Managerial Accounting

Added on 2022-11-24

11 Pages1878 Words198 Views

MANAGERIAL ACCOUNTING

TABLE OF CONTENTS

QUESTION 1.............................................................................................................................3

Part A.....................................................................................................................................3

Part B......................................................................................................................................3

QUESTION 2.............................................................................................................................4

QUESTION 3.............................................................................................................................5

QUESTION 4.............................................................................................................................6

QUESTION 5.............................................................................................................................8

QUESTION 6.............................................................................................................................9

REFERENCES.........................................................................................................................11

QUESTION 1.............................................................................................................................3

Part A.....................................................................................................................................3

Part B......................................................................................................................................3

QUESTION 2.............................................................................................................................4

QUESTION 3.............................................................................................................................5

QUESTION 4.............................................................................................................................6

QUESTION 5.............................................................................................................................8

QUESTION 6.............................................................................................................................9

REFERENCES.........................................................................................................................11

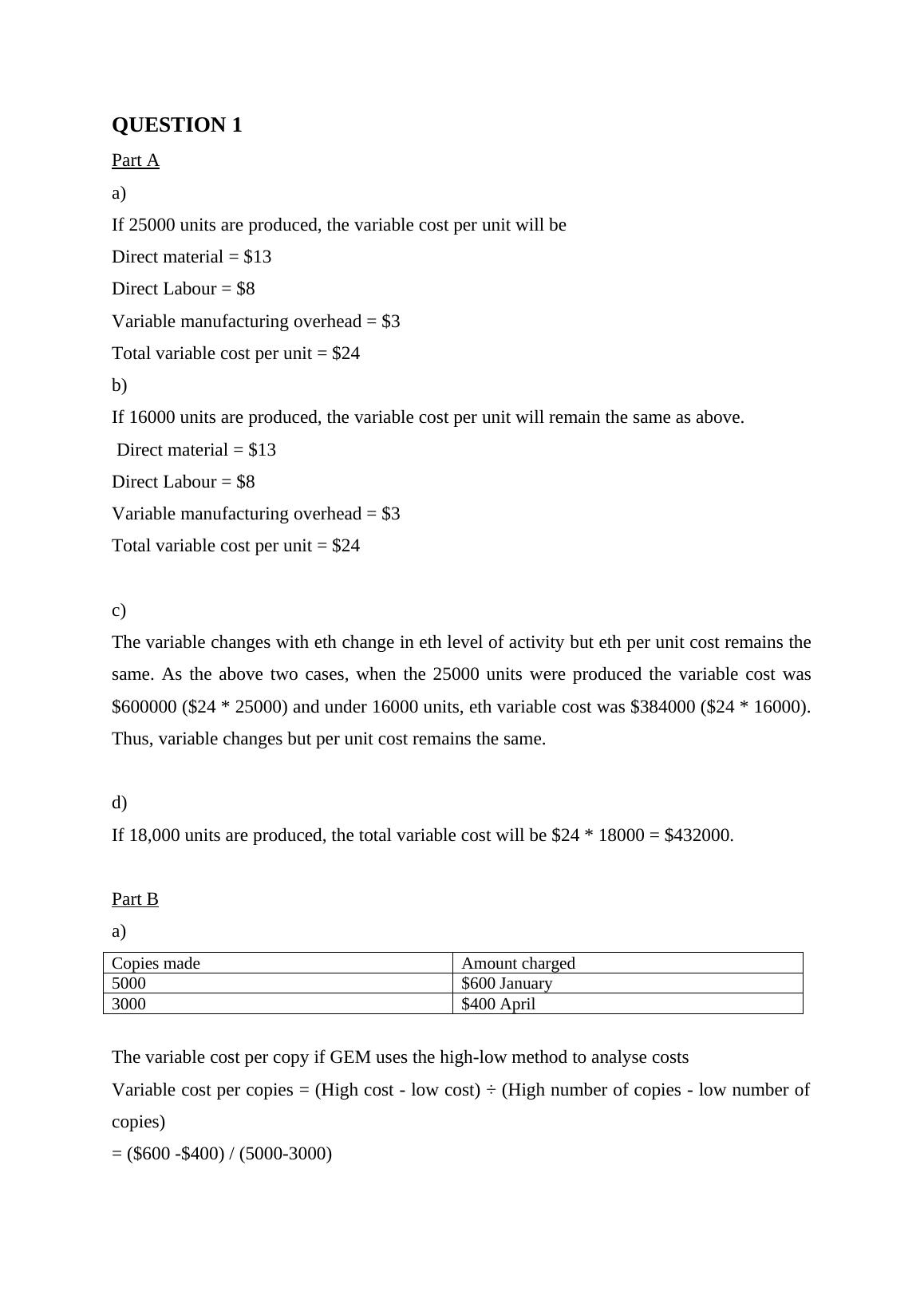

QUESTION 1

Part A

a)

If 25000 units are produced, the variable cost per unit will be

Direct material = $13

Direct Labour = $8

Variable manufacturing overhead = $3

Total variable cost per unit = $24

b)

If 16000 units are produced, the variable cost per unit will remain the same as above.

Direct material = $13

Direct Labour = $8

Variable manufacturing overhead = $3

Total variable cost per unit = $24

c)

The variable changes with eth change in eth level of activity but eth per unit cost remains the

same. As the above two cases, when the 25000 units were produced the variable cost was

$600000 ($24 * 25000) and under 16000 units, eth variable cost was $384000 ($24 * 16000).

Thus, variable changes but per unit cost remains the same.

d)

If 18,000 units are produced, the total variable cost will be $24 * 18000 = $432000.

Part B

a)

Copies made Amount charged

5000 $600 January

3000 $400 April

The variable cost per copy if GEM uses the high-low method to analyse costs

Variable cost per copies = (High cost - low cost) ÷ (High number of copies - low number of

copies)

= ($600 -$400) / (5000-3000)

Part A

a)

If 25000 units are produced, the variable cost per unit will be

Direct material = $13

Direct Labour = $8

Variable manufacturing overhead = $3

Total variable cost per unit = $24

b)

If 16000 units are produced, the variable cost per unit will remain the same as above.

Direct material = $13

Direct Labour = $8

Variable manufacturing overhead = $3

Total variable cost per unit = $24

c)

The variable changes with eth change in eth level of activity but eth per unit cost remains the

same. As the above two cases, when the 25000 units were produced the variable cost was

$600000 ($24 * 25000) and under 16000 units, eth variable cost was $384000 ($24 * 16000).

Thus, variable changes but per unit cost remains the same.

d)

If 18,000 units are produced, the total variable cost will be $24 * 18000 = $432000.

Part B

a)

Copies made Amount charged

5000 $600 January

3000 $400 April

The variable cost per copy if GEM uses the high-low method to analyse costs

Variable cost per copies = (High cost - low cost) ÷ (High number of copies - low number of

copies)

= ($600 -$400) / (5000-3000)

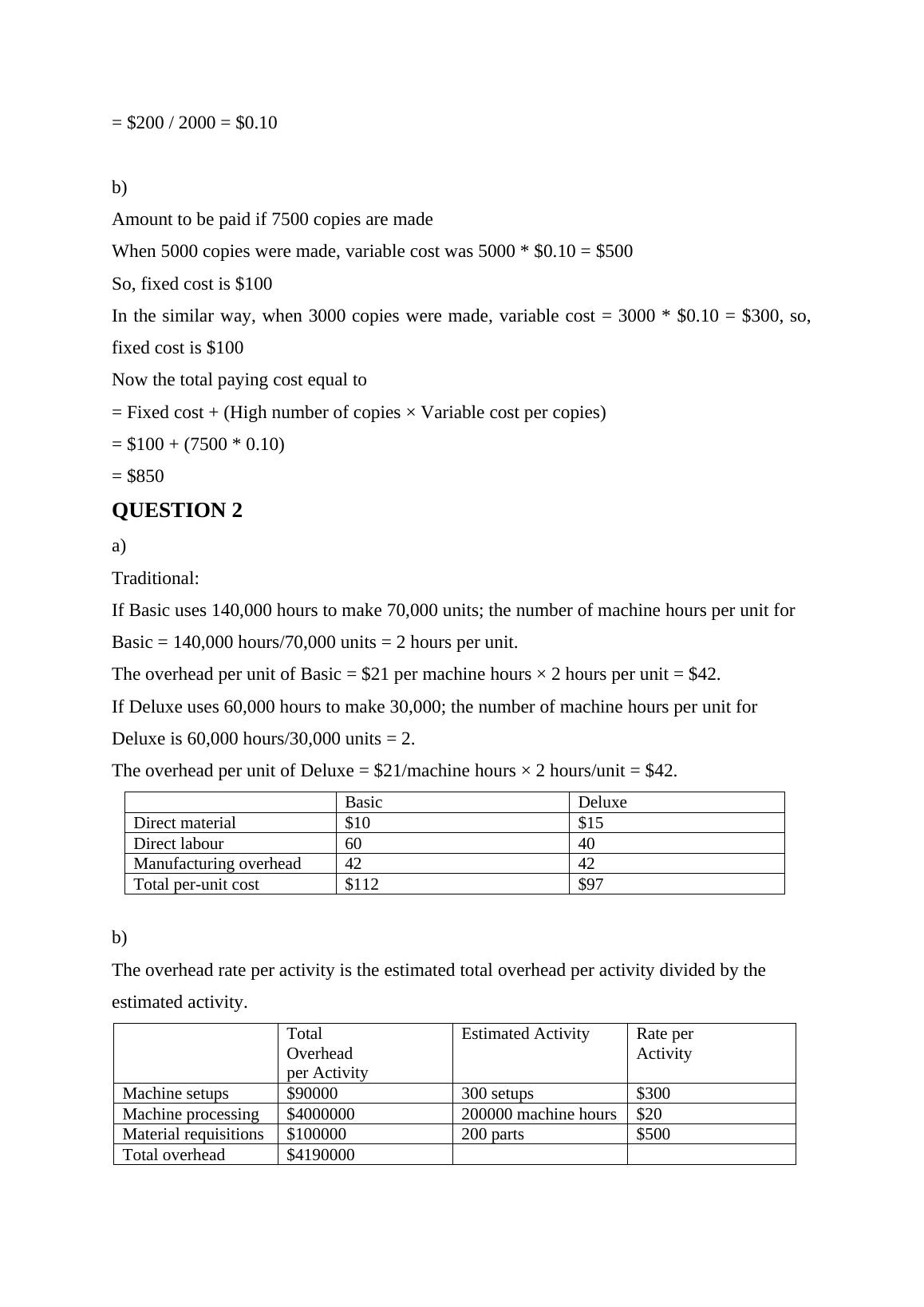

= $200 / 2000 = $0.10

b)

Amount to be paid if 7500 copies are made

When 5000 copies were made, variable cost was 5000 * $0.10 = $500

So, fixed cost is $100

In the similar way, when 3000 copies were made, variable cost = 3000 * $0.10 = $300, so,

fixed cost is $100

Now the total paying cost equal to

= Fixed cost + (High number of copies × Variable cost per copies)

= $100 + (7500 * 0.10)

= $850

QUESTION 2

a)

Traditional:

If Basic uses 140,000 hours to make 70,000 units; the number of machine hours per unit for

Basic = 140,000 hours/70,000 units = 2 hours per unit.

The overhead per unit of Basic = $21 per machine hours × 2 hours per unit = $42.

If Deluxe uses 60,000 hours to make 30,000; the number of machine hours per unit for

Deluxe is 60,000 hours/30,000 units = 2.

The overhead per unit of Deluxe = $21/machine hours × 2 hours/unit = $42.

Basic Deluxe

Direct material $10 $15

Direct labour 60 40

Manufacturing overhead 42 42

Total per-unit cost $112 $97

b)

The overhead rate per activity is the estimated total overhead per activity divided by the

estimated activity.

Total

Overhead

per Activity

Estimated Activity Rate per

Activity

Machine setups $90000 300 setups $300

Machine

processing

$4000000 200000 machine

hours

$20

Material $100000 200 parts $500

b)

Amount to be paid if 7500 copies are made

When 5000 copies were made, variable cost was 5000 * $0.10 = $500

So, fixed cost is $100

In the similar way, when 3000 copies were made, variable cost = 3000 * $0.10 = $300, so,

fixed cost is $100

Now the total paying cost equal to

= Fixed cost + (High number of copies × Variable cost per copies)

= $100 + (7500 * 0.10)

= $850

QUESTION 2

a)

Traditional:

If Basic uses 140,000 hours to make 70,000 units; the number of machine hours per unit for

Basic = 140,000 hours/70,000 units = 2 hours per unit.

The overhead per unit of Basic = $21 per machine hours × 2 hours per unit = $42.

If Deluxe uses 60,000 hours to make 30,000; the number of machine hours per unit for

Deluxe is 60,000 hours/30,000 units = 2.

The overhead per unit of Deluxe = $21/machine hours × 2 hours/unit = $42.

Basic Deluxe

Direct material $10 $15

Direct labour 60 40

Manufacturing overhead 42 42

Total per-unit cost $112 $97

b)

The overhead rate per activity is the estimated total overhead per activity divided by the

estimated activity.

Total

Overhead

per Activity

Estimated Activity Rate per

Activity

Machine setups $90000 300 setups $300

Machine

processing

$4000000 200000 machine

hours

$20

Material $100000 200 parts $500

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

FNSACC507 Management Accounting Information - Practice Questions and Solutionslg...

|8

|2079

|431

Management Accountinglg...

|13

|432

|59

Financial Performance (Online Exam)lg...

|13

|2787

|36

Zero Based Budgeting vs Incremental Budgetinglg...

|14

|2181

|84

Online Exam (Management and Cost Accounting)lg...

|17

|2620

|100

Management Accounting: Financial Analysis and Profit Maximizationlg...

|4

|735

|415