Evaluating Financial Resources and Performance Management Report

VerifiedAdded on 2023/04/07

|20

|5935

|251

Report

AI Summary

This report provides a comprehensive analysis of financial resources and performance management within an organization. It covers key performance ratios, costing methods, and the application of marginal costing for short-term decision-making. The report also explores cost management methodologies, including lean enterprise, business excellence, and value chain analysis. Furthermore, it delves into strategic management accounting for investments in advanced manufacturing technology and competitive strategy. Capital investment projects are appraised using alternative methodologies, and the cost of capital is calculated. The report also addresses financial risks in international markets, international investment decisions, and financing options for overseas subsidiaries. Finally, it identifies and evaluates organizational risks, employing techniques for risk management and reporting. This document is available on Desklib, a platform offering study tools and solved assignments.

Management of Financial Resources and Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction.................................................................................................................................................3

LO1.............................................................................................................................................................3

1.1 Identifying, calculating and interpreting key performance ratios from an organisation’s financial

statements....................................................................................................................................................3

1.1.1 Interpretation of efficiency, liquidity and financing ratios..................................................................3

1.1.2 Interpretation of Investment ratios......................................................................................................3

1.1.3 Recommendation of how performance can be improved....................................................................3

1.3 Using financial statements for evaluating comparative performance.....................................................3

1.3.1 Using of financial statement and online data to compare between competitors and industrial

averages.......................................................................................................................................................3

1.3.2 Use of industry comparison information and subscriber intelligence services....................................3

LO2.............................................................................................................................................................4

2.1 Evaluating several methodologies as well as approaches to the costing methods of services, functions,

products and activities.................................................................................................................................4

2.1.1 Treatment of direct and indirect cost in costing product and services.................................................4

2.1.2 Description of different cost treatment of job process and contracts...................................................4

2.1.3 Features and consequences of absorption costing...............................................................................4

2.2 Using methodology on marginal cost for supporting decision making procedures of short term...........4

2.2.1 Difference between fixed and variable cost........................................................................................4

2.2.2 Cost-Volume-Profit analysis and short term decision analysis...........................................................5

2.2.3 Relevant cost and application to decision making..............................................................................5

LO3.............................................................................................................................................................5

3.2 Using methodology on cost management for supporting business excellence, lean enterprise as well as

value chain analysis.....................................................................................................................................5

3.2.1 Relationship between lean enterprise, business excellence and value chains......................................5

3.2.2 Contribution of financial analysis on cost benefit of quality, throughput accounting, analysis of

waste, value analysis of activity chain.........................................................................................................6

3.2.3 Resource audit of value chain to measure effectiveness of each element and competitive advantage

of each process............................................................................................................................................6

3.3 Preparing and presenting accounting information of strategic management for analysing investment in

an advanced manufacturing technology as well as supporting competitive strategy....................................6

Introduction.................................................................................................................................................3

LO1.............................................................................................................................................................3

1.1 Identifying, calculating and interpreting key performance ratios from an organisation’s financial

statements....................................................................................................................................................3

1.1.1 Interpretation of efficiency, liquidity and financing ratios..................................................................3

1.1.2 Interpretation of Investment ratios......................................................................................................3

1.1.3 Recommendation of how performance can be improved....................................................................3

1.3 Using financial statements for evaluating comparative performance.....................................................3

1.3.1 Using of financial statement and online data to compare between competitors and industrial

averages.......................................................................................................................................................3

1.3.2 Use of industry comparison information and subscriber intelligence services....................................3

LO2.............................................................................................................................................................4

2.1 Evaluating several methodologies as well as approaches to the costing methods of services, functions,

products and activities.................................................................................................................................4

2.1.1 Treatment of direct and indirect cost in costing product and services.................................................4

2.1.2 Description of different cost treatment of job process and contracts...................................................4

2.1.3 Features and consequences of absorption costing...............................................................................4

2.2 Using methodology on marginal cost for supporting decision making procedures of short term...........4

2.2.1 Difference between fixed and variable cost........................................................................................4

2.2.2 Cost-Volume-Profit analysis and short term decision analysis...........................................................5

2.2.3 Relevant cost and application to decision making..............................................................................5

LO3.............................................................................................................................................................5

3.2 Using methodology on cost management for supporting business excellence, lean enterprise as well as

value chain analysis.....................................................................................................................................5

3.2.1 Relationship between lean enterprise, business excellence and value chains......................................5

3.2.2 Contribution of financial analysis on cost benefit of quality, throughput accounting, analysis of

waste, value analysis of activity chain.........................................................................................................6

3.2.3 Resource audit of value chain to measure effectiveness of each element and competitive advantage

of each process............................................................................................................................................6

3.3 Preparing and presenting accounting information of strategic management for analysing investment in

an advanced manufacturing technology as well as supporting competitive strategy....................................6

3.3.1 Identifying place of management accounting by analysing response to strategic positioning,

competitors and competitive advantage.......................................................................................................6

3.3.2 Appraising investments in the advanced technology..........................................................................7

3.3.3 Using balanced scorecard for supporting achievement over vision and strategy................................7

LO6.............................................................................................................................................................7

6.1 Appraising projects on capital investment utilising alternative methodologies......................................8

6.1.1 Distinction between profit and cash and the relevance to long term investment proposals.................8

6.1.2 Accounting rate of return, Payback and Net present value of an investment proposals......................9

6.1.3 Features and advantages of the alternative investment appraisal techniques.....................................10

6.2 Calculating cost of capital of any organisation and explaining limitations of uses..............................10

6.2.1 Calculation of equity, preferences and debt......................................................................................10

6.2.2 Weighted average cost and cost of capital using market and balance sheet values...........................11

6.2.3 Merits and demerits of different approaches of calculating cost of capital.......................................11

6.3 Evaluating opportunities of strategic investment as well as financially appraising strategic proposals11

6.3.1 Suitability of strategic investments in terms of strategic fits and exploitation of core competencies 11

6.3.2 Acceptability and feasibility of strategic investment against proposals criteria, stakeholders

expectations and strategic capability.........................................................................................................12

6.3.3 Qualitative and quantitative issues of strategic proposals.................................................................12

LO7...........................................................................................................................................................13

7.1 Identifying financial risks to operate in any international market........................................................13

7.1.1 Role and importance of international financial markets....................................................................13

7.1.2 Financial risk in the operation in international markets....................................................................13

7.1.3 Approaches for the managing economic, translation and transaction risk in international operations

................................................................................................................................................................... 13

7.2 Appraising decisions of international investment................................................................................13

7.2.1 Risk and complexities of capital budgeting in International context.................................................13

7.2.2 Calculation of forward rate and evaluation of a foreign capital project............................................13

7.2.3 Indirect and non quantifiable benefits and cost of international investment decision.......................13

7.3 Evaluating options of financing for overseas subsidiaries and multinationals.....................................14

7.3.1 Evaluation of internal and external source of finance for multinationals..........................................14

7.3.2 Role of Eurocurrency in international finance..................................................................................14

LO8...........................................................................................................................................................14

8.1 Identifying sources and types of risk in organisations.........................................................................14

8.1.1 Types and sources of risk in organisations........................................................................................14

competitors and competitive advantage.......................................................................................................6

3.3.2 Appraising investments in the advanced technology..........................................................................7

3.3.3 Using balanced scorecard for supporting achievement over vision and strategy................................7

LO6.............................................................................................................................................................7

6.1 Appraising projects on capital investment utilising alternative methodologies......................................8

6.1.1 Distinction between profit and cash and the relevance to long term investment proposals.................8

6.1.2 Accounting rate of return, Payback and Net present value of an investment proposals......................9

6.1.3 Features and advantages of the alternative investment appraisal techniques.....................................10

6.2 Calculating cost of capital of any organisation and explaining limitations of uses..............................10

6.2.1 Calculation of equity, preferences and debt......................................................................................10

6.2.2 Weighted average cost and cost of capital using market and balance sheet values...........................11

6.2.3 Merits and demerits of different approaches of calculating cost of capital.......................................11

6.3 Evaluating opportunities of strategic investment as well as financially appraising strategic proposals11

6.3.1 Suitability of strategic investments in terms of strategic fits and exploitation of core competencies 11

6.3.2 Acceptability and feasibility of strategic investment against proposals criteria, stakeholders

expectations and strategic capability.........................................................................................................12

6.3.3 Qualitative and quantitative issues of strategic proposals.................................................................12

LO7...........................................................................................................................................................13

7.1 Identifying financial risks to operate in any international market........................................................13

7.1.1 Role and importance of international financial markets....................................................................13

7.1.2 Financial risk in the operation in international markets....................................................................13

7.1.3 Approaches for the managing economic, translation and transaction risk in international operations

................................................................................................................................................................... 13

7.2 Appraising decisions of international investment................................................................................13

7.2.1 Risk and complexities of capital budgeting in International context.................................................13

7.2.2 Calculation of forward rate and evaluation of a foreign capital project............................................13

7.2.3 Indirect and non quantifiable benefits and cost of international investment decision.......................13

7.3 Evaluating options of financing for overseas subsidiaries and multinationals.....................................14

7.3.1 Evaluation of internal and external source of finance for multinationals..........................................14

7.3.2 Role of Eurocurrency in international finance..................................................................................14

LO8...........................................................................................................................................................14

8.1 Identifying sources and types of risk in organisations.........................................................................14

8.1.1 Types and sources of risk in organisations........................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8.1.3 Methods to deal with risk specific to overseas operation..................................................................15

8.2 Using appropriate techniques to evaluate and manage risks................................................................15

8.2.1 Risk maps and surveys......................................................................................................................15

8.2.2 Contingency plans for dealing with potential risk.............................................................................15

8.2.3 Assessing techniques to manage risk through avoidance, reduction transference and retention.......15

8.3 Preparing and utilising reports of risk management.............................................................................16

8.3.1 Need and value of formal risk management......................................................................................16

8.3.2 Identification of impact of risk in report linked to sensitivity...........................................................16

8.3.3 Content of risk management and way risk is to be managed.............................................................16

Conclusion.................................................................................................................................................16

References.................................................................................................................................................18

8.2 Using appropriate techniques to evaluate and manage risks................................................................15

8.2.1 Risk maps and surveys......................................................................................................................15

8.2.2 Contingency plans for dealing with potential risk.............................................................................15

8.2.3 Assessing techniques to manage risk through avoidance, reduction transference and retention.......15

8.3 Preparing and utilising reports of risk management.............................................................................16

8.3.1 Need and value of formal risk management......................................................................................16

8.3.2 Identification of impact of risk in report linked to sensitivity...........................................................16

8.3.3 Content of risk management and way risk is to be managed.............................................................16

Conclusion.................................................................................................................................................16

References.................................................................................................................................................18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

The smooth operation of an organisation depends upon proper managing of decision on business

operation and allocation of resources and funds. The support of the decision on the business

work helps in the proper availing of organisational success. In the following report the strategic

decision made for the proper achievement of success is dealt with. Along with the rise in the

better requirement of proper availing of resources, the success rate of organisation is depended

upon the interpretation of the financial statements and the resources of the organisation which is

considered to be Wired Retail.

LO1

1.1 Identifying, calculating and interpreting key performance ratios from an organisation’s

financial statements

1.1.1 Interpretation of efficiency, liquidity and financing ratios

The interpretation of the efficiency ratio helps in the better understanding of the efficiency of the

organization in dealing with unforeseen situation. The liquidity ratio marks the situation of the

organization in which the organization is capable enough to pay off the organisational debt.

1.1.2 Interpretation of Investment ratios

Interpretation of the investment ratios helps in the better understanding of the organisation, in

this case Wired Retail investment in the outside market. The achievement of the proper

interpretation of the investment ratio helps in the better understanding of the investment situation

in the organization.

1.1.3 Recommendation of how performance can be improved

The performance in Wired Retail can be improved with the ride in the better allocation of the

cash in the organization. The support of the cash flow analysis in the organisation would also

helps in the betterment of the performance of the organisation

1.3 Using financial statements for evaluating comparative performance

1.3.1 Using of financial statement and online data to compare between competitors and

industrial averages

The using of the financial statement in the context of online data regarding Wired Retail helps in

the better achieving of the success in the interpretation of the organizational operation. The value

of the organisation is better understood by the analysis of the financial statements.

1.3.2 Use of industry comparison information and subscriber intelligence services

The smooth operation of an organisation depends upon proper managing of decision on business

operation and allocation of resources and funds. The support of the decision on the business

work helps in the proper availing of organisational success. In the following report the strategic

decision made for the proper achievement of success is dealt with. Along with the rise in the

better requirement of proper availing of resources, the success rate of organisation is depended

upon the interpretation of the financial statements and the resources of the organisation which is

considered to be Wired Retail.

LO1

1.1 Identifying, calculating and interpreting key performance ratios from an organisation’s

financial statements

1.1.1 Interpretation of efficiency, liquidity and financing ratios

The interpretation of the efficiency ratio helps in the better understanding of the efficiency of the

organization in dealing with unforeseen situation. The liquidity ratio marks the situation of the

organization in which the organization is capable enough to pay off the organisational debt.

1.1.2 Interpretation of Investment ratios

Interpretation of the investment ratios helps in the better understanding of the organisation, in

this case Wired Retail investment in the outside market. The achievement of the proper

interpretation of the investment ratio helps in the better understanding of the investment situation

in the organization.

1.1.3 Recommendation of how performance can be improved

The performance in Wired Retail can be improved with the ride in the better allocation of the

cash in the organization. The support of the cash flow analysis in the organisation would also

helps in the betterment of the performance of the organisation

1.3 Using financial statements for evaluating comparative performance

1.3.1 Using of financial statement and online data to compare between competitors and

industrial averages

The using of the financial statement in the context of online data regarding Wired Retail helps in

the better achieving of the success in the interpretation of the organizational operation. The value

of the organisation is better understood by the analysis of the financial statements.

1.3.2 Use of industry comparison information and subscriber intelligence services

The intelligence services in an organisation generally deals with the ideas and the innovation

views of the organisation. The support of the organisation is better managed by the proper usage

of the intelligence services of the organisation

LO2

2.1 Evaluating several methodologies as well as approaches to the costing methods of

services, functions, products and activities

2.1.1 Treatment of direct and indirect cost in costing product and services

Direct costs are the cost incurred directly in the process of production and the indirect costs are

the cost incurred in the operation in directly related to the production sector. Indirectly costs

salaries and direct cost is wages. In order to control costs specific methodology can be followed

under which costing can be done on basis of approach of activity based costing. Under this for

different activities costing can be done separately and activities where cost is highly incurred can

be identified to make cost control decisions.

2.1.2 Description of different cost treatment of job process and contracts

There are mainly three types of job cost contract for the contracts. The fixed price or the lump

sum contracts, time and material contracts and the cost reimbursable contracts are namely the

types of the job cost in relation to the job cost contracts. All these contracts terms and conditions

must be evaluated in proper manner and accordingly cost must be computed. By doing so it can

be ensured that appropriate type of contract is selected in order to keep cost minimum.

2.1.3 Features and consequences of absorption costing

Absorption costing marks per unit cost of the organisation. The fixed cost of the organisation

simply divided by the number of units manufactured. In the absorption costing both fixed and

variable expenses are taken in to account. It is not necessary that every year firm incur fixed cost

in its business. In case fixed cost is not incurred previous year fixed cost will be taken in to

account which does not allowed accurate measurement of costing and profitability of business.

2.2 Using methodology on marginal cost for supporting decision making procedures of

short term

2.2.1 Difference between fixed and variable cost

The costs which are likely to change in the next moment or period is called variable cost and the

cost which are likely to remain the same for the coming years is called the fixed cost. Fixed cost

is incurred on specific day under big deal but variable cost is incurred on daily basis in the

views of the organisation. The support of the organisation is better managed by the proper usage

of the intelligence services of the organisation

LO2

2.1 Evaluating several methodologies as well as approaches to the costing methods of

services, functions, products and activities

2.1.1 Treatment of direct and indirect cost in costing product and services

Direct costs are the cost incurred directly in the process of production and the indirect costs are

the cost incurred in the operation in directly related to the production sector. Indirectly costs

salaries and direct cost is wages. In order to control costs specific methodology can be followed

under which costing can be done on basis of approach of activity based costing. Under this for

different activities costing can be done separately and activities where cost is highly incurred can

be identified to make cost control decisions.

2.1.2 Description of different cost treatment of job process and contracts

There are mainly three types of job cost contract for the contracts. The fixed price or the lump

sum contracts, time and material contracts and the cost reimbursable contracts are namely the

types of the job cost in relation to the job cost contracts. All these contracts terms and conditions

must be evaluated in proper manner and accordingly cost must be computed. By doing so it can

be ensured that appropriate type of contract is selected in order to keep cost minimum.

2.1.3 Features and consequences of absorption costing

Absorption costing marks per unit cost of the organisation. The fixed cost of the organisation

simply divided by the number of units manufactured. In the absorption costing both fixed and

variable expenses are taken in to account. It is not necessary that every year firm incur fixed cost

in its business. In case fixed cost is not incurred previous year fixed cost will be taken in to

account which does not allowed accurate measurement of costing and profitability of business.

2.2 Using methodology on marginal cost for supporting decision making procedures of

short term

2.2.1 Difference between fixed and variable cost

The costs which are likely to change in the next moment or period is called variable cost and the

cost which are likely to remain the same for the coming years is called the fixed cost. Fixed cost

is incurred on specific day under big deal but variable cost is incurred on daily basis in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business. This reflect that frequency of expenditure is high in case of variable expenses then

fixed expenses.

2.2.2 Cost-Volume-Profit analysis and short term decision analysis

Table Cost volume profit analysis

Sales 200000

Variable expenses 50000

Contribution 150000

Fixed cost 180

BEP 833.3333

Cost volume profit analysis is one of the most important method that reflect number of units that firm

need to sale in order to cover cost of production. As facts reveal there is need to sale 833 units to cover

variable expenses in business. The cost volume profit analysis is depended on the volume of

product sold on a price in relation to the cost of the product. The short term decision analyses are

based on the calculation related to the changes in the coming or nearby future.

2.2.3 Relevant cost and application to decision making

The cost and the relevance in the decision making are prime factor, as the decision made are

based on the cost spend by the organisation. The support of the organisation is thus provided by

the relevant cost and application.

LO3

3.2 Using methodology on cost management for supporting business excellence, lean

enterprise as well as value chain analysis

On the proper understanding of the values of the lean enterprise the proper, method that can be

availed for the better understanding of the values and the ideas is the secondary form of data

collection. The secondary form of data collection helps the further understanding of the operation

of the lean enterprise and the values of the chain analysis. The use of the research articles by

other writer would helps in the better understanding of the situation and the importance of the

organisation.

3.2.1 Relationship between lean enterprise, business excellence and value chains

As inferred by Liu et al. (2016, p.358), the lean enterprise model helps in the understanding the

smooth operation of the organisation it is related to the business excellence and value chains as it

monitors the objective of the organisation and optimises the enterprise flow. At same time cost

related data must also be gathered in order to keep tracking of expenses consistently in the

fixed expenses.

2.2.2 Cost-Volume-Profit analysis and short term decision analysis

Table Cost volume profit analysis

Sales 200000

Variable expenses 50000

Contribution 150000

Fixed cost 180

BEP 833.3333

Cost volume profit analysis is one of the most important method that reflect number of units that firm

need to sale in order to cover cost of production. As facts reveal there is need to sale 833 units to cover

variable expenses in business. The cost volume profit analysis is depended on the volume of

product sold on a price in relation to the cost of the product. The short term decision analyses are

based on the calculation related to the changes in the coming or nearby future.

2.2.3 Relevant cost and application to decision making

The cost and the relevance in the decision making are prime factor, as the decision made are

based on the cost spend by the organisation. The support of the organisation is thus provided by

the relevant cost and application.

LO3

3.2 Using methodology on cost management for supporting business excellence, lean

enterprise as well as value chain analysis

On the proper understanding of the values of the lean enterprise the proper, method that can be

availed for the better understanding of the values and the ideas is the secondary form of data

collection. The secondary form of data collection helps the further understanding of the operation

of the lean enterprise and the values of the chain analysis. The use of the research articles by

other writer would helps in the better understanding of the situation and the importance of the

organisation.

3.2.1 Relationship between lean enterprise, business excellence and value chains

As inferred by Liu et al. (2016, p.358), the lean enterprise model helps in the understanding the

smooth operation of the organisation it is related to the business excellence and value chains as it

monitors the objective of the organisation and optimises the enterprise flow. At same time cost

related data must also be gathered in order to keep tracking of expenses consistently in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business. By doing so cost can be controlled in the business and more control can be maintained

on waste. It keeps in check the useless flow of information. The lean enterprise also helps in the

focusing of the customer and thus leads to the rise in the reputation of the organisation in the

society.

3.2.2 Contribution of financial analysis on cost benefit of quality, throughput accounting,

analysis of waste, value analysis of activity chain

Analysis of the benefits gathered for the cost benefit quality analysis helps in the better

management of the organisational success and the proper understanding of the situation of the

organization operating in. It can be said that strategic management improve to great extent

because financial analysis help firm in evaluating its performance from different sides. Managers

make strategic decisions in respect to firm weak points and try to improve its performance.

Strategic decision may be related to quality control, cost and waste control. However, if firm will

ignore any important factor in analysis then ineffective strategic decision can be made by

managers. It is evident that the rise in the operation of the organisation is well cleared out of the

management. The management of the waste and the analysis of the value in the activity chain

also mark the opportunity of the organisation.

3.2.3 Resource audit of value chain to measure effectiveness of each element and

competitive advantage of each process

Audit plays an important role in the managing of the organisation operation. Resource

management and audit helps in the better understanding of the situation and the allocation of the

resources in the organisation. It is evident that the resource in the organisation needs to be well

allocated for the better achievement of the success and the proper meeting of the organisational

objective.

3.3 Preparing and presenting accounting information of strategic management for

analysing investment in an advanced manufacturing technology as well as supporting

competitive strategy

3.3.1 Identifying place of management accounting by analysing response to strategic

positioning, competitors and competitive advantage

Cost cutting is the one of the importance area where every firm like to place itself in respect to

strategic positioning. This is because if price of product will be low then in that case firm will be

able to offer its product at low price to customers. It is management accounting that provide

on waste. It keeps in check the useless flow of information. The lean enterprise also helps in the

focusing of the customer and thus leads to the rise in the reputation of the organisation in the

society.

3.2.2 Contribution of financial analysis on cost benefit of quality, throughput accounting,

analysis of waste, value analysis of activity chain

Analysis of the benefits gathered for the cost benefit quality analysis helps in the better

management of the organisational success and the proper understanding of the situation of the

organization operating in. It can be said that strategic management improve to great extent

because financial analysis help firm in evaluating its performance from different sides. Managers

make strategic decisions in respect to firm weak points and try to improve its performance.

Strategic decision may be related to quality control, cost and waste control. However, if firm will

ignore any important factor in analysis then ineffective strategic decision can be made by

managers. It is evident that the rise in the operation of the organisation is well cleared out of the

management. The management of the waste and the analysis of the value in the activity chain

also mark the opportunity of the organisation.

3.2.3 Resource audit of value chain to measure effectiveness of each element and

competitive advantage of each process

Audit plays an important role in the managing of the organisation operation. Resource

management and audit helps in the better understanding of the situation and the allocation of the

resources in the organisation. It is evident that the resource in the organisation needs to be well

allocated for the better achievement of the success and the proper meeting of the organisational

objective.

3.3 Preparing and presenting accounting information of strategic management for

analysing investment in an advanced manufacturing technology as well as supporting

competitive strategy

3.3.1 Identifying place of management accounting by analysing response to strategic

positioning, competitors and competitive advantage

Cost cutting is the one of the importance area where every firm like to place itself in respect to

strategic positioning. This is because if price of product will be low then in that case firm will be

able to offer its product at low price to customers. It is management accounting that provide

relevant inputs to managers in respect to evaluating cost and making relevant decisions. By

identifying areas where work need to be done and taking action on same firm make its strategic

position strong. All these things keep firm one step ahead of rivals and lead to development of

competitive advantage in business. As supported by Durand et al. (2017, p), the competitive

advantages in the organization is well managed and determined by the development in the

organizational process of decision making. The decision making is to be settle in terms of the

position of the organization. Better positioning and proper analysis of the competitors helps in

bringing out the competitive advantage of the organisation.

3.3.2 Appraising investments in the advanced technology

Investments in advanced technology are of prime importance as the growth in the organisation

depends upon the proper implementation of the technology. The investment in the advanced

technology helps in bringing in more production and results in hike revenue. The opportunity

also increases with the broadening of the area in technology field. Thus, strategic decision is to

select whether to investment in an advanced technology related to manufacturing. Investment

must be made in the project but strategic issues must also be identified like it is possible that

advanced technology related to manufacturing acquired by firm but it become obsolete in few

years before completion of life. In that situation biggest challenge is to ensure that asset will be

used more and more within certain time period. If it became obsolete in 3 to 4 years the

investment may go waste. There is rationale behind considering these factors because by doing

so better decision can be made in respect to investment. However, decision would be that

investment must be made in advanced technology that is in current time period. If it became

obsolete shortly then same can be sold to other firm in nation or in foreign country and from

proceeds amount new technology can be acquired. By doing so issue can be eliminated.

3.3.3 Using balanced scorecard for supporting achievement over vision and strategy

As supported by Mechler, (2016, p.2122), the opportunity provided by the usage of the scorecard

is mainly in gaining advantages over the strategies in the organization. The organisational

support is more effectively achieved with the better achievement of the vision and strategies. The

vision and the strategy are correlated to each other as there is strong relation between them in

bringing in the success of the organisation.

LO6

6.1 Appraising projects on capital investment utilising alternative methodologies

identifying areas where work need to be done and taking action on same firm make its strategic

position strong. All these things keep firm one step ahead of rivals and lead to development of

competitive advantage in business. As supported by Durand et al. (2017, p), the competitive

advantages in the organization is well managed and determined by the development in the

organizational process of decision making. The decision making is to be settle in terms of the

position of the organization. Better positioning and proper analysis of the competitors helps in

bringing out the competitive advantage of the organisation.

3.3.2 Appraising investments in the advanced technology

Investments in advanced technology are of prime importance as the growth in the organisation

depends upon the proper implementation of the technology. The investment in the advanced

technology helps in bringing in more production and results in hike revenue. The opportunity

also increases with the broadening of the area in technology field. Thus, strategic decision is to

select whether to investment in an advanced technology related to manufacturing. Investment

must be made in the project but strategic issues must also be identified like it is possible that

advanced technology related to manufacturing acquired by firm but it become obsolete in few

years before completion of life. In that situation biggest challenge is to ensure that asset will be

used more and more within certain time period. If it became obsolete in 3 to 4 years the

investment may go waste. There is rationale behind considering these factors because by doing

so better decision can be made in respect to investment. However, decision would be that

investment must be made in advanced technology that is in current time period. If it became

obsolete shortly then same can be sold to other firm in nation or in foreign country and from

proceeds amount new technology can be acquired. By doing so issue can be eliminated.

3.3.3 Using balanced scorecard for supporting achievement over vision and strategy

As supported by Mechler, (2016, p.2122), the opportunity provided by the usage of the scorecard

is mainly in gaining advantages over the strategies in the organization. The organisational

support is more effectively achieved with the better achievement of the vision and strategies. The

vision and the strategy are correlated to each other as there is strong relation between them in

bringing in the success of the organisation.

LO6

6.1 Appraising projects on capital investment utilising alternative methodologies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6.1.1 Distinction between profit and cash and the relevance to long term investment

proposals

Profit is the earning of an organization from the expenses and the saving of the organisation. The

profit of an organisation is generally of long terms benefits whereas the support of the cash is

current basis and is not much helpful in the organisation. The profit can be used in the

organisation in further future for the operation, but the cash is all in current basis.

Payback period

Payback period means following an approach under which duration after which project

will generate profit is identified. It is one of the important tool that is used for measuring

viability of project.

Benefits Main benefit of payback period method is that it reflect the duration in which investment

can be covered by the firm. Thus, loss making duration in respect to project is identified

by using payback period method.

Limitation Present value concept is not used in the payback period method for valuation of the

project.

Average rate of return

ARR indicate mean return that can be gained on the project if investment is made in

same. It can be said that it is the tool which reflect the overall performance of the project.

Merits Main merit of ARR method is that it reflect mean return that can be earned on project.

Means that overview of project returns is taken by using ARR method.

Demerits It does not reflect that after deducting investment value from cash flows what amount of

average return can be earned.

NPV

NPV reflect the residual value of the project which remain after considering investment

and cash flow value. It is another important method that is used in project evaluation.

Merits

proposals

Profit is the earning of an organization from the expenses and the saving of the organisation. The

profit of an organisation is generally of long terms benefits whereas the support of the cash is

current basis and is not much helpful in the organisation. The profit can be used in the

organisation in further future for the operation, but the cash is all in current basis.

Payback period

Payback period means following an approach under which duration after which project

will generate profit is identified. It is one of the important tool that is used for measuring

viability of project.

Benefits Main benefit of payback period method is that it reflect the duration in which investment

can be covered by the firm. Thus, loss making duration in respect to project is identified

by using payback period method.

Limitation Present value concept is not used in the payback period method for valuation of the

project.

Average rate of return

ARR indicate mean return that can be gained on the project if investment is made in

same. It can be said that it is the tool which reflect the overall performance of the project.

Merits Main merit of ARR method is that it reflect mean return that can be earned on project.

Means that overview of project returns is taken by using ARR method.

Demerits It does not reflect that after deducting investment value from cash flows what amount of

average return can be earned.

NPV

NPV reflect the residual value of the project which remain after considering investment

and cash flow value. It is another important method that is used in project evaluation.

Merits

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Present value concept is taken in to account for project valuation and to identify net value

of same.

Demerits

Calculation process is tough in case of NPV method due to this reason individual that

have non finance background cannot use this technique effectively.

6.1.2 Accounting rate of return, Payback and Net present value of an investment proposals

For analysis purpose entire data is taken from the reports that are available in respect to company.

Payback period

Table 1Calculation of payback period

Project

Initial

investment -800

1 210 -590

2 490 -100

3 686 586

4 882 1468

Average accounting income

Table 2Calculation of ARR

Project

Initial

investment 800

1 210

2 490

3 686

4 882

Total 2268

Average 567

ARR 70.88%

NPV

Table 3Calculation of NPV

Project

Pv @

10% Present value

Initial

investment 800

of same.

Demerits

Calculation process is tough in case of NPV method due to this reason individual that

have non finance background cannot use this technique effectively.

6.1.2 Accounting rate of return, Payback and Net present value of an investment proposals

For analysis purpose entire data is taken from the reports that are available in respect to company.

Payback period

Table 1Calculation of payback period

Project

Initial

investment -800

1 210 -590

2 490 -100

3 686 586

4 882 1468

Average accounting income

Table 2Calculation of ARR

Project

Initial

investment 800

1 210

2 490

3 686

4 882

Total 2268

Average 567

ARR 70.88%

NPV

Table 3Calculation of NPV

Project

Pv @

10% Present value

Initial

investment 800

1 210 0.909 191

2 490 0.826 405

3 686 0.751 515

4 882 0.683 602

Total 1714

NPV 914

6.1.3 Features and advantages of the alternative investment appraisal techniques

The advantages if the investment appraisal technique lies on the smooth understanding of the

investment values and the techniques. On the other hand the investment appraisal technique does

not value money in time. The valuation of time ion aspect of the money would result in the better

achievement of the appraisal techniques.

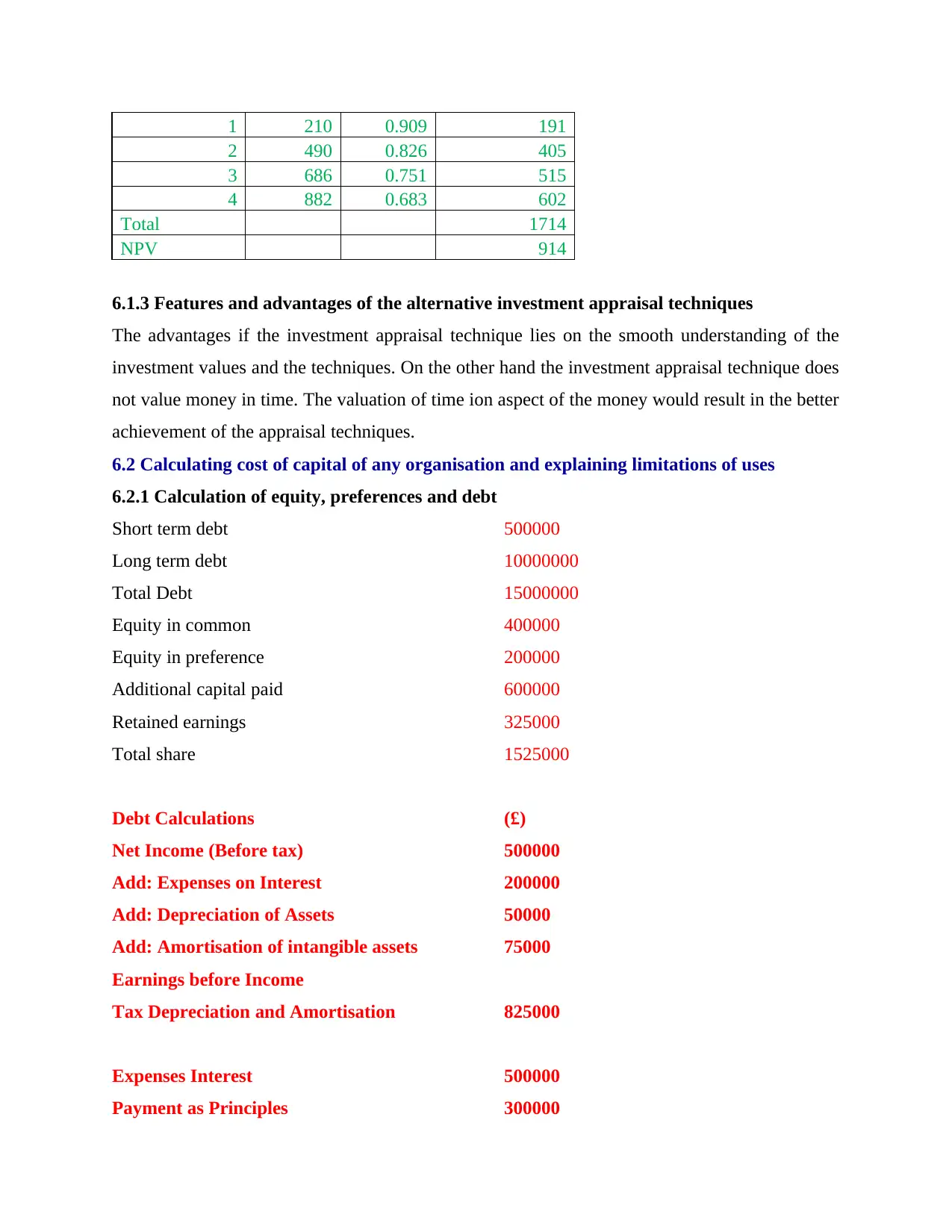

6.2 Calculating cost of capital of any organisation and explaining limitations of uses

6.2.1 Calculation of equity, preferences and debt

Short term debt 500000

Long term debt 10000000

Total Debt 15000000

Equity in common 400000

Equity in preference 200000

Additional capital paid 600000

Retained earnings 325000

Total share 1525000

Debt Calculations (£)

Net Income (Before tax) 500000

Add: Expenses on Interest 200000

Add: Depreciation of Assets 50000

Add: Amortisation of intangible assets 75000

Earnings before Income

Tax Depreciation and Amortisation 825000

Expenses Interest 500000

Payment as Principles 300000

2 490 0.826 405

3 686 0.751 515

4 882 0.683 602

Total 1714

NPV 914

6.1.3 Features and advantages of the alternative investment appraisal techniques

The advantages if the investment appraisal technique lies on the smooth understanding of the

investment values and the techniques. On the other hand the investment appraisal technique does

not value money in time. The valuation of time ion aspect of the money would result in the better

achievement of the appraisal techniques.

6.2 Calculating cost of capital of any organisation and explaining limitations of uses

6.2.1 Calculation of equity, preferences and debt

Short term debt 500000

Long term debt 10000000

Total Debt 15000000

Equity in common 400000

Equity in preference 200000

Additional capital paid 600000

Retained earnings 325000

Total share 1525000

Debt Calculations (£)

Net Income (Before tax) 500000

Add: Expenses on Interest 200000

Add: Depreciation of Assets 50000

Add: Amortisation of intangible assets 75000

Earnings before Income

Tax Depreciation and Amortisation 825000

Expenses Interest 500000

Payment as Principles 300000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.