Management Accounting Report: Systems, Analysis, and Planning Tools

VerifiedAdded on 2021/02/21

|16

|3982

|47

Report

AI Summary

This report provides a detailed overview of management accounting, focusing on its systems, reporting methods, and practical applications within the context of Next PLC, a UK-based retailer. The report explores various management accounting systems, including inventory management, cost accounting, price optimization, and job order costing, highlighting their benefits and integration with company processes. It examines different reporting methods such as budget reports, performance reports, and cost reports, emphasizing their role in decision-making and performance evaluation. Furthermore, the report delves into cost analysis techniques, the application of planning tools like cash flow budgeting and benchmarking, and the interpretation of financial statements. The analysis aims to provide insights into how management accounting supports financial control, operational efficiency, and strategic planning within the organization, ultimately contributing to improved profitability and business performance.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Part 1...........................................................................................................................................3

Different reporting methods under management accounting:.....................................................5

Benefits of management accounting system:..............................................................................7

Management accounting system and reports are integrate with company processes:................7

Part 2:..........................................................................................................................................7

Analysis the use of different planning tools and their application:.............................................9

TASK 2............................................................................................................................................9

Part 1...........................................................................................................................................9

Calculating cost though proper cost analysis' technique to preparing income statement:..........9

Part 2.........................................................................................................................................11

Analysis and interpretation of financial statement of NEXT PLC:..........................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

ANNEXURE..................................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Part 1...........................................................................................................................................3

Different reporting methods under management accounting:.....................................................5

Benefits of management accounting system:..............................................................................7

Management accounting system and reports are integrate with company processes:................7

Part 2:..........................................................................................................................................7

Analysis the use of different planning tools and their application:.............................................9

TASK 2............................................................................................................................................9

Part 1...........................................................................................................................................9

Calculating cost though proper cost analysis' technique to preparing income statement:..........9

Part 2.........................................................................................................................................11

Analysis and interpretation of financial statement of NEXT PLC:..........................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

ANNEXURE..................................................................................................................................14

INTRODUCTION

Management accounting is crucial aspect of accounting. It comprises all the fiscal and

managing tasks necessary for retrieving information for company's key decisions. Management

personnels and accounting officials both play crucial character in management accounting's

processes. Account officers gathers data which is further used in various systems to accomplish

overall goals of management accounting (Agrawal, 2018). Organisation's implements

management accounting as per their existing capabilities and efficiencies while focusing on their

potentials. This study exhibits entire management accounting concept and its systems, how

managing personnels reports and to what extent management accounting systems are

advantageous in context of Next Plc. It is top retailer of clothings, home care products and foot

wears etc. in UK. Company is operating its retail chain through approx 680 stores. The study

also combines practical implication of cost techniques and application of planning tools.

TASK 1

Part 1

(A) Management accounting and types

Management accounting relates to interpreting, analysing, characterizing, identifying,

managing and presenting a commercial enterprise's data acquired through financial accounting

and cost accounting. Management accounting assists business organization's executives in policy

implementation, policy and decision making and even in the company's day-to-day tasks and

activities. Organising vital variables of an entity's performance and operations is important thing

which can be efficiently done through adaption of various systems (Bryson, Crosby and

Bloomberg, 2014). Routine working of a company generate events and transactions which

ultimately shows impact on their targets so management is divided into different layers, which

assist in monitoring such events and manage them to improve performance. The whole process is

incomplete without management accounting's systems because it provide help in fixation of

responsibilities and maintain accountability within company. Following headings contains

different systems and their requirements in context of Next Plc:

Inventory Management System: This system comprises formulating and implementing

policies for managing and directing usages of an entity's stock. Inventory are important fiscal

Management accounting is crucial aspect of accounting. It comprises all the fiscal and

managing tasks necessary for retrieving information for company's key decisions. Management

personnels and accounting officials both play crucial character in management accounting's

processes. Account officers gathers data which is further used in various systems to accomplish

overall goals of management accounting (Agrawal, 2018). Organisation's implements

management accounting as per their existing capabilities and efficiencies while focusing on their

potentials. This study exhibits entire management accounting concept and its systems, how

managing personnels reports and to what extent management accounting systems are

advantageous in context of Next Plc. It is top retailer of clothings, home care products and foot

wears etc. in UK. Company is operating its retail chain through approx 680 stores. The study

also combines practical implication of cost techniques and application of planning tools.

TASK 1

Part 1

(A) Management accounting and types

Management accounting relates to interpreting, analysing, characterizing, identifying,

managing and presenting a commercial enterprise's data acquired through financial accounting

and cost accounting. Management accounting assists business organization's executives in policy

implementation, policy and decision making and even in the company's day-to-day tasks and

activities. Organising vital variables of an entity's performance and operations is important thing

which can be efficiently done through adaption of various systems (Bryson, Crosby and

Bloomberg, 2014). Routine working of a company generate events and transactions which

ultimately shows impact on their targets so management is divided into different layers, which

assist in monitoring such events and manage them to improve performance. The whole process is

incomplete without management accounting's systems because it provide help in fixation of

responsibilities and maintain accountability within company. Following headings contains

different systems and their requirements in context of Next Plc:

Inventory Management System: This system comprises formulating and implementing

policies for managing and directing usages of an entity's stock. Inventory are important fiscal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

figure in computation of net results. It requires details of each stock items from processing heads

to enable effective tracing of inventory's usage. It provide the list of items causing excess in cost

of stocks, which help in reducing or eliminating such costs. As in Next Plc store managers and

other key officials transfers details of inventory in store, inventory in transit etc. that assist in

tracking value of wastages, sold units and items still unsold. This system provides details of

inventory store and outlet wise which also exhibits performance of each store. These are major

inventory recording approaches, as follows:

FIFO Method: It defines valuation of stock as per a that in a particular sequence first

bought or processed inventory is sold at first in such sequence.

LIFO Method: It emphasises on theory of valuation which consists that in a particular

sequence recently purchased or processes inventory is sold at first in such sequence.

Average Cost Method: In valuing process of inventory average going on stock value is

used under this method.

Cost accounting system: Expenditures are managed under this systems with intention to

achieve desired increment in company's performance profitability. This is significantly relevant

for companies to assess entire process's costs and related variables to know whether these are

within stipulated figures. A company can attain profitability without increasing their sales just

only by optimisation of numerous expenditures (Charifzadeh and Taschner, 2017). In Next Plc

this system determines the viability of decision of opening new store, launch new product range,

develop new processes and so on. Moreover, such system company can evaluate effect of costs

on company's results and profitability level. Relationship between costs and profitability is

analysed in this system to assess the need of improvement in existing operational efficiencies.

Price optimisation system: Main framework of this system consists of interrelation of

company's items price and their demand. Managers evaluates how effectively pricing strategies

are working in company. It ensures targeted demand is achieved along with adequate profit

figures. Prices are changed to an extent at which demand is at effective level. In Next Plc this

system is utilised to enhance the sales at particular store, achieve targeted demand potentials and

set pricing policies. Effective price of company's each items is determined and responses are

analysed by management for choosing most favourable price of its products. Company's internal

pricing structure are formed by applying this system.

to enable effective tracing of inventory's usage. It provide the list of items causing excess in cost

of stocks, which help in reducing or eliminating such costs. As in Next Plc store managers and

other key officials transfers details of inventory in store, inventory in transit etc. that assist in

tracking value of wastages, sold units and items still unsold. This system provides details of

inventory store and outlet wise which also exhibits performance of each store. These are major

inventory recording approaches, as follows:

FIFO Method: It defines valuation of stock as per a that in a particular sequence first

bought or processed inventory is sold at first in such sequence.

LIFO Method: It emphasises on theory of valuation which consists that in a particular

sequence recently purchased or processes inventory is sold at first in such sequence.

Average Cost Method: In valuing process of inventory average going on stock value is

used under this method.

Cost accounting system: Expenditures are managed under this systems with intention to

achieve desired increment in company's performance profitability. This is significantly relevant

for companies to assess entire process's costs and related variables to know whether these are

within stipulated figures. A company can attain profitability without increasing their sales just

only by optimisation of numerous expenditures (Charifzadeh and Taschner, 2017). In Next Plc

this system determines the viability of decision of opening new store, launch new product range,

develop new processes and so on. Moreover, such system company can evaluate effect of costs

on company's results and profitability level. Relationship between costs and profitability is

analysed in this system to assess the need of improvement in existing operational efficiencies.

Price optimisation system: Main framework of this system consists of interrelation of

company's items price and their demand. Managers evaluates how effectively pricing strategies

are working in company. It ensures targeted demand is achieved along with adequate profit

figures. Prices are changed to an extent at which demand is at effective level. In Next Plc this

system is utilised to enhance the sales at particular store, achieve targeted demand potentials and

set pricing policies. Effective price of company's each items is determined and responses are

analysed by management for choosing most favourable price of its products. Company's internal

pricing structure are formed by applying this system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job order costing system: Job costing or Job order costing is a mechanism for

delegating and accumulating production expenses to an individual production unit. The costing

scheme for work orders is shown when the distinct products generated differ adequately from

one another and each one has a substantial price. As there is a substantial variability in the

products produced, of each item (each work or unique order) job order costing scheme needs a

distinct work price record. In Next Plc, it is applied to facilitate accountability in its different

products which are different from company's normal product chain. In company it is used in

some segments for effectively managing expenses by allocated to jobs.

Different reporting methods under management accounting:

Management Accounting Reporting: This is a structure which is responsible for

communicating effective informations within a corporate entity. Such communication being

formal in nature and information concerned should be used to determine company's actions.

Management accounting reports are often used for success prediction, regulation, policy-making

and measurement. As per the demands, these statements are produced continually all through the

books finalisation and accounting (Goh and Scerri, 2016). Since many sensitive choices rely on

the credibility of these accounts, specialists who are skilled at record keeping should thoroughly

prepare them. These reports are then analysed by managers to accentuate such trends and

transform them into helpful business data. Following are mainly used reports by managing

officials, as follows:

Budget Report: Budget accounting managerial reports are most crucial in evaluating the

efficiency of entity and are mainly produced as a whole for entire company and departmentally.

Each corporation, however, generates an general budget to comprehend their company's internal

system. However, in budget projected amounts are filled on the basis of past experiences, a large

budget often provides for possible unanticipated conditions. Budgets list out sources of income

and costs. A business is trying to accomplish its objectives and predetermined goals while

remaining within the quantity budgeted. In Next Plc along with financial budgets and small sub

budgets are also formed by officials to determine their efficiencies and future performance.

Performance Report: Performance reports are mostly framed to review and track

efficiencies performance as entirely along with considering every employee over a time-frame.

In Next Plc, departmental reports are issued by respective department's heads to review

department performance. Manager officials using such reports forms strategical judgements

delegating and accumulating production expenses to an individual production unit. The costing

scheme for work orders is shown when the distinct products generated differ adequately from

one another and each one has a substantial price. As there is a substantial variability in the

products produced, of each item (each work or unique order) job order costing scheme needs a

distinct work price record. In Next Plc, it is applied to facilitate accountability in its different

products which are different from company's normal product chain. In company it is used in

some segments for effectively managing expenses by allocated to jobs.

Different reporting methods under management accounting:

Management Accounting Reporting: This is a structure which is responsible for

communicating effective informations within a corporate entity. Such communication being

formal in nature and information concerned should be used to determine company's actions.

Management accounting reports are often used for success prediction, regulation, policy-making

and measurement. As per the demands, these statements are produced continually all through the

books finalisation and accounting (Goh and Scerri, 2016). Since many sensitive choices rely on

the credibility of these accounts, specialists who are skilled at record keeping should thoroughly

prepare them. These reports are then analysed by managers to accentuate such trends and

transform them into helpful business data. Following are mainly used reports by managing

officials, as follows:

Budget Report: Budget accounting managerial reports are most crucial in evaluating the

efficiency of entity and are mainly produced as a whole for entire company and departmentally.

Each corporation, however, generates an general budget to comprehend their company's internal

system. However, in budget projected amounts are filled on the basis of past experiences, a large

budget often provides for possible unanticipated conditions. Budgets list out sources of income

and costs. A business is trying to accomplish its objectives and predetermined goals while

remaining within the quantity budgeted. In Next Plc along with financial budgets and small sub

budgets are also formed by officials to determine their efficiencies and future performance.

Performance Report: Performance reports are mostly framed to review and track

efficiencies performance as entirely along with considering every employee over a time-frame.

In Next Plc, departmental reports are issued by respective department's heads to review

department performance. Manager officials using such reports forms strategical judgements

about forthcoming performances. Individuals in respective company are oftentimes awarded and

honoured according to their task handling efficiencies and other performance measures. Whereas

for low performing personnels are recognised and more efforts are put on such individuals in

order to increase their performances. Such reports also facilitates in deep and effective insight on

acts of employees. Role of these reports is indispensable for company as it maintain an faithful

measurement of strategy dedicated to company's mission.

Cost Report: This kind of report is formed to evaluate each variable of costs and effects

of such variables on profitability and results. It is main aspect of cost accounting systems which

in long run assures company's performance in term of profitability. It offers a list of company's

all expenses and also exhibits any potential increment in expenses (Kaplan and Atkinson, 2015).

In Next Plc cost reports defines cost effectiveness of company's operations and any specific

project. Inventory wastage cost, hourly workers costs, and other effective overhead forming part

this report. These all generates an perfect perceptive of different expenses, that is vital for

controlling costs and increasing profits.

Account Receivable Ageing Reports: For business entities which are mostly relies on

extending loans and credits this ageing report is significant. Break-down of rest balances

different customers into particular time intervals allows managing officials to recognise possible

defaulters and to short out problems regarding company's collection process. This report provide

ground work for making credit policies and assess viability of existing credit period provided to

different clients. In Next Plc it facilitates company to know the status of company's major clients

and in fixing terms of credits provided by company. It also segregates current and long term

credits of company for better accountability.

Inventory Report: this report is mainly emphasised on analysing and evaluating status

of inventory in a business organisation. In wide entity like Next Plc this report is needed to

arrange their large volume of inventory's items. Store managers and inventory heads coordinates

with each other in order to prepare inventory report. In company they both hold their own stock

records and at the time of preparation of inventory report both provide informations. Any lost in

transit of stock, excessive stock holding charges and other related stock expenses are easily

minimised with help of data of inventory report.

honoured according to their task handling efficiencies and other performance measures. Whereas

for low performing personnels are recognised and more efforts are put on such individuals in

order to increase their performances. Such reports also facilitates in deep and effective insight on

acts of employees. Role of these reports is indispensable for company as it maintain an faithful

measurement of strategy dedicated to company's mission.

Cost Report: This kind of report is formed to evaluate each variable of costs and effects

of such variables on profitability and results. It is main aspect of cost accounting systems which

in long run assures company's performance in term of profitability. It offers a list of company's

all expenses and also exhibits any potential increment in expenses (Kaplan and Atkinson, 2015).

In Next Plc cost reports defines cost effectiveness of company's operations and any specific

project. Inventory wastage cost, hourly workers costs, and other effective overhead forming part

this report. These all generates an perfect perceptive of different expenses, that is vital for

controlling costs and increasing profits.

Account Receivable Ageing Reports: For business entities which are mostly relies on

extending loans and credits this ageing report is significant. Break-down of rest balances

different customers into particular time intervals allows managing officials to recognise possible

defaulters and to short out problems regarding company's collection process. This report provide

ground work for making credit policies and assess viability of existing credit period provided to

different clients. In Next Plc it facilitates company to know the status of company's major clients

and in fixing terms of credits provided by company. It also segregates current and long term

credits of company for better accountability.

Inventory Report: this report is mainly emphasised on analysing and evaluating status

of inventory in a business organisation. In wide entity like Next Plc this report is needed to

arrange their large volume of inventory's items. Store managers and inventory heads coordinates

with each other in order to prepare inventory report. In company they both hold their own stock

records and at the time of preparation of inventory report both provide informations. Any lost in

transit of stock, excessive stock holding charges and other related stock expenses are easily

minimised with help of data of inventory report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benefits of management accounting system:

Above discussed systems have various benefits for business and mangers also considers

these benefits before implementation of any system. Following table describes advantages of

different management accounting systems in context of Next Plc, as follows:

Systems Benefits

Cost Accounting System It minimises the costs and allocates any

activity leading to excessive costs.

It help in finalisation of annual fiscal

reports and budgets in respective

company.

Inventory Management System It facilitates basic structure managing

items of variety stocks.

Assisting in optimisation of expenses of

storing stocks, managing them and any

wastages (Lindholm, Laine and

Suomala, 2017).

Price Optimisation System Help to fix particular price of each

selling item effectively.

Boost the demand by determining

pricing policies.

Job order Costing System It provides desired accountability in

tasks performance in Next Plc.

Management accounting system and reports are integrate with company processes:

Above explained systems and reports facilitates a basis for operating different processes

within a corporate entity. In Next Plc reporting and systems are interconnected to generate

simultaneous impacts on and benefits for each others. Foe intense, in company accounting tasks

and processes retrieves fiscal information which is at last used by managers thoroughly in

different managerial accounting systems.

Above discussed systems have various benefits for business and mangers also considers

these benefits before implementation of any system. Following table describes advantages of

different management accounting systems in context of Next Plc, as follows:

Systems Benefits

Cost Accounting System It minimises the costs and allocates any

activity leading to excessive costs.

It help in finalisation of annual fiscal

reports and budgets in respective

company.

Inventory Management System It facilitates basic structure managing

items of variety stocks.

Assisting in optimisation of expenses of

storing stocks, managing them and any

wastages (Lindholm, Laine and

Suomala, 2017).

Price Optimisation System Help to fix particular price of each

selling item effectively.

Boost the demand by determining

pricing policies.

Job order Costing System It provides desired accountability in

tasks performance in Next Plc.

Management accounting system and reports are integrate with company processes:

Above explained systems and reports facilitates a basis for operating different processes

within a corporate entity. In Next Plc reporting and systems are interconnected to generate

simultaneous impacts on and benefits for each others. Foe intense, in company accounting tasks

and processes retrieves fiscal information which is at last used by managers thoroughly in

different managerial accounting systems.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part 2:

Cash Flow Budgeting: This is planning tool which focuses on preparation of cash flow

statement while covering estimation of cash flows during a time-period. Through it accountants

summaries monetary cash transactions and prepares a summary of these transactions to asses real

flow of cash in or outside the entity. It also contains some sub techniques to easily manage the

movement of cash thoroughly. In Next Plc this budget assisting in allocating negative cash

figures and finding reasons for negative cash flow. It contributes in managing cash resources in

efficient manner to ensure proper cash management. It tracks the usage of cash in company's

different operations. Advantages and dis-advantages of cash flow budgeting:

Advantages: It assist company in maintaining adequate flow of cash and determines

appropriate cash level.

Dis-advantages: It shows ambiguous results as it combines cash flows arises through the

sale of capital assets, fines, security deposits and so on non-sustainable transactions.

Benchmarking: This is most applied planning tool which determines a basis for setting

standards and contains analysis of any over and under performance of company on the basis of

such standards. A benchmarking covers different performance variables which help to asses

company's operating effectiveness (Melnyk and et.al, 2014). In Next Plc, managerial officials

conduct routine analysis to determines variables to be analysed in Benchmarking Process, then

they fix criteria for performing benchmarking tasks. At last any difference is evaluated to know

main causes of such differences. Following are advantages and dis-advantages of benchmarking,

as follows:

Advantage: It help to minimise any adverse gape in performance by identifying

improvement fields within organisational structure.

Dis-advantage: This tool seem inadequate in determining entire performance of entity as

it covers only deviations in performance.

Activity based costing: This tool is mostly preferred in case of differentiated products or

items which are not consistent with company's traditional product line. Companies through it

determine each activity' costs. This tool contributes in arranging costs by allocating tasks in

different process and activities. It also includes ranking of activities as per their priority level. In

Next Plc this tool is used by departments for internal purposes to know which activity is causing

more expenses (Samuelsson and et. al., 2016). It classifies various expenses which are straight-

Cash Flow Budgeting: This is planning tool which focuses on preparation of cash flow

statement while covering estimation of cash flows during a time-period. Through it accountants

summaries monetary cash transactions and prepares a summary of these transactions to asses real

flow of cash in or outside the entity. It also contains some sub techniques to easily manage the

movement of cash thoroughly. In Next Plc this budget assisting in allocating negative cash

figures and finding reasons for negative cash flow. It contributes in managing cash resources in

efficient manner to ensure proper cash management. It tracks the usage of cash in company's

different operations. Advantages and dis-advantages of cash flow budgeting:

Advantages: It assist company in maintaining adequate flow of cash and determines

appropriate cash level.

Dis-advantages: It shows ambiguous results as it combines cash flows arises through the

sale of capital assets, fines, security deposits and so on non-sustainable transactions.

Benchmarking: This is most applied planning tool which determines a basis for setting

standards and contains analysis of any over and under performance of company on the basis of

such standards. A benchmarking covers different performance variables which help to asses

company's operating effectiveness (Melnyk and et.al, 2014). In Next Plc, managerial officials

conduct routine analysis to determines variables to be analysed in Benchmarking Process, then

they fix criteria for performing benchmarking tasks. At last any difference is evaluated to know

main causes of such differences. Following are advantages and dis-advantages of benchmarking,

as follows:

Advantage: It help to minimise any adverse gape in performance by identifying

improvement fields within organisational structure.

Dis-advantage: This tool seem inadequate in determining entire performance of entity as

it covers only deviations in performance.

Activity based costing: This tool is mostly preferred in case of differentiated products or

items which are not consistent with company's traditional product line. Companies through it

determine each activity' costs. This tool contributes in arranging costs by allocating tasks in

different process and activities. It also includes ranking of activities as per their priority level. In

Next Plc this tool is used by departments for internal purposes to know which activity is causing

more expenses (Samuelsson and et. al., 2016). It classifies various expenses which are straight-

away related to selling of product and assign such costs to particular product-activity. These are

advantages and dis-advantage of activity-based costing, as follows:

Advantage: It enhance the accuracy of product's cost by recognising activities leading to

increase in costs.

Dis-advantage: Adoption of activity based along with traditional costing method leads to

complexities and also an expensive task.

Analysis the use of different planning tools and their application:

Controlling budgets is tuff task for business organisation, to provide easiness in this task

different planning tools are used by managerial officials. Budget are threshold for entity's

performance which determines overall effectiveness of company by making comparison with

budgeted figures. As respective company is using benchmarking to know usages of funds and

assess efficiencies, which ultimately help in process of monetary and budgetary control (Nitzl,

2016).

TASK 2

Part 1

Calculating cost though proper cost analysis' technique to preparing income statement:

Marginal costing: It is a costing technique which does not consider fixed overheads or

inventory while calculating cost of foods sold. The profit obtained under this is termed as

contribution and is attained by using profit volume ratio and changes with per unit of

production.

Absorption costing: This is a costing technique wherein fixed production overheads is

considered under cost of sales with direct material, labour. It includes valuation of both opening

as well as closing stock. This expenses all costs associated with manufacturing of a particular

product or service (Otley, , 2016).

Practical Sum:

Income statement under absorption costing method for month of May & June:

Particulars May June

(in £) (in £)

Total sales 10.5 4200000 3780000

advantages and dis-advantage of activity-based costing, as follows:

Advantage: It enhance the accuracy of product's cost by recognising activities leading to

increase in costs.

Dis-advantage: Adoption of activity based along with traditional costing method leads to

complexities and also an expensive task.

Analysis the use of different planning tools and their application:

Controlling budgets is tuff task for business organisation, to provide easiness in this task

different planning tools are used by managerial officials. Budget are threshold for entity's

performance which determines overall effectiveness of company by making comparison with

budgeted figures. As respective company is using benchmarking to know usages of funds and

assess efficiencies, which ultimately help in process of monetary and budgetary control (Nitzl,

2016).

TASK 2

Part 1

Calculating cost though proper cost analysis' technique to preparing income statement:

Marginal costing: It is a costing technique which does not consider fixed overheads or

inventory while calculating cost of foods sold. The profit obtained under this is termed as

contribution and is attained by using profit volume ratio and changes with per unit of

production.

Absorption costing: This is a costing technique wherein fixed production overheads is

considered under cost of sales with direct material, labour. It includes valuation of both opening

as well as closing stock. This expenses all costs associated with manufacturing of a particular

product or service (Otley, , 2016).

Practical Sum:

Income statement under absorption costing method for month of May & June:

Particulars May June

(in £) (in £)

Total sales 10.5 4200000 3780000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

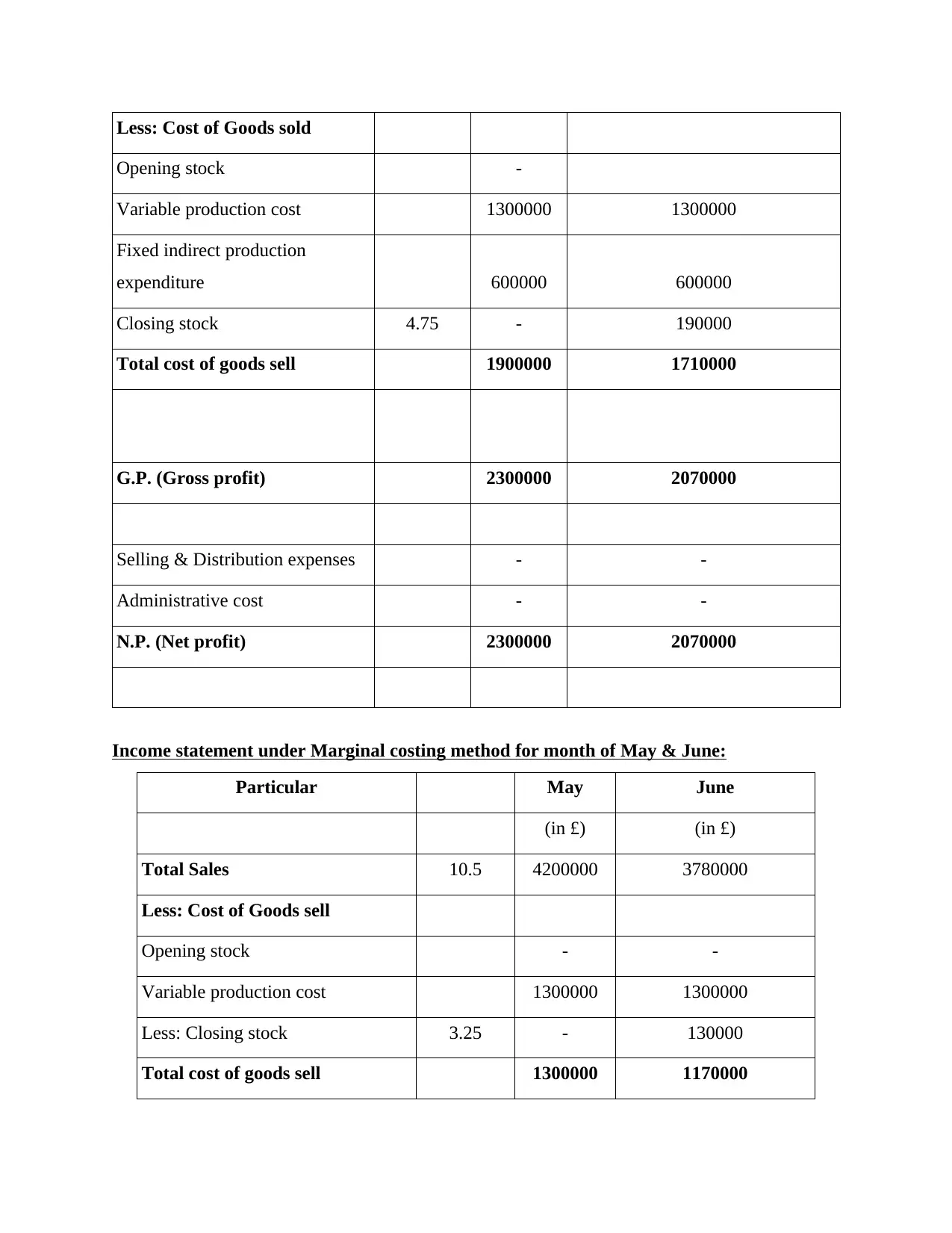

Less: Cost of Goods sold

Opening stock -

Variable production cost 1300000 1300000

Fixed indirect production

expenditure 600000 600000

Closing stock 4.75 - 190000

Total cost of goods sell 1900000 1710000

G.P. (Gross profit) 2300000 2070000

Selling & Distribution expenses - -

Administrative cost - -

N.P. (Net profit) 2300000 2070000

Income statement under Marginal costing method for month of May & June:

Particular May June

(in £) (in £)

Total Sales 10.5 4200000 3780000

Less: Cost of Goods sell

Opening stock - -

Variable production cost 1300000 1300000

Less: Closing stock 3.25 - 130000

Total cost of goods sell 1300000 1170000

Opening stock -

Variable production cost 1300000 1300000

Fixed indirect production

expenditure 600000 600000

Closing stock 4.75 - 190000

Total cost of goods sell 1900000 1710000

G.P. (Gross profit) 2300000 2070000

Selling & Distribution expenses - -

Administrative cost - -

N.P. (Net profit) 2300000 2070000

Income statement under Marginal costing method for month of May & June:

Particular May June

(in £) (in £)

Total Sales 10.5 4200000 3780000

Less: Cost of Goods sell

Opening stock - -

Variable production cost 1300000 1300000

Less: Closing stock 3.25 - 130000

Total cost of goods sell 1300000 1170000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

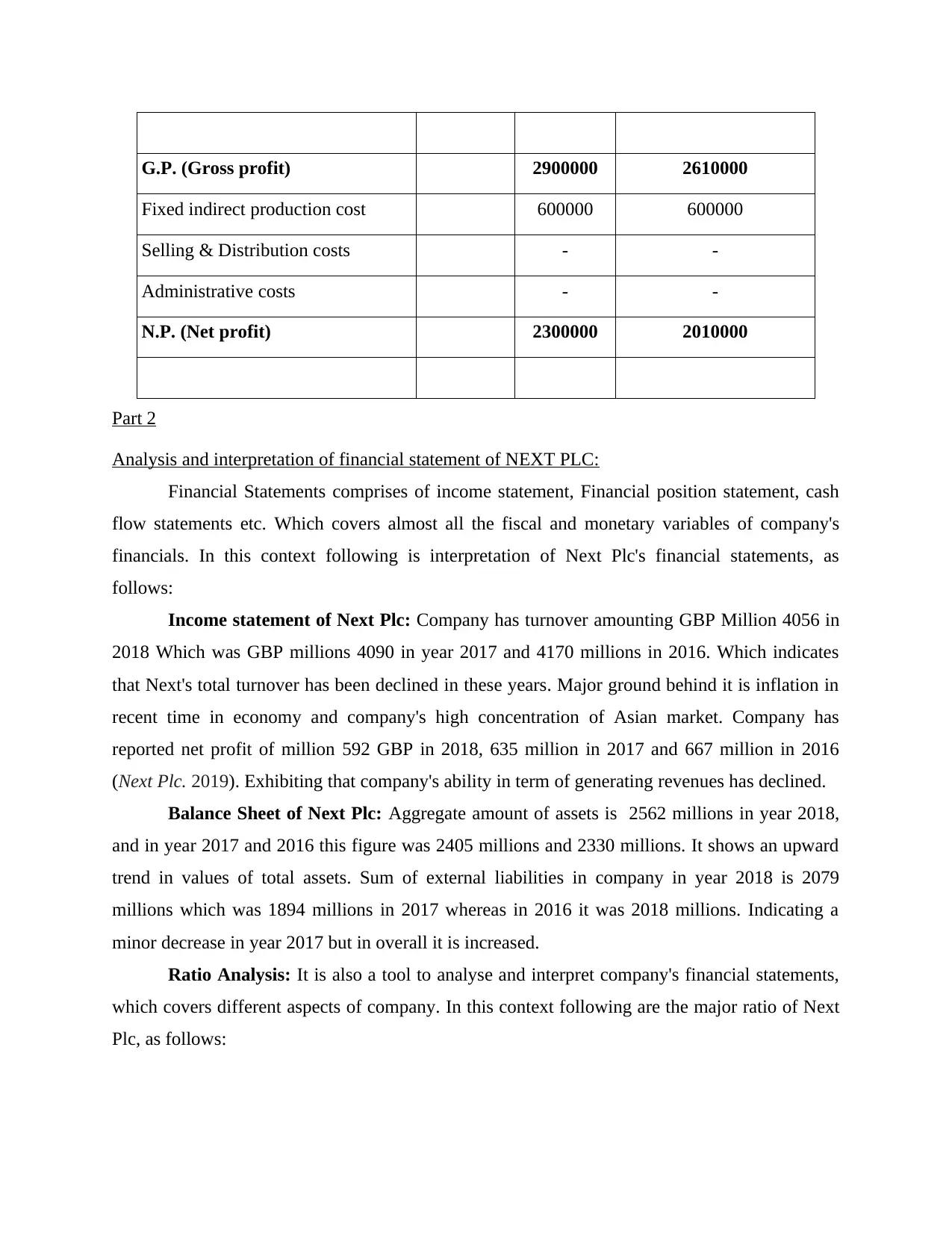

G.P. (Gross profit) 2900000 2610000

Fixed indirect production cost 600000 600000

Selling & Distribution costs - -

Administrative costs - -

N.P. (Net profit) 2300000 2010000

Part 2

Analysis and interpretation of financial statement of NEXT PLC:

Financial Statements comprises of income statement, Financial position statement, cash

flow statements etc. Which covers almost all the fiscal and monetary variables of company's

financials. In this context following is interpretation of Next Plc's financial statements, as

follows:

Income statement of Next Plc: Company has turnover amounting GBP Million 4056 in

2018 Which was GBP millions 4090 in year 2017 and 4170 millions in 2016. Which indicates

that Next's total turnover has been declined in these years. Major ground behind it is inflation in

recent time in economy and company's high concentration of Asian market. Company has

reported net profit of million 592 GBP in 2018, 635 million in 2017 and 667 million in 2016

(Next Plc. 2019). Exhibiting that company's ability in term of generating revenues has declined.

Balance Sheet of Next Plc: Aggregate amount of assets is 2562 millions in year 2018,

and in year 2017 and 2016 this figure was 2405 millions and 2330 millions. It shows an upward

trend in values of total assets. Sum of external liabilities in company in year 2018 is 2079

millions which was 1894 millions in 2017 whereas in 2016 it was 2018 millions. Indicating a

minor decrease in year 2017 but in overall it is increased.

Ratio Analysis: It is also a tool to analyse and interpret company's financial statements,

which covers different aspects of company. In this context following are the major ratio of Next

Plc, as follows:

Fixed indirect production cost 600000 600000

Selling & Distribution costs - -

Administrative costs - -

N.P. (Net profit) 2300000 2010000

Part 2

Analysis and interpretation of financial statement of NEXT PLC:

Financial Statements comprises of income statement, Financial position statement, cash

flow statements etc. Which covers almost all the fiscal and monetary variables of company's

financials. In this context following is interpretation of Next Plc's financial statements, as

follows:

Income statement of Next Plc: Company has turnover amounting GBP Million 4056 in

2018 Which was GBP millions 4090 in year 2017 and 4170 millions in 2016. Which indicates

that Next's total turnover has been declined in these years. Major ground behind it is inflation in

recent time in economy and company's high concentration of Asian market. Company has

reported net profit of million 592 GBP in 2018, 635 million in 2017 and 667 million in 2016

(Next Plc. 2019). Exhibiting that company's ability in term of generating revenues has declined.

Balance Sheet of Next Plc: Aggregate amount of assets is 2562 millions in year 2018,

and in year 2017 and 2016 this figure was 2405 millions and 2330 millions. It shows an upward

trend in values of total assets. Sum of external liabilities in company in year 2018 is 2079

millions which was 1894 millions in 2017 whereas in 2016 it was 2018 millions. Indicating a

minor decrease in year 2017 but in overall it is increased.

Ratio Analysis: It is also a tool to analyse and interpret company's financial statements,

which covers different aspects of company. In this context following are the major ratio of Next

Plc, as follows:

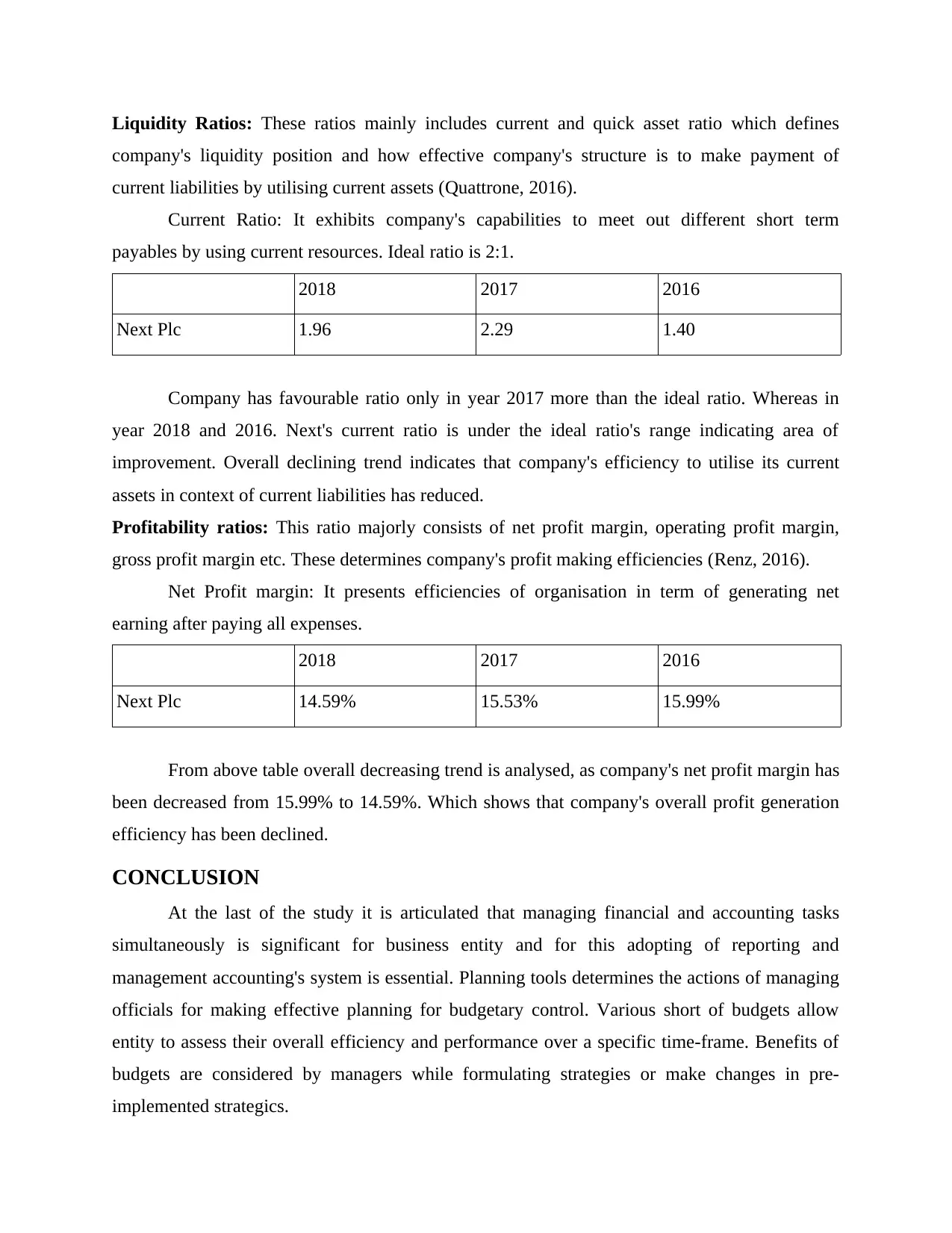

Liquidity Ratios: These ratios mainly includes current and quick asset ratio which defines

company's liquidity position and how effective company's structure is to make payment of

current liabilities by utilising current assets (Quattrone, 2016).

Current Ratio: It exhibits company's capabilities to meet out different short term

payables by using current resources. Ideal ratio is 2:1.

2018 2017 2016

Next Plc 1.96 2.29 1.40

Company has favourable ratio only in year 2017 more than the ideal ratio. Whereas in

year 2018 and 2016. Next's current ratio is under the ideal ratio's range indicating area of

improvement. Overall declining trend indicates that company's efficiency to utilise its current

assets in context of current liabilities has reduced.

Profitability ratios: This ratio majorly consists of net profit margin, operating profit margin,

gross profit margin etc. These determines company's profit making efficiencies (Renz, 2016).

Net Profit margin: It presents efficiencies of organisation in term of generating net

earning after paying all expenses.

2018 2017 2016

Next Plc 14.59% 15.53% 15.99%

From above table overall decreasing trend is analysed, as company's net profit margin has

been decreased from 15.99% to 14.59%. Which shows that company's overall profit generation

efficiency has been declined.

CONCLUSION

At the last of the study it is articulated that managing financial and accounting tasks

simultaneously is significant for business entity and for this adopting of reporting and

management accounting's system is essential. Planning tools determines the actions of managing

officials for making effective planning for budgetary control. Various short of budgets allow

entity to assess their overall efficiency and performance over a specific time-frame. Benefits of

budgets are considered by managers while formulating strategies or make changes in pre-

implemented strategics.

company's liquidity position and how effective company's structure is to make payment of

current liabilities by utilising current assets (Quattrone, 2016).

Current Ratio: It exhibits company's capabilities to meet out different short term

payables by using current resources. Ideal ratio is 2:1.

2018 2017 2016

Next Plc 1.96 2.29 1.40

Company has favourable ratio only in year 2017 more than the ideal ratio. Whereas in

year 2018 and 2016. Next's current ratio is under the ideal ratio's range indicating area of

improvement. Overall declining trend indicates that company's efficiency to utilise its current

assets in context of current liabilities has reduced.

Profitability ratios: This ratio majorly consists of net profit margin, operating profit margin,

gross profit margin etc. These determines company's profit making efficiencies (Renz, 2016).

Net Profit margin: It presents efficiencies of organisation in term of generating net

earning after paying all expenses.

2018 2017 2016

Next Plc 14.59% 15.53% 15.99%

From above table overall decreasing trend is analysed, as company's net profit margin has

been decreased from 15.99% to 14.59%. Which shows that company's overall profit generation

efficiency has been declined.

CONCLUSION

At the last of the study it is articulated that managing financial and accounting tasks

simultaneously is significant for business entity and for this adopting of reporting and

management accounting's system is essential. Planning tools determines the actions of managing

officials for making effective planning for budgetary control. Various short of budgets allow

entity to assess their overall efficiency and performance over a specific time-frame. Benefits of

budgets are considered by managers while formulating strategies or make changes in pre-

implemented strategics.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.