Significance of Management Accounting : Report

19 Pages5698 Words198 Views

Added on 2020-01-15

Significance of Management Accounting : Report

Added on 2020-01-15

ShareRelated Documents

MANAGEMENTACCOUNTING

Table of ContentsINTRODUCTION......................................................................................................................1TASK 1......................................................................................................................................1AC 1.1 Cost classification based on element, function, nature and behaviour.................1AC 1.2 Computation of total and unit cost for Job no. 444 through using job costingmethod...............................................................................................................................2AC 1.3 Determination of cost of Exquisite through using job costing method................3AC 1.4 Computation of cost through using direct labour hours for overhead absorption5TASK 2......................................................................................................................................6AC 2.1 Preparation and analysis of cost report and comment on respective variances....6AC 2.2 Performance indicators to determine potential improvement areas.....................7AC 2.3 Suggestive ways to reduce cost, enhance value and quality................................8TASK 3......................................................................................................................................9AC 3.1 Purpose and nature of budgeting process to Jeffrey & Son's budget holders......9AC 3.2 Appropriate budgeting method for Jeffrey & Son's.............................................9AC 3.3 Preparation of production and material purchase budget.....................................9AC 3.4 Preparation of Jeffrey & Son's cash budget.........................................................9TASK 4......................................................................................................................................9AC 4.1 Detecting variances, its causes and recommend corrective actions.....................9AC 4.2 Preparation of operating statement through reconciling budgeted and actual results...........................................................................................................................................9AC 4.3 Report of findings to responsibility centres.........................................................9CONCLUSION..........................................................................................................................9REFERENCES...........................................................................................................................9

INTRODUCTIONManagers play a crucial role in the business success as they analyse company'sfinancial performance and take strategic decisions. Management accounting is the process ofpreparing managerial reports from financial information, taking effective decisions, ensureoptimum allocation of resources, and manage firm’s operational and financial risk. Jeffrey &Son's is a manufacturing organization which produces variety of popular and brandedproducts, called Exquisite. In present project report, various kinds of managerial tools will bediscussed for improving company's performance. The report will describe the significance ofmanagement accounting for cost computation, effective cost management, preparing costreport, variance analysis and taking corrective actions to eliminate adverse variances.Moreover, various budgeting techniques will be explained to manage firms operations. TASK 1AC 1.1 Cost classification based on element, function, nature and behaviourCost elements: Jeffrey & Son's has three types of cost elements that are material,labour and overhead. Quantity and amount of raw material which have been used inproduction process to convert it into finished goods is known as material cost such as cost ofpurchasing raw material. However, wages paid by Jeffrey & Son's to their employees iscalled labour cost (Weygandt, Kimmel and Kieso, 2015). All the other expenses are known asoverheads such as telephone, office rent, building depreciation, royalty and cost of scrap. Cost function: On that basis, cost can be classified into various types such asadministration, factory and selling and distribution overheads. In context to Jeffrey & Son's,office rent, stationery, printing and photocopier charges are the types of administrative cost.However, factory rent, lighting and energy will be included in factory cost while all theexpenses which have been incurred for selling Exquisite product into the market is known asselling and distribution overheads (Gibson and Haynes, 2015). For instance, advertisement,marketing and cost of distributing free samples. Cost nature: There are two types of cost nature, direct and indirect. Direct cost can bespecifically charged to a specific cost element and cost centre. On contrary, indirect costcannot be charged to a specific cost centre or elements. Direct material can be charged to anspecific cost centre and integral part of Exquisite whilst indirect material cost cannot bedirectly charged to an individual cost centres (Ward, 2012). For instance, cost of consumablestores, oil and lubricants are known as indirect material cost. Direct labour can be directlycharged to an individual cost centre and paid to the employees who are involve in Jeffrey &1 | P a g e

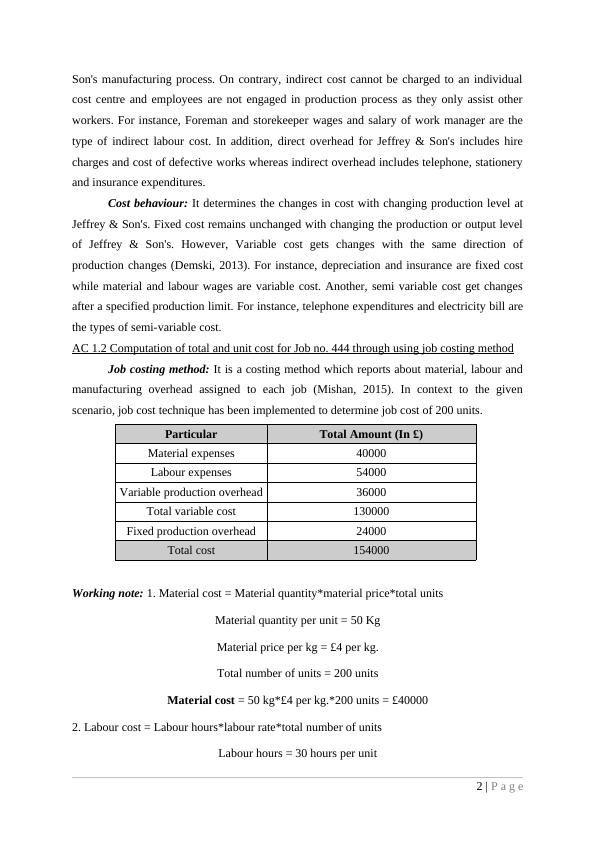

Son's manufacturing process. On contrary, indirect cost cannot be charged to an individualcost centre and employees are not engaged in production process as they only assist otherworkers. For instance, Foreman and storekeeper wages and salary of work manager are thetype of indirect labour cost. In addition, direct overhead for Jeffrey & Son's includes hirecharges and cost of defective works whereas indirect overhead includes telephone, stationeryand insurance expenditures. Cost behaviour: It determines the changes in cost with changing production level atJeffrey & Son's. Fixed cost remains unchanged with changing the production or output levelof Jeffrey & Son's. However, Variable cost gets changes with the same direction ofproduction changes (Demski, 2013). For instance, depreciation and insurance are fixed costwhile material and labour wages are variable cost. Another, semi variable cost get changesafter a specified production limit. For instance, telephone expenditures and electricity bill arethe types of semi-variable cost.AC 1.2 Computation of total and unit cost for Job no. 444 through using job costing methodJob costing method: It is a costing method which reports about material, labour andmanufacturing overhead assigned to each job (Mishan, 2015). In context to the givenscenario, job cost technique has been implemented to determine job cost of 200 units. ParticularTotal Amount (In £)Material expenses40000Labour expenses54000Variable production overhead36000Total variable cost130000Fixed production overhead24000Total cost154000Working note: 1. Material cost = Material quantity*material price*total unitsMaterial quantity per unit = 50 KgMaterial price per kg = £4 per kg.Total number of units = 200 units Material cost = 50 kg*£4 per kg.*200 units = £400002. Labour cost = Labour hours*labour rate*total number of unitsLabour hours = 30 hours per unit2 | P a g e

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting - Jeffrey & Son'slg...

|18

|5067

|40

Management Accounting Costing & Budgeting Assignmentlg...

|21

|5977

|134

The Roles and Responsibilities of Management Accountinglg...

|17

|5403

|31

Role of Management Accountinglg...

|20

|5348

|89

MANAGEMENT ACCOUNTING INTRODUCTION 1 TASK 11 AC 1.1 Classification of different types of cost1 AC 1.2 Unit cost and total job cost for Exquisite using absorption costing 3 Method3lg...

|21

|6431

|412

Management Accounting Costing and Budgeting - Reportlg...

|23

|5749

|171