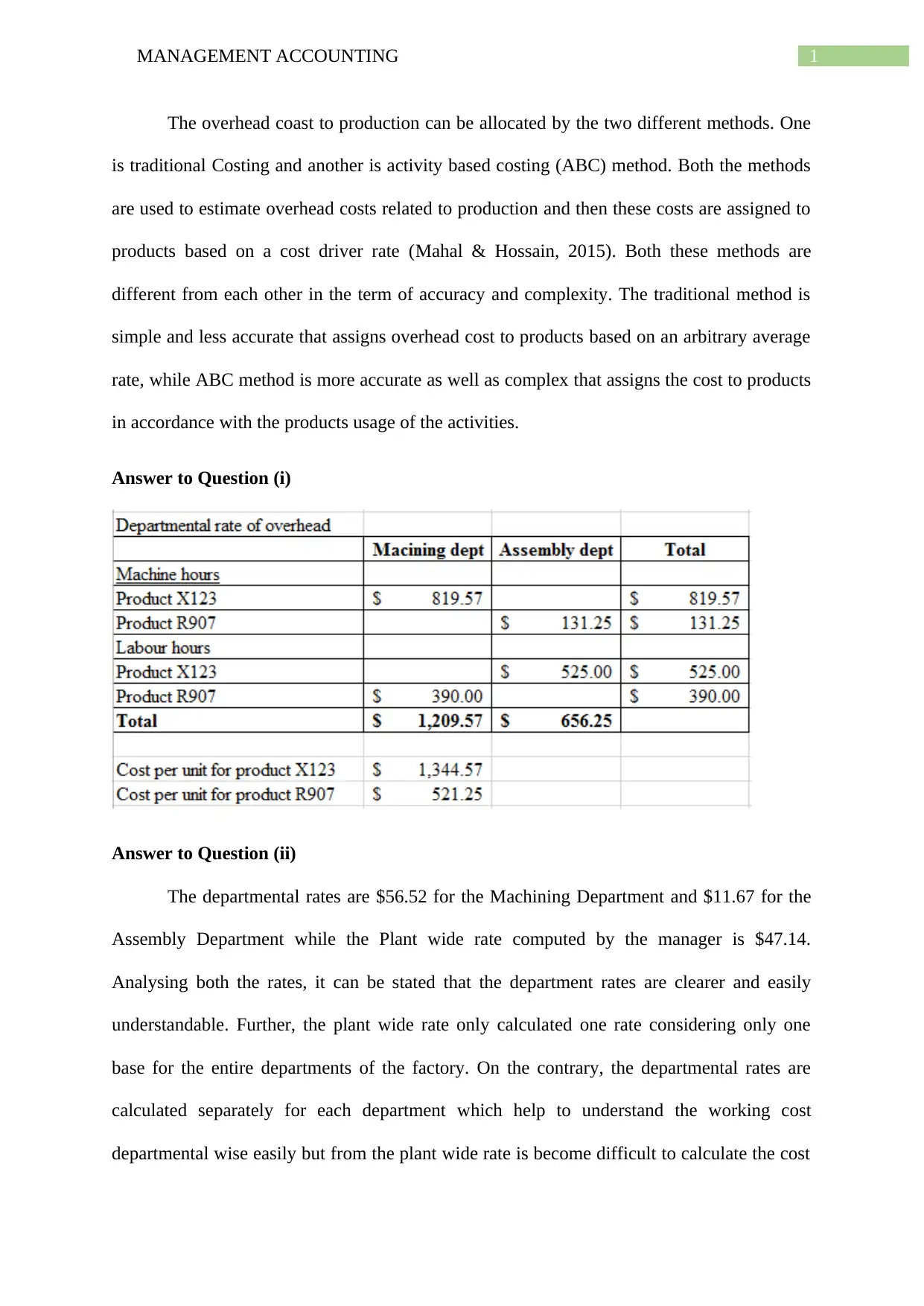

This document discusses the overhead cost allocation methods in management accounting, specifically the traditional costing method and activity-based costing (ABC) method. It explains the differences between these two methods in terms of accuracy and complexity. The document also analyzes the departmental rates and plant wide rate for overhead allocation and recommends the use of departmental rates for better cost calculation. Additionally, it highlights the drawbacks of Rex's plant wide overhead allocation method and suggests using a more accurate method. Finally, it discusses the benefits of ABC method in improving overhead allocation and identifies its advantages over traditional costing approach.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)