Management Accounting Tutorial - Finance Assignment Solution

VerifiedAdded on 2023/01/06

|13

|1981

|76

Homework Assignment

AI Summary

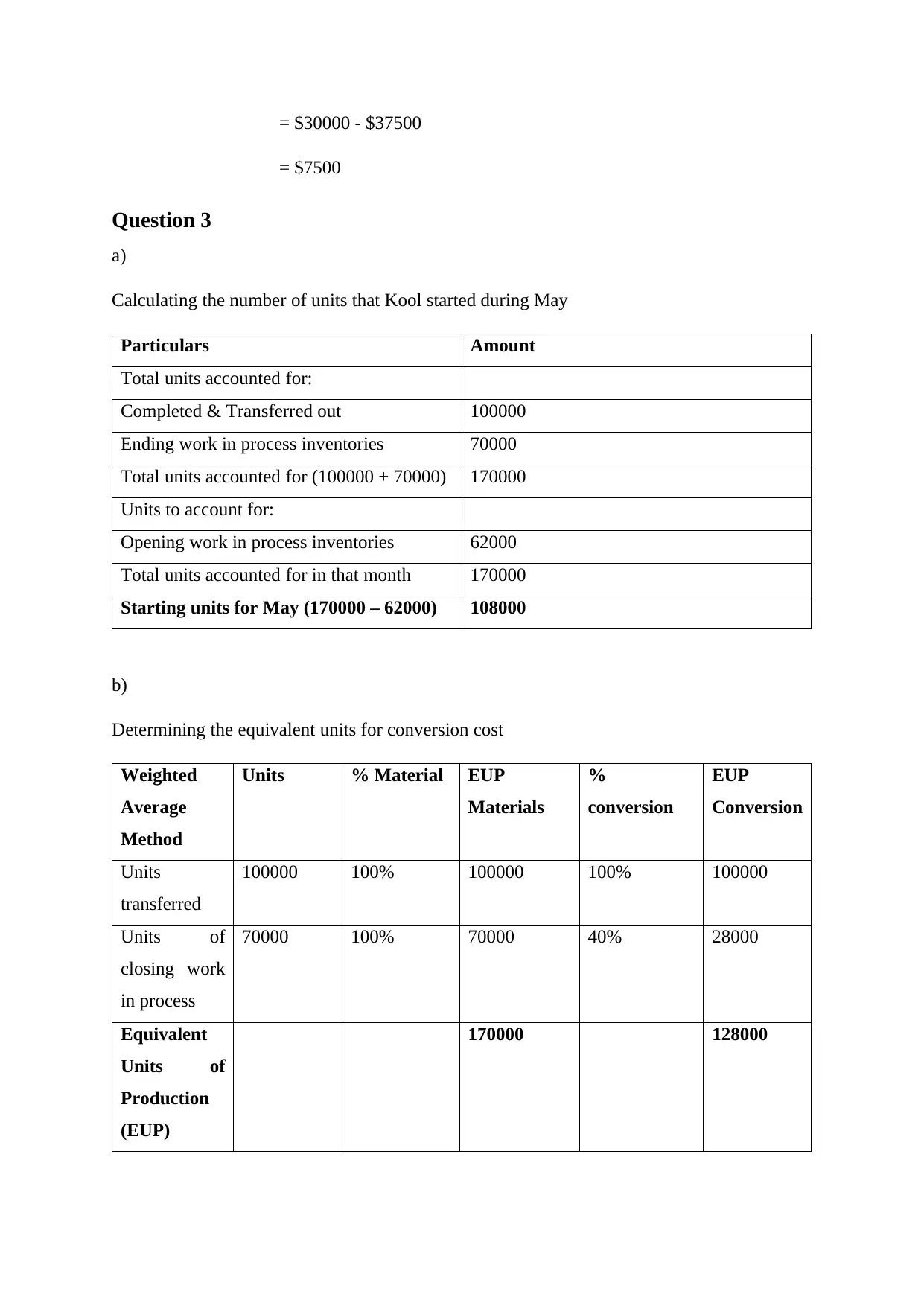

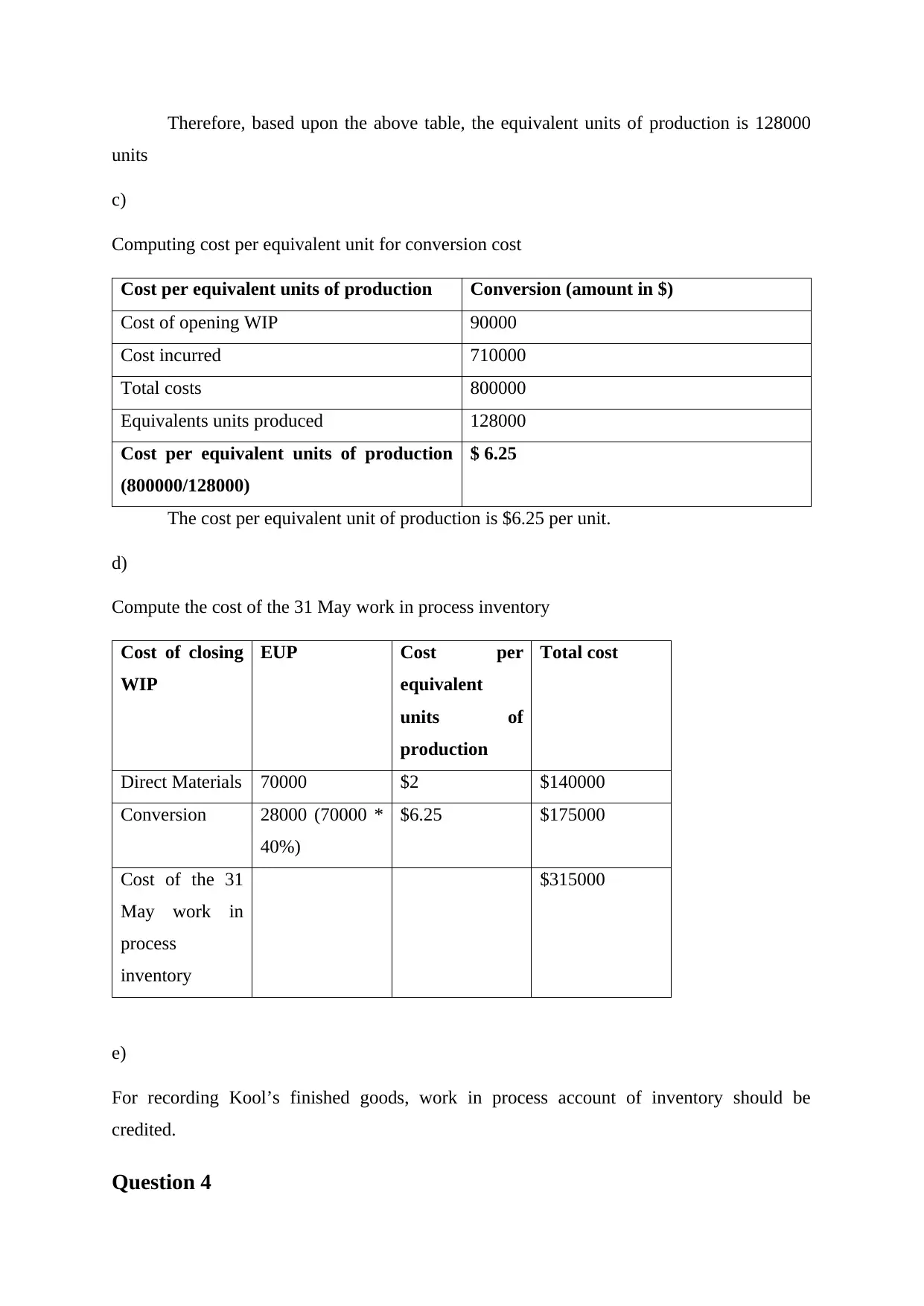

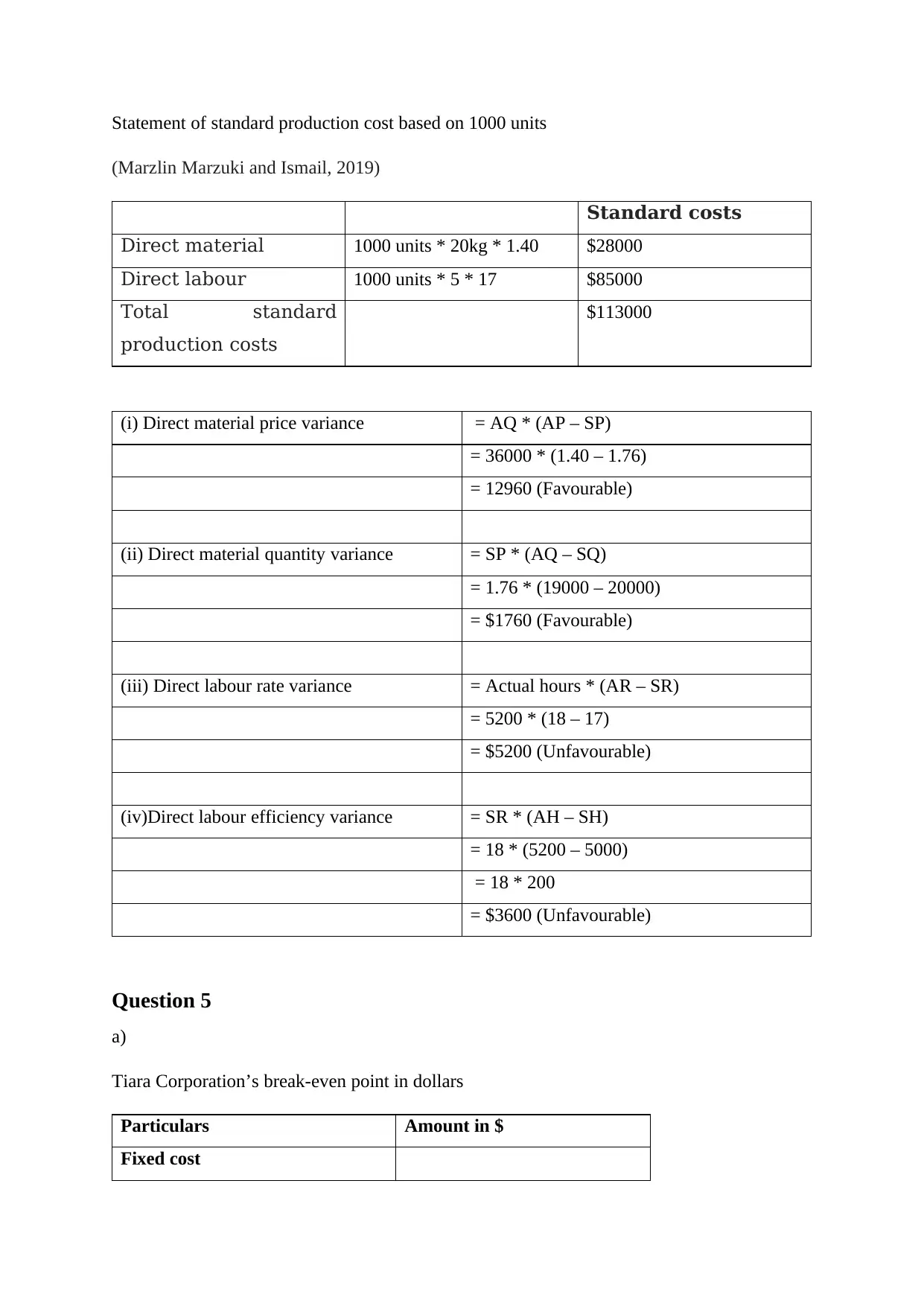

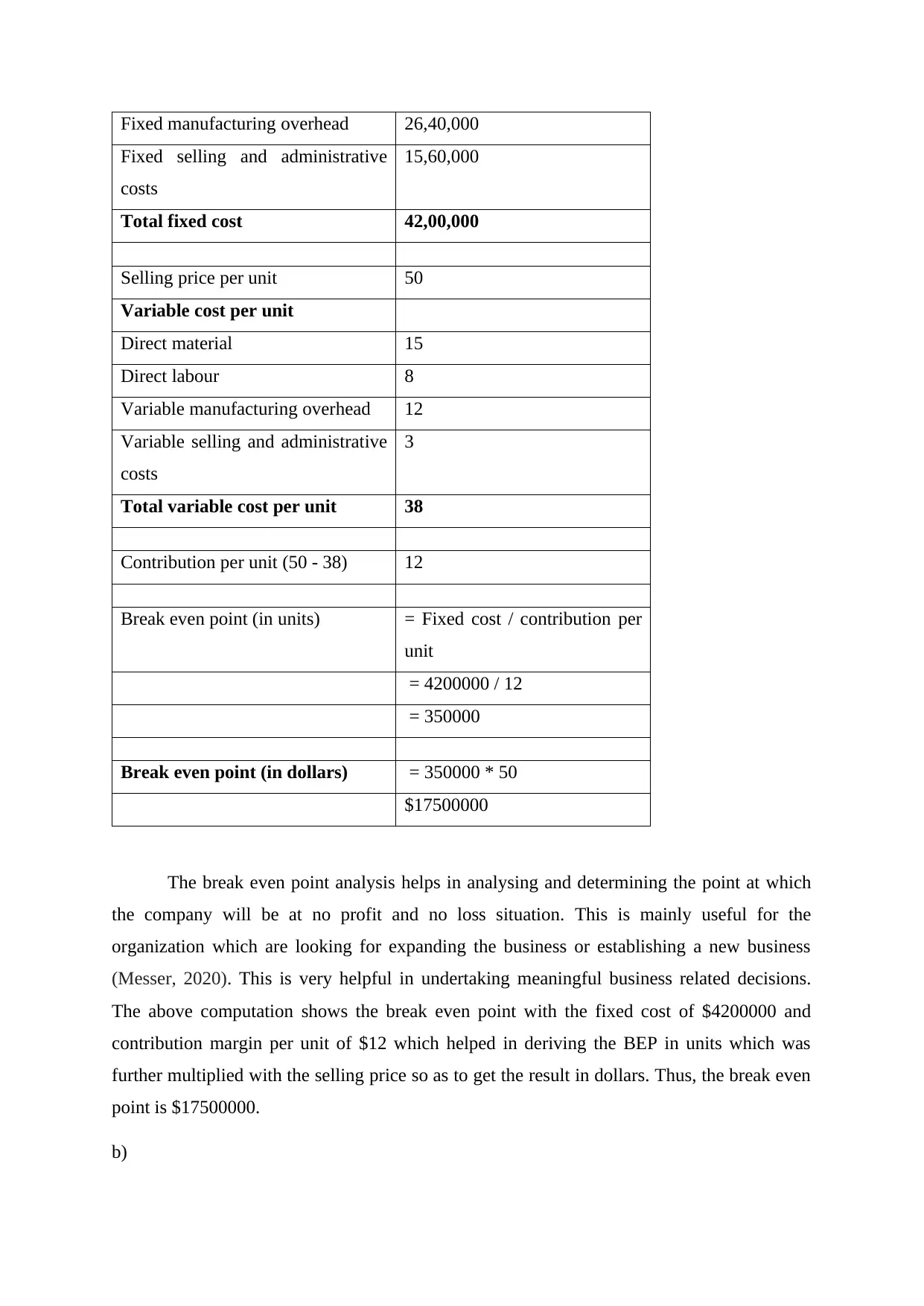

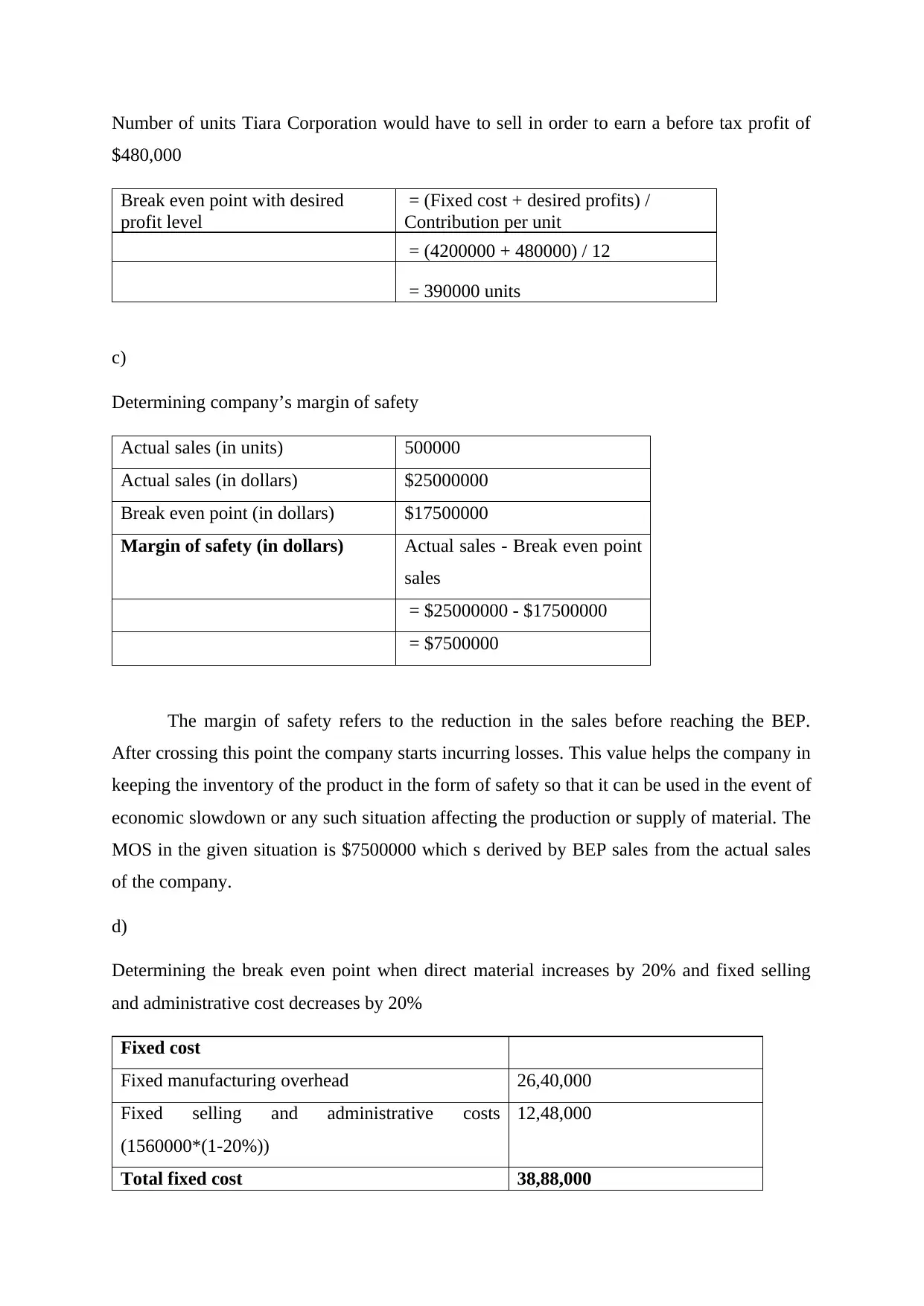

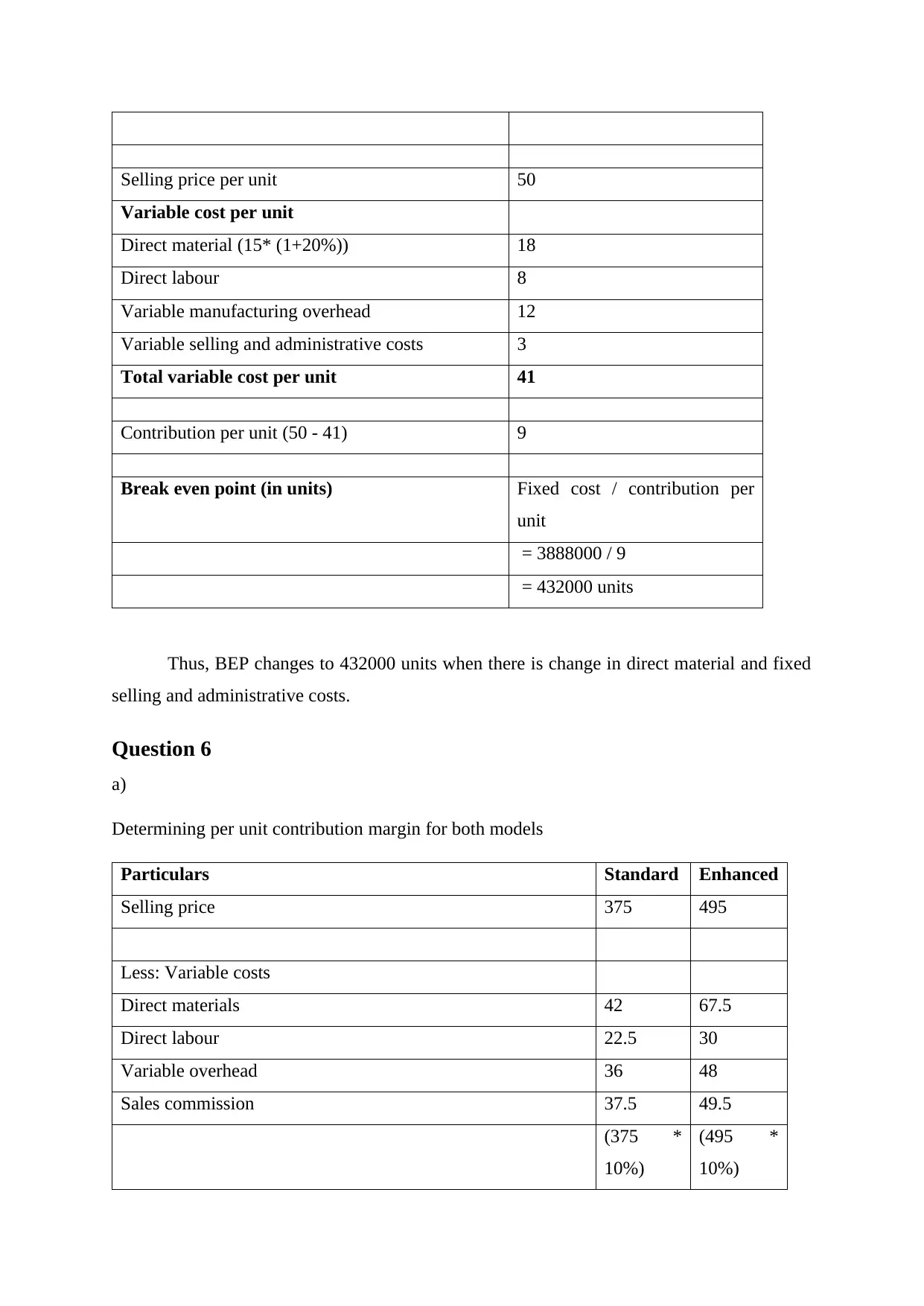

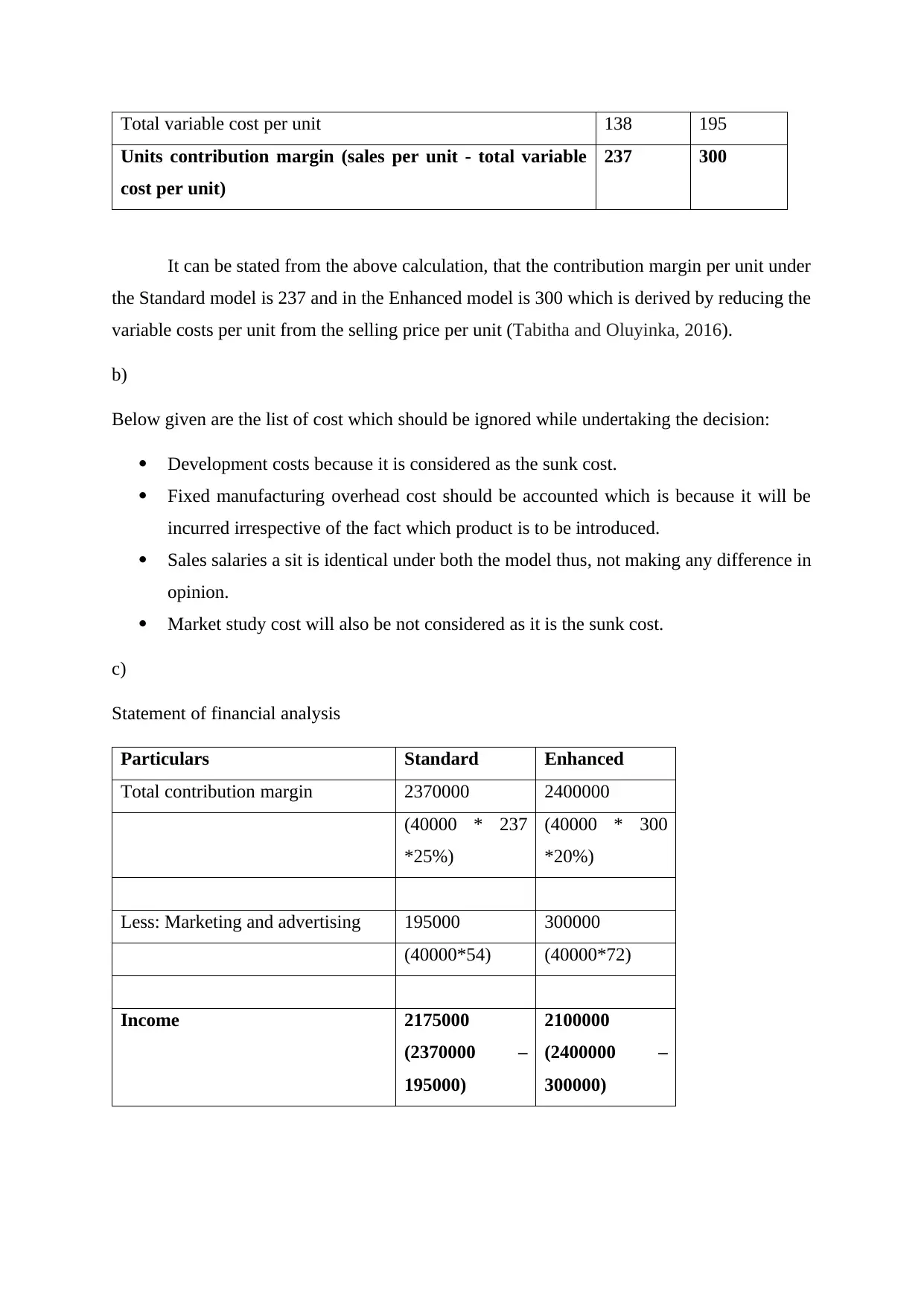

This document provides a comprehensive solution to a management accounting tutorial, addressing key concepts and calculations. It begins by analyzing cost behavior using the high-low method, distinguishing between fixed and variable costs, and formulating cost functions. The solution then delves into predetermined overhead rates, calculating and applying manufacturing overhead. Further analysis includes process costing, determining equivalent units of production, cost per equivalent unit, and work-in-process inventory valuation. The document also covers standard costing and variance analysis, computing direct material and labor variances. Break-even analysis is performed, calculating break-even points in units and dollars, and determining the margin of safety, along with an assessment of how changes in cost structures affect the break-even point. Finally, the solution concludes with a financial analysis of different product models, determining contribution margins, and providing recommendations based on the financial outcomes.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.