Management Accounting: Systems, Methods, and Benefits

VerifiedAdded on 2023/01/11

|17

|3868

|87

AI Summary

This document provides an in-depth analysis of management accounting, including its systems, methods, and benefits. It explains the essential requirements of management accounting systems and different reporting methods. It also evaluates the benefits of management accounting systems and their application. The document further discusses the integration between systems and reporting under management accounting. The second part of the document focuses on budgeting, including the purpose and types of budgets.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

Project Part 1..............................................................................................................................3

Section 1.....................................................................................................................................3

1.1 Explaining management accounting systems with essential requirements of its several

systems...................................................................................................................................3

1.2 Explaining different methods that are used for reporting under management accounting

................................................................................................................................................3

1.3 Evaluating benefits of the MA systems and its application.............................................4

1.4 Critically evaluating integrating between systems and reporting under management

accounting..............................................................................................................................6

Section 2.....................................................................................................................................6

2.1 Computing cost using appropriate techniques.................................................................6

2.2 Presenting the financial reporting document....................................................................8

2.3 Presenting financial reports..............................................................................................9

Project Part 2............................................................................................................................10

Section 3...................................................................................................................................10

3.1 Purpose and types of budgets.........................................................................................10

Section 4...................................................................................................................................12

4.1 Comparing organizations adopting MA systems...........................................................12

4.2 Management accounting helps in achieving sustainable success..................................13

4.3 Evaluation of the planning tools....................................................................................14

CONCLUSION........................................................................................................................15

REFERENCES.........................................................................................................................16

INTRODUCTION......................................................................................................................3

Project Part 1..............................................................................................................................3

Section 1.....................................................................................................................................3

1.1 Explaining management accounting systems with essential requirements of its several

systems...................................................................................................................................3

1.2 Explaining different methods that are used for reporting under management accounting

................................................................................................................................................3

1.3 Evaluating benefits of the MA systems and its application.............................................4

1.4 Critically evaluating integrating between systems and reporting under management

accounting..............................................................................................................................6

Section 2.....................................................................................................................................6

2.1 Computing cost using appropriate techniques.................................................................6

2.2 Presenting the financial reporting document....................................................................8

2.3 Presenting financial reports..............................................................................................9

Project Part 2............................................................................................................................10

Section 3...................................................................................................................................10

3.1 Purpose and types of budgets.........................................................................................10

Section 4...................................................................................................................................12

4.1 Comparing organizations adopting MA systems...........................................................12

4.2 Management accounting helps in achieving sustainable success..................................13

4.3 Evaluation of the planning tools....................................................................................14

CONCLUSION........................................................................................................................15

REFERENCES.........................................................................................................................16

INTRODUCTION

Management accounting (MA) is the accounting system that which provides

assistance to the business in taking managerial decisions which results into optimum

utilization of resources. It is mainly used by the internal management team. Management

accounting helps in increasing the profitability of the business in the long run. This report

presents about the concept, techniques and systems of management accounting and its

contribution in the accomplishment of the objectives.

Project Part 1

Section 1

1.1 Explaining management accounting systems with essential requirements of its several

systems

Management accounting refers to the process of managing the cost and business

operation in an effective manner by preparing the relevant reports with the help of financial

reports and accounts that can be derived from the finance department (Yigitbasioglu, 2016).

It is the process which transfers data into meaningful information which will help the

management in taking relevant business decisions. It is an essential part of the business

organization for formulating internal reports which assists in taking decisions which are

relevant for long term and short-term business goals. The essential aspects of it plays an

important role which are as follows:

Determining aim: On the basis of the information available, the MA systems helps in

setting the aims of the business and also finds the way to meet it.

Assist in planning process: MA system helps n formulating the plan as per the needs

and requirements. It assists the management in analysing the future and current prospects of

the future.

Reducing cost: MA system helps the management in reducing its cost while

manufacturing goods by using the cost accounting system. it helps in setting the standards

based on which product is produced which leads to providing better services to the

customers.

1.2 Explaining different methods that are used for reporting under management accounting

The different methods of management accounting are stated below.

Management accounting (MA) is the accounting system that which provides

assistance to the business in taking managerial decisions which results into optimum

utilization of resources. It is mainly used by the internal management team. Management

accounting helps in increasing the profitability of the business in the long run. This report

presents about the concept, techniques and systems of management accounting and its

contribution in the accomplishment of the objectives.

Project Part 1

Section 1

1.1 Explaining management accounting systems with essential requirements of its several

systems

Management accounting refers to the process of managing the cost and business

operation in an effective manner by preparing the relevant reports with the help of financial

reports and accounts that can be derived from the finance department (Yigitbasioglu, 2016).

It is the process which transfers data into meaningful information which will help the

management in taking relevant business decisions. It is an essential part of the business

organization for formulating internal reports which assists in taking decisions which are

relevant for long term and short-term business goals. The essential aspects of it plays an

important role which are as follows:

Determining aim: On the basis of the information available, the MA systems helps in

setting the aims of the business and also finds the way to meet it.

Assist in planning process: MA system helps n formulating the plan as per the needs

and requirements. It assists the management in analysing the future and current prospects of

the future.

Reducing cost: MA system helps the management in reducing its cost while

manufacturing goods by using the cost accounting system. it helps in setting the standards

based on which product is produced which leads to providing better services to the

customers.

1.2 Explaining different methods that are used for reporting under management accounting

The different methods of management accounting are stated below.

Inventory management system

This system helps in managing the inventory of the company and keeps track of the

movement of inventory from place to another or from ne process to another. It also helps in

assessing the need of the inventory to the business as each and everything is automated and

this helps in timely ordering the resources which helps in avoiding the situation of out of

stock (Aro-Gordon and Gupte, 2016). It provides complete report about the level of inventory

flowing into the business and how much is left unused at the place of production. The report

provided by it helps the management in determining the optimum level of inventory which

helps in avoiding the situation of wastage, spoilage because of more production and helps in

achieving increased productivity.

Job costing system

The technique records cost for creating or assembling the activity rather than the

process. This system will help the supervisor monitor cost for every single activity,

maintaining the data that is seen as more relevant to operations of business (Zahller, 2017). It

helps in deciding the areas that gives higher income with the goal that organization could

focus or put extra effort in building up those areas as opposed to those incurring losses or

wastage efforts and the time on the low beneficial areas. This system reports analysis the

disbursement when the venture is at growth stage with the goal that it could address the areas

before the cut rolls out of control.

Price optimization system

It is the arithmetical tool which is used by the firm in determining the price of its

product. Price determination is completely based on the response of the customers with

respect to their needs and responsiveness to pay for that product at different price levels

(Siebert and et.al, 2019). It takes into consideration operating cost, historic prices, inventory,

sales and so forth. This system is mainly suitable for the companies which is formed for

gaining large customer base and the market share. In this, products are manufactured as per

the needs and preferences of the customers along with the affordable prices so that large

portion of market can eb acquired.

1.3 Evaluating benefits of the MA systems and its application

Benefits of inventory management system

This system helps in managing the inventory of the company and keeps track of the

movement of inventory from place to another or from ne process to another. It also helps in

assessing the need of the inventory to the business as each and everything is automated and

this helps in timely ordering the resources which helps in avoiding the situation of out of

stock (Aro-Gordon and Gupte, 2016). It provides complete report about the level of inventory

flowing into the business and how much is left unused at the place of production. The report

provided by it helps the management in determining the optimum level of inventory which

helps in avoiding the situation of wastage, spoilage because of more production and helps in

achieving increased productivity.

Job costing system

The technique records cost for creating or assembling the activity rather than the

process. This system will help the supervisor monitor cost for every single activity,

maintaining the data that is seen as more relevant to operations of business (Zahller, 2017). It

helps in deciding the areas that gives higher income with the goal that organization could

focus or put extra effort in building up those areas as opposed to those incurring losses or

wastage efforts and the time on the low beneficial areas. This system reports analysis the

disbursement when the venture is at growth stage with the goal that it could address the areas

before the cut rolls out of control.

Price optimization system

It is the arithmetical tool which is used by the firm in determining the price of its

product. Price determination is completely based on the response of the customers with

respect to their needs and responsiveness to pay for that product at different price levels

(Siebert and et.al, 2019). It takes into consideration operating cost, historic prices, inventory,

sales and so forth. This system is mainly suitable for the companies which is formed for

gaining large customer base and the market share. In this, products are manufactured as per

the needs and preferences of the customers along with the affordable prices so that large

portion of market can eb acquired.

1.3 Evaluating benefits of the MA systems and its application

Benefits of inventory management system

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

The main benefit of this system is that it helps in effectively managing the inventory

very easily as it saves times, efforts and money (Nazarov and Broner, 2017). The

fluctuation in the market leads to changes in the stock level continuously, thus

inventory management system assists the management in avoiding the risk of errors as

it is fully automated.

It helps in proper management of inventory and the delivery of the same within the

specified time leads to making customers happier and more satisfied.

It assists in eliminating the unwanted cost that is caused because of the human error

and also it helps in further cost saving like shortening the lead time by improving the

supplier management relationships.

Benefits of job costing system

This system helps in assigning cost to individually toe ach and every job and helps in

computing profits.

It also helps in analysing the performance of the employees as it helps in gathering

relevant information based on which the performance of the employees can be

evaluated in respect to efficiency, productivity and so forth.

It assigns the particular cost to the respective account to which it belongs which

makes it accurate and adequate in managing the cost of each and every job through

which the product is undergone.

Benefits of Price optimization system

It helps the management in focussing on the variety of goals such as margin of sales,

conversion rate etc. this helps in analysing the benefits attached to it in a better way

(Simchi-Levi, 2017).

It provides assistance to the management in making quick and informed business

decisions by understanding and analysing the buying patterns of the consumers.

This reduces the manual work which leads to reduction in errors, resulting into

attaining more accurate forecasting. It also helps the businesses in making

adjustments in their product prices automatically whenever there is a change in the

market trends.

very easily as it saves times, efforts and money (Nazarov and Broner, 2017). The

fluctuation in the market leads to changes in the stock level continuously, thus

inventory management system assists the management in avoiding the risk of errors as

it is fully automated.

It helps in proper management of inventory and the delivery of the same within the

specified time leads to making customers happier and more satisfied.

It assists in eliminating the unwanted cost that is caused because of the human error

and also it helps in further cost saving like shortening the lead time by improving the

supplier management relationships.

Benefits of job costing system

This system helps in assigning cost to individually toe ach and every job and helps in

computing profits.

It also helps in analysing the performance of the employees as it helps in gathering

relevant information based on which the performance of the employees can be

evaluated in respect to efficiency, productivity and so forth.

It assigns the particular cost to the respective account to which it belongs which

makes it accurate and adequate in managing the cost of each and every job through

which the product is undergone.

Benefits of Price optimization system

It helps the management in focussing on the variety of goals such as margin of sales,

conversion rate etc. this helps in analysing the benefits attached to it in a better way

(Simchi-Levi, 2017).

It provides assistance to the management in making quick and informed business

decisions by understanding and analysing the buying patterns of the consumers.

This reduces the manual work which leads to reduction in errors, resulting into

attaining more accurate forecasting. It also helps the businesses in making

adjustments in their product prices automatically whenever there is a change in the

market trends.

1.4 Critically evaluating integrating between systems and reporting under management

accounting

The management accounting system plays an important role in running the business

efficiently and effectively. It assists the organization in attaining higher profits with the lower

cost and the higher profit margins. The integration of management accounting and reporting

in an organization results into an integrated system. This will help the organization in

efficiently analysing the performance and productivity which will help in proper decision

making and the managerial reports provides a road map to the managers in respect to making

effective strategy.

Section 2

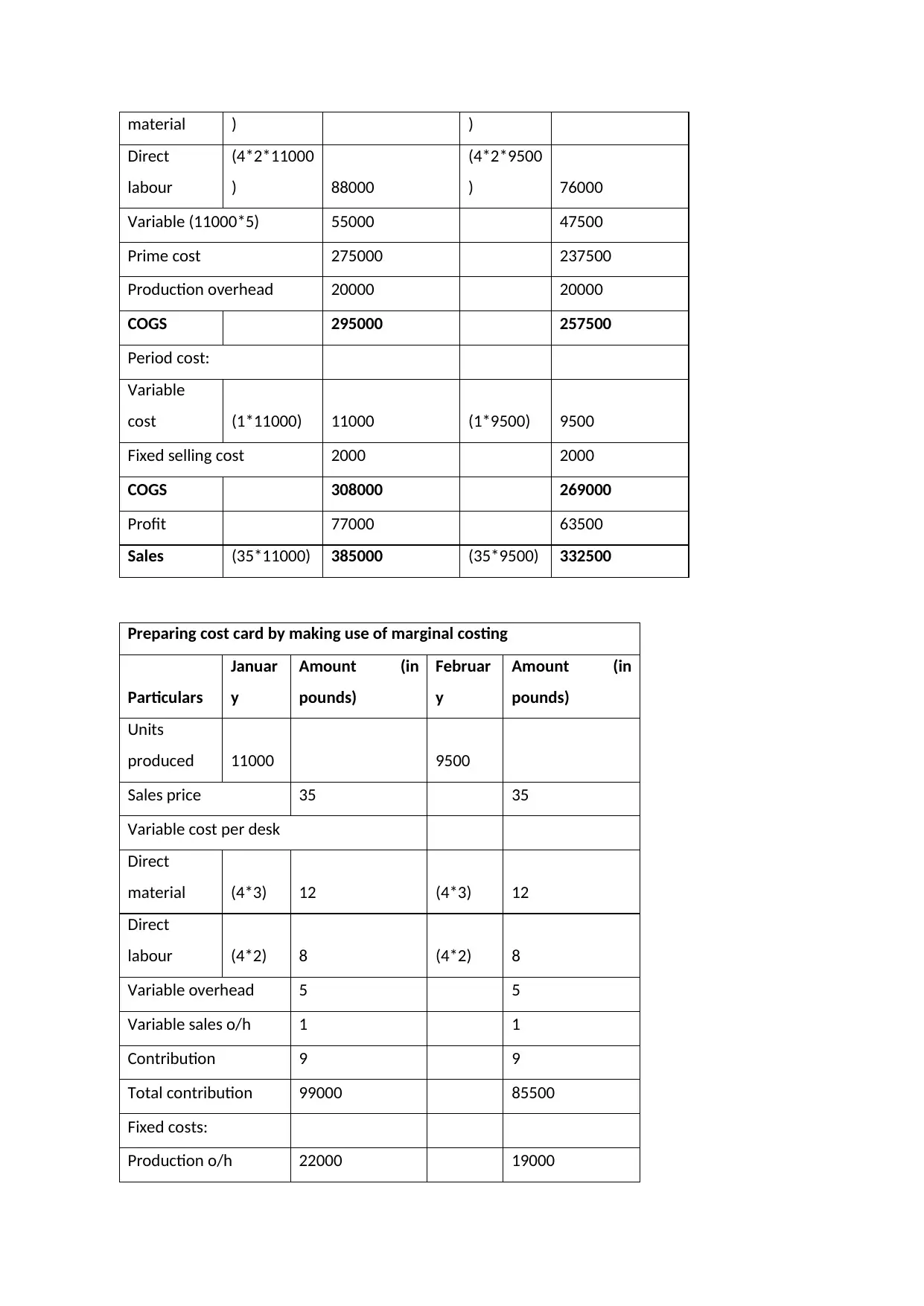

2.1 Computing cost using appropriate techniques

(a)

Absorption costing

It is the MA technique which considers different types of costs in relation to the

production of a specific product. It involves both direct and indirect cost. This method is

required by GAAP for external reporting. Under this technique, fixed overhead cost is

allocated to the products even if the product is not sold.

Marginal costing

The marginal costing helps in determining the variable cost per unit. It helps in

ascertaining the additional cost per unit and its impact on the overall profitability of the

business on account of change in the volume of sales (Milling, 2019). It is divided into 2

forms, fixed and variable cost. It is used by the manager for decision making process which is

majorly helpful in new product introduction or the business expansion. As it helps in

determining break-even point based on which price is decided.

Preparing cost card by making use of absorption costing

Particulars January

Amount (in

pounds) February

Amount (in

pounds)

Units

produced 11000 9500

Direct (4*3*11000 132000 (4*3*9500 114000

accounting

The management accounting system plays an important role in running the business

efficiently and effectively. It assists the organization in attaining higher profits with the lower

cost and the higher profit margins. The integration of management accounting and reporting

in an organization results into an integrated system. This will help the organization in

efficiently analysing the performance and productivity which will help in proper decision

making and the managerial reports provides a road map to the managers in respect to making

effective strategy.

Section 2

2.1 Computing cost using appropriate techniques

(a)

Absorption costing

It is the MA technique which considers different types of costs in relation to the

production of a specific product. It involves both direct and indirect cost. This method is

required by GAAP for external reporting. Under this technique, fixed overhead cost is

allocated to the products even if the product is not sold.

Marginal costing

The marginal costing helps in determining the variable cost per unit. It helps in

ascertaining the additional cost per unit and its impact on the overall profitability of the

business on account of change in the volume of sales (Milling, 2019). It is divided into 2

forms, fixed and variable cost. It is used by the manager for decision making process which is

majorly helpful in new product introduction or the business expansion. As it helps in

determining break-even point based on which price is decided.

Preparing cost card by making use of absorption costing

Particulars January

Amount (in

pounds) February

Amount (in

pounds)

Units

produced 11000 9500

Direct (4*3*11000 132000 (4*3*9500 114000

material ) )

Direct

labour

(4*2*11000

) 88000

(4*2*9500

) 76000

Variable (11000*5) 55000 47500

Prime cost 275000 237500

Production overhead 20000 20000

COGS 295000 257500

Period cost:

Variable

cost (1*11000) 11000 (1*9500) 9500

Fixed selling cost 2000 2000

COGS 308000 269000

Profit 77000 63500

Sales (35*11000) 385000 (35*9500) 332500

Preparing cost card by making use of marginal costing

Particulars

Januar

y

Amount (in

pounds)

Februar

y

Amount (in

pounds)

Units

produced 11000 9500

Sales price 35 35

Variable cost per desk

Direct

material (4*3) 12 (4*3) 12

Direct

labour (4*2) 8 (4*2) 8

Variable overhead 5 5

Variable sales o/h 1 1

Contribution 9 9

Total contribution 99000 85500

Fixed costs:

Production o/h 22000 19000

Direct

labour

(4*2*11000

) 88000

(4*2*9500

) 76000

Variable (11000*5) 55000 47500

Prime cost 275000 237500

Production overhead 20000 20000

COGS 295000 257500

Period cost:

Variable

cost (1*11000) 11000 (1*9500) 9500

Fixed selling cost 2000 2000

COGS 308000 269000

Profit 77000 63500

Sales (35*11000) 385000 (35*9500) 332500

Preparing cost card by making use of marginal costing

Particulars

Januar

y

Amount (in

pounds)

Februar

y

Amount (in

pounds)

Units

produced 11000 9500

Sales price 35 35

Variable cost per desk

Direct

material (4*3) 12 (4*3) 12

Direct

labour (4*2) 8 (4*2) 8

Variable overhead 5 5

Variable sales o/h 1 1

Contribution 9 9

Total contribution 99000 85500

Fixed costs:

Production o/h 22000 19000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales overhead 2000 2000

Profit 75000 64500

Interpretation: The absorption costing technique is more preferable by the entities as

it presents the actual profitability as it takes into account fixed and variable cost while

determining the cost of production in comparison to marginal costing.

(b)

Absorption costing

Advantages Disadvantages

This technique assists the management in

computing the gross and net profit

separately in the income statement.

Under this method, it is difficult to ensure

effective comparison and

It assists the management in making proper

distribution of the fixed overheads.

It fails to provide help to the management in

deciding the right product mix.

Marginal costing

Advantages Disadvantages

It is very effective in determining and

exercising control over the production costs.

This method cannot be used for external

reporting purpose.

It is mostly useful in short term planning

and provides graphical representation of

profits and the break-even points.

Under this, variable cost is apportioned on

an estimated basis rather than on actual

basis.

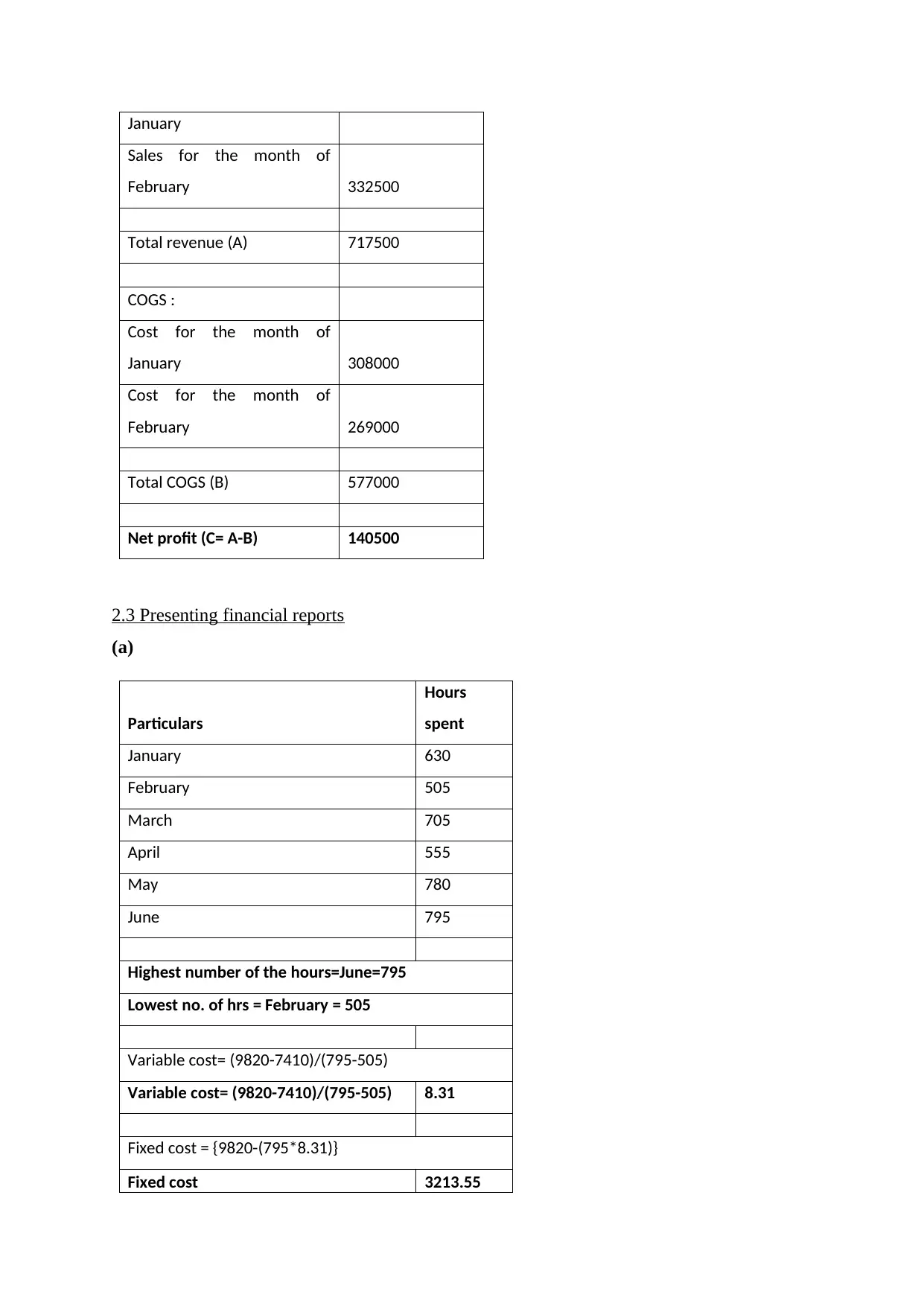

2.2 Presenting the financial reporting document

Income statement for the year ending February

Particulars

Amount (in

pounds)

Revenue

Sales for the month of 385000

Profit 75000 64500

Interpretation: The absorption costing technique is more preferable by the entities as

it presents the actual profitability as it takes into account fixed and variable cost while

determining the cost of production in comparison to marginal costing.

(b)

Absorption costing

Advantages Disadvantages

This technique assists the management in

computing the gross and net profit

separately in the income statement.

Under this method, it is difficult to ensure

effective comparison and

It assists the management in making proper

distribution of the fixed overheads.

It fails to provide help to the management in

deciding the right product mix.

Marginal costing

Advantages Disadvantages

It is very effective in determining and

exercising control over the production costs.

This method cannot be used for external

reporting purpose.

It is mostly useful in short term planning

and provides graphical representation of

profits and the break-even points.

Under this, variable cost is apportioned on

an estimated basis rather than on actual

basis.

2.2 Presenting the financial reporting document

Income statement for the year ending February

Particulars

Amount (in

pounds)

Revenue

Sales for the month of 385000

January

Sales for the month of

February 332500

Total revenue (A) 717500

COGS :

Cost for the month of

January 308000

Cost for the month of

February 269000

Total COGS (B) 577000

Net profit (C= A-B) 140500

2.3 Presenting financial reports

(a)

Particulars

Hours

spent

January 630

February 505

March 705

April 555

May 780

June 795

Highest number of the hours=June=795

Lowest no. of hrs = February = 505

Variable cost= (9820-7410)/(795-505)

Variable cost= (9820-7410)/(795-505) 8.31

Fixed cost = {9820-(795*8.31)}

Fixed cost 3213.55

Sales for the month of

February 332500

Total revenue (A) 717500

COGS :

Cost for the month of

January 308000

Cost for the month of

February 269000

Total COGS (B) 577000

Net profit (C= A-B) 140500

2.3 Presenting financial reports

(a)

Particulars

Hours

spent

January 630

February 505

March 705

April 555

May 780

June 795

Highest number of the hours=June=795

Lowest no. of hrs = February = 505

Variable cost= (9820-7410)/(795-505)

Variable cost= (9820-7410)/(795-505) 8.31

Fixed cost = {9820-(795*8.31)}

Fixed cost 3213.55

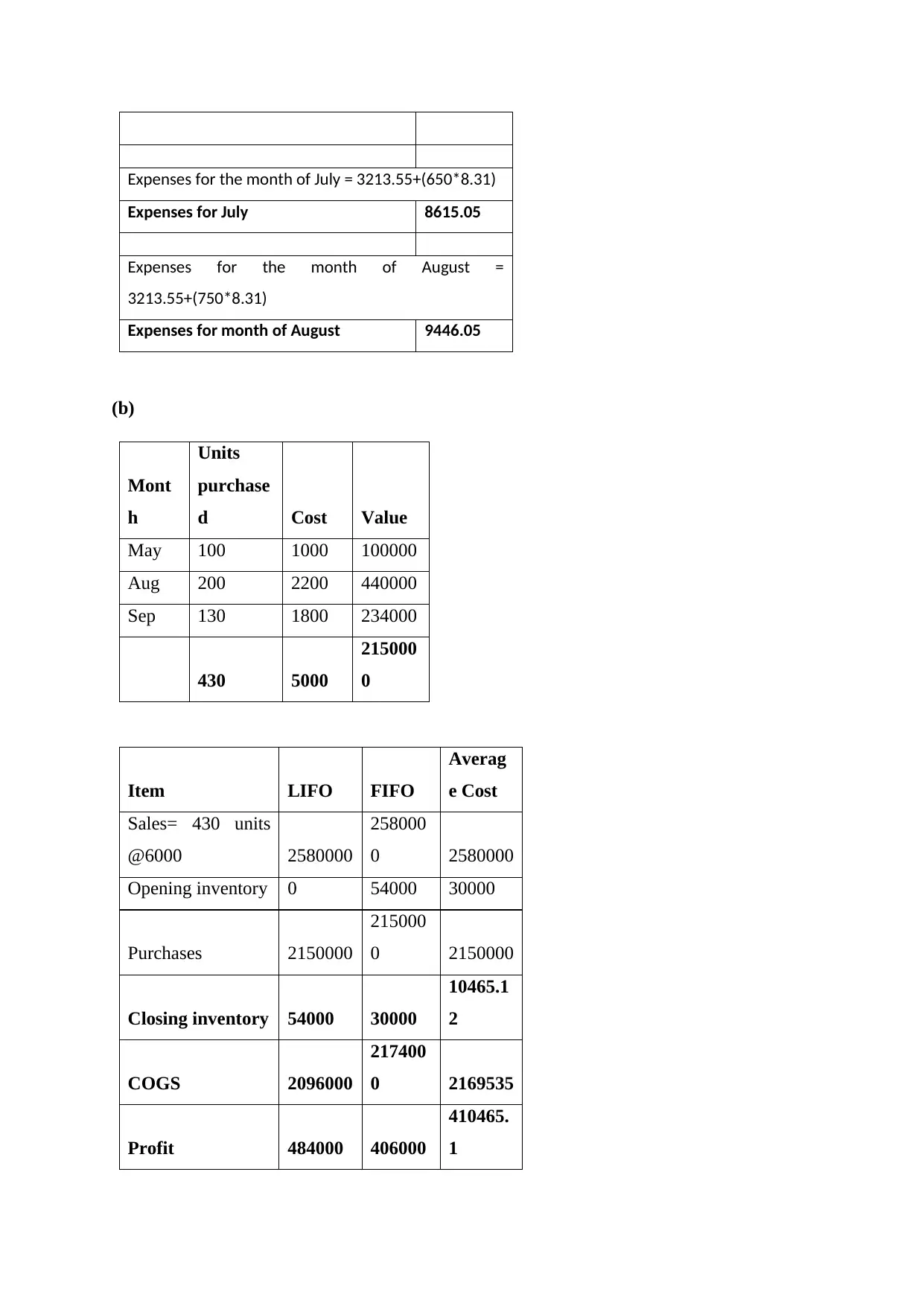

Expenses for the month of July = 3213.55+(650*8.31)

Expenses for July 8615.05

Expenses for the month of August =

3213.55+(750*8.31)

Expenses for month of August 9446.05

(b)

Mont

h

Units

purchase

d Cost Value

May 100 1000 100000

Aug 200 2200 440000

Sep 130 1800 234000

430 5000

215000

0

Item LIFO FIFO

Averag

e Cost

Sales= 430 units

@6000 2580000

258000

0 2580000

Opening inventory 0 54000 30000

Purchases 2150000

215000

0 2150000

Closing inventory 54000 30000

10465.1

2

COGS 2096000

217400

0 2169535

Profit 484000 406000

410465.

1

Expenses for July 8615.05

Expenses for the month of August =

3213.55+(750*8.31)

Expenses for month of August 9446.05

(b)

Mont

h

Units

purchase

d Cost Value

May 100 1000 100000

Aug 200 2200 440000

Sep 130 1800 234000

430 5000

215000

0

Item LIFO FIFO

Averag

e Cost

Sales= 430 units

@6000 2580000

258000

0 2580000

Opening inventory 0 54000 30000

Purchases 2150000

215000

0 2150000

Closing inventory 54000 30000

10465.1

2

COGS 2096000

217400

0 2169535

Profit 484000 406000

410465.

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Project Part 2

Section 3

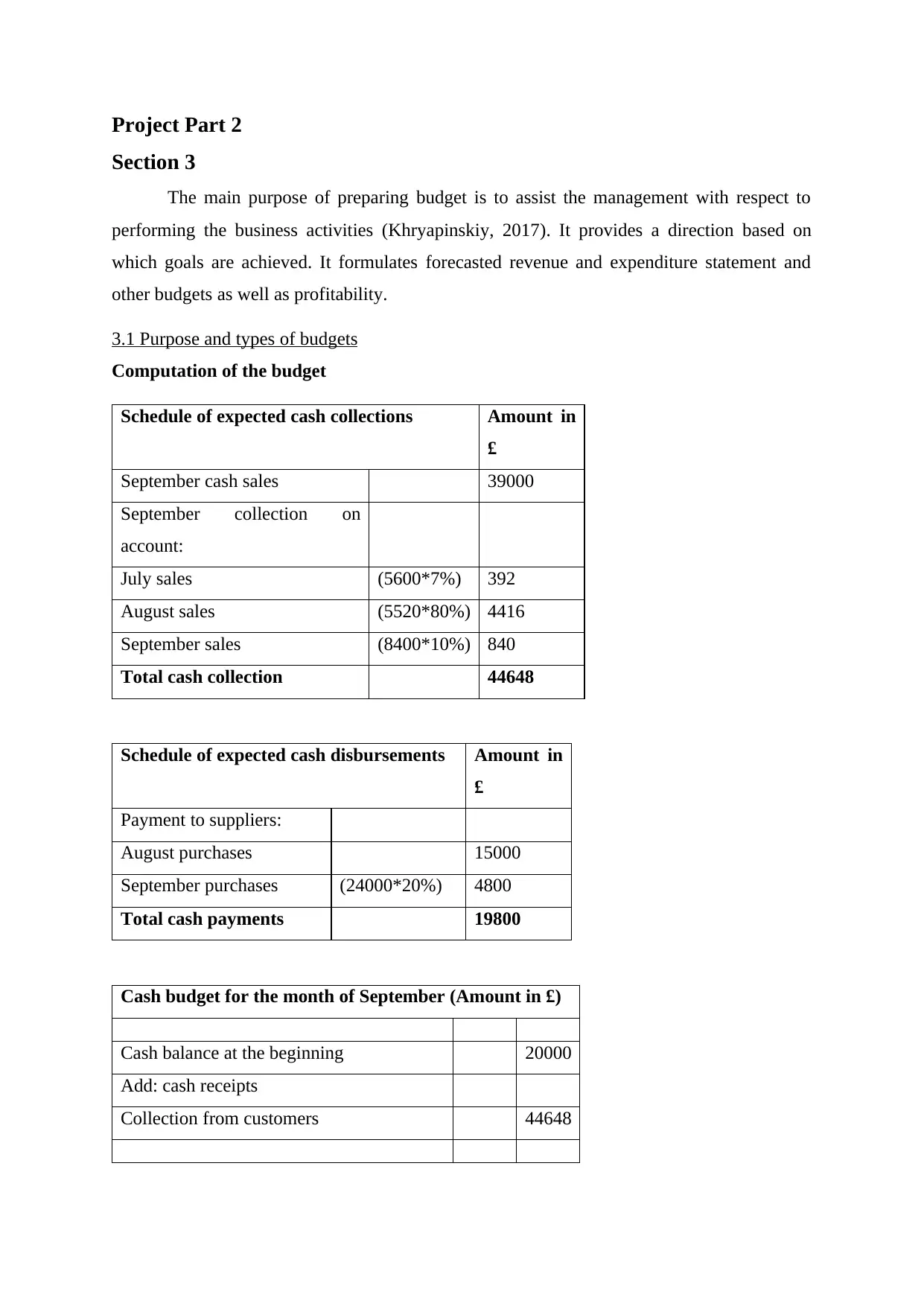

The main purpose of preparing budget is to assist the management with respect to

performing the business activities (Khryapinskiy, 2017). It provides a direction based on

which goals are achieved. It formulates forecasted revenue and expenditure statement and

other budgets as well as profitability.

3.1 Purpose and types of budgets

Computation of the budget

Schedule of expected cash collections Amount in

£

September cash sales 39000

September collection on

account:

July sales (5600*7%) 392

August sales (5520*80%) 4416

September sales (8400*10%) 840

Total cash collection 44648

Schedule of expected cash disbursements Amount in

£

Payment to suppliers:

August purchases 15000

September purchases (24000*20%) 4800

Total cash payments 19800

Cash budget for the month of September (Amount in £)

Cash balance at the beginning 20000

Add: cash receipts

Collection from customers 44648

Section 3

The main purpose of preparing budget is to assist the management with respect to

performing the business activities (Khryapinskiy, 2017). It provides a direction based on

which goals are achieved. It formulates forecasted revenue and expenditure statement and

other budgets as well as profitability.

3.1 Purpose and types of budgets

Computation of the budget

Schedule of expected cash collections Amount in

£

September cash sales 39000

September collection on

account:

July sales (5600*7%) 392

August sales (5520*80%) 4416

September sales (8400*10%) 840

Total cash collection 44648

Schedule of expected cash disbursements Amount in

£

Payment to suppliers:

August purchases 15000

September purchases (24000*20%) 4800

Total cash payments 19800

Cash budget for the month of September (Amount in £)

Cash balance at the beginning 20000

Add: cash receipts

Collection from customers 44648

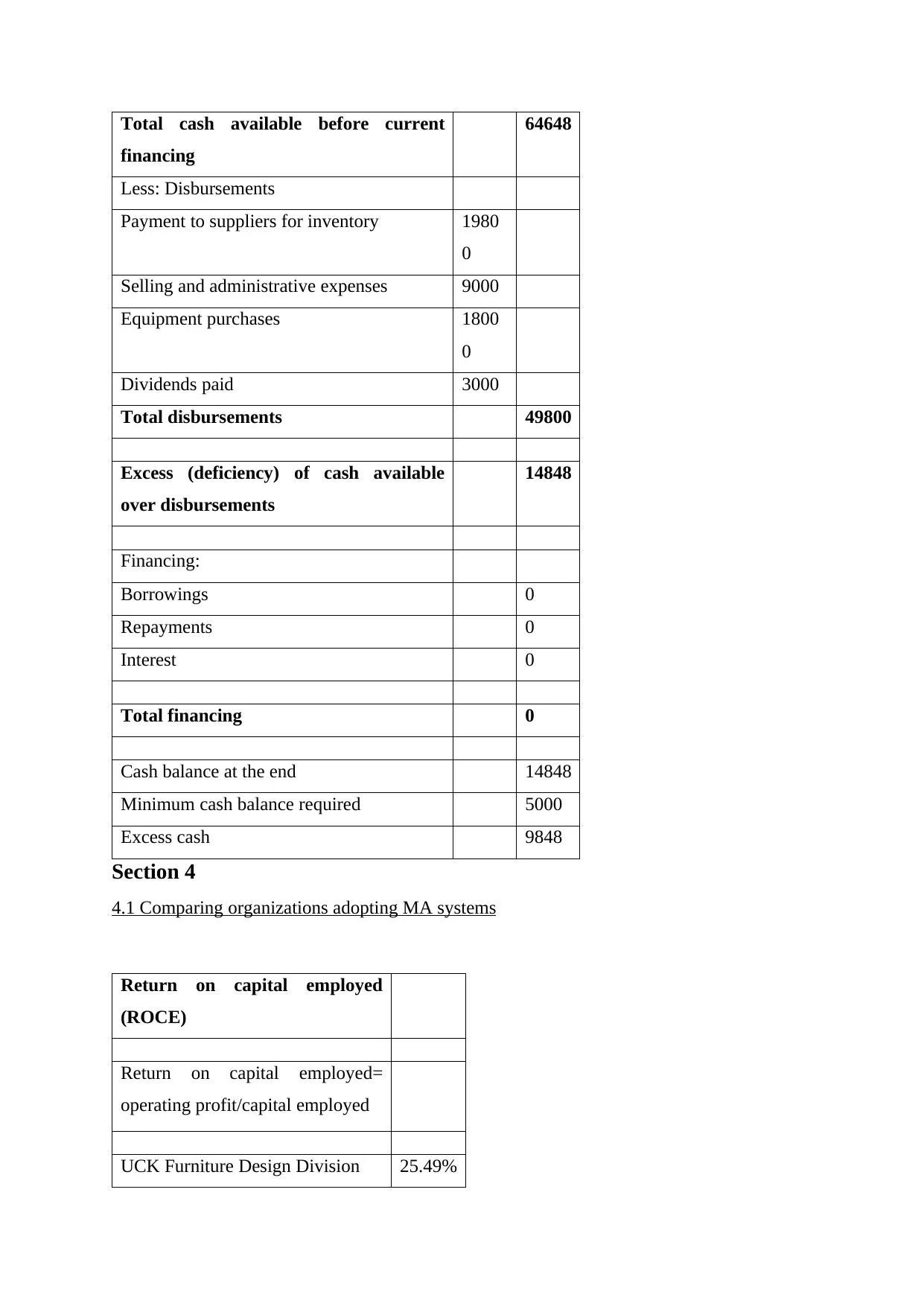

Total cash available before current

financing

64648

Less: Disbursements

Payment to suppliers for inventory 1980

0

Selling and administrative expenses 9000

Equipment purchases 1800

0

Dividends paid 3000

Total disbursements 49800

Excess (deficiency) of cash available

over disbursements

14848

Financing:

Borrowings 0

Repayments 0

Interest 0

Total financing 0

Cash balance at the end 14848

Minimum cash balance required 5000

Excess cash 9848

Section 4

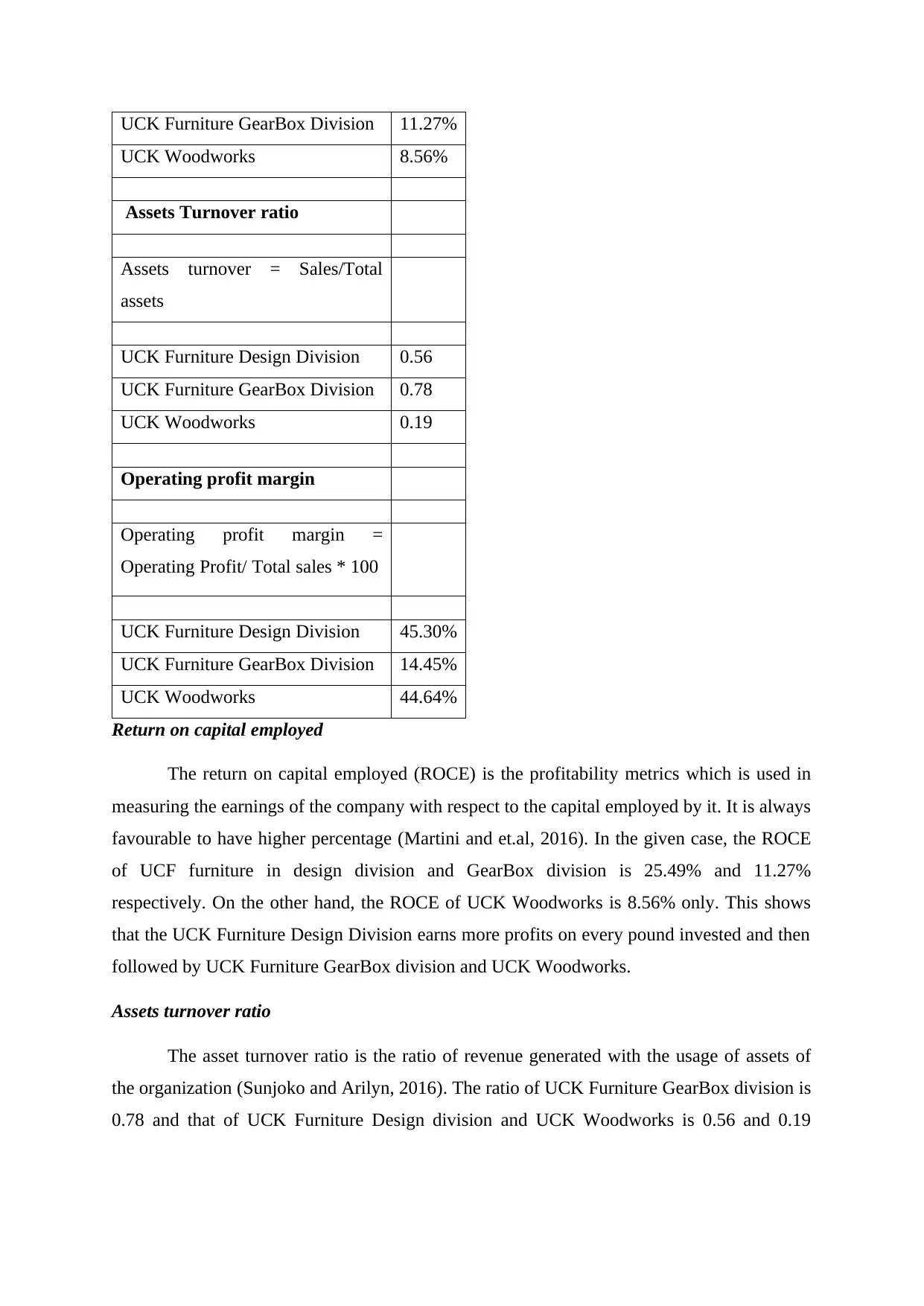

4.1 Comparing organizations adopting MA systems

Return on capital employed

(ROCE)

Return on capital employed=

operating profit/capital employed

UCK Furniture Design Division 25.49%

financing

64648

Less: Disbursements

Payment to suppliers for inventory 1980

0

Selling and administrative expenses 9000

Equipment purchases 1800

0

Dividends paid 3000

Total disbursements 49800

Excess (deficiency) of cash available

over disbursements

14848

Financing:

Borrowings 0

Repayments 0

Interest 0

Total financing 0

Cash balance at the end 14848

Minimum cash balance required 5000

Excess cash 9848

Section 4

4.1 Comparing organizations adopting MA systems

Return on capital employed

(ROCE)

Return on capital employed=

operating profit/capital employed

UCK Furniture Design Division 25.49%

UCK Furniture GearBox Division 11.27%

UCK Woodworks 8.56%

Assets Turnover ratio

Assets turnover = Sales/Total

assets

UCK Furniture Design Division 0.56

UCK Furniture GearBox Division 0.78

UCK Woodworks 0.19

Operating profit margin

Operating profit margin =

Operating Profit/ Total sales * 100

UCK Furniture Design Division 45.30%

UCK Furniture GearBox Division 14.45%

UCK Woodworks 44.64%

Return on capital employed

The return on capital employed (ROCE) is the profitability metrics which is used in

measuring the earnings of the company with respect to the capital employed by it. It is always

favourable to have higher percentage (Martini and et.al, 2016). In the given case, the ROCE

of UCF furniture in design division and GearBox division is 25.49% and 11.27%

respectively. On the other hand, the ROCE of UCK Woodworks is 8.56% only. This shows

that the UCK Furniture Design Division earns more profits on every pound invested and then

followed by UCK Furniture GearBox division and UCK Woodworks.

Assets turnover ratio

The asset turnover ratio is the ratio of revenue generated with the usage of assets of

the organization (Sunjoko and Arilyn, 2016). The ratio of UCK Furniture GearBox division is

0.78 and that of UCK Furniture Design division and UCK Woodworks is 0.56 and 0.19

UCK Woodworks 8.56%

Assets Turnover ratio

Assets turnover = Sales/Total

assets

UCK Furniture Design Division 0.56

UCK Furniture GearBox Division 0.78

UCK Woodworks 0.19

Operating profit margin

Operating profit margin =

Operating Profit/ Total sales * 100

UCK Furniture Design Division 45.30%

UCK Furniture GearBox Division 14.45%

UCK Woodworks 44.64%

Return on capital employed

The return on capital employed (ROCE) is the profitability metrics which is used in

measuring the earnings of the company with respect to the capital employed by it. It is always

favourable to have higher percentage (Martini and et.al, 2016). In the given case, the ROCE

of UCF furniture in design division and GearBox division is 25.49% and 11.27%

respectively. On the other hand, the ROCE of UCK Woodworks is 8.56% only. This shows

that the UCK Furniture Design Division earns more profits on every pound invested and then

followed by UCK Furniture GearBox division and UCK Woodworks.

Assets turnover ratio

The asset turnover ratio is the ratio of revenue generated with the usage of assets of

the organization (Sunjoko and Arilyn, 2016). The ratio of UCK Furniture GearBox division is

0.78 and that of UCK Furniture Design division and UCK Woodworks is 0.56 and 0.19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

respectively. This ratio shows that the UCK Furniture GearBox division is generating more

revenue from its assets in comparison to others.

Operating profit margin

This ratio is represented as the ratio of operating profit with respect to sales in terms

of percentage. Higher the ratio better it is for the company (AFFANDI, SUNARKO and

YUNANTO, 2019). The operating profit of UCK Woodworks is 44.64%, of UCK Furniture

Design Division is 45.30% and that of UCK Furniture GearBox division is 14.45%. This ratio

indicates that the position of UCK Woodworks is better as compared to others.

4.2 Management accounting helps in achieving sustainable success

The management accounting can help in enhancing the performance of the

organization as it brings into notice important and significant financial figures in connection

with the business. This figure can be additionally improved which can ended up being useful

for the organization. The ratios determined above gives important information to the

administration which can be utilized by the inside group to think of the strategies to improve

those figures by taking remedial steps pertinent in that circumstance. This will help with

managing the operation of the organization in a much better manner and furthermore helps in

making the sustainable progress.

4.3 Evaluation of the planning tools

The planning tools of management accounting helps the business organization in

mitigating its financial problems which helps in effectively achieving the sustainable success.

A detailed evaluation of various planning tools are stated below.

Budgeting

Budget is the formal document which includes the estimated statement which is the

part of the planning process. These reports are in respect to the sales, purchase, production,

expenses etc. This helps in evaluating the performance of the business with respect to the set

target. Also, analyses the actual and the budgeted performance to know the direction in which

business is moving.

Budgetary control

In this technique, the management compares the budgetary targets with the actual

result of the business (Mazikana, 2019). This helps in determining any deviation between the

revenue from its assets in comparison to others.

Operating profit margin

This ratio is represented as the ratio of operating profit with respect to sales in terms

of percentage. Higher the ratio better it is for the company (AFFANDI, SUNARKO and

YUNANTO, 2019). The operating profit of UCK Woodworks is 44.64%, of UCK Furniture

Design Division is 45.30% and that of UCK Furniture GearBox division is 14.45%. This ratio

indicates that the position of UCK Woodworks is better as compared to others.

4.2 Management accounting helps in achieving sustainable success

The management accounting can help in enhancing the performance of the

organization as it brings into notice important and significant financial figures in connection

with the business. This figure can be additionally improved which can ended up being useful

for the organization. The ratios determined above gives important information to the

administration which can be utilized by the inside group to think of the strategies to improve

those figures by taking remedial steps pertinent in that circumstance. This will help with

managing the operation of the organization in a much better manner and furthermore helps in

making the sustainable progress.

4.3 Evaluation of the planning tools

The planning tools of management accounting helps the business organization in

mitigating its financial problems which helps in effectively achieving the sustainable success.

A detailed evaluation of various planning tools are stated below.

Budgeting

Budget is the formal document which includes the estimated statement which is the

part of the planning process. These reports are in respect to the sales, purchase, production,

expenses etc. This helps in evaluating the performance of the business with respect to the set

target. Also, analyses the actual and the budgeted performance to know the direction in which

business is moving.

Budgetary control

In this technique, the management compares the budgetary targets with the actual

result of the business (Mazikana, 2019). This helps in determining any deviation between the

two and if any deviation is there then corrective actions are taken to reduce the same. In other

words, it helps in fixing the problem that caused the difference.

Project appraisal

The specific undertaking in which the company is intrigued to put resources into

ought to be assessed at a standard time frame to know whether the cask inflows anticipated

from the venture is really being incurring according to the pre-decided objectives. The way of

assessing the project is known as project appraisal (Jilin, 2018). It helps in identifying the risk

so moves can be made to lessen it. It likewise helps in enhancing the proficiency level and

help with guaranteeing that the pre-determined goals are met within the particular time period

and furthermore the results are in accordance with the guidelines set.

Analysis of the cost variance

In this, the cost is analysed of the specific project with respect to the standards set

with objective to find the variance. The cost variance is analysed along with the reasons of

the variance (Kumar, 2019). On completion of the analysis the corrective actions are taken by

the management for resolving such issues.

Ratio analysis

It is also an important tool which is used to measure the financial performance and

position of the business. There are different types of ratios that can be used such as

profitability, liquidity, efficiency ratio etc. Each these ratios have various other ratios. It helps

in analysing the areas where the company needs to put more pressure for improving its

performance.

There, all these stated planning tools is helpful in managing the financial problems

being faced by the organizations which will help in effectively achieving the desired

objectives.

CONCLUSION

It can be summarized from the above that management accounting has a huge

contribution towards growth and development of the organization. The major limitation of

this concept is that it requires to incur a lot of expenses along with time and efforts. The

various techniques can be used for evaluating the business activities and solving financial

words, it helps in fixing the problem that caused the difference.

Project appraisal

The specific undertaking in which the company is intrigued to put resources into

ought to be assessed at a standard time frame to know whether the cask inflows anticipated

from the venture is really being incurring according to the pre-decided objectives. The way of

assessing the project is known as project appraisal (Jilin, 2018). It helps in identifying the risk

so moves can be made to lessen it. It likewise helps in enhancing the proficiency level and

help with guaranteeing that the pre-determined goals are met within the particular time period

and furthermore the results are in accordance with the guidelines set.

Analysis of the cost variance

In this, the cost is analysed of the specific project with respect to the standards set

with objective to find the variance. The cost variance is analysed along with the reasons of

the variance (Kumar, 2019). On completion of the analysis the corrective actions are taken by

the management for resolving such issues.

Ratio analysis

It is also an important tool which is used to measure the financial performance and

position of the business. There are different types of ratios that can be used such as

profitability, liquidity, efficiency ratio etc. Each these ratios have various other ratios. It helps

in analysing the areas where the company needs to put more pressure for improving its

performance.

There, all these stated planning tools is helpful in managing the financial problems

being faced by the organizations which will help in effectively achieving the desired

objectives.

CONCLUSION

It can be summarized from the above that management accounting has a huge

contribution towards growth and development of the organization. The major limitation of

this concept is that it requires to incur a lot of expenses along with time and efforts. The

various techniques can be used for evaluating the business activities and solving financial

problems. Therefore, it can be said that management accounting is an essential part of every

business and is required to be followed by every business in order to survive and grow.

business and is required to be followed by every business in order to survive and grow.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Yigitbasioglu, O., 2016. Firms’ information system characteristics and management

accounting adaptability. International Journal of Accounting and Information

Management.

Zahller, K. A., 2017. Truffle in paradise: Job costing for a small business. Journal of

Accounting Education. 40. pp.32-42.

Siebert, L. C. and et.al, 2019. Customer targeting optimization system for price‐based

demand response programs. International Transactions on Electrical Energy

Systems. 29(2). p.e2709.

Simchi-Levi, D., 2017. The new frontier of price optimization. MIT Sloan Management

Review. 59(1). p.22.

Milling, M., 2019. Contribution Accounting–a planning and controlling tool to observe costs

and profit achievements within management decisions.

Khryapinskiy, P. V., 2017. Unintended Use of Budget, Excess of Expenditure Limits or

Provisions of Budgeting Loans without an Established Purpose in the Budget or in

Excess of Budget: Issue of Special Implementation regarding Release from Criminal

Liability. JE Eur. L. p.4.

Martini, R. and et.al, 2016. INTELLECTUAL CAPITAL AND RETURN ON

INVESTMENT: IN MINING COMPANIES. In Proceeding Forum in Research,

Science, and Technology (FIRST) 2016. Politeknik Negeri Sriwijaya.

Sunjoko, M. I. and Arilyn, E. J., 2016. Effects of inventory turnover, total asset turnover,

fixed asset turnover, current ratio and average collection period on profitability. Jurnal

Bisnis dan Akuntansi. 18(1). pp.79-83.

AFFANDI, F., SUNARKO, B. and YUNANTO, A., 2019. The Impact of Cash Ratio, Debt

To Equity Ratio, Receivables Turnover, Net Profit Margin, Return On Equity, and

Institutional Ownership To Dividend Payout Ratio. Journal of Research in

Management. 1(4).

Mazikana, A. T., 2019. The Effect of Budgetary Controls on the Performance of an

Organization. Available at SSRN 3445247.

Jilin, L., 2018. The Rules Clarified: How the Project Passed Appraisal. In Constructing a

Paradigm for Children’s Contextualized Learning (pp. 101-111). Springer, Berlin,

Heidelberg.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal. 54(10). pp.65-73.

Aro-Gordon, S. and Gupte, J., 2016, January. Contemporary Inventory Management

Techniques: A Conceptual Investigation. In Proceedings of the International

Conference on Operations Management and Research (pp. 21-22).

Nazarov, A. and Broner, V., 2017, September. Inventory management system with on/off

control of input product flow. In International Conference on Information

Technologies and Mathematical Modelling (pp. 370-381). Springer, Cham.

Books and Journals

Yigitbasioglu, O., 2016. Firms’ information system characteristics and management

accounting adaptability. International Journal of Accounting and Information

Management.

Zahller, K. A., 2017. Truffle in paradise: Job costing for a small business. Journal of

Accounting Education. 40. pp.32-42.

Siebert, L. C. and et.al, 2019. Customer targeting optimization system for price‐based

demand response programs. International Transactions on Electrical Energy

Systems. 29(2). p.e2709.

Simchi-Levi, D., 2017. The new frontier of price optimization. MIT Sloan Management

Review. 59(1). p.22.

Milling, M., 2019. Contribution Accounting–a planning and controlling tool to observe costs

and profit achievements within management decisions.

Khryapinskiy, P. V., 2017. Unintended Use of Budget, Excess of Expenditure Limits or

Provisions of Budgeting Loans without an Established Purpose in the Budget or in

Excess of Budget: Issue of Special Implementation regarding Release from Criminal

Liability. JE Eur. L. p.4.

Martini, R. and et.al, 2016. INTELLECTUAL CAPITAL AND RETURN ON

INVESTMENT: IN MINING COMPANIES. In Proceeding Forum in Research,

Science, and Technology (FIRST) 2016. Politeknik Negeri Sriwijaya.

Sunjoko, M. I. and Arilyn, E. J., 2016. Effects of inventory turnover, total asset turnover,

fixed asset turnover, current ratio and average collection period on profitability. Jurnal

Bisnis dan Akuntansi. 18(1). pp.79-83.

AFFANDI, F., SUNARKO, B. and YUNANTO, A., 2019. The Impact of Cash Ratio, Debt

To Equity Ratio, Receivables Turnover, Net Profit Margin, Return On Equity, and

Institutional Ownership To Dividend Payout Ratio. Journal of Research in

Management. 1(4).

Mazikana, A. T., 2019. The Effect of Budgetary Controls on the Performance of an

Organization. Available at SSRN 3445247.

Jilin, L., 2018. The Rules Clarified: How the Project Passed Appraisal. In Constructing a

Paradigm for Children’s Contextualized Learning (pp. 101-111). Springer, Berlin,

Heidelberg.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal. 54(10). pp.65-73.

Aro-Gordon, S. and Gupte, J., 2016, January. Contemporary Inventory Management

Techniques: A Conceptual Investigation. In Proceedings of the International

Conference on Operations Management and Research (pp. 21-22).

Nazarov, A. and Broner, V., 2017, September. Inventory management system with on/off

control of input product flow. In International Conference on Information

Technologies and Mathematical Modelling (pp. 370-381). Springer, Cham.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.