Management Accounting Report: Costing and Value Chain Analysis

VerifiedAdded on 2023/01/18

|15

|2210

|39

Report

AI Summary

This comprehensive management accounting report delves into various aspects of financial analysis and cost management. It begins with an in-depth examination of value chains, specifically analyzing Wesfarmers' value chain, identifying primary and secondary activities, and discussing associated management accounting challenges. The report then proceeds to detailed cost accounting exercises, including the preparation of a cost of goods manufactured statement, a cost of sales statement, and an income statement for Portland Precision Engineering Company. Furthermore, it explores cost allocation methods, comparing and contrasting the direct, step-down, and reciprocal methods, and providing a justification for the most accurate approach. The report continues with a discussion on job costing and process costing methods, including the application of weighted average and FIFO methods in process costing, providing a complete overview of cost accounting principles and practices.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student

Name of the University

Author’s Note

Management Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Answer to Question 1: Value Chains.........................................................................................3

1.1 Introduction......................................................................................................................3

1.2 Value Chain of Wesfarmers.............................................................................................3

1.2.1 Primary Activities.....................................................................................................3

1.2.2 Secondary Activities.................................................................................................4

1.3 Conclusion........................................................................................................................5

Answer to Question 2: Cost Manufacturing Statement..............................................................5

Requirement [1].....................................................................................................................5

Requirement [2].....................................................................................................................6

Requirement [3] and [4].........................................................................................................6

Answer to Question 3: Cost Allocation.....................................................................................7

Requirement [1].....................................................................................................................7

Requirement [2].....................................................................................................................7

Requirement [3].....................................................................................................................7

Requirement [4].....................................................................................................................7

Requirement [5].....................................................................................................................8

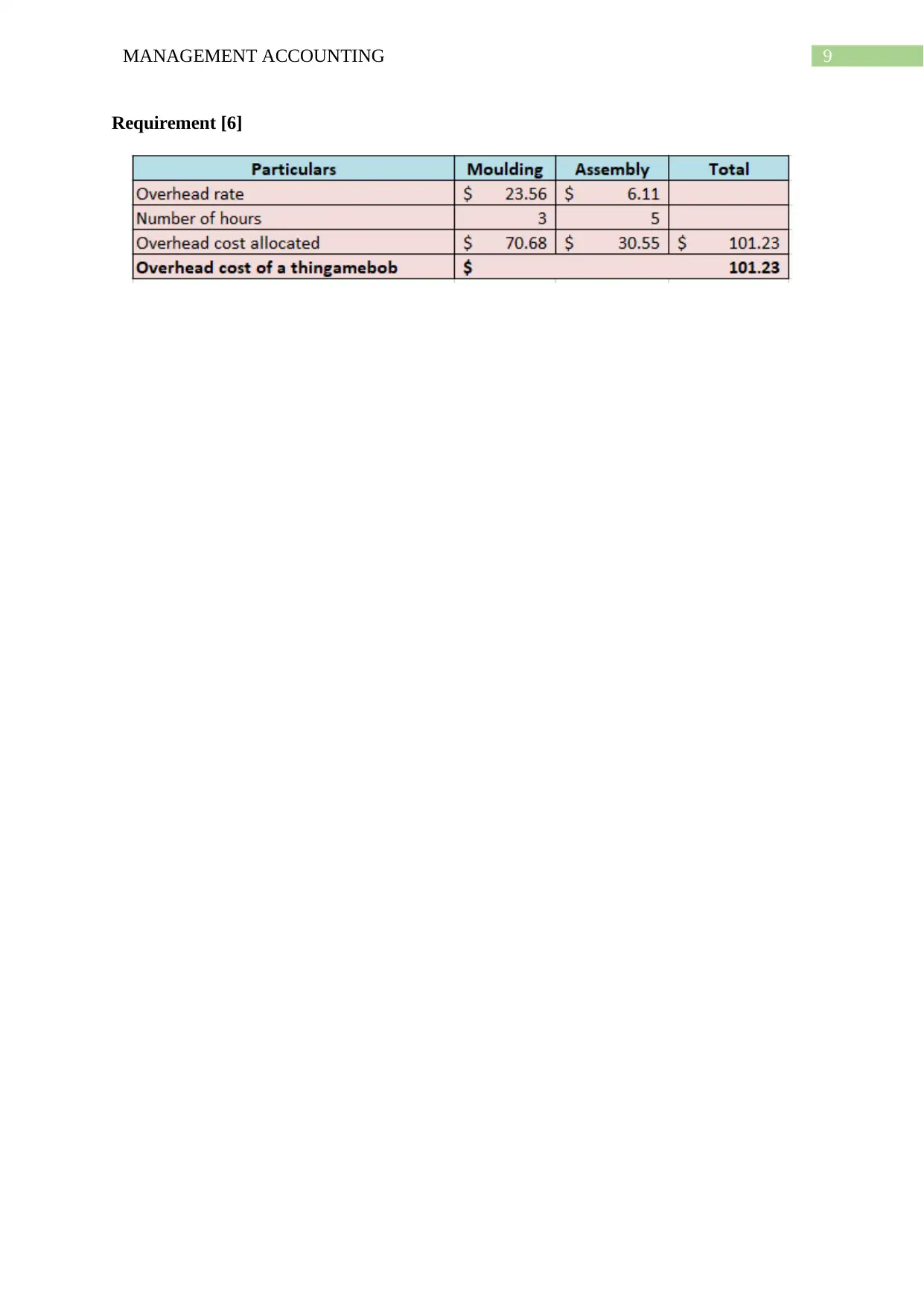

Requirement [6].....................................................................................................................8

Requirement [7].....................................................................................................................9

Answer to Question 4: Job Costing..........................................................................................11

Requirement [1]...................................................................................................................11

Table of Contents

Answer to Question 1: Value Chains.........................................................................................3

1.1 Introduction......................................................................................................................3

1.2 Value Chain of Wesfarmers.............................................................................................3

1.2.1 Primary Activities.....................................................................................................3

1.2.2 Secondary Activities.................................................................................................4

1.3 Conclusion........................................................................................................................5

Answer to Question 2: Cost Manufacturing Statement..............................................................5

Requirement [1].....................................................................................................................5

Requirement [2].....................................................................................................................6

Requirement [3] and [4].........................................................................................................6

Answer to Question 3: Cost Allocation.....................................................................................7

Requirement [1].....................................................................................................................7

Requirement [2].....................................................................................................................7

Requirement [3].....................................................................................................................7

Requirement [4].....................................................................................................................7

Requirement [5].....................................................................................................................8

Requirement [6].....................................................................................................................8

Requirement [7].....................................................................................................................9

Answer to Question 4: Job Costing..........................................................................................11

Requirement [1]...................................................................................................................11

2MANAGEMENT ACCOUNTING

Requirement [2]...................................................................................................................11

Requirement [3]...................................................................................................................11

Answer to Question 5: Process Costing...................................................................................11

Requirement [1]...................................................................................................................11

Requirement [2]...................................................................................................................12

References................................................................................................................................13

Requirement [2]...................................................................................................................11

Requirement [3]...................................................................................................................11

Answer to Question 5: Process Costing...................................................................................11

Requirement [1]...................................................................................................................11

Requirement [2]...................................................................................................................12

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

Answer to Question 1: Value Chains

1.1 Introduction

Value chain is considered as a set of activities perfumed by a specific firm with the

aim to deliver valuable products and services to the customers (Mudambi & Puck, 2016). The

main aim of this report is the analysis of the value chain of Wesfarmers Limited

(Wesfarmers).

1.2 Value Chain of Wesfarmers

In the recent years, Wesfarmers is facing certain management accounting issues in

relation to the value chain. Some of the issues in Wesfarmers are lose in the vision as well as

overall strategy through dividing their operations into various activities, difficulties in

segregating the primary and supporting activities as a result of increased complexity, gaining

required accounting information due to the division in different processes and others. In order

to overcome these management accounting related difficulties, Wesfarmers has upgraded

their value chain (Koc & Bozdag, 2017). The following discussion shows the main

components of the value chain of Wesfarmers.

According to Porter’s Value Chain model, Wesfarmers has segregated their value

chain in two activities; they are Primary Activities and Secondary Activities.

1.2.1 Primary Activities

The primary value chain activities of Wesfarmers have direct involvement with the

production and selling products. The primary activities are:

Inbound Logistics – Wesfarmers maintain strong relationship with their suppliers to gain

their support for receiving, storing and distributing products (Mohajeri et al., 2014).

Answer to Question 1: Value Chains

1.1 Introduction

Value chain is considered as a set of activities perfumed by a specific firm with the

aim to deliver valuable products and services to the customers (Mudambi & Puck, 2016). The

main aim of this report is the analysis of the value chain of Wesfarmers Limited

(Wesfarmers).

1.2 Value Chain of Wesfarmers

In the recent years, Wesfarmers is facing certain management accounting issues in

relation to the value chain. Some of the issues in Wesfarmers are lose in the vision as well as

overall strategy through dividing their operations into various activities, difficulties in

segregating the primary and supporting activities as a result of increased complexity, gaining

required accounting information due to the division in different processes and others. In order

to overcome these management accounting related difficulties, Wesfarmers has upgraded

their value chain (Koc & Bozdag, 2017). The following discussion shows the main

components of the value chain of Wesfarmers.

According to Porter’s Value Chain model, Wesfarmers has segregated their value

chain in two activities; they are Primary Activities and Secondary Activities.

1.2.1 Primary Activities

The primary value chain activities of Wesfarmers have direct involvement with the

production and selling products. The primary activities are:

Inbound Logistics – Wesfarmers maintain strong relationship with their suppliers to gain

their support for receiving, storing and distributing products (Mohajeri et al., 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

Operations – Wesfarmers has implemented effective processes for processing the raw

materials into the end products so that they can be launched to the market.

Outbound Logistics – Wesfarmers has implement outbound logistics services like material

handling, warehousing, scheduling, order processing, transporting and delivering to the

destinations (Mohajeri et al., 2014).

Marketing and Sales – Under this activity, Wesfarmers has taken initiatives like developing

sales-force, advertising, pricing, promotional activities, relationship development with the

customers, competitor analysis and others (Mohajeri et al., 2014).

Services – Wesfarmers has ensured the introduction of both the pre-sale and post-sales

services to their customers with the aim to cater to their needs in better manner.

1.2.2 Secondary Activities

These activities play a crucial role in providing support to these primary activities and

these activities of Wesfarmers are shown below:

Infrastructure – Wesfarmers has introduced system like quality management, handling of

legal matters, financial planning, accounting and strategic management. These activities help

Wesfarmers in optimising the whole value chain (Sivula & Kantola, 2014).

Human Resource Management – Wesfarmers has considered the evaluation of certain

human resource aspects like recruiting, selecting, training, rewarding, performance

management and others (Sivula & Kantola, 2014).

Technology Development – Wesfarmers has introduced certain services like automation

software, technology-driven customer care, product design research and others.

Operations – Wesfarmers has implemented effective processes for processing the raw

materials into the end products so that they can be launched to the market.

Outbound Logistics – Wesfarmers has implement outbound logistics services like material

handling, warehousing, scheduling, order processing, transporting and delivering to the

destinations (Mohajeri et al., 2014).

Marketing and Sales – Under this activity, Wesfarmers has taken initiatives like developing

sales-force, advertising, pricing, promotional activities, relationship development with the

customers, competitor analysis and others (Mohajeri et al., 2014).

Services – Wesfarmers has ensured the introduction of both the pre-sale and post-sales

services to their customers with the aim to cater to their needs in better manner.

1.2.2 Secondary Activities

These activities play a crucial role in providing support to these primary activities and

these activities of Wesfarmers are shown below:

Infrastructure – Wesfarmers has introduced system like quality management, handling of

legal matters, financial planning, accounting and strategic management. These activities help

Wesfarmers in optimising the whole value chain (Sivula & Kantola, 2014).

Human Resource Management – Wesfarmers has considered the evaluation of certain

human resource aspects like recruiting, selecting, training, rewarding, performance

management and others (Sivula & Kantola, 2014).

Technology Development – Wesfarmers has introduced certain services like automation

software, technology-driven customer care, product design research and others.

5MANAGEMENT ACCOUNTING

Procurement – Wesfarmers has carefully considered the procurement activities such as

purchase of raw materials, purchase of machineries and others for the production of finished

goods (Sivula & Kantola, 2014).

1.3 Conclusion

It can be seen from the above discussion that Wesfarmers has implemented certain

processes and procedures for their primary and secondary activities in value chain. It needs to

be mentioned that these processes of the value chain of Wesfarmers have been majorly

helpful for the company to resolve the range of issues in the field of management accounting.

At the same time, the company is needed to consider the continuous improvements of these

operations.

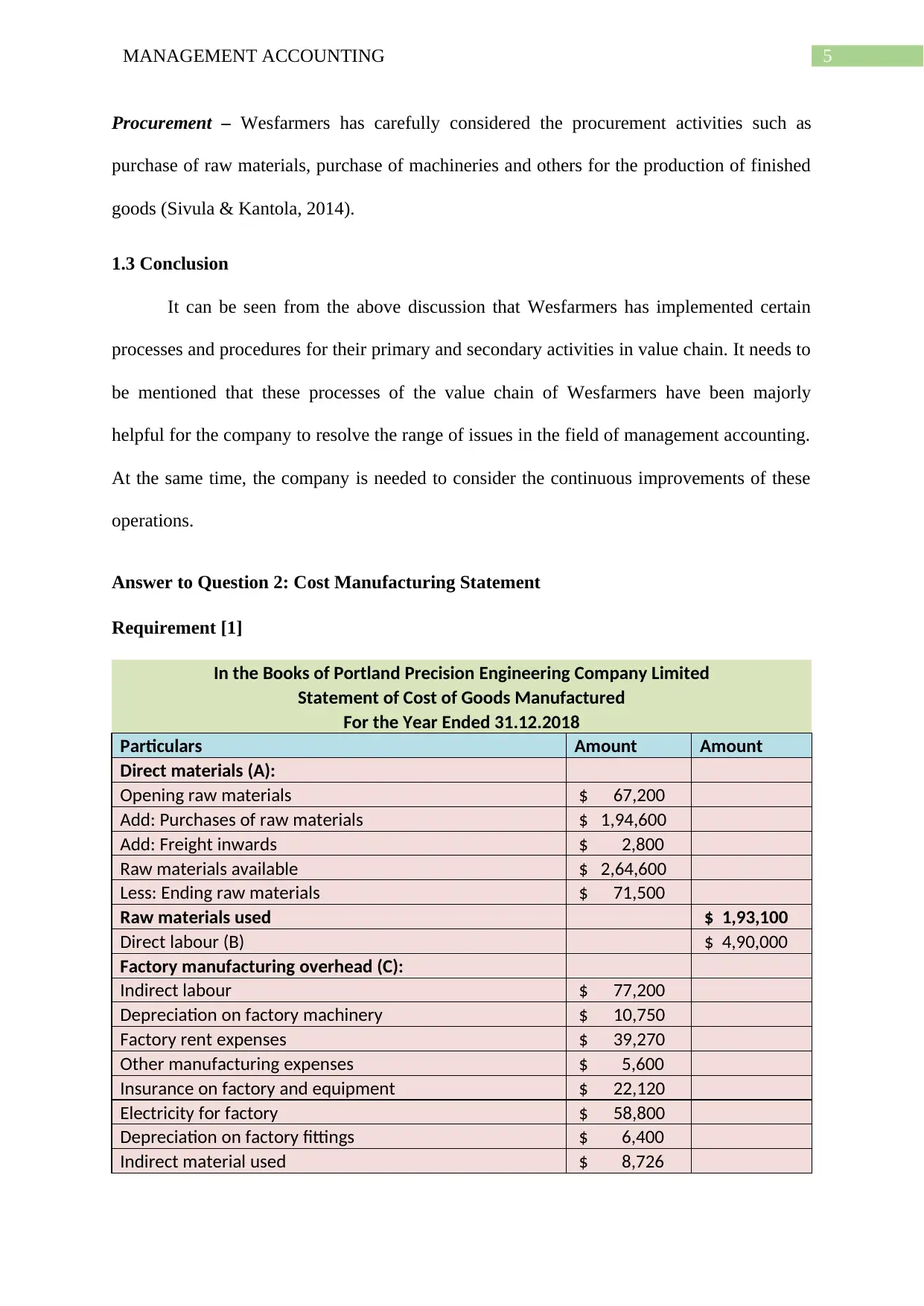

Answer to Question 2: Cost Manufacturing Statement

Requirement [1]

In the Books of Portland Precision Engineering Company Limited

Statement of Cost of Goods Manufactured

For the Year Ended 31.12.2018

Particulars Amount Amount

Direct materials (A):

Opening raw materials $ 67,200

Add: Purchases of raw materials $ 1,94,600

Add: Freight inwards $ 2,800

Raw materials available $ 2,64,600

Less: Ending raw materials $ 71,500

Raw materials used $ 1,93,100

Direct labour (B) $ 4,90,000

Factory manufacturing overhead (C):

Indirect labour $ 77,200

Depreciation on factory machinery $ 10,750

Factory rent expenses $ 39,270

Other manufacturing expenses $ 5,600

Insurance on factory and equipment $ 22,120

Electricity for factory $ 58,800

Depreciation on factory fittings $ 6,400

Indirect material used $ 8,726

Procurement – Wesfarmers has carefully considered the procurement activities such as

purchase of raw materials, purchase of machineries and others for the production of finished

goods (Sivula & Kantola, 2014).

1.3 Conclusion

It can be seen from the above discussion that Wesfarmers has implemented certain

processes and procedures for their primary and secondary activities in value chain. It needs to

be mentioned that these processes of the value chain of Wesfarmers have been majorly

helpful for the company to resolve the range of issues in the field of management accounting.

At the same time, the company is needed to consider the continuous improvements of these

operations.

Answer to Question 2: Cost Manufacturing Statement

Requirement [1]

In the Books of Portland Precision Engineering Company Limited

Statement of Cost of Goods Manufactured

For the Year Ended 31.12.2018

Particulars Amount Amount

Direct materials (A):

Opening raw materials $ 67,200

Add: Purchases of raw materials $ 1,94,600

Add: Freight inwards $ 2,800

Raw materials available $ 2,64,600

Less: Ending raw materials $ 71,500

Raw materials used $ 1,93,100

Direct labour (B) $ 4,90,000

Factory manufacturing overhead (C):

Indirect labour $ 77,200

Depreciation on factory machinery $ 10,750

Factory rent expenses $ 39,270

Other manufacturing expenses $ 5,600

Insurance on factory and equipment $ 22,120

Electricity for factory $ 58,800

Depreciation on factory fittings $ 6,400

Indirect material used $ 8,726

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

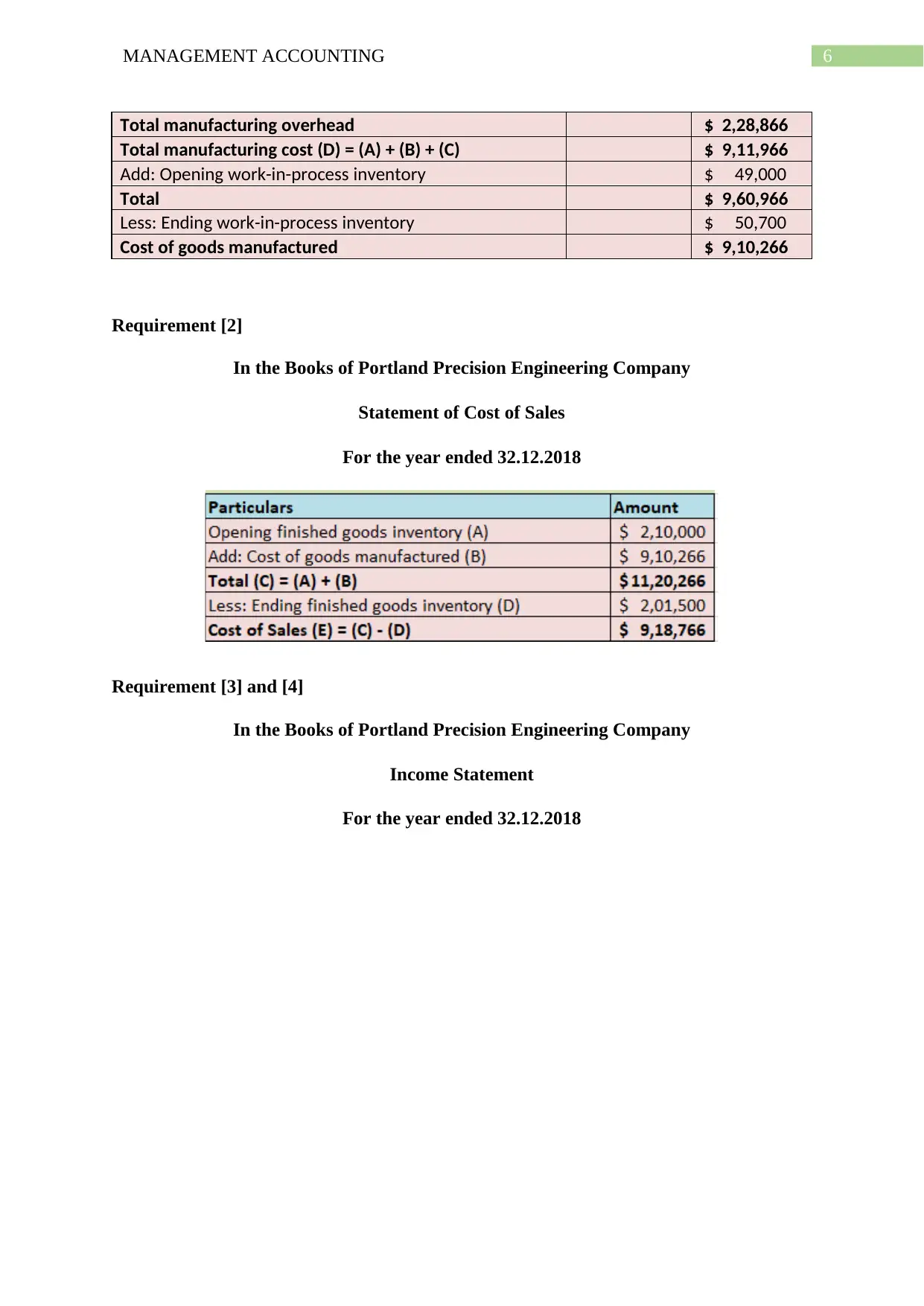

Total manufacturing overhead $ 2,28,866

Total manufacturing cost (D) = (A) + (B) + (C) $ 9,11,966

Add: Opening work-in-process inventory $ 49,000

Total $ 9,60,966

Less: Ending work-in-process inventory $ 50,700

Cost of goods manufactured $ 9,10,266

Requirement [2]

In the Books of Portland Precision Engineering Company

Statement of Cost of Sales

For the year ended 32.12.2018

Requirement [3] and [4]

In the Books of Portland Precision Engineering Company

Income Statement

For the year ended 32.12.2018

Total manufacturing overhead $ 2,28,866

Total manufacturing cost (D) = (A) + (B) + (C) $ 9,11,966

Add: Opening work-in-process inventory $ 49,000

Total $ 9,60,966

Less: Ending work-in-process inventory $ 50,700

Cost of goods manufactured $ 9,10,266

Requirement [2]

In the Books of Portland Precision Engineering Company

Statement of Cost of Sales

For the year ended 32.12.2018

Requirement [3] and [4]

In the Books of Portland Precision Engineering Company

Income Statement

For the year ended 32.12.2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

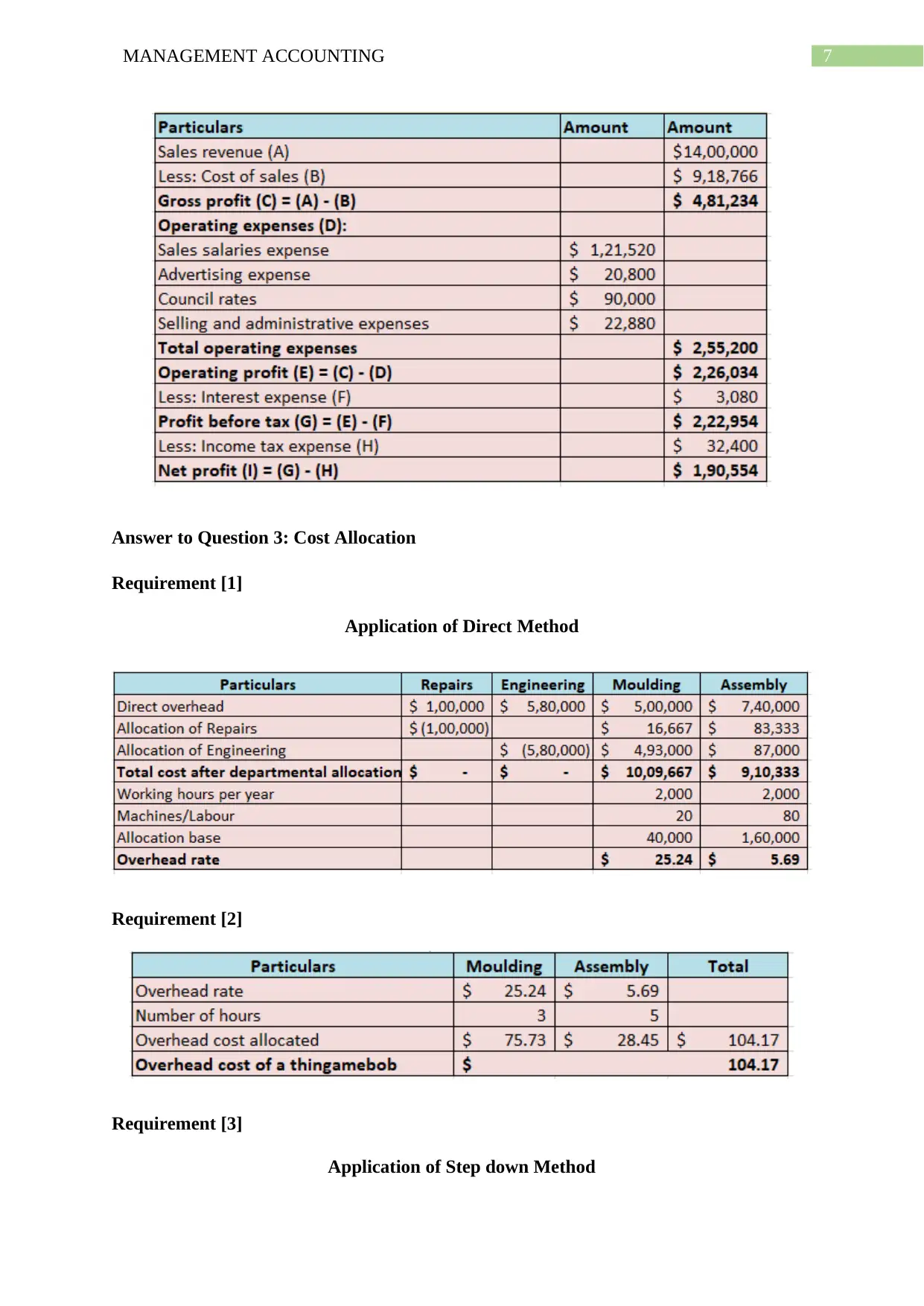

Answer to Question 3: Cost Allocation

Requirement [1]

Application of Direct Method

Requirement [2]

Requirement [3]

Application of Step down Method

Answer to Question 3: Cost Allocation

Requirement [1]

Application of Direct Method

Requirement [2]

Requirement [3]

Application of Step down Method

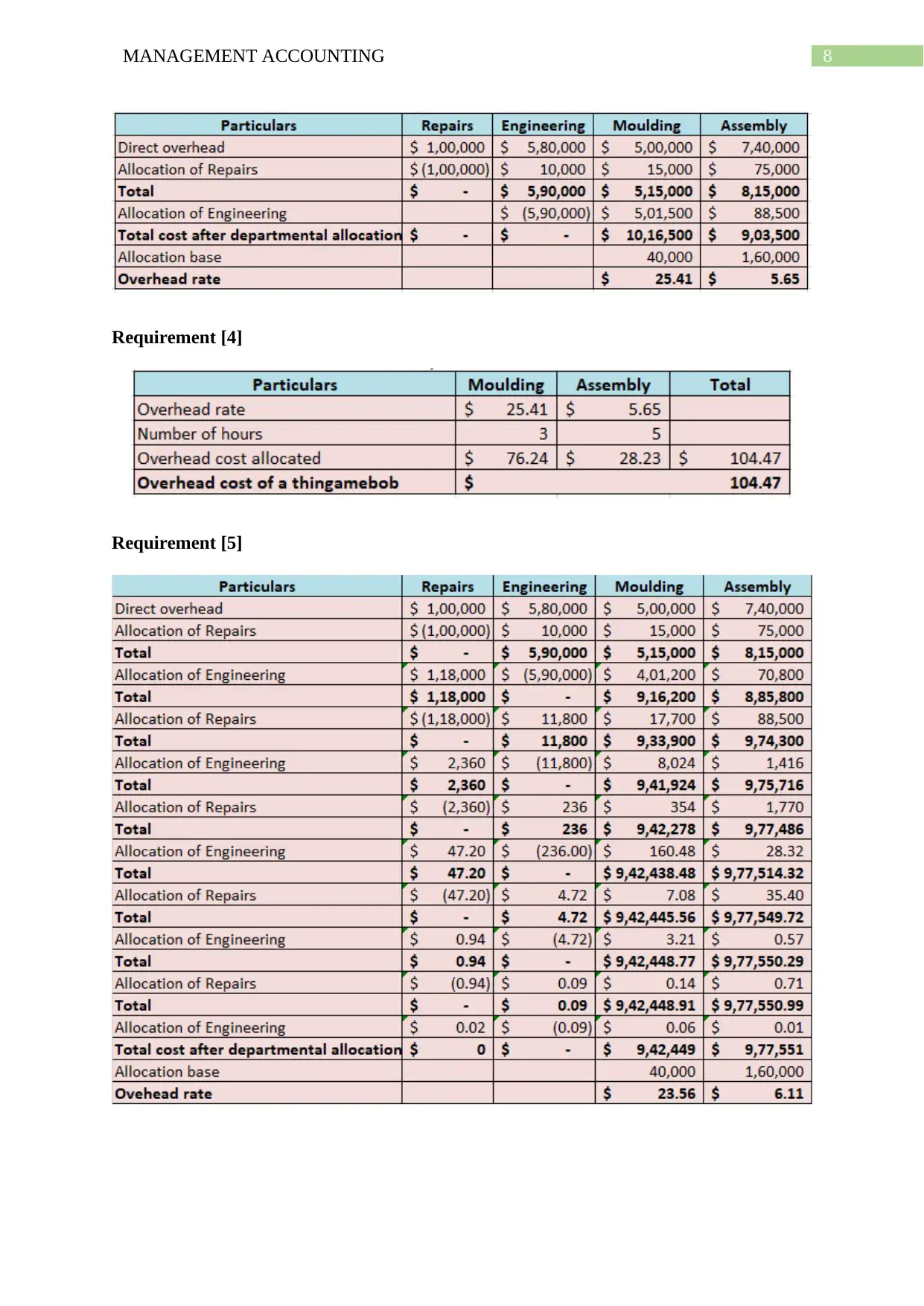

8MANAGEMENT ACCOUNTING

Requirement [4]

Requirement [5]

Requirement [4]

Requirement [5]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

Requirement [6]

Requirement [6]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

Requirement [7]

Memo

TO: The Chief Financial Officer

FROM: David Jones

DATE: 10.04.2019

SUBJECT: Explanation on the most accurate method to support departmental cost allocation

The main intention behind writing this internal memo is to provide the Chief Financial

Officer with the suggestion on the fact that which method is the most appropriate for the

process of departmental cost allocation for determining the most accurate overhead rates and

product cost. The following discussion considers the analysis of three methods; they are

Direct method, Step-down method and Reciprocal method.

The direct method is considered as the simplest method among these three methods and the

level of complexity is less in this method (Drury, 2013). Under this method, the accountants

of the companies are needed to assign the costs of each services to each operating department

on the basis of the share of each department and the accountants are needed to consider the

allocation base in this case. One major aspect in this method is that this method does not

provide the accountants with the scope to consider the services used by the other service

departments (Drury, 2013). This method is not used for tackling the complex costing

situations of the companies.

The Step-down method is different from the above discussed direct method in the presence of

certain aspects. Under this particular method, the accountants are needed to consider

assigning costs to each of the service departments on the sequential basis (Kieso, Weygandt

& Warfield, 2016). The commencement of these sequences can be seen with the service

Requirement [7]

Memo

TO: The Chief Financial Officer

FROM: David Jones

DATE: 10.04.2019

SUBJECT: Explanation on the most accurate method to support departmental cost allocation

The main intention behind writing this internal memo is to provide the Chief Financial

Officer with the suggestion on the fact that which method is the most appropriate for the

process of departmental cost allocation for determining the most accurate overhead rates and

product cost. The following discussion considers the analysis of three methods; they are

Direct method, Step-down method and Reciprocal method.

The direct method is considered as the simplest method among these three methods and the

level of complexity is less in this method (Drury, 2013). Under this method, the accountants

of the companies are needed to assign the costs of each services to each operating department

on the basis of the share of each department and the accountants are needed to consider the

allocation base in this case. One major aspect in this method is that this method does not

provide the accountants with the scope to consider the services used by the other service

departments (Drury, 2013). This method is not used for tackling the complex costing

situations of the companies.

The Step-down method is different from the above discussed direct method in the presence of

certain aspects. Under this particular method, the accountants are needed to consider

assigning costs to each of the service departments on the sequential basis (Kieso, Weygandt

& Warfield, 2016). The commencement of these sequences can be seen with the service

11MANAGEMENT ACCOUNTING

departments since these are the departments that consume maximum costs. After the

assignment of the costs to each of the service department, the accountants consider the

service departments with the next maximum amount of cost. The continuation of this process

can be seen until the department in the company with the lowest cost has allocated all of the

cots. Thus, it can be seen that step-down method consider the sequential distribution of costs

to the service departments (Kieso, Weygandt & Warfield, 2016).

The reciprocal method has major differences with the above two discussed methods sue to the

fact that this method includes major complexities. This particular method makes the cost of

service departments enable to operate department wise along with the other service

departments (Klychova et al., 2015). Under this method, the accountants of the companies

undertake recognizing the relationship between different service departments. At the same

time, under this process, the accountants of the companies are needed to allocate the costs to

and from each of the service departments for the provided specific services. This aspect

indicates towards the fact that this method takes into consideration each of the costs on the

basis of each of the services departments. This particular process ensures the effective

allocation of the costs of the companies in each department on an effective manner (Klychova

et al., 2015).

Thus, it can be seen from the above discussion that all the above-discussed three methods

have different features, but the reciprocal method can be considered as most accurate since it

ensures accurate allocation of costs in all the service departments. At the same time, this

method helps the companies in minimizing the overall expenses that is majorly helpful for

them. For these reasons, reciprocal method is considered as the most accurate method.

departments since these are the departments that consume maximum costs. After the

assignment of the costs to each of the service department, the accountants consider the

service departments with the next maximum amount of cost. The continuation of this process

can be seen until the department in the company with the lowest cost has allocated all of the

cots. Thus, it can be seen that step-down method consider the sequential distribution of costs

to the service departments (Kieso, Weygandt & Warfield, 2016).

The reciprocal method has major differences with the above two discussed methods sue to the

fact that this method includes major complexities. This particular method makes the cost of

service departments enable to operate department wise along with the other service

departments (Klychova et al., 2015). Under this method, the accountants of the companies

undertake recognizing the relationship between different service departments. At the same

time, under this process, the accountants of the companies are needed to allocate the costs to

and from each of the service departments for the provided specific services. This aspect

indicates towards the fact that this method takes into consideration each of the costs on the

basis of each of the services departments. This particular process ensures the effective

allocation of the costs of the companies in each department on an effective manner (Klychova

et al., 2015).

Thus, it can be seen from the above discussion that all the above-discussed three methods

have different features, but the reciprocal method can be considered as most accurate since it

ensures accurate allocation of costs in all the service departments. At the same time, this

method helps the companies in minimizing the overall expenses that is majorly helpful for

them. For these reasons, reciprocal method is considered as the most accurate method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.