Management Accounting Techniques for Responding to Financial Issues

VerifiedAdded on 2023/01/12

|13

|3081

|86

Report

AI Summary

This report provides a comprehensive overview of management accounting techniques and their application in addressing financial problems within organizations. It covers various cost analysis methods, including marginal and absorption costing, to prepare income statements and analyze profitability. The report also explores different planning tools such as budgeting and cost-volume-profit analysis, highlighting their advantages and disadvantages in budgetary control and financial forecasting. Furthermore, it examines how organizations adapt management accounting systems to respond to financial challenges and achieve sustainable success. Financial reporting documents like balance sheets, income statements, and cash flow statements are discussed in the context of management accounting, emphasizing their role in informed decision-making. The document concludes by underscoring the importance of management accounting in strategic financial planning and problem-solving, with Desklib offering additional resources like past papers and solved assignments for further study.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

L.O.2: Apply a range of management accounting techniques.........................................................3

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................3

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents.........................................................................................................8

L.O.3: Explain the use of planning tools used in management accounting using budgets for

planning and control........................................................................................................................9

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................9

M3. Use of different planning tools and their application for preparing and forecasting budgets10

L.O.4: Compare ways in which organizations could use management accounting to respond to

financial problems.........................................................................................................................11

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................11

M4. Analyze how in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

L.O.2: Apply a range of management accounting techniques.........................................................3

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs...........................................................................3

M2. Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents.........................................................................................................8

L.O.3: Explain the use of planning tools used in management accounting using budgets for

planning and control........................................................................................................................9

P4. Explain the advantages and disadvantages of different types of planning tools used for

budgetary control.........................................................................................................................9

M3. Use of different planning tools and their application for preparing and forecasting budgets10

L.O.4: Compare ways in which organizations could use management accounting to respond to

financial problems.........................................................................................................................11

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems.....................................................................................................................11

M4. Analyze how in responding to financial problems, management accounting can lead

organizations to sustainable success..........................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

For the internal purpose of the company - hence the name. Facts and figures are confidential o

management team and other decision-making individuals. There is not a set pattern or format or

reporting. Statistics are communicated according to the target audience, and therefore may or

may not include information as per their requirement. Reports can include both financial and

non-financial data as required. No formal audit structure is required for such reporting. Reporting

is done more than a year since information is used to improve decisions made for forecasting

schemes. In this project report management accounting techniques with advantages and

disadvantages of each has discussed. How management accounting methods can solve financial

problems of the company with effective tools and attain sustainable success for the company.

L.O.2: Apply a range of management accounting techniques

P3. Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costs

Cost: During the production of any item, the total amount spent on it is called cost. There are

many prices like expenditure on raw materials, expenses on running the machine, salary of

employees, etc. The sum that is combined with all these expenses is called the cost of production

(Quinn and Oliveira, 2018).

Different costs and cost analysis:

Based on production; costs are of two types; direct and indirect. Where direct costs directly

associated with production process; while indirect costs are not directly associated with

production process. On the basis of occurrence two further types of costs; variable and fixed

costs calculated to identify standard cost of the product. Cost can be identified through two

methods discussed below:

Marginal costing: Marginal cost includes costs that vary with the level of production, while

other costs that do not vary with production are considered fixed. For example, the direct cost of

producing an automobile usually includes the cost of labor and parts required for the additional

automobile.

For the internal purpose of the company - hence the name. Facts and figures are confidential o

management team and other decision-making individuals. There is not a set pattern or format or

reporting. Statistics are communicated according to the target audience, and therefore may or

may not include information as per their requirement. Reports can include both financial and

non-financial data as required. No formal audit structure is required for such reporting. Reporting

is done more than a year since information is used to improve decisions made for forecasting

schemes. In this project report management accounting techniques with advantages and

disadvantages of each has discussed. How management accounting methods can solve financial

problems of the company with effective tools and attain sustainable success for the company.

L.O.2: Apply a range of management accounting techniques

P3. Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costs

Cost: During the production of any item, the total amount spent on it is called cost. There are

many prices like expenditure on raw materials, expenses on running the machine, salary of

employees, etc. The sum that is combined with all these expenses is called the cost of production

(Quinn and Oliveira, 2018).

Different costs and cost analysis:

Based on production; costs are of two types; direct and indirect. Where direct costs directly

associated with production process; while indirect costs are not directly associated with

production process. On the basis of occurrence two further types of costs; variable and fixed

costs calculated to identify standard cost of the product. Cost can be identified through two

methods discussed below:

Marginal costing: Marginal cost includes costs that vary with the level of production, while

other costs that do not vary with production are considered fixed. For example, the direct cost of

producing an automobile usually includes the cost of labor and parts required for the additional

automobile.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

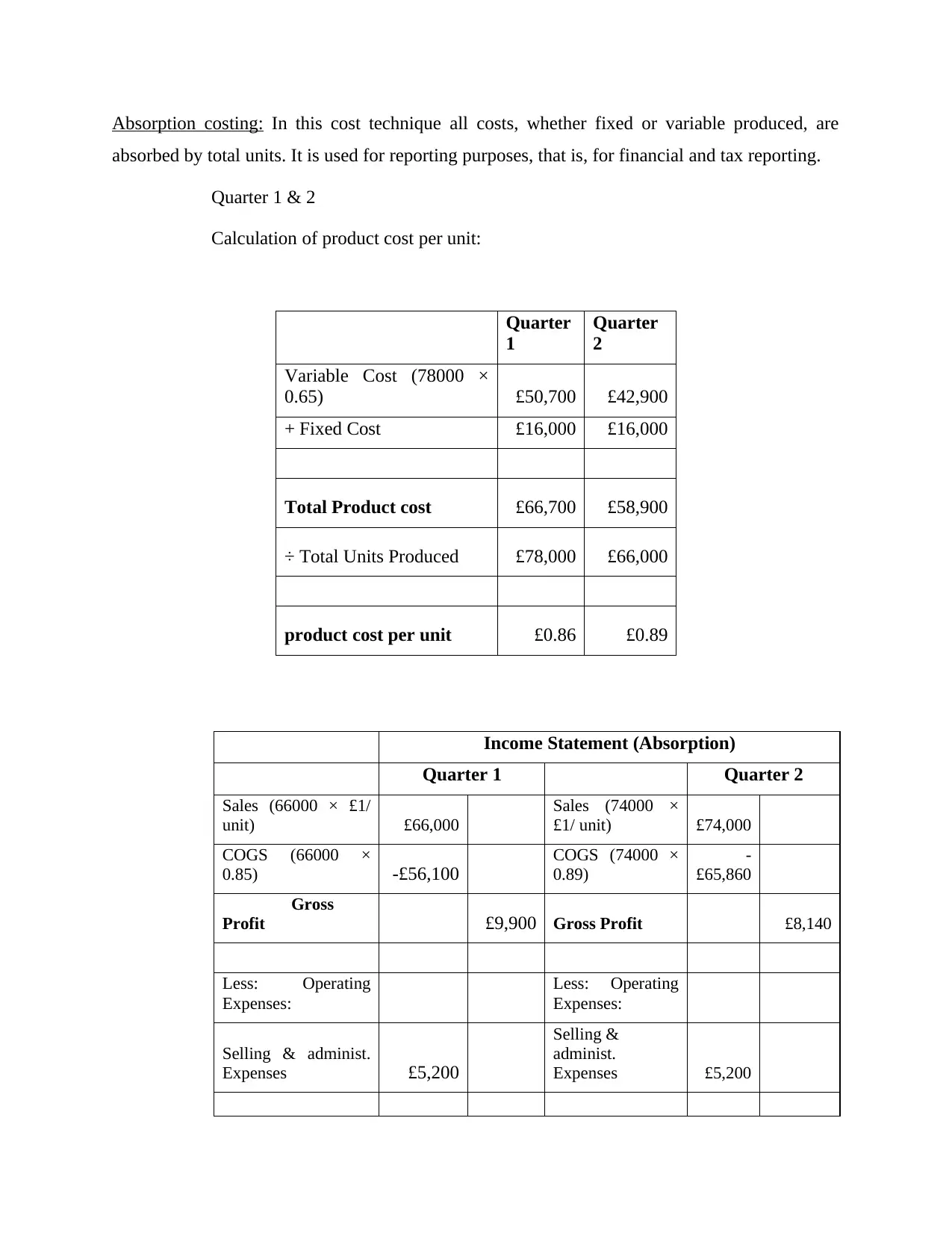

Absorption costing: In this cost technique all costs, whether fixed or variable produced, are

absorbed by total units. It is used for reporting purposes, that is, for financial and tax reporting.

Quarter 1 & 2

Calculation of product cost per unit:

Quarter

1

Quarter

2

Variable Cost (78000 ×

0.65) £50,700 £42,900

+ Fixed Cost £16,000 £16,000

Total Product cost £66,700 £58,900

÷ Total Units Produced £78,000 £66,000

product cost per unit £0.86 £0.89

Income Statement (Absorption)

Quarter 1 Quarter 2

Sales (66000 × £1/

unit) £66,000

Sales (74000 ×

£1/ unit) £74,000

COGS (66000 ×

0.85) -£56,100

COGS (74000 ×

0.89)

-

£65,860

Gross

Profit £9,900 Gross Profit £8,140

Less: Operating

Expenses:

Less: Operating

Expenses:

Selling & administ.

Expenses £5,200

Selling &

administ.

Expenses £5,200

absorbed by total units. It is used for reporting purposes, that is, for financial and tax reporting.

Quarter 1 & 2

Calculation of product cost per unit:

Quarter

1

Quarter

2

Variable Cost (78000 ×

0.65) £50,700 £42,900

+ Fixed Cost £16,000 £16,000

Total Product cost £66,700 £58,900

÷ Total Units Produced £78,000 £66,000

product cost per unit £0.86 £0.89

Income Statement (Absorption)

Quarter 1 Quarter 2

Sales (66000 × £1/

unit) £66,000

Sales (74000 ×

£1/ unit) £74,000

COGS (66000 ×

0.85) -£56,100

COGS (74000 ×

0.89)

-

£65,860

Gross

Profit £9,900 Gross Profit £8,140

Less: Operating

Expenses:

Less: Operating

Expenses:

Selling & administ.

Expenses £5,200

Selling &

administ.

Expenses £5,200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

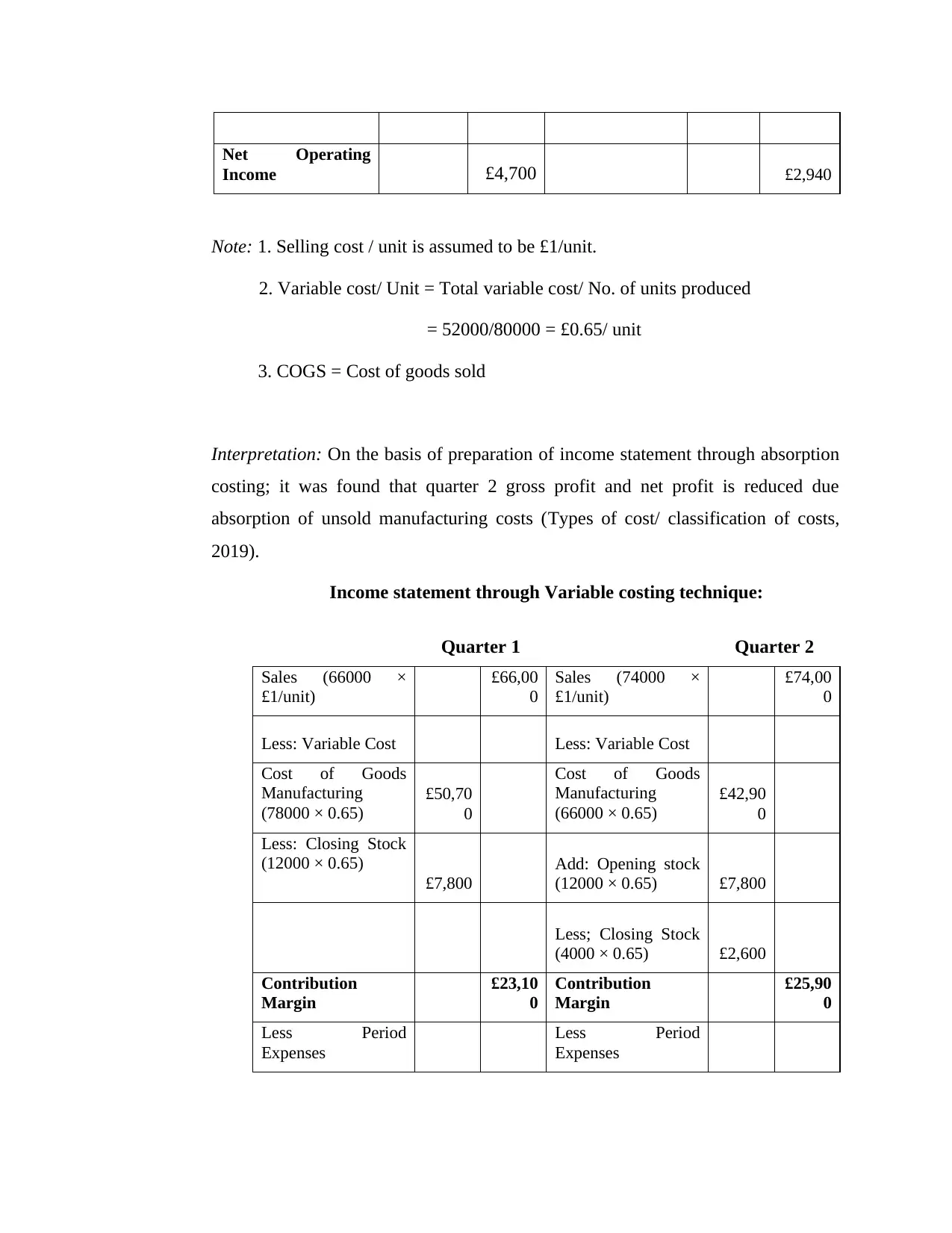

Net Operating

Income £4,700 £2,940

Note: 1. Selling cost / unit is assumed to be £1/unit.

2. Variable cost/ Unit = Total variable cost/ No. of units produced

= 52000/80000 = £0.65/ unit

3. COGS = Cost of goods sold

Interpretation: On the basis of preparation of income statement through absorption

costing; it was found that quarter 2 gross profit and net profit is reduced due

absorption of unsold manufacturing costs (Types of cost/ classification of costs,

2019).

Income statement through Variable costing technique:

Quarter 1 Quarter 2

Sales (66000 ×

£1/unit)

£66,00

0

Sales (74000 ×

£1/unit)

£74,00

0

Less: Variable Cost Less: Variable Cost

Cost of Goods

Manufacturing

(78000 × 0.65)

£50,70

0

Cost of Goods

Manufacturing

(66000 × 0.65)

£42,90

0

Less: Closing Stock

(12000 × 0.65)

£7,800

Add: Opening stock

(12000 × 0.65) £7,800

Less; Closing Stock

(4000 × 0.65) £2,600

Contribution

Margin

£23,10

0

Contribution

Margin

£25,90

0

Less Period

Expenses

Less Period

Expenses

Income £4,700 £2,940

Note: 1. Selling cost / unit is assumed to be £1/unit.

2. Variable cost/ Unit = Total variable cost/ No. of units produced

= 52000/80000 = £0.65/ unit

3. COGS = Cost of goods sold

Interpretation: On the basis of preparation of income statement through absorption

costing; it was found that quarter 2 gross profit and net profit is reduced due

absorption of unsold manufacturing costs (Types of cost/ classification of costs,

2019).

Income statement through Variable costing technique:

Quarter 1 Quarter 2

Sales (66000 ×

£1/unit)

£66,00

0

Sales (74000 ×

£1/unit)

£74,00

0

Less: Variable Cost Less: Variable Cost

Cost of Goods

Manufacturing

(78000 × 0.65)

£50,70

0

Cost of Goods

Manufacturing

(66000 × 0.65)

£42,90

0

Less: Closing Stock

(12000 × 0.65)

£7,800

Add: Opening stock

(12000 × 0.65) £7,800

Less; Closing Stock

(4000 × 0.65) £2,600

Contribution

Margin

£23,10

0

Contribution

Margin

£25,90

0

Less Period

Expenses

Less Period

Expenses

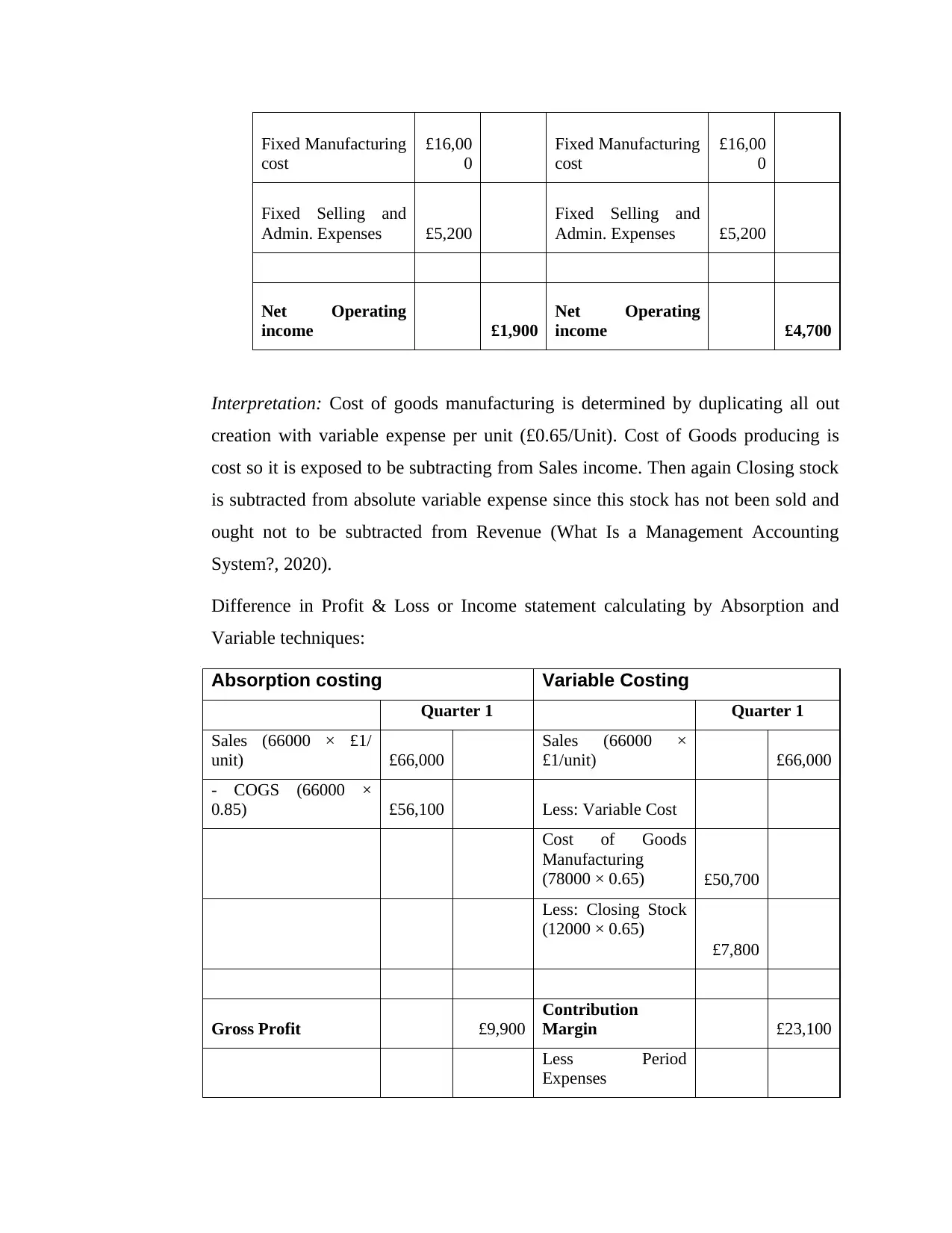

Fixed Manufacturing

cost

£16,00

0

Fixed Manufacturing

cost

£16,00

0

Fixed Selling and

Admin. Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

income £1,900

Net Operating

income £4,700

Interpretation: Cost of goods manufacturing is determined by duplicating all out

creation with variable expense per unit (£0.65/Unit). Cost of Goods producing is

cost so it is exposed to be subtracting from Sales income. Then again Closing stock

is subtracted from absolute variable expense since this stock has not been sold and

ought not to be subtracted from Revenue (What Is a Management Accounting

System?, 2020).

Difference in Profit & Loss or Income statement calculating by Absorption and

Variable techniques:

Absorption costing Variable Costing

Quarter 1 Quarter 1

Sales (66000 × £1/

unit) £66,000

Sales (66000 ×

£1/unit) £66,000

- COGS (66000 ×

0.85) £56,100 Less: Variable Cost

Cost of Goods

Manufacturing

(78000 × 0.65) £50,700

Less: Closing Stock

(12000 × 0.65)

£7,800

Gross Profit £9,900

Contribution

Margin £23,100

Less Period

Expenses

cost

£16,00

0

Fixed Manufacturing

cost

£16,00

0

Fixed Selling and

Admin. Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

income £1,900

Net Operating

income £4,700

Interpretation: Cost of goods manufacturing is determined by duplicating all out

creation with variable expense per unit (£0.65/Unit). Cost of Goods producing is

cost so it is exposed to be subtracting from Sales income. Then again Closing stock

is subtracted from absolute variable expense since this stock has not been sold and

ought not to be subtracted from Revenue (What Is a Management Accounting

System?, 2020).

Difference in Profit & Loss or Income statement calculating by Absorption and

Variable techniques:

Absorption costing Variable Costing

Quarter 1 Quarter 1

Sales (66000 × £1/

unit) £66,000

Sales (66000 ×

£1/unit) £66,000

- COGS (66000 ×

0.85) £56,100 Less: Variable Cost

Cost of Goods

Manufacturing

(78000 × 0.65) £50,700

Less: Closing Stock

(12000 × 0.65)

£7,800

Gross Profit £9,900

Contribution

Margin £23,100

Less Period

Expenses

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Operating

Expenses:

Fixed

Manufacturing cost £16,000

Selling & administ.

Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

Income £4,700

Net Operating

income £1,900

Interpretation: Income through absorption costing shows less gross profit than

variable costing method; the main reason behind this difference is calculation of per

unit variable and fixed cost. Another reason for variance is variable cost of

manufacturing product; which is not considered by Variable costing method.

Absorption costing Quarter 2 Variable Costing Quarter 2

Sales (74000 × £1/

unit) £74,000

Sales (74000 ×

£1/unit) £74,000

- COGS (74000 ×

0.89) £65,860 Less: Variable Cost

Cost of Goods

Manufacturing

(66000 × 0.65) £42,900

Add: Opening stock

(12000 × 0.65) £7,800

Less; Closing Stock

(4000 × 0.65) £2,600

Gross Loss £8,140

Contribution

Margin £25,900

Less Period

Expenses

Less: Operating

Expenses:

Fixed

Manufacturing cost £16,000

Selling & administ.

Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Expenses:

Fixed

Manufacturing cost £16,000

Selling & administ.

Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Net Operating

Income £4,700

Net Operating

income £1,900

Interpretation: Income through absorption costing shows less gross profit than

variable costing method; the main reason behind this difference is calculation of per

unit variable and fixed cost. Another reason for variance is variable cost of

manufacturing product; which is not considered by Variable costing method.

Absorption costing Quarter 2 Variable Costing Quarter 2

Sales (74000 × £1/

unit) £74,000

Sales (74000 ×

£1/unit) £74,000

- COGS (74000 ×

0.89) £65,860 Less: Variable Cost

Cost of Goods

Manufacturing

(66000 × 0.65) £42,900

Add: Opening stock

(12000 × 0.65) £7,800

Less; Closing Stock

(4000 × 0.65) £2,600

Gross Loss £8,140

Contribution

Margin £25,900

Less Period

Expenses

Less: Operating

Expenses:

Fixed

Manufacturing cost £16,000

Selling & administ.

Expenses £5,200

Fixed Selling and

Admin. Expenses £5,200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Operating

income £2,940

Net Operating

income £4,700

Interpretation: The translation for this figure is like above figure. Assimilation

costing incorporates all expenses, including fixed costs which are just identified

with creation, while variable costing just incorporates the variable expenses

legitimately acquired underway (Schaltegger and Burritt, 2017).

M2. Accurately apply a range of management accounting techniques and

produce appropriate financial reporting documents

Management accounting techniques are useful for managers to generate valuable reports for

making business decisions. On the basis of application of such techniques financial reporting

documents have been produced below:

Financial statements: Financial statement refers to the statement that states the financial position

of the business at the end of the accounting period and the results of business operations. The

main purpose of financial statements is to provide the information needed by their users to make

the right decision (Management Accounting – Meaning, Advantages & Functions, 2020).

Balance sheet: A balance sheet reports a company's assets, liabilities, and shareholders' equity at

a specific point in time, and provides the basis for calculating rates of return and evaluating its

capital structure. It is a financial statement that provides a snapshot of the amount invested by the

owners of a company as well as shareholders.

Income statement: An income statement or profit and loss account (also known as profit and loss

statement (P&L), profit or loss statement, revenue statement, statement of financial performance,

income statement, operating statement, or statement of operations) Is) one of the financial

statements of a company and shows the revenue and expenditure of the company during a

particular period.

Cash flow statement: Cash flow statement (CFS) measures how well a company manages its

cash position, which means that the company creates cash to fund its debt obligations and fund

its operating expenses. Cash flow statement complies with balance sheet and income statement.

income £2,940

Net Operating

income £4,700

Interpretation: The translation for this figure is like above figure. Assimilation

costing incorporates all expenses, including fixed costs which are just identified

with creation, while variable costing just incorporates the variable expenses

legitimately acquired underway (Schaltegger and Burritt, 2017).

M2. Accurately apply a range of management accounting techniques and

produce appropriate financial reporting documents

Management accounting techniques are useful for managers to generate valuable reports for

making business decisions. On the basis of application of such techniques financial reporting

documents have been produced below:

Financial statements: Financial statement refers to the statement that states the financial position

of the business at the end of the accounting period and the results of business operations. The

main purpose of financial statements is to provide the information needed by their users to make

the right decision (Management Accounting – Meaning, Advantages & Functions, 2020).

Balance sheet: A balance sheet reports a company's assets, liabilities, and shareholders' equity at

a specific point in time, and provides the basis for calculating rates of return and evaluating its

capital structure. It is a financial statement that provides a snapshot of the amount invested by the

owners of a company as well as shareholders.

Income statement: An income statement or profit and loss account (also known as profit and loss

statement (P&L), profit or loss statement, revenue statement, statement of financial performance,

income statement, operating statement, or statement of operations) Is) one of the financial

statements of a company and shows the revenue and expenditure of the company during a

particular period.

Cash flow statement: Cash flow statement (CFS) measures how well a company manages its

cash position, which means that the company creates cash to fund its debt obligations and fund

its operating expenses. Cash flow statement complies with balance sheet and income statement.

L.O.3: Explain the use of planning tools used in management accounting

using budgets for planning and control

P4. Explain the advantages and disadvantages of different types of planning

tools used for budgetary control

Budgeting: The budget is a statement of estimated receipts and expenses under a certain period,

a comparative table giving the amounts of income and expenses to be incurred; In addition, it is

an order or authority given by the appropriate authorities to collect and spend income (Budgeting

and Forecasting Software, 2020).

Types of Budgets:

1. Operating budget: This budget helps company in identifying whether personal finances are

enough to handle working capital requirement or not. Its main structure consists of preparing

sales/ revenue, cost of sales, gross profit, interest and depreciation and fixed assets. This

budget shows expected money after deducting operating activities from gross profit.

2. Capital budget: It is the process of allocation of funds for undertaking major projects by

business for the growth of business. For instance, construction of new plant, investment in

new venture. The main process includes, taking fixed amount of money out for investing in

project; later alternatives in the form of different available projects identifies and after sort

listing available projects on the basis of evaluation; company release amount of budget

(Budgeting software, 2020).

Advantages and disadvantages of different types of planning tools:

Budgets: The form in which a statement of income and expenditure of the company is

collected is called the budget. The annual financial statement of the income and expenditure

estimates of the previous year is presented in the budget.

Advantages Disadvantages

It supports business through build coordination

between different functional departments.

It is rigid in nature and cannot be

modified once prepared.

Budget is powerful technique along with

controlling expenses, also keep track of

income and expenses,

Due to less participation of employees;

it raises the situation of discouraging

workers.

using budgets for planning and control

P4. Explain the advantages and disadvantages of different types of planning

tools used for budgetary control

Budgeting: The budget is a statement of estimated receipts and expenses under a certain period,

a comparative table giving the amounts of income and expenses to be incurred; In addition, it is

an order or authority given by the appropriate authorities to collect and spend income (Budgeting

and Forecasting Software, 2020).

Types of Budgets:

1. Operating budget: This budget helps company in identifying whether personal finances are

enough to handle working capital requirement or not. Its main structure consists of preparing

sales/ revenue, cost of sales, gross profit, interest and depreciation and fixed assets. This

budget shows expected money after deducting operating activities from gross profit.

2. Capital budget: It is the process of allocation of funds for undertaking major projects by

business for the growth of business. For instance, construction of new plant, investment in

new venture. The main process includes, taking fixed amount of money out for investing in

project; later alternatives in the form of different available projects identifies and after sort

listing available projects on the basis of evaluation; company release amount of budget

(Budgeting software, 2020).

Advantages and disadvantages of different types of planning tools:

Budgets: The form in which a statement of income and expenditure of the company is

collected is called the budget. The annual financial statement of the income and expenditure

estimates of the previous year is presented in the budget.

Advantages Disadvantages

It supports business through build coordination

between different functional departments.

It is rigid in nature and cannot be

modified once prepared.

Budget is powerful technique along with

controlling expenses, also keep track of

income and expenses,

Due to less participation of employees;

it raises the situation of discouraging

workers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

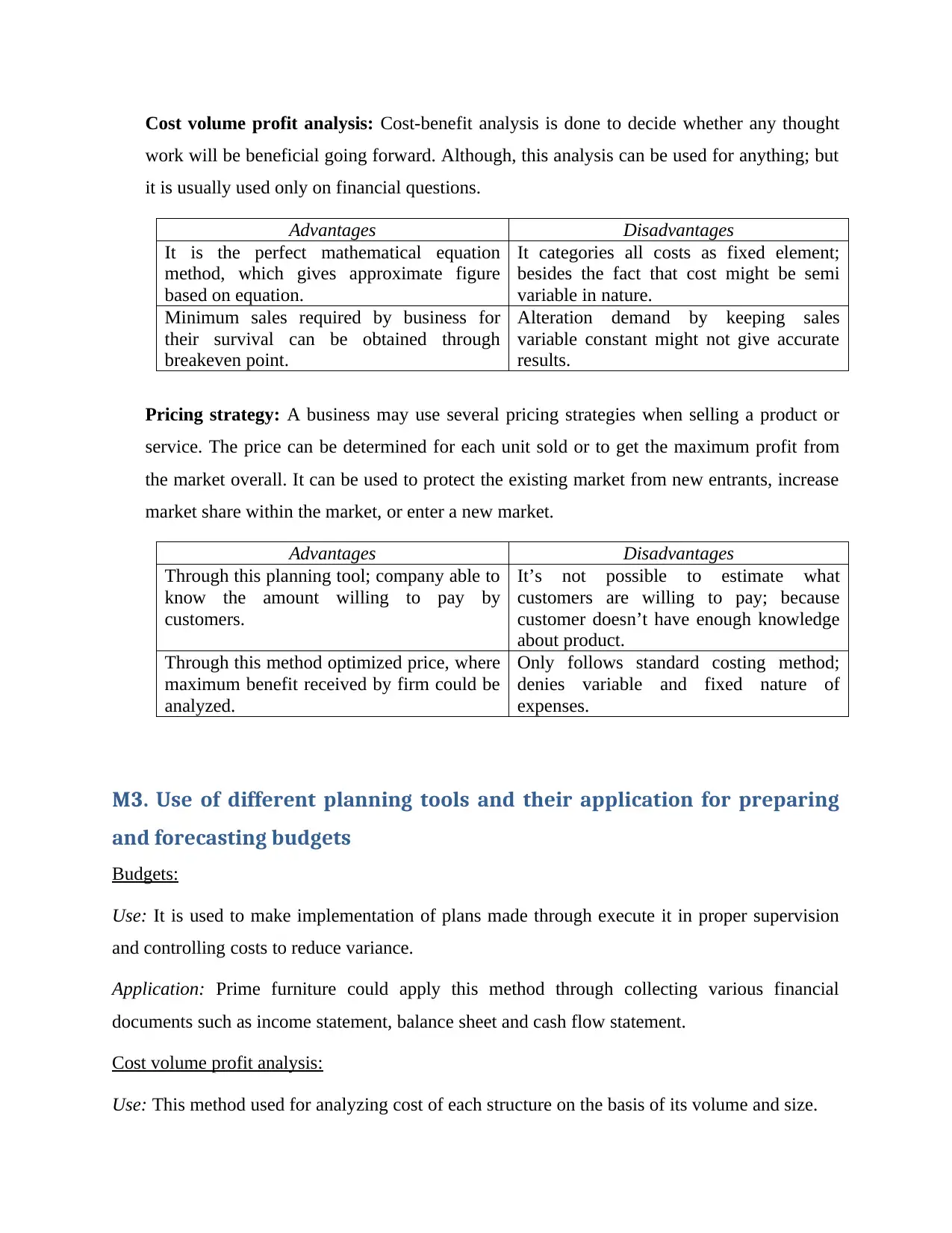

Cost volume profit analysis: Cost-benefit analysis is done to decide whether any thought

work will be beneficial going forward. Although, this analysis can be used for anything; but

it is usually used only on financial questions.

Advantages Disadvantages

It is the perfect mathematical equation

method, which gives approximate figure

based on equation.

It categories all costs as fixed element;

besides the fact that cost might be semi

variable in nature.

Minimum sales required by business for

their survival can be obtained through

breakeven point.

Alteration demand by keeping sales

variable constant might not give accurate

results.

Pricing strategy: A business may use several pricing strategies when selling a product or

service. The price can be determined for each unit sold or to get the maximum profit from

the market overall. It can be used to protect the existing market from new entrants, increase

market share within the market, or enter a new market.

Advantages Disadvantages

Through this planning tool; company able to

know the amount willing to pay by

customers.

It’s not possible to estimate what

customers are willing to pay; because

customer doesn’t have enough knowledge

about product.

Through this method optimized price, where

maximum benefit received by firm could be

analyzed.

Only follows standard costing method;

denies variable and fixed nature of

expenses.

M3. Use of different planning tools and their application for preparing

and forecasting budgets

Budgets:

Use: It is used to make implementation of plans made through execute it in proper supervision

and controlling costs to reduce variance.

Application: Prime furniture could apply this method through collecting various financial

documents such as income statement, balance sheet and cash flow statement.

Cost volume profit analysis:

Use: This method used for analyzing cost of each structure on the basis of its volume and size.

work will be beneficial going forward. Although, this analysis can be used for anything; but

it is usually used only on financial questions.

Advantages Disadvantages

It is the perfect mathematical equation

method, which gives approximate figure

based on equation.

It categories all costs as fixed element;

besides the fact that cost might be semi

variable in nature.

Minimum sales required by business for

their survival can be obtained through

breakeven point.

Alteration demand by keeping sales

variable constant might not give accurate

results.

Pricing strategy: A business may use several pricing strategies when selling a product or

service. The price can be determined for each unit sold or to get the maximum profit from

the market overall. It can be used to protect the existing market from new entrants, increase

market share within the market, or enter a new market.

Advantages Disadvantages

Through this planning tool; company able to

know the amount willing to pay by

customers.

It’s not possible to estimate what

customers are willing to pay; because

customer doesn’t have enough knowledge

about product.

Through this method optimized price, where

maximum benefit received by firm could be

analyzed.

Only follows standard costing method;

denies variable and fixed nature of

expenses.

M3. Use of different planning tools and their application for preparing

and forecasting budgets

Budgets:

Use: It is used to make implementation of plans made through execute it in proper supervision

and controlling costs to reduce variance.

Application: Prime furniture could apply this method through collecting various financial

documents such as income statement, balance sheet and cash flow statement.

Cost volume profit analysis:

Use: This method used for analyzing cost of each structure on the basis of its volume and size.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Application: This method can be applied by Prime Furniture through categorizing fixed and

variable cost separately and analyzing the impact of each costs and their importance for

operating core activities (The 5 Step Risk Management Process, 2018).

Pricing strategy:

Use: This strategy is useful to identify cost to be charged from customer.

Application: Prime furniture can apply this method through identify standard costing per unit and

adding some value as a desired profit.

L.O.4: Compare ways in which organizations could use management

accounting to respond to financial problems

P5. Compare how organizations are adapting management accounting systems

to respond to financial problems

Prime furniture can apply various key performance tools for analyzing its financial performance

to compare it with its competitors to know what problems are becoming hurdle in the way of

achieving goal. Some of the performance analyses tools which help company in comparison are

discussed below:

Return on capital employed: This performance analyses tool will support Prime furniture in

knowing how much proportion of net profit is earned by firm compare to capital employed. More

proportion indicates better performance.

Assets turnover: This tool shows how efficiently Prime Furniture has converted its invested fixed

assets into money. It usually compares net sales with proportion to fixed assets; more turnover

better for the company. As fewer turnovers indicates inefficiency of company and indicates non

performance of assets (Risk management, 2019).

Operating profit margin: This tool compares operating profit with net sales; it shows how much

proportion of net sales is successfully converted into operating profit. More proportion better for

the Prime Furniture; shows good performance through controlling minimizing the impact of

variable costs.

variable cost separately and analyzing the impact of each costs and their importance for

operating core activities (The 5 Step Risk Management Process, 2018).

Pricing strategy:

Use: This strategy is useful to identify cost to be charged from customer.

Application: Prime furniture can apply this method through identify standard costing per unit and

adding some value as a desired profit.

L.O.4: Compare ways in which organizations could use management

accounting to respond to financial problems

P5. Compare how organizations are adapting management accounting systems

to respond to financial problems

Prime furniture can apply various key performance tools for analyzing its financial performance

to compare it with its competitors to know what problems are becoming hurdle in the way of

achieving goal. Some of the performance analyses tools which help company in comparison are

discussed below:

Return on capital employed: This performance analyses tool will support Prime furniture in

knowing how much proportion of net profit is earned by firm compare to capital employed. More

proportion indicates better performance.

Assets turnover: This tool shows how efficiently Prime Furniture has converted its invested fixed

assets into money. It usually compares net sales with proportion to fixed assets; more turnover

better for the company. As fewer turnovers indicates inefficiency of company and indicates non

performance of assets (Risk management, 2019).

Operating profit margin: This tool compares operating profit with net sales; it shows how much

proportion of net sales is successfully converted into operating profit. More proportion better for

the Prime Furniture; shows good performance through controlling minimizing the impact of

variable costs.

M4. Analyze how in responding to financial problems, management

accounting can lead organizations to sustainable success

Management accounting can help Prime Furniture in improving financial performance of the

company in achieving sustainable success in following ways:

Advanced technology and features: Management accounting tools with its efficient advanced

technology like budget control, costing methods and evaluation process could support Prime

furniture in solving financial problem and attaining sustainable success (Sustainable Success,

2020).

Cost transparency: Management accounting will help Prime Furniture in maintaining

transparency and clarity of various costs among different functional departments. This will help

Prime furniture in achieving sustainable success.

Flexibility and independence: Due to flexible nature of management accounting; automated

artificial intelligence make it possible for Prime Furniture to reduce its involvement in making

reports yearly, monthly and weekly (Sustainable Success, 2020).

CONCLUSION

So, on the basis of project report it can be concluded that; the scope of management accounting

is wide and this creates many difficulties in the implementation process. Management requires

information from accounting as well as non-accounting sources. This leads to fairness and

subordination in the conclusions derived from it. The purpose of management accounting is to

provide managers with both qualitative and quantitative information to help them make

decisions, and thus maximize profit. This article is designed to help you learn the important

differences between financial accounting and management accounting. It is also recommended

that Prime furniture should adopt mix strategies by applying best suitable management

accounting tools which fulfills business requirement.

accounting can lead organizations to sustainable success

Management accounting can help Prime Furniture in improving financial performance of the

company in achieving sustainable success in following ways:

Advanced technology and features: Management accounting tools with its efficient advanced

technology like budget control, costing methods and evaluation process could support Prime

furniture in solving financial problem and attaining sustainable success (Sustainable Success,

2020).

Cost transparency: Management accounting will help Prime Furniture in maintaining

transparency and clarity of various costs among different functional departments. This will help

Prime furniture in achieving sustainable success.

Flexibility and independence: Due to flexible nature of management accounting; automated

artificial intelligence make it possible for Prime Furniture to reduce its involvement in making

reports yearly, monthly and weekly (Sustainable Success, 2020).

CONCLUSION

So, on the basis of project report it can be concluded that; the scope of management accounting

is wide and this creates many difficulties in the implementation process. Management requires

information from accounting as well as non-accounting sources. This leads to fairness and

subordination in the conclusions derived from it. The purpose of management accounting is to

provide managers with both qualitative and quantitative information to help them make

decisions, and thus maximize profit. This article is designed to help you learn the important

differences between financial accounting and management accounting. It is also recommended

that Prime furniture should adopt mix strategies by applying best suitable management

accounting tools which fulfills business requirement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.