MANAGEMENT ACCOUNTING INTRODUCTION 1 TASK 11 AC 1.1 Classification of different types of cost1 AC 1.2 Unit cost and total job cost for Exquisite using absorption costing 3 Method3

21 Pages6431 Words412 Views

Added on 2019-12-28

About This Document

Deduce overhead recovery rates for each production departments using machine hours 6 AC 1.4 Analyse cost data using appropriate techniques 7 TASK 28 AC 2.1 Preparation of cost report for Jeffrey and Son's Ltd for the month of September, determine variances with necessary comment 8 AC 2.2 Various performance indicators for potential improvements 10 AC 2.3 Way's to reduce cost, enhance value and quality10 TASK 311 AC 3.1 Purpose and nature of the budgeting process to the budget holders of Jeffery and Son’s Ltd.

MANAGEMENT ACCOUNTING INTRODUCTION 1 TASK 11 AC 1.1 Classification of different types of cost1 AC 1.2 Unit cost and total job cost for Exquisite using absorption costing 3 Method3

Added on 2019-12-28

ShareRelated Documents

MANAGEMENT

ACCOUNTING

1 | P a g e

ACCOUNTING

1 | P a g e

Table of Contents

INTRODUCTION .....................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Classification of different types of cost................................................................1

AC 1.2 Unit cost and total job cost for Job 444................................................................2

AC 1.3 Computation of total cost and per unit cost for Exquisite using absorption costing 3

Method..............................................................................................................................3

a. Allocate and apportion overheads to Jeffrey & Son's production units........................4

b. Reapportion the support department cost to the production units................................4

c. Deduce overhead recovery rates for each production departments using machine hours. 6

AC 1.4 Analyse cost data using appropriate techniques...................................................7

TASK 2......................................................................................................................................8

AC 2.1 Preparation of cost report for Jeffrey and Son's Ltd for the month of September,

determine variances with necessary comment..................................................................8

AC 2.2 Various performance indicators for potential improvements.............................10

AC 2.3 Way's to reduce cost, enhance value and quality ..............................................10

TASK 3....................................................................................................................................11

AC 3.1 Purpose and nature of the budgeting process to the budget holders of Jeffery and

Son’s Ltd.........................................................................................................................11

AC 3.2 Appropriate budgeting methods for Jeffrey and Son's Ltd. and its needs..........12

AC 3.3 Production and material purchase budget for Jeffrey & Son's Ltd....................13

AC 3.4 Preparation of cash budget of Jeffrey & Sons for the three months ending on..14

September.......................................................................................................................14

TASK 4....................................................................................................................................15

AC 4.1 Variance computation, its causes and take corrective actions to eliminate adverse

.........................................................................................................................................15

Variances.........................................................................................................................15

AC 4.2 Operating statement that reconcile budgeted and actual results ........................17

AC 4.3 Report to the responsibility centres....................................................................17

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................18

2 | P a g e

INTRODUCTION .....................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Classification of different types of cost................................................................1

AC 1.2 Unit cost and total job cost for Job 444................................................................2

AC 1.3 Computation of total cost and per unit cost for Exquisite using absorption costing 3

Method..............................................................................................................................3

a. Allocate and apportion overheads to Jeffrey & Son's production units........................4

b. Reapportion the support department cost to the production units................................4

c. Deduce overhead recovery rates for each production departments using machine hours. 6

AC 1.4 Analyse cost data using appropriate techniques...................................................7

TASK 2......................................................................................................................................8

AC 2.1 Preparation of cost report for Jeffrey and Son's Ltd for the month of September,

determine variances with necessary comment..................................................................8

AC 2.2 Various performance indicators for potential improvements.............................10

AC 2.3 Way's to reduce cost, enhance value and quality ..............................................10

TASK 3....................................................................................................................................11

AC 3.1 Purpose and nature of the budgeting process to the budget holders of Jeffery and

Son’s Ltd.........................................................................................................................11

AC 3.2 Appropriate budgeting methods for Jeffrey and Son's Ltd. and its needs..........12

AC 3.3 Production and material purchase budget for Jeffrey & Son's Ltd....................13

AC 3.4 Preparation of cash budget of Jeffrey & Sons for the three months ending on..14

September.......................................................................................................................14

TASK 4....................................................................................................................................15

AC 4.1 Variance computation, its causes and take corrective actions to eliminate adverse

.........................................................................................................................................15

Variances.........................................................................................................................15

AC 4.2 Operating statement that reconcile budgeted and actual results ........................17

AC 4.3 Report to the responsibility centres....................................................................17

CONCLUSION........................................................................................................................18

REFERENCES.........................................................................................................................18

2 | P a g e

INTRODUCTION

In the present competitive age, management accounting plays a crucial role as it helps

to examine and evaluate financial performance and take effective decisions. Jeffrey & Son's

Ltd is a manufacturing organization who produces variety of popular products called,

Exquisite. Present report will helps to discuss the role and its importance of management

accounting in the success of the company. The report will explain different costing methods

to determine accurate product cost and take pricing decisions accordingly. Moreover, under

the budgetary analysis, project report will describe various kind of budgets for variance

detections and eliminate it through taking necessary corrective actions. Along with this,

various performance indicators will be explain through which performance can be improved.

Furthermore, different ways will be suggested to reduce cost, enhance value and quality.

TASK 1

AC 1.1 Classification of different types of cost

Cost is the value or price of something which is needed to pay for acquiring goods

and services. It can be classified into various groups according to the nature and purpose.

These are stated as follows:

Classification on the basis of nature: According to nature of elements, costs are classified

into direct and indirect cost in terms of materials, labour and expenses. Material cost is

further classified into direct and indirect material cost. In Jeffrey and Son’s Ltd, direct

material cost includes cost of consumption of direct materials like raw materials, taxes and

duties. Indirect materials are those small values which cannot be directly allocated to a cost

centres for example; lubricants and spare parts of machinery (Robinson, 2008).

Direct labour cost is the amount incurred on salary packages or wages provided to

workers by the staff of Jeffrey and Son’s Ltd which includes fringe benefits such as

incentives, PPFs and gratuity. On the other hand, indirect labour costs consists of cost of

daily wages payable to workers which are not directly allocable to the office or industry of

the organisation like security guards or accountants.

Direct Expenses are royalties, hiring charges for tools &equipment’s and job

processing charges other than direct material and labour cost. Indirect expenses are expenses

which cannot be directly allocated to cost centres of Jeffrey and Son’s Ltd.

3 | P a g e

In the present competitive age, management accounting plays a crucial role as it helps

to examine and evaluate financial performance and take effective decisions. Jeffrey & Son's

Ltd is a manufacturing organization who produces variety of popular products called,

Exquisite. Present report will helps to discuss the role and its importance of management

accounting in the success of the company. The report will explain different costing methods

to determine accurate product cost and take pricing decisions accordingly. Moreover, under

the budgetary analysis, project report will describe various kind of budgets for variance

detections and eliminate it through taking necessary corrective actions. Along with this,

various performance indicators will be explain through which performance can be improved.

Furthermore, different ways will be suggested to reduce cost, enhance value and quality.

TASK 1

AC 1.1 Classification of different types of cost

Cost is the value or price of something which is needed to pay for acquiring goods

and services. It can be classified into various groups according to the nature and purpose.

These are stated as follows:

Classification on the basis of nature: According to nature of elements, costs are classified

into direct and indirect cost in terms of materials, labour and expenses. Material cost is

further classified into direct and indirect material cost. In Jeffrey and Son’s Ltd, direct

material cost includes cost of consumption of direct materials like raw materials, taxes and

duties. Indirect materials are those small values which cannot be directly allocated to a cost

centres for example; lubricants and spare parts of machinery (Robinson, 2008).

Direct labour cost is the amount incurred on salary packages or wages provided to

workers by the staff of Jeffrey and Son’s Ltd which includes fringe benefits such as

incentives, PPFs and gratuity. On the other hand, indirect labour costs consists of cost of

daily wages payable to workers which are not directly allocable to the office or industry of

the organisation like security guards or accountants.

Direct Expenses are royalties, hiring charges for tools &equipment’s and job

processing charges other than direct material and labour cost. Indirect expenses are expenses

which cannot be directly allocated to cost centres of Jeffrey and Son’s Ltd.

3 | P a g e

Classification on the basis of Elements of Product: By nature of elements of a product, cost

can be classified into direct material, direct labour, and factory overheads. This classification

provides information regarding income measurement and product pricing:

Material: This cost consists of cost of procurement of inventories, taxes freight

inwards, trade discounts, sales tax and all other cost of material required for the

production of product or services (Vaidya, 2008).

Labour: This cost includes payment made to employees in the form of salary

packages or wages. Labour cost is either directly or indirectly involved in the

production process. Here, salary packages consist of all benefits and compensations

provided to employees of Jeffrey and Son’s Ltd. like bonuses, leave encashment,

PPFs etc. Manufacturing Overheads: It is inclusive of all manufacturing costs other than labour

and material cost. Examples of factory overheads costs are like expenditures on

account utilities, account supervisors, factory facilities charges and rental payments

etc.

Classification on the basis on functions and activities: Cost can be classified on the basis of

various functions and activities performed like: Production, Administration, Selling and

Distribution, Finance, Quality Check and Research and Development (R&D) etc.

Classification on the basis of behaviour: The behaviour of cost is predicted with respect to

responses to change in activities or volume. Further, the costs are classified into fixed,

Variable and Semi-variable costs. These costs do not vary with the change in activities, total

fixed cost remain constant irrespective of change in output. For example; salaries, rental

payments and insurance etc are inclusive in this. In variable cost, total costs changes with

respect to change in volume activities (Lal and Srivastava, 2013). Variable costs are under the

control of head department of Jeffrey and Son’s Ltd. All the implications and planning of

variable costs are done by management department of the company. It includes sales

commissions, packaging, freights, direct labour and materials. Semi variable costs consist of

both fixed and variable cost. Fixed part of the same represents the minimal fee charged for

setting up of any service and use of that service charges variable cost for example; telephone

services (Needles, 2010.).

AC 1.2 Unit cost and total job cost for Job 444

Job costing is a order specific costing that accumulates all the incurred

production expenditures for the specified job (Horngren, 2009). Every job contains a

4 | P a g e

can be classified into direct material, direct labour, and factory overheads. This classification

provides information regarding income measurement and product pricing:

Material: This cost consists of cost of procurement of inventories, taxes freight

inwards, trade discounts, sales tax and all other cost of material required for the

production of product or services (Vaidya, 2008).

Labour: This cost includes payment made to employees in the form of salary

packages or wages. Labour cost is either directly or indirectly involved in the

production process. Here, salary packages consist of all benefits and compensations

provided to employees of Jeffrey and Son’s Ltd. like bonuses, leave encashment,

PPFs etc. Manufacturing Overheads: It is inclusive of all manufacturing costs other than labour

and material cost. Examples of factory overheads costs are like expenditures on

account utilities, account supervisors, factory facilities charges and rental payments

etc.

Classification on the basis on functions and activities: Cost can be classified on the basis of

various functions and activities performed like: Production, Administration, Selling and

Distribution, Finance, Quality Check and Research and Development (R&D) etc.

Classification on the basis of behaviour: The behaviour of cost is predicted with respect to

responses to change in activities or volume. Further, the costs are classified into fixed,

Variable and Semi-variable costs. These costs do not vary with the change in activities, total

fixed cost remain constant irrespective of change in output. For example; salaries, rental

payments and insurance etc are inclusive in this. In variable cost, total costs changes with

respect to change in volume activities (Lal and Srivastava, 2013). Variable costs are under the

control of head department of Jeffrey and Son’s Ltd. All the implications and planning of

variable costs are done by management department of the company. It includes sales

commissions, packaging, freights, direct labour and materials. Semi variable costs consist of

both fixed and variable cost. Fixed part of the same represents the minimal fee charged for

setting up of any service and use of that service charges variable cost for example; telephone

services (Needles, 2010.).

AC 1.2 Unit cost and total job cost for Job 444

Job costing is a order specific costing that accumulates all the incurred

production expenditures for the specified job (Horngren, 2009). Every job contains a

4 | P a g e

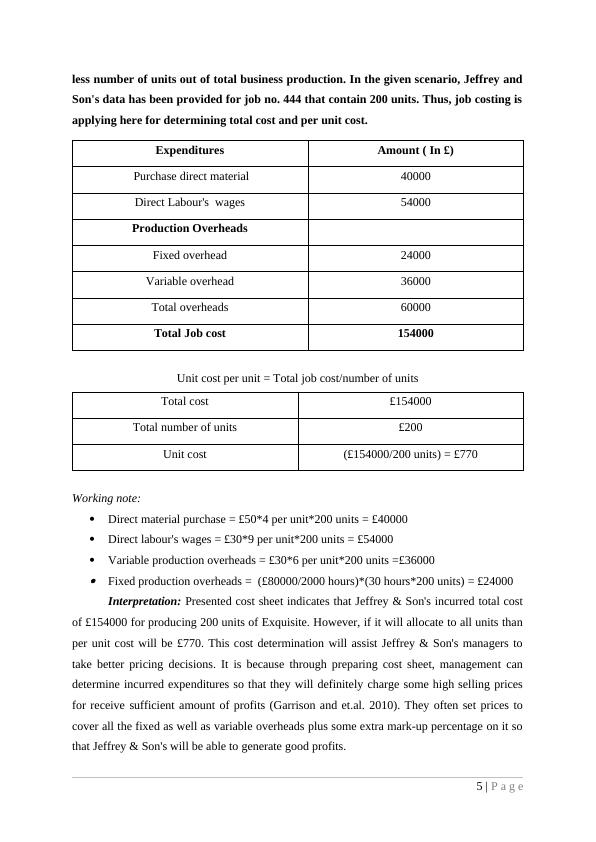

less number of units out of total business production. In the given scenario, Jeffrey and

Son's data has been provided for job no. 444 that contain 200 units. Thus, job costing is

applying here for determining total cost and per unit cost.

Expenditures Amount ( In £)

Purchase direct material 40000

Direct Labour's wages 54000

Production Overheads

Fixed overhead 24000

Variable overhead 36000

Total overheads 60000

Total Job cost 154000

Unit cost per unit = Total job cost/number of units

Total cost £154000

Total number of units £200

Unit cost (£154000/200 units) = £770

Working note:

Direct material purchase = £50*4 per unit*200 units = £40000

Direct labour's wages = £30*9 per unit*200 units = £54000

Variable production overheads = £30*6 per unit*200 units =£36000 Fixed production overheads = (£80000/2000 hours)*(30 hours*200 units) = £24000

Interpretation: Presented cost sheet indicates that Jeffrey & Son's incurred total cost

of £154000 for producing 200 units of Exquisite. However, if it will allocate to all units than

per unit cost will be £770. This cost determination will assist Jeffrey & Son's managers to

take better pricing decisions. It is because through preparing cost sheet, management can

determine incurred expenditures so that they will definitely charge some high selling prices

for receive sufficient amount of profits (Garrison and et.al. 2010). They often set prices to

cover all the fixed as well as variable overheads plus some extra mark-up percentage on it so

that Jeffrey & Son's will be able to generate good profits.

5 | P a g e

Son's data has been provided for job no. 444 that contain 200 units. Thus, job costing is

applying here for determining total cost and per unit cost.

Expenditures Amount ( In £)

Purchase direct material 40000

Direct Labour's wages 54000

Production Overheads

Fixed overhead 24000

Variable overhead 36000

Total overheads 60000

Total Job cost 154000

Unit cost per unit = Total job cost/number of units

Total cost £154000

Total number of units £200

Unit cost (£154000/200 units) = £770

Working note:

Direct material purchase = £50*4 per unit*200 units = £40000

Direct labour's wages = £30*9 per unit*200 units = £54000

Variable production overheads = £30*6 per unit*200 units =£36000 Fixed production overheads = (£80000/2000 hours)*(30 hours*200 units) = £24000

Interpretation: Presented cost sheet indicates that Jeffrey & Son's incurred total cost

of £154000 for producing 200 units of Exquisite. However, if it will allocate to all units than

per unit cost will be £770. This cost determination will assist Jeffrey & Son's managers to

take better pricing decisions. It is because through preparing cost sheet, management can

determine incurred expenditures so that they will definitely charge some high selling prices

for receive sufficient amount of profits (Garrison and et.al. 2010). They often set prices to

cover all the fixed as well as variable overheads plus some extra mark-up percentage on it so

that Jeffrey & Son's will be able to generate good profits.

5 | P a g e

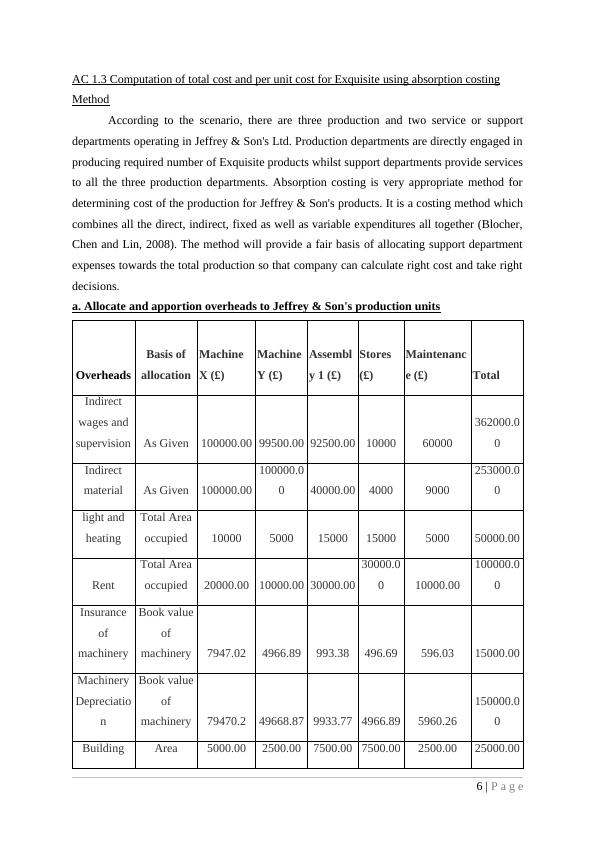

AC 1.3 Computation of total cost and per unit cost for Exquisite using absorption costing

Method

According to the scenario, there are three production and two service or support

departments operating in Jeffrey & Son's Ltd. Production departments are directly engaged in

producing required number of Exquisite products whilst support departments provide services

to all the three production departments. Absorption costing is very appropriate method for

determining cost of the production for Jeffrey & Son's products. It is a costing method which

combines all the direct, indirect, fixed as well as variable expenditures all together (Blocher,

Chen and Lin, 2008). The method will provide a fair basis of allocating support department

expenses towards the total production so that company can calculate right cost and take right

decisions.

a. Allocate and apportion overheads to Jeffrey & Son's production units

Overheads

Basis of

allocation

Machine

X (£)

Machine

Y (£)

Assembl

y 1 (£)

Stores

(£)

Maintenanc

e (£) Total

Indirect

wages and

supervision As Given 100000.00 99500.00 92500.00 10000 60000

362000.0

0

Indirect

material As Given 100000.00

100000.0

0 40000.00 4000 9000

253000.0

0

light and

heating

Total Area

occupied 10000 5000 15000 15000 5000 50000.00

Rent

Total Area

occupied 20000.00 10000.00 30000.00

30000.0

0 10000.00

100000.0

0

Insurance

of

machinery

Book value

of

machinery 7947.02 4966.89 993.38 496.69 596.03 15000.00

Machinery

Depreciatio

n

Book value

of

machinery 79470.2 49668.87 9933.77 4966.89 5960.26

150000.0

0

Building Area 5000.00 2500.00 7500.00 7500.00 2500.00 25000.00

6 | P a g e

Method

According to the scenario, there are three production and two service or support

departments operating in Jeffrey & Son's Ltd. Production departments are directly engaged in

producing required number of Exquisite products whilst support departments provide services

to all the three production departments. Absorption costing is very appropriate method for

determining cost of the production for Jeffrey & Son's products. It is a costing method which

combines all the direct, indirect, fixed as well as variable expenditures all together (Blocher,

Chen and Lin, 2008). The method will provide a fair basis of allocating support department

expenses towards the total production so that company can calculate right cost and take right

decisions.

a. Allocate and apportion overheads to Jeffrey & Son's production units

Overheads

Basis of

allocation

Machine

X (£)

Machine

Y (£)

Assembl

y 1 (£)

Stores

(£)

Maintenanc

e (£) Total

Indirect

wages and

supervision As Given 100000.00 99500.00 92500.00 10000 60000

362000.0

0

Indirect

material As Given 100000.00

100000.0

0 40000.00 4000 9000

253000.0

0

light and

heating

Total Area

occupied 10000 5000 15000 15000 5000 50000.00

Rent

Total Area

occupied 20000.00 10000.00 30000.00

30000.0

0 10000.00

100000.0

0

Insurance

of

machinery

Book value

of

machinery 7947.02 4966.89 993.38 496.69 596.03 15000.00

Machinery

Depreciatio

n

Book value

of

machinery 79470.2 49668.87 9933.77 4966.89 5960.26

150000.0

0

Building Area 5000.00 2500.00 7500.00 7500.00 2500.00 25000.00

6 | P a g e

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Costing & Budgeting Assignmentlg...

|21

|5977

|134

Significance of Management Accounting : Reportlg...

|19

|5698

|198

Task 14 Task 14 - Cost classification and analysis of cost report of September month10lg...

|20

|4735

|64

Report On Jeffrey & Son's Ltd | Evaluation Of Cost Conceptslg...

|25

|6772

|43

Case Study of Jeffrey and Son's | Reportlg...

|23

|5849

|40

(Doc) Management Accounting Reportlg...

|18

|5348

|67