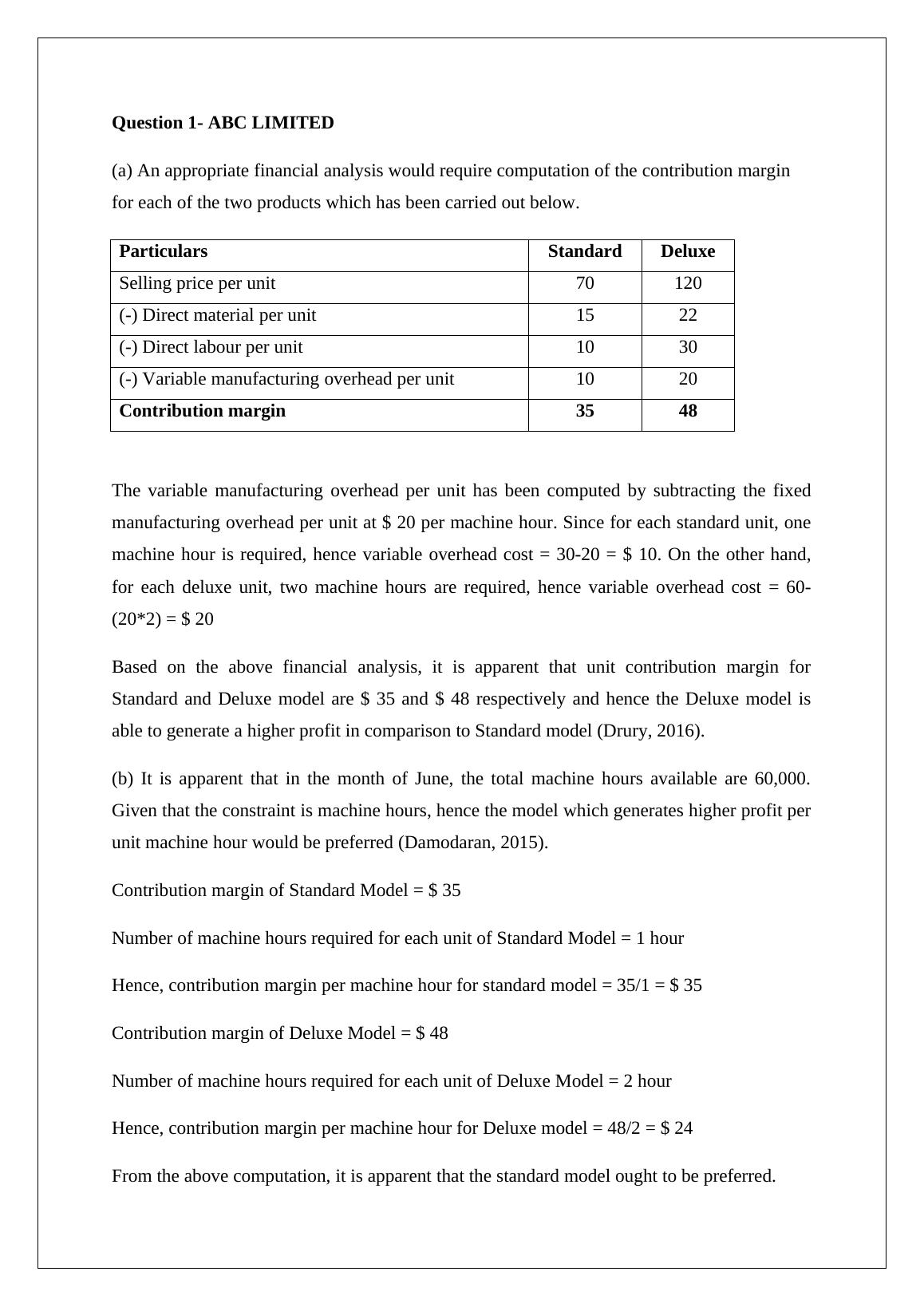

Management Accounting: Financial Analysis and Profit Maximization

4 Pages735 Words415 Views

Added on 2023-05-31

About This Document

This article discusses financial analysis and profit maximization in management accounting, with a focus on a case study of ABC Limited and Sam. It covers topics such as contribution margin, incremental costs and benefits, and machine hour constraints. The article also includes references to relevant textbooks on the subject.

Management Accounting: Financial Analysis and Profit Maximization

Added on 2023-05-31

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Managerial Accounting: Fixed, Variable and Semi-Variable Costs

|7

|1127

|426

ACC203 Management Accounting

|7

|934

|30

Managerial Accounting Assignment on Break-Even Analysis and Sales Mix

|9

|996

|180

Managerial Accounting: Solved Assignments and Essays - Desklib

|8

|699

|91

Decision Support Tools : Assignment

|7

|1107

|270

Technical Analysis Definition

|17

|906

|342