Importance of Management Accounting Reports

VerifiedAdded on 2020/07/23

|14

|4222

|174

AI Summary

The provided report focuses on the significance of management accounting in various contexts, including planning tools used in budgetary control. It highlights the importance of effective management accounting systems, different types of management accounting systems, and essential requirements. The report also discusses cost-evaluating techniques, advantages, and disadvantages of planning tools used in budgetary control.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Management accounting and the essential requirements of management accounting system

.....................................................................................................................................................1

B) Presenting financial information............................................................................................4

M1 Evaluate the benefits of management accounting systems and their application.................6

D1 Critically evaluate how management accounting system and report is integrated with in

business process..........................................................................................................................6

TASK 2............................................................................................................................................6

1. Absorption costing..................................................................................................................6

2. Marginal costing......................................................................................................................7

M2 Accurately apply the techniques and adjust profit to produce financial reporting document

.....................................................................................................................................................8

D2 Apply and interpret the data for the business activities........................................................8

TASK 3............................................................................................................................................8

a) Different kinds of budgets and their advantages and disadvantages......................................8

b) Budget preparation process including determination of price and different costing system..9

c) Importance of budgets as a tool for planning and control purpose.......................................10

M3 analyse the use of the different planning tools and their application for making budget...10

D3 evaluate how planning tools for accounting respond appropriately to solving financial

problem.....................................................................................................................................10

TASK 4..........................................................................................................................................10

M4 Analyse how management accounting lead organisation by solving financial problems. .11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Management accounting and the essential requirements of management accounting system

.....................................................................................................................................................1

B) Presenting financial information............................................................................................4

M1 Evaluate the benefits of management accounting systems and their application.................6

D1 Critically evaluate how management accounting system and report is integrated with in

business process..........................................................................................................................6

TASK 2............................................................................................................................................6

1. Absorption costing..................................................................................................................6

2. Marginal costing......................................................................................................................7

M2 Accurately apply the techniques and adjust profit to produce financial reporting document

.....................................................................................................................................................8

D2 Apply and interpret the data for the business activities........................................................8

TASK 3............................................................................................................................................8

a) Different kinds of budgets and their advantages and disadvantages......................................8

b) Budget preparation process including determination of price and different costing system..9

c) Importance of budgets as a tool for planning and control purpose.......................................10

M3 analyse the use of the different planning tools and their application for making budget...10

D3 evaluate how planning tools for accounting respond appropriately to solving financial

problem.....................................................................................................................................10

TASK 4..........................................................................................................................................10

M4 Analyse how management accounting lead organisation by solving financial problems. .11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting and techniques combine used in organisation. Enhancing

decision making skills and improving management business skills is main objective of

management accounting (Qian, Burritt and Monroe, 2011. This report is prepared to analyse the

meaning of management accounting. Essential requirement of management accounting system

explained in this report. Financial information used in management accounting reports and

importance of management accounting information to understand defined in this context. Cost

techniques are used to evaluate profit and planning and tools which are used in planning and

control purpose. Advantages and disadvantages and importance of planning in respect of

decision making defined in this context. How Tech (UK) adopted management accounting

system to overcome financial problems illustrated in this report.

TASK 1

A) Management accounting and the essential requirements of management accounting system

Management accounting

Assisting managerial decision and decision making process management accounting

system is adapted by organisation. This is one of the essential tool which is use for better

management and operation of business divisions. Management accounting is a combination of

management accounting techniques and tools which assist management decisions and strategic

planing. Management accounting is considered as a professional course which remain based

upon professional tactics (Management accounting and its importance, 2017).

1. Distinguishing Management accounting from financial accounting

Basis of difference Management accounting Financial accounting

Purpose Providing relevant data and

sources for better forecasting

and budgeting of plans is main

purpose of management

accounting.

Recording day to day financial

transactions and preparing financial

reports is one of the main purpose of

financial accounting.

Objective Making planning and decision

making process more strong and

flexible is main objective of

Managing financial resources with

effective financial management is the

main objective of financial accounting.

1

Management accounting and techniques combine used in organisation. Enhancing

decision making skills and improving management business skills is main objective of

management accounting (Qian, Burritt and Monroe, 2011. This report is prepared to analyse the

meaning of management accounting. Essential requirement of management accounting system

explained in this report. Financial information used in management accounting reports and

importance of management accounting information to understand defined in this context. Cost

techniques are used to evaluate profit and planning and tools which are used in planning and

control purpose. Advantages and disadvantages and importance of planning in respect of

decision making defined in this context. How Tech (UK) adopted management accounting

system to overcome financial problems illustrated in this report.

TASK 1

A) Management accounting and the essential requirements of management accounting system

Management accounting

Assisting managerial decision and decision making process management accounting

system is adapted by organisation. This is one of the essential tool which is use for better

management and operation of business divisions. Management accounting is a combination of

management accounting techniques and tools which assist management decisions and strategic

planing. Management accounting is considered as a professional course which remain based

upon professional tactics (Management accounting and its importance, 2017).

1. Distinguishing Management accounting from financial accounting

Basis of difference Management accounting Financial accounting

Purpose Providing relevant data and

sources for better forecasting

and budgeting of plans is main

purpose of management

accounting.

Recording day to day financial

transactions and preparing financial

reports is one of the main purpose of

financial accounting.

Objective Making planning and decision

making process more strong and

flexible is main objective of

Managing financial resources with

effective financial management is the

main objective of financial accounting.

1

management accounting. Preparing financial statements and

reports to make financial plans.

Users Management accounting

information and data are used

for internal purpose of

organisation. It helps to analyse

the effectiveness of management

decisions and plans. Managers,

senior level authorities are

considered main users under

management accounting.

Suppliers, debtors, financial institutions,

stockholders, shareholders, government

and external parties are known as main

users under financial accounting. These

are also called as stakeholders of

organisation. These users may be

business partners, well wishers or

financial critics.

Reports Management reports remain

essential for internal parties of

organisation. Job cost reports,

budgetary reports and inventory

management reports are some

essential reports which are

prepared under management

accounting.

Financial reports such as income and

expenditure statements, profit and loss

statements and financial position

statements are main reports which are

prepared in financial accounting.

2. Importance of management accounting information as a decision making tool for

departmental managers

Management accounting system is also illustrated as managerial accounting. Majorly

management accounting remain associated with business operations and managements (Shah,

Malik and Malik, 2011). It is an internal part of management and operations which assist

managers to maintain ethical order with in organisation. Informations and data which are

prepared under management accounting system are basically use to making financial plans and

strategies. Managers take help of management reports to find out management issues and

problems which occurs while decision making process.

Management accounting system will help Tech UK in various ways such as:

2

reports to make financial plans.

Users Management accounting

information and data are used

for internal purpose of

organisation. It helps to analyse

the effectiveness of management

decisions and plans. Managers,

senior level authorities are

considered main users under

management accounting.

Suppliers, debtors, financial institutions,

stockholders, shareholders, government

and external parties are known as main

users under financial accounting. These

are also called as stakeholders of

organisation. These users may be

business partners, well wishers or

financial critics.

Reports Management reports remain

essential for internal parties of

organisation. Job cost reports,

budgetary reports and inventory

management reports are some

essential reports which are

prepared under management

accounting.

Financial reports such as income and

expenditure statements, profit and loss

statements and financial position

statements are main reports which are

prepared in financial accounting.

2. Importance of management accounting information as a decision making tool for

departmental managers

Management accounting system is also illustrated as managerial accounting. Majorly

management accounting remain associated with business operations and managements (Shah,

Malik and Malik, 2011). It is an internal part of management and operations which assist

managers to maintain ethical order with in organisation. Informations and data which are

prepared under management accounting system are basically use to making financial plans and

strategies. Managers take help of management reports to find out management issues and

problems which occurs while decision making process.

Management accounting system will help Tech UK in various ways such as:

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Analysing aim: it provides various type of financial and non financial analysis reports

which used in decision making process. There is an analysis and evaluation done by mangers and

accountants subjecting creating aims and objectives of organisation. Analysis is done subject to

actual results and and targets with estimated and budgeted targets.

Assisting managers to make plans: this process helps in managing and retaining

financial and non financial transactions in books (Vaivio and Sirén, 2010). All these transaction

are consolidated in the end of financial year and summarised reports are published to stake

holders and internal parties of organisation. Managers take helps of these reports and information

to prepare plans and strategies.

Analysing performance: Analysing the performance for better management and

effective operation is one of the main objective of management accounting. Management

accounting helps to analyse the performance of different departments of business in proper

manner. It provides opportunities to compare existent performance of employees with budgeted

results and outcomes.

3. Cost accounting system

Cost is one of the measurable aspect which helps to analyse the cost of operations and

bifurcating the cost among individual products. This accounting system is popular accounting

system which is used by manufacturing and production organisation. This accounting system

provides path and system to analyse the cost of goods sold, cost incurred in operations and

production process. There are two type of cost are found in organisational context such as direct

cost and indirect cost.

Cost which remain directly part of manufacturing and production process is considered as

direct cost. Direct material, direct cost and direct expenses are some essential part of managerial

direct cost. Cost which do not remain the part of manufacturing process is considered as indirect

cost. Selling and distribution expenses, advertising are some indirect expenses and cost which

are called indirect cost.

4. Inventory management system

this accounting system basically used to manage the level of raw material for producing

required amount of production units. Economic order quantity method is the part of inventory

management system which helps to analyse the production life cycle (Van Helden and Northcott,

2010). It assist stock managers and accountants to analyse the requirement of stocks, wastage,

3

which used in decision making process. There is an analysis and evaluation done by mangers and

accountants subjecting creating aims and objectives of organisation. Analysis is done subject to

actual results and and targets with estimated and budgeted targets.

Assisting managers to make plans: this process helps in managing and retaining

financial and non financial transactions in books (Vaivio and Sirén, 2010). All these transaction

are consolidated in the end of financial year and summarised reports are published to stake

holders and internal parties of organisation. Managers take helps of these reports and information

to prepare plans and strategies.

Analysing performance: Analysing the performance for better management and

effective operation is one of the main objective of management accounting. Management

accounting helps to analyse the performance of different departments of business in proper

manner. It provides opportunities to compare existent performance of employees with budgeted

results and outcomes.

3. Cost accounting system

Cost is one of the measurable aspect which helps to analyse the cost of operations and

bifurcating the cost among individual products. This accounting system is popular accounting

system which is used by manufacturing and production organisation. This accounting system

provides path and system to analyse the cost of goods sold, cost incurred in operations and

production process. There are two type of cost are found in organisational context such as direct

cost and indirect cost.

Cost which remain directly part of manufacturing and production process is considered as

direct cost. Direct material, direct cost and direct expenses are some essential part of managerial

direct cost. Cost which do not remain the part of manufacturing process is considered as indirect

cost. Selling and distribution expenses, advertising are some indirect expenses and cost which

are called indirect cost.

4. Inventory management system

this accounting system basically used to manage the level of raw material for producing

required amount of production units. Economic order quantity method is the part of inventory

management system which helps to analyse the production life cycle (Van Helden and Northcott,

2010). It assist stock managers and accountants to analyse the requirement of stocks, wastage,

3

scrape and cost of closing stock. This management accounting system will help Tech UK to

utilise optimum requirement of resources for manufacturing goods and products. It helps to

detect that how much amount of stocks are required for individual departments and sections. To

achieve individual goals and objectives inventory management system plays significant role.

5. Job costing system

There is a vital role and importance found of job costing system in large organisations

and divisions. This accounting system helps to analyse the cost of individual departments and

divisions. Job costing system determine and classify the cost as per cost nature (Garrison and et.

al., 2010). Organisations which deals in multi products and sections use job costing techniques.

This system aids to consolidate and centralise all over manufacturing and production cost in

single format. With the use of Job costing system Tech UK would be able to control raw

material, direct expenses and labour hours which are incurred in production process.

B) Presenting financial information

1. Different types of managerial accounting reports

Management accounting reports present the information and details related to

management can operation of business. These reports are the part of the planing and decision

making process. With assistance of management accounting reports managers and accountants

become eligible to analyse the effectiveness of management decisions and plans in better and

optimistic manner. Various type of management reports are prepared as per decision making and

strategic planning perspective.

Budget reports: these reports contains the detailed information about income and

expenditures incurred for a particular period. These reports analyse the actual and

budgeted results and detect the difference creating factors. Cost accountants and accounts

managers use the information and details to analyse the cost increasing factors and

aspects. Information which are provided through budgetary reports remain essential to

control cost. Performance of organisation evaluated on the basis of cost controlling

capacity of organisation.

Accounting receivable reports: How much amount to be collected from debtors and

creditors are maintained are mentioned in account receivable reports. These reports

contains all the essential details and information which remain associated with collection

process from customers and debtors (Macintosh and Quattrone, 2010). These reports

4

utilise optimum requirement of resources for manufacturing goods and products. It helps to

detect that how much amount of stocks are required for individual departments and sections. To

achieve individual goals and objectives inventory management system plays significant role.

5. Job costing system

There is a vital role and importance found of job costing system in large organisations

and divisions. This accounting system helps to analyse the cost of individual departments and

divisions. Job costing system determine and classify the cost as per cost nature (Garrison and et.

al., 2010). Organisations which deals in multi products and sections use job costing techniques.

This system aids to consolidate and centralise all over manufacturing and production cost in

single format. With the use of Job costing system Tech UK would be able to control raw

material, direct expenses and labour hours which are incurred in production process.

B) Presenting financial information

1. Different types of managerial accounting reports

Management accounting reports present the information and details related to

management can operation of business. These reports are the part of the planing and decision

making process. With assistance of management accounting reports managers and accountants

become eligible to analyse the effectiveness of management decisions and plans in better and

optimistic manner. Various type of management reports are prepared as per decision making and

strategic planning perspective.

Budget reports: these reports contains the detailed information about income and

expenditures incurred for a particular period. These reports analyse the actual and

budgeted results and detect the difference creating factors. Cost accountants and accounts

managers use the information and details to analyse the cost increasing factors and

aspects. Information which are provided through budgetary reports remain essential to

control cost. Performance of organisation evaluated on the basis of cost controlling

capacity of organisation.

Accounting receivable reports: How much amount to be collected from debtors and

creditors are maintained are mentioned in account receivable reports. These reports

contains all the essential details and information which remain associated with collection

process from customers and debtors (Macintosh and Quattrone, 2010). These reports

4

assist managers to estimate the collection period and rotation of cash flow with in the

organisation. By implementing accounting receivable reports managers of Tech UK will

be able to make optimum and effective credit limit for customers. It helps to manage the

bed debts or unrecoverable amounts from customers and debtors.

Inventory reports: these reports helps to analyse the consumption level of raw material

and resources. There is a brief information and details are discussed in these reports

which remain associated with manufacturing and productions process. Consumption rate,

amount of wastage, average inventory required to maintain break even sales and

production are some information which are mentioned in inventory reports.

Job cost reports: these reports contains information and details remain associated with

cost records of different department of organisation. High cost incurred and low cost

incurred areas are defined and identified in job cost reports.

2. Why it is important for the information to be presented in manner that must be

understandable

Management accounting reports has significant role to understand the complex business

situations and equations. Importance of management accounting reports can be categorised in

three manor parts which are as follows; Reducing loss: with the help of management accounting reports managers be able to

bifurcate the cost occurring factors which increase the cost of products and services.

Analysing actual requirement of resources and utilising them as per suitability of

organisation (Nandan, 2010). This enables the spirit of analysis of business problems and

situations. For example non manufacturing cost such as selling and distributing cost is

one of the essential aspect which reduce the loss and helps in reducing loss. Decision making: Accurate information and details assist managers and accountants to

make effective decision making or strategic planning process. It improves the decision

making process subject to preparing more accurate plans for growth and development.

Future planing, performance management and risk management are subject to effective

management information and details.

Improving financial returns: with the helps of accounting reports managers and

accountant analyse the effectiveness of investment and business plans. By improving the

scale of positive returns on investment is one of the main objective of management

5

organisation. By implementing accounting receivable reports managers of Tech UK will

be able to make optimum and effective credit limit for customers. It helps to manage the

bed debts or unrecoverable amounts from customers and debtors.

Inventory reports: these reports helps to analyse the consumption level of raw material

and resources. There is a brief information and details are discussed in these reports

which remain associated with manufacturing and productions process. Consumption rate,

amount of wastage, average inventory required to maintain break even sales and

production are some information which are mentioned in inventory reports.

Job cost reports: these reports contains information and details remain associated with

cost records of different department of organisation. High cost incurred and low cost

incurred areas are defined and identified in job cost reports.

2. Why it is important for the information to be presented in manner that must be

understandable

Management accounting reports has significant role to understand the complex business

situations and equations. Importance of management accounting reports can be categorised in

three manor parts which are as follows; Reducing loss: with the help of management accounting reports managers be able to

bifurcate the cost occurring factors which increase the cost of products and services.

Analysing actual requirement of resources and utilising them as per suitability of

organisation (Nandan, 2010). This enables the spirit of analysis of business problems and

situations. For example non manufacturing cost such as selling and distributing cost is

one of the essential aspect which reduce the loss and helps in reducing loss. Decision making: Accurate information and details assist managers and accountants to

make effective decision making or strategic planning process. It improves the decision

making process subject to preparing more accurate plans for growth and development.

Future planing, performance management and risk management are subject to effective

management information and details.

Improving financial returns: with the helps of accounting reports managers and

accountant analyse the effectiveness of investment and business plans. By improving the

scale of positive returns on investment is one of the main objective of management

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reports. Management accounting reports analyse the ability of extraordinary skills and

training to employees.

M1 Evaluate the benefits of management accounting systems and their application

Management accounting helps to resolve financial problems and as per nature and

operations of Tech UK, organisation has two options of implying management accounting

system such as

Job costing system: this accounting system will help to comprise the cost of various job

centre in single format. This helps to centralise overall cost of manufacturing.

Inventory management system: this management system helps to manage the order of

inventories, this management system remain associated with material management (Nixon and

Burns, 2012).

D1 Critically evaluate how management accounting system and report is integrated with in

business process

Various type of reports are produced under management accounting system which helps

managers to take important business decisions and plans. Management system is considered base

of which provides a path to retain the records and transactions for making management reports.

With effective management system management accounting reports can not be imagined by

organisation (Quinn, 2014).

TASK 2

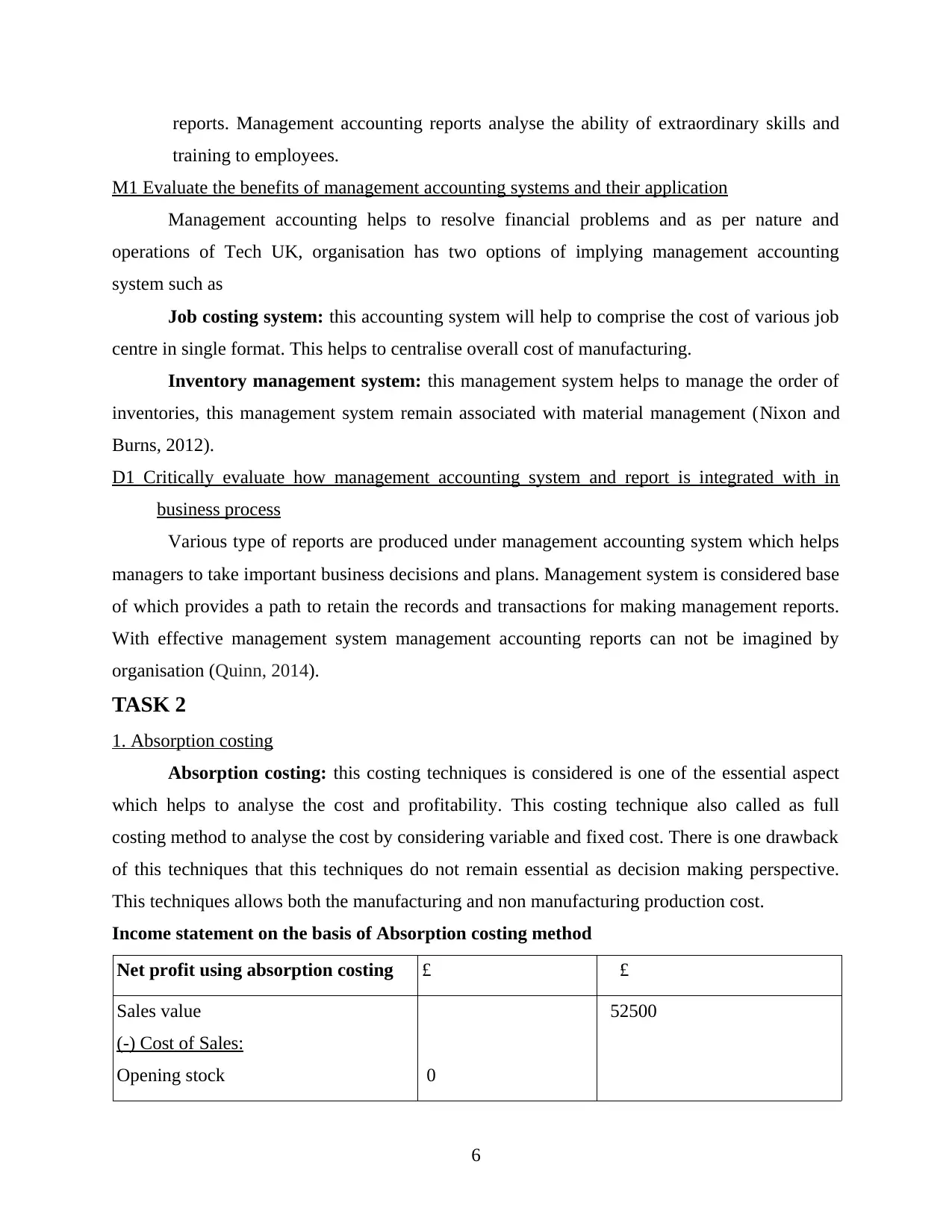

1. Absorption costing

Absorption costing: this costing techniques is considered is one of the essential aspect

which helps to analyse the cost and profitability. This costing technique also called as full

costing method to analyse the cost by considering variable and fixed cost. There is one drawback

of this techniques that this techniques do not remain essential as decision making perspective.

This techniques allows both the manufacturing and non manufacturing production cost.

Income statement on the basis of Absorption costing method

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock 0

52500

6

training to employees.

M1 Evaluate the benefits of management accounting systems and their application

Management accounting helps to resolve financial problems and as per nature and

operations of Tech UK, organisation has two options of implying management accounting

system such as

Job costing system: this accounting system will help to comprise the cost of various job

centre in single format. This helps to centralise overall cost of manufacturing.

Inventory management system: this management system helps to manage the order of

inventories, this management system remain associated with material management (Nixon and

Burns, 2012).

D1 Critically evaluate how management accounting system and report is integrated with in

business process

Various type of reports are produced under management accounting system which helps

managers to take important business decisions and plans. Management system is considered base

of which provides a path to retain the records and transactions for making management reports.

With effective management system management accounting reports can not be imagined by

organisation (Quinn, 2014).

TASK 2

1. Absorption costing

Absorption costing: this costing techniques is considered is one of the essential aspect

which helps to analyse the cost and profitability. This costing technique also called as full

costing method to analyse the cost by considering variable and fixed cost. There is one drawback

of this techniques that this techniques do not remain essential as decision making perspective.

This techniques allows both the manufacturing and non manufacturing production cost.

Income statement on the basis of Absorption costing method

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock 0

52500

6

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

40000

(10000)

7875

10000

(30000)

(5000)

17500

17875

(375)

Working note:

1. Calculation of cost of goods sold under absorption

costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

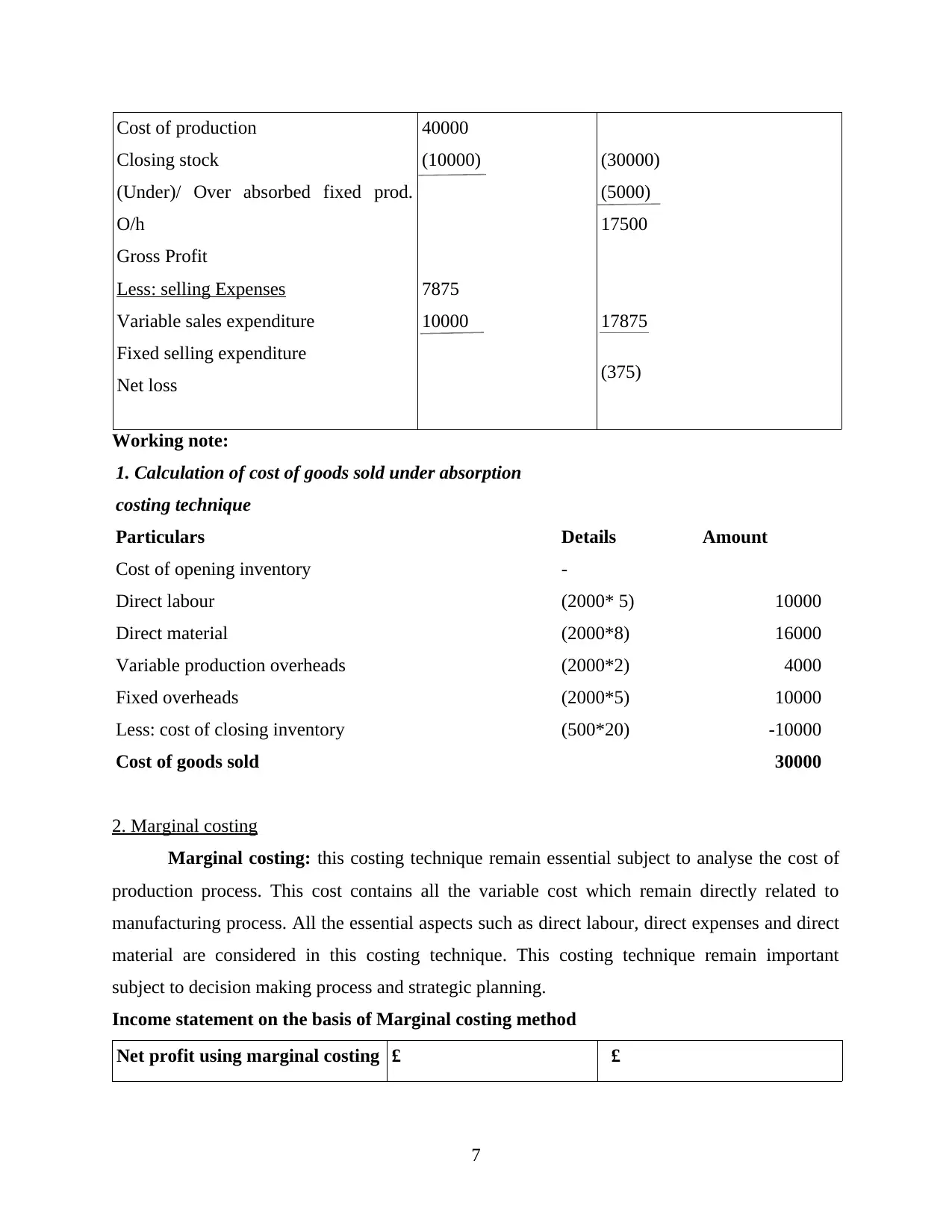

2. Marginal costing

Marginal costing: this costing technique remain essential subject to analyse the cost of

production process. This cost contains all the variable cost which remain directly related to

manufacturing process. All the essential aspects such as direct labour, direct expenses and direct

material are considered in this costing technique. This costing technique remain important

subject to decision making process and strategic planning.

Income statement on the basis of Marginal costing method

Net profit using marginal costing £ £

7

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

40000

(10000)

7875

10000

(30000)

(5000)

17500

17875

(375)

Working note:

1. Calculation of cost of goods sold under absorption

costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Fixed overheads (2000*5) 10000

Less: cost of closing inventory (500*20) -10000

Cost of goods sold 30000

2. Marginal costing

Marginal costing: this costing technique remain essential subject to analyse the cost of

production process. This cost contains all the variable cost which remain directly related to

manufacturing process. All the essential aspects such as direct labour, direct expenses and direct

material are considered in this costing technique. This costing technique remain important

subject to decision making process and strategic planning.

Income statement on the basis of Marginal costing method

Net profit using marginal costing £ £

7

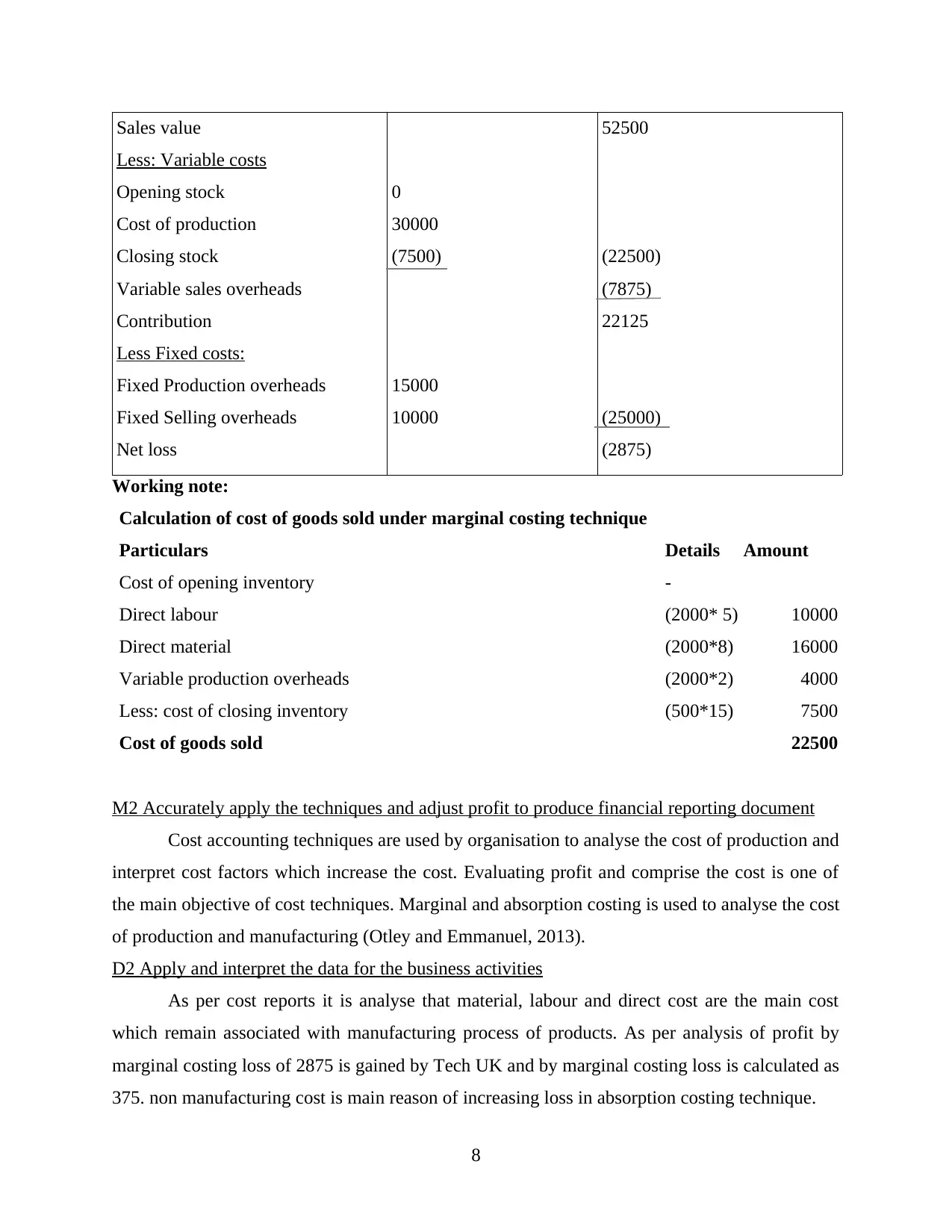

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Working note:

Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

M2 Accurately apply the techniques and adjust profit to produce financial reporting document

Cost accounting techniques are used by organisation to analyse the cost of production and

interpret cost factors which increase the cost. Evaluating profit and comprise the cost is one of

the main objective of cost techniques. Marginal and absorption costing is used to analyse the cost

of production and manufacturing (Otley and Emmanuel, 2013).

D2 Apply and interpret the data for the business activities

As per cost reports it is analyse that material, labour and direct cost are the main cost

which remain associated with manufacturing process of products. As per analysis of profit by

marginal costing loss of 2875 is gained by Tech UK and by marginal costing loss is calculated as

375. non manufacturing cost is main reason of increasing loss in absorption costing technique.

8

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Working note:

Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (2000* 5) 10000

Direct material (2000*8) 16000

Variable production overheads (2000*2) 4000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 22500

M2 Accurately apply the techniques and adjust profit to produce financial reporting document

Cost accounting techniques are used by organisation to analyse the cost of production and

interpret cost factors which increase the cost. Evaluating profit and comprise the cost is one of

the main objective of cost techniques. Marginal and absorption costing is used to analyse the cost

of production and manufacturing (Otley and Emmanuel, 2013).

D2 Apply and interpret the data for the business activities

As per cost reports it is analyse that material, labour and direct cost are the main cost

which remain associated with manufacturing process of products. As per analysis of profit by

marginal costing loss of 2875 is gained by Tech UK and by marginal costing loss is calculated as

375. non manufacturing cost is main reason of increasing loss in absorption costing technique.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TASK 3

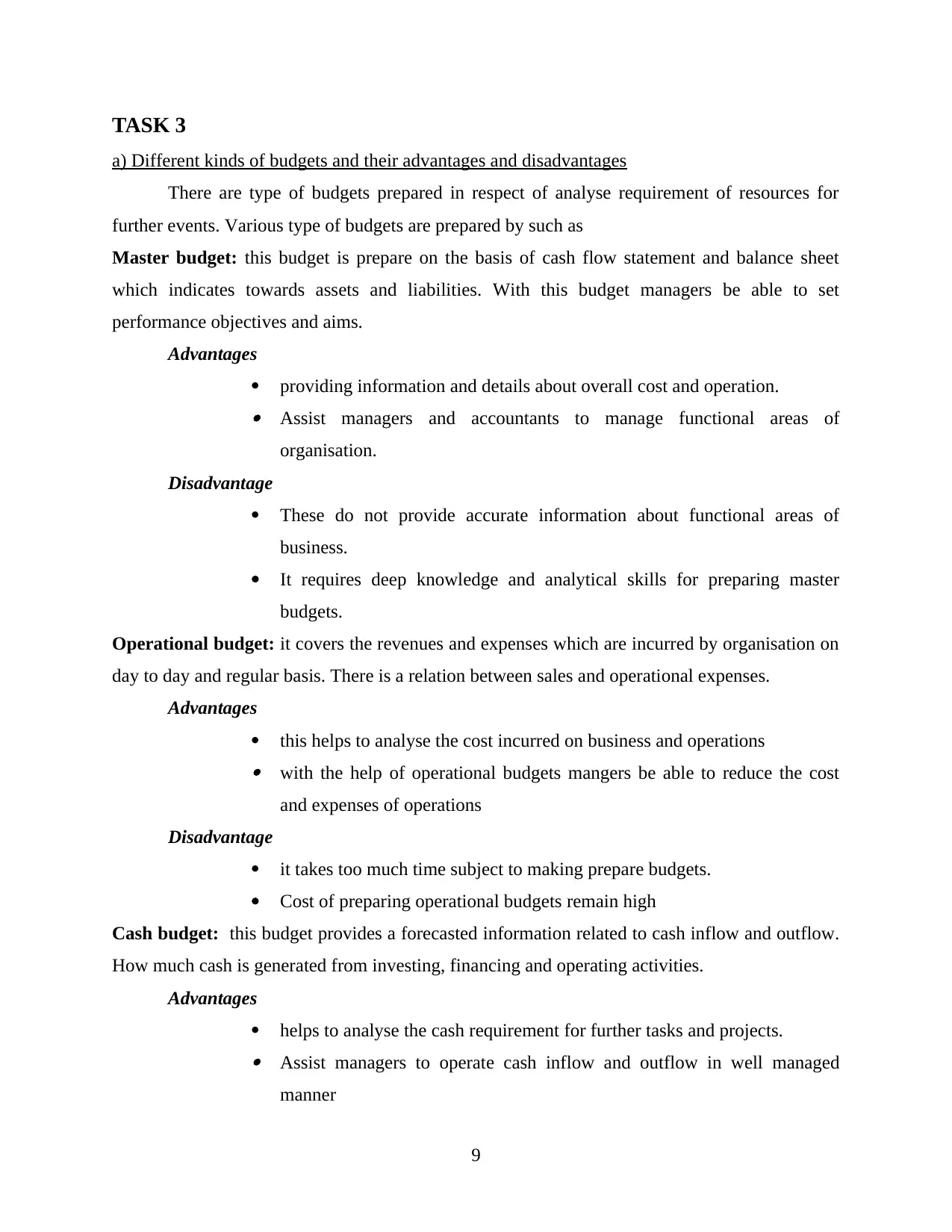

a) Different kinds of budgets and their advantages and disadvantages

There are type of budgets prepared in respect of analyse requirement of resources for

further events. Various type of budgets are prepared by such as

Master budget: this budget is prepare on the basis of cash flow statement and balance sheet

which indicates towards assets and liabilities. With this budget managers be able to set

performance objectives and aims.

Advantages

providing information and details about overall cost and operation.

Assist managers and accountants to manage functional areas of

organisation.

Disadvantage

These do not provide accurate information about functional areas of

business.

It requires deep knowledge and analytical skills for preparing master

budgets.

Operational budget: it covers the revenues and expenses which are incurred by organisation on

day to day and regular basis. There is a relation between sales and operational expenses.

Advantages

this helps to analyse the cost incurred on business and operations

with the help of operational budgets mangers be able to reduce the cost

and expenses of operations

Disadvantage

it takes too much time subject to making prepare budgets.

Cost of preparing operational budgets remain high

Cash budget: this budget provides a forecasted information related to cash inflow and outflow.

How much cash is generated from investing, financing and operating activities.

Advantages

helps to analyse the cash requirement for further tasks and projects.

Assist managers to operate cash inflow and outflow in well managed

manner

9

a) Different kinds of budgets and their advantages and disadvantages

There are type of budgets prepared in respect of analyse requirement of resources for

further events. Various type of budgets are prepared by such as

Master budget: this budget is prepare on the basis of cash flow statement and balance sheet

which indicates towards assets and liabilities. With this budget managers be able to set

performance objectives and aims.

Advantages

providing information and details about overall cost and operation.

Assist managers and accountants to manage functional areas of

organisation.

Disadvantage

These do not provide accurate information about functional areas of

business.

It requires deep knowledge and analytical skills for preparing master

budgets.

Operational budget: it covers the revenues and expenses which are incurred by organisation on

day to day and regular basis. There is a relation between sales and operational expenses.

Advantages

this helps to analyse the cost incurred on business and operations

with the help of operational budgets mangers be able to reduce the cost

and expenses of operations

Disadvantage

it takes too much time subject to making prepare budgets.

Cost of preparing operational budgets remain high

Cash budget: this budget provides a forecasted information related to cash inflow and outflow.

How much cash is generated from investing, financing and operating activities.

Advantages

helps to analyse the cash requirement for further tasks and projects.

Assist managers to operate cash inflow and outflow in well managed

manner

9

Disadvantage

Lack of accuracy in respect of future cash transactions and events

it is difficult to manage cash inflows and outflows for better management

and operation.

b) Budget preparation process including determination of price and different costing system

Pricing system Price skimming- this technique helps to increase sales records and maximising profit

graphs.

Economy Pricing- this method helps to retain the price of products on the basis of

customers choice.

Costing system Direct costing- cost evaluation of products and services depends upon direct cost

incurred in producing products. Direct cost, material and labour are example of direct

costing.

Standard costing: there is variance analysis done subject to controlling cost by

comparing standard and actual cost.

c) Importance of budgets as a tool for planning and control purpose

Budgeting tools helps to control the cost of operations and functions. All the main aspects

are analysed with the help of planing and controlling purpose. Creation of financial roadmap,

centralise expenditure size is one of the main objective of planning and controlling process.

M3 analyse the use of the different planning tools and their application for making budget

Planning and forecasting tools helps to analyse the budgets for income and expenditure. It

not only helps to analyse future complex situation but also helps to analyse growth and

development opportunities for organisation (Hilton and Platt, 2013). Planning tools assist

decision making process and analyse information for better forecast. It helps to achieve desired

aims and objective of organisation in respect by estimating future events.

D3 evaluate how planning tools for accounting respond appropriately to solving financial

problem

As per profitability and financial analysis of Tech UK, it is resulted that the organisation

is being loss. Effective budgetary policy would help to overcome with this financial problem.

Various type of forecasting tools are used in budgetary control process which helps to make

10

Lack of accuracy in respect of future cash transactions and events

it is difficult to manage cash inflows and outflows for better management

and operation.

b) Budget preparation process including determination of price and different costing system

Pricing system Price skimming- this technique helps to increase sales records and maximising profit

graphs.

Economy Pricing- this method helps to retain the price of products on the basis of

customers choice.

Costing system Direct costing- cost evaluation of products and services depends upon direct cost

incurred in producing products. Direct cost, material and labour are example of direct

costing.

Standard costing: there is variance analysis done subject to controlling cost by

comparing standard and actual cost.

c) Importance of budgets as a tool for planning and control purpose

Budgeting tools helps to control the cost of operations and functions. All the main aspects

are analysed with the help of planing and controlling purpose. Creation of financial roadmap,

centralise expenditure size is one of the main objective of planning and controlling process.

M3 analyse the use of the different planning tools and their application for making budget

Planning and forecasting tools helps to analyse the budgets for income and expenditure. It

not only helps to analyse future complex situation but also helps to analyse growth and

development opportunities for organisation (Hilton and Platt, 2013). Planning tools assist

decision making process and analyse information for better forecast. It helps to achieve desired

aims and objective of organisation in respect by estimating future events.

D3 evaluate how planning tools for accounting respond appropriately to solving financial

problem

As per profitability and financial analysis of Tech UK, it is resulted that the organisation

is being loss. Effective budgetary policy would help to overcome with this financial problem.

Various type of forecasting tools are used in budgetary control process which helps to make

10

budgets and plans to estimate cost and prevent extra cost (Fullerton, Kennedy and Widener,

2014).

TASK 4

Tech UK limited recently gain a loss of £1.5 million due to which its financial

performance get affected. There are some solutions provided by the organisation to resolve this

financial problem which are defined as follow:

Balance scorecard approach

this approach is bifurcated in four perspectives

Analysing Financial requirements and needs

information provided to Customer and stakeholder

Internal process such as achieving efficiency and quality.

Analysing Organisational capacity subject to deal with financial risk and uncertainties.

M4 Analyse how management accounting lead organisation by solving financial problems

Management accounting system manoeuvres managing operations and functions of

organisation. It also assist managers and accountants to identify financial problems and provides

appropriate solutions. Analysis of financial statement to determine financial performance of

organisation is one of the effecting technique which is used in management accounting (Soin

and Collier, 2013).

CONCLUSION

This reports is prepared to elaborate the meaning of management accounting system.

How management decisions and plans are made with the help of effective management

accounting system is illustrated in this context. Various type of management accounting system

and essential requirement of management accounting system defined in this context. Importance

of management accounting reports in decision making process discussed in organisational

context. Cost evaluating techniques are illustrated with practical based scenario. Advantages and

disadvantages of planning tools used in budgetary control defined in this report.

11

2014).

TASK 4

Tech UK limited recently gain a loss of £1.5 million due to which its financial

performance get affected. There are some solutions provided by the organisation to resolve this

financial problem which are defined as follow:

Balance scorecard approach

this approach is bifurcated in four perspectives

Analysing Financial requirements and needs

information provided to Customer and stakeholder

Internal process such as achieving efficiency and quality.

Analysing Organisational capacity subject to deal with financial risk and uncertainties.

M4 Analyse how management accounting lead organisation by solving financial problems

Management accounting system manoeuvres managing operations and functions of

organisation. It also assist managers and accountants to identify financial problems and provides

appropriate solutions. Analysis of financial statement to determine financial performance of

organisation is one of the effecting technique which is used in management accounting (Soin

and Collier, 2013).

CONCLUSION

This reports is prepared to elaborate the meaning of management accounting system.

How management decisions and plans are made with the help of effective management

accounting system is illustrated in this context. Various type of management accounting system

and essential requirement of management accounting system defined in this context. Importance

of management accounting reports in decision making process discussed in organisational

context. Cost evaluating techniques are illustrated with practical based scenario. Advantages and

disadvantages of planning tools used in budgetary control defined in this report.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability

Journal. 24(1). pp.93-128.

Shah, H., Malik, A. and Malik, M.S., 2011. Strategic Management Accounting-A Messiah For

Management Accounting?. Australian Journal of Business and Management Research.

1(4). p.1.

Vaivio, J. and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive

management accounting research. Management Accounting Research. 21(2). pp.130-

141.

Van Helden, G.J. and Northcott, D., 2010. Examining the practical relevance of public sector

management accounting research. Financial Accountability & Management. 26(2).

pp.213-240.

Garrison, R.H. And et. al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Nandan, R., 2010. Management accounting needs of SMEs and the role of professional

accountants: A renewed research agenda. Journal of applied management accounting

research. 8(1). p.65.

Nixon, B. and Burns, J., 2012. The paradox of strategic management accounting. Management

Accounting Research. 23(4). pp.229-244.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Hilton, R. W. and Platt, D. E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and

control.

Quinn, M., 2014. Stability and change in management accounting over time—A century or so of

evidence from Guinness. Management Accounting Research. 25(1). pp.76-92.

Online:

Management accounting and its importance, 2017. [Online]. Available through:

<https://www.invensis.net/blog/finance-and-accounting/what-is-management-

accounting-and-its-importance/>.

12

Books and Journals:

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability

Journal. 24(1). pp.93-128.

Shah, H., Malik, A. and Malik, M.S., 2011. Strategic Management Accounting-A Messiah For

Management Accounting?. Australian Journal of Business and Management Research.

1(4). p.1.

Vaivio, J. and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive

management accounting research. Management Accounting Research. 21(2). pp.130-

141.

Van Helden, G.J. and Northcott, D., 2010. Examining the practical relevance of public sector

management accounting research. Financial Accountability & Management. 26(2).

pp.213-240.

Garrison, R.H. And et. al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Nandan, R., 2010. Management accounting needs of SMEs and the role of professional

accountants: A renewed research agenda. Journal of applied management accounting

research. 8(1). p.65.

Nixon, B. and Burns, J., 2012. The paradox of strategic management accounting. Management

Accounting Research. 23(4). pp.229-244.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Hilton, R. W. and Platt, D. E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

Fullerton, R. R., Kennedy, F. A. and Widener, S. K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and

control.

Quinn, M., 2014. Stability and change in management accounting over time—A century or so of

evidence from Guinness. Management Accounting Research. 25(1). pp.76-92.

Online:

Management accounting and its importance, 2017. [Online]. Available through:

<https://www.invensis.net/blog/finance-and-accounting/what-is-management-

accounting-and-its-importance/>.

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.