Managerial Accounting

Added on 2023-03-31

11 Pages3524 Words342 Views

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

1MANAGERIAL ACCOUNTING

Table of Contents

Part A: Case Study Analysis....................................................................................................................2

Answer to 1.......................................................................................................................................2

Answer to 2.......................................................................................................................................2

Answer to 3.......................................................................................................................................3

Answer to 4.......................................................................................................................................3

Answer to 5.......................................................................................................................................4

Part B: Journal Article Critique...............................................................................................................5

Answer to 1.......................................................................................................................................5

Answer to 2.......................................................................................................................................6

Answer to 3.......................................................................................................................................7

References.............................................................................................................................................9

Table of Contents

Part A: Case Study Analysis....................................................................................................................2

Answer to 1.......................................................................................................................................2

Answer to 2.......................................................................................................................................2

Answer to 3.......................................................................................................................................3

Answer to 4.......................................................................................................................................3

Answer to 5.......................................................................................................................................4

Part B: Journal Article Critique...............................................................................................................5

Answer to 1.......................................................................................................................................5

Answer to 2.......................................................................................................................................6

Answer to 3.......................................................................................................................................7

References.............................................................................................................................................9

2MANAGERIAL ACCOUNTING

Part A: Case Study Analysis

Answer to 1

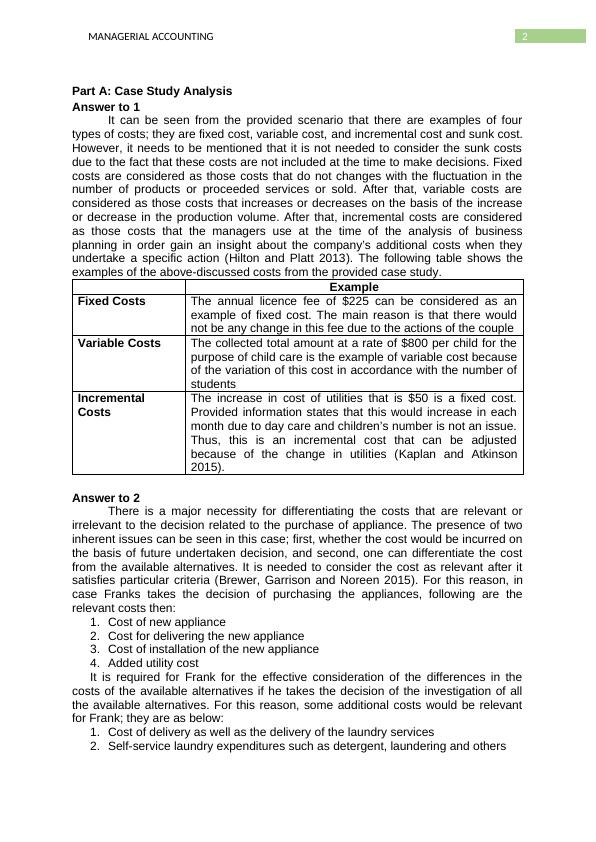

It can be seen from the provided scenario that there are examples of four

types of costs; they are fixed cost, variable cost, and incremental cost and sunk cost.

However, it needs to be mentioned that it is not needed to consider the sunk costs

due to the fact that these costs are not included at the time to make decisions. Fixed

costs are considered as those costs that do not changes with the fluctuation in the

number of products or proceeded services or sold. After that, variable costs are

considered as those costs that increases or decreases on the basis of the increase

or decrease in the production volume. After that, incremental costs are considered

as those costs that the managers use at the time of the analysis of business

planning in order gain an insight about the company’s additional costs when they

undertake a specific action (Hilton and Platt 2013). The following table shows the

examples of the above-discussed costs from the provided case study.

Example

Fixed Costs The annual licence fee of $225 can be considered as an

example of fixed cost. The main reason is that there would

not be any change in this fee due to the actions of the couple

Variable Costs The collected total amount at a rate of $800 per child for the

purpose of child care is the example of variable cost because

of the variation of this cost in accordance with the number of

students

Incremental

Costs

The increase in cost of utilities that is $50 is a fixed cost.

Provided information states that this would increase in each

month due to day care and children’s number is not an issue.

Thus, this is an incremental cost that can be adjusted

because of the change in utilities (Kaplan and Atkinson

2015).

Answer to 2

There is a major necessity for differentiating the costs that are relevant or

irrelevant to the decision related to the purchase of appliance. The presence of two

inherent issues can be seen in this case; first, whether the cost would be incurred on

the basis of future undertaken decision, and second, one can differentiate the cost

from the available alternatives. It is needed to consider the cost as relevant after it

satisfies particular criteria (Brewer, Garrison and Noreen 2015). For this reason, in

case Franks takes the decision of purchasing the appliances, following are the

relevant costs then:

1. Cost of new appliance

2. Cost for delivering the new appliance

3. Cost of installation of the new appliance

4. Added utility cost

It is required for Frank for the effective consideration of the differences in the

costs of the available alternatives if he takes the decision of the investigation of all

the available alternatives. For this reason, some additional costs would be relevant

for Frank; they are as below:

1. Cost of delivery as well as the delivery of the laundry services

2. Self-service laundry expenditures such as detergent, laundering and others

Part A: Case Study Analysis

Answer to 1

It can be seen from the provided scenario that there are examples of four

types of costs; they are fixed cost, variable cost, and incremental cost and sunk cost.

However, it needs to be mentioned that it is not needed to consider the sunk costs

due to the fact that these costs are not included at the time to make decisions. Fixed

costs are considered as those costs that do not changes with the fluctuation in the

number of products or proceeded services or sold. After that, variable costs are

considered as those costs that increases or decreases on the basis of the increase

or decrease in the production volume. After that, incremental costs are considered

as those costs that the managers use at the time of the analysis of business

planning in order gain an insight about the company’s additional costs when they

undertake a specific action (Hilton and Platt 2013). The following table shows the

examples of the above-discussed costs from the provided case study.

Example

Fixed Costs The annual licence fee of $225 can be considered as an

example of fixed cost. The main reason is that there would

not be any change in this fee due to the actions of the couple

Variable Costs The collected total amount at a rate of $800 per child for the

purpose of child care is the example of variable cost because

of the variation of this cost in accordance with the number of

students

Incremental

Costs

The increase in cost of utilities that is $50 is a fixed cost.

Provided information states that this would increase in each

month due to day care and children’s number is not an issue.

Thus, this is an incremental cost that can be adjusted

because of the change in utilities (Kaplan and Atkinson

2015).

Answer to 2

There is a major necessity for differentiating the costs that are relevant or

irrelevant to the decision related to the purchase of appliance. The presence of two

inherent issues can be seen in this case; first, whether the cost would be incurred on

the basis of future undertaken decision, and second, one can differentiate the cost

from the available alternatives. It is needed to consider the cost as relevant after it

satisfies particular criteria (Brewer, Garrison and Noreen 2015). For this reason, in

case Franks takes the decision of purchasing the appliances, following are the

relevant costs then:

1. Cost of new appliance

2. Cost for delivering the new appliance

3. Cost of installation of the new appliance

4. Added utility cost

It is required for Frank for the effective consideration of the differences in the

costs of the available alternatives if he takes the decision of the investigation of all

the available alternatives. For this reason, some additional costs would be relevant

for Frank; they are as below:

1. Cost of delivery as well as the delivery of the laundry services

2. Self-service laundry expenditures such as detergent, laundering and others

3MANAGERIAL ACCOUNTING

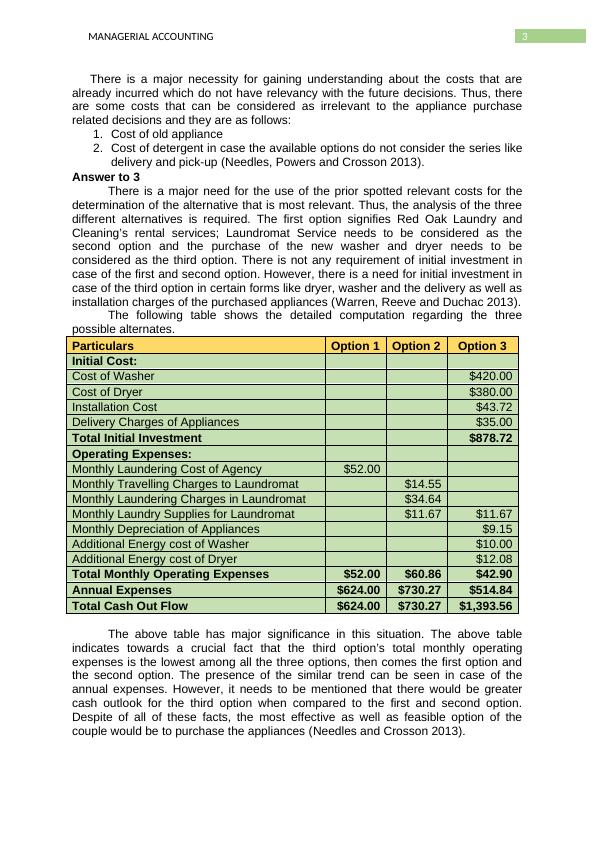

There is a major necessity for gaining understanding about the costs that are

already incurred which do not have relevancy with the future decisions. Thus, there

are some costs that can be considered as irrelevant to the appliance purchase

related decisions and they are as follows:

1. Cost of old appliance

2. Cost of detergent in case the available options do not consider the series like

delivery and pick-up (Needles, Powers and Crosson 2013).

Answer to 3

There is a major need for the use of the prior spotted relevant costs for the

determination of the alternative that is most relevant. Thus, the analysis of the three

different alternatives is required. The first option signifies Red Oak Laundry and

Cleaning’s rental services; Laundromat Service needs to be considered as the

second option and the purchase of the new washer and dryer needs to be

considered as the third option. There is not any requirement of initial investment in

case of the first and second option. However, there is a need for initial investment in

case of the third option in certain forms like dryer, washer and the delivery as well as

installation charges of the purchased appliances (Warren, Reeve and Duchac 2013).

The following table shows the detailed computation regarding the three

possible alternates.

Particulars Option 1 Option 2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to Laundromat $14.55

Monthly Laundering Charges in Laundromat $34.64

Monthly Laundry Supplies for Laundromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Total Cash Out Flow $624.00 $730.27 $1,393.56

The above table has major significance in this situation. The above table

indicates towards a crucial fact that the third option’s total monthly operating

expenses is the lowest among all the three options, then comes the first option and

the second option. The presence of the similar trend can be seen in case of the

annual expenses. However, it needs to be mentioned that there would be greater

cash outlook for the third option when compared to the first and second option.

Despite of all of these facts, the most effective as well as feasible option of the

couple would be to purchase the appliances (Needles and Crosson 2013).

There is a major necessity for gaining understanding about the costs that are

already incurred which do not have relevancy with the future decisions. Thus, there

are some costs that can be considered as irrelevant to the appliance purchase

related decisions and they are as follows:

1. Cost of old appliance

2. Cost of detergent in case the available options do not consider the series like

delivery and pick-up (Needles, Powers and Crosson 2013).

Answer to 3

There is a major need for the use of the prior spotted relevant costs for the

determination of the alternative that is most relevant. Thus, the analysis of the three

different alternatives is required. The first option signifies Red Oak Laundry and

Cleaning’s rental services; Laundromat Service needs to be considered as the

second option and the purchase of the new washer and dryer needs to be

considered as the third option. There is not any requirement of initial investment in

case of the first and second option. However, there is a need for initial investment in

case of the third option in certain forms like dryer, washer and the delivery as well as

installation charges of the purchased appliances (Warren, Reeve and Duchac 2013).

The following table shows the detailed computation regarding the three

possible alternates.

Particulars Option 1 Option 2 Option 3

Initial Cost:

Cost of Washer $420.00

Cost of Dryer $380.00

Installation Cost $43.72

Delivery Charges of Appliances $35.00

Total Initial Investment $878.72

Operating Expenses:

Monthly Laundering Cost of Agency $52.00

Monthly Travelling Charges to Laundromat $14.55

Monthly Laundering Charges in Laundromat $34.64

Monthly Laundry Supplies for Laundromat $11.67 $11.67

Monthly Depreciation of Appliances $9.15

Additional Energy cost of Washer $10.00

Additional Energy cost of Dryer $12.08

Total Monthly Operating Expenses $52.00 $60.86 $42.90

Annual Expenses $624.00 $730.27 $514.84

Total Cash Out Flow $624.00 $730.27 $1,393.56

The above table has major significance in this situation. The above table

indicates towards a crucial fact that the third option’s total monthly operating

expenses is the lowest among all the three options, then comes the first option and

the second option. The presence of the similar trend can be seen in case of the

annual expenses. However, it needs to be mentioned that there would be greater

cash outlook for the third option when compared to the first and second option.

Despite of all of these facts, the most effective as well as feasible option of the

couple would be to purchase the appliances (Needles and Crosson 2013).

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Case Studieslg...

|10

|3315

|402

Managerial Accountinglg...

|11

|3245

|91

Managerial Accounting: Case Study Analysislg...

|11

|3036

|223

Management Accounting Case Studieslg...

|11

|3347

|500

Management Accounting Case Studieslg...

|10

|2664

|434

Managerial Accountinglg...

|17

|4100

|99