Detailed Management Accounting Report for Tech (UK) Limited

VerifiedAdded on 2024/05/21

|19

|4559

|220

Report

AI Summary

This management accounting report analyzes the financial situation of Tech (UK) Limited, a retail business facing losses in the mobile telephone and gadget market. The report distinguishes between management and financial accounting, emphasizing the importance of management accounting information for decision-making. It covers key areas such as future forecasting, investment return analysis, variance analysis, cash flow management, and productivity improvement. Different cost accounting systems (actual, normal, and standard costing) and inventory management systems (FIFO, LIFO, ABC analysis) are discussed. The report also presents various managerial accounting reports, including external, internal, and enterprise reports. It further includes income statements and an analysis of the Balanced Scorecard approach for addressing Tech's financial problems, comparing it to other management accounting approaches. Desklib provides access to this and other solved assignments for students.

Management accounting report for Tech (UK) Limited

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................3

Task 1..........................................................................................................................................................4

a) Explanation of management accounting and the essential requirements of management accounting

(P1, M1 and D1).......................................................................................................................................4

b) Presenting financial information.........................................................................................................8

Task 2..........................................................................................................................................................9

P3: You are required to prepare income statements (M2, D2)................................................................9

Task 3........................................................................................................................................................13

P4: In report including (M3, D3)............................................................................................................13

Task 4........................................................................................................................................................16

Referring to Tech’s current financial situation, explain ways by which the Balanced Scorecard

approach suggested by the auditors can be used to respond its financial problem and compare this

approach to another management accounting approach used in another organisation of your choice

...............................................................................................................................................................16

Conclusion.................................................................................................................................................18

Bibliography...............................................................................................................................................19

2

Introduction.................................................................................................................................................3

Task 1..........................................................................................................................................................4

a) Explanation of management accounting and the essential requirements of management accounting

(P1, M1 and D1).......................................................................................................................................4

b) Presenting financial information.........................................................................................................8

Task 2..........................................................................................................................................................9

P3: You are required to prepare income statements (M2, D2)................................................................9

Task 3........................................................................................................................................................13

P4: In report including (M3, D3)............................................................................................................13

Task 4........................................................................................................................................................16

Referring to Tech’s current financial situation, explain ways by which the Balanced Scorecard

approach suggested by the auditors can be used to respond its financial problem and compare this

approach to another management accounting approach used in another organisation of your choice

...............................................................................................................................................................16

Conclusion.................................................................................................................................................18

Bibliography...............................................................................................................................................19

2

Introduction:

Tech (UK) Limited is in huge losses doing business in mobile telephone and other carry-on

gadgets in UK on retail basis. The current situation of the company that is being reported by the

managers but there is lack of financial and information due to which the decision making is

getting affected. A report to evaluate such financial information is to be made where the use of

Management Accounting system, management Accounting report, balanced scorecard approach,

ABC analysis, variance analysis has to be reported to the team. Here is the brief report of all such

requirement for the company.

3

Tech (UK) Limited is in huge losses doing business in mobile telephone and other carry-on

gadgets in UK on retail basis. The current situation of the company that is being reported by the

managers but there is lack of financial and information due to which the decision making is

getting affected. A report to evaluate such financial information is to be made where the use of

Management Accounting system, management Accounting report, balanced scorecard approach,

ABC analysis, variance analysis has to be reported to the team. Here is the brief report of all such

requirement for the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1:

a) Explanation of management accounting and the essential requirements of management

accounting (P1, M1 and D1):

I. Distinguishing Management Accounting from Financial Accounting.

The preparation of financial information and providing such information to various business

managers so that such information can help them in making decision is called as Management

Accounting. Management Accounting reports and Management Accounting prepares is for the

internal management team. Management Accounting provides the users with the where position

of the company and the user here at the part of the internal team. The purpose behind

Management Accounting report is to help to management and the various departments so that we

can provide them various result of their department for the Welfare of the company. (Vitez,

2018).

Financial accounting reports the outsiders of the company that are investors, suppliers etc. to

show their company’s actual position to them. Particularly every year financial accounting

reports have to be generated as they are compulsory as per the requirement of law. For

preparation of financial accounting reports various accounting standards in accounting policies

have to be kept in mind and the financial reports shall be complied with all such requirements.

(Vitez, 2018)

II. The importance of management accounting information as a decision making tool for

department managers.

These are discussed below:

Future forecasting – accounting systems helps in deciding the future while considering decision

making. (Vitez, 2018). Future forecasting is very important for a business as such forecasting

helps in analysing various reports and provides what actions the company should take in the

future so that such decisions are fruitful for the company. Management accounting report helps

in making in forecasting of the future and helps the managers to make decisions regarding the

4

a) Explanation of management accounting and the essential requirements of management

accounting (P1, M1 and D1):

I. Distinguishing Management Accounting from Financial Accounting.

The preparation of financial information and providing such information to various business

managers so that such information can help them in making decision is called as Management

Accounting. Management Accounting reports and Management Accounting prepares is for the

internal management team. Management Accounting provides the users with the where position

of the company and the user here at the part of the internal team. The purpose behind

Management Accounting report is to help to management and the various departments so that we

can provide them various result of their department for the Welfare of the company. (Vitez,

2018).

Financial accounting reports the outsiders of the company that are investors, suppliers etc. to

show their company’s actual position to them. Particularly every year financial accounting

reports have to be generated as they are compulsory as per the requirement of law. For

preparation of financial accounting reports various accounting standards in accounting policies

have to be kept in mind and the financial reports shall be complied with all such requirements.

(Vitez, 2018)

II. The importance of management accounting information as a decision making tool for

department managers.

These are discussed below:

Future forecasting – accounting systems helps in deciding the future while considering decision

making. (Vitez, 2018). Future forecasting is very important for a business as such forecasting

helps in analysing various reports and provides what actions the company should take in the

future so that such decisions are fruitful for the company. Management accounting report helps

in making in forecasting of the future and helps the managers to make decisions regarding the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business. With the help of past results and trend analysis the managers can forecast the future

and such forecasted future is helpful for them in decision making.

Analyses investment return- For the management to make a decision which involves heavy

investment, the rate of return for such investment has to be calculated, so that the company can

analyse weather such investment is beneficial for the company or not. Not only this when there

are more than 2 investment that the company has to do, it helps in calculating rate of return of all

such investments available and provides the managers with the best. Rate of return the amount of

earnings that the company will be provided with when the organisation invests in the investment.

(mishra, 2018)

Analyses in variances- It is not always correct what has been predicted by the management and

what have been the actual results. The difference between the two gives the rise to variances.

Search variances are identified by the management accounting system and have corrected there

by the managers. Variances can be of two types that are positive variances and negative

variances. The management accounting system takes the advantage of the positive variances and

corrects the negative variances. There are various analytical techniques through with the

variances can be identified and corrected. Search techniques are part of management accounting

system and Management Accounting system help them in identifying the variances and to help

them in making decisions.

Aid in decision making process - For a production manager and production team it is the most

difficult to whether purchase or produce equipment. Such decisions are highly evaluated by the

company so as to ensure that the most out of the list can be taken by the company. Considering

the cost of both of the proposals is necessary for the company before making such evaluation as

what to consider. (mishra, 2018)

For evaluating the cost of both the proposal Management Accounting system is highly

recommended and is found most beneficial for the entities. One has to understand the

management accounting system and its policies and principles prove it becomes very easy for the

user to evaluate to proposal of making the products at home or buying it from outside. So as to

take the decision of making it or buying it management accounting system are very helpful.

(mishra, 2018)

5

and such forecasted future is helpful for them in decision making.

Analyses investment return- For the management to make a decision which involves heavy

investment, the rate of return for such investment has to be calculated, so that the company can

analyse weather such investment is beneficial for the company or not. Not only this when there

are more than 2 investment that the company has to do, it helps in calculating rate of return of all

such investments available and provides the managers with the best. Rate of return the amount of

earnings that the company will be provided with when the organisation invests in the investment.

(mishra, 2018)

Analyses in variances- It is not always correct what has been predicted by the management and

what have been the actual results. The difference between the two gives the rise to variances.

Search variances are identified by the management accounting system and have corrected there

by the managers. Variances can be of two types that are positive variances and negative

variances. The management accounting system takes the advantage of the positive variances and

corrects the negative variances. There are various analytical techniques through with the

variances can be identified and corrected. Search techniques are part of management accounting

system and Management Accounting system help them in identifying the variances and to help

them in making decisions.

Aid in decision making process - For a production manager and production team it is the most

difficult to whether purchase or produce equipment. Such decisions are highly evaluated by the

company so as to ensure that the most out of the list can be taken by the company. Considering

the cost of both of the proposals is necessary for the company before making such evaluation as

what to consider. (mishra, 2018)

For evaluating the cost of both the proposal Management Accounting system is highly

recommended and is found most beneficial for the entities. One has to understand the

management accounting system and its policies and principles prove it becomes very easy for the

user to evaluate to proposal of making the products at home or buying it from outside. So as to

take the decision of making it or buying it management accounting system are very helpful.

(mishra, 2018)

5

Ascertaining cash flows- The revenue growth of a company is totally dependent on the

projected cash flows that are being presented by the managers to the users of the company. The

information that has been provided to the manager of the company used to decide how the

evaluation of money and resources is to be done so that the company can be benefited with the

decision that the manager has taken. The manager can easily predict the cash flows and the

impact of the cash flow on the business with the help of Management Accounting system.

Management accounting system helps the manager by providing them with the information

which includes the cash outflow inflow for the business during the year. With the help of these

past results and trend analysis the managers can easily identify the cost that the company will

incur in the near future. (Vitez, 2018)

To improve productivity and profitability: In an entity the production process should be

evaluated as and when required. About the production process a production manager can give a

detailed analysis of the productivity that the companies is providing and if the user of the report

provided by the production manager is not satisfied with the productivity levels that has been

stated by the manager, productivity needs to be improved. The productivity can be improved

with a Management Accounting system through with such productivity can be increased. For

increasing the productivity of the company will have to consider the profitability as well as.

Earning that the company is making by selling the product produced by the company. The

profitability and productivity can be improved with the help of Management Accounting system.

(Vitez, 2018)

III. Cost accounting systems (actual, normal and standard costing)

When a product is made various costs related to the product occur in manufacturing such

product. Accounting of such costs is called as cost accounting system. (Vitez, 2018)

It can be further divided into:

Normal costing –In this system, actual material costs, actual labour and variable overhead cost

are calculated (Drury, 2013).

Actual costing – It ascertained actual cost which is incurred for production of products.

6

projected cash flows that are being presented by the managers to the users of the company. The

information that has been provided to the manager of the company used to decide how the

evaluation of money and resources is to be done so that the company can be benefited with the

decision that the manager has taken. The manager can easily predict the cash flows and the

impact of the cash flow on the business with the help of Management Accounting system.

Management accounting system helps the manager by providing them with the information

which includes the cash outflow inflow for the business during the year. With the help of these

past results and trend analysis the managers can easily identify the cost that the company will

incur in the near future. (Vitez, 2018)

To improve productivity and profitability: In an entity the production process should be

evaluated as and when required. About the production process a production manager can give a

detailed analysis of the productivity that the companies is providing and if the user of the report

provided by the production manager is not satisfied with the productivity levels that has been

stated by the manager, productivity needs to be improved. The productivity can be improved

with a Management Accounting system through with such productivity can be increased. For

increasing the productivity of the company will have to consider the profitability as well as.

Earning that the company is making by selling the product produced by the company. The

profitability and productivity can be improved with the help of Management Accounting system.

(Vitez, 2018)

III. Cost accounting systems (actual, normal and standard costing)

When a product is made various costs related to the product occur in manufacturing such

product. Accounting of such costs is called as cost accounting system. (Vitez, 2018)

It can be further divided into:

Normal costing –In this system, actual material costs, actual labour and variable overhead cost

are calculated (Drury, 2013).

Actual costing – It ascertained actual cost which is incurred for production of products.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Standard costing- The estimated general cost that the product will involve of various material

labour and overhead cost are called as standard costing.

IV. Inventory management systems.

Inventory management systems-

Various combination processes and Technology that is done for the maintenance of the products

and whether the products are available in stock on the company. Inventory management system

is useful in many ways as it helps in identifying the inventory that weather for the inventory has

barcode labels or other tags that are useful for identifying the stock. Inventory management

system includes in itself various tools through which the barcode labels can be identified and

scanned. Inventory management system is highly recommended where the stock levels are high

and to analyses high data level is necessary and to generate report on timely basis is

recommended. Inventory management system applies the inventory principles which are FIFO

method, LIFO method and ABC analysis.

Inventory management system does not let the inventory to fall below the minimum level and it

always keeps stock available so that the company’s staff may not run out. Whenever the

company runs out of stock it affects its position in the market so as to avoid this Management

Accounting system provides inventory management system which is basically very useful for a

business to maintain it stock levels.

V. Job costing systems

Job costing systems

The cost of a job is to be calculated is called as job costing. It is done for calculating the cost of

various completed job done for manufacturing of product. Job costing system provides feasibility

of various jobs. For the purpose of calculating cost of a product all the cost involved in the

various jobs are maintained in ledger and then are added to the cost of the product.

The purpose behind job costing system used to analyses the profits of the company

understanding the cost of production and various overhead that weather they are below the

7

labour and overhead cost are called as standard costing.

IV. Inventory management systems.

Inventory management systems-

Various combination processes and Technology that is done for the maintenance of the products

and whether the products are available in stock on the company. Inventory management system

is useful in many ways as it helps in identifying the inventory that weather for the inventory has

barcode labels or other tags that are useful for identifying the stock. Inventory management

system includes in itself various tools through which the barcode labels can be identified and

scanned. Inventory management system is highly recommended where the stock levels are high

and to analyses high data level is necessary and to generate report on timely basis is

recommended. Inventory management system applies the inventory principles which are FIFO

method, LIFO method and ABC analysis.

Inventory management system does not let the inventory to fall below the minimum level and it

always keeps stock available so that the company’s staff may not run out. Whenever the

company runs out of stock it affects its position in the market so as to avoid this Management

Accounting system provides inventory management system which is basically very useful for a

business to maintain it stock levels.

V. Job costing systems

Job costing systems

The cost of a job is to be calculated is called as job costing. It is done for calculating the cost of

various completed job done for manufacturing of product. Job costing system provides feasibility

of various jobs. For the purpose of calculating cost of a product all the cost involved in the

various jobs are maintained in ledger and then are added to the cost of the product.

The purpose behind job costing system used to analyses the profits of the company

understanding the cost of production and various overhead that weather they are below the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

projected cost or not, through which company profit can be easily ascertained. There are various

documents that are used in the job costing procedure which are-

Production order- it is a type of work order through which is the production manager is

authorized to produce the amount of products that are mentioned in the production order,

Cost sheet- for the purpose of recording various costs another document which is called as Cost

sheet is used it provides the detailed cost that are incurred during the production process. (Drury,

2013).

Job costing system has many objective that are to complete a product to maintain a separate

account for a product that involve specific job and the calculation of the job on the basis of cost

involved in each job. It helps management to provide price of a certain work that has been asked

by the customer on the basis of the cost incurred in the previous jobs done by them.

b) Presenting financial information.

I. Different types of managerial accounting reports.

1. Managerial accounting reports-

The managers in providing expertise in financial reporting and also it help to control

management in Planning and performance of management system. (Vitez, 2018)

Types of Managerial accounting reports-

External report- the report that the management prepare for the outsiders of the business is

known as external report. Involve external users which are shareholders, investor and creditors.

The answer ability of the company is not meant to the outsiders but the reports are to be provided

to them. Company provides reports through the medium of the income statement and the balance

sheet that the company provides to the registrar of companies at the end of every financial year.

(Vitez, 2018)

Internal report- the report that is meant for the different level of management internal is called

as internal report. Internal report is not public document and not available for the public they are

8

documents that are used in the job costing procedure which are-

Production order- it is a type of work order through which is the production manager is

authorized to produce the amount of products that are mentioned in the production order,

Cost sheet- for the purpose of recording various costs another document which is called as Cost

sheet is used it provides the detailed cost that are incurred during the production process. (Drury,

2013).

Job costing system has many objective that are to complete a product to maintain a separate

account for a product that involve specific job and the calculation of the job on the basis of cost

involved in each job. It helps management to provide price of a certain work that has been asked

by the customer on the basis of the cost incurred in the previous jobs done by them.

b) Presenting financial information.

I. Different types of managerial accounting reports.

1. Managerial accounting reports-

The managers in providing expertise in financial reporting and also it help to control

management in Planning and performance of management system. (Vitez, 2018)

Types of Managerial accounting reports-

External report- the report that the management prepare for the outsiders of the business is

known as external report. Involve external users which are shareholders, investor and creditors.

The answer ability of the company is not meant to the outsiders but the reports are to be provided

to them. Company provides reports through the medium of the income statement and the balance

sheet that the company provides to the registrar of companies at the end of every financial year.

(Vitez, 2018)

Internal report- the report that is meant for the different level of management internal is called

as internal report. Internal report is not public document and not available for the public they are

8

there to help the department manager to understand the company's working and system. Reports

are meant for lower level, and top level management of the company. There is no access

compulsory requirement for providing such report their frequency depends upon the uses of the

company. Some of the examples of reports are changes in working capital, sales report, material

utilization reports etc. (Vitez, 2018)

Enterprise report- when all the departments are taken together as a single concerned and a

single report is provided is called as enterprise report. These reports are helpful in

communicating with outsiders and also concerned many activities relating to the business. These

enterprise reports are highly beneficial for the outsider and the outsider can invest in the

company with the help of these reports by making and interpretation of the financial statements

that have been provided to the user of the report. Enterprise reports are income tax returns,

employment report etc. (Vitez, 2018)

II. Why it is important for the information to be presented in manner that must be

understandable.

The accounting information that is provided to the users has quantitative and qualitative

characteristics. Such characteristics provide the user with the importance of the financial

information that is to be understandable by the user. Information provided is not understandable

to the user, its usefulness becomes of no use. Where the information provided is incorrect or

incomplete then it can hamper companies management system as information is required for

making decision and if the information is incorrect or incomplete it can lead to wrong decision

making. (Vitez, 2018)

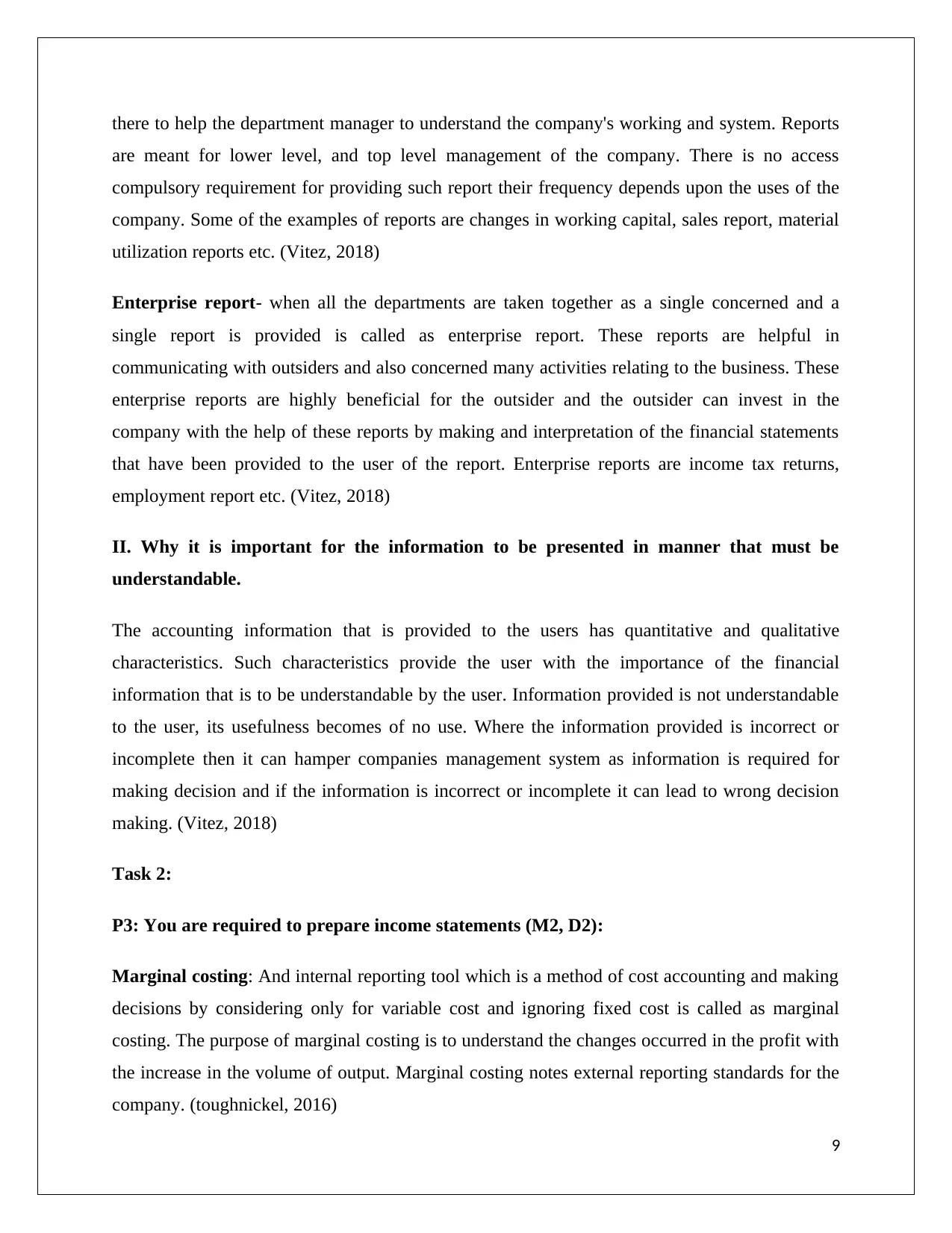

Task 2:

P3: You are required to prepare income statements (M2, D2):

Marginal costing: And internal reporting tool which is a method of cost accounting and making

decisions by considering only for variable cost and ignoring fixed cost is called as marginal

costing. The purpose of marginal costing is to understand the changes occurred in the profit with

the increase in the volume of output. Marginal costing notes external reporting standards for the

company. (toughnickel, 2016)

9

are meant for lower level, and top level management of the company. There is no access

compulsory requirement for providing such report their frequency depends upon the uses of the

company. Some of the examples of reports are changes in working capital, sales report, material

utilization reports etc. (Vitez, 2018)

Enterprise report- when all the departments are taken together as a single concerned and a

single report is provided is called as enterprise report. These reports are helpful in

communicating with outsiders and also concerned many activities relating to the business. These

enterprise reports are highly beneficial for the outsider and the outsider can invest in the

company with the help of these reports by making and interpretation of the financial statements

that have been provided to the user of the report. Enterprise reports are income tax returns,

employment report etc. (Vitez, 2018)

II. Why it is important for the information to be presented in manner that must be

understandable.

The accounting information that is provided to the users has quantitative and qualitative

characteristics. Such characteristics provide the user with the importance of the financial

information that is to be understandable by the user. Information provided is not understandable

to the user, its usefulness becomes of no use. Where the information provided is incorrect or

incomplete then it can hamper companies management system as information is required for

making decision and if the information is incorrect or incomplete it can lead to wrong decision

making. (Vitez, 2018)

Task 2:

P3: You are required to prepare income statements (M2, D2):

Marginal costing: And internal reporting tool which is a method of cost accounting and making

decisions by considering only for variable cost and ignoring fixed cost is called as marginal

costing. The purpose of marginal costing is to understand the changes occurred in the profit with

the increase in the volume of output. Marginal costing notes external reporting standards for the

company. (toughnickel, 2016)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The disadvantage of marginal costing is that it becomes very difficult to separate all the fixed

and variable cost and many a time’s marginal costing can give misleading results. Usability of

marginal costing is lesser than absorption costing. Semi variable cost is considered fully without

eliminating the fixed Element and can provide wrong result.

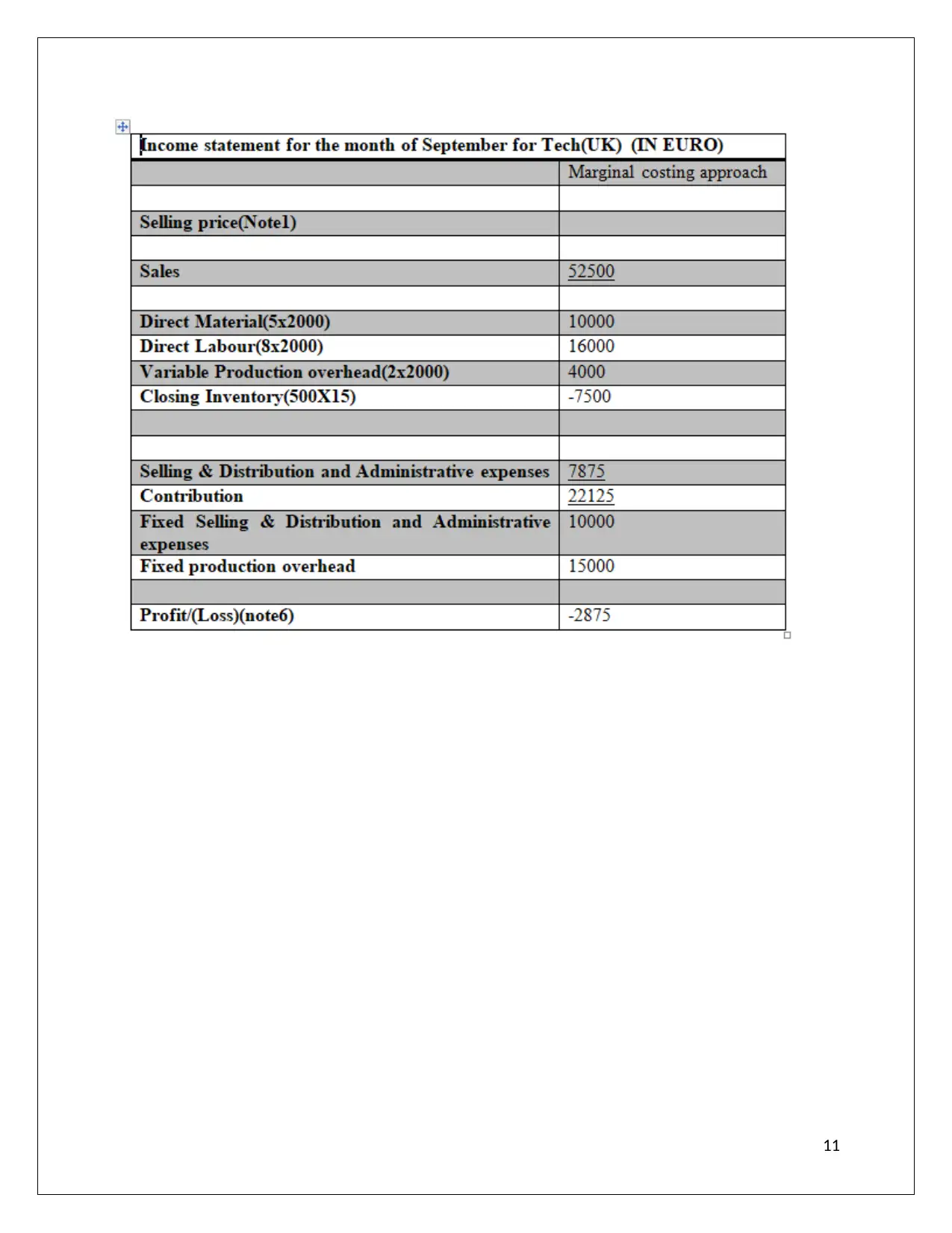

Absorption costing: Calculation of a cost of a product by including all the cost whether variable

or fixed this called as absorption costing. (toughnickel, 2016)

Disadvantage of absorption costing is that it involved in the manipulation of profit as it includes

fixed cost which are done for the purpose of manufacturing a product or not. (Silva, and

Jayamaha, 2012).

The difference in absorption costing and marginal costing:

Difference between marginal costing and absorption costing is the involvement of fixed cost in

the calculation of the cost of the product.

10

and variable cost and many a time’s marginal costing can give misleading results. Usability of

marginal costing is lesser than absorption costing. Semi variable cost is considered fully without

eliminating the fixed Element and can provide wrong result.

Absorption costing: Calculation of a cost of a product by including all the cost whether variable

or fixed this called as absorption costing. (toughnickel, 2016)

Disadvantage of absorption costing is that it involved in the manipulation of profit as it includes

fixed cost which are done for the purpose of manufacturing a product or not. (Silva, and

Jayamaha, 2012).

The difference in absorption costing and marginal costing:

Difference between marginal costing and absorption costing is the involvement of fixed cost in

the calculation of the cost of the product.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Analysis: The difference in the profit is because of the fixed cost involvement in the absorption

cost and not in the marginal cost.

12

cost and not in the marginal cost.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.