Requirements of Management Accounting Systems

Added on 2020-10-22

21 Pages5731 Words102 Views

MANAGEMENTACCOUNTING

Table of ContentsINTRODUCTION...........................................................................................................................1MAIN BODY...................................................................................................................................1LO 1.................................................................................................................................................11 Essential requirements of different types of management accounting system....................12. Different methods used for management accounting reporting.........................................33. Benefits of management accounting system......................................................................44.Integration of management accounting and reporting system.............................................5LO 2 please don’t change................................................................................................................61. Calculation of marginal and absorption costing.................................................................6LO 3.................................................................................................................................................81.Different types of budgetary tools and their advantages and disadvantages......................82. Application of different budgetary tools and their application in preparing forecastingbudgets..................................................................................................................................10LO 4...............................................................................................................................................121. Adaption of management accounting system to solve financial problems......................16Analyzing planning tools in solving financial problems......................................................17CONCLUSIONS............................................................................................................................17REFERENCES..............................................................................................................................18

INTRODUCTIONManagement accounting is advice to the organization and provision of financial data use incompany and development of business. It is the procedure of preparing and developingmanagement reports and accounts that give timely and accurate statistical and financialstatements. It is used to give data to the internal users and support the company in makingdecisions. Management accounting objective is to provide all the essential financial informationto management. For further information on MA, the report explain various requirements ofmanagement accounting systems which includes Cost accounting system, Inventory managementsystem, and Job costing system. It will focus on various study that is used by company in processof MA report. It will depict the importance of application of various management system in thecompany. It will outline the different methods used for cost calculation which are marginalcosting and absorption costing and will help the company in finding out the better methodbetween these two. The report will finally show pro and cons of different budgetary control toolsand how the performance indicators are used to resolve financial problems of the organization.MAIN BODYLO 11 Essential requirements of different types of management accounting systemMA helps internal users in supplying all the applicable information. This system of thecompany makes it easy for mangers by assembling information based on trend charts, break evencharts, budgeting, etc which help in forecasting future (Martello, 2016). Essential requirements of different types of MA system are as follows :Inventory management system Company's inventory management system tracks good and raw materials throughout thebusiness operations. This system helps the manager of the company in making efficient decisionsrelated to investment and decisions related to manufacturing the raw material in the organizationor purchasing it from outside. The installation cost of this system is high but efficiency of workgets high. It includes bar coding on the product, tools that are used to report quantity and price ofinventory. It helps the company in forecasting inventory by showing the requirement of rawmaterials in the future, by alerting management about inventory in case it gets finished whichhelp manager in taking decisions (Maas, 2016). It helps in tracking the inventory with serial1

number and tracking batch feature which allow the company to keep record of movement ofitems and to control expiry of batch. Valuation of inventory can be done through 2 ways :LIFO – It stands for last in first out where goods that are bought at last are sold at firstplace (Hopper and Bui, 2016.)FIFO – It stands for first in last out in which goods that are bought first are sold at firstplace (Bergeron, 2017).Cost accounting system : It is basically a frame work which is utilized by an organization fordetermining the expenditure of goods in order to analyze profit. It is mainly utilized bymanufacturing firm for recording production activities by utilizing a perpetual inventory system(Cai and et.al, 2018). Job order costing – It is basically a system of assigning as well as aggregatingmanufacturing costs of per unit of output(Hopper, 2016).Process costing – it is generally technique which includes assignment of costs to units ofproduction in an organization manufacturing huge amount of consistent products. (Weight,2015). Job costing system : It includes accumulation o data related to cost that is related with specialtype of production (Weight, 2015). The data provided by job costing system assist indetermining accuracy of estimation (Weight, 2015).Price Optimization System: It Is a mathematical analysis that helps to determine howcustomer respond to different prices for its substitute through variety of channel (Kokubu andKitada, 2015). For example, using price optimization software, company will handle complexsituation.Budget System: It provides a means by which government of the country decides howmuch should be spent, how to raise the money it has to spend (Ofori-Kuragu, Baiden and Badu,2016). For example, when a new product is launch by the firm at that time, government decidethe price and budget needs to be allocated. 2

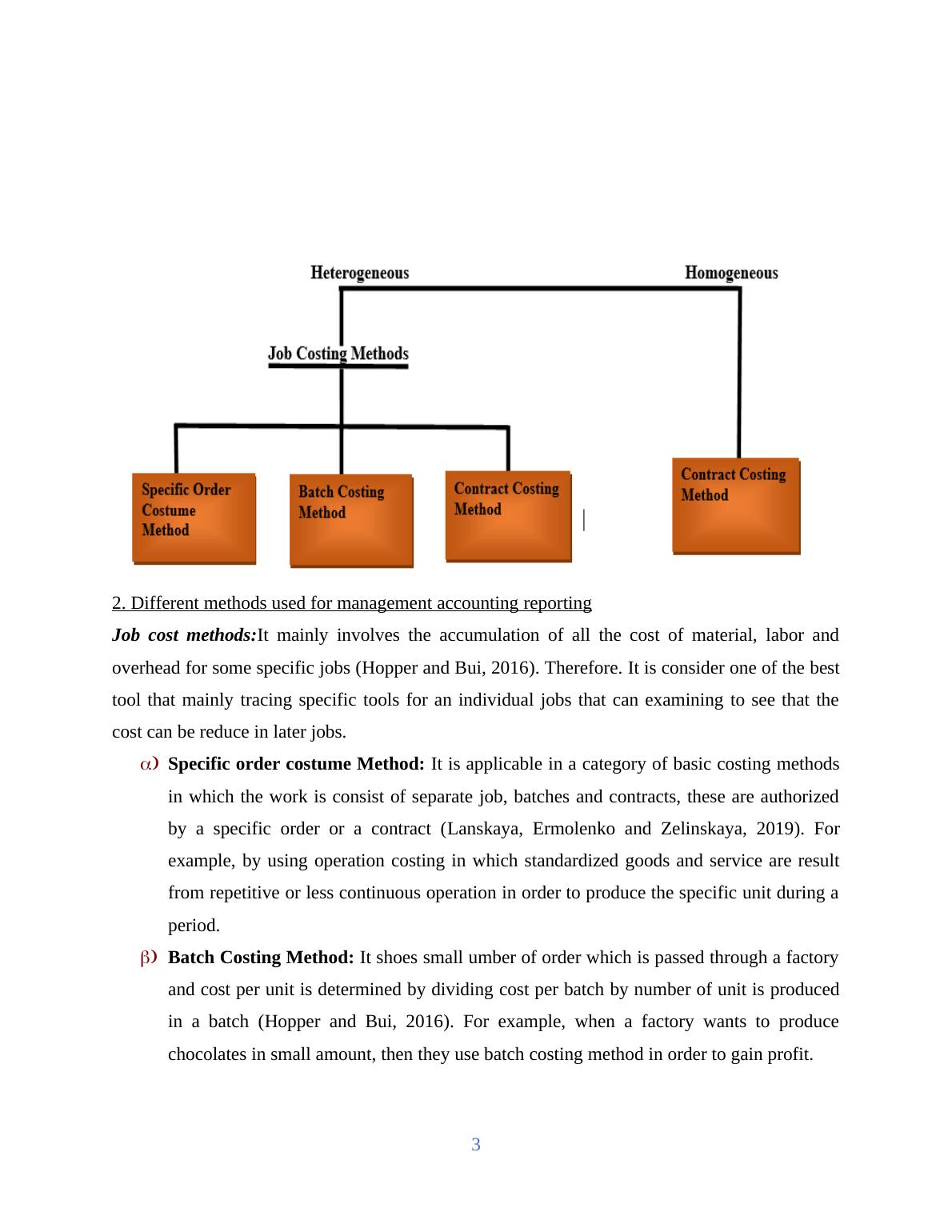

2. Different methods used for management accounting reportingJob cost methods:It mainly involves the accumulation of all the cost of material, labor andoverhead for some specific jobs (Hopper and Bui, 2016). Therefore. It is consider one of the besttool that mainly tracing specific tools for an individual jobs that can examining to see that thecost can be reduce in later jobs. a)Specific order costume Method: It is applicable in a category of basic costing methodsin which the work is consist of separate job, batches and contracts, these are authorizedby a specific order or a contract (Lanskaya, Ermolenko and Zelinskaya, 2019). Forexample, by using operation costing in which standardized goods and service are resultfrom repetitive or less continuous operation in order to produce the specific unit during aperiod. b)Batch Costing Method: It shoes small umber of order which is passed through a factoryand cost per unit is determined by dividing cost per batch by number of unit is producedin a batch (Hopper and Bui, 2016). For example, when a factory wants to producechocolates in small amount, then they use batch costing method in order to gain profit. 3Illustration 1: Given by Lecture

c)Contract costing method: this method is used when a firm is deal at different countryand at that time, there is a need to make separate account which is kept for eachindividual contract (Weight, 2015). For example, a construction company uses thismethod in order to maintain contract with builders, engineers and labors etc.d)Process costing method:This is suitable for industries where production is continuousand well-defined process such that finished products become raw material of subsequentprocess and all the products are produced with same process (Martello, 2016). Forexample, when a company produces different products with or without by product andthen produces simultaneously at same process and those products are clearly identical.Different typea of reports are as mention below:Budget reports – it is basically a internal report which is utilized by management in anenterprise for comparing estimated costs with budgeted. Budget report assist management inanalyzing the business performance and support in identifying the area which requireimprovement. (Chan, 2015). Cost Report: it is the financial report which determine the cost and also identify chargesrelated to healthcare services (Jyothi, Vatsala and Gupta, 2019). Variance Analysis report: It is the quantitative investigation and a difference betweenactual and planned behavior, further it is als used to maintain control over a business(Lanskaya, Ermolenko, and Zelinskaya, 2019). Account receivable aging report –It is basically a report which consist of detailed informationabout unpaid customer invoices as well as underutilized credit memos. Account receivableaging report is generally utilized by an individual responsible for collecting payment. Thosepersonnel utilize the Account receivable aging report for determining the invoices which aredue.Job cost report – It provides clear view of cost incurred by the particular project or jobin the company. It helps in comparing estimated cost with actual revenue the helps the companyin differentiate between the best performance job and least performer project (Cai, and et.al,2018 ). This report evaluates the profitability of specific projects and optimize their working.4

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Activities: Systems, Reporting, and Planning Toolslg...

|13

|3603

|186

Assignment on Management Accounting on Oshodi plc Ltdlg...

|21

|6497

|17

Management Accounting Systems and Principles - LO 1, 2, 3 and 4lg...

|15

|4059

|195

Evaluation of Management Accounting Systems and Reportinglg...

|18

|4527

|51

Management Accounting: Types of Systems, Reporting Methods, Costing Systems, and Planning Toolslg...

|14

|3773

|220

Management Accounting and Techniqueslg...

|16

|3360

|71