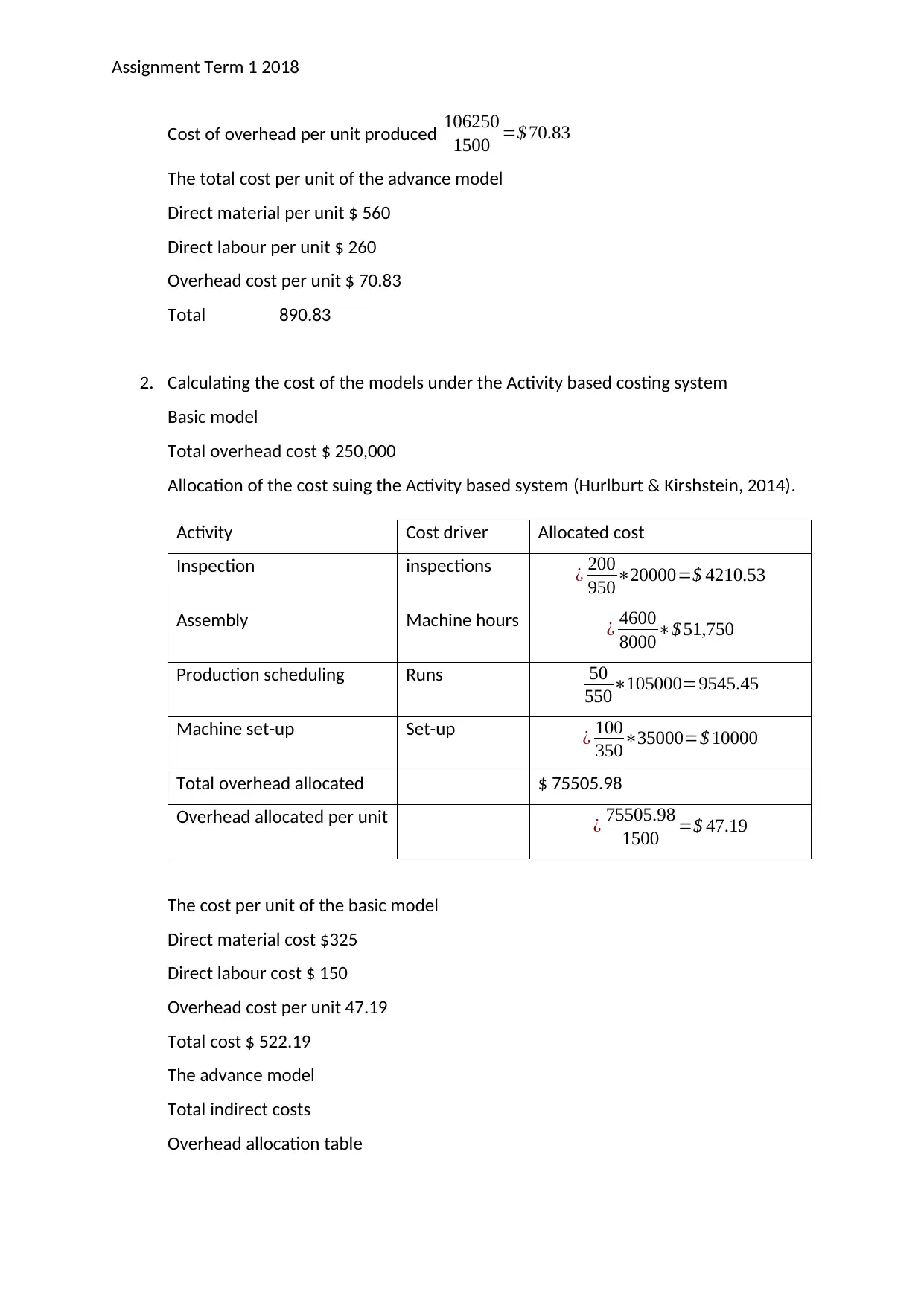

Cost of overhead per unit produced 106250

1500 =$ 70.83

The total cost per unit of the advance model

Direct material per unit $ 560

Direct labour per unit $ 260

Overhead cost per unit $ 70.83

Total 890.83

2. Calculating the cost of the models under the Activity based costing system

Basic model

Total overhead cost $ 250,000

Allocation of the cost suing the Activity based system (Hurlburt & Kirshstein, 2014).

Activity Cost driver Allocated cost

Inspection inspections ¿ 200

950∗20000=$ 4210.53

Assembly Machine hours ¿ 4600

8000∗$ 51,750

Production scheduling Runs 50

550∗105000=9545.45

Machine set-up Set-up ¿ 100

350∗35000=$ 10000

Total overhead allocated $ 75505.98

Overhead allocated per unit ¿ 75505.98

1500 =$ 47.19

The cost per unit of the basic model

Direct material cost $325

Direct labour cost $ 150

Overhead cost per unit 47.19

Total cost $ 522.19

The advance model

Total indirect costs

Overhead allocation table

Cost of overhead per unit produced 106250

1500 =$ 70.83

The total cost per unit of the advance model

Direct material per unit $ 560

Direct labour per unit $ 260

Overhead cost per unit $ 70.83

Total 890.83

2. Calculating the cost of the models under the Activity based costing system

Basic model

Total overhead cost $ 250,000

Allocation of the cost suing the Activity based system (Hurlburt & Kirshstein, 2014).

Activity Cost driver Allocated cost

Inspection inspections ¿ 200

950∗20000=$ 4210.53

Assembly Machine hours ¿ 4600

8000∗$ 51,750

Production scheduling Runs 50

550∗105000=9545.45

Machine set-up Set-up ¿ 100

350∗35000=$ 10000

Total overhead allocated $ 75505.98

Overhead allocated per unit ¿ 75505.98

1500 =$ 47.19

The cost per unit of the basic model

Direct material cost $325

Direct labour cost $ 150

Overhead cost per unit 47.19

Total cost $ 522.19

The advance model

Total indirect costs

Overhead allocation table

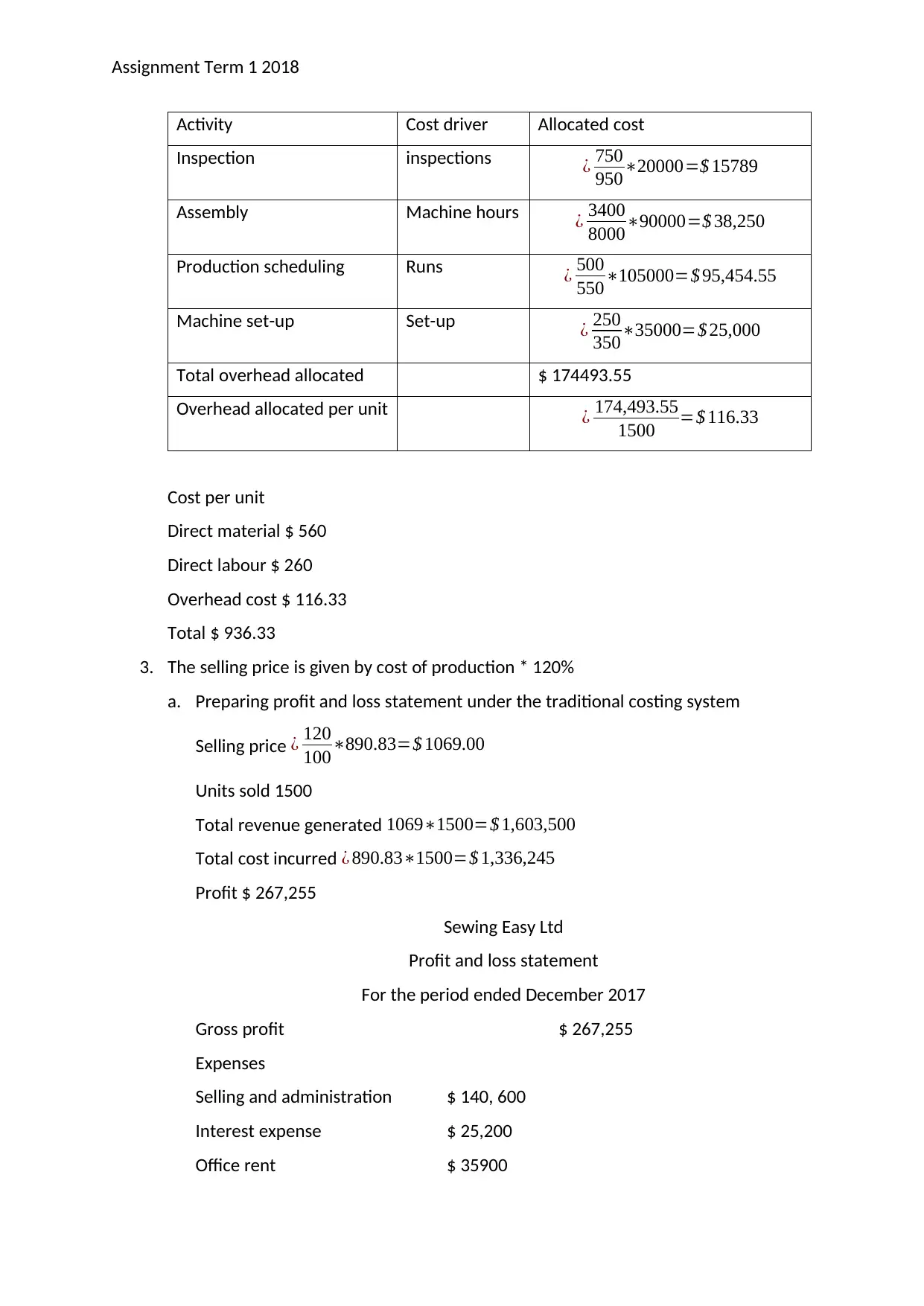

Assignment Term 1 2018

Activity Cost driver Allocated cost

Inspection inspections ¿ 750

950∗20000=$ 15789

Assembly Machine hours ¿ 3400

8000∗90000=$ 38,250

Production scheduling Runs ¿ 500

550∗105000=$ 95,454.55

Machine set-up Set-up ¿ 250

350∗35000=$ 25,000

Total overhead allocated $ 174493.55

Overhead allocated per unit ¿ 174,493.55

1500 =$ 116.33

Cost per unit

Direct material $ 560

Direct labour $ 260

Overhead cost $ 116.33

Total $ 936.33

3. The selling price is given by cost of production * 120%

a. Preparing profit and loss statement under the traditional costing system

Selling price ¿ 120

100∗890.83=$ 1069.00

Units sold 1500

Total revenue generated 1069∗1500=$ 1,603,500

Total cost incurred ¿ 890.83∗1500=$ 1,336,245

Profit $ 267,255

Sewing Easy Ltd

Profit and loss statement

For the period ended December 2017

Gross profit $ 267,255

Expenses

Selling and administration $ 140, 600

Interest expense $ 25,200

Office rent $ 35900

Activity Cost driver Allocated cost

Inspection inspections ¿ 750

950∗20000=$ 15789

Assembly Machine hours ¿ 3400

8000∗90000=$ 38,250

Production scheduling Runs ¿ 500

550∗105000=$ 95,454.55

Machine set-up Set-up ¿ 250

350∗35000=$ 25,000

Total overhead allocated $ 174493.55

Overhead allocated per unit ¿ 174,493.55

1500 =$ 116.33

Cost per unit

Direct material $ 560

Direct labour $ 260

Overhead cost $ 116.33

Total $ 936.33

3. The selling price is given by cost of production * 120%

a. Preparing profit and loss statement under the traditional costing system

Selling price ¿ 120

100∗890.83=$ 1069.00

Units sold 1500

Total revenue generated 1069∗1500=$ 1,603,500

Total cost incurred ¿ 890.83∗1500=$ 1,336,245

Profit $ 267,255

Sewing Easy Ltd

Profit and loss statement

For the period ended December 2017

Gross profit $ 267,255

Expenses

Selling and administration $ 140, 600

Interest expense $ 25,200

Office rent $ 35900

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assignment Term 1 2018

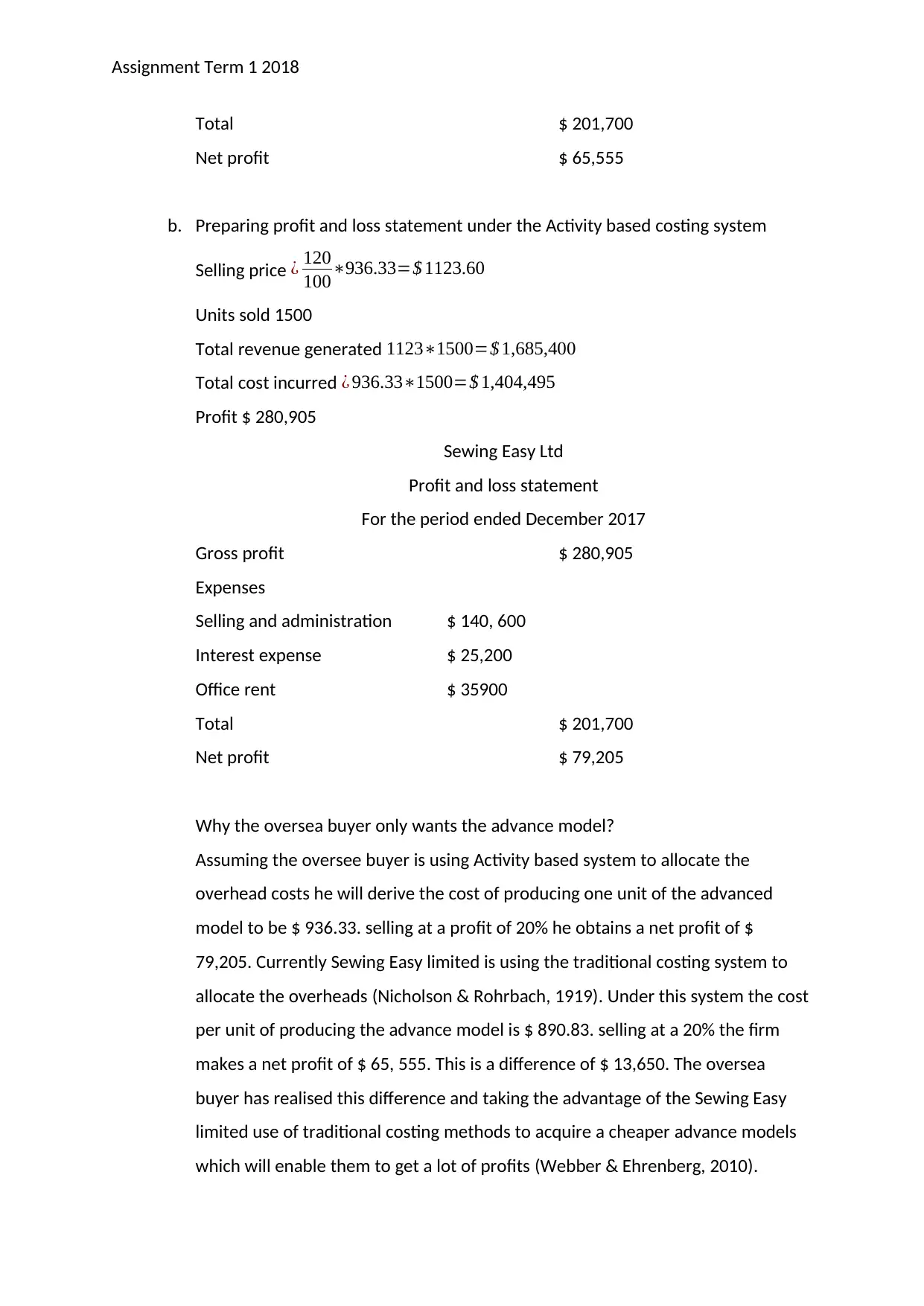

Total $ 201,700

Net profit $ 65,555

b. Preparing profit and loss statement under the Activity based costing system

Selling price ¿ 120

100∗936.33=$ 1123.60

Units sold 1500

Total revenue generated 1123∗1500=$ 1,685,400

Total cost incurred ¿ 936.33∗1500=$ 1,404,495

Profit $ 280,905

Sewing Easy Ltd

Profit and loss statement

For the period ended December 2017

Gross profit $ 280,905

Expenses

Selling and administration $ 140, 600

Interest expense $ 25,200

Office rent $ 35900

Total $ 201,700

Net profit $ 79,205

Why the oversea buyer only wants the advance model?

Assuming the oversee buyer is using Activity based system to allocate the

overhead costs he will derive the cost of producing one unit of the advanced

model to be $ 936.33. selling at a profit of 20% he obtains a net profit of $

79,205. Currently Sewing Easy limited is using the traditional costing system to

allocate the overheads (Nicholson & Rohrbach, 1919). Under this system the cost

per unit of producing the advance model is $ 890.83. selling at a 20% the firm

makes a net profit of $ 65, 555. This is a difference of $ 13,650. The oversea

buyer has realised this difference and taking the advantage of the Sewing Easy

limited use of traditional costing methods to acquire a cheaper advance models

which will enable them to get a lot of profits (Webber & Ehrenberg, 2010).

Total $ 201,700

Net profit $ 65,555

b. Preparing profit and loss statement under the Activity based costing system

Selling price ¿ 120

100∗936.33=$ 1123.60

Units sold 1500

Total revenue generated 1123∗1500=$ 1,685,400

Total cost incurred ¿ 936.33∗1500=$ 1,404,495

Profit $ 280,905

Sewing Easy Ltd

Profit and loss statement

For the period ended December 2017

Gross profit $ 280,905

Expenses

Selling and administration $ 140, 600

Interest expense $ 25,200

Office rent $ 35900

Total $ 201,700

Net profit $ 79,205

Why the oversea buyer only wants the advance model?

Assuming the oversee buyer is using Activity based system to allocate the

overhead costs he will derive the cost of producing one unit of the advanced

model to be $ 936.33. selling at a profit of 20% he obtains a net profit of $

79,205. Currently Sewing Easy limited is using the traditional costing system to

allocate the overheads (Nicholson & Rohrbach, 1919). Under this system the cost

per unit of producing the advance model is $ 890.83. selling at a 20% the firm

makes a net profit of $ 65, 555. This is a difference of $ 13,650. The oversea

buyer has realised this difference and taking the advantage of the Sewing Easy

limited use of traditional costing methods to acquire a cheaper advance models

which will enable them to get a lot of profits (Webber & Ehrenberg, 2010).

Assignment Term 1 2018

Importance of accurate product costing

Product cost entails assigning costs to inventory and the production with

consideration to the expenses incurred when producing a product. It is very vital

for a firm to be precise and accurate when allocating costs to products (Destri, et

al., 2012).

Accuracy; this is the efficiency with which the firm’s expenses can be traced

through the products cost to the inventory values. Accuracy in the costing

process ensures the business can adhere to the matching principle concept I.e.

attaching costs to values they create throughout the business operations.

Project tracking; this is keeping an eye on the products budget to verify whether

the costs are as per the expectation after assigning them at various stages of the

product. Costing is a vital process in the project tracking. Inaccuracy in the

costing system makes analysis of cashflows and evaluation of the success of a

project to be a futile procedure. Through accurate costing various costs can be

distributed to departments for accuracy evaluation.

Making decisions; whenever the management of a firm decides profitability is

usually at the centre of it. For instance, in our case the firm would wish to expand

its sales to an external buyer. This decision may appear profitable due to

inaccurate costing when in reality the firm is making a loss. This indicate the role

accuracy plays when it comes to decision making. Poor costing system may be

the difference between a firm’s viability and failure.

Project development; this refers to innovation of new products. Whenever a firm

intends to design a new product, the profitability of the item will dictate whether

the firm should pursue the new idea or not. Poor costing may hence means

making a blind decision (Szatmary, 2011).

4. Why the actual overhead does vary from the applied overhead?

The overhead applied by the firms during the production costing is normally

different from the actual overhead which will be realised in the accounting process.

This difference can be attributed to the factors highlighted below;

Inconsistent occurrence of the overhead costs, some of the indirect costs do occur

ununiformly over the cause of the business activities. An example is the heating cost.

This may be lower during summer than in winter. It is though very unrealistic for the

Importance of accurate product costing

Product cost entails assigning costs to inventory and the production with

consideration to the expenses incurred when producing a product. It is very vital

for a firm to be precise and accurate when allocating costs to products (Destri, et

al., 2012).

Accuracy; this is the efficiency with which the firm’s expenses can be traced

through the products cost to the inventory values. Accuracy in the costing

process ensures the business can adhere to the matching principle concept I.e.

attaching costs to values they create throughout the business operations.

Project tracking; this is keeping an eye on the products budget to verify whether

the costs are as per the expectation after assigning them at various stages of the

product. Costing is a vital process in the project tracking. Inaccuracy in the

costing system makes analysis of cashflows and evaluation of the success of a

project to be a futile procedure. Through accurate costing various costs can be

distributed to departments for accuracy evaluation.

Making decisions; whenever the management of a firm decides profitability is

usually at the centre of it. For instance, in our case the firm would wish to expand

its sales to an external buyer. This decision may appear profitable due to

inaccurate costing when in reality the firm is making a loss. This indicate the role

accuracy plays when it comes to decision making. Poor costing system may be

the difference between a firm’s viability and failure.

Project development; this refers to innovation of new products. Whenever a firm

intends to design a new product, the profitability of the item will dictate whether

the firm should pursue the new idea or not. Poor costing may hence means

making a blind decision (Szatmary, 2011).

4. Why the actual overhead does vary from the applied overhead?

The overhead applied by the firms during the production costing is normally

different from the actual overhead which will be realised in the accounting process.

This difference can be attributed to the factors highlighted below;

Inconsistent occurrence of the overhead costs, some of the indirect costs do occur

ununiformly over the cause of the business activities. An example is the heating cost.

This may be lower during summer than in winter. It is though very unrealistic for the

Assignment Term 1 2018

firm to keep on shifting the cost allocating to fit a single month hence may apply a

uniform cost for the entire period which makes it different from the actual cost.

The management fix some of the costs, for instance the depreciation may be fixed at

a given percentage over a period. Since the production rate do fluctuate from time

to time the fixed applied cost may not correspond to the actual cost realised

(Blocher, et al., 2016).

The overhead costs are occasionally predetermined, this predetermined value is

allocated before the actual value is incurred. This means its just a mere estimate

using the historical data. This past data may not reflect the current situation and

hence the actual incurred overhead end up being difference.

Overhead costs can be treated in three ways;

The value may be written off in the costing profit and loss statement accounts.

Secondly, it is possible to calculate a supplementary rate then apply it to the

production.

Thirdly the value can be carried forwards and written off in the subsequent period’s

profit and loss accounts.

5. Benefits of ABC

Product costing accuracy, the use of ABC system means more accurate cost and

reliable information for making management decisions. The focus is put on the

relationship between the cost and the effect on the product. This way the activities

that trigger the costs are stressed and therefore ABC gives a more accurate cost

especially in advanced manufacturing situations where technology is highly applied.

Cost behaviour information, the use of ABC identifies the nature of costs behaviour.

With this information the managers can identify costly activities which do not add

much value to the entire production process and eliminate them. Through regulation

of activities that may have triggered the fixed overhead costs the managers are able

to exercise a level of control. The use of ABC has made cost behaviours to be more

visible hence can easily be influenced by the management decisions.

Tracing activities to their costs, ABC makes use of several cost drivers many of which

are based on transactions instead of quantity of product produced. This concern

firm to keep on shifting the cost allocating to fit a single month hence may apply a

uniform cost for the entire period which makes it different from the actual cost.

The management fix some of the costs, for instance the depreciation may be fixed at

a given percentage over a period. Since the production rate do fluctuate from time

to time the fixed applied cost may not correspond to the actual cost realised

(Blocher, et al., 2016).

The overhead costs are occasionally predetermined, this predetermined value is

allocated before the actual value is incurred. This means its just a mere estimate

using the historical data. This past data may not reflect the current situation and

hence the actual incurred overhead end up being difference.

Overhead costs can be treated in three ways;

The value may be written off in the costing profit and loss statement accounts.

Secondly, it is possible to calculate a supplementary rate then apply it to the

production.

Thirdly the value can be carried forwards and written off in the subsequent period’s

profit and loss accounts.

5. Benefits of ABC

Product costing accuracy, the use of ABC system means more accurate cost and

reliable information for making management decisions. The focus is put on the

relationship between the cost and the effect on the product. This way the activities

that trigger the costs are stressed and therefore ABC gives a more accurate cost

especially in advanced manufacturing situations where technology is highly applied.

Cost behaviour information, the use of ABC identifies the nature of costs behaviour.

With this information the managers can identify costly activities which do not add

much value to the entire production process and eliminate them. Through regulation

of activities that may have triggered the fixed overhead costs the managers are able

to exercise a level of control. The use of ABC has made cost behaviours to be more

visible hence can easily be influenced by the management decisions.

Tracing activities to their costs, ABC makes use of several cost drivers many of which

are based on transactions instead of quantity of product produced. This concern

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assignment Term 1 2018

with activities within and beyond the firm enables the managers to be able to trace

the costs to specific products.

Informed decision making, the ability of ABC to avail accurate product costs makes it

easy for the managers to make accurate decisions as they have the relevant

information needed to do so. The selling price for a product can therefore be fixed at

a realistic value due to the readily available production cost.

Capacity utilisation and cost minimisation, the pooling of activity costs and activity

cost identification accompanying ABC system can be applied in several ways. For

instance, in identifying excess capacity and fostering costs through a comparison of

resources currently being consumed and those needed under ABC. This gives room

for implementing an activity-based budgeting where resource relationship as

identified by ABC can be used to project the future resource demand (Lederman,

2013).

Limitations of ABC

Despite enjoying several advantages ABC also comes with a pack of challenges below

are a few highlights;

Complex and expensive, the use of ABC is accompanied by several cost pols and

multiple cost drivers making it more complex than the use of traditional costing

system. The complexity is associated with high management costs.

Difficulties in selecting cost drivers, the cost driver’s selection, assignment as well as

variations is a difficult task which consumes resources and time (Maher, et al., 2005).

Unfavourable to some firms, the utility of ABC varies with the size of the

organizations. For instance, the system is more advantageous to larger organizations

than the smaller firms. The firms who apply cost plus pricing may find it more

favourable to apply the ABC as the pricing can be easily derived from the ABC unit

cost. This though is not the case with the firms applying market-based pricing. The

ABC’s impact is also altered based on the magnitude of technology applied in a firm

Measurement complications, the major problem incurred under ABC is the

measurements that need to be done to implement it. The use of ABC demand that

management estimate costs of activity pools and identify appropriate cost driver to

serve as the allocation base. This entire process is composed of several data

with activities within and beyond the firm enables the managers to be able to trace

the costs to specific products.

Informed decision making, the ability of ABC to avail accurate product costs makes it

easy for the managers to make accurate decisions as they have the relevant

information needed to do so. The selling price for a product can therefore be fixed at

a realistic value due to the readily available production cost.

Capacity utilisation and cost minimisation, the pooling of activity costs and activity

cost identification accompanying ABC system can be applied in several ways. For

instance, in identifying excess capacity and fostering costs through a comparison of

resources currently being consumed and those needed under ABC. This gives room

for implementing an activity-based budgeting where resource relationship as

identified by ABC can be used to project the future resource demand (Lederman,

2013).

Limitations of ABC

Despite enjoying several advantages ABC also comes with a pack of challenges below

are a few highlights;

Complex and expensive, the use of ABC is accompanied by several cost pols and

multiple cost drivers making it more complex than the use of traditional costing

system. The complexity is associated with high management costs.

Difficulties in selecting cost drivers, the cost driver’s selection, assignment as well as

variations is a difficult task which consumes resources and time (Maher, et al., 2005).

Unfavourable to some firms, the utility of ABC varies with the size of the

organizations. For instance, the system is more advantageous to larger organizations

than the smaller firms. The firms who apply cost plus pricing may find it more

favourable to apply the ABC as the pricing can be easily derived from the ABC unit

cost. This though is not the case with the firms applying market-based pricing. The

ABC’s impact is also altered based on the magnitude of technology applied in a firm

Measurement complications, the major problem incurred under ABC is the

measurements that need to be done to implement it. The use of ABC demand that

management estimate costs of activity pools and identify appropriate cost driver to

serve as the allocation base. This entire process is composed of several data

Assignment Term 1 2018

collection and calculations. This is a costly affair especially if you consider that the

cost rates also need to be adjusted regularly.

References

Blocher, S. & Cokins, J., 2016. Cost Management - A Strategic Emphasis. 7th ed. s.l.:McGraw-

Hill.

Destri, L. A. M., Picone, P. M. & Minà, A., 2012. Bringing Strategy Back into Financial Systems

of Performance Measurement: Integrating EVA and PBC. Business System Review, 1(1), pp.

85-102..

Hurlburt, S. & Kirshstein, R., 2014. The ABCs of Activity-Based Costing in Community

Colleges, s.l.: American Institutes for Research .

Lederman, D., 2013. CFO survey reveals doubts about financial sustainability. [Online]

Available at: http://www.insidehighered.com/news/survey/cfo-survey-revealsdoubts-about-

financial-sustainability#sthash.KqLNIe4E.dpbs

[Accessed 21 May 2018].

Maher, Lanen & Rahan, 2005. Fundamentals of Cost Accounting. 1st ed. s.l.:McGraw-Hill.

Nicholson, J. & Rohrbach, J. D., 1919. Cost accounting. New York: Ronald Press.

Szatmary, D. P., 2011. Activity-based budgeting in higher education. Continuing Higher

Education, 75(1), p. 69–85. .

Webber, D. A. & Ehrenberg, R. G., 2010. Do expenditures other than instructional

expenditures affect graduation and persistence rates in American higher education?.

Economics of Education Review, 29(6), p. 947–958.

collection and calculations. This is a costly affair especially if you consider that the

cost rates also need to be adjusted regularly.

References

Blocher, S. & Cokins, J., 2016. Cost Management - A Strategic Emphasis. 7th ed. s.l.:McGraw-

Hill.

Destri, L. A. M., Picone, P. M. & Minà, A., 2012. Bringing Strategy Back into Financial Systems

of Performance Measurement: Integrating EVA and PBC. Business System Review, 1(1), pp.

85-102..

Hurlburt, S. & Kirshstein, R., 2014. The ABCs of Activity-Based Costing in Community

Colleges, s.l.: American Institutes for Research .

Lederman, D., 2013. CFO survey reveals doubts about financial sustainability. [Online]

Available at: http://www.insidehighered.com/news/survey/cfo-survey-revealsdoubts-about-

financial-sustainability#sthash.KqLNIe4E.dpbs

[Accessed 21 May 2018].

Maher, Lanen & Rahan, 2005. Fundamentals of Cost Accounting. 1st ed. s.l.:McGraw-Hill.

Nicholson, J. & Rohrbach, J. D., 1919. Cost accounting. New York: Ronald Press.

Szatmary, D. P., 2011. Activity-based budgeting in higher education. Continuing Higher

Education, 75(1), p. 69–85. .

Webber, D. A. & Ehrenberg, R. G., 2010. Do expenditures other than instructional

expenditures affect graduation and persistence rates in American higher education?.

Economics of Education Review, 29(6), p. 947–958.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.