Managerial Accounting: Evaluating Financial and Non-Financial Measures for Executive Remuneration

VerifiedAdded on 2023/06/07

|23

|4723

|88

AI Summary

The purpose of this study is to illustrate the variety of financial and non financial measures that promote remuneration pay of executives. It studies how the financial measures contribute to the overall remuneration plan as well as the non financial measures that has a part to play in impacting the incentive plan of executives. This report compares the remuneration policies of two companies that belong in the same industry and summarises the findings of the remuneration policies found on reviewing those two companies. The study aims to find out what means best promote employee performance and what financial and non financial measures have on the growth of overall organisational objectives.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGERAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Author Note

Managerial Accounting

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGERIAL ACCOUTING

Executive summary

The purpose of this study is to illustrate the variety of financial and non financial measures

that promote remuneration pay of executives. It studies how the financial measures

contribute to the overall remuneration plan as well as the non financial measures that has a

part to play in impacting the incentive plan of executives. This report compares the

remuneration policies of two companies that belong in the same industry and summarises the

findings of the remuneration policies found on reviewing those two companies. The study

aims to find out what means best promote employee performance and what financial and non

financial measures have on the growth of overall organisational objectives.

Executive summary

The purpose of this study is to illustrate the variety of financial and non financial measures

that promote remuneration pay of executives. It studies how the financial measures

contribute to the overall remuneration plan as well as the non financial measures that has a

part to play in impacting the incentive plan of executives. This report compares the

remuneration policies of two companies that belong in the same industry and summarises the

findings of the remuneration policies found on reviewing those two companies. The study

aims to find out what means best promote employee performance and what financial and non

financial measures have on the growth of overall organisational objectives.

2MANAGERIAL ACCOUTING

Table of Contents

Introduction................................................................................................................................3

Review of topic and of literature................................................................................................3

Company review........................................................................................................................6

Reliance worldwide....................................................................................................................6

Details for remuneration committee and its membership......................................................7

Allocation of executive remuneration....................................................................................7

Mix of performances used......................................................................................................8

ALS limited..............................................................................................................................12

Details of remuneration committee and its membership......................................................12

Allocation of executive remuneration.................................................................................12

Summary of findings................................................................................................................17

Analysis and comparison of remuneration methods used........................................................18

Conclusion................................................................................................................................19

References................................................................................................................................20

Table of Contents

Introduction................................................................................................................................3

Review of topic and of literature................................................................................................3

Company review........................................................................................................................6

Reliance worldwide....................................................................................................................6

Details for remuneration committee and its membership......................................................7

Allocation of executive remuneration....................................................................................7

Mix of performances used......................................................................................................8

ALS limited..............................................................................................................................12

Details of remuneration committee and its membership......................................................12

Allocation of executive remuneration.................................................................................12

Summary of findings................................................................................................................17

Analysis and comparison of remuneration methods used........................................................18

Conclusion................................................................................................................................19

References................................................................................................................................20

3MANAGERIAL ACCOUTING

Introduction

The ability of organisations to reward and evaluate the performance of executives in

the public sector is of the upmost importance. This is especially important if the performance

measurement systems can promote a positive implementation of the strategic goals and

objectives of a company. In his report we provide variety of methods that can be used to

evaluate the administrative performance in public sector undertakings(Kerzner,2017). These

methods allows the managers to concentrate on what is most vital to their company and

customers. This makes their performance assessments not only to the organisation’ objectives

but also but also gives the leaders an explicit linkage between performance attributes to the

individual and organisation objectives (Buchanan, 2016). We evaluate the various methods

of measuring executive performance and how their effectiveness we also give detail about

what these methods provide to aid in the evaluation process and examine in detail about the

implications of these systems on performance management. we take two companies and

compare their remuneration reports and based on that we analyse the performance of

executive employees(Van Dooren, Bouckaert and Halligan, 2015)

Review of topic and of literature

There has been a significant growth of performance based management system . This

has been rising both in terms of their norm and importance. Performance management is the

methodical way by which a company involves its employees in improving organisational

effectiveness (Mone and London, 2018). It can be applied to organisations, departments ,

processes ,programs or products to internal or executive customers in both private and public

sector organisations. This helps in pushing executives to measure and examine results.

Executive evaluation should be directed in such a way that it should help the organisation in

achieving the desired outcome (Arnaboldi, Lapsley and Steccolini, 2015).

Introduction

The ability of organisations to reward and evaluate the performance of executives in

the public sector is of the upmost importance. This is especially important if the performance

measurement systems can promote a positive implementation of the strategic goals and

objectives of a company. In his report we provide variety of methods that can be used to

evaluate the administrative performance in public sector undertakings(Kerzner,2017). These

methods allows the managers to concentrate on what is most vital to their company and

customers. This makes their performance assessments not only to the organisation’ objectives

but also but also gives the leaders an explicit linkage between performance attributes to the

individual and organisation objectives (Buchanan, 2016). We evaluate the various methods

of measuring executive performance and how their effectiveness we also give detail about

what these methods provide to aid in the evaluation process and examine in detail about the

implications of these systems on performance management. we take two companies and

compare their remuneration reports and based on that we analyse the performance of

executive employees(Van Dooren, Bouckaert and Halligan, 2015)

Review of topic and of literature

There has been a significant growth of performance based management system . This

has been rising both in terms of their norm and importance. Performance management is the

methodical way by which a company involves its employees in improving organisational

effectiveness (Mone and London, 2018). It can be applied to organisations, departments ,

processes ,programs or products to internal or executive customers in both private and public

sector organisations. This helps in pushing executives to measure and examine results.

Executive evaluation should be directed in such a way that it should help the organisation in

achieving the desired outcome (Arnaboldi, Lapsley and Steccolini, 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGERIAL ACCOUTING

Executive performance management needs to be effective in maintaining the

effectiveness of organisations. The system must have the backing or support of stakeholder

executives. Executives must understand its purpose and how it works. They must see how the

system and how it will benefit them personally (Kamierczyk, Kamierczyk and Aptacy,

2016). According to a study sponsored by the us department of veteran affairs, it revealed a

number of essentials for effective executive performance management that includes: 1)

strategic alignment 2) result based organisation culture 3) executive buy in 4) unambiguous

performance evaluations

A major finding from this study suggested that performance evaluations directly

relate to executives job levels and roles. Executives must have the ability to influence

outcomes that they will be assessed against. Only then they will be motivated enough to

pursue t recognition and rewards that come from achieving performance targets. In the

absence of a direct link between performance evaluating criteria and executive

responsibilities, performance measurement is reduced from a powerful behaviour change tool

to a potentially frustrating and demotivating administrative task.

Management by objectives(MBO) is a concept that makes all managers of a firm

participate in the strategic planning process. This is a process that improves execution of a

particular planning process. Further the MBO process requires the management to use a

range of performance measurement systems. This would help the organisation to achieve its

organisational goals. MBO principles have helped in creating a performance measurement

system for evaluating the performance of employees in public sector organisations. The

principles of MBO include cascading organisational goals and objectives and also defines

the specific roles of each member of an organisation. This includes in involving managers in

providing an evaluation and feedback on performance(Kamierczyk, Kamierczyk and Aptacy,

2016).

Executive performance management needs to be effective in maintaining the

effectiveness of organisations. The system must have the backing or support of stakeholder

executives. Executives must understand its purpose and how it works. They must see how the

system and how it will benefit them personally (Kamierczyk, Kamierczyk and Aptacy,

2016). According to a study sponsored by the us department of veteran affairs, it revealed a

number of essentials for effective executive performance management that includes: 1)

strategic alignment 2) result based organisation culture 3) executive buy in 4) unambiguous

performance evaluations

A major finding from this study suggested that performance evaluations directly

relate to executives job levels and roles. Executives must have the ability to influence

outcomes that they will be assessed against. Only then they will be motivated enough to

pursue t recognition and rewards that come from achieving performance targets. In the

absence of a direct link between performance evaluating criteria and executive

responsibilities, performance measurement is reduced from a powerful behaviour change tool

to a potentially frustrating and demotivating administrative task.

Management by objectives(MBO) is a concept that makes all managers of a firm

participate in the strategic planning process. This is a process that improves execution of a

particular planning process. Further the MBO process requires the management to use a

range of performance measurement systems. This would help the organisation to achieve its

organisational goals. MBO principles have helped in creating a performance measurement

system for evaluating the performance of employees in public sector organisations. The

principles of MBO include cascading organisational goals and objectives and also defines

the specific roles of each member of an organisation. This includes in involving managers in

providing an evaluation and feedback on performance(Kamierczyk, Kamierczyk and Aptacy,

2016).

5MANAGERIAL ACCOUTING

A balanced scorecard is also a method to evaluate effective executive performance.

Senior executives comprehend that the measurement system of the organisation affects the

behaviour of managers. Executives also comprehend that old-fashioned financial practices

like return on investment and earning per share give misguided signals for incessant

improvement and innovation. These are the type of activities that the competitive

environment demands (Akkermans and Van Oorschot, 2018). The traditional financial

measures might have worked well in , but they are out of their depth in the context of today’s

environment. Nowadays the managers chose to focus on operational measures as well as

financial measures. They believe that operational measures will automatically improve

financial measures. The balanced scorecard allows managers to view the business from four

important angles namely financial perspective, customer perspective , internal business

practice and innovation and learning practice. The balanced scorecard link performance

measures with that of four perspectives that raises important questions. These questions

relate to how do customers see the organisation( customer perspective), how do they look to

shareholders( financial perspective),what must the company excel at (internal practice) and

what the company can do to prove and crate value(innovation and learning perspective).this

helps in minimising information overload by limiting the number of measures used. It makes

the manager in focusing on the handful of measures that are the most critical (Hansen and

Schaltegger, 2016).

There is also another approach called a results based leadership. It focuses on

attributes and results. Leaders must strive for excellence not only in terms of results and

objectives , but by demonstrating attributes of success. This approach offers four criteria for

judging whether managers are focused on achieving results. Those four criteria includes the

executives balance concerns of employees, the results linking strongly to the strategy of the

firm’s strategy and competitive position , whether results meet both short term and long term

A balanced scorecard is also a method to evaluate effective executive performance.

Senior executives comprehend that the measurement system of the organisation affects the

behaviour of managers. Executives also comprehend that old-fashioned financial practices

like return on investment and earning per share give misguided signals for incessant

improvement and innovation. These are the type of activities that the competitive

environment demands (Akkermans and Van Oorschot, 2018). The traditional financial

measures might have worked well in , but they are out of their depth in the context of today’s

environment. Nowadays the managers chose to focus on operational measures as well as

financial measures. They believe that operational measures will automatically improve

financial measures. The balanced scorecard allows managers to view the business from four

important angles namely financial perspective, customer perspective , internal business

practice and innovation and learning practice. The balanced scorecard link performance

measures with that of four perspectives that raises important questions. These questions

relate to how do customers see the organisation( customer perspective), how do they look to

shareholders( financial perspective),what must the company excel at (internal practice) and

what the company can do to prove and crate value(innovation and learning perspective).this

helps in minimising information overload by limiting the number of measures used. It makes

the manager in focusing on the handful of measures that are the most critical (Hansen and

Schaltegger, 2016).

There is also another approach called a results based leadership. It focuses on

attributes and results. Leaders must strive for excellence not only in terms of results and

objectives , but by demonstrating attributes of success. This approach offers four criteria for

judging whether managers are focused on achieving results. Those four criteria includes the

executives balance concerns of employees, the results linking strongly to the strategy of the

firm’s strategy and competitive position , whether results meet both short term and long term

6MANAGERIAL ACCOUTING

goals and finally whether results support the whole enterprise and transcend the personal

gain of managers. This approach moves management away from thinking about inputs of

leaders and instead focuses the management to take steps about the outcomes of their

leadership. It thus provides an effective framework that measures the effectiveness of the

leader(Donate and de Pablo, 2015).

Company review

This section deals with comparing the remuneration practices of two companies in

Australia belonging to the same industry. The first company that is already included in the

assignment, is Reliance Worldwide. Reliance worldwide belongs to the industrial sector and

is the world’s largest manufacturer of plumbing fittings. It also specialises in the

manufacture of specialist water control valves. Another company that has been chosen for

this comparison purpose is ALS limited. It is a global leader in providing laboratory testing,

inspection, certification and verification solutions. It provides high quality , innovative and

professional testing services to clients .it also belongs to the industrial sector.

Reliance worldwide

The first part of this remuneration analysis illustrates the remuneration policy of reliance

worldwide.

Details for remuneration committee and its membership.

The procedure for selecting directors for appointment purposes is ovesseen by the

nomination and remuneration committee. It also does the performance evaluation of

individual directors(Rwc.com, 2018). This committee is headed by an independent director.

Other members include two non executive directors (Tan and Liu, 2016.) .The nomination

goals and finally whether results support the whole enterprise and transcend the personal

gain of managers. This approach moves management away from thinking about inputs of

leaders and instead focuses the management to take steps about the outcomes of their

leadership. It thus provides an effective framework that measures the effectiveness of the

leader(Donate and de Pablo, 2015).

Company review

This section deals with comparing the remuneration practices of two companies in

Australia belonging to the same industry. The first company that is already included in the

assignment, is Reliance Worldwide. Reliance worldwide belongs to the industrial sector and

is the world’s largest manufacturer of plumbing fittings. It also specialises in the

manufacture of specialist water control valves. Another company that has been chosen for

this comparison purpose is ALS limited. It is a global leader in providing laboratory testing,

inspection, certification and verification solutions. It provides high quality , innovative and

professional testing services to clients .it also belongs to the industrial sector.

Reliance worldwide

The first part of this remuneration analysis illustrates the remuneration policy of reliance

worldwide.

Details for remuneration committee and its membership.

The procedure for selecting directors for appointment purposes is ovesseen by the

nomination and remuneration committee. It also does the performance evaluation of

individual directors(Rwc.com, 2018). This committee is headed by an independent director.

Other members include two non executive directors (Tan and Liu, 2016.) .The nomination

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUTING

and remuneration committee consists of members that are Jonathan Munz, Ross Dobinson

and Stuart Crosby.

Some of its responsibilities include mentioning to the Board about the remuneration

arrangements to the CEO. It also includes reviewing and facilitating shareholder and other

stakeholder engagement

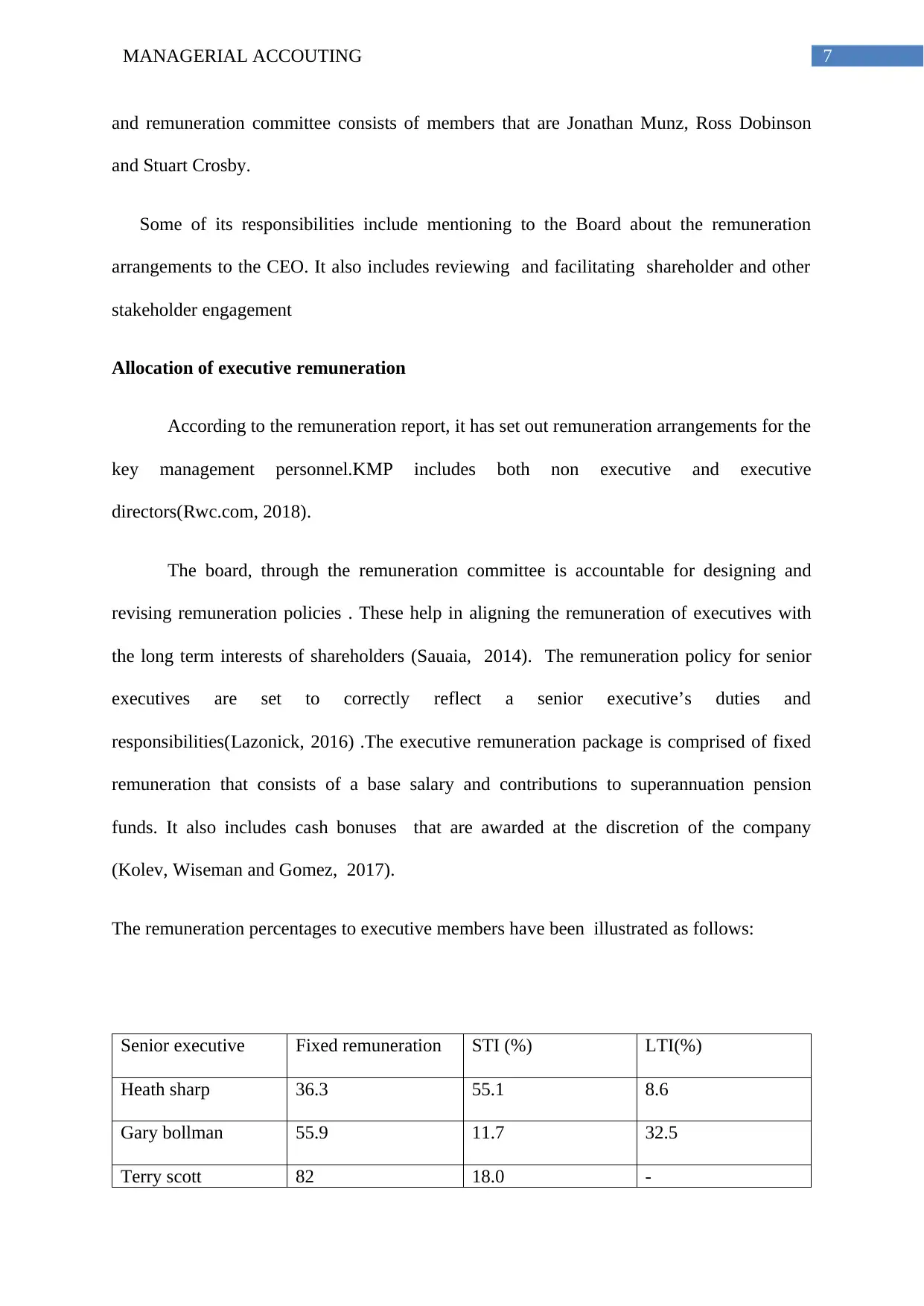

Allocation of executive remuneration

According to the remuneration report, it has set out remuneration arrangements for the

key management personnel.KMP includes both non executive and executive

directors(Rwc.com, 2018).

The board, through the remuneration committee is accountable for designing and

revising remuneration policies . These help in aligning the remuneration of executives with

the long term interests of shareholders (Sauaia, 2014). The remuneration policy for senior

executives are set to correctly reflect a senior executive’s duties and

responsibilities(Lazonick, 2016) .The executive remuneration package is comprised of fixed

remuneration that consists of a base salary and contributions to superannuation pension

funds. It also includes cash bonuses that are awarded at the discretion of the company

(Kolev, Wiseman and Gomez, 2017).

The remuneration percentages to executive members have been illustrated as follows:

Senior executive Fixed remuneration STI (%) LTI(%)

Heath sharp 36.3 55.1 8.6

Gary bollman 55.9 11.7 32.5

Terry scott 82 18.0 -

and remuneration committee consists of members that are Jonathan Munz, Ross Dobinson

and Stuart Crosby.

Some of its responsibilities include mentioning to the Board about the remuneration

arrangements to the CEO. It also includes reviewing and facilitating shareholder and other

stakeholder engagement

Allocation of executive remuneration

According to the remuneration report, it has set out remuneration arrangements for the

key management personnel.KMP includes both non executive and executive

directors(Rwc.com, 2018).

The board, through the remuneration committee is accountable for designing and

revising remuneration policies . These help in aligning the remuneration of executives with

the long term interests of shareholders (Sauaia, 2014). The remuneration policy for senior

executives are set to correctly reflect a senior executive’s duties and

responsibilities(Lazonick, 2016) .The executive remuneration package is comprised of fixed

remuneration that consists of a base salary and contributions to superannuation pension

funds. It also includes cash bonuses that are awarded at the discretion of the company

(Kolev, Wiseman and Gomez, 2017).

The remuneration percentages to executive members have been illustrated as follows:

Senior executive Fixed remuneration STI (%) LTI(%)

Heath sharp 36.3 55.1 8.6

Gary bollman 55.9 11.7 32.5

Terry scott 82 18.0 -

8MANAGERIAL ACCOUTING

Figure 1- remuneration percentages

Source- (Rwc.com, 2018)

Mix of performances used

The remuneration structure of reliance worldwide were as follows:

Fixed remuneration- according to this the terms of this remuneration structure containthr

following;

A fixed annual remuneration component encompassing a base salary and appropriate

superannuation funds

Other accepted benefits include items such as free transport, vehicles, mobile phone

etc

Senior executives have obtained a competitive fixed remuneration. This is in accordance

with the terms as set in the senior executive’s remuneration service agreement(Cecchetti and

Kharroubi,2015).some key performance indiactors that impact remuneration pay of

executives include:

Figure 2- key performance indicators

Figure 1- remuneration percentages

Source- (Rwc.com, 2018)

Mix of performances used

The remuneration structure of reliance worldwide were as follows:

Fixed remuneration- according to this the terms of this remuneration structure containthr

following;

A fixed annual remuneration component encompassing a base salary and appropriate

superannuation funds

Other accepted benefits include items such as free transport, vehicles, mobile phone

etc

Senior executives have obtained a competitive fixed remuneration. This is in accordance

with the terms as set in the senior executive’s remuneration service agreement(Cecchetti and

Kharroubi,2015).some key performance indiactors that impact remuneration pay of

executives include:

Figure 2- key performance indicators

9MANAGERIAL ACCOUTING

Source- (Rwc.com, 2018)

The company’s share price increased of 8.1 % during financial year 2017 . the public

offering had an issue price of $2.50 per share so that the closing price of 30th june 2017

represented a 33.6 percent premium to that issue price. Senior executives were rewarded I

recognition of this strong performance and delivering quality returns to shareholders.

Short term incentive

Under the company’s bonus plan, bonus are awarded to senior executive at the option

of the board . The overall performance of the group needs to be considered in determining

whether a cash bonus will be awarded in deliberation to attainment of key performance

objectives(Rwc.com, 2018).

The STI bonuses is awarded to the senior executives. It recognise their performance

in leading the company during its successful first full year since listing in the ASX. . the

company also experienced positive financial results in the financial year 2017 , as evidenced

by the positive shareholder returns. (Bussin and Modau, 2015).

Long term incentive

The company established the Equity incentive Plan . This plan was established to

assist the motivation, retention and reward of eligible employees. The plan is designed to

align the interests of employees with the interests of shareholders . This can be done by

providing an opportunity for eligible employees. This helps in receiving an equity interest in

the company(Ghazvini et al.,2015). There were an award that included being provided to the

Source- (Rwc.com, 2018)

The company’s share price increased of 8.1 % during financial year 2017 . the public

offering had an issue price of $2.50 per share so that the closing price of 30th june 2017

represented a 33.6 percent premium to that issue price. Senior executives were rewarded I

recognition of this strong performance and delivering quality returns to shareholders.

Short term incentive

Under the company’s bonus plan, bonus are awarded to senior executive at the option

of the board . The overall performance of the group needs to be considered in determining

whether a cash bonus will be awarded in deliberation to attainment of key performance

objectives(Rwc.com, 2018).

The STI bonuses is awarded to the senior executives. It recognise their performance

in leading the company during its successful first full year since listing in the ASX. . the

company also experienced positive financial results in the financial year 2017 , as evidenced

by the positive shareholder returns. (Bussin and Modau, 2015).

Long term incentive

The company established the Equity incentive Plan . This plan was established to

assist the motivation, retention and reward of eligible employees. The plan is designed to

align the interests of employees with the interests of shareholders . This can be done by

providing an opportunity for eligible employees. This helps in receiving an equity interest in

the company(Ghazvini et al.,2015). There were an award that included being provided to the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGERIAL ACCOUTING

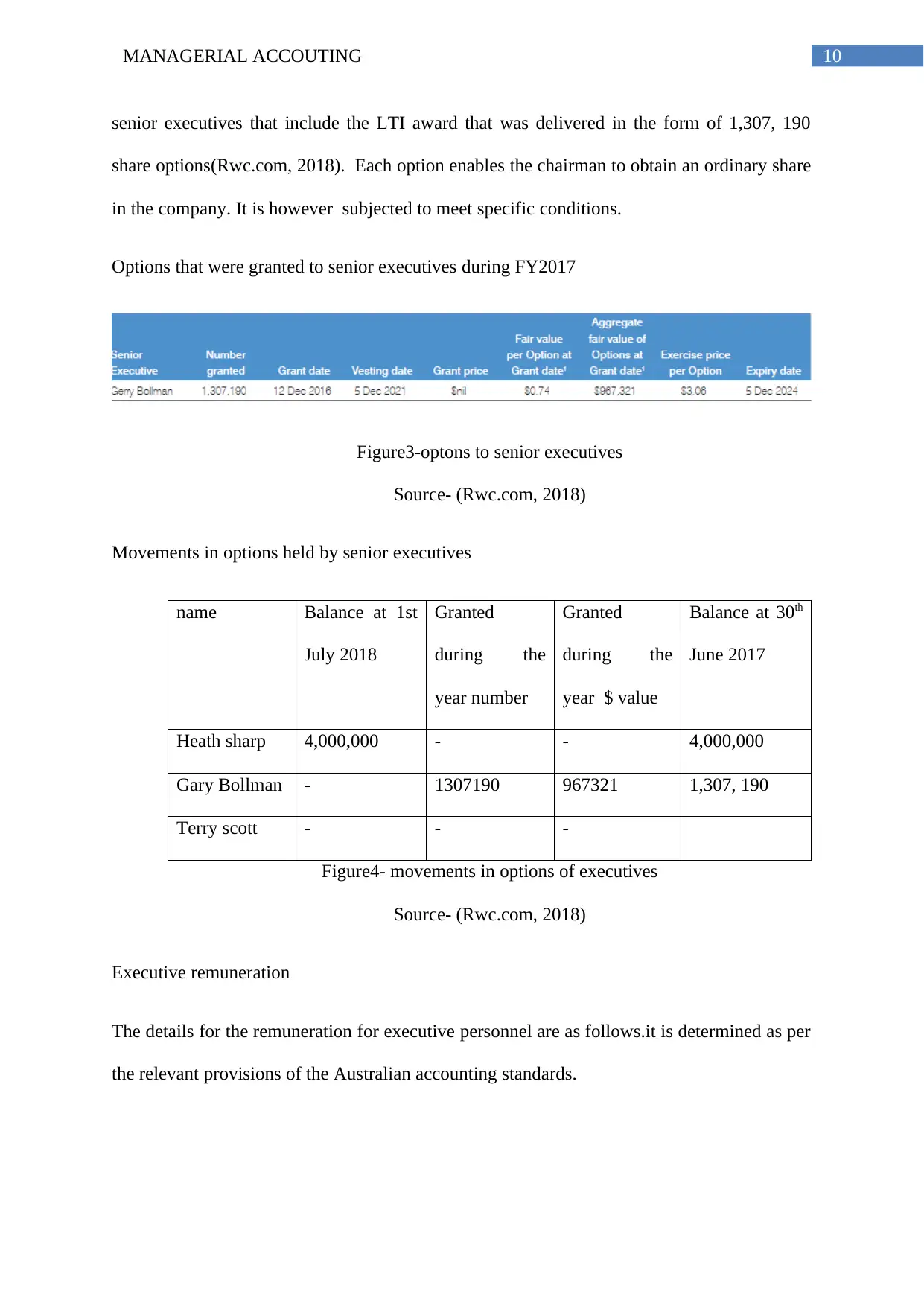

senior executives that include the LTI award that was delivered in the form of 1,307, 190

share options(Rwc.com, 2018). Each option enables the chairman to obtain an ordinary share

in the company. It is however subjected to meet specific conditions.

Options that were granted to senior executives during FY2017

Figure3-optons to senior executives

Source- (Rwc.com, 2018)

Movements in options held by senior executives

name Balance at 1st

July 2018

Granted

during the

year number

Granted

during the

year $ value

Balance at 30th

June 2017

Heath sharp 4,000,000 - - 4,000,000

Gary Bollman - 1307190 967321 1,307, 190

Terry scott - - -

Figure4- movements in options of executives

Source- (Rwc.com, 2018)

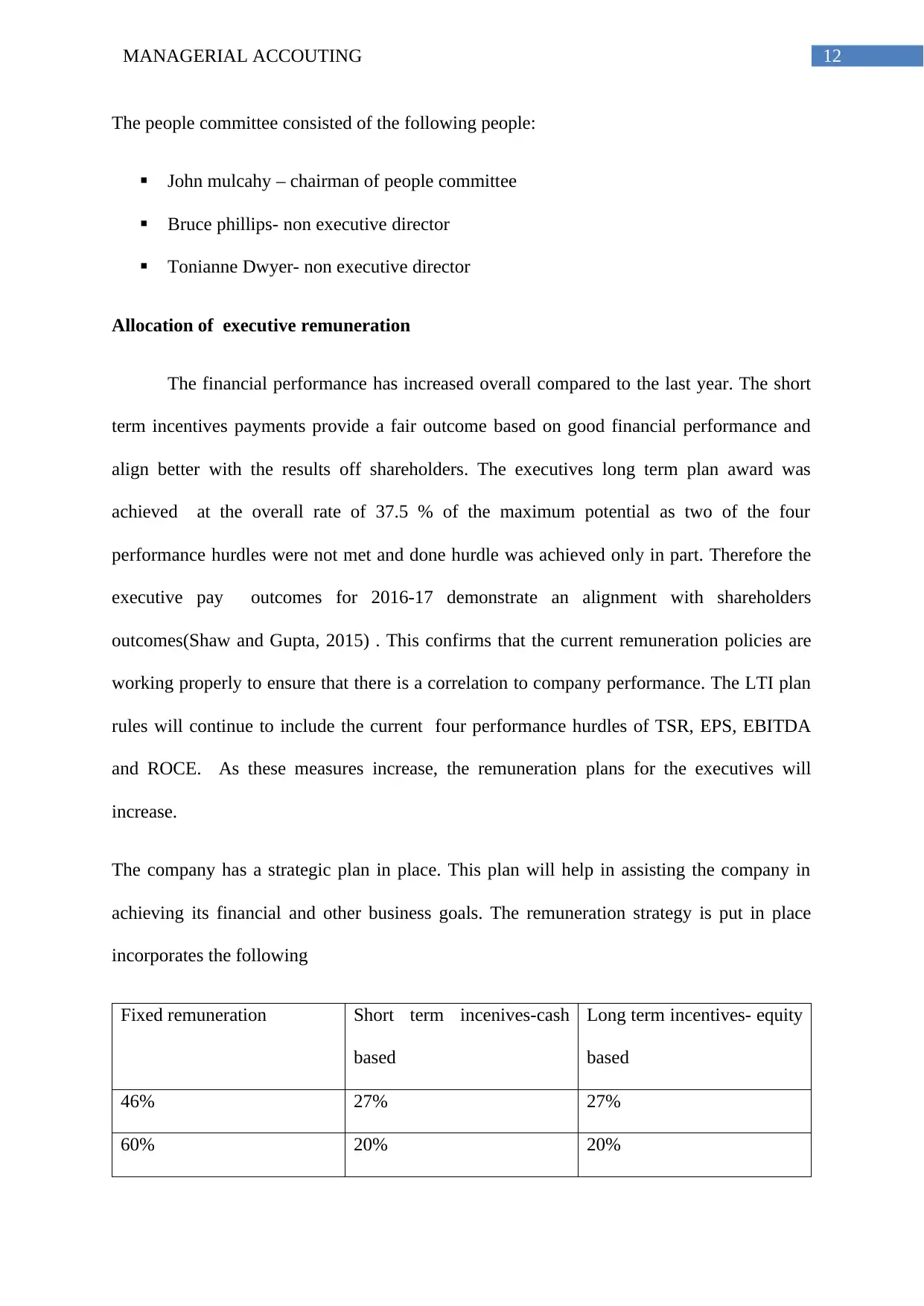

Executive remuneration

The details for the remuneration for executive personnel are as follows.it is determined as per

the relevant provisions of the Australian accounting standards.

senior executives that include the LTI award that was delivered in the form of 1,307, 190

share options(Rwc.com, 2018). Each option enables the chairman to obtain an ordinary share

in the company. It is however subjected to meet specific conditions.

Options that were granted to senior executives during FY2017

Figure3-optons to senior executives

Source- (Rwc.com, 2018)

Movements in options held by senior executives

name Balance at 1st

July 2018

Granted

during the

year number

Granted

during the

year $ value

Balance at 30th

June 2017

Heath sharp 4,000,000 - - 4,000,000

Gary Bollman - 1307190 967321 1,307, 190

Terry scott - - -

Figure4- movements in options of executives

Source- (Rwc.com, 2018)

Executive remuneration

The details for the remuneration for executive personnel are as follows.it is determined as per

the relevant provisions of the Australian accounting standards.

11MANAGERIAL ACCOUTING

Figure 5-remuneration details

Source- (Rwc.com, 2018)

ALS limited

The next part of this remuneration policy deals with the company ALS limited.

Details of remuneration committee and its membership

A new committee, now called the people committee , formerly known as the

remuneration committee was established by the board to create a wider scope for the existing

remuneration committee. The committee consist of the three independent non executive

directors. The committee considers to consider all aspects of remuneration strategy , policy

and process for executive key management personnel. It also has an oversight of the key

remuneration programs for the company globally(Alsglobal.com,2018).

Figure 5-remuneration details

Source- (Rwc.com, 2018)

ALS limited

The next part of this remuneration policy deals with the company ALS limited.

Details of remuneration committee and its membership

A new committee, now called the people committee , formerly known as the

remuneration committee was established by the board to create a wider scope for the existing

remuneration committee. The committee consist of the three independent non executive

directors. The committee considers to consider all aspects of remuneration strategy , policy

and process for executive key management personnel. It also has an oversight of the key

remuneration programs for the company globally(Alsglobal.com,2018).

12MANAGERIAL ACCOUTING

The people committee consisted of the following people:

John mulcahy – chairman of people committee

Bruce phillips- non executive director

Tonianne Dwyer- non executive director

Allocation of executive remuneration

The financial performance has increased overall compared to the last year. The short

term incentives payments provide a fair outcome based on good financial performance and

align better with the results off shareholders. The executives long term plan award was

achieved at the overall rate of 37.5 % of the maximum potential as two of the four

performance hurdles were not met and done hurdle was achieved only in part. Therefore the

executive pay outcomes for 2016-17 demonstrate an alignment with shareholders

outcomes(Shaw and Gupta, 2015) . This confirms that the current remuneration policies are

working properly to ensure that there is a correlation to company performance. The LTI plan

rules will continue to include the current four performance hurdles of TSR, EPS, EBITDA

and ROCE. As these measures increase, the remuneration plans for the executives will

increase.

The company has a strategic plan in place. This plan will help in assisting the company in

achieving its financial and other business goals. The remuneration strategy is put in place

incorporates the following

Fixed remuneration Short term incenives-cash

based

Long term incentives- equity

based

46% 27% 27%

60% 20% 20%

The people committee consisted of the following people:

John mulcahy – chairman of people committee

Bruce phillips- non executive director

Tonianne Dwyer- non executive director

Allocation of executive remuneration

The financial performance has increased overall compared to the last year. The short

term incentives payments provide a fair outcome based on good financial performance and

align better with the results off shareholders. The executives long term plan award was

achieved at the overall rate of 37.5 % of the maximum potential as two of the four

performance hurdles were not met and done hurdle was achieved only in part. Therefore the

executive pay outcomes for 2016-17 demonstrate an alignment with shareholders

outcomes(Shaw and Gupta, 2015) . This confirms that the current remuneration policies are

working properly to ensure that there is a correlation to company performance. The LTI plan

rules will continue to include the current four performance hurdles of TSR, EPS, EBITDA

and ROCE. As these measures increase, the remuneration plans for the executives will

increase.

The company has a strategic plan in place. This plan will help in assisting the company in

achieving its financial and other business goals. The remuneration strategy is put in place

incorporates the following

Fixed remuneration Short term incenives-cash

based

Long term incentives- equity

based

46% 27% 27%

60% 20% 20%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MANAGERIAL ACCOUTING

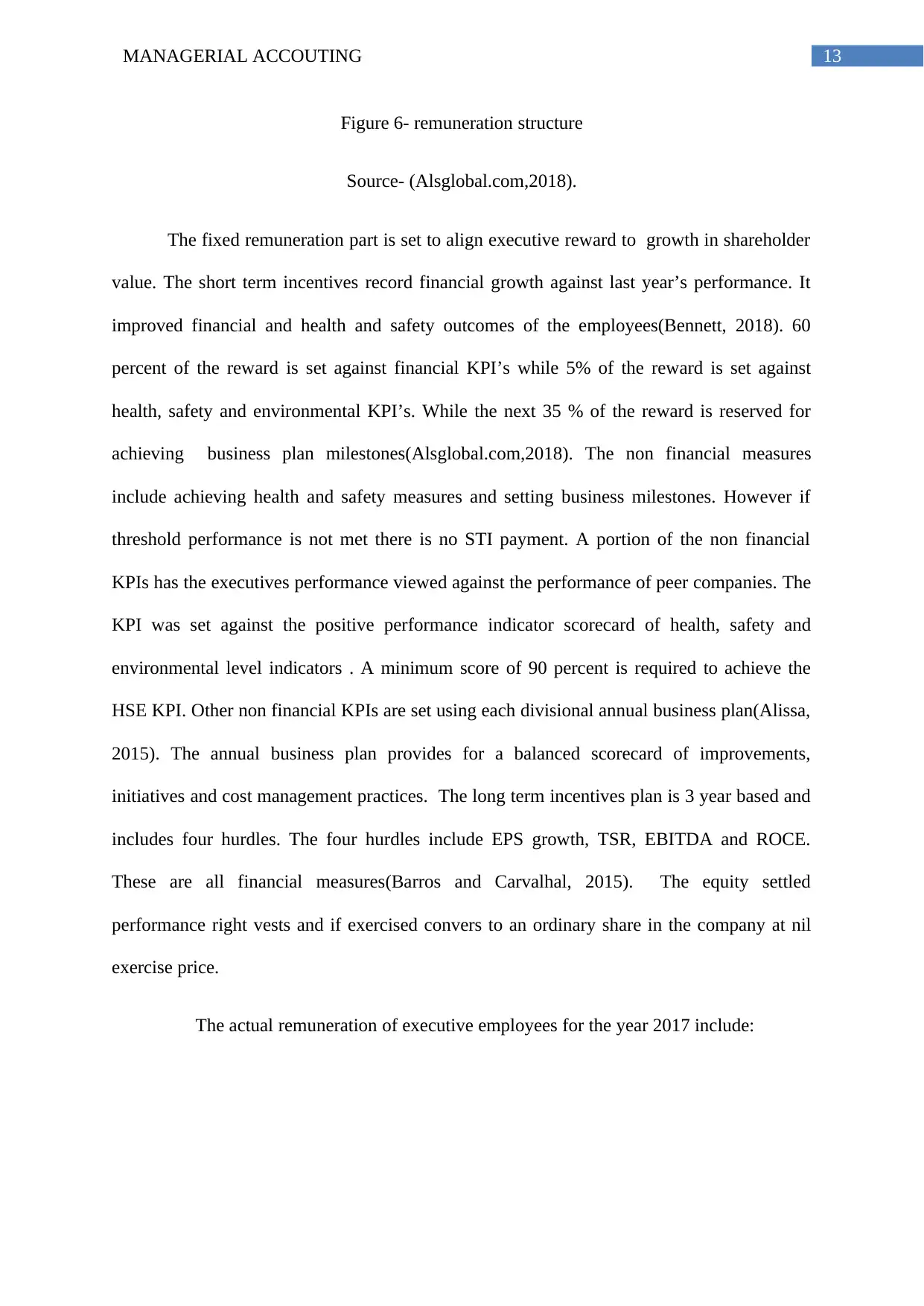

Figure 6- remuneration structure

Source- (Alsglobal.com,2018).

The fixed remuneration part is set to align executive reward to growth in shareholder

value. The short term incentives record financial growth against last year’s performance. It

improved financial and health and safety outcomes of the employees(Bennett, 2018). 60

percent of the reward is set against financial KPI’s while 5% of the reward is set against

health, safety and environmental KPI’s. While the next 35 % of the reward is reserved for

achieving business plan milestones(Alsglobal.com,2018). The non financial measures

include achieving health and safety measures and setting business milestones. However if

threshold performance is not met there is no STI payment. A portion of the non financial

KPIs has the executives performance viewed against the performance of peer companies. The

KPI was set against the positive performance indicator scorecard of health, safety and

environmental level indicators . A minimum score of 90 percent is required to achieve the

HSE KPI. Other non financial KPIs are set using each divisional annual business plan(Alissa,

2015). The annual business plan provides for a balanced scorecard of improvements,

initiatives and cost management practices. The long term incentives plan is 3 year based and

includes four hurdles. The four hurdles include EPS growth, TSR, EBITDA and ROCE.

These are all financial measures(Barros and Carvalhal, 2015). The equity settled

performance right vests and if exercised convers to an ordinary share in the company at nil

exercise price.

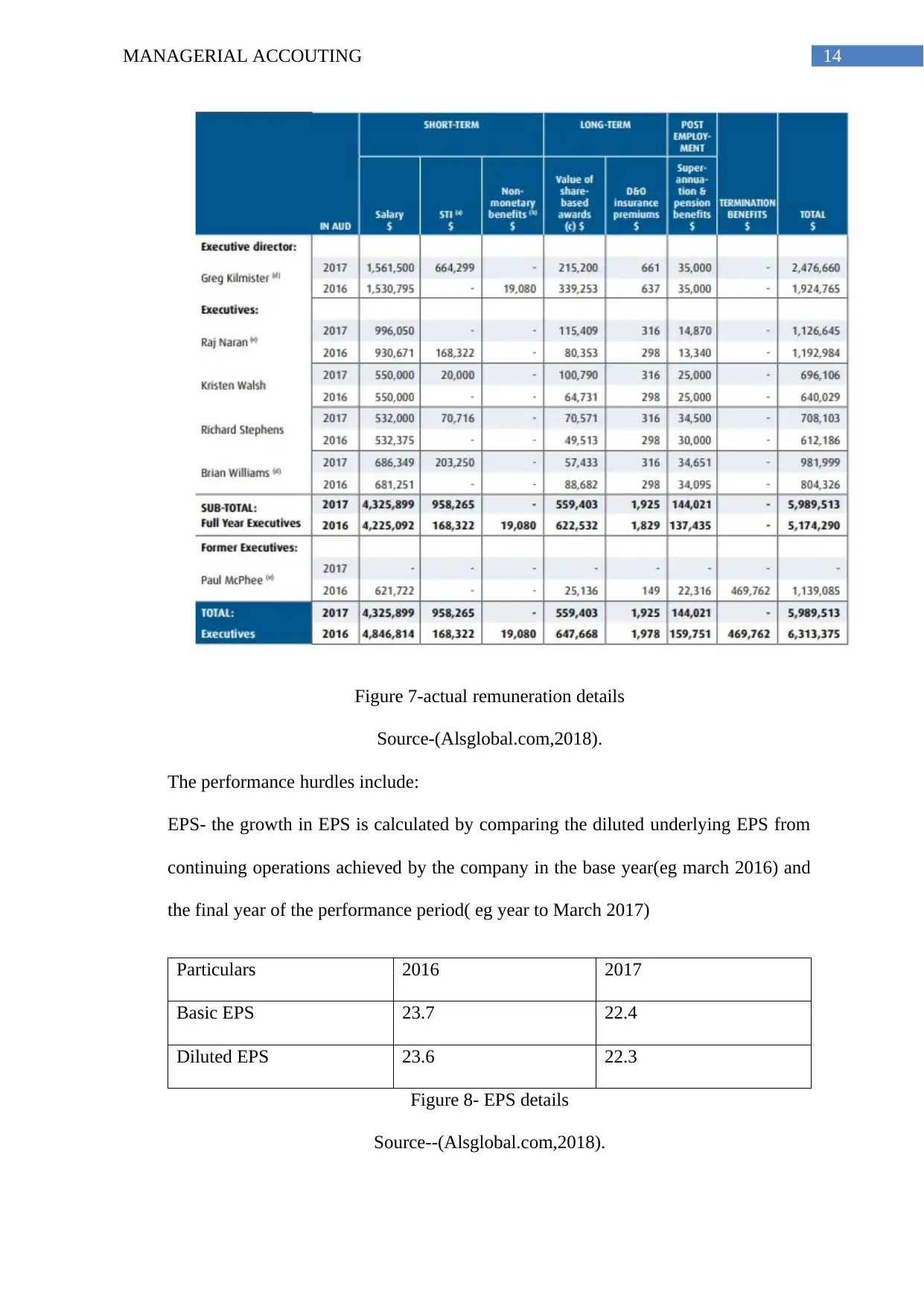

The actual remuneration of executive employees for the year 2017 include:

Figure 6- remuneration structure

Source- (Alsglobal.com,2018).

The fixed remuneration part is set to align executive reward to growth in shareholder

value. The short term incentives record financial growth against last year’s performance. It

improved financial and health and safety outcomes of the employees(Bennett, 2018). 60

percent of the reward is set against financial KPI’s while 5% of the reward is set against

health, safety and environmental KPI’s. While the next 35 % of the reward is reserved for

achieving business plan milestones(Alsglobal.com,2018). The non financial measures

include achieving health and safety measures and setting business milestones. However if

threshold performance is not met there is no STI payment. A portion of the non financial

KPIs has the executives performance viewed against the performance of peer companies. The

KPI was set against the positive performance indicator scorecard of health, safety and

environmental level indicators . A minimum score of 90 percent is required to achieve the

HSE KPI. Other non financial KPIs are set using each divisional annual business plan(Alissa,

2015). The annual business plan provides for a balanced scorecard of improvements,

initiatives and cost management practices. The long term incentives plan is 3 year based and

includes four hurdles. The four hurdles include EPS growth, TSR, EBITDA and ROCE.

These are all financial measures(Barros and Carvalhal, 2015). The equity settled

performance right vests and if exercised convers to an ordinary share in the company at nil

exercise price.

The actual remuneration of executive employees for the year 2017 include:

14MANAGERIAL ACCOUTING

Figure 7-actual remuneration details

Source-(Alsglobal.com,2018).

The performance hurdles include:

EPS- the growth in EPS is calculated by comparing the diluted underlying EPS from

continuing operations achieved by the company in the base year(eg march 2016) and

the final year of the performance period( eg year to March 2017)

Particulars 2016 2017

Basic EPS 23.7 22.4

Diluted EPS 23.6 22.3

Figure 8- EPS details

Source--(Alsglobal.com,2018).

Figure 7-actual remuneration details

Source-(Alsglobal.com,2018).

The performance hurdles include:

EPS- the growth in EPS is calculated by comparing the diluted underlying EPS from

continuing operations achieved by the company in the base year(eg march 2016) and

the final year of the performance period( eg year to March 2017)

Particulars 2016 2017

Basic EPS 23.7 22.4

Diluted EPS 23.6 22.3

Figure 8- EPS details

Source--(Alsglobal.com,2018).

15MANAGERIAL ACCOUTING

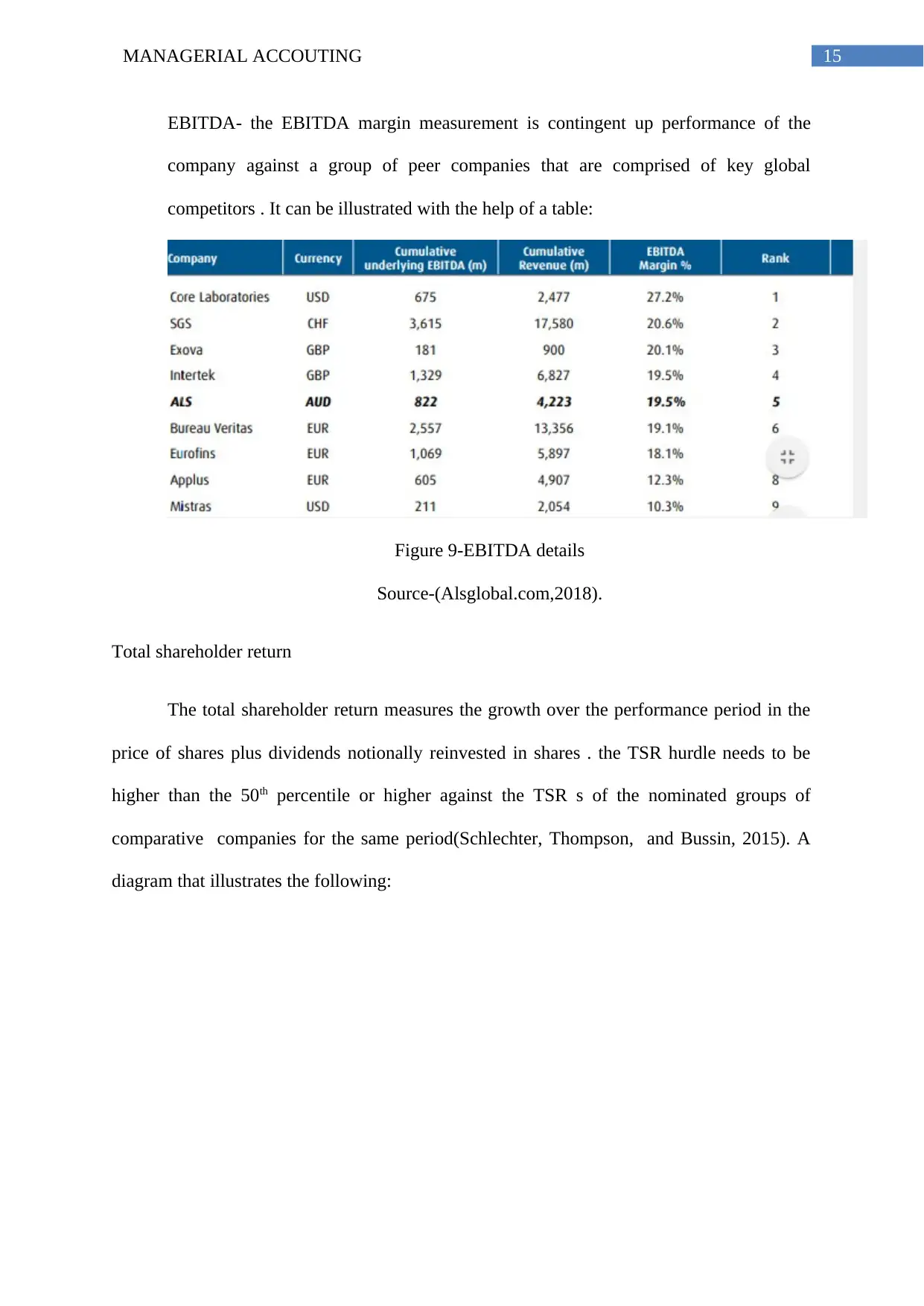

EBITDA- the EBITDA margin measurement is contingent up performance of the

company against a group of peer companies that are comprised of key global

competitors . It can be illustrated with the help of a table:

Figure 9-EBITDA details

Source-(Alsglobal.com,2018).

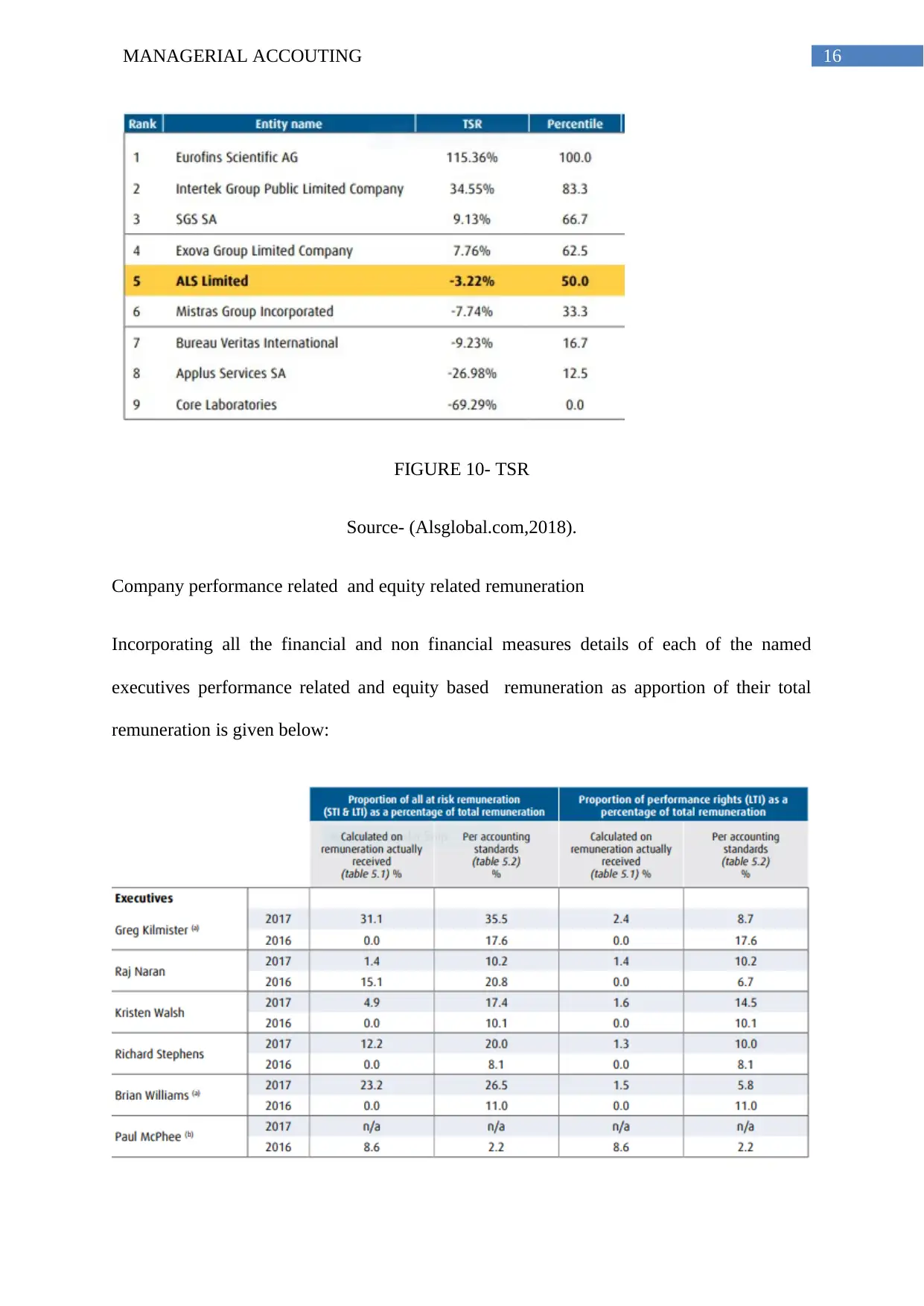

Total shareholder return

The total shareholder return measures the growth over the performance period in the

price of shares plus dividends notionally reinvested in shares . the TSR hurdle needs to be

higher than the 50th percentile or higher against the TSR s of the nominated groups of

comparative companies for the same period(Schlechter, Thompson, and Bussin, 2015). A

diagram that illustrates the following:

EBITDA- the EBITDA margin measurement is contingent up performance of the

company against a group of peer companies that are comprised of key global

competitors . It can be illustrated with the help of a table:

Figure 9-EBITDA details

Source-(Alsglobal.com,2018).

Total shareholder return

The total shareholder return measures the growth over the performance period in the

price of shares plus dividends notionally reinvested in shares . the TSR hurdle needs to be

higher than the 50th percentile or higher against the TSR s of the nominated groups of

comparative companies for the same period(Schlechter, Thompson, and Bussin, 2015). A

diagram that illustrates the following:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MANAGERIAL ACCOUTING

FIGURE 10- TSR

Source- (Alsglobal.com,2018).

Company performance related and equity related remuneration

Incorporating all the financial and non financial measures details of each of the named

executives performance related and equity based remuneration as apportion of their total

remuneration is given below:

FIGURE 10- TSR

Source- (Alsglobal.com,2018).

Company performance related and equity related remuneration

Incorporating all the financial and non financial measures details of each of the named

executives performance related and equity based remuneration as apportion of their total

remuneration is given below:

17MANAGERIAL ACCOUTING

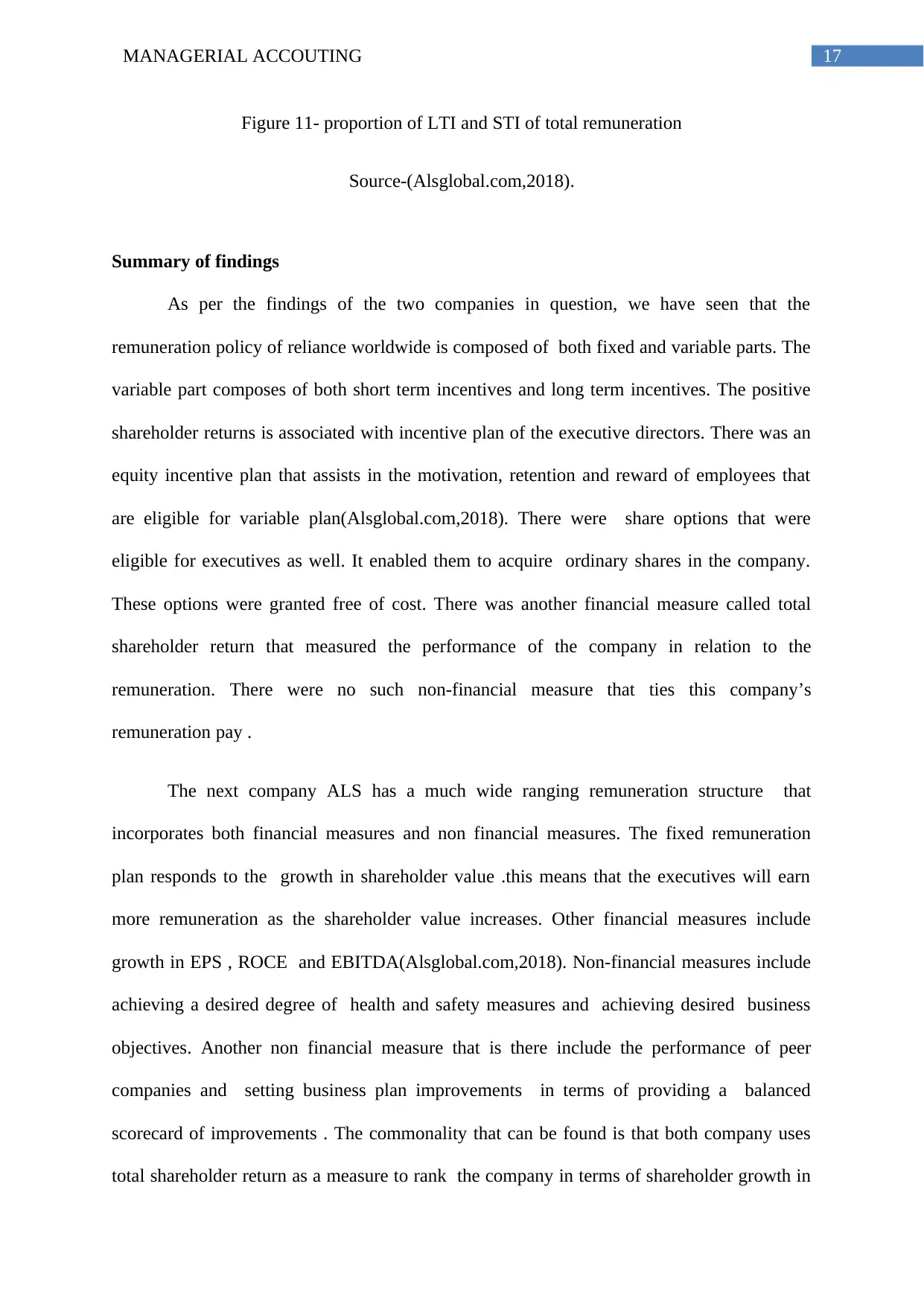

Figure 11- proportion of LTI and STI of total remuneration

Source-(Alsglobal.com,2018).

Summary of findings

As per the findings of the two companies in question, we have seen that the

remuneration policy of reliance worldwide is composed of both fixed and variable parts. The

variable part composes of both short term incentives and long term incentives. The positive

shareholder returns is associated with incentive plan of the executive directors. There was an

equity incentive plan that assists in the motivation, retention and reward of employees that

are eligible for variable plan(Alsglobal.com,2018). There were share options that were

eligible for executives as well. It enabled them to acquire ordinary shares in the company.

These options were granted free of cost. There was another financial measure called total

shareholder return that measured the performance of the company in relation to the

remuneration. There were no such non-financial measure that ties this company’s

remuneration pay .

The next company ALS has a much wide ranging remuneration structure that

incorporates both financial measures and non financial measures. The fixed remuneration

plan responds to the growth in shareholder value .this means that the executives will earn

more remuneration as the shareholder value increases. Other financial measures include

growth in EPS , ROCE and EBITDA(Alsglobal.com,2018). Non-financial measures include

achieving a desired degree of health and safety measures and achieving desired business

objectives. Another non financial measure that is there include the performance of peer

companies and setting business plan improvements in terms of providing a balanced

scorecard of improvements . The commonality that can be found is that both company uses

total shareholder return as a measure to rank the company in terms of shareholder growth in

Figure 11- proportion of LTI and STI of total remuneration

Source-(Alsglobal.com,2018).

Summary of findings

As per the findings of the two companies in question, we have seen that the

remuneration policy of reliance worldwide is composed of both fixed and variable parts. The

variable part composes of both short term incentives and long term incentives. The positive

shareholder returns is associated with incentive plan of the executive directors. There was an

equity incentive plan that assists in the motivation, retention and reward of employees that

are eligible for variable plan(Alsglobal.com,2018). There were share options that were

eligible for executives as well. It enabled them to acquire ordinary shares in the company.

These options were granted free of cost. There was another financial measure called total

shareholder return that measured the performance of the company in relation to the

remuneration. There were no such non-financial measure that ties this company’s

remuneration pay .

The next company ALS has a much wide ranging remuneration structure that

incorporates both financial measures and non financial measures. The fixed remuneration

plan responds to the growth in shareholder value .this means that the executives will earn

more remuneration as the shareholder value increases. Other financial measures include

growth in EPS , ROCE and EBITDA(Alsglobal.com,2018). Non-financial measures include

achieving a desired degree of health and safety measures and achieving desired business

objectives. Another non financial measure that is there include the performance of peer

companies and setting business plan improvements in terms of providing a balanced

scorecard of improvements . The commonality that can be found is that both company uses

total shareholder return as a measure to rank the company in terms of shareholder growth in

18MANAGERIAL ACCOUTING

other peer reviewed company. Both companies also provides share options to companies at

nil exercise price.

Analysis and comparison of remuneration methods used

In terms of the remuneration policy of the company reliance worldwide, both

companies followed a short term and long term incentive structure that measured employees

pay based on financial and non financial measures of the executive employees. The principla

goal behind these incentive plans is to focus the executives on long term outcomes, ensuring

the retention of top employees and encouraging teamwork and motivation through company

performance hurdles(Barros and Carvalhal, 2015). In the case of ALS global, the NPAT

target was fully met as were all the non financial KPI’s. The second NPAT hurdle was

however only partially met while an STI payment is due at 71 percent of the total potential.

In the case of Reliance worldwide, the financial targets were fully met in terms of NPAT and

positive shareholder returns. The company recognises the performance of the senior

executives and hence awarded the bonus during its first successful year since listing in the

ASX.

Conclusion

As per the discussion above it is clear that both financial and non financial measures

form a key component of the remuneration structure of the executives who work in the two

companies , reliance worldwide an ALS global. However financial measures are more

significant of the two. It is clear that financial measures that relates to EBITDA, EPS have a

more greater impact in expanding remuneration pay since large scale companies like these

are judged by the shareholder value or their market capitalisation rate. Both these companies

provide share options to executives. This makes them feel more involved in the company and

its operational activities. They feel like that they are part of the company itself. A further

other peer reviewed company. Both companies also provides share options to companies at

nil exercise price.

Analysis and comparison of remuneration methods used

In terms of the remuneration policy of the company reliance worldwide, both

companies followed a short term and long term incentive structure that measured employees

pay based on financial and non financial measures of the executive employees. The principla

goal behind these incentive plans is to focus the executives on long term outcomes, ensuring

the retention of top employees and encouraging teamwork and motivation through company

performance hurdles(Barros and Carvalhal, 2015). In the case of ALS global, the NPAT

target was fully met as were all the non financial KPI’s. The second NPAT hurdle was

however only partially met while an STI payment is due at 71 percent of the total potential.

In the case of Reliance worldwide, the financial targets were fully met in terms of NPAT and

positive shareholder returns. The company recognises the performance of the senior

executives and hence awarded the bonus during its first successful year since listing in the

ASX.

Conclusion

As per the discussion above it is clear that both financial and non financial measures

form a key component of the remuneration structure of the executives who work in the two

companies , reliance worldwide an ALS global. However financial measures are more

significant of the two. It is clear that financial measures that relates to EBITDA, EPS have a

more greater impact in expanding remuneration pay since large scale companies like these

are judged by the shareholder value or their market capitalisation rate. Both these companies

provide share options to executives. This makes them feel more involved in the company and

its operational activities. They feel like that they are part of the company itself. A further

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19MANAGERIAL ACCOUTING

remuneration report analysis off the two companies shows their incentive plans which is

designed to improve organisational performance as well as improve the motivational levels of

employees. Some of the measures are attached to achieving health and safety standards and

achieving milestones in business process. A variety of financial measures enable a more

encompassing view of how the remuneration policy is structured in terms of meeting specific

targets in EPS, shareholder value and total shareholder return.

remuneration report analysis off the two companies shows their incentive plans which is

designed to improve organisational performance as well as improve the motivational levels of

employees. Some of the measures are attached to achieving health and safety standards and

achieving milestones in business process. A variety of financial measures enable a more

encompassing view of how the remuneration policy is structured in terms of meeting specific

targets in EPS, shareholder value and total shareholder return.

20MANAGERIAL ACCOUTING

References:

Akkermans, H.A. and Van Oorschot, K.E., 2018. Relevance assumed: a case study of

balanced scorecard development using system dynamics. In System Dynamics (pp. 107-132).

Palgrave Macmillan, London.

Alissa, W., 2015. Boards’ response to shareholders’ dissatisfaction: The case of shareholders’

say on pay in the UK. European Accounting Review, 24(4), pp.727-752.

Alsglobal.com.2018 [online] Available at:

<https://www.alsglobal.com/-/media/als/resources/myals/.../2017-annual-report.pdf?la=en>

[Accessed 11 September 2018].

Arnaboldi, M., Lapsley, I. and Steccolini, I., 2015. Performance management in the public

sector: The ultimate challenge. Financial Accountability & Management, 31(1), pp.1-22.

Barros, P. and Carvalhal, A., 2015. Do firms controlled by private equity pay higher

executive compensation?. Corporate Ownership & Control, 12(4), pp.364-370.

Bennett, A.J., 2018. The Impact of Active and Passive Ownership on Total Shareholder

Return and Environmental, Social, and Governance Performance of Companies.

Buchanan, T., 2016. Self-report measures of executive function problems correlate with

personality, not performance-based executive function measures, in nonclinical

samples. Psychological Assessment, 28(4), p.372.

Bussin, M. and Modau, M.F., 2015. The relationship between Chief Executive Officer

remuneration and financial performance in South Africa between 2006 and 2012. SA Journal

of Human Resource Management, 13(1), pp.1-18.

Cecchetti, S.G. and Kharroubi, E., 2015. Why does financial sector growth crowd out real

economic growth?.

References:

Akkermans, H.A. and Van Oorschot, K.E., 2018. Relevance assumed: a case study of

balanced scorecard development using system dynamics. In System Dynamics (pp. 107-132).

Palgrave Macmillan, London.

Alissa, W., 2015. Boards’ response to shareholders’ dissatisfaction: The case of shareholders’

say on pay in the UK. European Accounting Review, 24(4), pp.727-752.

Alsglobal.com.2018 [online] Available at:

<https://www.alsglobal.com/-/media/als/resources/myals/.../2017-annual-report.pdf?la=en>

[Accessed 11 September 2018].

Arnaboldi, M., Lapsley, I. and Steccolini, I., 2015. Performance management in the public

sector: The ultimate challenge. Financial Accountability & Management, 31(1), pp.1-22.

Barros, P. and Carvalhal, A., 2015. Do firms controlled by private equity pay higher

executive compensation?. Corporate Ownership & Control, 12(4), pp.364-370.

Bennett, A.J., 2018. The Impact of Active and Passive Ownership on Total Shareholder

Return and Environmental, Social, and Governance Performance of Companies.

Buchanan, T., 2016. Self-report measures of executive function problems correlate with

personality, not performance-based executive function measures, in nonclinical

samples. Psychological Assessment, 28(4), p.372.

Bussin, M. and Modau, M.F., 2015. The relationship between Chief Executive Officer

remuneration and financial performance in South Africa between 2006 and 2012. SA Journal

of Human Resource Management, 13(1), pp.1-18.

Cecchetti, S.G. and Kharroubi, E., 2015. Why does financial sector growth crowd out real

economic growth?.

21MANAGERIAL ACCOUTING

Donate, M.J. and de Pablo, J.D.S., 2015. The role of knowledge-oriented leadership in

knowledge management practices and innovation. Journal of Business Research, 68(2),

pp.360-370.

Ghazvini, M.A.F., Soares, J., Horta, N., Neves, R., Castro, R. and Vale, Z., 2015. A multi-

objective model for scheduling of short-term incentive-based demand response programs

offered by electricity retailers. Applied Energy, 151, pp.102-118.

Hansen, E.G. and Schaltegger, S., 2016. The sustainability balanced scorecard: A systematic

review of architectures. Journal of Business Ethics, 133(2), pp.193-221.

Kamierczyk, J., Kamierczyk, J. and Aptacy, M., 2016. The management by objectives in

banks: the Polish case. Entrepreneurship and Sustainability Issues, 4(2), pp.146-158.

Kerzner, H., 2017. Project management metrics, KPIs, and dashboards: a guide to

measuring and monitoring project performance. John Wiley & Sons.

Kolev, K., Wiseman, R.M. and Gomez-Mejia, L.R., 2017. Do CEOs ever lose? Fairness

perspective on the allocation of residuals between CEOs and shareholders. Journal of

Management, 43(2), pp.610-637.

Lazonick, W., 2016. The value-extracting CEO: How executive stock-based pay undermines

investment in productive capabilities.

Mallin, C., Melis, A. and Gaia, S., 2015. The remuneration of independent directors in the

UK and Italy: An empirical analysis based on agency theory. International Business

Review, 24(2), pp.175-186.

Mone, E.M. and London, M., 2018. Employee engagement through effective performance

management: A practical guide for managers. Routledge.

Donate, M.J. and de Pablo, J.D.S., 2015. The role of knowledge-oriented leadership in

knowledge management practices and innovation. Journal of Business Research, 68(2),

pp.360-370.

Ghazvini, M.A.F., Soares, J., Horta, N., Neves, R., Castro, R. and Vale, Z., 2015. A multi-

objective model for scheduling of short-term incentive-based demand response programs

offered by electricity retailers. Applied Energy, 151, pp.102-118.

Hansen, E.G. and Schaltegger, S., 2016. The sustainability balanced scorecard: A systematic

review of architectures. Journal of Business Ethics, 133(2), pp.193-221.

Kamierczyk, J., Kamierczyk, J. and Aptacy, M., 2016. The management by objectives in

banks: the Polish case. Entrepreneurship and Sustainability Issues, 4(2), pp.146-158.

Kerzner, H., 2017. Project management metrics, KPIs, and dashboards: a guide to

measuring and monitoring project performance. John Wiley & Sons.

Kolev, K., Wiseman, R.M. and Gomez-Mejia, L.R., 2017. Do CEOs ever lose? Fairness

perspective on the allocation of residuals between CEOs and shareholders. Journal of

Management, 43(2), pp.610-637.

Lazonick, W., 2016. The value-extracting CEO: How executive stock-based pay undermines

investment in productive capabilities.

Mallin, C., Melis, A. and Gaia, S., 2015. The remuneration of independent directors in the

UK and Italy: An empirical analysis based on agency theory. International Business

Review, 24(2), pp.175-186.

Mone, E.M. and London, M., 2018. Employee engagement through effective performance

management: A practical guide for managers. Routledge.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22MANAGERIAL ACCOUTING

Rwc.com. 2018. [online] Available at:

<http://www.rwc.com/wp-content/uploads/2017/09/2017-Annual-Report-FINAL-small.pdf>

[Accessed 11 September 2018].

Sauaia, A.C.A., 2014, March. Evaluation of performance in business games: financial and

non financial approaches. In Developments in Business Simulation and Experiential

Learning: Proceedings of the Annual ABSEL conference (Vol. 28).

Schlechter, A., Thompson, N.C. and Bussin, M., 2015. Attractiveness of non-financial

rewards for prospective knowledge workers: An experimental investigation. Employee

Relations, 37(3), pp.274-295.

Shaw, J.D. and Gupta, N., 2015. Let the evidence speak again! Financial incentives are more

effective than we thought. Human Resource Management Journal, 25(3), pp.281-293.

Tan, M. and Liu, B., 2016. CEO's managerial power, board committee memberships and

idiosyncratic volatility. International Review of Financial Analysis, 48, pp.21-30.

Van Dooren, W., Bouckaert, G. and Halligan, J., 2015. Performance management in the

public sector. Routledge.

Rwc.com. 2018. [online] Available at:

<http://www.rwc.com/wp-content/uploads/2017/09/2017-Annual-Report-FINAL-small.pdf>

[Accessed 11 September 2018].

Sauaia, A.C.A., 2014, March. Evaluation of performance in business games: financial and

non financial approaches. In Developments in Business Simulation and Experiential

Learning: Proceedings of the Annual ABSEL conference (Vol. 28).

Schlechter, A., Thompson, N.C. and Bussin, M., 2015. Attractiveness of non-financial

rewards for prospective knowledge workers: An experimental investigation. Employee

Relations, 37(3), pp.274-295.

Shaw, J.D. and Gupta, N., 2015. Let the evidence speak again! Financial incentives are more

effective than we thought. Human Resource Management Journal, 25(3), pp.281-293.

Tan, M. and Liu, B., 2016. CEO's managerial power, board committee memberships and

idiosyncratic volatility. International Review of Financial Analysis, 48, pp.21-30.

Van Dooren, W., Bouckaert, G. and Halligan, J., 2015. Performance management in the

public sector. Routledge.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.