Management Accounting Report: Katie Walker Furniture Analysis

VerifiedAdded on 2023/01/13

|20

|4842

|83

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its systems, techniques, and applications within an organization. It begins with an introduction to management accounting and its role in decision-making, followed by an exploration of different management accounting systems such as cost accounting, inventory management, job costing, and price optimization. The report then critically evaluates the integration of management accounting and reporting, highlighting various methods used in management accounting reporting, including budget reports, account receivable aging reports, job cost reports, and performance reports. Furthermore, it delves into cost calculation techniques, comparing marginal and absorption costing methods. The report also examines different planning tools for budgetary control, such as zero-based budgeting and capital budgeting, and discusses various pricing strategies to address financial problems. Finally, it compares how organizations can utilize management accounting to respond to financial challenges, drawing upon the case of Katie Walker Furniture. The report concludes with a discussion of the key takeaways and implications of the analysis.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

Management Accounting system and its types............................................................................3

Critical evaluation of integrating management accounting and reporting in an organization.....5

Methods used in management accounting reporting...................................................................5

LO2..................................................................................................................................................9

Calculating cost using appropriate techniques............................................................................9

LO3................................................................................................................................................10

Different types of planning tools for budgetary control............................................................10

Different types of pricing strategies that can be used to tackle financial problems..................12

LO4................................................................................................................................................13

Comparing the ways in which organization could use management accounting to respond to

financial problems.....................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES................................................................................................................................1

APPENDIX-1..................................................................................................................................2

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

Management Accounting system and its types............................................................................3

Critical evaluation of integrating management accounting and reporting in an organization.....5

Methods used in management accounting reporting...................................................................5

LO2..................................................................................................................................................9

Calculating cost using appropriate techniques............................................................................9

LO3................................................................................................................................................10

Different types of planning tools for budgetary control............................................................10

Different types of pricing strategies that can be used to tackle financial problems..................12

LO4................................................................................................................................................13

Comparing the ways in which organization could use management accounting to respond to

financial problems.....................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES................................................................................................................................1

APPENDIX-1..................................................................................................................................2

INTRODUCTION

Management accounting (MA) is the branch of accounting which involves gathering and

analysing relevant information and involves preparing timely reports that assists the manager in

taking managerial decision. In this, reports are prepared periodically and often include details of

the company's details. Reports are prepared for internal use by the management. It assists the

managers and supervisors in monitoring the performance of the organization and the reports are

prepared on weekly, monthly or quarterly basis as per the requirement and can be prepared as

requested by the manager. In this report, Katie Walker Furniture is taken as an organization,

which is in manufacturing sector. This report covers, introduction to MA and the different

methods used for MA reporting. It also includes different types of MA techniques, different

tools that are used in budgetary control and also a comparison is drawn between two companies

in respond to different financial problems.

LO1

Management Accounting system and its types

As per IMA, management accountant is a profession in which professionals requires

executing and apply different professional skills and knowledge in order to take meaningful

decisions managerial, planning and performance management and helps in implementing control

to assist management in formulating and implementing strategic management strategy

(Management accounting. 2020).

In simple words, management accounting is the system that is used by the internal

management team to analyse the data both financial and non financial in order to take decisions

at the right time.

Different Types of management accounting system

MA system is the system deployed by the management that helps in preparing reports in

the that can be used by the management in taking decisions. There are different types of MA

system that can be used by the organization, some of them are stated below.

Cost accounting system: It is a system that helps in determining the estimated cost of their

product which is used for the profitability analysis and cost control. It assists manufacturers in

keeping track on the production activities (Yang, Yu and Wang, 2016). In simple words, it is

used by the manufacturing organization in tracking the organization's inventory through various

production. It starts by tracking the raw material as and when it goes through the production

Management accounting (MA) is the branch of accounting which involves gathering and

analysing relevant information and involves preparing timely reports that assists the manager in

taking managerial decision. In this, reports are prepared periodically and often include details of

the company's details. Reports are prepared for internal use by the management. It assists the

managers and supervisors in monitoring the performance of the organization and the reports are

prepared on weekly, monthly or quarterly basis as per the requirement and can be prepared as

requested by the manager. In this report, Katie Walker Furniture is taken as an organization,

which is in manufacturing sector. This report covers, introduction to MA and the different

methods used for MA reporting. It also includes different types of MA techniques, different

tools that are used in budgetary control and also a comparison is drawn between two companies

in respond to different financial problems.

LO1

Management Accounting system and its types

As per IMA, management accountant is a profession in which professionals requires

executing and apply different professional skills and knowledge in order to take meaningful

decisions managerial, planning and performance management and helps in implementing control

to assist management in formulating and implementing strategic management strategy

(Management accounting. 2020).

In simple words, management accounting is the system that is used by the internal

management team to analyse the data both financial and non financial in order to take decisions

at the right time.

Different Types of management accounting system

MA system is the system deployed by the management that helps in preparing reports in

the that can be used by the management in taking decisions. There are different types of MA

system that can be used by the organization, some of them are stated below.

Cost accounting system: It is a system that helps in determining the estimated cost of their

product which is used for the profitability analysis and cost control. It assists manufacturers in

keeping track on the production activities (Yang, Yu and Wang, 2016). In simple words, it is

used by the manufacturing organization in tracking the organization's inventory through various

production. It starts by tracking the raw material as and when it goes through the production

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

process and then turned into finished product. For example, as the material moves from one stage

to another, the cost accounting system tracks and updates on the computer system The essential

of this system is that it must suits the size and nature of the organization.

Benefits:

Periodical determination of profit and loss.

Helps in executing control over material and supplies.

Helps in classification and division of cost.

Provides guidance for future production policies.

Inventory management system: It's a management tools that assists an organization in keeping

track of its inventory across the supply chain. It optimizes entire system from placing the order to

the supplier to the order delivery to the final customer. It includes the process of ordering, storing

and handling the inventory. It is important for every business irrespective of size. It is systematic

process which maintains and monitor the stocked products, raw material, finished and unfinished

products. The essential of this system is that it provides relevant information to maximize the

productivity.

Benefits:

Helps in minimizing the inventory cost and increasing the sales and profits.

Helps in integrating entire business.

Maintain customer satisfaction.

Reduces the risk of being out of stock.

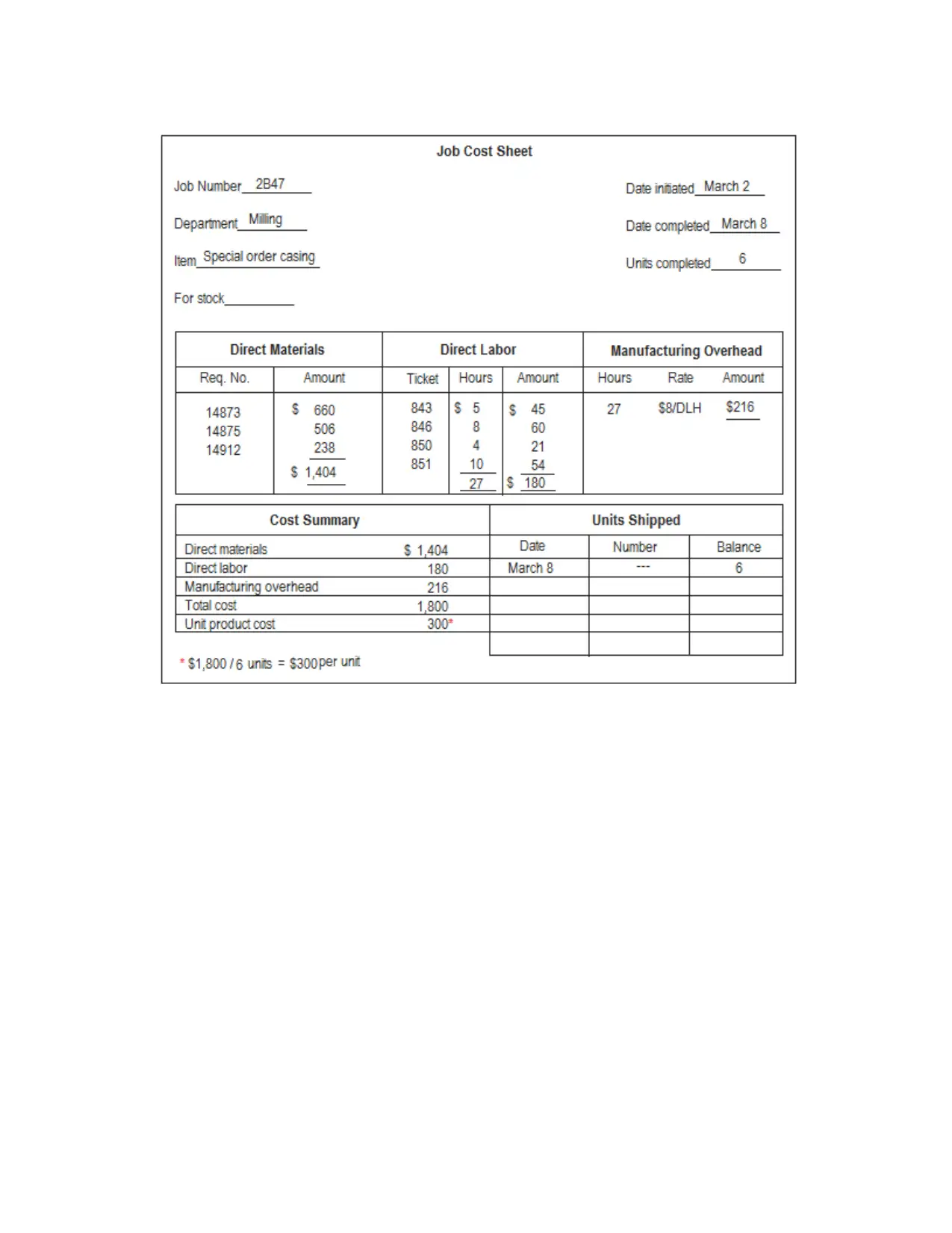

Job costing system: This system involves gathering the information with respect to the cost

attached with a product and service. It is useful for businesses that provides products and

services of different cost which is based on the customer specification. It takes into account

direct material and labour cost and indirect costs. It is essential in order to provide complete

details about the contract to the customers.

Benefits:

It helps in evaluating profitability of each job separately.

It can be used for estimating the cost of job similar to the previous one.

Helps in detecting defective work with specific job.

It provides details about the different cost associated with the job such as cost of

material and labour and overhead expenses of each job.

to another, the cost accounting system tracks and updates on the computer system The essential

of this system is that it must suits the size and nature of the organization.

Benefits:

Periodical determination of profit and loss.

Helps in executing control over material and supplies.

Helps in classification and division of cost.

Provides guidance for future production policies.

Inventory management system: It's a management tools that assists an organization in keeping

track of its inventory across the supply chain. It optimizes entire system from placing the order to

the supplier to the order delivery to the final customer. It includes the process of ordering, storing

and handling the inventory. It is important for every business irrespective of size. It is systematic

process which maintains and monitor the stocked products, raw material, finished and unfinished

products. The essential of this system is that it provides relevant information to maximize the

productivity.

Benefits:

Helps in minimizing the inventory cost and increasing the sales and profits.

Helps in integrating entire business.

Maintain customer satisfaction.

Reduces the risk of being out of stock.

Job costing system: This system involves gathering the information with respect to the cost

attached with a product and service. It is useful for businesses that provides products and

services of different cost which is based on the customer specification. It takes into account

direct material and labour cost and indirect costs. It is essential in order to provide complete

details about the contract to the customers.

Benefits:

It helps in evaluating profitability of each job separately.

It can be used for estimating the cost of job similar to the previous one.

Helps in detecting defective work with specific job.

It provides details about the different cost associated with the job such as cost of

material and labour and overhead expenses of each job.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimization system: It is the process in which evaluates how demand varies with price

and helps in fixing the price of the product and is also depends upon the customer's willingness

to pay. It is very important if the organization wants to link the volume with the profits and most

essential for raising profit with the same customer base. It determines how sensitive its clients

with respect to the change in the price. The essential of this system is to get the complete

information of cost and the recommended prices.

Benefits:

It automates the entire process.

Helps in better and quick decision making.

It helps in focusing on the various goals which results in better financial benefits.

Helps in tracking and optimizing price.

All the above are the different MA system that the organization can use to effectively

manage their business functioning. The successful implementation of the same will help the

organization to better decision and avoid unnecessary cost and wastage.

Critical evaluation of integrating management accounting and reporting in an organization

The integration of management accounting and reporting in an organization results into

integrated system. This will help the organization in efficiently analysing the performance and

proper decisions which will help in proper decision making and the managerial reports provides

direction to the managers in order to make effective strategy.

Methods used in management accounting reporting

Managerial reports helps organizations in monitoring company's performance. It is

prepared periodically as per the requirement. A detailed analysis is given below.

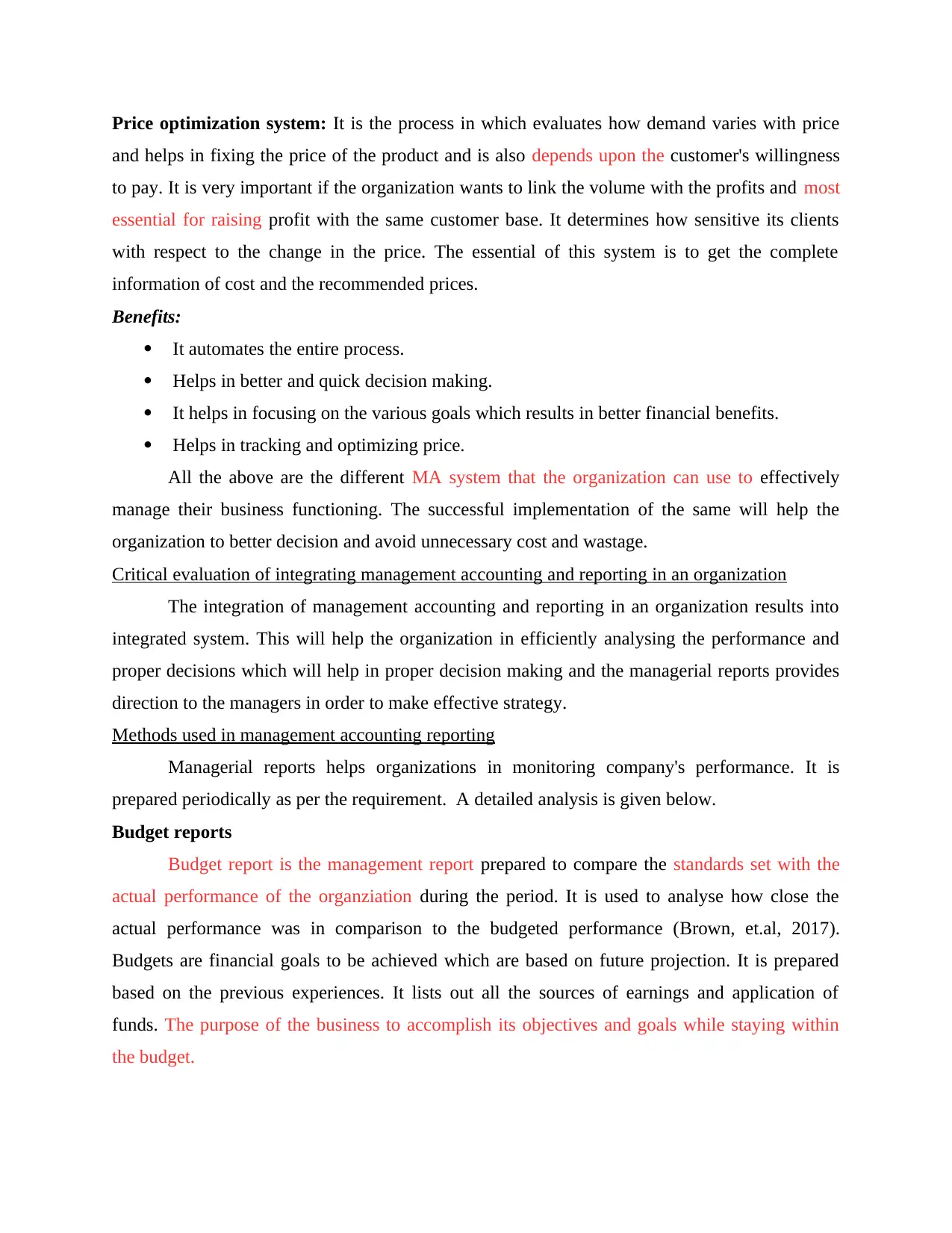

Budget reports

Budget report is the management report prepared to compare the standards set with the

actual performance of the organziation during the period. It is used to analyse how close the

actual performance was in comparison to the budgeted performance (Brown, et.al, 2017).

Budgets are financial goals to be achieved which are based on future projection. It is prepared

based on the previous experiences. It lists out all the sources of earnings and application of

funds. The purpose of the business to accomplish its objectives and goals while staying within

the budget.

and helps in fixing the price of the product and is also depends upon the customer's willingness

to pay. It is very important if the organization wants to link the volume with the profits and most

essential for raising profit with the same customer base. It determines how sensitive its clients

with respect to the change in the price. The essential of this system is to get the complete

information of cost and the recommended prices.

Benefits:

It automates the entire process.

Helps in better and quick decision making.

It helps in focusing on the various goals which results in better financial benefits.

Helps in tracking and optimizing price.

All the above are the different MA system that the organization can use to effectively

manage their business functioning. The successful implementation of the same will help the

organization to better decision and avoid unnecessary cost and wastage.

Critical evaluation of integrating management accounting and reporting in an organization

The integration of management accounting and reporting in an organization results into

integrated system. This will help the organization in efficiently analysing the performance and

proper decisions which will help in proper decision making and the managerial reports provides

direction to the managers in order to make effective strategy.

Methods used in management accounting reporting

Managerial reports helps organizations in monitoring company's performance. It is

prepared periodically as per the requirement. A detailed analysis is given below.

Budget reports

Budget report is the management report prepared to compare the standards set with the

actual performance of the organziation during the period. It is used to analyse how close the

actual performance was in comparison to the budgeted performance (Brown, et.al, 2017).

Budgets are financial goals to be achieved which are based on future projection. It is prepared

based on the previous experiences. It lists out all the sources of earnings and application of

funds. The purpose of the business to accomplish its objectives and goals while staying within

the budget.

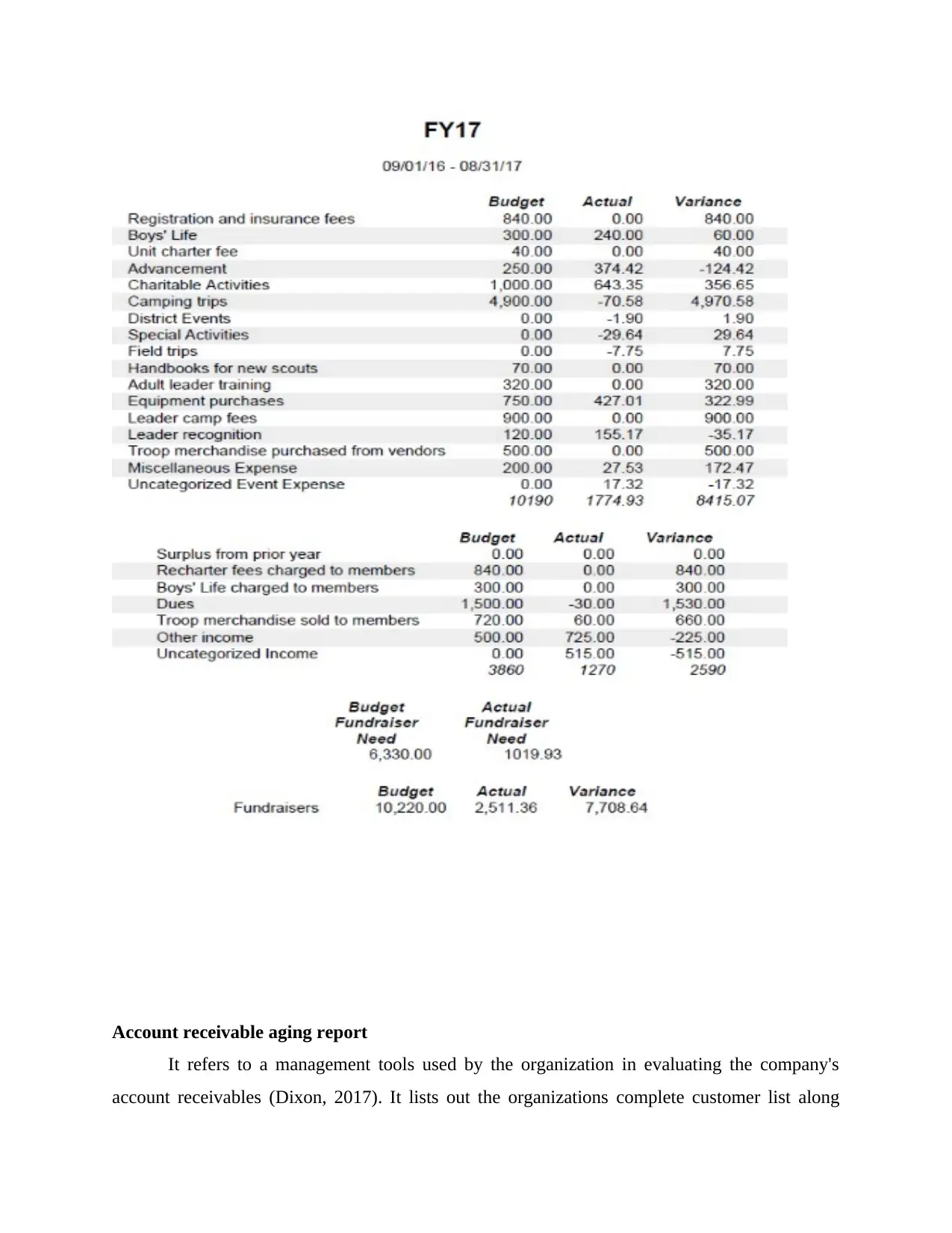

Account receivable aging report

It refers to a management tools used by the organization in evaluating the company's

account receivables (Dixon, 2017). It lists out the organizations complete customer list along

It refers to a management tools used by the organization in evaluating the company's

account receivables (Dixon, 2017). It lists out the organizations complete customer list along

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with the remaining balance. It also helps in determining the defaulters and any issues in the

company's collection process. This report provides an estimate of the amount of bad debts that

can incur and according to which provision is prepared.

Job cost report

It is report that tracks on the ongoing cost of the project. These are actually matched with

the revenue so that organization can determine the profits associated with the specific job

(Sullivan Denise, 2019). It helps the company to focus in the area where there are higher

earnings and does not waste time and efforts in the job with low margins. It also helps in

analysing the expense in the ongoing projects so the corrective actions can be taken before cost

escalate.

company's collection process. This report provides an estimate of the amount of bad debts that

can incur and according to which provision is prepared.

Job cost report

It is report that tracks on the ongoing cost of the project. These are actually matched with

the revenue so that organization can determine the profits associated with the specific job

(Sullivan Denise, 2019). It helps the company to focus in the area where there are higher

earnings and does not waste time and efforts in the job with low margins. It also helps in

analysing the expense in the ongoing projects so the corrective actions can be taken before cost

escalate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance report

This report is prepared to measure the organization's performance as a whole as well as

each employee within it. In large organizations, department wise reports are prepared, these

reports are used by mangers to take strategic decisions for achieving future goals of the

organization. These reports provide deep insight into the working of the organization. This report

plays an important role for the company to accurately measure their strategy.

LO2

Calculating cost using appropriate techniques

Calculations enclosed in Appendix-1

There are two different approaches that are used for valuation of inventory are marginal

and absorption costing methods. A detailed description is given below.

Marginal costing

It helps in de terming the variable cost per unit. It helps in ascertaining the additional cost

per unit and its impact on the overall profit of the organization with respect to change in the sales

volume. It is bifurcated into two types fixed and variable cost. It is used by the management for

decision making process which is mainly used in business expansion. As it helps in determining

break even point.

Absorption costing

This report is prepared to measure the organization's performance as a whole as well as

each employee within it. In large organizations, department wise reports are prepared, these

reports are used by mangers to take strategic decisions for achieving future goals of the

organization. These reports provide deep insight into the working of the organization. This report

plays an important role for the company to accurately measure their strategy.

LO2

Calculating cost using appropriate techniques

Calculations enclosed in Appendix-1

There are two different approaches that are used for valuation of inventory are marginal

and absorption costing methods. A detailed description is given below.

Marginal costing

It helps in de terming the variable cost per unit. It helps in ascertaining the additional cost

per unit and its impact on the overall profit of the organization with respect to change in the sales

volume. It is bifurcated into two types fixed and variable cost. It is used by the management for

decision making process which is mainly used in business expansion. As it helps in determining

break even point.

Absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is the accounting method which captures different costs in relation to a particular

product. It includes both direct and indirect cost. This method is required by GAAP for external

reporting. In this method, fixed overhead cost is allocated to the products irrespective to the fact

whether the product is sold or not.

It can be inferred from the calculation that absorption costing is more appropriate than

marginal method of costing. Absorption costing method helps organization in looking at the cost

completely and will be able to form strategy based on cost effectively. It takes in account both

fixed and variable cost while calculating cost of production. Also, it puts emphasis on cost of

each unit and change in opening and closing stocks affects the cost per unit. Marginal costing is

beneficial for the companies who have just started out their business and wants to know the

contribution per unit and the break even point for further decision making. Absorption costing is

widely used and also required by GAAP for reporting purpose. Thus, absorption costing method

is best for the valuation of inventory.

LO3

Different types of planning tools for budgetary control

Budget usually estimates the future outcome of the organization and the financial position

of the business (Hoggett, et.al, 2018). It is for future planning and performance measurement

needs. There are different types of tools that can be used are stated below.

Zero based budgeting

It is a method of budgeting in which the process starts from the scratch, that is, from zero

base. In this, budget is justified for each new period (Zero Based Budgeting (ZBB) – Overview &

Advantages. 2019). Each and every departments are analysed for its needs and cost. Based on

this budget is prepared irrespective of whether budget is higher or lower than the previous year.

Advantages:

It identifies obsolete process which is not necessary and are scrapped by the management.

It changes with the change in organization as underlying assumptions needs to be

changes.

It helps in efficient allocation of resources and increase profitability. It helps in lowering the cost as it carries out complete analysis.

Disadvantages:

product. It includes both direct and indirect cost. This method is required by GAAP for external

reporting. In this method, fixed overhead cost is allocated to the products irrespective to the fact

whether the product is sold or not.

It can be inferred from the calculation that absorption costing is more appropriate than

marginal method of costing. Absorption costing method helps organization in looking at the cost

completely and will be able to form strategy based on cost effectively. It takes in account both

fixed and variable cost while calculating cost of production. Also, it puts emphasis on cost of

each unit and change in opening and closing stocks affects the cost per unit. Marginal costing is

beneficial for the companies who have just started out their business and wants to know the

contribution per unit and the break even point for further decision making. Absorption costing is

widely used and also required by GAAP for reporting purpose. Thus, absorption costing method

is best for the valuation of inventory.

LO3

Different types of planning tools for budgetary control

Budget usually estimates the future outcome of the organization and the financial position

of the business (Hoggett, et.al, 2018). It is for future planning and performance measurement

needs. There are different types of tools that can be used are stated below.

Zero based budgeting

It is a method of budgeting in which the process starts from the scratch, that is, from zero

base. In this, budget is justified for each new period (Zero Based Budgeting (ZBB) – Overview &

Advantages. 2019). Each and every departments are analysed for its needs and cost. Based on

this budget is prepared irrespective of whether budget is higher or lower than the previous year.

Advantages:

It identifies obsolete process which is not necessary and are scrapped by the management.

It changes with the change in organization as underlying assumptions needs to be

changes.

It helps in efficient allocation of resources and increase profitability. It helps in lowering the cost as it carries out complete analysis.

Disadvantages:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is based on cost benefit analysis for a particular, the benefit of which can be achieved

in long term.

It is a time consuming process that requires lot of time and efforts to formulate it.

Manipulation can be done by managers to get more resource to their departments.

May incur conflict among managers over the allocation of funds.

Capital budgeting

It is process of evaluation whether to invest in a particular project or not and huge

expenses to be incurred with the aim to obtain the best return on investment. It usually takes into

consideration long term perspective of the organization (Khan, 2019). It revolves around capital

expenditure of the organization. Most business have the future plan to expand their business

which requires enough capital, that's where capital budgeting is used.

Advantages:

It helps in identifying and understanding the risk and its effects on the business.

Helps in exercising adequate control over expenditure.

Helps in better decision making related to investment opportunity. It abstains the organization from over or under investing.

Disadvantages:

Decisions are majorly for long term and are irreversible in nature.

Requires highly skilled professionals.

Wrong decision will adversely affect the business for long term.

Uncertainty or lack of accurate information will lead to wrong applicability.

Cash budgeting

It is a budget prepared for estimating the organizations cash receipt and expenditure for a

particular period. It takes into consideration cash inflow and cash outflow and helps in

determining the organization's cash position (Cash budget. 2020). This budget is used to

determine whether the organization is having sufficient amount to cash to carry out it day to day

business activities. It also helps in prioritizing the expenses based on its important. This budget is

made after preparing other budgets such as sales, purchase, production etc.

Advantages:

It helps to coordinate the different activities.

It helps in evaluating the cash position of the business.

in long term.

It is a time consuming process that requires lot of time and efforts to formulate it.

Manipulation can be done by managers to get more resource to their departments.

May incur conflict among managers over the allocation of funds.

Capital budgeting

It is process of evaluation whether to invest in a particular project or not and huge

expenses to be incurred with the aim to obtain the best return on investment. It usually takes into

consideration long term perspective of the organization (Khan, 2019). It revolves around capital

expenditure of the organization. Most business have the future plan to expand their business

which requires enough capital, that's where capital budgeting is used.

Advantages:

It helps in identifying and understanding the risk and its effects on the business.

Helps in exercising adequate control over expenditure.

Helps in better decision making related to investment opportunity. It abstains the organization from over or under investing.

Disadvantages:

Decisions are majorly for long term and are irreversible in nature.

Requires highly skilled professionals.

Wrong decision will adversely affect the business for long term.

Uncertainty or lack of accurate information will lead to wrong applicability.

Cash budgeting

It is a budget prepared for estimating the organizations cash receipt and expenditure for a

particular period. It takes into consideration cash inflow and cash outflow and helps in

determining the organization's cash position (Cash budget. 2020). This budget is used to

determine whether the organization is having sufficient amount to cash to carry out it day to day

business activities. It also helps in prioritizing the expenses based on its important. This budget is

made after preparing other budgets such as sales, purchase, production etc.

Advantages:

It helps to coordinate the different activities.

It helps in evaluating the cash position of the business.

It determines whether organization is having cash to meet its daily expenses. Helps in getting the clear picture of the reality.

Disadvantages:

It limits the spending power of the organization.

It does not reflect right profit.

It is based on the estimation and assumption.

Can be easily manipulated as per the requirement.

So, these planning tools helps Katie Walker Furniture, in solving financial problems

which will help the organization in achieving sustainable success. To be successful it requires

successful implementation of the same.

Different types of pricing strategies that can be used to tackle financial problems

There are different types of pricing strategies some of them are stated below.

Penetration pricing: In this pricing strategy, company uses low prices in order to enter the

market or to introduce new product.

Advantages

Acts as a barrier to new entrants.

It reduces competition as weaker and small competitors will leave the market.

Possibility to achieve dominant market position.

Disadvantages

Low quality of product will lead to loss of customers.

Price war with competitors lead to no gain of market share.

Brand conscious customers may not switch to low price products.

Price skimming: With this strategy, businesses enter the market with high priced products with

the aim of gaining revenue (Tay, K., 2019).

Advantages

Helps in gaining higher profits.

Effective in recovering cost.

Creates a high-quality image.

Disadvantages

Tough competition.

Much higher price may not be accepted by the consumers.

Disadvantages:

It limits the spending power of the organization.

It does not reflect right profit.

It is based on the estimation and assumption.

Can be easily manipulated as per the requirement.

So, these planning tools helps Katie Walker Furniture, in solving financial problems

which will help the organization in achieving sustainable success. To be successful it requires

successful implementation of the same.

Different types of pricing strategies that can be used to tackle financial problems

There are different types of pricing strategies some of them are stated below.

Penetration pricing: In this pricing strategy, company uses low prices in order to enter the

market or to introduce new product.

Advantages

Acts as a barrier to new entrants.

It reduces competition as weaker and small competitors will leave the market.

Possibility to achieve dominant market position.

Disadvantages

Low quality of product will lead to loss of customers.

Price war with competitors lead to no gain of market share.

Brand conscious customers may not switch to low price products.

Price skimming: With this strategy, businesses enter the market with high priced products with

the aim of gaining revenue (Tay, K., 2019).

Advantages

Helps in gaining higher profits.

Effective in recovering cost.

Creates a high-quality image.

Disadvantages

Tough competition.

Much higher price may not be accepted by the consumers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.