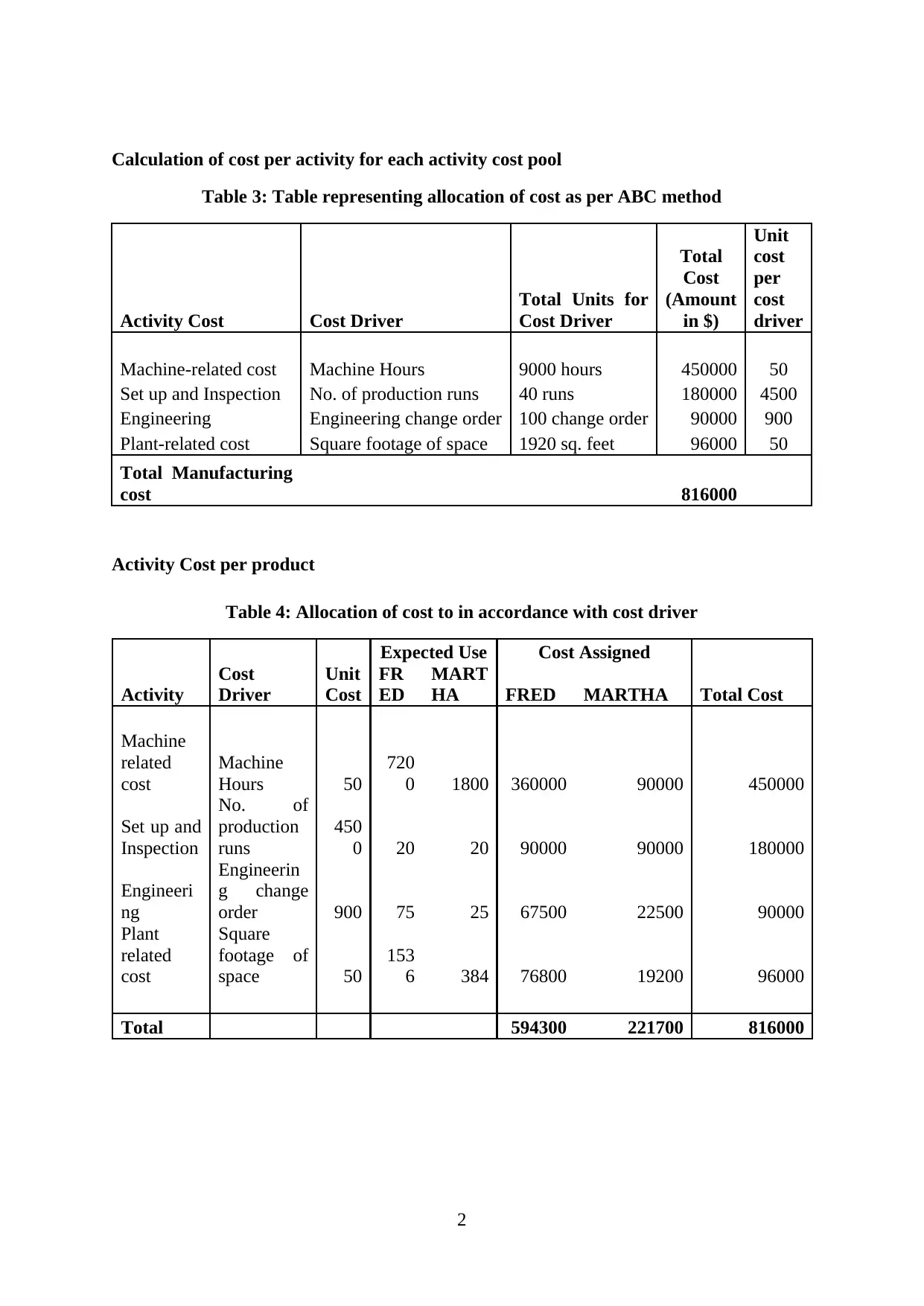

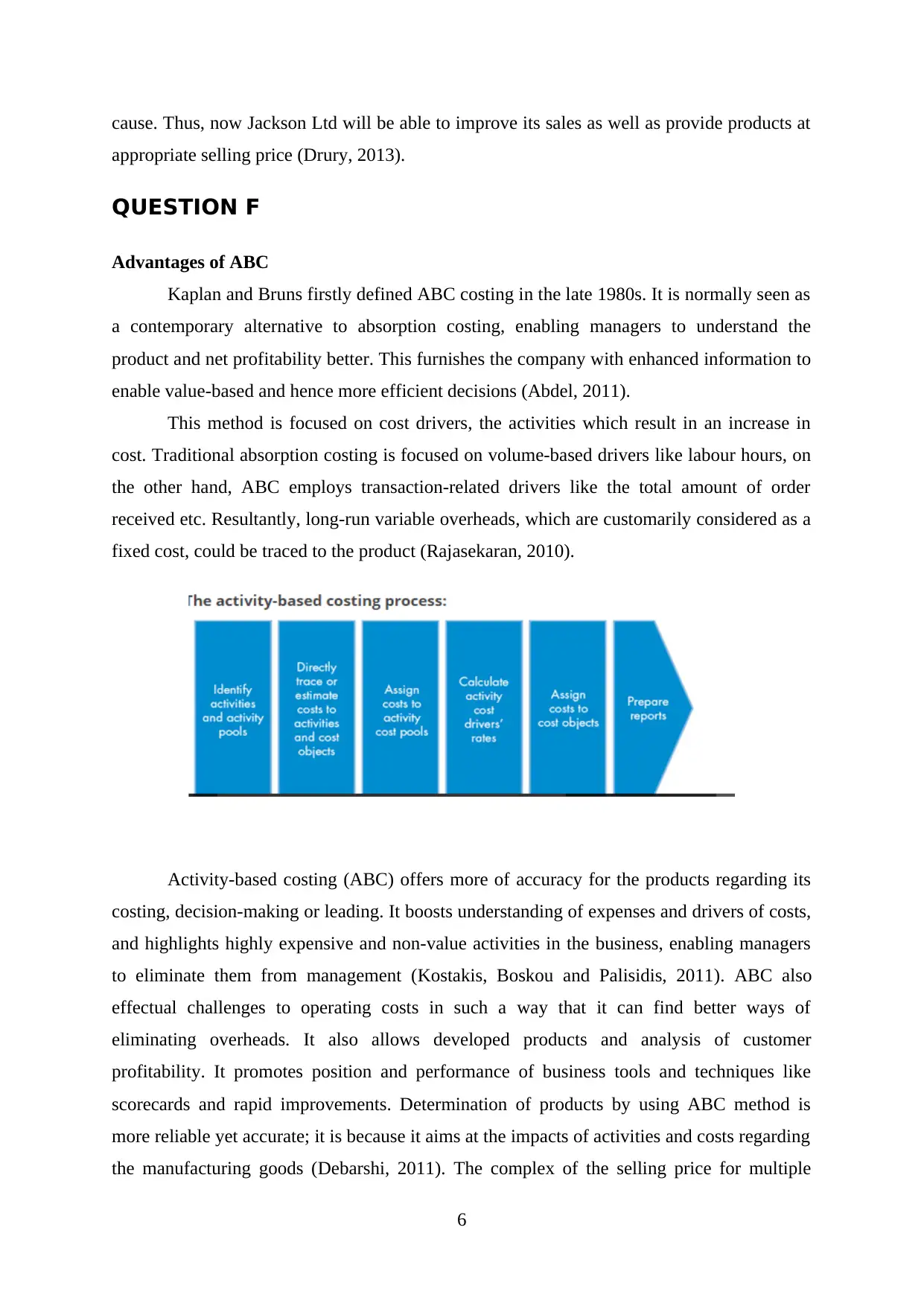

Activity-Based Costing (ABC) is a method that aims to allocate costs more accurately by identifying the root cause of expenses and allocating them based on cost drivers. This approach addresses the weaknesses of traditional absorption costing, which focuses on volume-based drivers like labor hours. ABC, on the other hand, employs transaction-related drivers like total order received, allowing for the tracing of long-run variable overheads to specific products. The advantages of ABC include improved understanding of expenses and drivers of costs, highlighting expensive and non-value activities, enabling better decision-making, and promoting product development and analysis of customer profitability.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)