Effective Management Accounting Systems: A Case Study of R.L. Maynard Limited

VerifiedAdded on 2019/12/18

|19

|4825

|383

Essay

AI Summary

R.L. Maynard Limited uses various management accounting systems, including high-quality materials, lean accounting, transfer pricing, and budgetary control, to reduce financial problems and improve the company's performance. The use of these systems enables the company to utilize raw materials effectively, eliminate extra expenses, and make informed decisions. By adopting these management accounting approaches, R.L. Maynard Limited can overcome financial constraints, enhance its productivity and efficiency, and ultimately increase its revenue and profit levels.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

Management accounting is a process where different kinds of reports as well as accounts

are prepared with help of various financial transactions. Further, by this the entrepreneur able to

decide that whether the company is performing well in the industry or not and take corrective

actions if it generates negative return. In the present case study, there is R.L. Maynard Limited

organisation is selected which is UK based small enterprise as well as operating in the

construction segment. It has 24 number of employees along with 10.00 GBP sales at the end of

financial year. The report shows numerous kinds of systems and approaches of management

accounting which are required for the R.L. Maynard Limited in order to give response to the

financial obstacles. Further, it describes that what are differences among the absorption as well

as marginal costing method. Beside this, current study focuses on different tools of financial

planning used by the company to make it more profitable in the UK's construction sector.

TASK 1

P1 Explanation of different management accounting systems along with requirements in R.L.

Maynard Limited

Business Report

To,

Board of Directors,

R. L. Maynard Limited

Date: 20th April 2017

Subject: Management accounting systems

Throughput accounting system: It is a term of management accounting which are used

for the performance measurement. Throughput accounting is way to measure all financial aspect

in R. L. Maynard Limited. It mainly discusses on cash factor. Throughput accounting is differed

from the cost account in cost accounting we measure overall cost investing in company but in

throughput account mainly focus on cash, which means mainly focus on what revenue ratio is

generated and how much we loose (B Douglas Clinton CMA and CFM, 2012).

Lean accounting system: Lean accounting is a term of management accounting where

1

Management accounting is a process where different kinds of reports as well as accounts

are prepared with help of various financial transactions. Further, by this the entrepreneur able to

decide that whether the company is performing well in the industry or not and take corrective

actions if it generates negative return. In the present case study, there is R.L. Maynard Limited

organisation is selected which is UK based small enterprise as well as operating in the

construction segment. It has 24 number of employees along with 10.00 GBP sales at the end of

financial year. The report shows numerous kinds of systems and approaches of management

accounting which are required for the R.L. Maynard Limited in order to give response to the

financial obstacles. Further, it describes that what are differences among the absorption as well

as marginal costing method. Beside this, current study focuses on different tools of financial

planning used by the company to make it more profitable in the UK's construction sector.

TASK 1

P1 Explanation of different management accounting systems along with requirements in R.L.

Maynard Limited

Business Report

To,

Board of Directors,

R. L. Maynard Limited

Date: 20th April 2017

Subject: Management accounting systems

Throughput accounting system: It is a term of management accounting which are used

for the performance measurement. Throughput accounting is way to measure all financial aspect

in R. L. Maynard Limited. It mainly discusses on cash factor. Throughput accounting is differed

from the cost account in cost accounting we measure overall cost investing in company but in

throughput account mainly focus on cash, which means mainly focus on what revenue ratio is

generated and how much we loose (B Douglas Clinton CMA and CFM, 2012).

Lean accounting system: Lean accounting is a term of management accounting where

1

managed all over the manufacturing environment. And in this accounting system management

will focus on the cost factor. Like indirect cost or direct cost. In this accounting system measure

all the occurring cost in R. L. Maynard company. This accounting system is less complex

accounting system. Lean accounting is managed by the managers and make sure about the

reduce all in direct expenses in an organization. Lean accounting is focus on reducing indirect

cost and increase productivity. Control over the lean production company increase their

performance and increase revenue.

Transfer pricing: In this type of accounting system company transfer its product to

subsidiary company, whereas company transact with the other subsidiary company. Transfer

price is also known as transfer cost (Otley, 2016). Most of the time transfer cost increase

addition cost and time consuming which is negative for R. L. Maynard. Extra manpower will be

required to execute this system. Moreover, transfer prices some times creates dysfunctional

behaviour between among employees and organisations. Transferring cost accounting system is

expensive system rather than others.

Budgetary control: It is a process of determine actual budget of the organisation and

control over the all costing. Budgetary control is established for future planning forecasting and

requirements expected performance of the R. L. Maynard in construction industry. Budgetary

control is helpful to elimination of wastes and increase in profitability. Budgetary control is a

way to difference between actual costing to estimated costing. Budgetary control is a process to

control over the all expenses such as indirect expense or direct expenses. Reducing all those

expenses are help to increasing productivity and generating revenue. One of the main

disadvantage of budgetary control for R. L. Maynard is uncertain future, whereas sudden

changes are greatly high impact on estimated budgets.

Inventory accounting: Inventory accounting system is based on properly control over

the manufacturing system as well as production system. Inventory control system is an internal

system of control, where check internal all stock inventory, along with reducing over

manufacturing. In this accounting system company has to be information about the inventory

control system (Boyns and Edwards, 2013). Inventory control system is beneficial for the R. L.

Maynard whereas less stock wasted. Inventory control system is relay on LIFO and FIFO

system, where product manufacture in last but sale at their first. On other side product would be

2

will focus on the cost factor. Like indirect cost or direct cost. In this accounting system measure

all the occurring cost in R. L. Maynard company. This accounting system is less complex

accounting system. Lean accounting is managed by the managers and make sure about the

reduce all in direct expenses in an organization. Lean accounting is focus on reducing indirect

cost and increase productivity. Control over the lean production company increase their

performance and increase revenue.

Transfer pricing: In this type of accounting system company transfer its product to

subsidiary company, whereas company transact with the other subsidiary company. Transfer

price is also known as transfer cost (Otley, 2016). Most of the time transfer cost increase

addition cost and time consuming which is negative for R. L. Maynard. Extra manpower will be

required to execute this system. Moreover, transfer prices some times creates dysfunctional

behaviour between among employees and organisations. Transferring cost accounting system is

expensive system rather than others.

Budgetary control: It is a process of determine actual budget of the organisation and

control over the all costing. Budgetary control is established for future planning forecasting and

requirements expected performance of the R. L. Maynard in construction industry. Budgetary

control is helpful to elimination of wastes and increase in profitability. Budgetary control is a

way to difference between actual costing to estimated costing. Budgetary control is a process to

control over the all expenses such as indirect expense or direct expenses. Reducing all those

expenses are help to increasing productivity and generating revenue. One of the main

disadvantage of budgetary control for R. L. Maynard is uncertain future, whereas sudden

changes are greatly high impact on estimated budgets.

Inventory accounting: Inventory accounting system is based on properly control over

the manufacturing system as well as production system. Inventory control system is an internal

system of control, where check internal all stock inventory, along with reducing over

manufacturing. In this accounting system company has to be information about the inventory

control system (Boyns and Edwards, 2013). Inventory control system is beneficial for the R. L.

Maynard whereas less stock wasted. Inventory control system is relay on LIFO and FIFO

system, where product manufacture in last but sale at their first. On other side product would be

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

manufacture at firstly that it will be sale out firstly. In R. L. Maynard inventory control system

is check periodical in specific time. Inventory control system is less expensive and beneficial

for an organisation.

P2 Various methods of management accounting reporting in R.L. Maynard Limited

Business Report

To,

Board of Directors,

R. L. Maynard Limited

Date: 20th April 2017

Subject: Different methods of management accounting reporting

Reporting to management about the companies financials is used to take suitable actions

towards the growth of the organization. These report helps R. L. Maynard to make decisions for

the future of the organization. Also, to access the financial nature of organization. It includes

findings with supporting evidences in the form of other reports. Some of these reports are:

Job cost report: job cost reports provides information about the status of a job that in

how much time it will get completed and also helps to figure out the time it will take to

finish the task from a cost and revenue perspective. Talking in context with construction

company like R. L. Maynard job cost report includes every cost incurred on the project

from its actual to standard cost (Abdel-Maksoud, Abdallah and Youssef, 2012). Through

job cost report a company can evaluate the job's profitability. This helps identify earning

areas of business.

Payroll report: A payroll report in the construction business of R. L. Maynard includes

calculation of overtime, job hour tracking, workers compensation, new hire reporting,

bonus pay, double-time pay, commission pay, sick pay, etc. It is basically related to the

payment for the services that are taken from the workers. Managing workers'

information is also a part of payroll report within workplace of R. L. Maynard .

3

is check periodical in specific time. Inventory control system is less expensive and beneficial

for an organisation.

P2 Various methods of management accounting reporting in R.L. Maynard Limited

Business Report

To,

Board of Directors,

R. L. Maynard Limited

Date: 20th April 2017

Subject: Different methods of management accounting reporting

Reporting to management about the companies financials is used to take suitable actions

towards the growth of the organization. These report helps R. L. Maynard to make decisions for

the future of the organization. Also, to access the financial nature of organization. It includes

findings with supporting evidences in the form of other reports. Some of these reports are:

Job cost report: job cost reports provides information about the status of a job that in

how much time it will get completed and also helps to figure out the time it will take to

finish the task from a cost and revenue perspective. Talking in context with construction

company like R. L. Maynard job cost report includes every cost incurred on the project

from its actual to standard cost (Abdel-Maksoud, Abdallah and Youssef, 2012). Through

job cost report a company can evaluate the job's profitability. This helps identify earning

areas of business.

Payroll report: A payroll report in the construction business of R. L. Maynard includes

calculation of overtime, job hour tracking, workers compensation, new hire reporting,

bonus pay, double-time pay, commission pay, sick pay, etc. It is basically related to the

payment for the services that are taken from the workers. Managing workers'

information is also a part of payroll report within workplace of R. L. Maynard .

3

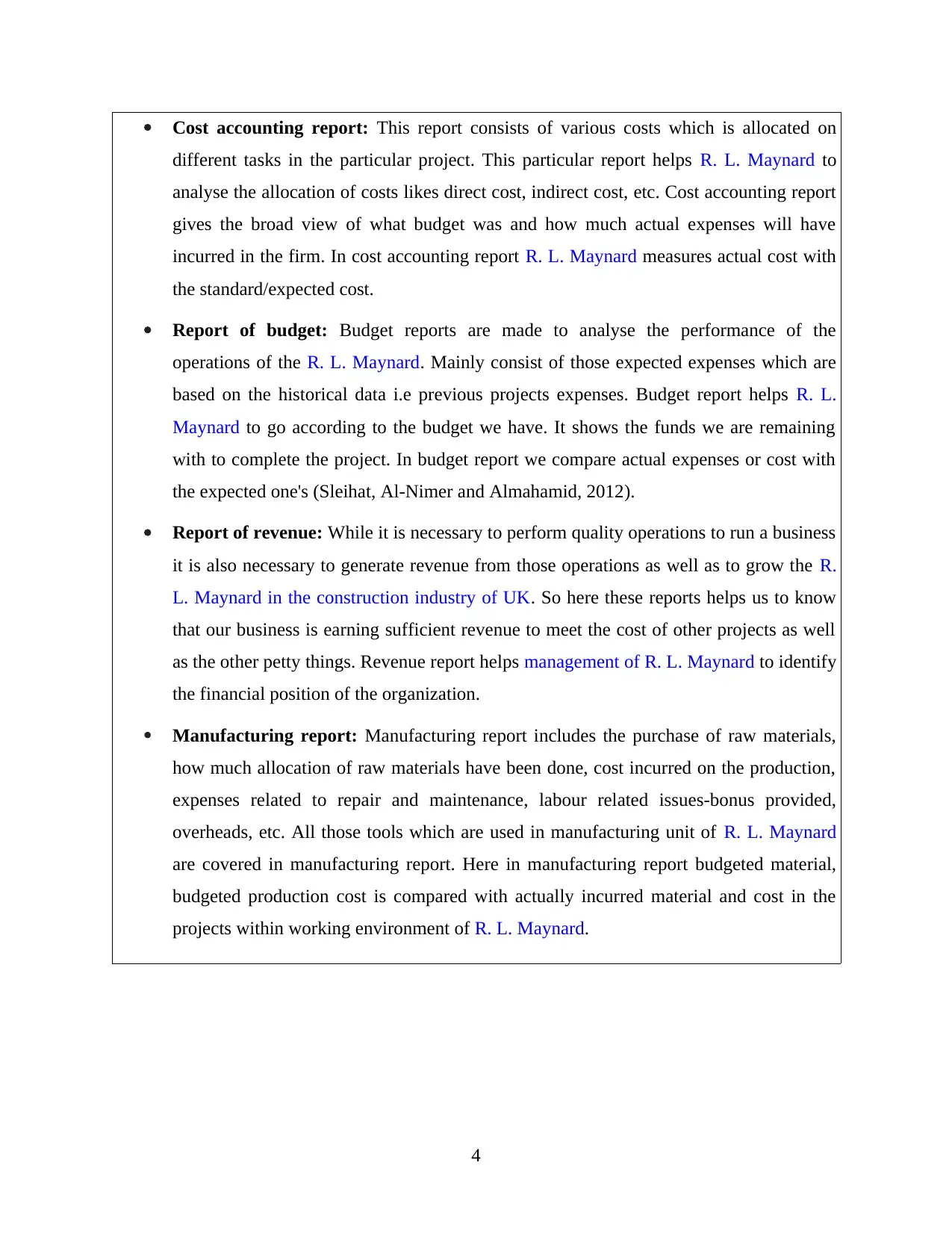

Cost accounting report: This report consists of various costs which is allocated on

different tasks in the particular project. This particular report helps R. L. Maynard to

analyse the allocation of costs likes direct cost, indirect cost, etc. Cost accounting report

gives the broad view of what budget was and how much actual expenses will have

incurred in the firm. In cost accounting report R. L. Maynard measures actual cost with

the standard/expected cost.

Report of budget: Budget reports are made to analyse the performance of the

operations of the R. L. Maynard. Mainly consist of those expected expenses which are

based on the historical data i.e previous projects expenses. Budget report helps R. L.

Maynard to go according to the budget we have. It shows the funds we are remaining

with to complete the project. In budget report we compare actual expenses or cost with

the expected one's (Sleihat, Al-Nimer and Almahamid, 2012).

Report of revenue: While it is necessary to perform quality operations to run a business

it is also necessary to generate revenue from those operations as well as to grow the R.

L. Maynard in the construction industry of UK. So here these reports helps us to know

that our business is earning sufficient revenue to meet the cost of other projects as well

as the other petty things. Revenue report helps management of R. L. Maynard to identify

the financial position of the organization.

Manufacturing report: Manufacturing report includes the purchase of raw materials,

how much allocation of raw materials have been done, cost incurred on the production,

expenses related to repair and maintenance, labour related issues-bonus provided,

overheads, etc. All those tools which are used in manufacturing unit of R. L. Maynard

are covered in manufacturing report. Here in manufacturing report budgeted material,

budgeted production cost is compared with actually incurred material and cost in the

projects within working environment of R. L. Maynard.

4

different tasks in the particular project. This particular report helps R. L. Maynard to

analyse the allocation of costs likes direct cost, indirect cost, etc. Cost accounting report

gives the broad view of what budget was and how much actual expenses will have

incurred in the firm. In cost accounting report R. L. Maynard measures actual cost with

the standard/expected cost.

Report of budget: Budget reports are made to analyse the performance of the

operations of the R. L. Maynard. Mainly consist of those expected expenses which are

based on the historical data i.e previous projects expenses. Budget report helps R. L.

Maynard to go according to the budget we have. It shows the funds we are remaining

with to complete the project. In budget report we compare actual expenses or cost with

the expected one's (Sleihat, Al-Nimer and Almahamid, 2012).

Report of revenue: While it is necessary to perform quality operations to run a business

it is also necessary to generate revenue from those operations as well as to grow the R.

L. Maynard in the construction industry of UK. So here these reports helps us to know

that our business is earning sufficient revenue to meet the cost of other projects as well

as the other petty things. Revenue report helps management of R. L. Maynard to identify

the financial position of the organization.

Manufacturing report: Manufacturing report includes the purchase of raw materials,

how much allocation of raw materials have been done, cost incurred on the production,

expenses related to repair and maintenance, labour related issues-bonus provided,

overheads, etc. All those tools which are used in manufacturing unit of R. L. Maynard

are covered in manufacturing report. Here in manufacturing report budgeted material,

budgeted production cost is compared with actually incurred material and cost in the

projects within working environment of R. L. Maynard.

4

TASK 2

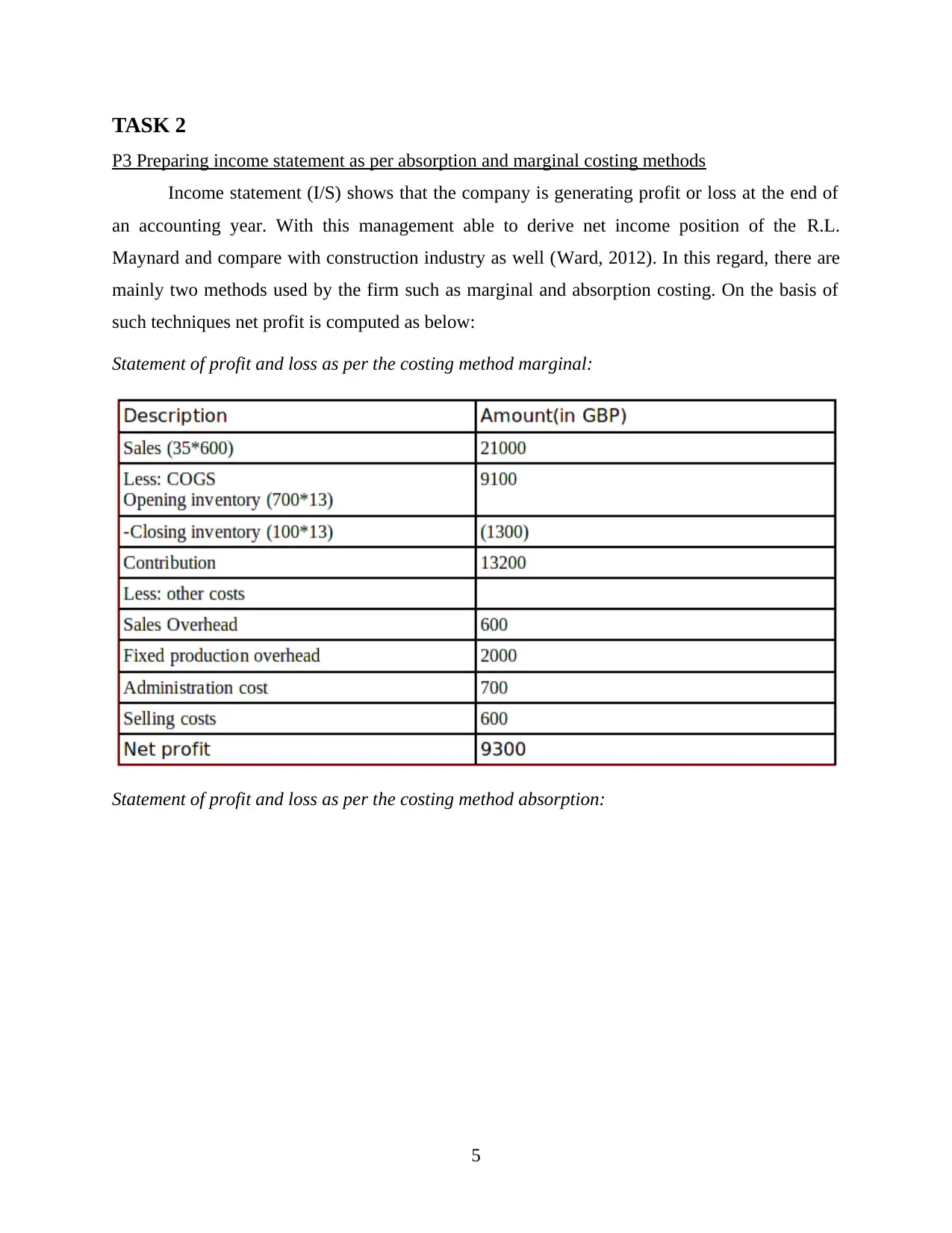

P3 Preparing income statement as per absorption and marginal costing methods

Income statement (I/S) shows that the company is generating profit or loss at the end of

an accounting year. With this management able to derive net income position of the R.L.

Maynard and compare with construction industry as well (Ward, 2012). In this regard, there are

mainly two methods used by the firm such as marginal and absorption costing. On the basis of

such techniques net profit is computed as below:

Statement of profit and loss as per the costing method marginal:

Statement of profit and loss as per the costing method absorption:

5

P3 Preparing income statement as per absorption and marginal costing methods

Income statement (I/S) shows that the company is generating profit or loss at the end of

an accounting year. With this management able to derive net income position of the R.L.

Maynard and compare with construction industry as well (Ward, 2012). In this regard, there are

mainly two methods used by the firm such as marginal and absorption costing. On the basis of

such techniques net profit is computed as below:

Statement of profit and loss as per the costing method marginal:

Statement of profit and loss as per the costing method absorption:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

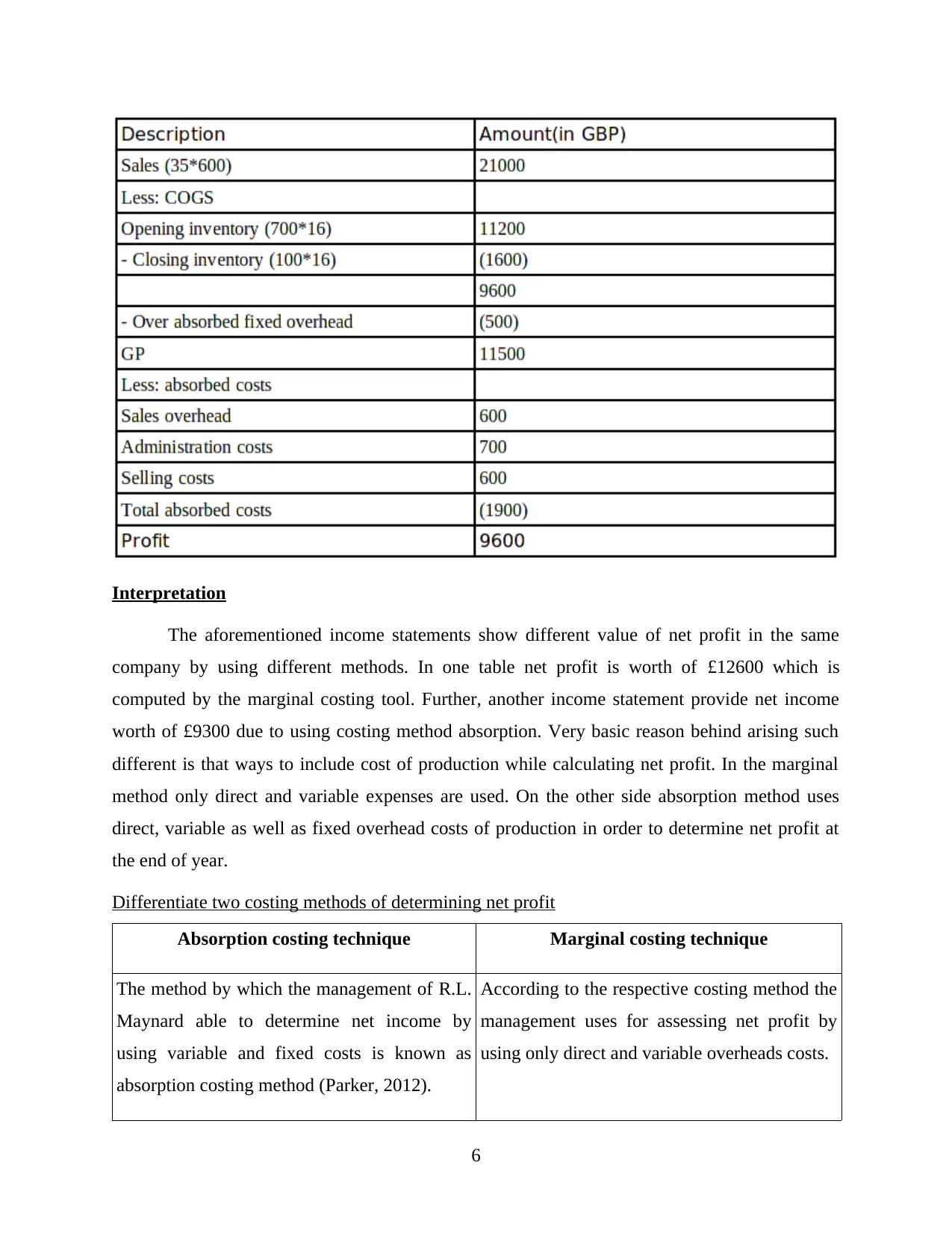

Interpretation

The aforementioned income statements show different value of net profit in the same

company by using different methods. In one table net profit is worth of £12600 which is

computed by the marginal costing tool. Further, another income statement provide net income

worth of £9300 due to using costing method absorption. Very basic reason behind arising such

different is that ways to include cost of production while calculating net profit. In the marginal

method only direct and variable expenses are used. On the other side absorption method uses

direct, variable as well as fixed overhead costs of production in order to determine net profit at

the end of year.

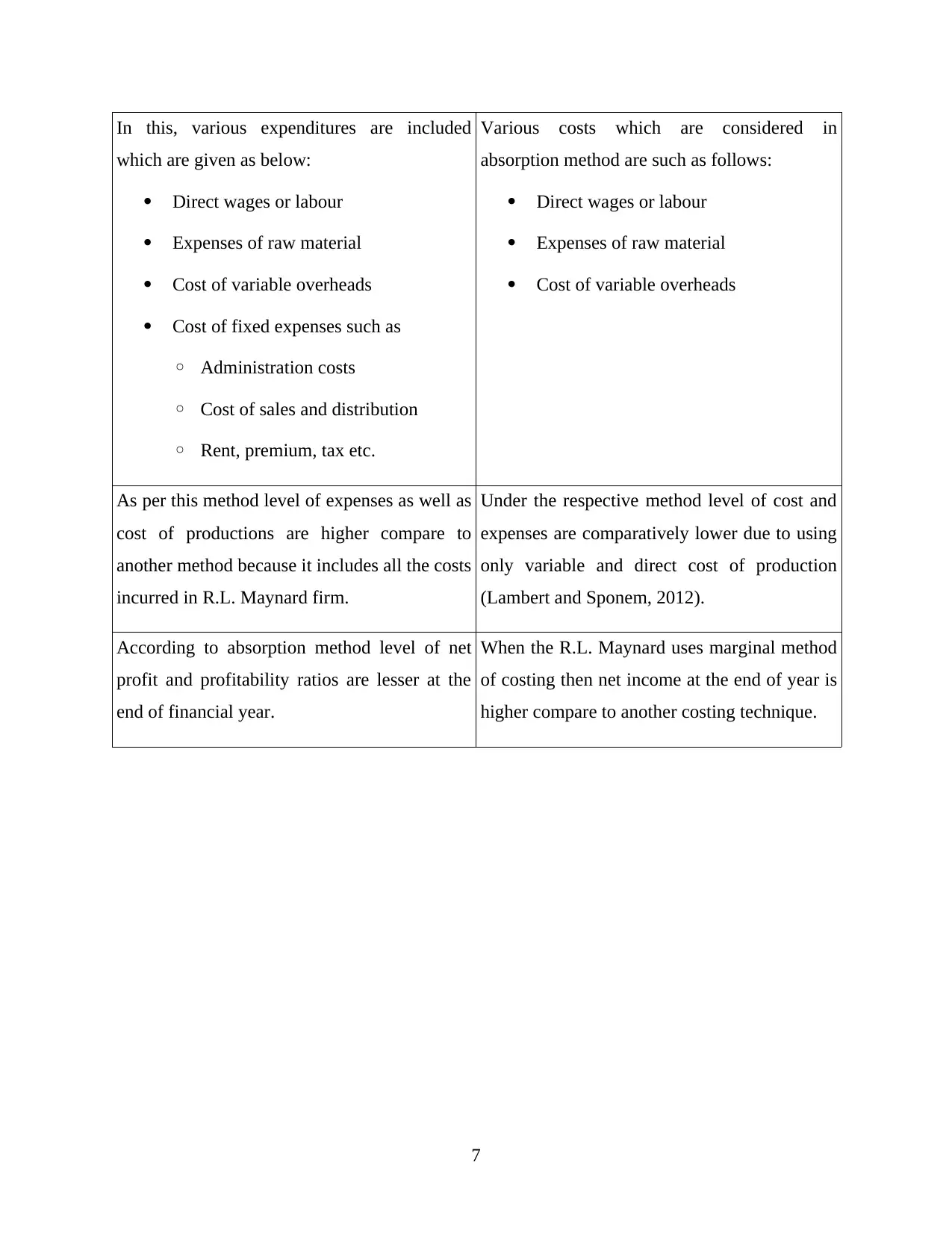

Differentiate two costing methods of determining net profit

Absorption costing technique Marginal costing technique

The method by which the management of R.L.

Maynard able to determine net income by

using variable and fixed costs is known as

absorption costing method (Parker, 2012).

According to the respective costing method the

management uses for assessing net profit by

using only direct and variable overheads costs.

6

The aforementioned income statements show different value of net profit in the same

company by using different methods. In one table net profit is worth of £12600 which is

computed by the marginal costing tool. Further, another income statement provide net income

worth of £9300 due to using costing method absorption. Very basic reason behind arising such

different is that ways to include cost of production while calculating net profit. In the marginal

method only direct and variable expenses are used. On the other side absorption method uses

direct, variable as well as fixed overhead costs of production in order to determine net profit at

the end of year.

Differentiate two costing methods of determining net profit

Absorption costing technique Marginal costing technique

The method by which the management of R.L.

Maynard able to determine net income by

using variable and fixed costs is known as

absorption costing method (Parker, 2012).

According to the respective costing method the

management uses for assessing net profit by

using only direct and variable overheads costs.

6

In this, various expenditures are included

which are given as below:

Direct wages or labour

Expenses of raw material

Cost of variable overheads

Cost of fixed expenses such as

◦ Administration costs

◦ Cost of sales and distribution

◦ Rent, premium, tax etc.

Various costs which are considered in

absorption method are such as follows:

Direct wages or labour

Expenses of raw material

Cost of variable overheads

As per this method level of expenses as well as

cost of productions are higher compare to

another method because it includes all the costs

incurred in R.L. Maynard firm.

Under the respective method level of cost and

expenses are comparatively lower due to using

only variable and direct cost of production

(Lambert and Sponem, 2012).

According to absorption method level of net

profit and profitability ratios are lesser at the

end of financial year.

When the R.L. Maynard uses marginal method

of costing then net income at the end of year is

higher compare to another costing technique.

7

which are given as below:

Direct wages or labour

Expenses of raw material

Cost of variable overheads

Cost of fixed expenses such as

◦ Administration costs

◦ Cost of sales and distribution

◦ Rent, premium, tax etc.

Various costs which are considered in

absorption method are such as follows:

Direct wages or labour

Expenses of raw material

Cost of variable overheads

As per this method level of expenses as well as

cost of productions are higher compare to

another method because it includes all the costs

incurred in R.L. Maynard firm.

Under the respective method level of cost and

expenses are comparatively lower due to using

only variable and direct cost of production

(Lambert and Sponem, 2012).

According to absorption method level of net

profit and profitability ratios are lesser at the

end of financial year.

When the R.L. Maynard uses marginal method

of costing then net income at the end of year is

higher compare to another costing technique.

7

TASK 3

P4 Benefits and disadvantages of various planning tools

Business Report

To,

Board of Directors,

R. L. Maynard Limited

Date: 20th April 2017

Subject: Different planning tools of budgetary control along with the

The business entity whether it operates in construction industry or any other needs to

make effective planning of finance, production or another function as well. In context to this,

financial plan plays a key important role in the business environment which helps to the

entrepreneur in order to maximize level of profit. There are different kinds of tools and

techniques of planning are very helpful and adopted by the selected construction company

(Bebbington and Thomson, 2013). The tools are such as budget, financial or investment

appraisal tools as well as financial ratio analysis which are described as below:

Budget: Key planning tool used by the company such as R.L. Maynard is budget which

is the most helpful in order to determine values of financial data for further accounting period.

There are different types of techniques are used for prepare budgets which are such as zero-

based, incremental, traditional etc. While using different budgeting methods values or outcomes

are differ. The reason is that one method takes base value which is past financial data, another

takes zero value and start without analysing past informations. In this regard, there are various

kinds of budgets are to be prepared for make effectual plan which are like as cash, sales,

production, material purchase, material usage etc. Among them cash and sales budget along

with example are shown below:

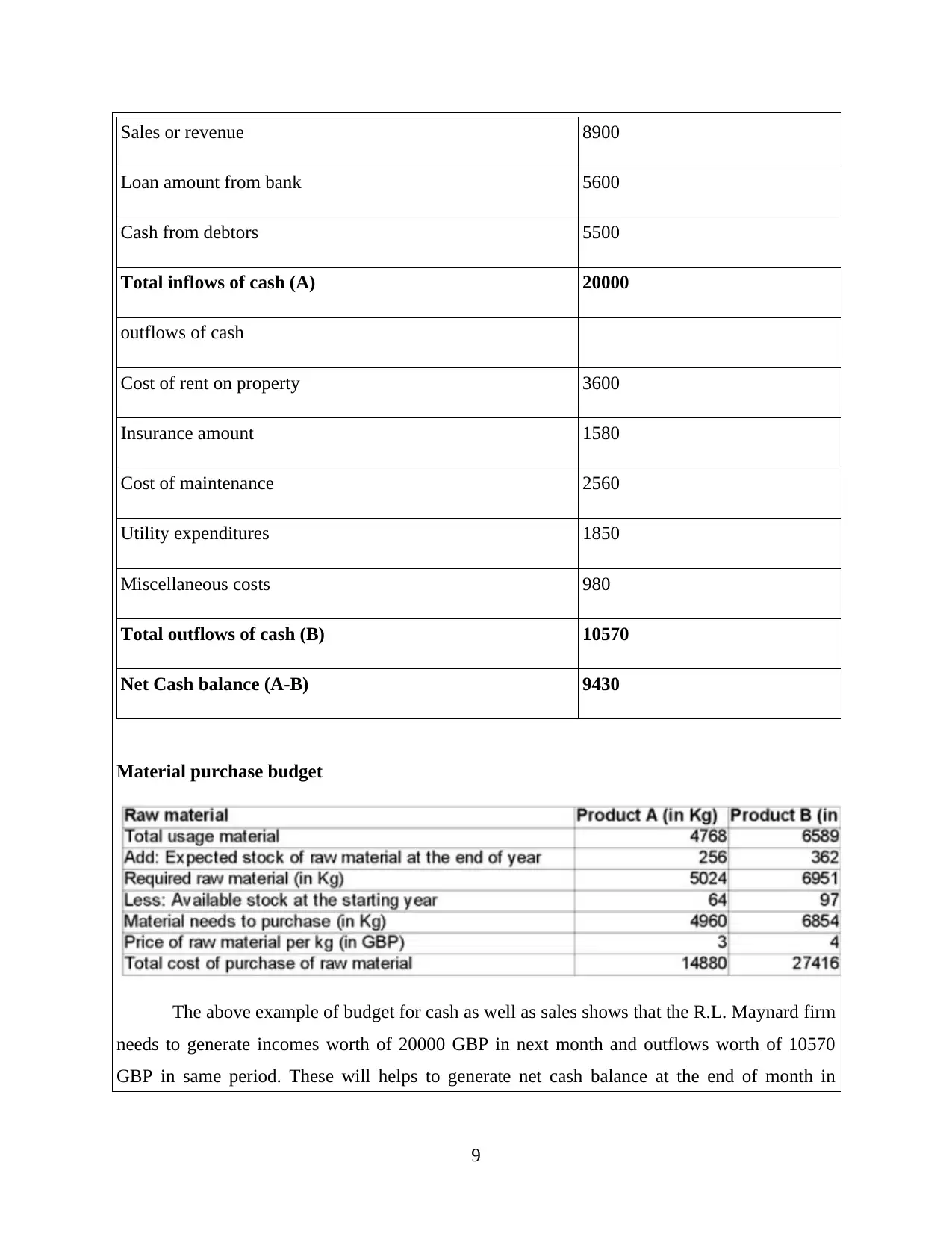

Budget for cash amount

Particulars Amount (in GBP)

Inflows of cash

8

P4 Benefits and disadvantages of various planning tools

Business Report

To,

Board of Directors,

R. L. Maynard Limited

Date: 20th April 2017

Subject: Different planning tools of budgetary control along with the

The business entity whether it operates in construction industry or any other needs to

make effective planning of finance, production or another function as well. In context to this,

financial plan plays a key important role in the business environment which helps to the

entrepreneur in order to maximize level of profit. There are different kinds of tools and

techniques of planning are very helpful and adopted by the selected construction company

(Bebbington and Thomson, 2013). The tools are such as budget, financial or investment

appraisal tools as well as financial ratio analysis which are described as below:

Budget: Key planning tool used by the company such as R.L. Maynard is budget which

is the most helpful in order to determine values of financial data for further accounting period.

There are different types of techniques are used for prepare budgets which are such as zero-

based, incremental, traditional etc. While using different budgeting methods values or outcomes

are differ. The reason is that one method takes base value which is past financial data, another

takes zero value and start without analysing past informations. In this regard, there are various

kinds of budgets are to be prepared for make effectual plan which are like as cash, sales,

production, material purchase, material usage etc. Among them cash and sales budget along

with example are shown below:

Budget for cash amount

Particulars Amount (in GBP)

Inflows of cash

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Sales or revenue 8900

Loan amount from bank 5600

Cash from debtors 5500

Total inflows of cash (A) 20000

outflows of cash

Cost of rent on property 3600

Insurance amount 1580

Cost of maintenance 2560

Utility expenditures 1850

Miscellaneous costs 980

Total outflows of cash (B) 10570

Net Cash balance (A-B) 9430

Material purchase budget

The above example of budget for cash as well as sales shows that the R.L. Maynard firm

needs to generate incomes worth of 20000 GBP in next month and outflows worth of 10570

GBP in same period. These will helps to generate net cash balance at the end of month in

9

Loan amount from bank 5600

Cash from debtors 5500

Total inflows of cash (A) 20000

outflows of cash

Cost of rent on property 3600

Insurance amount 1580

Cost of maintenance 2560

Utility expenditures 1850

Miscellaneous costs 980

Total outflows of cash (B) 10570

Net Cash balance (A-B) 9430

Material purchase budget

The above example of budget for cash as well as sales shows that the R.L. Maynard firm

needs to generate incomes worth of 20000 GBP in next month and outflows worth of 10570

GBP in same period. These will helps to generate net cash balance at the end of month in

9

positive manner which will 9430 GBP. Apart from this it requires to produce at least 18000

number of units and sell them at the price of 23 GBP by which it able to generate sales worth of

414000 GBP.

Benefits:

Very key benefit of the budgeting is that to estimate or forecast financial data and

informations for the current as well as future month or period of accounting.

It helps to allocate and distribute available financial resource in adequately and

effectually manner to make the firm highly profitable (Pondeville, Swaen and De

Rongé, 2013).

By this it able to find lack of costs as well as obstacles related to finance in the firm.

Further, can take corrective actions against it.

Moreover, budget is the most helpful for R.L. Maynard in order to improve cash balance

at the end of specific period of time.

It helps in order to manage risk of firm as well as control over the extra expenses which

incurred in production or operation process. Helpful for managers of the firm in order to make effectual plan for maximize profit and

minimize cost level in effectual way.

Disadvantages:

To make or prepare different types of budgets company such as R.L. Maynard needs to

appoint highly skilled employee or finance manager who charges higher cost which

leads to increase expenses.

Further, there are lack of accuracy in data because it is overall based on assumptions and

past data as well.

In the firm when there is an experienced person making budget every year then it leads

to create manipulation in accounting informations (Chenhall and Moers, 2015).

This method is very lengthy and time consuming for estimate data for the future as well

as it is costly tool.

10

number of units and sell them at the price of 23 GBP by which it able to generate sales worth of

414000 GBP.

Benefits:

Very key benefit of the budgeting is that to estimate or forecast financial data and

informations for the current as well as future month or period of accounting.

It helps to allocate and distribute available financial resource in adequately and

effectually manner to make the firm highly profitable (Pondeville, Swaen and De

Rongé, 2013).

By this it able to find lack of costs as well as obstacles related to finance in the firm.

Further, can take corrective actions against it.

Moreover, budget is the most helpful for R.L. Maynard in order to improve cash balance

at the end of specific period of time.

It helps in order to manage risk of firm as well as control over the extra expenses which

incurred in production or operation process. Helpful for managers of the firm in order to make effectual plan for maximize profit and

minimize cost level in effectual way.

Disadvantages:

To make or prepare different types of budgets company such as R.L. Maynard needs to

appoint highly skilled employee or finance manager who charges higher cost which

leads to increase expenses.

Further, there are lack of accuracy in data because it is overall based on assumptions and

past data as well.

In the firm when there is an experienced person making budget every year then it leads

to create manipulation in accounting informations (Chenhall and Moers, 2015).

This method is very lengthy and time consuming for estimate data for the future as well

as it is costly tool.

10

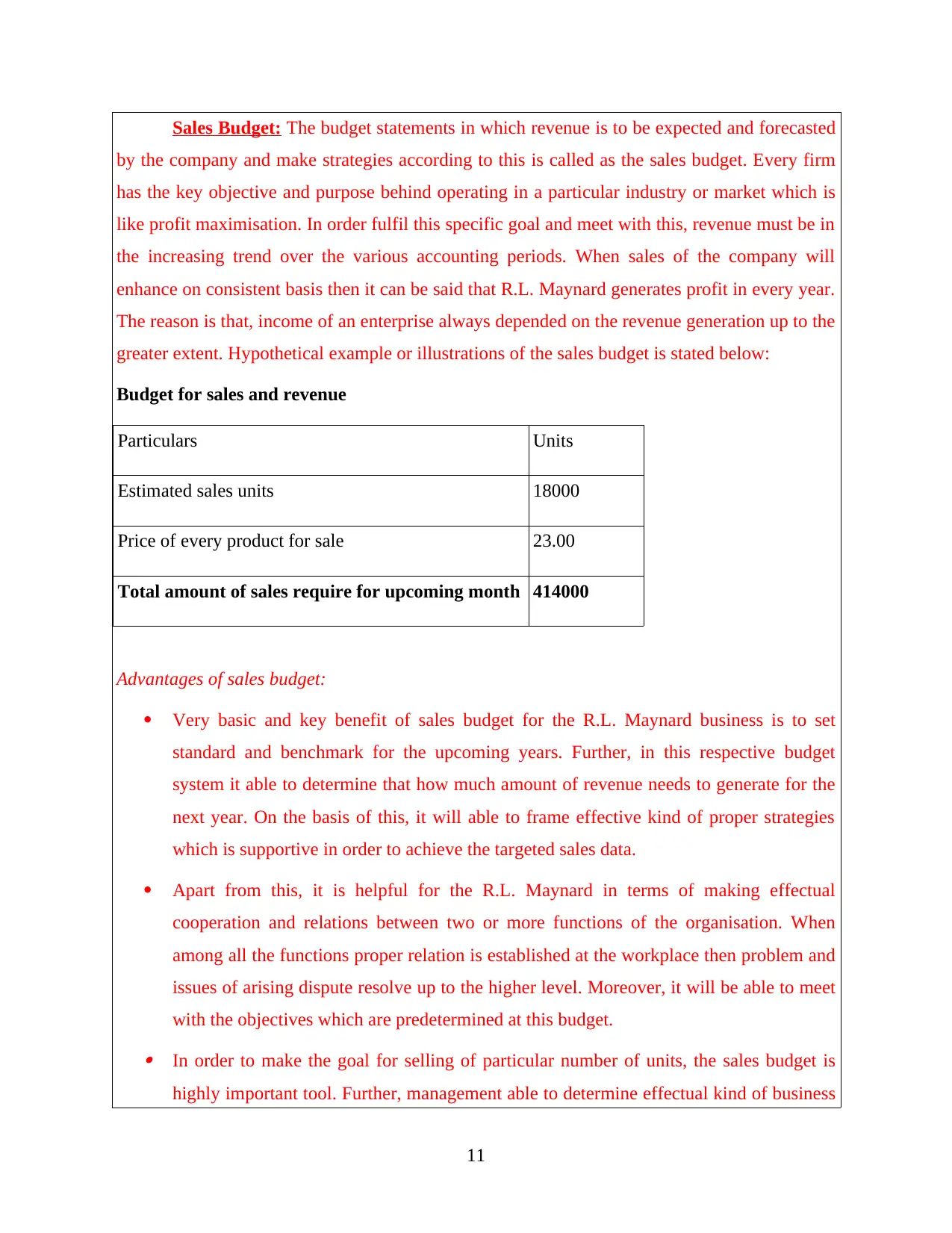

Sales Budget: The budget statements in which revenue is to be expected and forecasted

by the company and make strategies according to this is called as the sales budget. Every firm

has the key objective and purpose behind operating in a particular industry or market which is

like profit maximisation. In order fulfil this specific goal and meet with this, revenue must be in

the increasing trend over the various accounting periods. When sales of the company will

enhance on consistent basis then it can be said that R.L. Maynard generates profit in every year.

The reason is that, income of an enterprise always depended on the revenue generation up to the

greater extent. Hypothetical example or illustrations of the sales budget is stated below:

Budget for sales and revenue

Particulars Units

Estimated sales units 18000

Price of every product for sale 23.00

Total amount of sales require for upcoming month 414000

Advantages of sales budget:

Very basic and key benefit of sales budget for the R.L. Maynard business is to set

standard and benchmark for the upcoming years. Further, in this respective budget

system it able to determine that how much amount of revenue needs to generate for the

next year. On the basis of this, it will able to frame effective kind of proper strategies

which is supportive in order to achieve the targeted sales data.

Apart from this, it is helpful for the R.L. Maynard in terms of making effectual

cooperation and relations between two or more functions of the organisation. When

among all the functions proper relation is established at the workplace then problem and

issues of arising dispute resolve up to the higher level. Moreover, it will be able to meet

with the objectives which are predetermined at this budget. In order to make the goal for selling of particular number of units, the sales budget is

highly important tool. Further, management able to determine effectual kind of business

11

by the company and make strategies according to this is called as the sales budget. Every firm

has the key objective and purpose behind operating in a particular industry or market which is

like profit maximisation. In order fulfil this specific goal and meet with this, revenue must be in

the increasing trend over the various accounting periods. When sales of the company will

enhance on consistent basis then it can be said that R.L. Maynard generates profit in every year.

The reason is that, income of an enterprise always depended on the revenue generation up to the

greater extent. Hypothetical example or illustrations of the sales budget is stated below:

Budget for sales and revenue

Particulars Units

Estimated sales units 18000

Price of every product for sale 23.00

Total amount of sales require for upcoming month 414000

Advantages of sales budget:

Very basic and key benefit of sales budget for the R.L. Maynard business is to set

standard and benchmark for the upcoming years. Further, in this respective budget

system it able to determine that how much amount of revenue needs to generate for the

next year. On the basis of this, it will able to frame effective kind of proper strategies

which is supportive in order to achieve the targeted sales data.

Apart from this, it is helpful for the R.L. Maynard in terms of making effectual

cooperation and relations between two or more functions of the organisation. When

among all the functions proper relation is established at the workplace then problem and

issues of arising dispute resolve up to the higher level. Moreover, it will be able to meet

with the objectives which are predetermined at this budget. In order to make the goal for selling of particular number of units, the sales budget is

highly important tool. Further, management able to determine effectual kind of business

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

tactics and strategies which are suitable for it.

Disadvantages of sales budget:

The sales budget is made on the basis of past performance, predictions as well as

assumptions. Further, management predict wrong value and manufacture determined

number of volume which lead to reduce business performance in the overall industry of

construction.

The function of sales budget lead to create negative impact on the overall company

because of having knowledge and determination about the next financial year in proper

manner.

Along with this, if sales units and volume of the products and services are estimated in

the wrong ways or higher and lower number then it will hamper the smooth functioning

of the R.L. Maynard. Therefore, it can be said that, inventory of the entity affects which

lead to create impact on the revenue and profitability.

Production Budget: It is another tool of controlling and managing over the budgetary

system of the organisation where number of units are predetermined bt the R.L. Maynard.

Under the production budget, management able to forecast that how much number of houses

and buildings need to construct for the upcoming. Generally it is made after considering all the

data of past financial statements and performance. Further, sometimes level of the next

production units are predetermined with the help of doing proper and effectual market research.

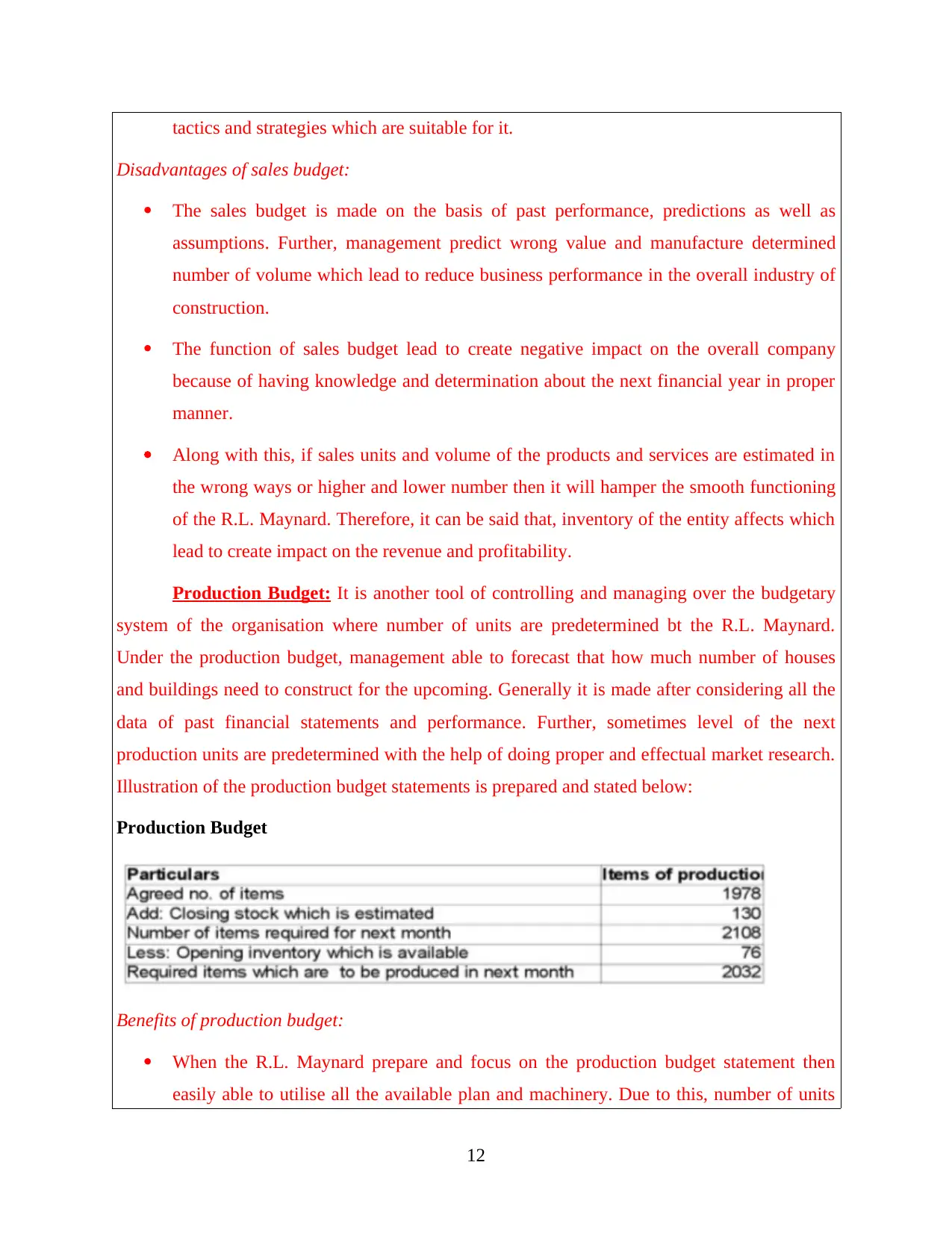

Illustration of the production budget statements is prepared and stated below:

Production Budget

Benefits of production budget:

When the R.L. Maynard prepare and focus on the production budget statement then

easily able to utilise all the available plan and machinery. Due to this, number of units

12

Disadvantages of sales budget:

The sales budget is made on the basis of past performance, predictions as well as

assumptions. Further, management predict wrong value and manufacture determined

number of volume which lead to reduce business performance in the overall industry of

construction.

The function of sales budget lead to create negative impact on the overall company

because of having knowledge and determination about the next financial year in proper

manner.

Along with this, if sales units and volume of the products and services are estimated in

the wrong ways or higher and lower number then it will hamper the smooth functioning

of the R.L. Maynard. Therefore, it can be said that, inventory of the entity affects which

lead to create impact on the revenue and profitability.

Production Budget: It is another tool of controlling and managing over the budgetary

system of the organisation where number of units are predetermined bt the R.L. Maynard.

Under the production budget, management able to forecast that how much number of houses

and buildings need to construct for the upcoming. Generally it is made after considering all the

data of past financial statements and performance. Further, sometimes level of the next

production units are predetermined with the help of doing proper and effectual market research.

Illustration of the production budget statements is prepared and stated below:

Production Budget

Benefits of production budget:

When the R.L. Maynard prepare and focus on the production budget statement then

easily able to utilise all the available plan and machinery. Due to this, number of units

12

will be enhance up to the higher extent and reduce the total cost of production and

operation at the workplace.

After setting and determining specific number of units, the R.L. Maynard able to

increase labour utilisation power which helps to enhance productivity.

In addition to this, expenses of the operation and production department will be declined

up to the greater level with the help of such mentioned budget statement. When it will able to use production budget in effectual manner then stock or inventory

level of R.L. Maynard reduced which is sign of revenue enhancing;.

Limitations of production budget:

Number of production units for the future financial year are to be predetermined with

the help of market research and predictions of the demand level. When the products are

to be produced accordingly then stock level affects in different ways like favourable or

adverse. In case, market researcher forecast that demand will be increased in the future

year but due to some reason demand decline. Further, because of wrong assumptions

stock level will increase at the workplace which lead to decline the revenue generation

capability at the end of year.

Along with this, production volume determines by making several market prediction and

due to this R.L. Maynard not able to make effectual kind of business strategies for

achieving targets.

In this, management of the selected entity focus on the past trend of demand and

production units also. Further, it is not compulsory that R.L. Maynard will generate or

construct same volume of the products and houses. Therefore, prediction can be

considered wrong which lead to reduce the effective business decision making.

P5 Analysis of management accounting systems that how R.L. Maynard firm respond to

financial problems

Business Report

13

operation at the workplace.

After setting and determining specific number of units, the R.L. Maynard able to

increase labour utilisation power which helps to enhance productivity.

In addition to this, expenses of the operation and production department will be declined

up to the greater level with the help of such mentioned budget statement. When it will able to use production budget in effectual manner then stock or inventory

level of R.L. Maynard reduced which is sign of revenue enhancing;.

Limitations of production budget:

Number of production units for the future financial year are to be predetermined with

the help of market research and predictions of the demand level. When the products are

to be produced accordingly then stock level affects in different ways like favourable or

adverse. In case, market researcher forecast that demand will be increased in the future

year but due to some reason demand decline. Further, because of wrong assumptions

stock level will increase at the workplace which lead to decline the revenue generation

capability at the end of year.

Along with this, production volume determines by making several market prediction and

due to this R.L. Maynard not able to make effectual kind of business strategies for

achieving targets.

In this, management of the selected entity focus on the past trend of demand and

production units also. Further, it is not compulsory that R.L. Maynard will generate or

construct same volume of the products and houses. Therefore, prediction can be

considered wrong which lead to reduce the effective business decision making.

P5 Analysis of management accounting systems that how R.L. Maynard firm respond to

financial problems

Business Report

13

To,

Board of Directors,

R. L. Maynard Limited

Date: 20th April 2017

Subject: Different systems of management accounting reporting

In each and every enterprise there are different types of problems and obstacles related

to finance are occurred and influence business performance in adverse manner. In order combat

financial related problems and constraints there are different management accounting systems

are used by the R.L. Maynard which are enumerated below:

Throughput accounting: It is one the most used accounting system which is more or

less related to the raw material which are needs to produce finished goods. The system is not

that much relies with the cost and expense factor incurred in operation process. In this raw

materials are utilized in proper as well as highly effectual manner where R.L. Maynard can

construct building by using high quality of materials (Sleihat, Al-Nimer and Almahamid, 2012).

Here respective business entity able to use the raw products at the better way and can insist the

production process in order to utilize such material in effectual manner. By this, materials will

be uses in appropriate way and constraint of reducing efficiency of the firm will be overcome.

Effective utilization of raw material directly impact on the productivity and efficiency of the

enterprise in the construction industry.

Lean accounting system: The system of management accounting i.e. lean accounting is

used by the entrepreneur in order to eliminate extra expenses which creates more burden on the

firm and reduce profit level. When the cost of products and services is to be reduce then it will

directly affect to the financial position in very positive manner. Along with this, the respective

accounting approach is highly used by the firm which helps to eliminate extra cost as well as

wastage products and services occurs in operation process. When problems such as incurring

more miscellaneous expenditures, enhance wastage etc. then such system is useful for R.L.

Maynard (Management Accounting – Introduction, 2017). Further, it can be said that the system

is help to increase efficiency and overcome financial problems.

Transfer pricing: A price on which the parent company sell processed and finished

14

Board of Directors,

R. L. Maynard Limited

Date: 20th April 2017

Subject: Different systems of management accounting reporting

In each and every enterprise there are different types of problems and obstacles related

to finance are occurred and influence business performance in adverse manner. In order combat

financial related problems and constraints there are different management accounting systems

are used by the R.L. Maynard which are enumerated below:

Throughput accounting: It is one the most used accounting system which is more or

less related to the raw material which are needs to produce finished goods. The system is not

that much relies with the cost and expense factor incurred in operation process. In this raw

materials are utilized in proper as well as highly effectual manner where R.L. Maynard can

construct building by using high quality of materials (Sleihat, Al-Nimer and Almahamid, 2012).

Here respective business entity able to use the raw products at the better way and can insist the

production process in order to utilize such material in effectual manner. By this, materials will

be uses in appropriate way and constraint of reducing efficiency of the firm will be overcome.

Effective utilization of raw material directly impact on the productivity and efficiency of the

enterprise in the construction industry.

Lean accounting system: The system of management accounting i.e. lean accounting is

used by the entrepreneur in order to eliminate extra expenses which creates more burden on the

firm and reduce profit level. When the cost of products and services is to be reduce then it will

directly affect to the financial position in very positive manner. Along with this, the respective

accounting approach is highly used by the firm which helps to eliminate extra cost as well as

wastage products and services occurs in operation process. When problems such as incurring

more miscellaneous expenditures, enhance wastage etc. then such system is useful for R.L.

Maynard (Management Accounting – Introduction, 2017). Further, it can be said that the system

is help to increase efficiency and overcome financial problems.

Transfer pricing: A price on which the parent company sell processed and finished

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

products and services to its own subsidiary business entity is known as transfer price. When the

R.L. Maynard purchase raw material and products from the parent company then it will allow at

the low cost compare to another firms. Further, it helps to reduce total cost of purchasing raw

materials and impact on the business performance in positive way. Financial sound of an

enterprise is depends on the cost and expenses which are incurred at the operational process.

With help of lean accounting the R.L. Maynard able to reduce the extra and unused cost which

lead to enhance level of sales and revenue at the end of an accounting year. Ultimately financial

problem of enhancing revenue and profit will be raise in highly appropriate way.

Budgetary control: Moreover, another management accounting system to reduce

financial problems is budgetary control where the manager of R.L. Maynard utilizes its raw

material by analysing budget. In the budget if there are inflows are higher compare to outflows

then it will take decisions in that accordance. Along with this, it helps to analyse business

performance by comparing actual results and estimated financial data. If it found that there are

adequate financial resource are available then it will make strategies in order to that. Further, if

business performance is not sound and it requires more capital, then formulate strategies that

how to raise fund (Venkatesh, 2016). Hence, it can be clearly identified that these all the

systems of management accounting are helps to R.L. Maynard in order to combat shortfalls and

eliminate financial obstacles up to greater level.

CONCLUSION

From the above management accounting report it has been assessed that in the costing

there are two methods are used by R.L. Maynard Limited in order to determine net profit and

prepare income statement as well. Both the methods provide different value of net profit at the

end of particular period of time. Further, it can be concluded that management accounting

systems such as throughput, cost, lean, inventory, transfer pricing etc. helps to R.L. Maynard

Limited for reducing financial problems which sometimes occur in the entity. Moreover, budget,

financial techniques as well as ratio analysis these three tools are very useful for the company

which helps to make effectual financial plan for current and future as well.

15

R.L. Maynard purchase raw material and products from the parent company then it will allow at

the low cost compare to another firms. Further, it helps to reduce total cost of purchasing raw

materials and impact on the business performance in positive way. Financial sound of an

enterprise is depends on the cost and expenses which are incurred at the operational process.

With help of lean accounting the R.L. Maynard able to reduce the extra and unused cost which

lead to enhance level of sales and revenue at the end of an accounting year. Ultimately financial

problem of enhancing revenue and profit will be raise in highly appropriate way.

Budgetary control: Moreover, another management accounting system to reduce

financial problems is budgetary control where the manager of R.L. Maynard utilizes its raw

material by analysing budget. In the budget if there are inflows are higher compare to outflows

then it will take decisions in that accordance. Along with this, it helps to analyse business

performance by comparing actual results and estimated financial data. If it found that there are

adequate financial resource are available then it will make strategies in order to that. Further, if

business performance is not sound and it requires more capital, then formulate strategies that

how to raise fund (Venkatesh, 2016). Hence, it can be clearly identified that these all the

systems of management accounting are helps to R.L. Maynard in order to combat shortfalls and

eliminate financial obstacles up to greater level.

CONCLUSION

From the above management accounting report it has been assessed that in the costing

there are two methods are used by R.L. Maynard Limited in order to determine net profit and

prepare income statement as well. Both the methods provide different value of net profit at the

end of particular period of time. Further, it can be concluded that management accounting

systems such as throughput, cost, lean, inventory, transfer pricing etc. helps to R.L. Maynard

Limited for reducing financial problems which sometimes occur in the entity. Moreover, budget,

financial techniques as well as ratio analysis these three tools are very useful for the company

which helps to make effectual financial plan for current and future as well.

15

16

17

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.