(PDF) Management Accounting Techniques

VerifiedAdded on 2021/02/20

|20

|4020

|457

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO 1.................................................................................................................................................1

P 1. Management accounting and its system. ............................................................................1

P 2. MA reporting.......................................................................................................................3

M 1. Benefits of MA systems.....................................................................................................4

D 1. Critical evaluation of MA systems and MA Report............................................................5

P 3. Calculate costs using appropriate techniques......................................................................5

P 4. Benefits and limitations of budgetary tools.......................................................................13

M 3. Forecasting budgetary tools..............................................................................................14

P 5. Comparing organizations to respond to financial problems through management

accounting systems...................................................................................................................15

M 4. Assessment of how resolving financial problems, lead organizations to sustainable

success.......................................................................................................................................15

D 3. Critically evaluating planning tools to solve financial problems......................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

LO 1.................................................................................................................................................1

P 1. Management accounting and its system. ............................................................................1

P 2. MA reporting.......................................................................................................................3

M 1. Benefits of MA systems.....................................................................................................4

D 1. Critical evaluation of MA systems and MA Report............................................................5

P 3. Calculate costs using appropriate techniques......................................................................5

P 4. Benefits and limitations of budgetary tools.......................................................................13

M 3. Forecasting budgetary tools..............................................................................................14

P 5. Comparing organizations to respond to financial problems through management

accounting systems...................................................................................................................15

M 4. Assessment of how resolving financial problems, lead organizations to sustainable

success.......................................................................................................................................15

D 3. Critically evaluating planning tools to solve financial problems......................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is an impelling process which helps in rendering and preparing

timely statistical and financial data to the internal management of the organization in order to

take effective strategic decision.

This study includes, management accounting techniques and also include various key

functions and elements of MA system. It will also critically evaluate the different methods used

in the management accounting reports. This study will further analyse the cost of the company

using various appropriate techniques in order to get effective results and outcomes. Furthermore,

this study will help in examining the benefits and limitations of different planning tools which

are used in budget control. This study will further, compare different organization who are

adapting to different management accounting system to solve varied financial problems

effectively.

Arcadia group is a multinational retail company which was founded in the year 2002.

This company mainly deals in clothes, accessories and shoes.

MAIN BODY

LO 1

P 1. Management accounting and its system.

Management accounting (MA) is an impelling process which helps in rendering and

preparing timely statistical and financial data to the internal management of the organization in

order to take effective strategic decision (Kaplan and Atkinson, 2015). It is an effective process

of formulating and preparing various management accounting reports which helps management

of the Arcadia group in taking in strategic decision on a timely manner without any delay.

Management accounting helps in planning, solving various financial problems, strategic decision

making and strategic management.

The main function of management accounting is to determine and evaluate the

profitability and operations of the organization. It also helps in forecasting the future which leads

to strategic decision making. Management accounting aids in financial accounting, variance

analysis and capital budgeting reasoning. It also helps in break even analysis, new product

analysis and stock valuation. Management accounting also facilitates in controlling cost of the

1

Management accounting is an impelling process which helps in rendering and preparing

timely statistical and financial data to the internal management of the organization in order to

take effective strategic decision.

This study includes, management accounting techniques and also include various key

functions and elements of MA system. It will also critically evaluate the different methods used

in the management accounting reports. This study will further analyse the cost of the company

using various appropriate techniques in order to get effective results and outcomes. Furthermore,

this study will help in examining the benefits and limitations of different planning tools which

are used in budget control. This study will further, compare different organization who are

adapting to different management accounting system to solve varied financial problems

effectively.

Arcadia group is a multinational retail company which was founded in the year 2002.

This company mainly deals in clothes, accessories and shoes.

MAIN BODY

LO 1

P 1. Management accounting and its system.

Management accounting (MA) is an impelling process which helps in rendering and

preparing timely statistical and financial data to the internal management of the organization in

order to take effective strategic decision (Kaplan and Atkinson, 2015). It is an effective process

of formulating and preparing various management accounting reports which helps management

of the Arcadia group in taking in strategic decision on a timely manner without any delay.

Management accounting helps in planning, solving various financial problems, strategic decision

making and strategic management.

The main function of management accounting is to determine and evaluate the

profitability and operations of the organization. It also helps in forecasting the future which leads

to strategic decision making. Management accounting aids in financial accounting, variance

analysis and capital budgeting reasoning. It also helps in break even analysis, new product

analysis and stock valuation. Management accounting also facilitates in controlling cost of the

1

business and serves as an effective mean for communication for strategic management and

decision making.

MA system

MA system helps in effective planning and taking strategic decision in order to reach

better results and outcomes for Arcadia group (Clarke and et.al., 2019). It is an effective process

that helps internal management of the company to effectively evaluate the operations of the

business with utmost accuracy and efficiency. This helps in forecasting the future and take

strategic decision in order to achieve goals and objective of the organization.

System of Management accounting helps in reducing cost and controlling the operations

of the business. It is also beneficial in measuring the actual performance by comparing it with the

management accounting and budgeted reports. It helps in effective decision making by lessening

the ambiguity.

Cost accounting system: This is also known as product costing system which helps in

effectively computating the cost of the various products of the company in order to analyse the

profit, cost control and inventory evaluation (Shields, 2018). This system helps in recording and

presenting various financial data.

Inventory management system: It is an effective management accounting system which

effectively evaluates the level of resources required for the production and operation of the

business. Inventory management system helps in tracking the orders, various inventory levels,

sales and deliveries (Kaplan and Atkinson, 2015). The various examples associated with

inventory management system is LIFO, FIFO and weighted average.

Job costing system: This is a strategic process that accumulates and assign cost to the

various per unit of the production. This system helps in keeping proper track of the various

expenses and accumulating cost to each unit by categorizing them into direct material, direct

labour and overhead cost.

Price optimization system: This is an effective MA system that determines and evaluate

the behaviour of the customers in relation to the change in the prices of the various products and

services of the company. This method focuses on finding the perfect balance between the value

and price of the product to generate higher profits.

2

decision making.

MA system

MA system helps in effective planning and taking strategic decision in order to reach

better results and outcomes for Arcadia group (Clarke and et.al., 2019). It is an effective process

that helps internal management of the company to effectively evaluate the operations of the

business with utmost accuracy and efficiency. This helps in forecasting the future and take

strategic decision in order to achieve goals and objective of the organization.

System of Management accounting helps in reducing cost and controlling the operations

of the business. It is also beneficial in measuring the actual performance by comparing it with the

management accounting and budgeted reports. It helps in effective decision making by lessening

the ambiguity.

Cost accounting system: This is also known as product costing system which helps in

effectively computating the cost of the various products of the company in order to analyse the

profit, cost control and inventory evaluation (Shields, 2018). This system helps in recording and

presenting various financial data.

Inventory management system: It is an effective management accounting system which

effectively evaluates the level of resources required for the production and operation of the

business. Inventory management system helps in tracking the orders, various inventory levels,

sales and deliveries (Kaplan and Atkinson, 2015). The various examples associated with

inventory management system is LIFO, FIFO and weighted average.

Job costing system: This is a strategic process that accumulates and assign cost to the

various per unit of the production. This system helps in keeping proper track of the various

expenses and accumulating cost to each unit by categorizing them into direct material, direct

labour and overhead cost.

Price optimization system: This is an effective MA system that determines and evaluate

the behaviour of the customers in relation to the change in the prices of the various products and

services of the company. This method focuses on finding the perfect balance between the value

and price of the product to generate higher profits.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

P 2. MA reporting.

Management accounting reporting constitutes of preparing various managerial reports for

the internal stakeholders of the Arcadia group in order to take strategic decision for future

sustainable growth. It also provides clear view about the performance and finances of the

company which leads to strategic management and decision making. There are various types of

Management accounting reports in order to evaluate the performance of the organization:

Budget report: This is one of the crucial MA report that helps company in evaluating the

past performance of the organisation and setting budget for the future. This report helps the

management of the organization in comparison the actual results with the budge plan, in order to

evaluate the deviation and take necessary action accordingly in order to reach greater heights and

productivity. This report also helps in analysing the performance of the company and also helps

in reducing cost. The key purpose of this report is to help management in evaluating the past

performance and setting standard is to achieve better productivity and attain higher profits.

Accounts receivable report: It is a critical tool that is useful in determining the invoices

which are due for the invoice payment. This report takes into consideration various credit

transactions and also critically evaluates the repayment capability of the customers. This is an

important tool which helps in evaluating the various invoices that are due for payment. Accounts

receivable report helps internal management of the organization in understanding the outstanding

receivables and time taken to recover the money which are due for payment. The key purpose of

this report is to help management in determining the amount of goods given on credit to the

customer also effectively evaluate the time taken to recover the cash for a specific period.

Performance report: This management accounting report helps in determining the

performance of the Arcadia group by comparing it with the budgeted plan (Clarke and et.al.,

2019). The key purpose of this report is to help management in controlling the cost of various

department which eventually leads to higher operational performance and productivity for the

Arcadia group. This is crucial for the company to keep a proper track on the efficiency of the

business and helps measure their strategy that helps in achieving strategic goals of the

institution. This report also helps in effectively analysing the performance of the each department

that contributes towards in achieving greater heights for future growth and development.

Cost report: This report aids in evaluating and estimating the cost of each activity in

terms of direct cost and indirect cost of material, labour and overhead. This method helps

3

Management accounting reporting constitutes of preparing various managerial reports for

the internal stakeholders of the Arcadia group in order to take strategic decision for future

sustainable growth. It also provides clear view about the performance and finances of the

company which leads to strategic management and decision making. There are various types of

Management accounting reports in order to evaluate the performance of the organization:

Budget report: This is one of the crucial MA report that helps company in evaluating the

past performance of the organisation and setting budget for the future. This report helps the

management of the organization in comparison the actual results with the budge plan, in order to

evaluate the deviation and take necessary action accordingly in order to reach greater heights and

productivity. This report also helps in analysing the performance of the company and also helps

in reducing cost. The key purpose of this report is to help management in evaluating the past

performance and setting standard is to achieve better productivity and attain higher profits.

Accounts receivable report: It is a critical tool that is useful in determining the invoices

which are due for the invoice payment. This report takes into consideration various credit

transactions and also critically evaluates the repayment capability of the customers. This is an

important tool which helps in evaluating the various invoices that are due for payment. Accounts

receivable report helps internal management of the organization in understanding the outstanding

receivables and time taken to recover the money which are due for payment. The key purpose of

this report is to help management in determining the amount of goods given on credit to the

customer also effectively evaluate the time taken to recover the cash for a specific period.

Performance report: This management accounting report helps in determining the

performance of the Arcadia group by comparing it with the budgeted plan (Clarke and et.al.,

2019). The key purpose of this report is to help management in controlling the cost of various

department which eventually leads to higher operational performance and productivity for the

Arcadia group. This is crucial for the company to keep a proper track on the efficiency of the

business and helps measure their strategy that helps in achieving strategic goals of the

institution. This report also helps in effectively analysing the performance of the each department

that contributes towards in achieving greater heights for future growth and development.

Cost report: This report aids in evaluating and estimating the cost of each activity in

terms of direct cost and indirect cost of material, labour and overhead. This method helps

3

management of the organization in estimating the cost allocated in producing each unit of the

output (Types of Managerial Accounting Reports, 2019). It also helps in reducing wastage and

controlling cost of the Arcadia group. This report also helps in evaluating the profitability

attached with different types of departments. This helps in focusing on those departments that are

more profitable and beneficial for the growth of the Arcadia group. The key function of this

report is to help management of the organization to have a clear picture regarding the cost

attached with the production of various different units in an effective and efficient manner for

strategic decision making.

Other managerial report: This report mainly incudes competitor analysis report and

other project reports which are cruciate for the business. This report gives best outcomes that

eventually helps in profit management, investment management and cot control in order to take

strategic decision for future growth and expansion of the Arcadia group.

M 1. Benefits of MA systems.

Cost accounting system: Cost accounting system helps in evaluating the profitability of

the various activity carried out in the Arcadia group. It helps in reducing cost for higher

profitability and efficiency.

Inventory management system: It is beneficial in keeping proper track on the various

inventory orders and raw material of the Arcadia group (Top 10 Benefits of Great Inventory

Management, 2011). This helps in optimum utilization of resources on a timely and efficient

manner. This management accounting system helps in improvising employee efficiency and

productivity, saving time and cost cutting.

Job costing system: The major advantage of Job costing system is that it helps in

providing detailed analysis and interpretation of the cost of each job. It also helps in estimating

the cost and profitability attached with various other jobs in the production activity. This system

also helps in determining the defective and spoilage work which further helps in controlling the

cost of different jobs in Arcadia group.

Price optimization system: This system helps in effectively determining the objectives of

the Arcadia group in order to maximize the operating profit to reach greater heights. This method

helps in determining the price that helps in achieving economies of scale and leads to higher

generation of profits.

4

output (Types of Managerial Accounting Reports, 2019). It also helps in reducing wastage and

controlling cost of the Arcadia group. This report also helps in evaluating the profitability

attached with different types of departments. This helps in focusing on those departments that are

more profitable and beneficial for the growth of the Arcadia group. The key function of this

report is to help management of the organization to have a clear picture regarding the cost

attached with the production of various different units in an effective and efficient manner for

strategic decision making.

Other managerial report: This report mainly incudes competitor analysis report and

other project reports which are cruciate for the business. This report gives best outcomes that

eventually helps in profit management, investment management and cot control in order to take

strategic decision for future growth and expansion of the Arcadia group.

M 1. Benefits of MA systems.

Cost accounting system: Cost accounting system helps in evaluating the profitability of

the various activity carried out in the Arcadia group. It helps in reducing cost for higher

profitability and efficiency.

Inventory management system: It is beneficial in keeping proper track on the various

inventory orders and raw material of the Arcadia group (Top 10 Benefits of Great Inventory

Management, 2011). This helps in optimum utilization of resources on a timely and efficient

manner. This management accounting system helps in improvising employee efficiency and

productivity, saving time and cost cutting.

Job costing system: The major advantage of Job costing system is that it helps in

providing detailed analysis and interpretation of the cost of each job. It also helps in estimating

the cost and profitability attached with various other jobs in the production activity. This system

also helps in determining the defective and spoilage work which further helps in controlling the

cost of different jobs in Arcadia group.

Price optimization system: This system helps in effectively determining the objectives of

the Arcadia group in order to maximize the operating profit to reach greater heights. This method

helps in determining the price that helps in achieving economies of scale and leads to higher

generation of profits.

4

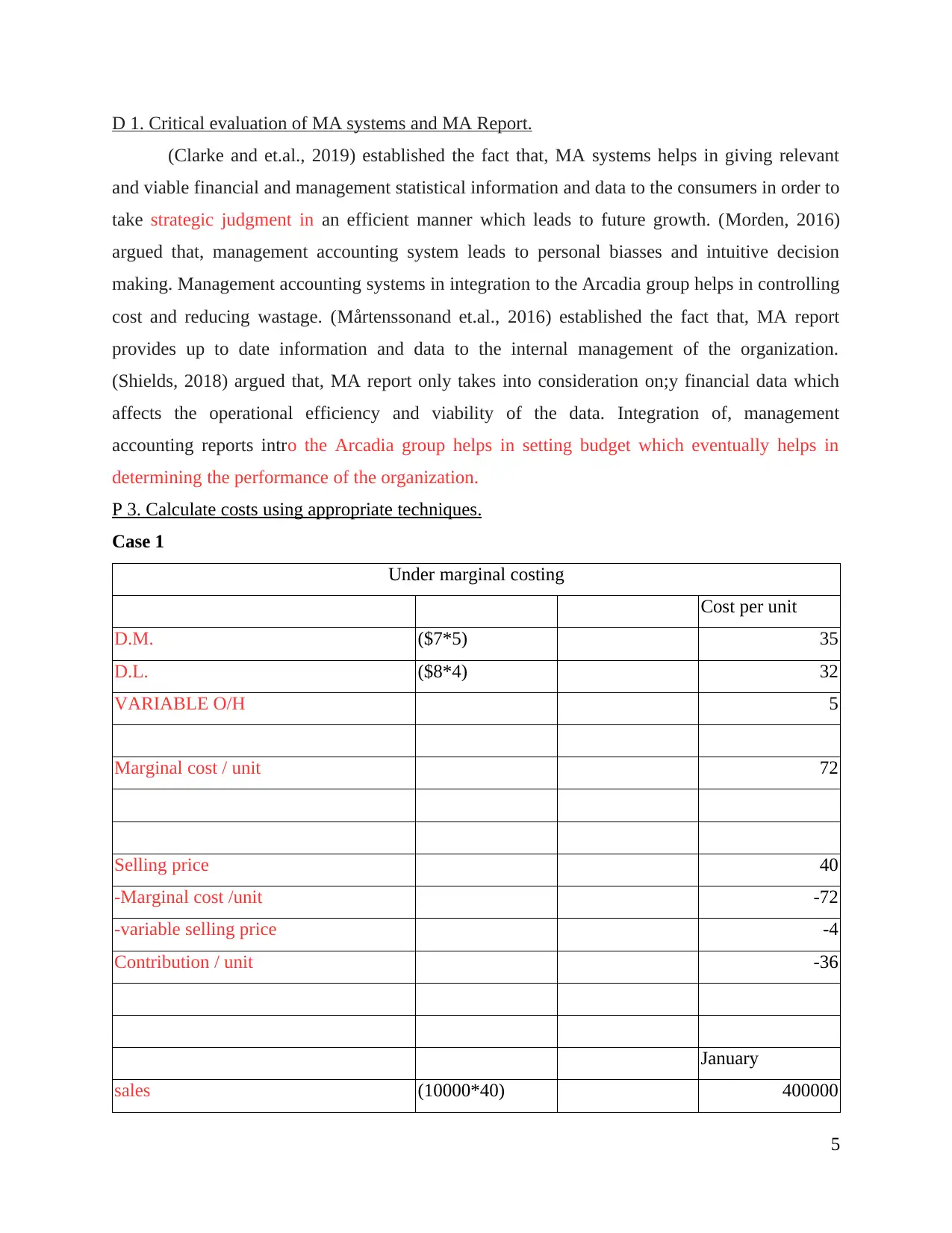

D 1. Critical evaluation of MA systems and MA Report.

(Clarke and et.al., 2019) established the fact that, MA systems helps in giving relevant

and viable financial and management statistical information and data to the consumers in order to

take strategic judgment in an efficient manner which leads to future growth. (Morden, 2016)

argued that, management accounting system leads to personal biasses and intuitive decision

making. Management accounting systems in integration to the Arcadia group helps in controlling

cost and reducing wastage. (Mårtenssonand et.al., 2016) established the fact that, MA report

provides up to date information and data to the internal management of the organization.

(Shields, 2018) argued that, MA report only takes into consideration on;y financial data which

affects the operational efficiency and viability of the data. Integration of, management

accounting reports intro the Arcadia group helps in setting budget which eventually helps in

determining the performance of the organization.

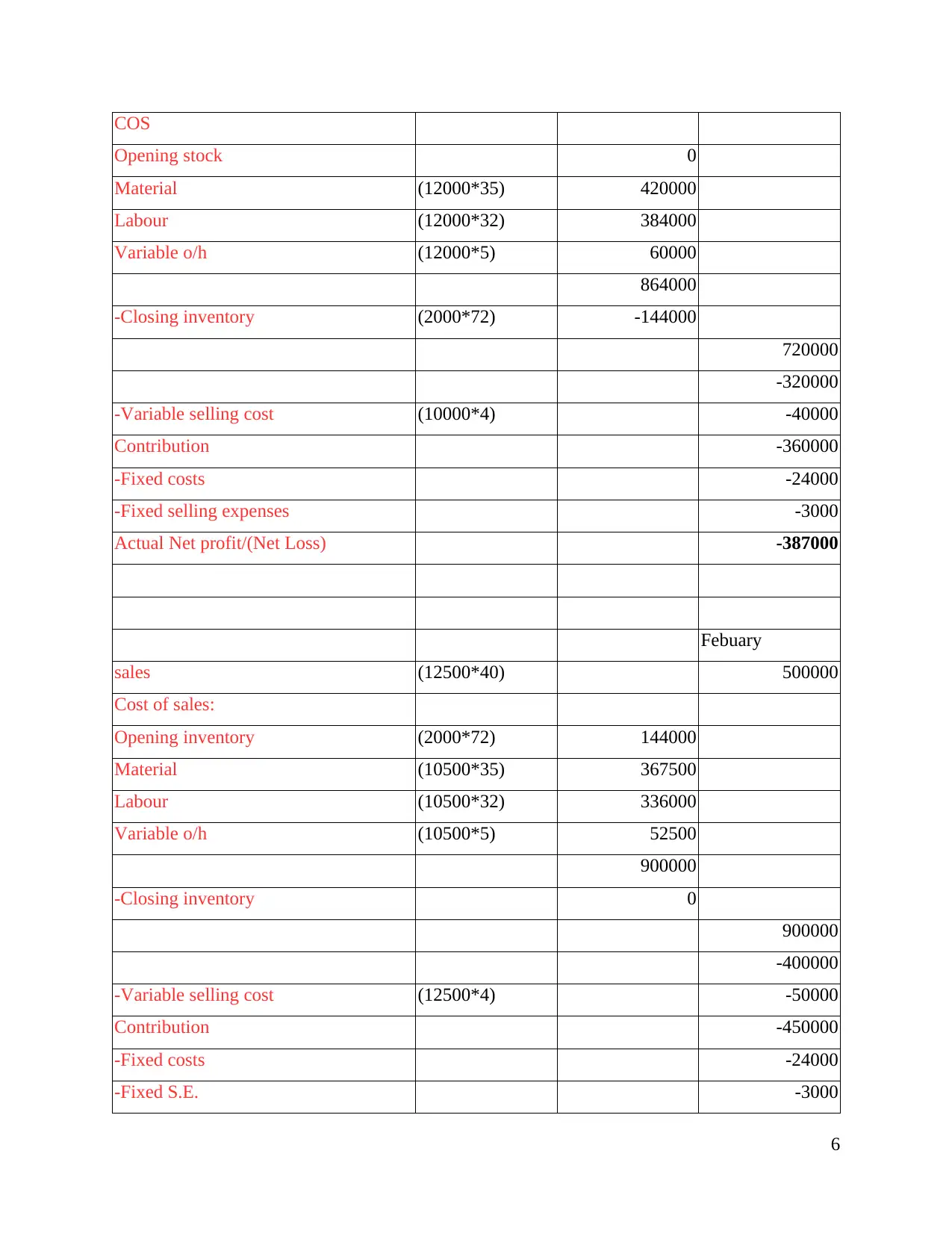

P 3. Calculate costs using appropriate techniques.

Case 1

Under marginal costing

Cost per unit

D.M. ($7*5) 35

D.L. ($8*4) 32

VARIABLE O/H 5

Marginal cost / unit 72

Selling price 40

-Marginal cost /unit -72

-variable selling price -4

Contribution / unit -36

January

sales (10000*40) 400000

5

(Clarke and et.al., 2019) established the fact that, MA systems helps in giving relevant

and viable financial and management statistical information and data to the consumers in order to

take strategic judgment in an efficient manner which leads to future growth. (Morden, 2016)

argued that, management accounting system leads to personal biasses and intuitive decision

making. Management accounting systems in integration to the Arcadia group helps in controlling

cost and reducing wastage. (Mårtenssonand et.al., 2016) established the fact that, MA report

provides up to date information and data to the internal management of the organization.

(Shields, 2018) argued that, MA report only takes into consideration on;y financial data which

affects the operational efficiency and viability of the data. Integration of, management

accounting reports intro the Arcadia group helps in setting budget which eventually helps in

determining the performance of the organization.

P 3. Calculate costs using appropriate techniques.

Case 1

Under marginal costing

Cost per unit

D.M. ($7*5) 35

D.L. ($8*4) 32

VARIABLE O/H 5

Marginal cost / unit 72

Selling price 40

-Marginal cost /unit -72

-variable selling price -4

Contribution / unit -36

January

sales (10000*40) 400000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COS

Opening stock 0

Material (12000*35) 420000

Labour (12000*32) 384000

Variable o/h (12000*5) 60000

864000

-Closing inventory (2000*72) -144000

720000

-320000

-Variable selling cost (10000*4) -40000

Contribution -360000

-Fixed costs -24000

-Fixed selling expenses -3000

Actual Net profit/(Net Loss) -387000

Febuary

sales (12500*40) 500000

Cost of sales:

Opening inventory (2000*72) 144000

Material (10500*35) 367500

Labour (10500*32) 336000

Variable o/h (10500*5) 52500

900000

-Closing inventory 0

900000

-400000

-Variable selling cost (12500*4) -50000

Contribution -450000

-Fixed costs -24000

-Fixed S.E. -3000

6

Opening stock 0

Material (12000*35) 420000

Labour (12000*32) 384000

Variable o/h (12000*5) 60000

864000

-Closing inventory (2000*72) -144000

720000

-320000

-Variable selling cost (10000*4) -40000

Contribution -360000

-Fixed costs -24000

-Fixed selling expenses -3000

Actual Net profit/(Net Loss) -387000

Febuary

sales (12500*40) 500000

Cost of sales:

Opening inventory (2000*72) 144000

Material (10500*35) 367500

Labour (10500*32) 336000

Variable o/h (10500*5) 52500

900000

-Closing inventory 0

900000

-400000

-Variable selling cost (12500*4) -50000

Contribution -450000

-Fixed costs -24000

-Fixed S.E. -3000

6

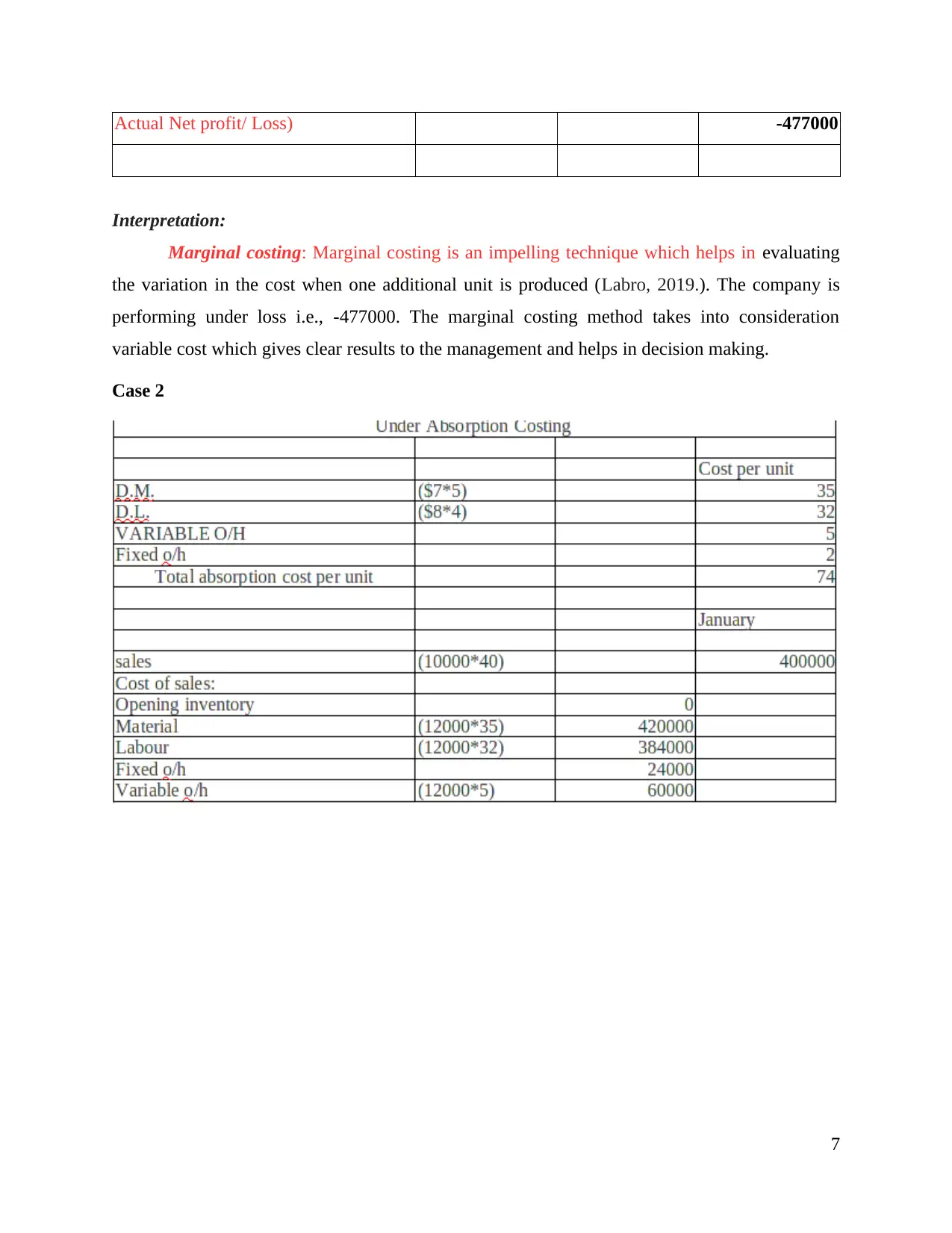

Actual Net profit/ Loss) -477000

Interpretation:

Marginal costing: Marginal costing is an impelling technique which helps in evaluating

the variation in the cost when one additional unit is produced (Labro, 2019.). The company is

performing under loss i.e., -477000. The marginal costing method takes into consideration

variable cost which gives clear results to the management and helps in decision making.

Case 2

7

Interpretation:

Marginal costing: Marginal costing is an impelling technique which helps in evaluating

the variation in the cost when one additional unit is produced (Labro, 2019.). The company is

performing under loss i.e., -477000. The marginal costing method takes into consideration

variable cost which gives clear results to the management and helps in decision making.

Case 2

7

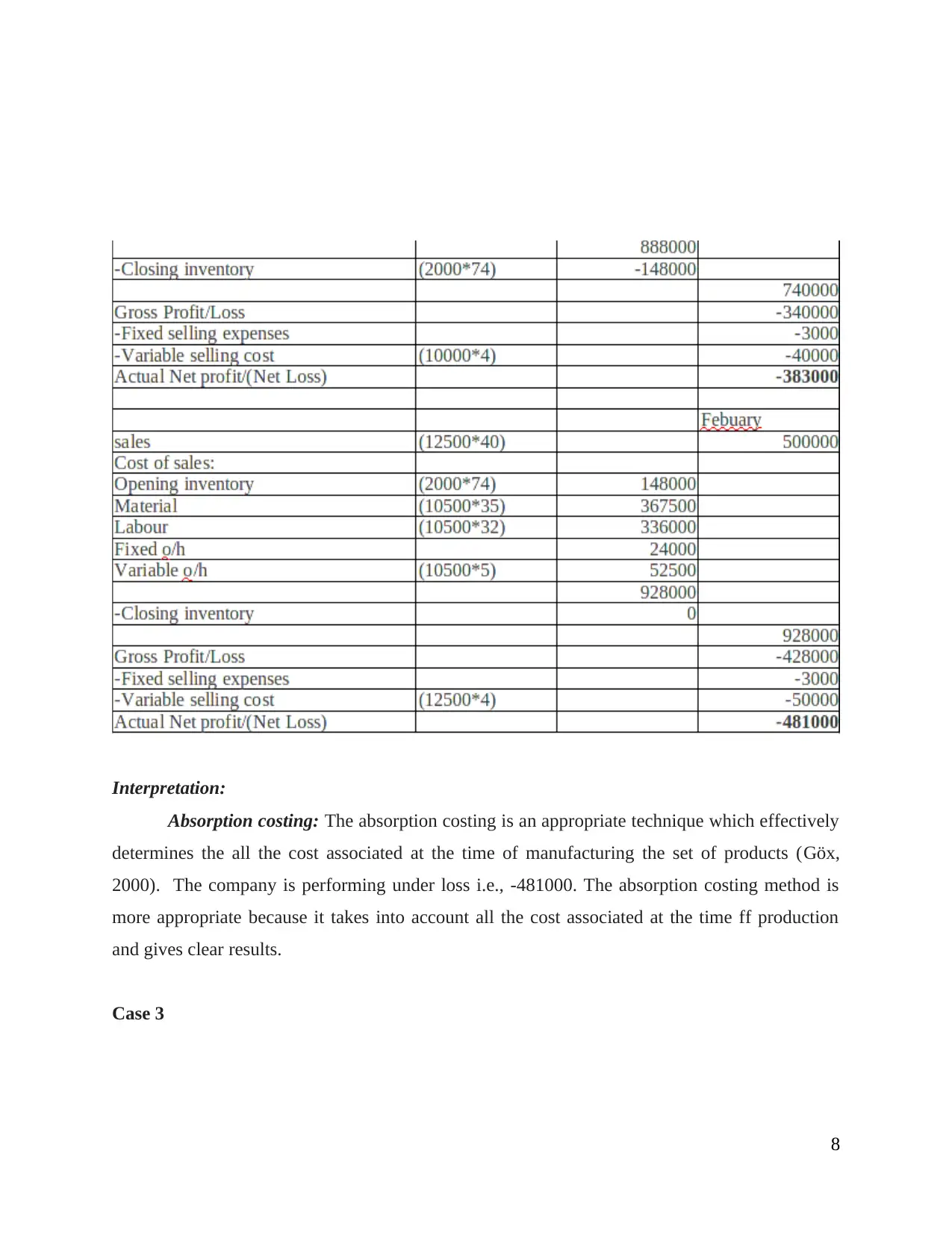

Interpretation:

Absorption costing: The absorption costing is an appropriate technique which effectively

determines the all the cost associated at the time of manufacturing the set of products (Göx,

2000). The company is performing under loss i.e., -481000. The absorption costing method is

more appropriate because it takes into account all the cost associated at the time ff production

and gives clear results.

Case 3

8

Absorption costing: The absorption costing is an appropriate technique which effectively

determines the all the cost associated at the time of manufacturing the set of products (Göx,

2000). The company is performing under loss i.e., -481000. The absorption costing method is

more appropriate because it takes into account all the cost associated at the time ff production

and gives clear results.

Case 3

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

9

10

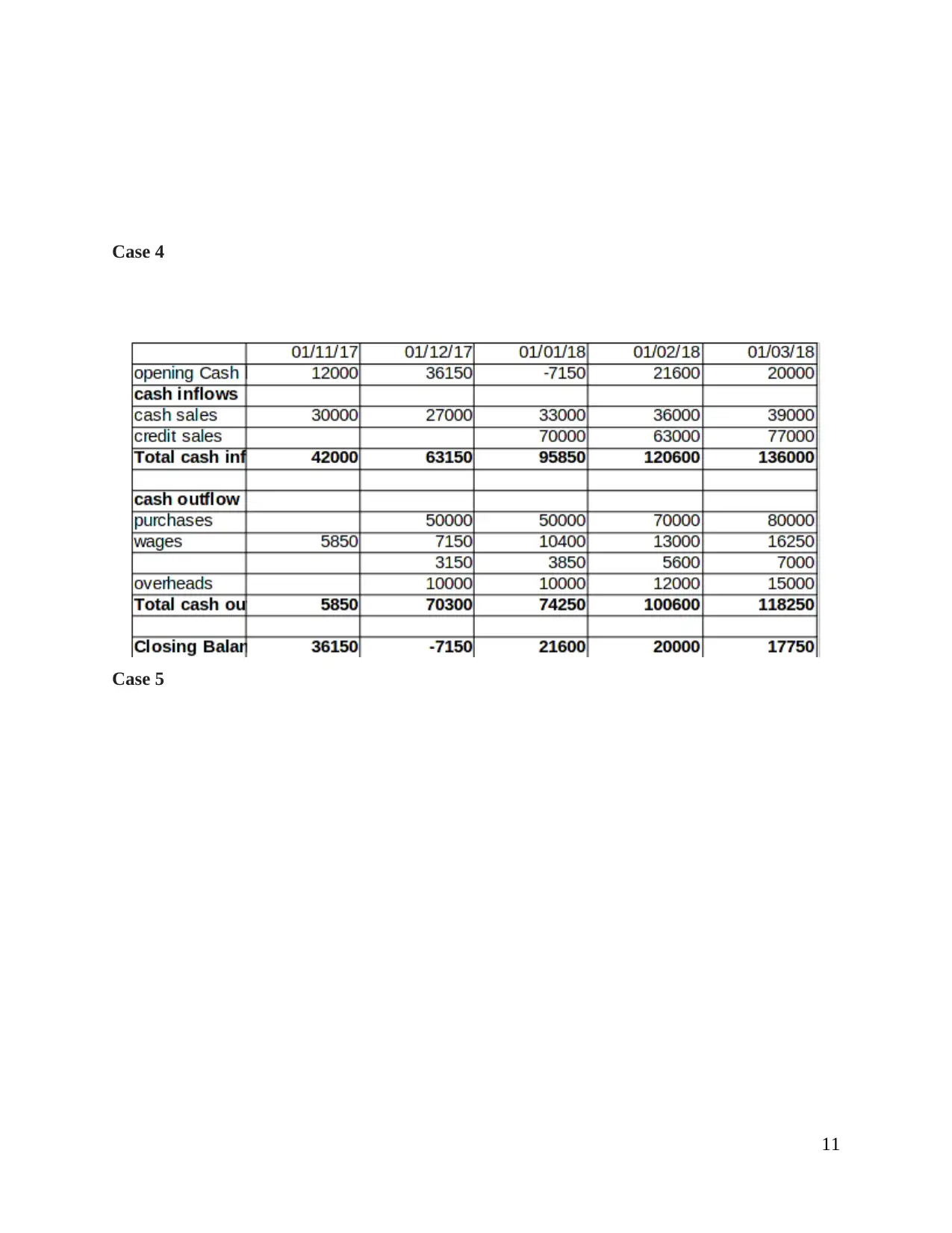

Case 4

Case 5

11

Case 5

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

12

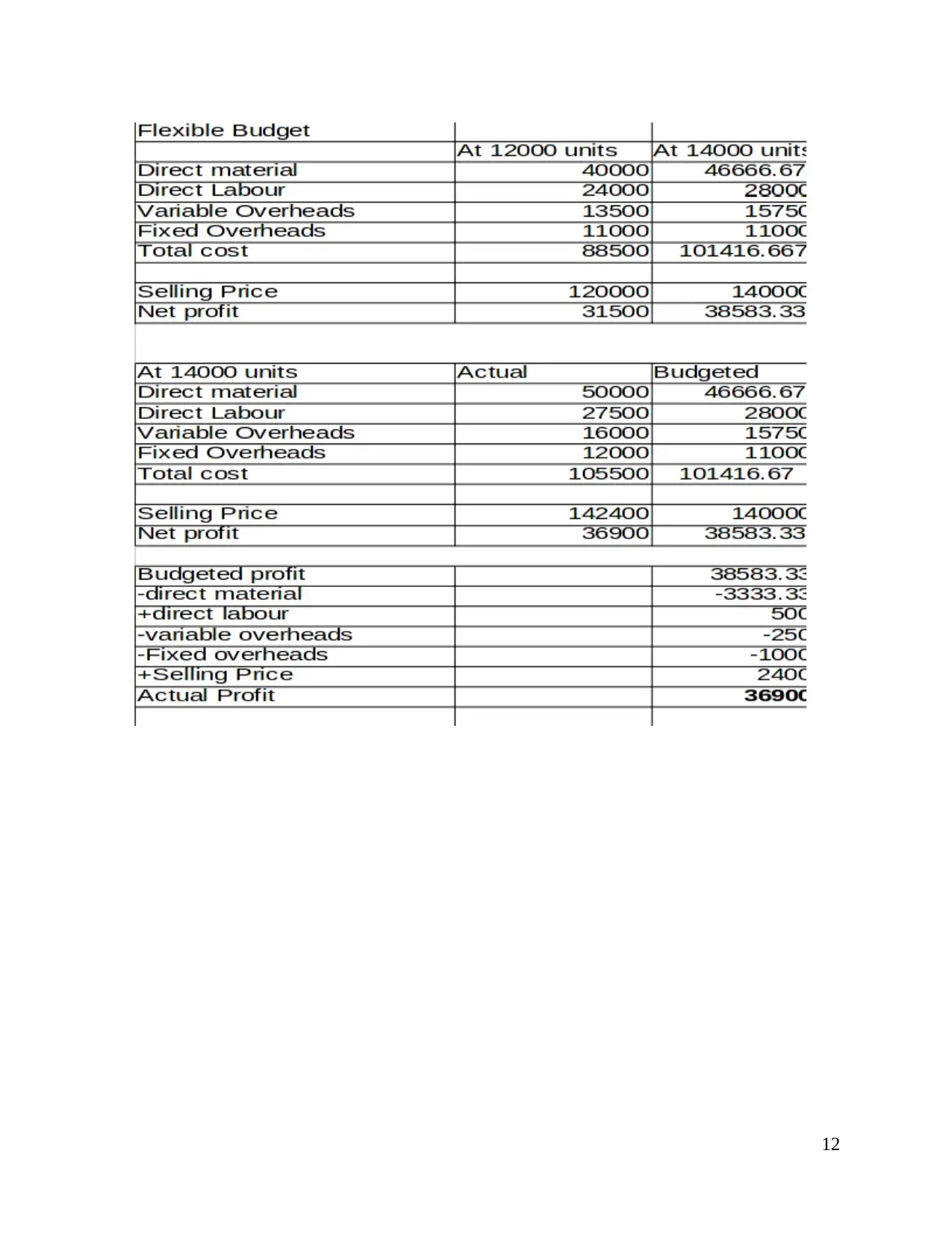

P 4. Benefits and limitations of budgetary tools.

Budgetary control is an effective process which helps in management of the organization

in setting various performance and financial goals in order to reach higher operational efficiency

and performance (Miller, 2018). The budgetary control tool focuses on setting standards and

comparing it with the actual results to critically evaluate the performance of the company in an

accurate and efficient manner.

Sales budgeting

It is an effective planning tool which helps in estimating sales for the particular financial

year. This planning tool is used to forecast future production requirements and also estimate

earning from the particular sales. It helps in evaluating the sales expenses and also determine the

revenue collected from each sales.

Advantages of Sales budgeting

Sales budget is essential in allocating the resources of different products which leads to

smooth functioning of the business. This planning tool also helps in determining the revenue

generated from a particular production unit. Sales budget helps in keeping the sales expenses in

control in order to generate higher profit. This also helps in determining various production units

which strengthen the performance and position of the Arcadia group. It helps in improving the

cash flow management of the company which leads to better cost control.

Disadvantages of Sales budgeting

Sales budget does not give clear picture as it does not take into consideration credit sales.

This hampers the decision making of the management of the organization. It is difficult to predict

revenue from the sales which leads to lower performance and productivity of the organization.

Flexible budgeting: This planning tool is also referred to as variable budget. It is an

effective planning tool which can be varied with the change in the volume of production. The

flexible budget plan will flex because the budget report will take into consideration variable rate

per unit of the activity (AlKhajeh and Khalid, 2018). Flexible budget effectively evaluate the

expenses and revenues in the current production of the company.

13

Budgetary control is an effective process which helps in management of the organization

in setting various performance and financial goals in order to reach higher operational efficiency

and performance (Miller, 2018). The budgetary control tool focuses on setting standards and

comparing it with the actual results to critically evaluate the performance of the company in an

accurate and efficient manner.

Sales budgeting

It is an effective planning tool which helps in estimating sales for the particular financial

year. This planning tool is used to forecast future production requirements and also estimate

earning from the particular sales. It helps in evaluating the sales expenses and also determine the

revenue collected from each sales.

Advantages of Sales budgeting

Sales budget is essential in allocating the resources of different products which leads to

smooth functioning of the business. This planning tool also helps in determining the revenue

generated from a particular production unit. Sales budget helps in keeping the sales expenses in

control in order to generate higher profit. This also helps in determining various production units

which strengthen the performance and position of the Arcadia group. It helps in improving the

cash flow management of the company which leads to better cost control.

Disadvantages of Sales budgeting

Sales budget does not give clear picture as it does not take into consideration credit sales.

This hampers the decision making of the management of the organization. It is difficult to predict

revenue from the sales which leads to lower performance and productivity of the organization.

Flexible budgeting: This planning tool is also referred to as variable budget. It is an

effective planning tool which can be varied with the change in the volume of production. The

flexible budget plan will flex because the budget report will take into consideration variable rate

per unit of the activity (AlKhajeh and Khalid, 2018). Flexible budget effectively evaluate the

expenses and revenues in the current production of the company.

13

Advantages of Flexible budgeting

It is one of the most beneficial budgetary tool which helps in evaluating the performance

of the company in an effective and efficient manner. This tool is beneficial for the company to

regularly update the budget plan and do not remain static for higher operational performance and

productivity. Flexible budget helps in updating current statics and data of the company. It also

helps in better cost control and estimation of effective profit margins.

Disadvantages of Flexible budgeting

Flexible budgeting is a time consuming process. This budgetary tool does to give the

accurate results as it overshadow the revenue of the company by estimating budgeted to the

actual (Maas, Schaltegger, and Crutzen, 2016). The flexible budget is little complicated and

leads to biasses of the data from the managerial staff to attain stipulated goals and target in an

effective, accurate and viable manner. Production budgeting: It is a financial plan which

helps in estimating the cost associated with the manufacturing and production of a particular

output. Production budget helps in making raw material available at the right time and at the

right place to effectively coordinate the function of various department.

Advantages of Production budgeting

Production budget helps in stabilizing the production of and controlling cost associated

with the manufacturing process to reach greater operational efficiency. This also helps in

reducing production expenses and maintaining enough stock for further growth and

development.

Disadvantages of Production budgeting

It is a very time consuming and tedious task to prepare the budget plan for the future. It is

very complex process as it is difficult to evaluate the various changes and need of material in the

production process.

M 3. Forecasting budgetary tools.

Production budget is used to track the cost of the manufacturing process which helps

Arcadia group in evaluating the cost attached with each production process. Sales budget is

useful in evaluating the revenue generated from the particular amount of sales. Flexible budget

focuses on determining the fluctuations with the change in the production report.

14

It is one of the most beneficial budgetary tool which helps in evaluating the performance

of the company in an effective and efficient manner. This tool is beneficial for the company to

regularly update the budget plan and do not remain static for higher operational performance and

productivity. Flexible budget helps in updating current statics and data of the company. It also

helps in better cost control and estimation of effective profit margins.

Disadvantages of Flexible budgeting

Flexible budgeting is a time consuming process. This budgetary tool does to give the

accurate results as it overshadow the revenue of the company by estimating budgeted to the

actual (Maas, Schaltegger, and Crutzen, 2016). The flexible budget is little complicated and

leads to biasses of the data from the managerial staff to attain stipulated goals and target in an

effective, accurate and viable manner. Production budgeting: It is a financial plan which

helps in estimating the cost associated with the manufacturing and production of a particular

output. Production budget helps in making raw material available at the right time and at the

right place to effectively coordinate the function of various department.

Advantages of Production budgeting

Production budget helps in stabilizing the production of and controlling cost associated

with the manufacturing process to reach greater operational efficiency. This also helps in

reducing production expenses and maintaining enough stock for further growth and

development.

Disadvantages of Production budgeting

It is a very time consuming and tedious task to prepare the budget plan for the future. It is

very complex process as it is difficult to evaluate the various changes and need of material in the

production process.

M 3. Forecasting budgetary tools.

Production budget is used to track the cost of the manufacturing process which helps

Arcadia group in evaluating the cost attached with each production process. Sales budget is

useful in evaluating the revenue generated from the particular amount of sales. Flexible budget

focuses on determining the fluctuations with the change in the production report.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

P 5. Comparing organizations to respond to financial problems through management accounting

systems.

Benchmarking: The key financial problem associated with the Arcadia group is that it

has higher competition, which eventually leads to lower market share.

Benchmarking is an effective process of evaluating the performance of the Arcadia group

by setting benchmark in order to achieve desired results and outcomes (Kaplan and Atkinson,

2015). This helps in drilling out the areas of improvement for future growth and development.

Benchmarking is an effective process of standardizing the set of metrics to achieve higher

results. Benchmarking helps in achieving economies of scale by reducing cost, this eventually

helps in achieving higher competitive position.

Key performance indicator: The key financial problem associated with the company is

that the sales of the company is reducing which eventually leads to lower revenue and profit

margins.

Key performance indicator is an effective technique which helps in determining the

various strategies to achieve the key goals and objective of the ScrewFix company (Parmenter,

2015). Key performance indicator helps in evaluating success of reaching desired target for

future growth and expansion.

Variance analysis: The key financial problem associated with the Boux Avenue

company is that the company is having lack of resources and raw material which adversely

impact the performance and productivity of the business.

Variance analysis is an effective technique which helps in determining the budgeted plan

with the actual results in order to maintain effective control over the efficiency of the business. It

helps in determining the cause of variance and take necessary action to optimally utilize the

resources of the organization which leads to higher productivity (Ray and Jenamani, 2016).

M 4. Assessment of how resolving financial problems, lead organizations to sustainable success.

Financial governance means compliance with various accounting standards and

legislations such as GAAP and IFRS. This is an effective strategy which helps in evaluating

financial data by complying with various regulatory rules. Financial governance helps in

tracking various financial transaction, controlling cost, disclosures, operations, compliance and

managerial performance which leads Arcadia group to sustainable success.

15

systems.

Benchmarking: The key financial problem associated with the Arcadia group is that it

has higher competition, which eventually leads to lower market share.

Benchmarking is an effective process of evaluating the performance of the Arcadia group

by setting benchmark in order to achieve desired results and outcomes (Kaplan and Atkinson,

2015). This helps in drilling out the areas of improvement for future growth and development.

Benchmarking is an effective process of standardizing the set of metrics to achieve higher

results. Benchmarking helps in achieving economies of scale by reducing cost, this eventually

helps in achieving higher competitive position.

Key performance indicator: The key financial problem associated with the company is

that the sales of the company is reducing which eventually leads to lower revenue and profit

margins.

Key performance indicator is an effective technique which helps in determining the

various strategies to achieve the key goals and objective of the ScrewFix company (Parmenter,

2015). Key performance indicator helps in evaluating success of reaching desired target for

future growth and expansion.

Variance analysis: The key financial problem associated with the Boux Avenue

company is that the company is having lack of resources and raw material which adversely

impact the performance and productivity of the business.

Variance analysis is an effective technique which helps in determining the budgeted plan

with the actual results in order to maintain effective control over the efficiency of the business. It

helps in determining the cause of variance and take necessary action to optimally utilize the

resources of the organization which leads to higher productivity (Ray and Jenamani, 2016).

M 4. Assessment of how resolving financial problems, lead organizations to sustainable success.

Financial governance means compliance with various accounting standards and

legislations such as GAAP and IFRS. This is an effective strategy which helps in evaluating

financial data by complying with various regulatory rules. Financial governance helps in

tracking various financial transaction, controlling cost, disclosures, operations, compliance and

managerial performance which leads Arcadia group to sustainable success.

15

D 3. Critically evaluating planning tools to solve financial problems.

(Otley, 2016) established the fact that, continuous and regular preparation of various

planning tools give full disclosure on a timely manner to the management of the Arcadia group

to take necessary strategic decision. The company must develop strategic tool and techniques to

resolve various financial problems by comparing actuals with the budgeted plan.

CONCLUSION

From the above study it has been summarized that, there are various management

accounting system which helps in evaluating the various MA system such as cost accounting

system, inventory management system, job costing system and price optimization system. It will

also evaluate MA reports such as budget report, accounts receivable report, performance report,

cost report and other managerial report. This study also evaluates marginal costing and

absorptions costing. Furthermore, it also examines various budgetary control tools and MA

techniques to solve financial problems.

16

(Otley, 2016) established the fact that, continuous and regular preparation of various

planning tools give full disclosure on a timely manner to the management of the Arcadia group

to take necessary strategic decision. The company must develop strategic tool and techniques to

resolve various financial problems by comparing actuals with the budgeted plan.

CONCLUSION

From the above study it has been summarized that, there are various management

accounting system which helps in evaluating the various MA system such as cost accounting

system, inventory management system, job costing system and price optimization system. It will

also evaluate MA reports such as budget report, accounts receivable report, performance report,

cost report and other managerial report. This study also evaluates marginal costing and

absorptions costing. Furthermore, it also examines various budgetary control tools and MA

techniques to solve financial problems.

16

REFERENCES

Books and Journals

AlKhajeh, M.H.A. and Khalid, A.A., 2018. Management Accounting Practices (MAPs) Impact

on Small and Medium Enterprise Business Performance within the Gauteng Province of

South Africa. Journal of Accounting and Auditing: Research & Practice.

Clarke, B and et.al., 2019. Strategic management accounting: CPA program.

Göx, R.F., 2000. Strategic transfer pricing, absorption costing, and observability. Management

Accounting Research.11(3). pp.327-348.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Labro, E., 2019. Costing Systems. Foundations and Trends® in Accounting.13(3-4). pp.267-

404.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production.136.

pp.237-248.

Mårtensson, M and et.al., 2016. Management accounting of control practices: a matter of and for

strategy. In the 9TH INTERNATIONAL EIASM PUBLIC SECTOR CONFERENCE, held in

LISBON, PORTUGAL, SEPTEMBER 6-8, 2016..

Miller, G., 2018. Performance based budgeting. Routledge.

Morden, T., 2016. Principles of strategic management. Routledge.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research.31. pp.45-62.

Parmenter, D., 2015. Key performance indicators: developing, implementing, and using winning

KPIs. John Wiley & Sons.

Ray, P. and Jenamani, M., 2016. Mean-variance analysis of sourcing decision under disruption

risk. European Journal of Operational Research.250(2).pp.679-689.

Shields, M.D., 2018. A Perspective on Management Accounting Research. Journal of

Management Accounting Research.30(3). pp.1-11.

Online

17

Books and Journals

AlKhajeh, M.H.A. and Khalid, A.A., 2018. Management Accounting Practices (MAPs) Impact

on Small and Medium Enterprise Business Performance within the Gauteng Province of

South Africa. Journal of Accounting and Auditing: Research & Practice.

Clarke, B and et.al., 2019. Strategic management accounting: CPA program.

Göx, R.F., 2000. Strategic transfer pricing, absorption costing, and observability. Management

Accounting Research.11(3). pp.327-348.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Labro, E., 2019. Costing Systems. Foundations and Trends® in Accounting.13(3-4). pp.267-

404.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production.136.

pp.237-248.

Mårtensson, M and et.al., 2016. Management accounting of control practices: a matter of and for

strategy. In the 9TH INTERNATIONAL EIASM PUBLIC SECTOR CONFERENCE, held in

LISBON, PORTUGAL, SEPTEMBER 6-8, 2016..

Miller, G., 2018. Performance based budgeting. Routledge.

Morden, T., 2016. Principles of strategic management. Routledge.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research.31. pp.45-62.

Parmenter, D., 2015. Key performance indicators: developing, implementing, and using winning

KPIs. John Wiley & Sons.

Ray, P. and Jenamani, M., 2016. Mean-variance analysis of sourcing decision under disruption

risk. European Journal of Operational Research.250(2).pp.679-689.

Shields, M.D., 2018. A Perspective on Management Accounting Research. Journal of

Management Accounting Research.30(3). pp.1-11.

Online

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Top 10 Benefits of Great Inventory Management. 2011. [Online]. Available

through<https://inventorysystemsoftware.wordpress.com/2011/05/02/top-10-benefits-

inventory-management/>

Types of Managerial Accounting Reports. 2019. [Online]. Available

through<https://smallbusiness.chron.com/types-managerial-accounting-reports-

58384.html>

18

through<https://inventorysystemsoftware.wordpress.com/2011/05/02/top-10-benefits-

inventory-management/>

Types of Managerial Accounting Reports. 2019. [Online]. Available

through<https://smallbusiness.chron.com/types-managerial-accounting-reports-

58384.html>

18

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.