Managerial Accounting: Budgets, Ratios, Variances, ROI and Residual Income

VerifiedAdded on 2023/06/09

|13

|1765

|318

AI Summary

This article covers various topics in Managerial Accounting such as Budgets, Ratios, Variances, ROI and Residual Income. It includes solved examples and calculations for better understanding.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Authors Note:

Managerial Accounting

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGERIAL ACCOUNTING

1

Table of Contents

Question 1:.................................................................................................................................3

a) Sales Budget:..........................................................................................................................3

b) Cash receipt Budget:..............................................................................................................3

c) Production Budget:................................................................................................................3

d) Direct Material Budget:.........................................................................................................4

e) Cash disbursements Budget for raw materials purchases:.....................................................4

Question 2:.................................................................................................................................5

a) Computing variable cost ratio and contribution margin ratio:...............................................5

b) Computing breakeven point in units and ringgit:..................................................................5

c) Number of units sold for earning profit of RM30,000:..........................................................6

d) Computing additional profits if sales were RM25,000 more than expected:........................6

e) Computing the margin of safety in units and ringgit:............................................................7

f.i) Expected change in operating income for revised forecast:.................................................7

f.ii) Expected total operating income after revising the sales forecast:.....................................7

Question 3:.................................................................................................................................8

a) Computing the direct material price and quantity variance and direct labour rated and

efficiency variance, while indicating whether the variance is favourable or unfavourable:......8

b) Explaining the main reasons behind the possible reasons for the variances:........................9

Question 4:.................................................................................................................................9

a) Computing the ROI for the most recent years:......................................................................9

b) Indicating whether being a Division Head of Office Products Division the new product line

is accepted or rejected:.............................................................................................................10

c) Indicating whether the general manager is anxious for the office products division to add

the new product line:................................................................................................................10

1

Table of Contents

Question 1:.................................................................................................................................3

a) Sales Budget:..........................................................................................................................3

b) Cash receipt Budget:..............................................................................................................3

c) Production Budget:................................................................................................................3

d) Direct Material Budget:.........................................................................................................4

e) Cash disbursements Budget for raw materials purchases:.....................................................4

Question 2:.................................................................................................................................5

a) Computing variable cost ratio and contribution margin ratio:...............................................5

b) Computing breakeven point in units and ringgit:..................................................................5

c) Number of units sold for earning profit of RM30,000:..........................................................6

d) Computing additional profits if sales were RM25,000 more than expected:........................6

e) Computing the margin of safety in units and ringgit:............................................................7

f.i) Expected change in operating income for revised forecast:.................................................7

f.ii) Expected total operating income after revising the sales forecast:.....................................7

Question 3:.................................................................................................................................8

a) Computing the direct material price and quantity variance and direct labour rated and

efficiency variance, while indicating whether the variance is favourable or unfavourable:......8

b) Explaining the main reasons behind the possible reasons for the variances:........................9

Question 4:.................................................................................................................................9

a) Computing the ROI for the most recent years:......................................................................9

b) Indicating whether being a Division Head of Office Products Division the new product line

is accepted or rejected:.............................................................................................................10

c) Indicating whether the general manager is anxious for the office products division to add

the new product line:................................................................................................................10

MANAGERIAL ACCOUNTING

2

d.i) Computing the Office Products Division’s residual income for the most recent year:.....10

d.ii) Indicating whether the new product line is accepted or rejected, as being the Division

Head of Office Products Division:...........................................................................................11

Bibliography:............................................................................................................................12

2

d.i) Computing the Office Products Division’s residual income for the most recent year:.....10

d.ii) Indicating whether the new product line is accepted or rejected, as being the Division

Head of Office Products Division:...........................................................................................11

Bibliography:............................................................................................................................12

MANAGERIAL ACCOUNTING

3

Question 1:

a) Sales Budget:

Sales Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Sales in units 2,000 6,000 8,000 4,000 20,000

Sale price 25 25 25 25 25

Total Sales 50,000 150,000 200,000 100,000 500,000

b) Cash receipt Budget:

Cash Receipts Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Sales in units 2,000 6,000 8,000 4,000 20,000

Sale price 25 25 25 25 25

Total Sales 50,000 150,000 200,000 100,000 500,000

Receipts from Q1 30,000 20,000 50,000

Receipts from Q2 90,000 60,000 150,000

Receipts from Q3 120,000 80,000 200,000

Receipts from Q4 60,000 60,000

Total Cash Receipts 30,000 110,000 180,000 140,000 460,000

c) Production Budget:

Production Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

3

Question 1:

a) Sales Budget:

Sales Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Sales in units 2,000 6,000 8,000 4,000 20,000

Sale price 25 25 25 25 25

Total Sales 50,000 150,000 200,000 100,000 500,000

b) Cash receipt Budget:

Cash Receipts Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Sales in units 2,000 6,000 8,000 4,000 20,000

Sale price 25 25 25 25 25

Total Sales 50,000 150,000 200,000 100,000 500,000

Receipts from Q1 30,000 20,000 50,000

Receipts from Q2 90,000 60,000 150,000

Receipts from Q3 120,000 80,000 200,000

Receipts from Q4 60,000 60,000

Total Cash Receipts 30,000 110,000 180,000 140,000 460,000

c) Production Budget:

Production Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGERIAL ACCOUNTING

4

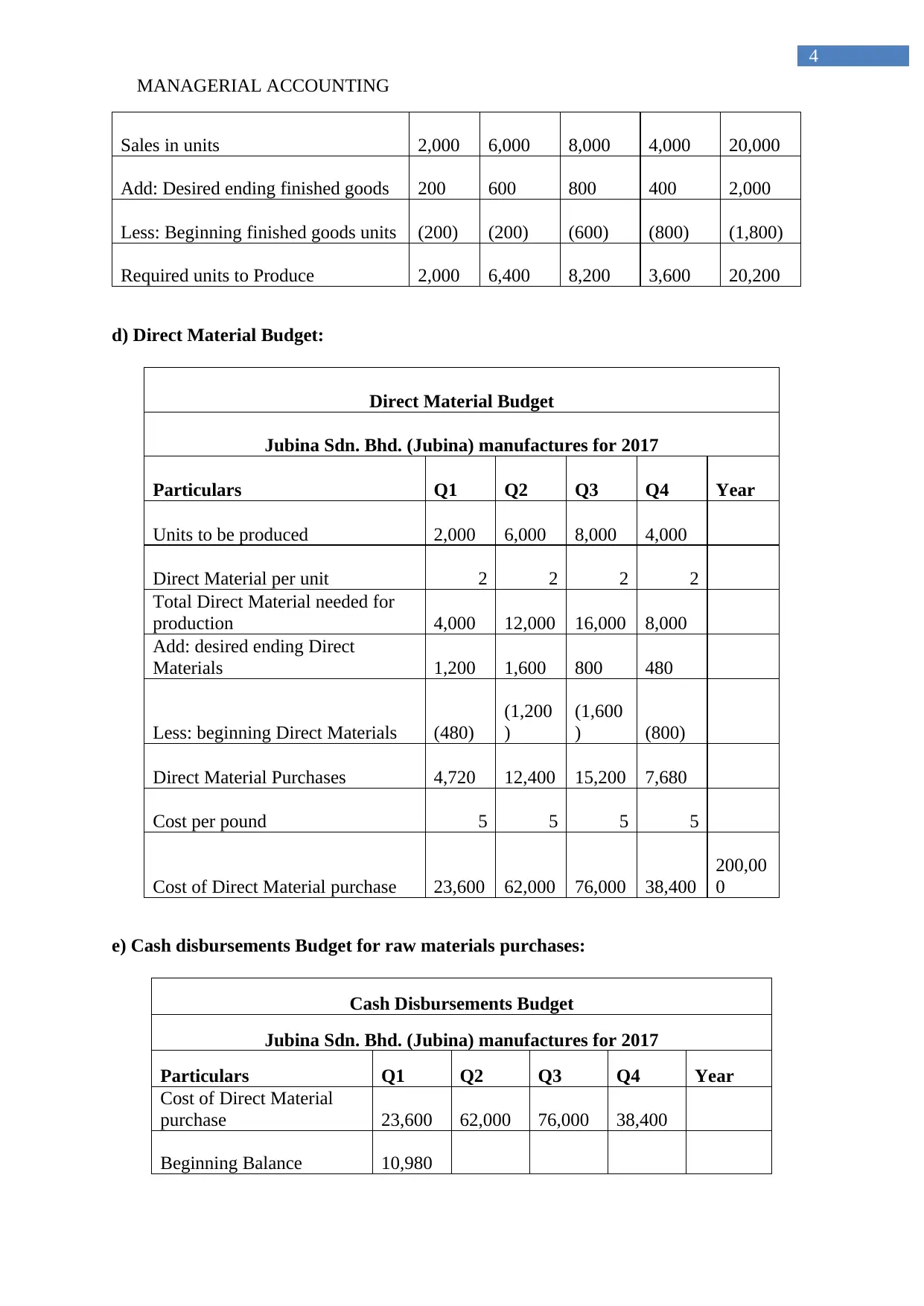

Sales in units 2,000 6,000 8,000 4,000 20,000

Add: Desired ending finished goods 200 600 800 400 2,000

Less: Beginning finished goods units (200) (200) (600) (800) (1,800)

Required units to Produce 2,000 6,400 8,200 3,600 20,200

d) Direct Material Budget:

Direct Material Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Units to be produced 2,000 6,000 8,000 4,000

Direct Material per unit 2 2 2 2

Total Direct Material needed for

production 4,000 12,000 16,000 8,000

Add: desired ending Direct

Materials 1,200 1,600 800 480

Less: beginning Direct Materials (480)

(1,200

)

(1,600

) (800)

Direct Material Purchases 4,720 12,400 15,200 7,680

Cost per pound 5 5 5 5

Cost of Direct Material purchase 23,600 62,000 76,000 38,400

200,00

0

e) Cash disbursements Budget for raw materials purchases:

Cash Disbursements Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Cost of Direct Material

purchase 23,600 62,000 76,000 38,400

Beginning Balance 10,980

4

Sales in units 2,000 6,000 8,000 4,000 20,000

Add: Desired ending finished goods 200 600 800 400 2,000

Less: Beginning finished goods units (200) (200) (600) (800) (1,800)

Required units to Produce 2,000 6,400 8,200 3,600 20,200

d) Direct Material Budget:

Direct Material Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Units to be produced 2,000 6,000 8,000 4,000

Direct Material per unit 2 2 2 2

Total Direct Material needed for

production 4,000 12,000 16,000 8,000

Add: desired ending Direct

Materials 1,200 1,600 800 480

Less: beginning Direct Materials (480)

(1,200

)

(1,600

) (800)

Direct Material Purchases 4,720 12,400 15,200 7,680

Cost per pound 5 5 5 5

Cost of Direct Material purchase 23,600 62,000 76,000 38,400

200,00

0

e) Cash disbursements Budget for raw materials purchases:

Cash Disbursements Budget

Jubina Sdn. Bhd. (Jubina) manufactures for 2017

Particulars Q1 Q2 Q3 Q4 Year

Cost of Direct Material

purchase 23,600 62,000 76,000 38,400

Beginning Balance 10,980

MANAGERIAL ACCOUNTING

5

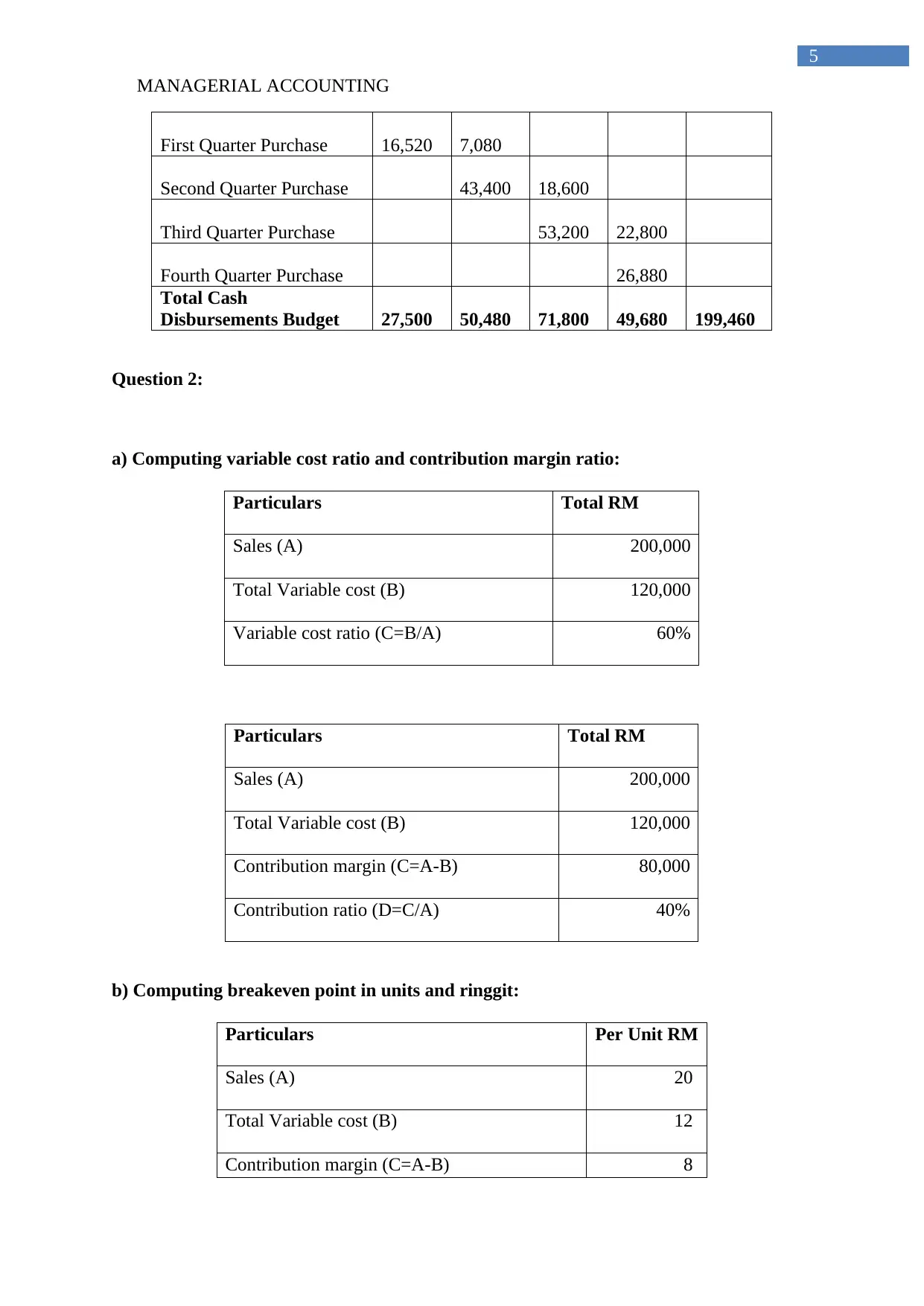

First Quarter Purchase 16,520 7,080

Second Quarter Purchase 43,400 18,600

Third Quarter Purchase 53,200 22,800

Fourth Quarter Purchase 26,880

Total Cash

Disbursements Budget 27,500 50,480 71,800 49,680 199,460

Question 2:

a) Computing variable cost ratio and contribution margin ratio:

Particulars Total RM

Sales (A) 200,000

Total Variable cost (B) 120,000

Variable cost ratio (C=B/A) 60%

Particulars Total RM

Sales (A) 200,000

Total Variable cost (B) 120,000

Contribution margin (C=A-B) 80,000

Contribution ratio (D=C/A) 40%

b) Computing breakeven point in units and ringgit:

Particulars Per Unit RM

Sales (A) 20

Total Variable cost (B) 12

Contribution margin (C=A-B) 8

5

First Quarter Purchase 16,520 7,080

Second Quarter Purchase 43,400 18,600

Third Quarter Purchase 53,200 22,800

Fourth Quarter Purchase 26,880

Total Cash

Disbursements Budget 27,500 50,480 71,800 49,680 199,460

Question 2:

a) Computing variable cost ratio and contribution margin ratio:

Particulars Total RM

Sales (A) 200,000

Total Variable cost (B) 120,000

Variable cost ratio (C=B/A) 60%

Particulars Total RM

Sales (A) 200,000

Total Variable cost (B) 120,000

Contribution margin (C=A-B) 80,000

Contribution ratio (D=C/A) 40%

b) Computing breakeven point in units and ringgit:

Particulars Per Unit RM

Sales (A) 20

Total Variable cost (B) 12

Contribution margin (C=A-B) 8

MANAGERIAL ACCOUNTING

6

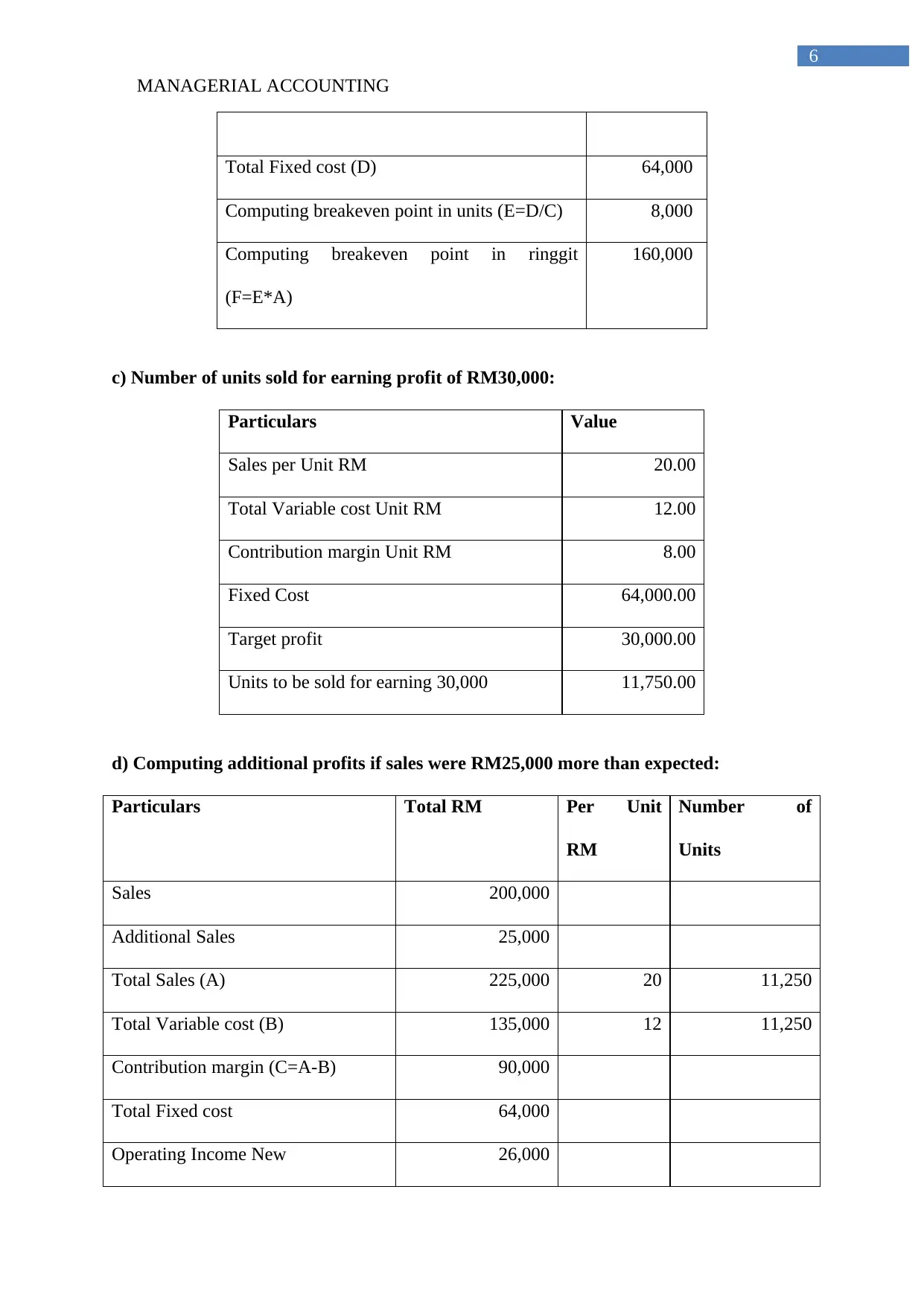

Total Fixed cost (D) 64,000

Computing breakeven point in units (E=D/C) 8,000

Computing breakeven point in ringgit

(F=E*A)

160,000

c) Number of units sold for earning profit of RM30,000:

Particulars Value

Sales per Unit RM 20.00

Total Variable cost Unit RM 12.00

Contribution margin Unit RM 8.00

Fixed Cost 64,000.00

Target profit 30,000.00

Units to be sold for earning 30,000 11,750.00

d) Computing additional profits if sales were RM25,000 more than expected:

Particulars Total RM Per Unit

RM

Number of

Units

Sales 200,000

Additional Sales 25,000

Total Sales (A) 225,000 20 11,250

Total Variable cost (B) 135,000 12 11,250

Contribution margin (C=A-B) 90,000

Total Fixed cost 64,000

Operating Income New 26,000

6

Total Fixed cost (D) 64,000

Computing breakeven point in units (E=D/C) 8,000

Computing breakeven point in ringgit

(F=E*A)

160,000

c) Number of units sold for earning profit of RM30,000:

Particulars Value

Sales per Unit RM 20.00

Total Variable cost Unit RM 12.00

Contribution margin Unit RM 8.00

Fixed Cost 64,000.00

Target profit 30,000.00

Units to be sold for earning 30,000 11,750.00

d) Computing additional profits if sales were RM25,000 more than expected:

Particulars Total RM Per Unit

RM

Number of

Units

Sales 200,000

Additional Sales 25,000

Total Sales (A) 225,000 20 11,250

Total Variable cost (B) 135,000 12 11,250

Contribution margin (C=A-B) 90,000

Total Fixed cost 64,000

Operating Income New 26,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING

7

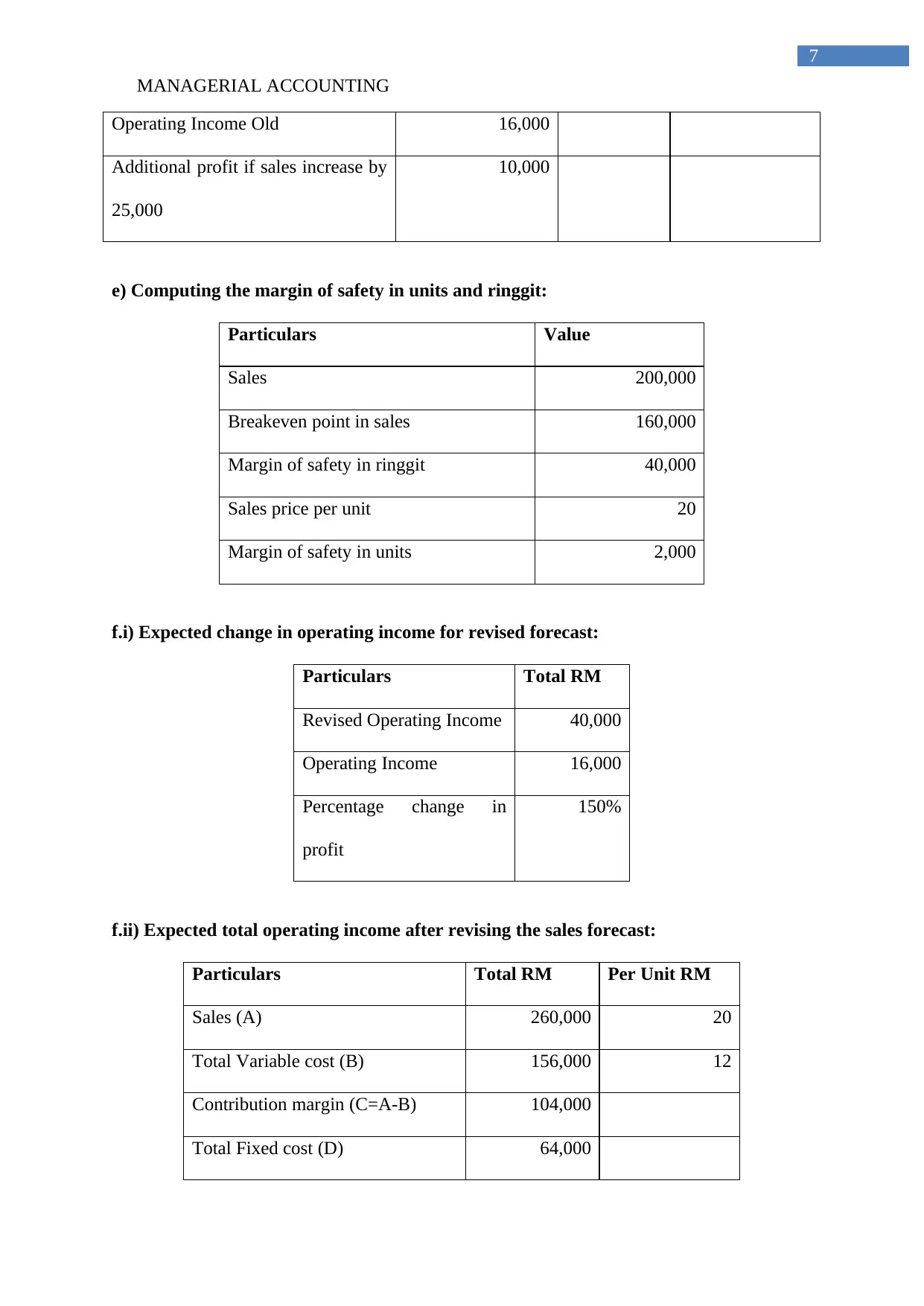

Operating Income Old 16,000

Additional profit if sales increase by

25,000

10,000

e) Computing the margin of safety in units and ringgit:

Particulars Value

Sales 200,000

Breakeven point in sales 160,000

Margin of safety in ringgit 40,000

Sales price per unit 20

Margin of safety in units 2,000

f.i) Expected change in operating income for revised forecast:

Particulars Total RM

Revised Operating Income 40,000

Operating Income 16,000

Percentage change in

profit

150%

f.ii) Expected total operating income after revising the sales forecast:

Particulars Total RM Per Unit RM

Sales (A) 260,000 20

Total Variable cost (B) 156,000 12

Contribution margin (C=A-B) 104,000

Total Fixed cost (D) 64,000

7

Operating Income Old 16,000

Additional profit if sales increase by

25,000

10,000

e) Computing the margin of safety in units and ringgit:

Particulars Value

Sales 200,000

Breakeven point in sales 160,000

Margin of safety in ringgit 40,000

Sales price per unit 20

Margin of safety in units 2,000

f.i) Expected change in operating income for revised forecast:

Particulars Total RM

Revised Operating Income 40,000

Operating Income 16,000

Percentage change in

profit

150%

f.ii) Expected total operating income after revising the sales forecast:

Particulars Total RM Per Unit RM

Sales (A) 260,000 20

Total Variable cost (B) 156,000 12

Contribution margin (C=A-B) 104,000

Total Fixed cost (D) 64,000

MANAGERIAL ACCOUNTING

8

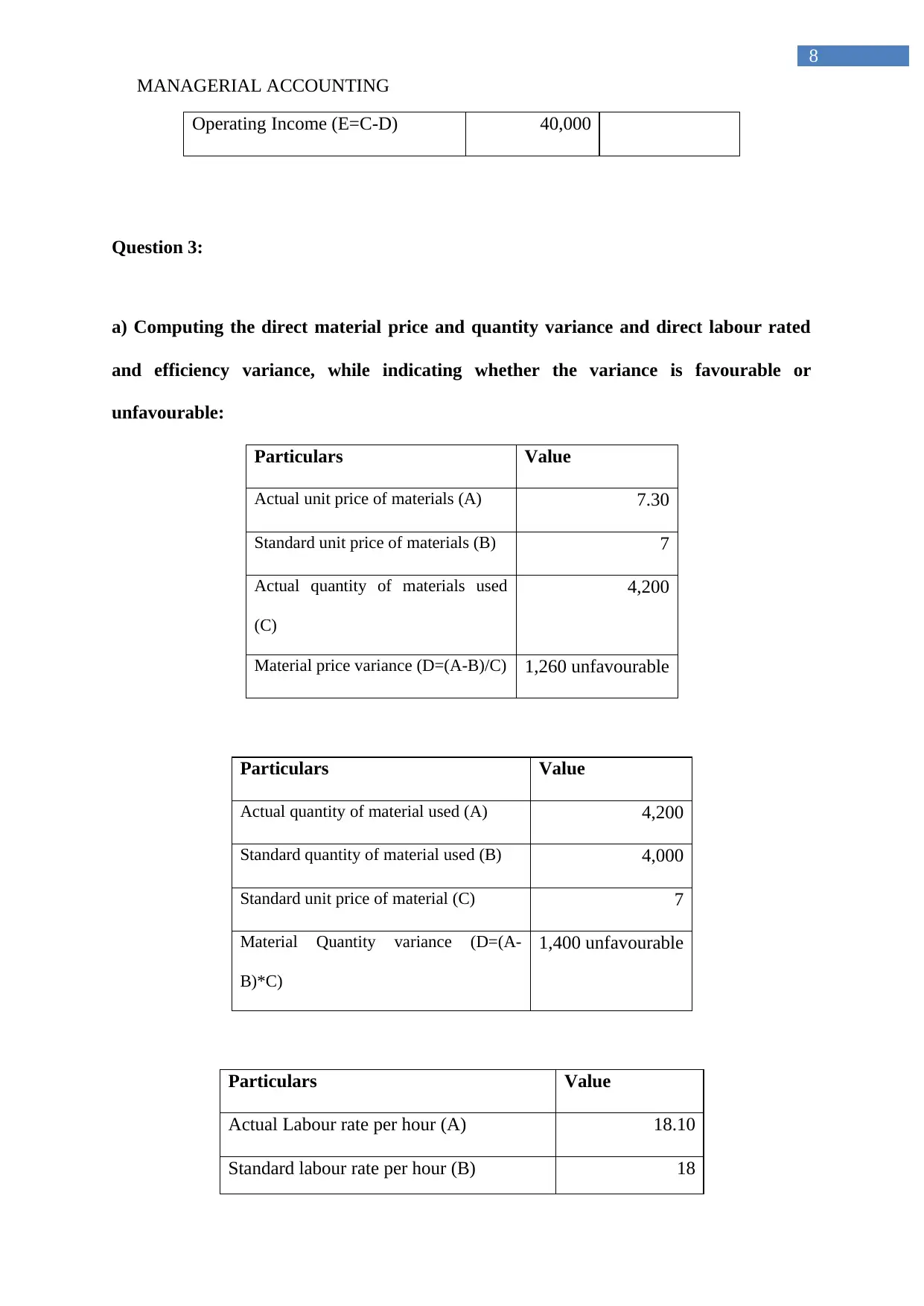

Operating Income (E=C-D) 40,000

Question 3:

a) Computing the direct material price and quantity variance and direct labour rated

and efficiency variance, while indicating whether the variance is favourable or

unfavourable:

Particulars Value

Actual unit price of materials (A) 7.30

Standard unit price of materials (B) 7

Actual quantity of materials used

(C)

4,200

Material price variance (D=(A-B)/C) 1,260 unfavourable

Particulars Value

Actual quantity of material used (A) 4,200

Standard quantity of material used (B) 4,000

Standard unit price of material (C) 7

Material Quantity variance (D=(A-

B)*C)

1,400 unfavourable

Particulars Value

Actual Labour rate per hour (A) 18.10

Standard labour rate per hour (B) 18

8

Operating Income (E=C-D) 40,000

Question 3:

a) Computing the direct material price and quantity variance and direct labour rated

and efficiency variance, while indicating whether the variance is favourable or

unfavourable:

Particulars Value

Actual unit price of materials (A) 7.30

Standard unit price of materials (B) 7

Actual quantity of materials used

(C)

4,200

Material price variance (D=(A-B)/C) 1,260 unfavourable

Particulars Value

Actual quantity of material used (A) 4,200

Standard quantity of material used (B) 4,000

Standard unit price of material (C) 7

Material Quantity variance (D=(A-

B)*C)

1,400 unfavourable

Particulars Value

Actual Labour rate per hour (A) 18.10

Standard labour rate per hour (B) 18

MANAGERIAL ACCOUNTING

9

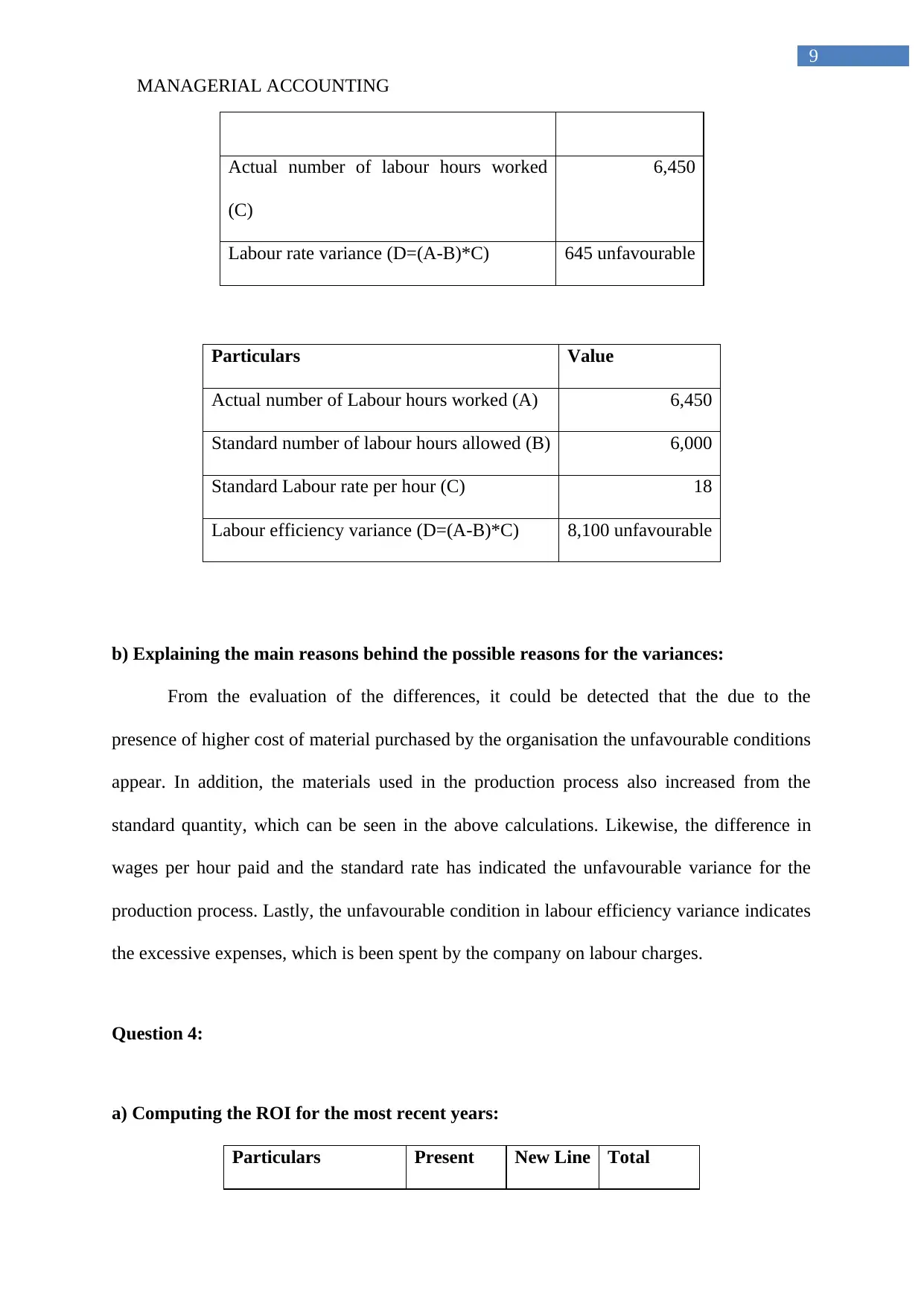

Actual number of labour hours worked

(C)

6,450

Labour rate variance (D=(A-B)*C) 645 unfavourable

Particulars Value

Actual number of Labour hours worked (A) 6,450

Standard number of labour hours allowed (B) 6,000

Standard Labour rate per hour (C) 18

Labour efficiency variance (D=(A-B)*C) 8,100 unfavourable

b) Explaining the main reasons behind the possible reasons for the variances:

From the evaluation of the differences, it could be detected that the due to the

presence of higher cost of material purchased by the organisation the unfavourable conditions

appear. In addition, the materials used in the production process also increased from the

standard quantity, which can be seen in the above calculations. Likewise, the difference in

wages per hour paid and the standard rate has indicated the unfavourable variance for the

production process. Lastly, the unfavourable condition in labour efficiency variance indicates

the excessive expenses, which is been spent by the company on labour charges.

Question 4:

a) Computing the ROI for the most recent years:

Particulars Present New Line Total

9

Actual number of labour hours worked

(C)

6,450

Labour rate variance (D=(A-B)*C) 645 unfavourable

Particulars Value

Actual number of Labour hours worked (A) 6,450

Standard number of labour hours allowed (B) 6,000

Standard Labour rate per hour (C) 18

Labour efficiency variance (D=(A-B)*C) 8,100 unfavourable

b) Explaining the main reasons behind the possible reasons for the variances:

From the evaluation of the differences, it could be detected that the due to the

presence of higher cost of material purchased by the organisation the unfavourable conditions

appear. In addition, the materials used in the production process also increased from the

standard quantity, which can be seen in the above calculations. Likewise, the difference in

wages per hour paid and the standard rate has indicated the unfavourable variance for the

production process. Lastly, the unfavourable condition in labour efficiency variance indicates

the excessive expenses, which is been spent by the company on labour charges.

Question 4:

a) Computing the ROI for the most recent years:

Particulars Present New Line Total

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGERIAL ACCOUNTING

10

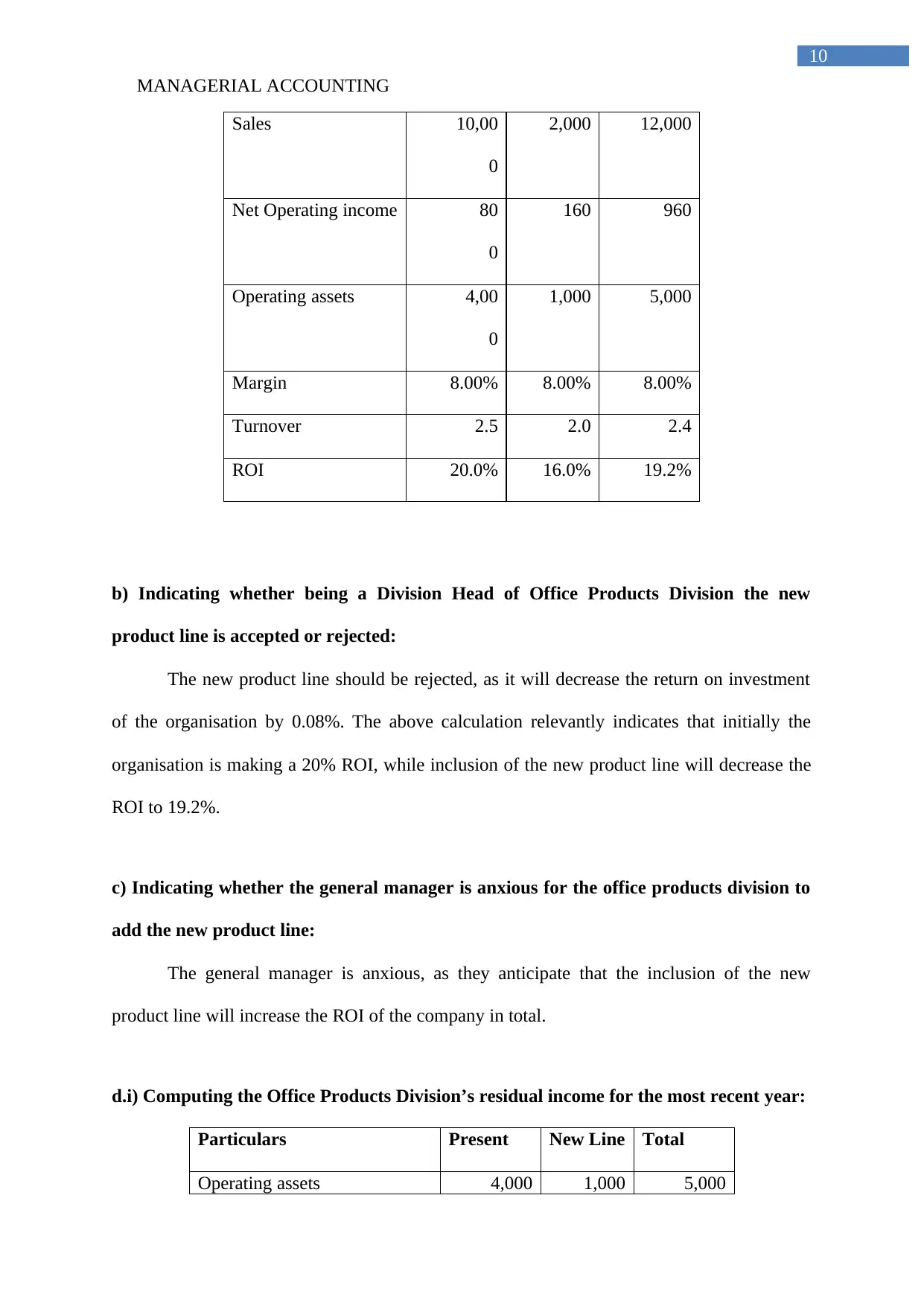

Sales 10,00

0

2,000 12,000

Net Operating income 80

0

160 960

Operating assets 4,00

0

1,000 5,000

Margin 8.00% 8.00% 8.00%

Turnover 2.5 2.0 2.4

ROI 20.0% 16.0% 19.2%

b) Indicating whether being a Division Head of Office Products Division the new

product line is accepted or rejected:

The new product line should be rejected, as it will decrease the return on investment

of the organisation by 0.08%. The above calculation relevantly indicates that initially the

organisation is making a 20% ROI, while inclusion of the new product line will decrease the

ROI to 19.2%.

c) Indicating whether the general manager is anxious for the office products division to

add the new product line:

The general manager is anxious, as they anticipate that the inclusion of the new

product line will increase the ROI of the company in total.

d.i) Computing the Office Products Division’s residual income for the most recent year:

Particulars Present New Line Total

Operating assets 4,000 1,000 5,000

10

Sales 10,00

0

2,000 12,000

Net Operating income 80

0

160 960

Operating assets 4,00

0

1,000 5,000

Margin 8.00% 8.00% 8.00%

Turnover 2.5 2.0 2.4

ROI 20.0% 16.0% 19.2%

b) Indicating whether being a Division Head of Office Products Division the new

product line is accepted or rejected:

The new product line should be rejected, as it will decrease the return on investment

of the organisation by 0.08%. The above calculation relevantly indicates that initially the

organisation is making a 20% ROI, while inclusion of the new product line will decrease the

ROI to 19.2%.

c) Indicating whether the general manager is anxious for the office products division to

add the new product line:

The general manager is anxious, as they anticipate that the inclusion of the new

product line will increase the ROI of the company in total.

d.i) Computing the Office Products Division’s residual income for the most recent year:

Particulars Present New Line Total

Operating assets 4,000 1,000 5,000

MANAGERIAL ACCOUNTING

11

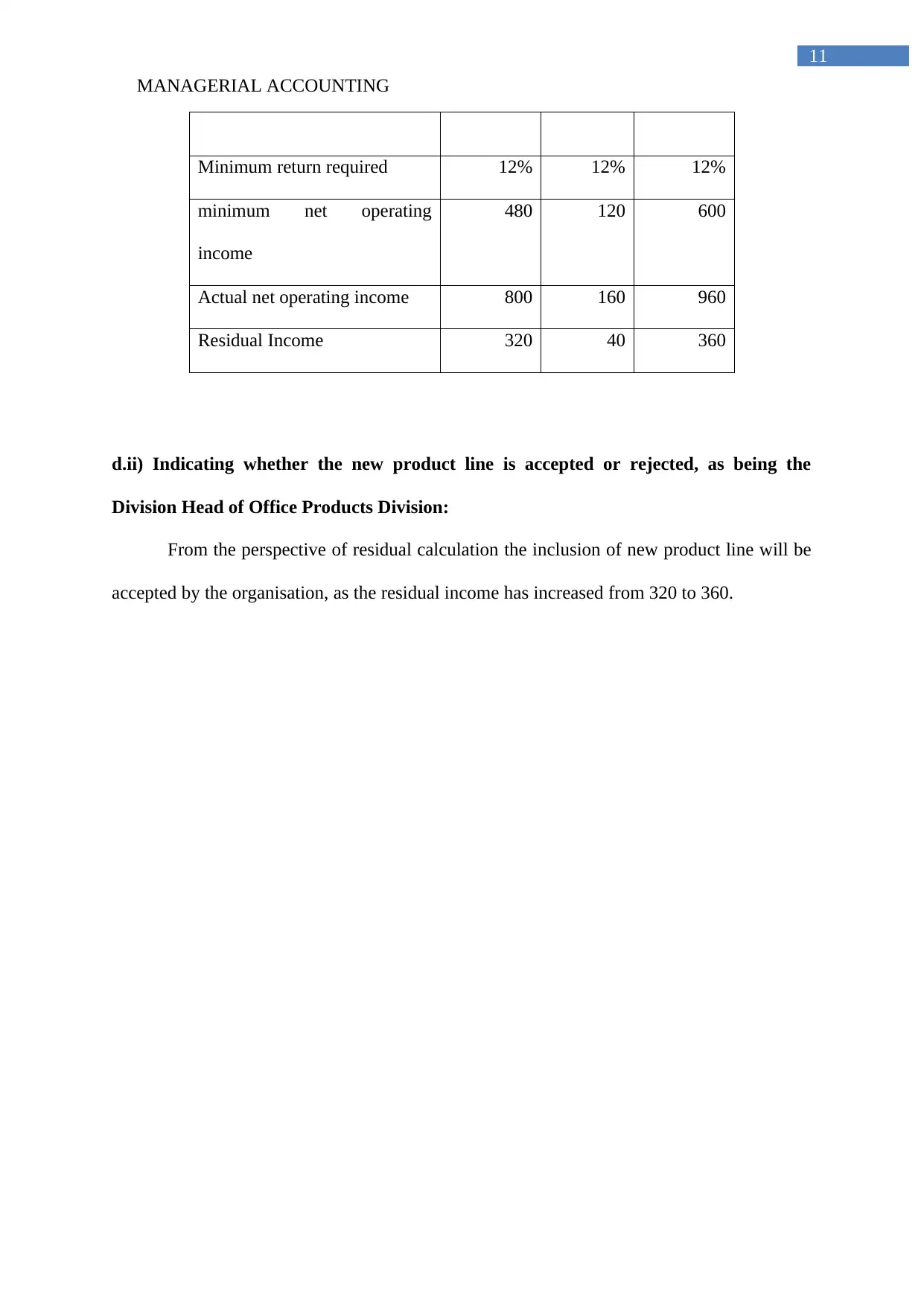

Minimum return required 12% 12% 12%

minimum net operating

income

480 120 600

Actual net operating income 800 160 960

Residual Income 320 40 360

d.ii) Indicating whether the new product line is accepted or rejected, as being the

Division Head of Office Products Division:

From the perspective of residual calculation the inclusion of new product line will be

accepted by the organisation, as the residual income has increased from 320 to 360.

11

Minimum return required 12% 12% 12%

minimum net operating

income

480 120 600

Actual net operating income 800 160 960

Residual Income 320 40 360

d.ii) Indicating whether the new product line is accepted or rejected, as being the

Division Head of Office Products Division:

From the perspective of residual calculation the inclusion of new product line will be

accepted by the organisation, as the residual income has increased from 320 to 360.

MANAGERIAL ACCOUNTING

12

Bibliography:

Noreen, E. W., Brewer, P. C., & Garrison, R. H. (2014). Managerial accounting for

managers. New York: McGraw-Hill/Irwin.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & managerial accounting.

John Wiley & Sons.

12

Bibliography:

Noreen, E. W., Brewer, P. C., & Garrison, R. H. (2014). Managerial accounting for

managers. New York: McGraw-Hill/Irwin.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & managerial accounting.

John Wiley & Sons.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.