Tech (UK) Limited: Analysis of Marginal and Absorption Costing Methods

VerifiedAdded on 2020/06/03

|4

|750

|355

Report

AI Summary

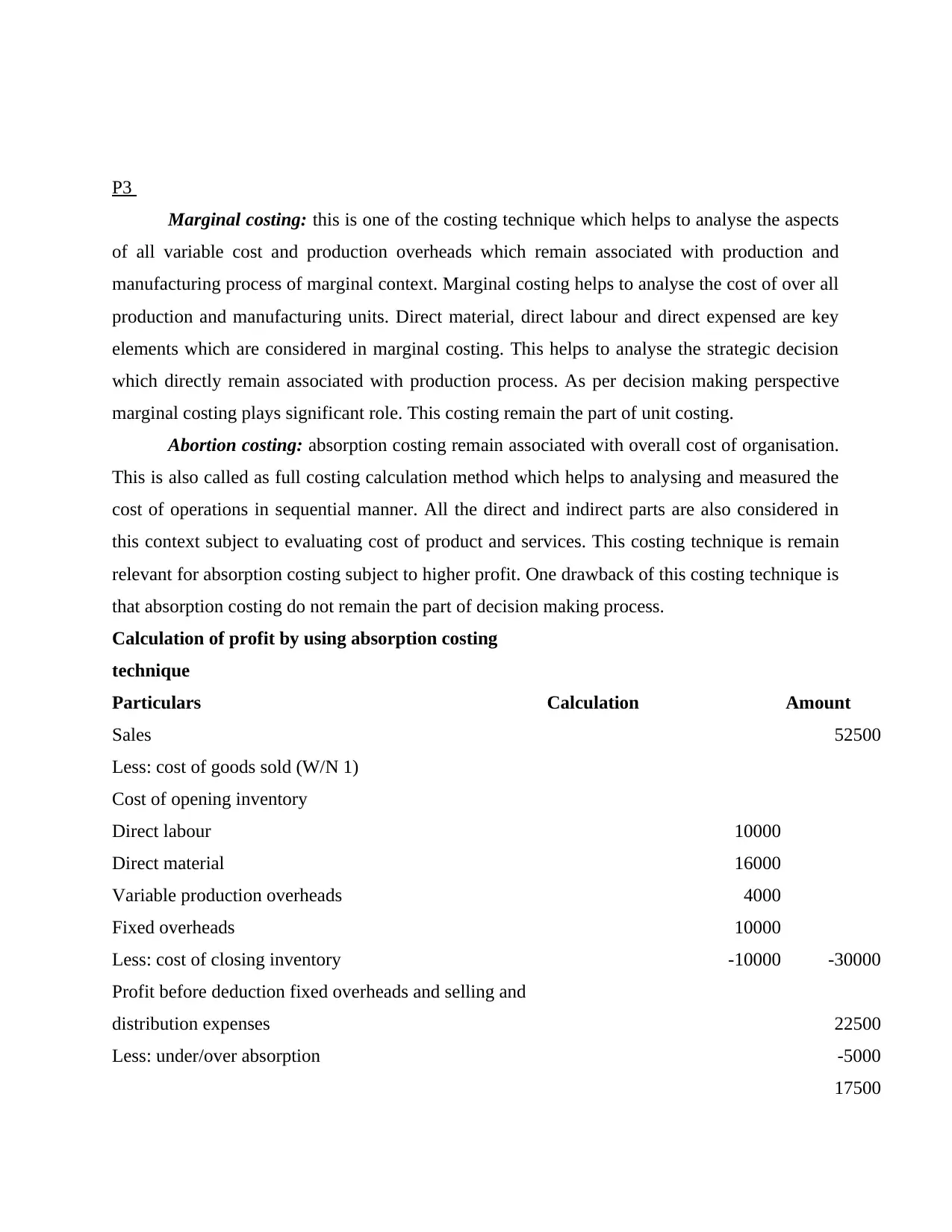

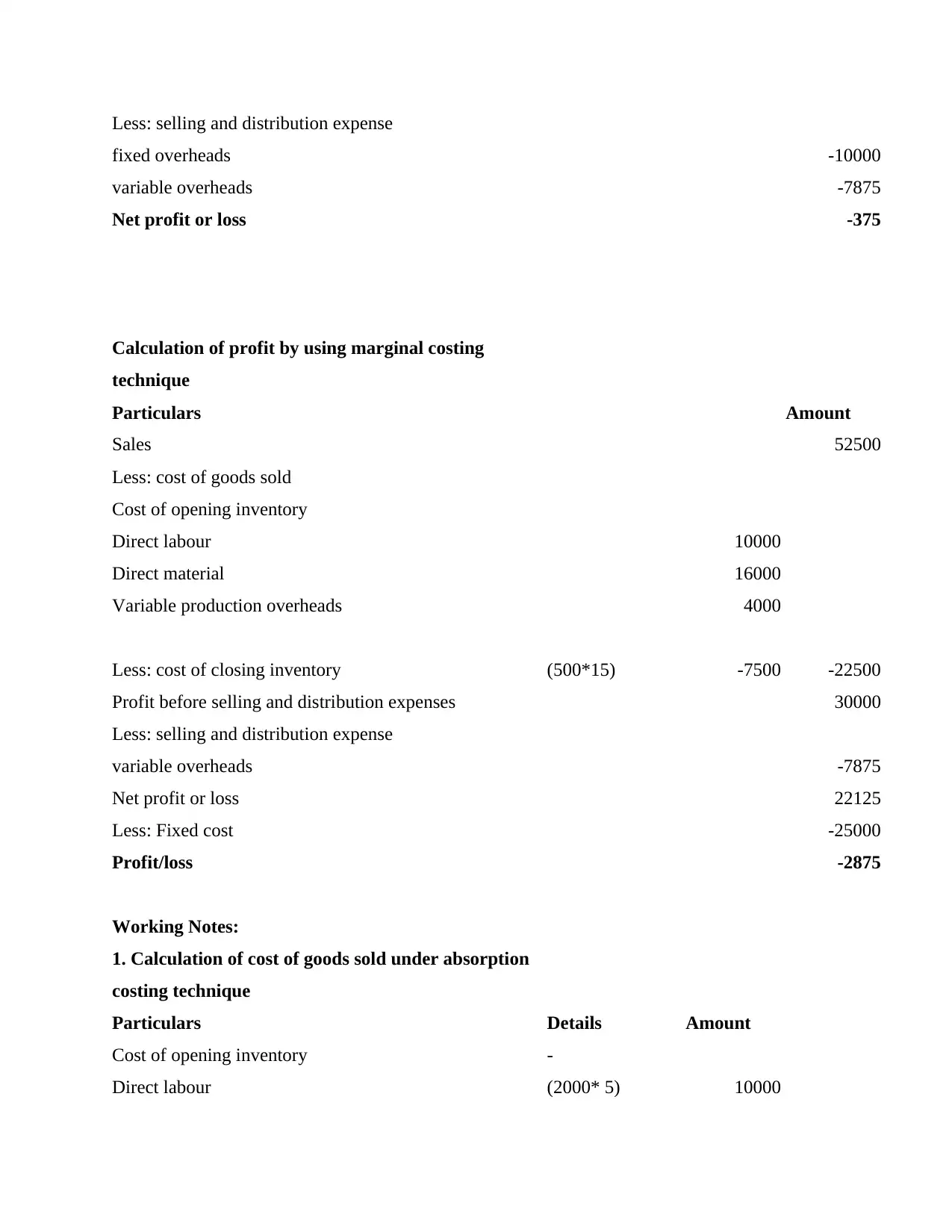

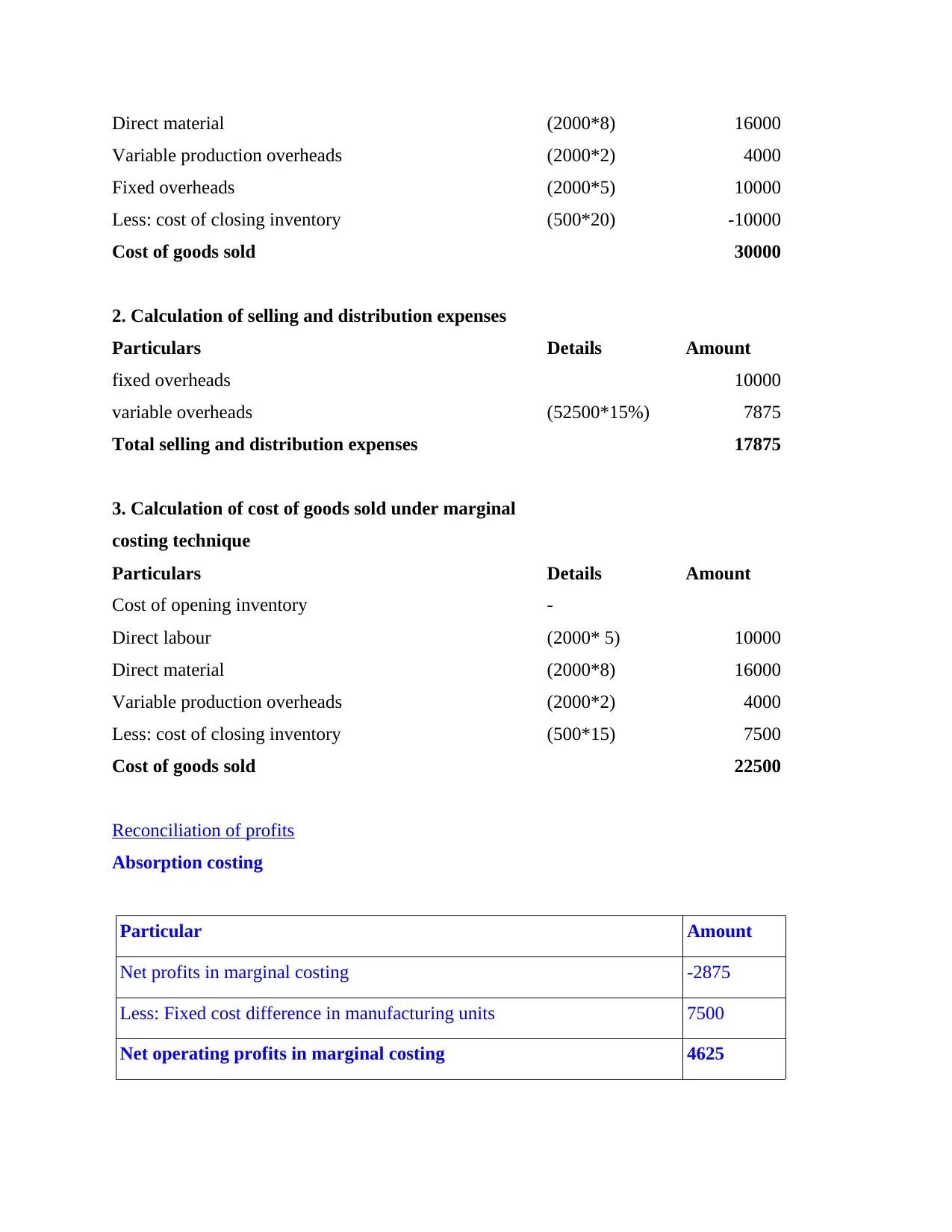

This report, prepared for Tech (UK) Limited, a company producing chargers, analyzes two key costing techniques: marginal costing and absorption costing. The assignment includes detailed calculations of profit and loss using both methods, considering direct materials, direct labor, variable production overheads, and fixed overheads. The report calculates the cost of goods sold and selling and distribution expenses under each costing method. A reconciliation statement is provided to highlight the differences in profit figures between the two approaches, demonstrating the impact of fixed costs on profit. The analysis provides insights into strategic decision-making and the role of costing techniques in management accounting. This report demonstrates the application of these techniques in a practical business context, allowing for the evaluation of operational performance.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.