Management Accounting: Financial Position and Earnings Statement

VerifiedAdded on 2023/06/14

|11

|1722

|353

AI Summary

This article provides a detailed analysis of the financial position and earnings statement of a company. It includes a statement of financial position and earnings statement, along with journal entries, an adjustment worksheet, depreciation computation, and inventory value. Additionally, the article includes a memo on internal control weaknesses and recommended solutions. The memo highlights the weaknesses in the debtor policy and cash receiving and recording system of the company and suggests measures to improve the internal control of the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MANAGEMENT ACCOUNTING

Table of Contents

Requirement 1:.................................................................................................................................2

Statement of Financial Position:..................................................................................................2

Statement of Earnings:.................................................................................................................3

Requirement 2:.................................................................................................................................4

Reference.........................................................................................................................................6

Appendix..........................................................................................................................................7

Journal Entries:............................................................................................................................7

Adjustment Worksheet:...............................................................................................................8

Depreciation Computation:........................................................................................................10

Inventory Value:........................................................................................................................10

MANAGEMENT ACCOUNTING

Table of Contents

Requirement 1:.................................................................................................................................2

Statement of Financial Position:..................................................................................................2

Statement of Earnings:.................................................................................................................3

Requirement 2:.................................................................................................................................4

Reference.........................................................................................................................................6

Appendix..........................................................................................................................................7

Journal Entries:............................................................................................................................7

Adjustment Worksheet:...............................................................................................................8

Depreciation Computation:........................................................................................................10

Inventory Value:........................................................................................................................10

2

MANAGEMENT ACCOUNTING

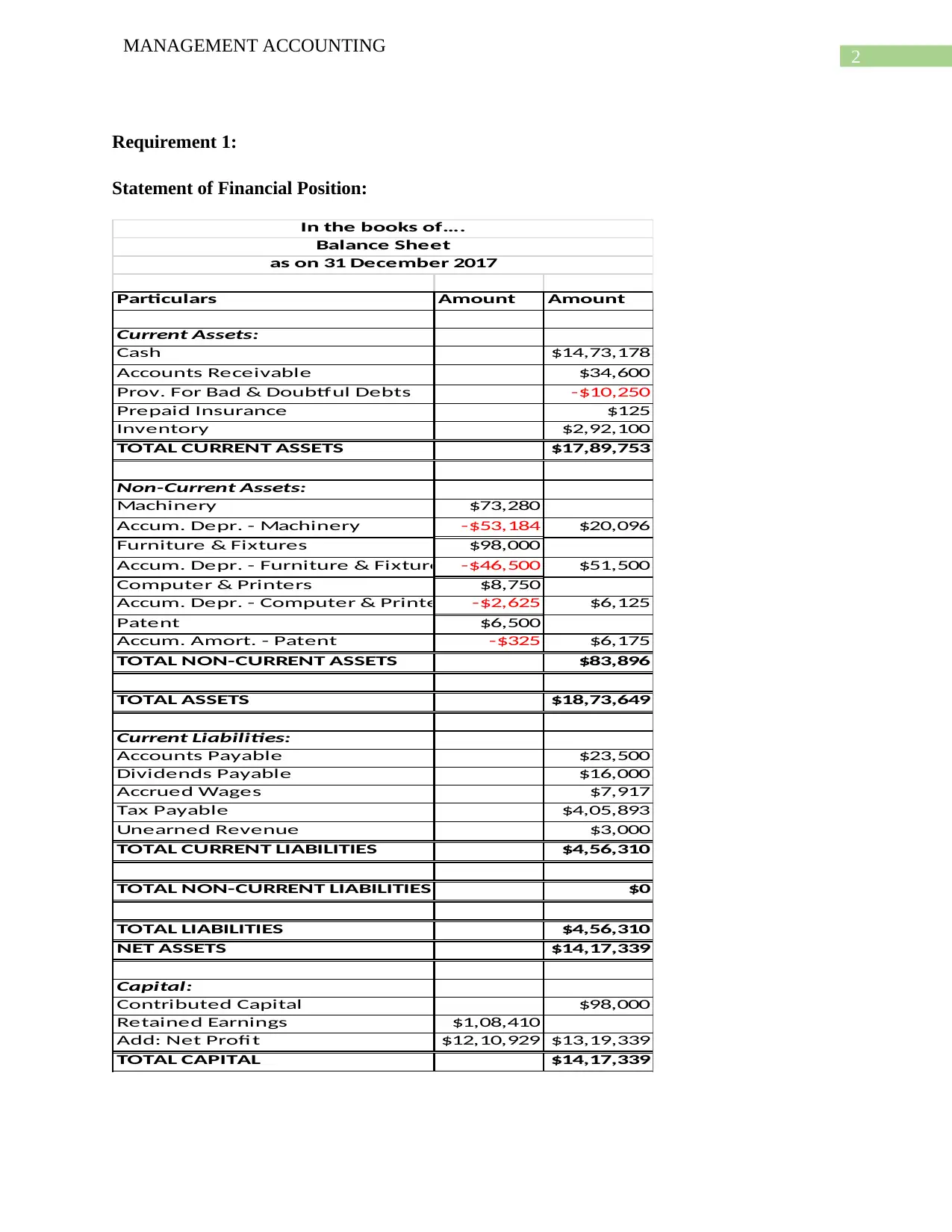

Requirement 1:

Statement of Financial Position:

Particulars Amount Amount

Current Assets:

Cash $14,73,178

Accounts Receivable $34,600

Prov. For Bad & Doubtful Debts -$10,250

Prepaid Insurance $125

Inventory $2,92,100

TOTAL CURRENT ASSETS $17,89,753

Non-Current Assets:

Machinery $73,280

Accum. Depr. - Machinery -$53,184 $20,096

Furniture & Fixtures $98,000

Accum. Depr. - Furniture & Fixtures -$46,500 $51,500

Computer & Printers $8,750

Accum. Depr. - Computer & Printers -$2,625 $6,125

Patent $6,500

Accum. Amort. - Patent -$325 $6,175

TOTAL NON-CURRENT ASSETS $83,896

TOTAL ASSETS $18,73,649

Current Liabilities:

Accounts Payable $23,500

Dividends Payable $16,000

Accrued Wages $7,917

Tax Payable $4,05,893

Unearned Revenue $3,000

TOTAL CURRENT LIABILITIES $4,56,310

TOTAL NON-CURRENT LIABILITIES $0

TOTAL LIABILITIES $4,56,310

NET ASSETS $14,17,339

Capital:

Contributed Capital $98,000

Retained Earnings $1,08,410

Add: Net Profit $12,10,929 $13,19,339

TOTAL CAPITAL $14,17,339

In the books of….

Balance Sheet

as on 31 December 2017

MANAGEMENT ACCOUNTING

Requirement 1:

Statement of Financial Position:

Particulars Amount Amount

Current Assets:

Cash $14,73,178

Accounts Receivable $34,600

Prov. For Bad & Doubtful Debts -$10,250

Prepaid Insurance $125

Inventory $2,92,100

TOTAL CURRENT ASSETS $17,89,753

Non-Current Assets:

Machinery $73,280

Accum. Depr. - Machinery -$53,184 $20,096

Furniture & Fixtures $98,000

Accum. Depr. - Furniture & Fixtures -$46,500 $51,500

Computer & Printers $8,750

Accum. Depr. - Computer & Printers -$2,625 $6,125

Patent $6,500

Accum. Amort. - Patent -$325 $6,175

TOTAL NON-CURRENT ASSETS $83,896

TOTAL ASSETS $18,73,649

Current Liabilities:

Accounts Payable $23,500

Dividends Payable $16,000

Accrued Wages $7,917

Tax Payable $4,05,893

Unearned Revenue $3,000

TOTAL CURRENT LIABILITIES $4,56,310

TOTAL NON-CURRENT LIABILITIES $0

TOTAL LIABILITIES $4,56,310

NET ASSETS $14,17,339

Capital:

Contributed Capital $98,000

Retained Earnings $1,08,410

Add: Net Profit $12,10,929 $13,19,339

TOTAL CAPITAL $14,17,339

In the books of….

Balance Sheet

as on 31 December 2017

3

MANAGEMENT ACCOUNTING

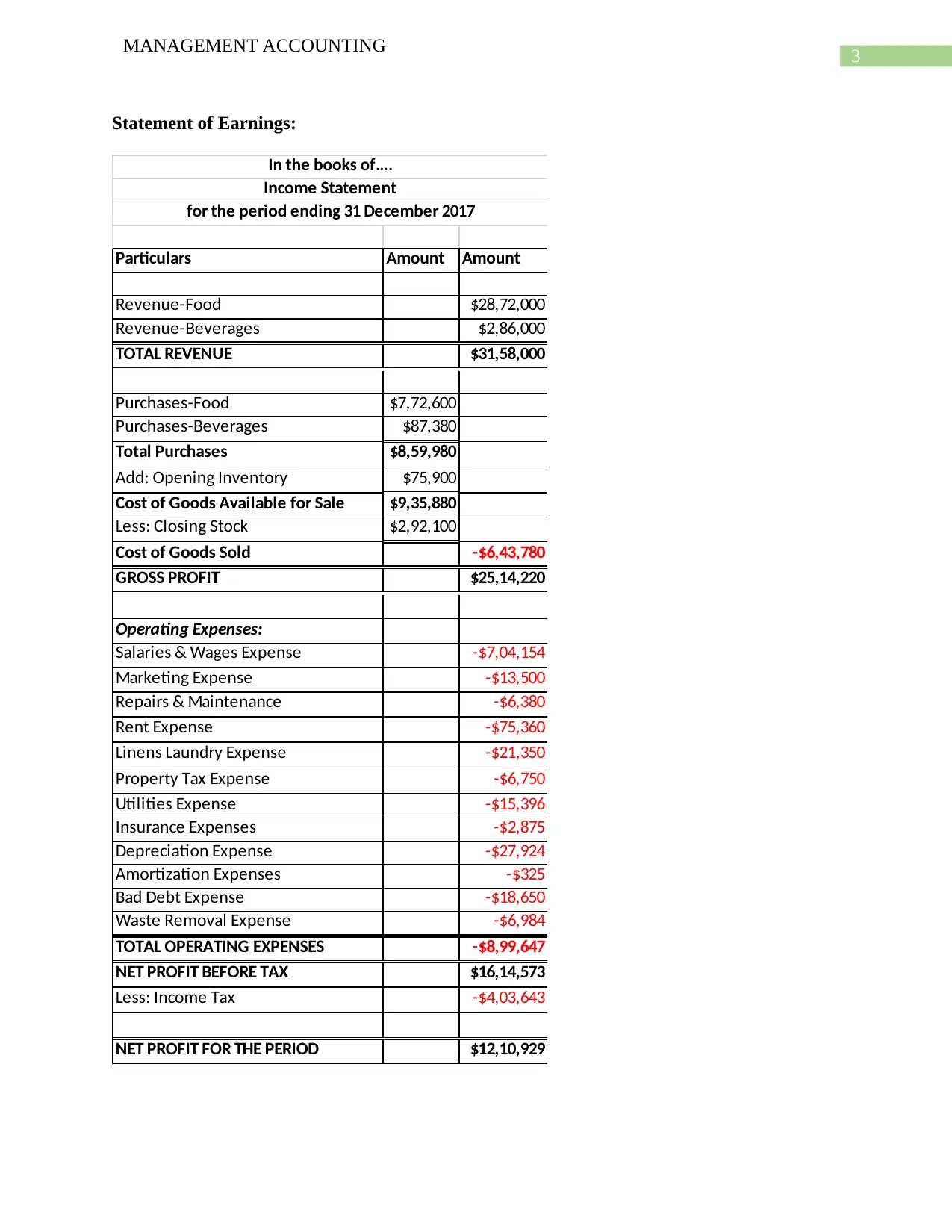

Statement of Earnings:

Particulars Amount Amount

Revenue-Food $28,72,000

Revenue-Beverages $2,86,000

TOTAL REVENUE $31,58,000

Purchases-Food $7,72,600

Purchases-Beverages $87,380

Total Purchases $8,59,980

Add: Opening Inventory $75,900

Cost of Goods Available for Sale $9,35,880

Less: Closing Stock $2,92,100

Cost of Goods Sold -$6,43,780

GROSS PROFIT $25,14,220

Operating Expenses:

Salaries & Wages Expense -$7,04,154

Marketing Expense -$13,500

Repairs & Maintenance -$6,380

Rent Expense -$75,360

Linens Laundry Expense -$21,350

Property Tax Expense -$6,750

Utilities Expense -$15,396

Insurance Expenses -$2,875

Depreciation Expense -$27,924

Amortization Expenses -$325

Bad Debt Expense -$18,650

Waste Removal Expense -$6,984

TOTAL OPERATING EXPENSES -$8,99,647

NET PROFIT BEFORE TAX $16,14,573

Less: Income Tax -$4,03,643

NET PROFIT FOR THE PERIOD $12,10,929

In the books of….

Income Statement

for the period ending 31 December 2017

MANAGEMENT ACCOUNTING

Statement of Earnings:

Particulars Amount Amount

Revenue-Food $28,72,000

Revenue-Beverages $2,86,000

TOTAL REVENUE $31,58,000

Purchases-Food $7,72,600

Purchases-Beverages $87,380

Total Purchases $8,59,980

Add: Opening Inventory $75,900

Cost of Goods Available for Sale $9,35,880

Less: Closing Stock $2,92,100

Cost of Goods Sold -$6,43,780

GROSS PROFIT $25,14,220

Operating Expenses:

Salaries & Wages Expense -$7,04,154

Marketing Expense -$13,500

Repairs & Maintenance -$6,380

Rent Expense -$75,360

Linens Laundry Expense -$21,350

Property Tax Expense -$6,750

Utilities Expense -$15,396

Insurance Expenses -$2,875

Depreciation Expense -$27,924

Amortization Expenses -$325

Bad Debt Expense -$18,650

Waste Removal Expense -$6,984

TOTAL OPERATING EXPENSES -$8,99,647

NET PROFIT BEFORE TAX $16,14,573

Less: Income Tax -$4,03,643

NET PROFIT FOR THE PERIOD $12,10,929

In the books of….

Income Statement

for the period ending 31 December 2017

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MANAGEMENT ACCOUNTING

Requirement 2:

Memo

To: Helmut Schneider

From: General

Date: 20th March 2018

RE: Internal Control Weaknesses and Recommended Solutions

The main purpose of this memo is to point out the internal control weaknesses which are

present in the business of Helmut’s Wurst Inc. One of the weakness in the policies of the

company is that the debtor policy of the company. The company allows credit sales of its food

products items which are purchased in bulk and no fixed time period is set for the collection of

such debts. The company is in tremendous needs of a proper debt collection policy which can

ensure that no part of the revenue of the company becomes a bad debt. The debt policy will be

including a period in which the debtors of the company has to pay back to the company. Another

weakness in the internal control system of the company is the cash receiving and recording

system of the business. The cash which is received by the stores are not properly recorded and

just a traditional journal for all receipts and payments are kept with the manager of the company

(Skaife, Veenman & Wangerin, 2013). All the cash which is generated from the operations of the

store are kept in the sealed drawer whose keys are with the manager of the store and such cash

generated are monthly deposited in banks. This is a weakness in the internal control system of

cash recording and maintenance.

If the management of the business does not look into the matter of debt management and

cash management then the company can face serious losses in the long run. If proper debt policy

is not implemented than the business will be having trouble to maintain the funds which are with

MANAGEMENT ACCOUNTING

Requirement 2:

Memo

To: Helmut Schneider

From: General

Date: 20th March 2018

RE: Internal Control Weaknesses and Recommended Solutions

The main purpose of this memo is to point out the internal control weaknesses which are

present in the business of Helmut’s Wurst Inc. One of the weakness in the policies of the

company is that the debtor policy of the company. The company allows credit sales of its food

products items which are purchased in bulk and no fixed time period is set for the collection of

such debts. The company is in tremendous needs of a proper debt collection policy which can

ensure that no part of the revenue of the company becomes a bad debt. The debt policy will be

including a period in which the debtors of the company has to pay back to the company. Another

weakness in the internal control system of the company is the cash receiving and recording

system of the business. The cash which is received by the stores are not properly recorded and

just a traditional journal for all receipts and payments are kept with the manager of the company

(Skaife, Veenman & Wangerin, 2013). All the cash which is generated from the operations of the

store are kept in the sealed drawer whose keys are with the manager of the store and such cash

generated are monthly deposited in banks. This is a weakness in the internal control system of

cash recording and maintenance.

If the management of the business does not look into the matter of debt management and

cash management then the company can face serious losses in the long run. If proper debt policy

is not implemented than the business will be having trouble to maintain the funds which are with

5

MANAGEMENT ACCOUNTING

the debts and also the overall liquidity of the business. There is also a chance of incurring losses

in the form of bad debts which can affect the business. In the case of cash management system of

the company, the journal which is maintained in the store can easily be tampered and

manipulated by employees or even by the manager. All it requires to engage in unethical

behavior is the opportunity to get away with the same (Klamm, Kobelsky & Watson, 2012). In

addition to this the company also needs to improve the deposit scheme which is followed for the

store. The cash which is kept in drawer can easily be misplaced or embezzled depending on the

access to the keys of the drawer. There is a risk of loss of money for the entire month which will

leave the shop in a devastated state.

The measures which can be suggested for improving the overall internal control of the

company are given below:

1. The management needs to incorporate debt collection strategies into the processes. The

credit period allowable will be depending on the level of purchases and dependence on

the buyer which can be of 60 days, 30 days or even more. Moreover, the business can

incorporate discounting techniques for early payments.

2. The management needs to implement computer-based recording of transaction techniques

with proper receipt available to the customers and the cash deposits of the company

should be made on a weekly basis for proper security of cash of the business.

MANAGEMENT ACCOUNTING

the debts and also the overall liquidity of the business. There is also a chance of incurring losses

in the form of bad debts which can affect the business. In the case of cash management system of

the company, the journal which is maintained in the store can easily be tampered and

manipulated by employees or even by the manager. All it requires to engage in unethical

behavior is the opportunity to get away with the same (Klamm, Kobelsky & Watson, 2012). In

addition to this the company also needs to improve the deposit scheme which is followed for the

store. The cash which is kept in drawer can easily be misplaced or embezzled depending on the

access to the keys of the drawer. There is a risk of loss of money for the entire month which will

leave the shop in a devastated state.

The measures which can be suggested for improving the overall internal control of the

company are given below:

1. The management needs to incorporate debt collection strategies into the processes. The

credit period allowable will be depending on the level of purchases and dependence on

the buyer which can be of 60 days, 30 days or even more. Moreover, the business can

incorporate discounting techniques for early payments.

2. The management needs to implement computer-based recording of transaction techniques

with proper receipt available to the customers and the cash deposits of the company

should be made on a weekly basis for proper security of cash of the business.

6

MANAGEMENT ACCOUNTING

Reference

Klamm, B. K., Kobelsky, K. W., & Watson, M. W. (2012). Determinants of the persistence of

internal control weaknesses. Accounting Horizons, 26(2), 307-333.

Skaife, H. A., Veenman, D., & Wangerin, D. (2013). Internal control over financial reporting and

managerial rent extraction: Evidence from the profitability of insider trading. Journal of

Accounting and Economics, 55(1), 91-110.

MANAGEMENT ACCOUNTING

Reference

Klamm, B. K., Kobelsky, K. W., & Watson, M. W. (2012). Determinants of the persistence of

internal control weaknesses. Accounting Horizons, 26(2), 307-333.

Skaife, H. A., Veenman, D., & Wangerin, D. (2013). Internal control over financial reporting and

managerial rent extraction: Evidence from the profitability of insider trading. Journal of

Accounting and Economics, 55(1), 91-110.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

Appendix

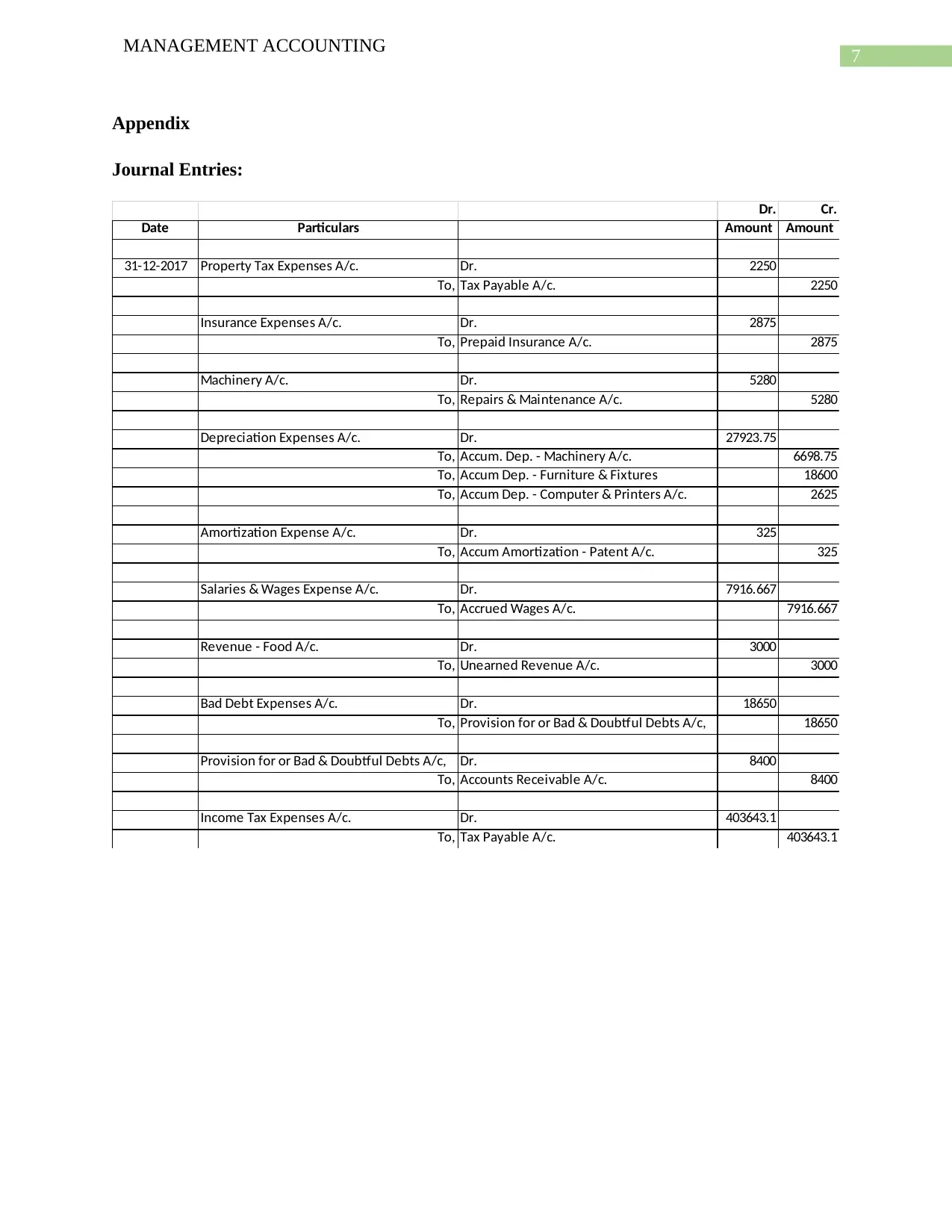

Journal Entries:

Dr. Cr.

Date Particulars Amount Amount

31-12-2017 Property Tax Expenses A/c. Dr. 2250

To, Tax Payable A/c. 2250

Insurance Expenses A/c. Dr. 2875

To, Prepaid Insurance A/c. 2875

Machinery A/c. Dr. 5280

To, Repairs & Maintenance A/c. 5280

Depreciation Expenses A/c. Dr. 27923.75

To, Accum. Dep. - Machinery A/c. 6698.75

To, Accum Dep. - Furniture & Fixtures 18600

To, Accum Dep. - Computer & Printers A/c. 2625

Amortization Expense A/c. Dr. 325

To, Accum Amortization - Patent A/c. 325

Salaries & Wages Expense A/c. Dr. 7916.667

To, Accrued Wages A/c. 7916.667

Revenue - Food A/c. Dr. 3000

To, Unearned Revenue A/c. 3000

Bad Debt Expenses A/c. Dr. 18650

To, Provision for or Bad & Doubtful Debts A/c, 18650

Provision for or Bad & Doubtful Debts A/c, Dr. 8400

To, Accounts Receivable A/c. 8400

Income Tax Expenses A/c. Dr. 403643.1

To, Tax Payable A/c. 403643.1

MANAGEMENT ACCOUNTING

Appendix

Journal Entries:

Dr. Cr.

Date Particulars Amount Amount

31-12-2017 Property Tax Expenses A/c. Dr. 2250

To, Tax Payable A/c. 2250

Insurance Expenses A/c. Dr. 2875

To, Prepaid Insurance A/c. 2875

Machinery A/c. Dr. 5280

To, Repairs & Maintenance A/c. 5280

Depreciation Expenses A/c. Dr. 27923.75

To, Accum. Dep. - Machinery A/c. 6698.75

To, Accum Dep. - Furniture & Fixtures 18600

To, Accum Dep. - Computer & Printers A/c. 2625

Amortization Expense A/c. Dr. 325

To, Accum Amortization - Patent A/c. 325

Salaries & Wages Expense A/c. Dr. 7916.667

To, Accrued Wages A/c. 7916.667

Revenue - Food A/c. Dr. 3000

To, Unearned Revenue A/c. 3000

Bad Debt Expenses A/c. Dr. 18650

To, Provision for or Bad & Doubtful Debts A/c, 18650

Provision for or Bad & Doubtful Debts A/c, Dr. 8400

To, Accounts Receivable A/c. 8400

Income Tax Expenses A/c. Dr. 403643.1

To, Tax Payable A/c. 403643.1

8

MANAGEMENT ACCOUNTING

Adjustment Worksheet:

MANAGEMENT ACCOUNTING

Adjustment Worksheet:

9

MANAGEMENT ACCOUNTING

Particulars Debit Credit Debit Credit Debit Credit

Cash $14,73,178 $14,73,178

Accounts Receivable $43,000 $8,400 $34,600

Prov. For Bad & Doubtful Debts $8,400 $18,650 $10,250

Prepaid Insurance $3,000 $2,875 $125

Inventory $75,900 $75,900

Machinery $68,000 $5,280 $73,280

Accum. Depr. - Machinery $46,485 $6,699 $53,184

Furniture & Fixtures $98,000 $98,000

Accum. Depr. - Furniture & Fixtures $27,900 $18,600 $46,500

Computer & Printers $8,750 $8,750

Accum. Depr. - Computer & Printers $2,625 $2,625

Patent $6,500 $6,500

Accum. Amort. - Patent $325 $325

Accounts Payable $23,500 $23,500

Dividends Payable $16,000 $16,000

Accrued Wages $7,917 $7,917

Tax Payable $4,05,893 $4,05,893

Unearned Revenue $3,000 $3,000

Contributed Capital $98,000 $98,000

Retained Earnings $1,08,410 $1,08,410

Revenue - Food $28,75,000 $3,000 $28,72,000

Revenue - Beverages $2,86,000 $2,86,000

Purchases - Food $7,72,600 $7,72,600

Purchases - Beverages $87,380 $87,380

Salaries & Wages Expense $6,96,237 $7,917 $7,04,154

Marketing Expense $13,500 $13,500

Repairs & Maintenance $11,660 $5,280 $6,380

Rent Expense $75,360 $75,360

Linens Laundry Expense $21,350 $21,350

Property Tax Expense $4,500 $2,250 $6,750

Utilities Expense $15,396 $15,396

Insurance Expenses $2,875 $2,875

Depreciation Expense $27,924 $27,924

Amortization Expenses $325 $325

Bad Debt Expense $18,650 $18,650

Profit on Adjustment of Inventory

Income Tax Expenses $4,03,643 $4,03,643

Waste Removal Expense $6,984 $6,984

TOTAL $34,81,295 $34,81,295 $4,80,264 $4,80,264 $39,33,604 $39,33,604

Unadjusted Trial

balance Adjustment Adjusted Trial balance

MANAGEMENT ACCOUNTING

Particulars Debit Credit Debit Credit Debit Credit

Cash $14,73,178 $14,73,178

Accounts Receivable $43,000 $8,400 $34,600

Prov. For Bad & Doubtful Debts $8,400 $18,650 $10,250

Prepaid Insurance $3,000 $2,875 $125

Inventory $75,900 $75,900

Machinery $68,000 $5,280 $73,280

Accum. Depr. - Machinery $46,485 $6,699 $53,184

Furniture & Fixtures $98,000 $98,000

Accum. Depr. - Furniture & Fixtures $27,900 $18,600 $46,500

Computer & Printers $8,750 $8,750

Accum. Depr. - Computer & Printers $2,625 $2,625

Patent $6,500 $6,500

Accum. Amort. - Patent $325 $325

Accounts Payable $23,500 $23,500

Dividends Payable $16,000 $16,000

Accrued Wages $7,917 $7,917

Tax Payable $4,05,893 $4,05,893

Unearned Revenue $3,000 $3,000

Contributed Capital $98,000 $98,000

Retained Earnings $1,08,410 $1,08,410

Revenue - Food $28,75,000 $3,000 $28,72,000

Revenue - Beverages $2,86,000 $2,86,000

Purchases - Food $7,72,600 $7,72,600

Purchases - Beverages $87,380 $87,380

Salaries & Wages Expense $6,96,237 $7,917 $7,04,154

Marketing Expense $13,500 $13,500

Repairs & Maintenance $11,660 $5,280 $6,380

Rent Expense $75,360 $75,360

Linens Laundry Expense $21,350 $21,350

Property Tax Expense $4,500 $2,250 $6,750

Utilities Expense $15,396 $15,396

Insurance Expenses $2,875 $2,875

Depreciation Expense $27,924 $27,924

Amortization Expenses $325 $325

Bad Debt Expense $18,650 $18,650

Profit on Adjustment of Inventory

Income Tax Expenses $4,03,643 $4,03,643

Waste Removal Expense $6,984 $6,984

TOTAL $34,81,295 $34,81,295 $4,80,264 $4,80,264 $39,33,604 $39,33,604

Unadjusted Trial

balance Adjustment Adjusted Trial balance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

MANAGEMENT ACCOUNTING

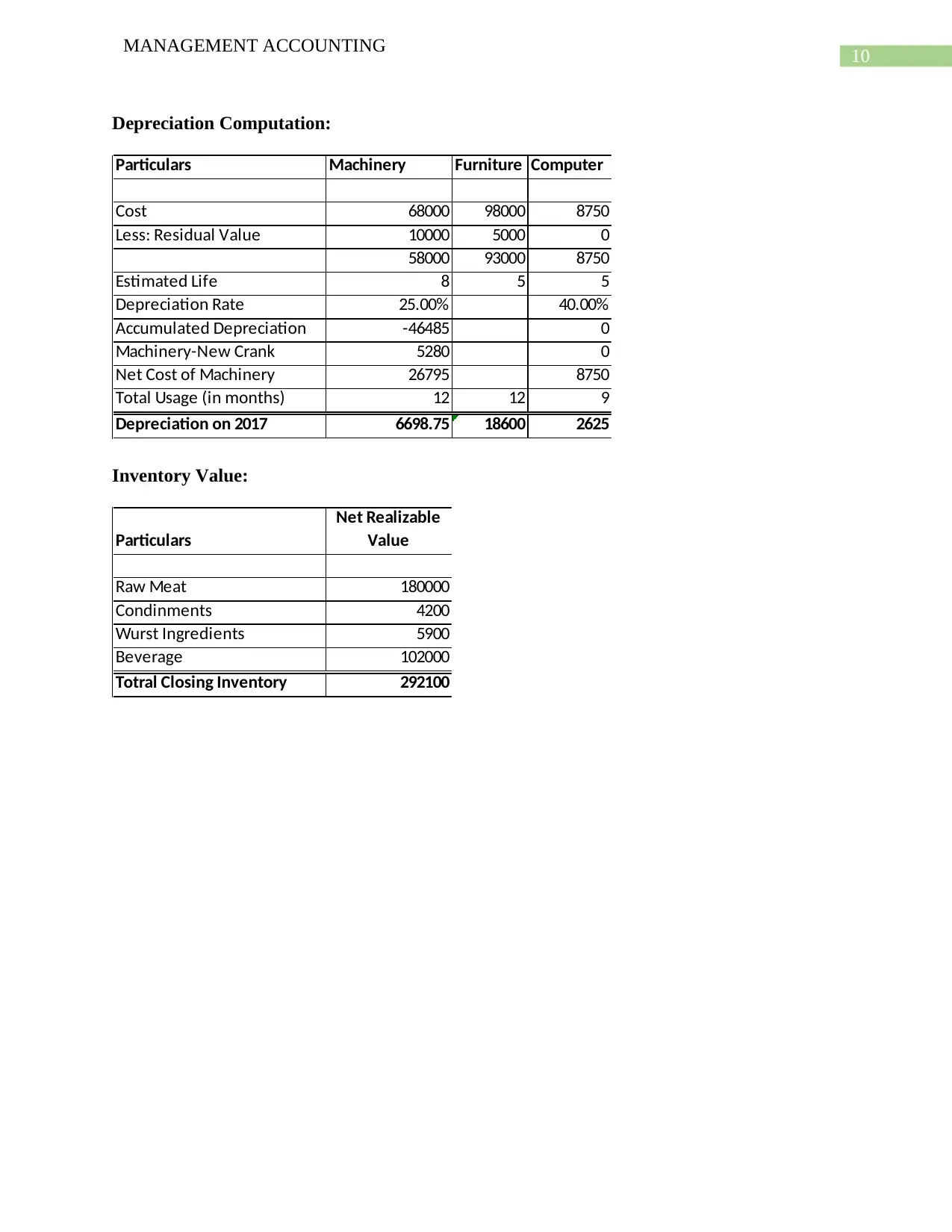

Depreciation Computation:

Particulars Machinery Furniture Computer

Cost 68000 98000 8750

Less: Residual Value 10000 5000 0

58000 93000 8750

Estimated Life 8 5 5

Depreciation Rate 25.00% 40.00%

Accumulated Depreciation -46485 0

Machinery-New Crank 5280 0

Net Cost of Machinery 26795 8750

Total Usage (in months) 12 12 9

Depreciation on 2017 6698.75 18600 2625

Inventory Value:

Particulars

Net Realizable

Value

Raw Meat 180000

Condinments 4200

Wurst Ingredients 5900

Beverage 102000

Totral Closing Inventory 292100

MANAGEMENT ACCOUNTING

Depreciation Computation:

Particulars Machinery Furniture Computer

Cost 68000 98000 8750

Less: Residual Value 10000 5000 0

58000 93000 8750

Estimated Life 8 5 5

Depreciation Rate 25.00% 40.00%

Accumulated Depreciation -46485 0

Machinery-New Crank 5280 0

Net Cost of Machinery 26795 8750

Total Usage (in months) 12 12 9

Depreciation on 2017 6698.75 18600 2625

Inventory Value:

Particulars

Net Realizable

Value

Raw Meat 180000

Condinments 4200

Wurst Ingredients 5900

Beverage 102000

Totral Closing Inventory 292100

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.