Costing Comparison: Marginal, Absorption, and Break-Even Analysis

VerifiedAdded on 2023/01/07

|4

|437

|73

Homework Assignment

AI Summary

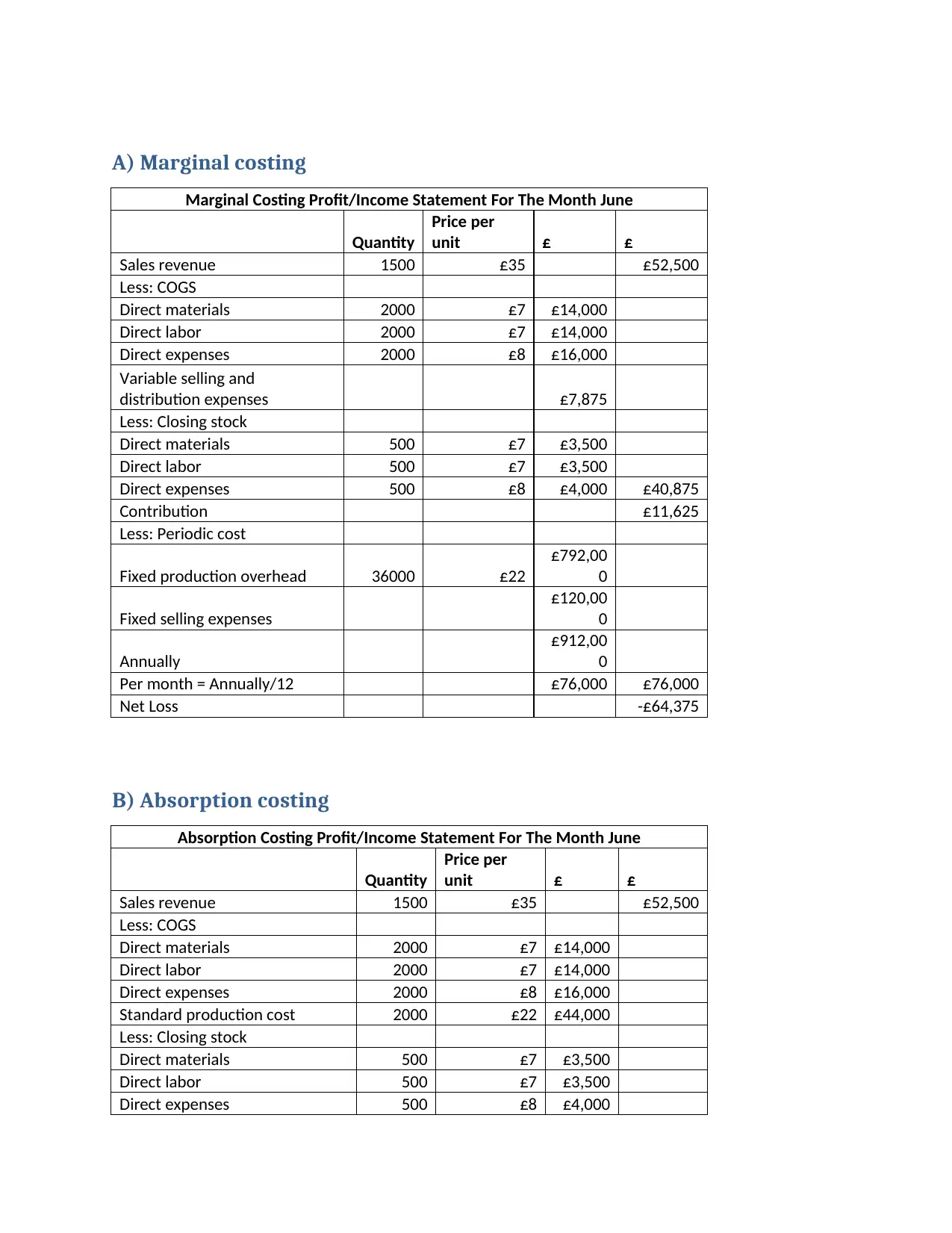

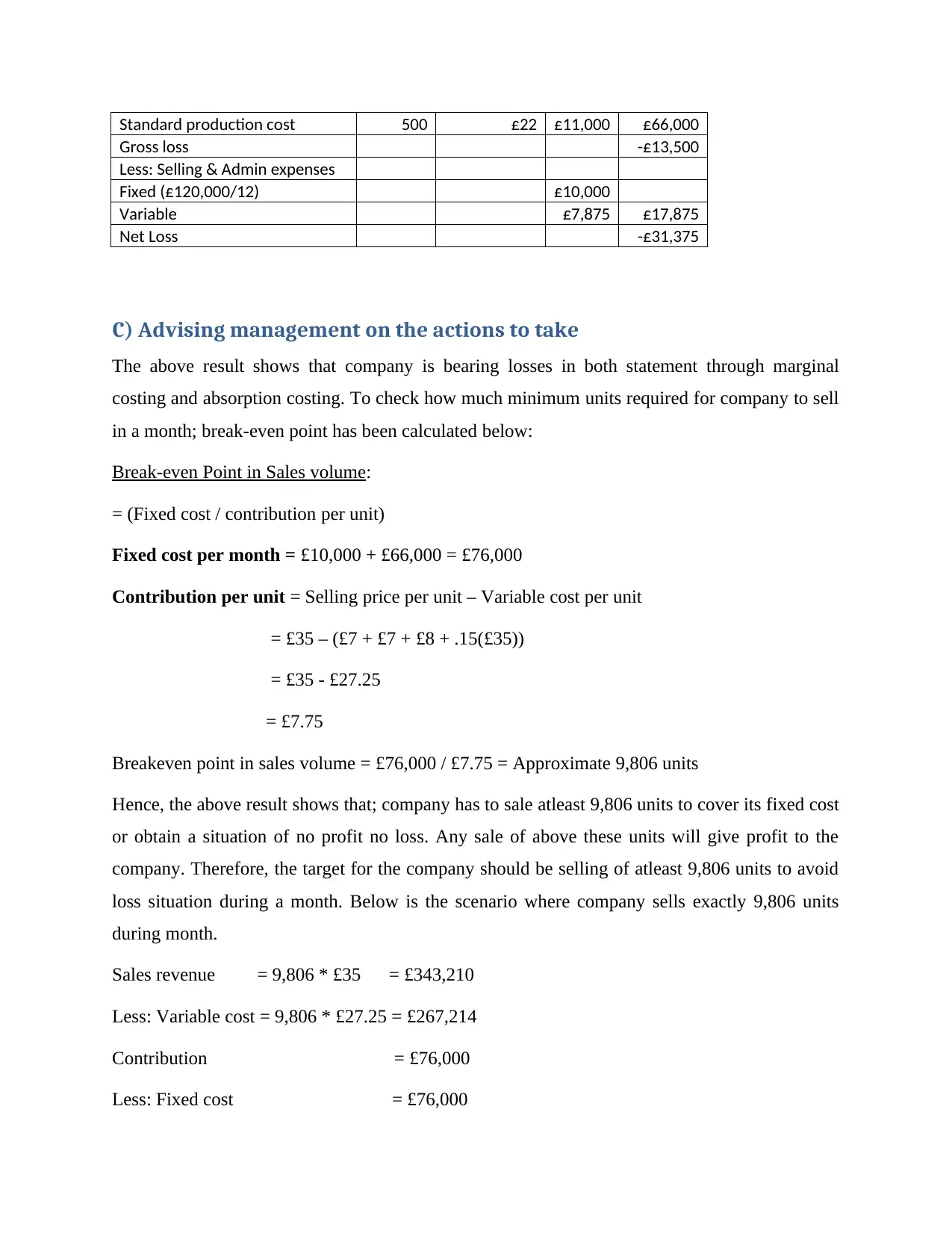

This assignment analyzes two primary costing methods: marginal costing and absorption costing. It presents profit/income statements for both methods, detailing sales revenue, cost of goods sold (COGS), and various expenses to determine net profit or loss. The solution also calculates the break-even point in sales volume, identifying the minimum number of units the company needs to sell to cover its fixed costs and avoid losses. Based on the analysis, the assignment offers management advice, emphasizing the importance of exceeding the break-even point to achieve profitability. The assignment provides a comprehensive overview of cost accounting principles and their application in financial analysis and decision-making.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.