Management Accounting Principles: Costing & Income Statement Analysis

VerifiedAdded on 2023/05/29

|14

|1203

|278

Presentation

AI Summary

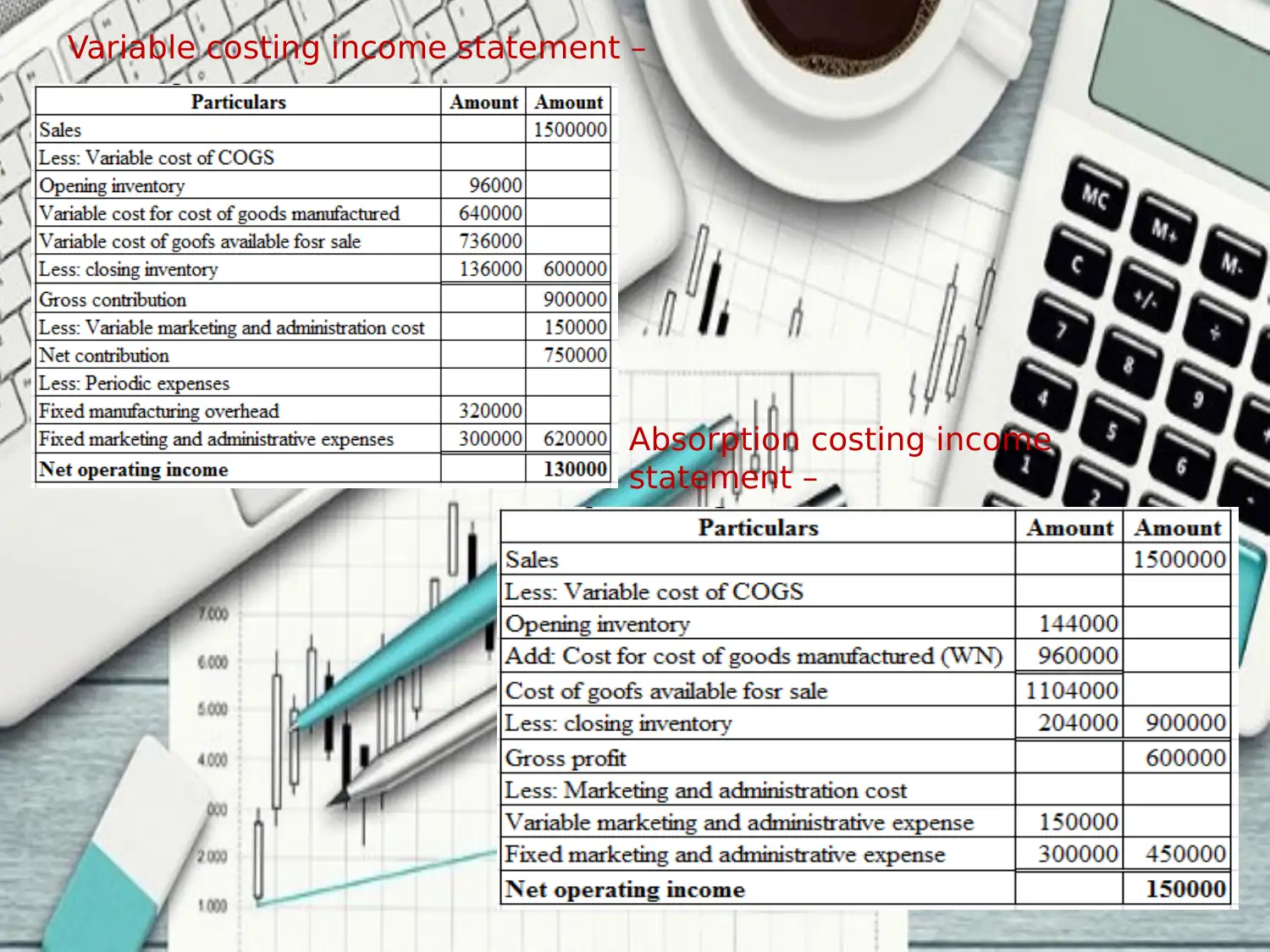

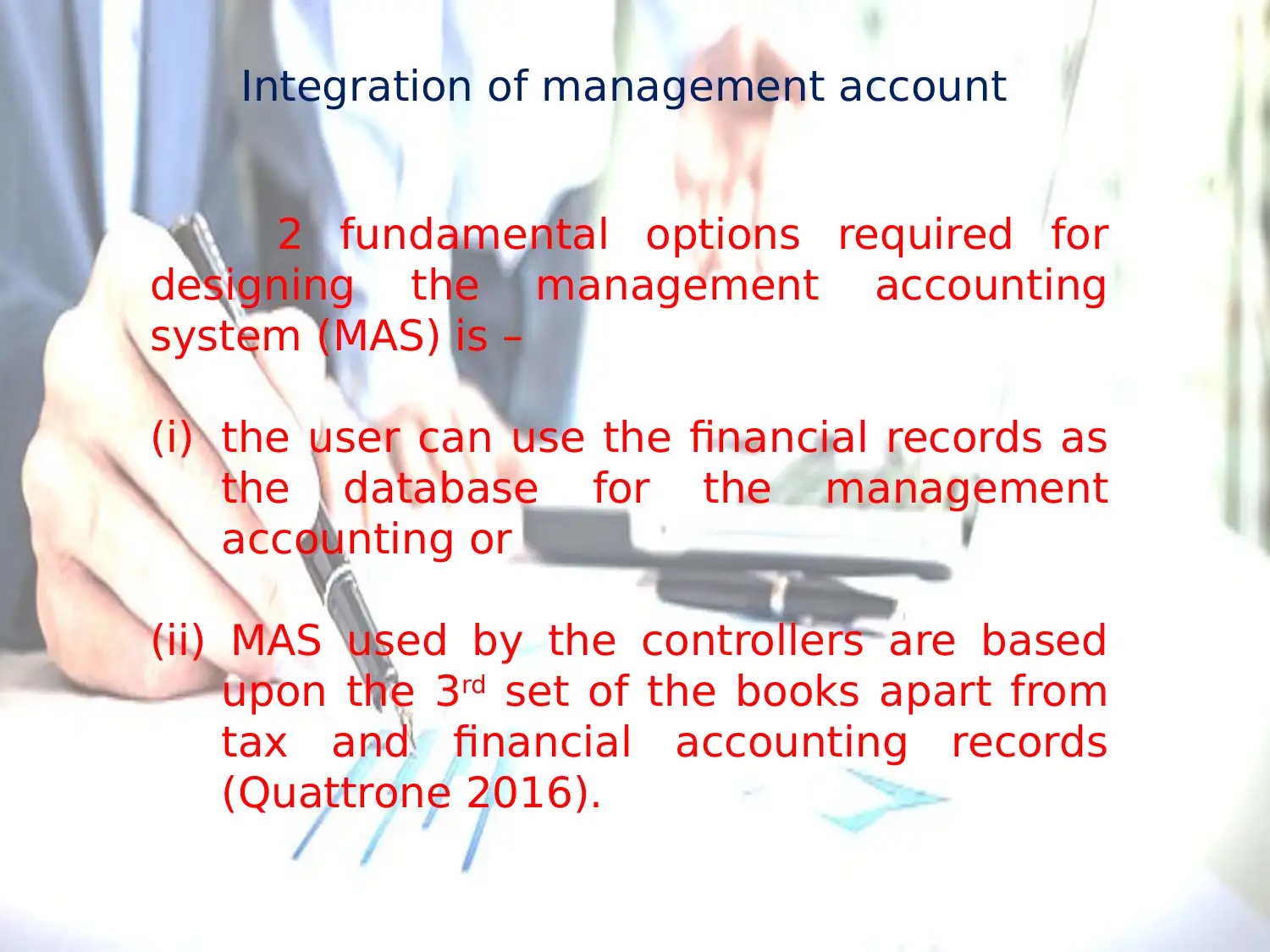

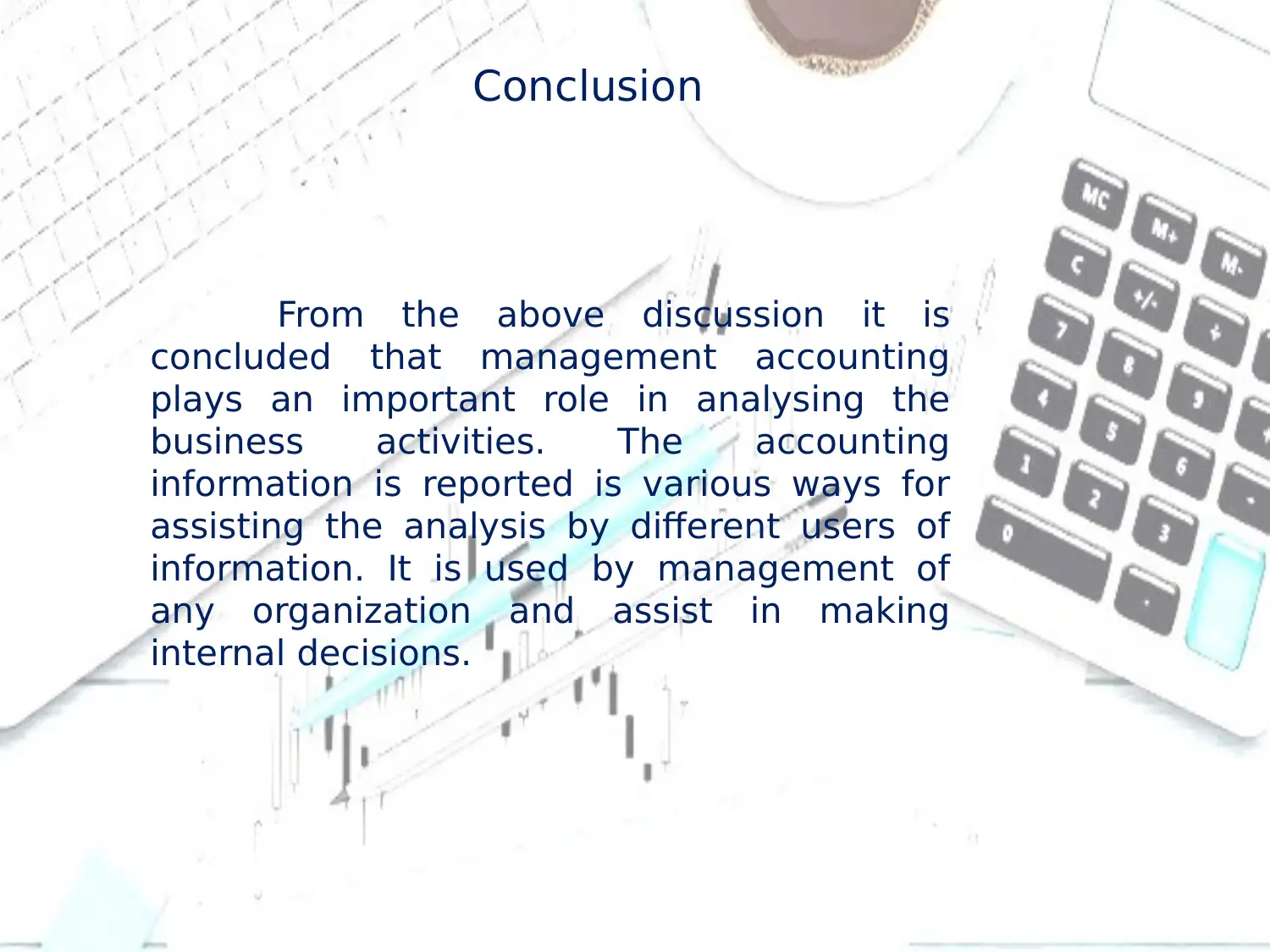

This presentation provides an overview of management accounting principles, focusing on the role of management accounting in analyzing business operations and costs for internal reporting and decision-making. It covers key aspects such as revenue and expense analysis, budgeting, and different management accounting systems. The presentation elucidates various methods used for management accounting reports, including financial and sales reports, and differentiates between period and product costs. A detailed comparison of absorption costing and marginal costing is presented, along with illustrative examples of income statements prepared using both variable and absorption costing techniques. Finally, the integration of management accounting within an organization is discussed, highlighting the importance of management accounting in achieving organizational goals. The presentation concludes by emphasizing the significance of management accounting in internal decision-making processes.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.