Analysis and Implication of Balance Scorecard in Management Accounting

VerifiedAdded on 2023/04/17

|9

|2001

|106

AI Summary

This article analyzes the balance scorecard approach in management accounting and its implications. It discusses the four elements of the balance scorecard and their significance for the company. The article also evaluates the arguments for and against the statement 'What's measured is what matters'.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction......................................................................................................................................3

Analysis and implication of Balance scorecard...............................................................................3

Balance Scorecard.......................................................................................................................3

Line of Causation.........................................................................................................................3

The implication of Balance Scorecard.........................................................................................5

Critical Evaluation – arguments for and against the statement...................................................5

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

Introduction......................................................................................................................................3

Analysis and implication of Balance scorecard...............................................................................3

Balance Scorecard.......................................................................................................................3

Line of Causation.........................................................................................................................3

The implication of Balance Scorecard.........................................................................................5

Critical Evaluation – arguments for and against the statement...................................................5

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

INTRODUCTION

Balance Scorecard model is developed by Robert Kaplan and David Norton, which measures the

strategic performance of the company (Kaplan, & Norton, 1992). The thesis is based on the

Evaluation of the statement

“What’s measured is what matters” and implication of the balance scorecard.

In this study, elements of balance scorecard will be analyzed. There are four elements, which

plays a significant role for the company, namely learning and growth perspective, internal

business process perspective, customer perspective, and financial perspective, are measured by

the company for evaluation of its performance. It assists the company in gaining a competitive

advantage as well as success in the long run period (Moore, Rowe, & Widener 2001). Further,

the critical evaluation for and against the statement is also described. The present report also

represents the manner in which balance Scorecard can be implemented by the company. The

argument against and in favour of the statement is reported in this study.

ANALYSIS AND IMPLICATION OF BALANCE SCORECARD

Balance Scorecard

The main objective of this approach is to convert the mission and vision of the company into the

actual performance. Thus, it is used by the management for the strategic planning and

communicating to the employees about their goals and objective of the company. It also assists

the company to balance the routine activities of employees according to their strategies and

evaluate and assess the performance in the direction of the strategic planning (Norreklit,

Jacobsen, & Mitchell, 2008). This approach is measured by the four crucial elements that have a

significant impact on the company. In the layman language, it can be said that Balance scorecard

measures the factors that build the value for the organization.

Line of Causation

The statement is what is measured is what matters; it means if X matters then it will be

measured. There are four elements such as learning and growth perspective, internal business

Balance Scorecard model is developed by Robert Kaplan and David Norton, which measures the

strategic performance of the company (Kaplan, & Norton, 1992). The thesis is based on the

Evaluation of the statement

“What’s measured is what matters” and implication of the balance scorecard.

In this study, elements of balance scorecard will be analyzed. There are four elements, which

plays a significant role for the company, namely learning and growth perspective, internal

business process perspective, customer perspective, and financial perspective, are measured by

the company for evaluation of its performance. It assists the company in gaining a competitive

advantage as well as success in the long run period (Moore, Rowe, & Widener 2001). Further,

the critical evaluation for and against the statement is also described. The present report also

represents the manner in which balance Scorecard can be implemented by the company. The

argument against and in favour of the statement is reported in this study.

ANALYSIS AND IMPLICATION OF BALANCE SCORECARD

Balance Scorecard

The main objective of this approach is to convert the mission and vision of the company into the

actual performance. Thus, it is used by the management for the strategic planning and

communicating to the employees about their goals and objective of the company. It also assists

the company to balance the routine activities of employees according to their strategies and

evaluate and assess the performance in the direction of the strategic planning (Norreklit,

Jacobsen, & Mitchell, 2008). This approach is measured by the four crucial elements that have a

significant impact on the company. In the layman language, it can be said that Balance scorecard

measures the factors that build the value for the organization.

Line of Causation

The statement is what is measured is what matters; it means if X matters then it will be

measured. There are four elements such as learning and growth perspective, internal business

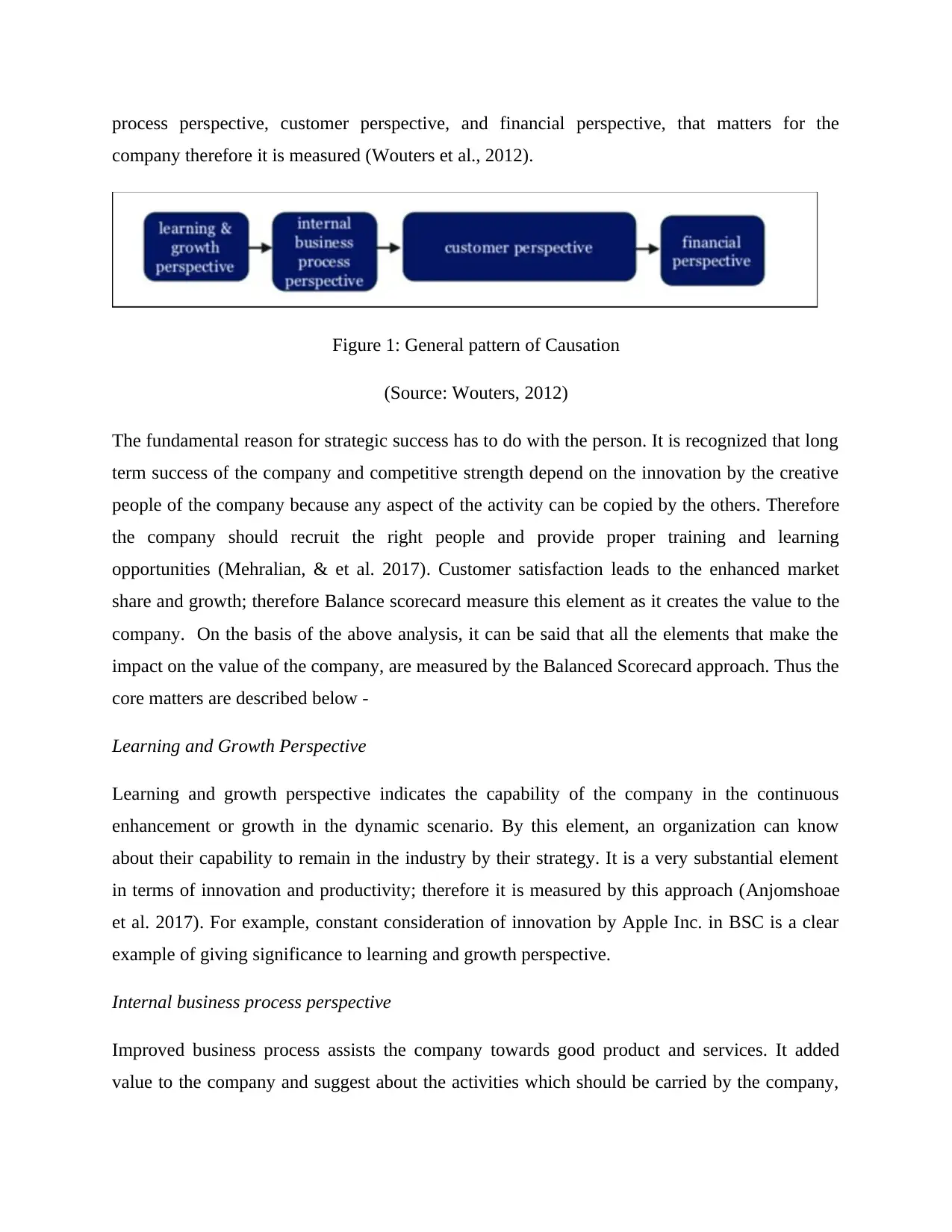

process perspective, customer perspective, and financial perspective, that matters for the

company therefore it is measured (Wouters et al., 2012).

Figure 1: General pattern of Causation

(Source: Wouters, 2012)

The fundamental reason for strategic success has to do with the person. It is recognized that long

term success of the company and competitive strength depend on the innovation by the creative

people of the company because any aspect of the activity can be copied by the others. Therefore

the company should recruit the right people and provide proper training and learning

opportunities (Mehralian, & et al. 2017). Customer satisfaction leads to the enhanced market

share and growth; therefore Balance scorecard measure this element as it creates the value to the

company. On the basis of the above analysis, it can be said that all the elements that make the

impact on the value of the company, are measured by the Balanced Scorecard approach. Thus the

core matters are described below -

Learning and Growth Perspective

Learning and growth perspective indicates the capability of the company in the continuous

enhancement or growth in the dynamic scenario. By this element, an organization can know

about their capability to remain in the industry by their strategy. It is a very substantial element

in terms of innovation and productivity; therefore it is measured by this approach (Anjomshoae

et al. 2017). For example, constant consideration of innovation by Apple Inc. in BSC is a clear

example of giving significance to learning and growth perspective.

Internal business process perspective

Improved business process assists the company towards good product and services. It added

value to the company and suggest about the activities which should be carried by the company,

company therefore it is measured (Wouters et al., 2012).

Figure 1: General pattern of Causation

(Source: Wouters, 2012)

The fundamental reason for strategic success has to do with the person. It is recognized that long

term success of the company and competitive strength depend on the innovation by the creative

people of the company because any aspect of the activity can be copied by the others. Therefore

the company should recruit the right people and provide proper training and learning

opportunities (Mehralian, & et al. 2017). Customer satisfaction leads to the enhanced market

share and growth; therefore Balance scorecard measure this element as it creates the value to the

company. On the basis of the above analysis, it can be said that all the elements that make the

impact on the value of the company, are measured by the Balanced Scorecard approach. Thus the

core matters are described below -

Learning and Growth Perspective

Learning and growth perspective indicates the capability of the company in the continuous

enhancement or growth in the dynamic scenario. By this element, an organization can know

about their capability to remain in the industry by their strategy. It is a very substantial element

in terms of innovation and productivity; therefore it is measured by this approach (Anjomshoae

et al. 2017). For example, constant consideration of innovation by Apple Inc. in BSC is a clear

example of giving significance to learning and growth perspective.

Internal business process perspective

Improved business process assists the company towards good product and services. It added

value to the company and suggest about the activities which should be carried by the company,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

so that objective can be achieved (Messeghem et al. 2018). This perspective assists the company

in its capability to satisfying their shareholders or customers. Nestle regular conducts the survey

from their customers and market participants to customize their products accordingly to

strengthen their BSC in terms of profit and customer satisfaction.

Customer perspective

Customer perspective plays a very important role in the success of the company. They make the

opinion about the company by considering the quality, services, price and many factors about the

company. By this perspective, the company can measure their brand image or position in the

market (Elbanna, Eid, and Kamel, 2015). Therefore, customer perspective makes the impact on

the company, and it is measured by this approach. On the basis of this aspect, Samsung includes

competitive reviews in their product analysis to improvise overall operational strategies.

Financial perspective

The quantification of the added value is the substantial element of the company. By this

approach, the company can ascertain about operational management and the implication of the

strategies and policies. Therefore it is measured by the balanced scorecard approach (Malagueño,

Lopez-Valeiras, and Gomez-Conde, 2017).

The management team of Volkswagen applies the balance scorecard approach after eight regular

years of financial loss. It assisted the company in applying the strategy to measure the financial

and project resources and to motivate and communicate the employees about the strategies and

planning.

The implication of Balance Scorecard

Any organization can implement the balanced scorecard approach; this includes the following

steps-

The company should establish its vision, mission, and strategic objectives.

Analysis and review the expectations of shareholders or customers by performing

stakeholder analysis (Hansen, and Schaltegger, 2016).

Identify critical success factors.

in its capability to satisfying their shareholders or customers. Nestle regular conducts the survey

from their customers and market participants to customize their products accordingly to

strengthen their BSC in terms of profit and customer satisfaction.

Customer perspective

Customer perspective plays a very important role in the success of the company. They make the

opinion about the company by considering the quality, services, price and many factors about the

company. By this perspective, the company can measure their brand image or position in the

market (Elbanna, Eid, and Kamel, 2015). Therefore, customer perspective makes the impact on

the company, and it is measured by this approach. On the basis of this aspect, Samsung includes

competitive reviews in their product analysis to improvise overall operational strategies.

Financial perspective

The quantification of the added value is the substantial element of the company. By this

approach, the company can ascertain about operational management and the implication of the

strategies and policies. Therefore it is measured by the balanced scorecard approach (Malagueño,

Lopez-Valeiras, and Gomez-Conde, 2017).

The management team of Volkswagen applies the balance scorecard approach after eight regular

years of financial loss. It assisted the company in applying the strategy to measure the financial

and project resources and to motivate and communicate the employees about the strategies and

planning.

The implication of Balance Scorecard

Any organization can implement the balanced scorecard approach; this includes the following

steps-

The company should establish its vision, mission, and strategic objectives.

Analysis and review the expectations of shareholders or customers by performing

stakeholder analysis (Hansen, and Schaltegger, 2016).

Identify critical success factors.

Convert the strategic planning into the goals.

Measure the objective by defining the key performance indicator.

Ascertain the values for the objectives that are to be obtained.

Convert the objective into the operational activities (Bourne, Melnyk, and Bititci, 2018).

Critical Evaluation – arguments for and against the statement

Balance Scorecard is implemented by the company to measure its performance. It is the

performance management technique that assists the managers in reviewing the activities of the

workers and outcomes of the activities (Cooper, Ezzamel, and Qu, 2017). All the above four

perspectives such as learning and growth perspective, internal business process perspective,

customer perspective, and financial perspective, are significant for the company, are measured

by the balanced scorecard approach. This approach permits the company to identify the gap

between the mission of the company and the manner by which the mission can be converted into

the operational performance of the company (Maestrini & et al. 2018). It also supports the day to

day activities of the company and suggests, how the activities can contribute to the mission and

objectives of the company. Along with this, by this, the company can ascertain about its

excellence regarding product, quality, service and some other aspect which leads to the

satisfaction of the consumers. Thus, it can be said that the Balance Scorecard approach helps in

the identification and measurement of the significant elements that are a matter to the company.

However, this approach is very subjective. It cannot be quantified except by the opinion of the

management and surveys. If the company, mandatorily make the policy for all the employees of

the company to meet the fixed training hours for learning and innovation, it does not necessarily

mean that every employee is attending the training in an effective manner. Further, by measuring

the four elements, the risk management and economic value of the company cannot be measured

accurately. Any goal and objective selected under the balanced scorecard approach, does not

consider the opportunity cost. Further, there are large numbers of variable considered by the

company to measure the elements, which is a very cumbersome and difficult task.

The things which are measured by the balanced scorecard approach is learning and growth

perspective, internal business process perspective, customer perspective, and financial

perspective. It cannot be said that everything that measured is a matter for the company. Since

Measure the objective by defining the key performance indicator.

Ascertain the values for the objectives that are to be obtained.

Convert the objective into the operational activities (Bourne, Melnyk, and Bititci, 2018).

Critical Evaluation – arguments for and against the statement

Balance Scorecard is implemented by the company to measure its performance. It is the

performance management technique that assists the managers in reviewing the activities of the

workers and outcomes of the activities (Cooper, Ezzamel, and Qu, 2017). All the above four

perspectives such as learning and growth perspective, internal business process perspective,

customer perspective, and financial perspective, are significant for the company, are measured

by the balanced scorecard approach. This approach permits the company to identify the gap

between the mission of the company and the manner by which the mission can be converted into

the operational performance of the company (Maestrini & et al. 2018). It also supports the day to

day activities of the company and suggests, how the activities can contribute to the mission and

objectives of the company. Along with this, by this, the company can ascertain about its

excellence regarding product, quality, service and some other aspect which leads to the

satisfaction of the consumers. Thus, it can be said that the Balance Scorecard approach helps in

the identification and measurement of the significant elements that are a matter to the company.

However, this approach is very subjective. It cannot be quantified except by the opinion of the

management and surveys. If the company, mandatorily make the policy for all the employees of

the company to meet the fixed training hours for learning and innovation, it does not necessarily

mean that every employee is attending the training in an effective manner. Further, by measuring

the four elements, the risk management and economic value of the company cannot be measured

accurately. Any goal and objective selected under the balanced scorecard approach, does not

consider the opportunity cost. Further, there are large numbers of variable considered by the

company to measure the elements, which is a very cumbersome and difficult task.

The things which are measured by the balanced scorecard approach is learning and growth

perspective, internal business process perspective, customer perspective, and financial

perspective. It cannot be said that everything that measured is a matter for the company. Since

the learning and growth aspect is connected with the employee of the company; it considers the

extent to which company can improve the manner of activities carried out by the employees

(Nielsen, Lund, and Thomsen, 2017), which supports its goal and objective. For this, the

company may start training to the employee, but it is not necessary that by training, knowledge

and skills of every employee can increase.

Further, there are some things that are important for the organization, which are not measured by

the balance scorecard approach. It mainly focuses on the internal aspect, but it does not consider

the external scenario of the company. It considers the consumers but does not take into account

the other key performance indicators such as any changes in the business environment or the

competitors are not considered by this approach. It may assist in more emphasis on the internal

performance and less focus on the external elements, by which the operational performance of

the company may get impacted (Lyu, Zhou, and Zhang, 2016).

Further, this can also be measured in the wrong way. This technique requires obtaining data from

the manager and will need them to assess other people. It also requires the building measures and

strategies of action, which is difficult. By which, the performance of the managers could be

impacted. Another problem is that there may be a possibility of false information. It is because,

high amount of information os required for the measurement; and there is no guarantee that the

information resultant will be correct which can falisified the measurement.

CONCLUSION

On the basis of the above analysis, it has been concluded that what is matter is measured by

BSC. Further, it has been evaluated that the Balance Scorecard approach can be implemented by

any company by establishing their vision, mission, and clarifying strategic objectives of the

company. Balance scorecard approach is an important technique for the performance

measurement, but it is a very subjective and cumbersome process.

extent to which company can improve the manner of activities carried out by the employees

(Nielsen, Lund, and Thomsen, 2017), which supports its goal and objective. For this, the

company may start training to the employee, but it is not necessary that by training, knowledge

and skills of every employee can increase.

Further, there are some things that are important for the organization, which are not measured by

the balance scorecard approach. It mainly focuses on the internal aspect, but it does not consider

the external scenario of the company. It considers the consumers but does not take into account

the other key performance indicators such as any changes in the business environment or the

competitors are not considered by this approach. It may assist in more emphasis on the internal

performance and less focus on the external elements, by which the operational performance of

the company may get impacted (Lyu, Zhou, and Zhang, 2016).

Further, this can also be measured in the wrong way. This technique requires obtaining data from

the manager and will need them to assess other people. It also requires the building measures and

strategies of action, which is difficult. By which, the performance of the managers could be

impacted. Another problem is that there may be a possibility of false information. It is because,

high amount of information os required for the measurement; and there is no guarantee that the

information resultant will be correct which can falisified the measurement.

CONCLUSION

On the basis of the above analysis, it has been concluded that what is matter is measured by

BSC. Further, it has been evaluated that the Balance Scorecard approach can be implemented by

any company by establishing their vision, mission, and clarifying strategic objectives of the

company. Balance scorecard approach is an important technique for the performance

measurement, but it is a very subjective and cumbersome process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Anjomshoae, A., Hassan, A., Kunz, N., Wong, K.Y. and de Leeuw, S., (2017). Toward a

dynamic balanced scorecard model for humanitarian relief organizations’ performance

management. Journal of Humanitarian Logistics and Supply Chain Management, 7(2), pp.194-

218.

Bourne, M., Melnyk, S. and Bititci, U.S., (2018). Performance measurement and management:

theory and practice. International Journal of Operations & Production Management, 38(11),

pp.2010-2021.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., (2017). Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research, 34(2), pp.991-1025.

Elbanna, S., Eid, R. and Kamel, H., (2015). Measuring hotel performance using the balanced

scorecard: A theoretical construct development and its empirical validation. International

Journal of Hospitality Management, 51(1), pp.105-114.

Hansen, E.G. and Schaltegger, S., (2016). The sustainability balanced scorecard: A systematic

review of architectures. Journal of Business Ethics, 133(2), pp.193-221.

Kaplan, R. S. & Norton, D. (1992). The Balanced Scorecard: Measures that Drive Performance.

Harvard Business Review 70(1), 71–79.

Lyu, H., Zhou, Z. and Zhang, Z., (2016). Measuring knowledge management performance in

organizations: an integrative framework of balanced scorecard and fuzzy

evaluation. Information, 7(2), p.29.

Maestrini, V., Martinez, V., Neely, A., Luzzini, D., Caniato, F. and Maccarrone, P., (2018). The

relationship regulator: a buyer-supplier collaborative performance measurement

system. International Journal of Operations & Production Management, 38(11), pp.2022-2039.

Malagueño, R., Lopez-Valeiras, E. and Gomez-Conde, J., (2017). Balanced scorecard in SMEs:

effects on innovation and financial performance. Small Business Economics, 1(1) pp.1-24.

Anjomshoae, A., Hassan, A., Kunz, N., Wong, K.Y. and de Leeuw, S., (2017). Toward a

dynamic balanced scorecard model for humanitarian relief organizations’ performance

management. Journal of Humanitarian Logistics and Supply Chain Management, 7(2), pp.194-

218.

Bourne, M., Melnyk, S. and Bititci, U.S., (2018). Performance measurement and management:

theory and practice. International Journal of Operations & Production Management, 38(11),

pp.2010-2021.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., (2017). Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research, 34(2), pp.991-1025.

Elbanna, S., Eid, R. and Kamel, H., (2015). Measuring hotel performance using the balanced

scorecard: A theoretical construct development and its empirical validation. International

Journal of Hospitality Management, 51(1), pp.105-114.

Hansen, E.G. and Schaltegger, S., (2016). The sustainability balanced scorecard: A systematic

review of architectures. Journal of Business Ethics, 133(2), pp.193-221.

Kaplan, R. S. & Norton, D. (1992). The Balanced Scorecard: Measures that Drive Performance.

Harvard Business Review 70(1), 71–79.

Lyu, H., Zhou, Z. and Zhang, Z., (2016). Measuring knowledge management performance in

organizations: an integrative framework of balanced scorecard and fuzzy

evaluation. Information, 7(2), p.29.

Maestrini, V., Martinez, V., Neely, A., Luzzini, D., Caniato, F. and Maccarrone, P., (2018). The

relationship regulator: a buyer-supplier collaborative performance measurement

system. International Journal of Operations & Production Management, 38(11), pp.2022-2039.

Malagueño, R., Lopez-Valeiras, E. and Gomez-Conde, J., (2017). Balanced scorecard in SMEs:

effects on innovation and financial performance. Small Business Economics, 1(1) pp.1-24.

Mehralian, G., Nazari, J.A., Nooriparto, G. and Rasekh, H.R., (2017). TQM and organizational

performance using the balanced scorecard approach. International Journal of Productivity and

Performance Management, 66(1), pp.111-125.

Messeghem, K., Bakkali, C., Sammut, S. and Swalhi, A., (2018). Measuring Nonprofit Incubator

Performance: Toward an Adapted Balanced Scorecard Approach. Journal of Small Business

Management, 56(4), pp.658-680.

Moore, Rowe, & Widener (2001). HCS: Designing a Balanced Scorecard in a Knowledge-Based

Firm. Issues in Accounting Education 16(4), 569–581.

Nielsen, C., Lund, M. and Thomsen, P., (2017). Killing the balanced scorecard to improve

internal disclosure. Journal of Intellectual Capital, 18(1), pp.45-62.

Norreklit, H., Jacobsen, M., & Mitchell, F. (2008). Pitfalls in using the balanced scorecard.

Journal of Corporate Accounting & Finance 19(6), 65–68.

Wouters et al., (2012), Cost management: Strategies for business decision. McGraw-Hill(p.804)

performance using the balanced scorecard approach. International Journal of Productivity and

Performance Management, 66(1), pp.111-125.

Messeghem, K., Bakkali, C., Sammut, S. and Swalhi, A., (2018). Measuring Nonprofit Incubator

Performance: Toward an Adapted Balanced Scorecard Approach. Journal of Small Business

Management, 56(4), pp.658-680.

Moore, Rowe, & Widener (2001). HCS: Designing a Balanced Scorecard in a Knowledge-Based

Firm. Issues in Accounting Education 16(4), 569–581.

Nielsen, C., Lund, M. and Thomsen, P., (2017). Killing the balanced scorecard to improve

internal disclosure. Journal of Intellectual Capital, 18(1), pp.45-62.

Norreklit, H., Jacobsen, M., & Mitchell, F. (2008). Pitfalls in using the balanced scorecard.

Journal of Corporate Accounting & Finance 19(6), 65–68.

Wouters et al., (2012), Cost management: Strategies for business decision. McGraw-Hill(p.804)

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.