Managerial Accounting : Solved Assignment

VerifiedAdded on 2021/06/18

|17

|3741

|42

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

University Name

Student Name

Authors’ Note

Managerial Accounting

University Name

Student Name

Authors’ Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

MANAGERIAL ACCOUNTING

Executive summary:

The report is prepared for analyzing the remuneration framework of chosen company by

evaluating the annual report. Analysis of review of literature is also demonstrated in then

report regarding the different methods that is used by organization for making remuneration

payment to their senior executives. Importance of involvement of stakeholders in

determination of remuneration of executives is also discussed and recommended in the

report. Different methods of determining remuneration of executives of Healthscope is

evaluated by viewing the annual report.

MANAGERIAL ACCOUNTING

Executive summary:

The report is prepared for analyzing the remuneration framework of chosen company by

evaluating the annual report. Analysis of review of literature is also demonstrated in then

report regarding the different methods that is used by organization for making remuneration

payment to their senior executives. Importance of involvement of stakeholders in

determination of remuneration of executives is also discussed and recommended in the

report. Different methods of determining remuneration of executives of Healthscope is

evaluated by viewing the annual report.

3

MANAGERIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Review of literature:...................................................................................................................3

Company review:.......................................................................................................................3

Summary of findings:.................................................................................................................3

Analysis of remuneration method used:.....................................................................................4

Details of remuneration committee and its membership:..........................................................4

Allocation of executive remuneration:.......................................................................................4

Mix of performance measures:...................................................................................................4

Reporting any changes in executive remuneration reporting-2016 versus 2017.......................4

Performance of company versus executive pay:........................................................................4

Recommendation:......................................................................................................................4

Conclusion:................................................................................................................................4

MANAGERIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................3

Review of literature:...................................................................................................................3

Company review:.......................................................................................................................3

Summary of findings:.................................................................................................................3

Analysis of remuneration method used:.....................................................................................4

Details of remuneration committee and its membership:..........................................................4

Allocation of executive remuneration:.......................................................................................4

Mix of performance measures:...................................................................................................4

Reporting any changes in executive remuneration reporting-2016 versus 2017.......................4

Performance of company versus executive pay:........................................................................4

Recommendation:......................................................................................................................4

Conclusion:................................................................................................................................4

4

MANAGERIAL ACCOUNTING

Introduction:

The report is prepared for evaluating the remuneration and executive performance of

public companies that is listed on Australian Stock exchange. Remuneration framework of

company is analyzed with the objective for determining the control system effectiveness in

terms of executive performance and reward system. For this purpose, a detailed analysis of

literature review is conducted on the mix of performance measures that is employed by

organizations. In this particular report, much required evidence is detailed on the relevance of

disclosure of remuneration along with releasing of formal and explicit disclosure

requirement. In this regard, the annual report of chosen company that is Healthscope is

adequately evaluated concerning remuneration structure and framework. Helathscope is a

company based in Melbourne, Australia that was established in year 1985 with its primary

operations in the management and ownership of medicals and hospital centres

(Healthscope.com.au 2018). In addition to this, company is also engaged in provision of

diagnostic and other pathology services. It is a leading private healthcare provider in the

country having leading pathology operations across Malaysia, Singapore and Newzealand.

Discussion:

Review of literature:

In this section, analysis of literature review concerning the methods used for the

computation of pay performance is demonstrated. In addition to this, the guideline and

position of shareholder association of Australia on remuneration executive is also

demonstrated. The relationship between the organization strategy and human resource

management is increasingly identified in the report. There are two common approaches

MANAGERIAL ACCOUNTING

Introduction:

The report is prepared for evaluating the remuneration and executive performance of

public companies that is listed on Australian Stock exchange. Remuneration framework of

company is analyzed with the objective for determining the control system effectiveness in

terms of executive performance and reward system. For this purpose, a detailed analysis of

literature review is conducted on the mix of performance measures that is employed by

organizations. In this particular report, much required evidence is detailed on the relevance of

disclosure of remuneration along with releasing of formal and explicit disclosure

requirement. In this regard, the annual report of chosen company that is Healthscope is

adequately evaluated concerning remuneration structure and framework. Helathscope is a

company based in Melbourne, Australia that was established in year 1985 with its primary

operations in the management and ownership of medicals and hospital centres

(Healthscope.com.au 2018). In addition to this, company is also engaged in provision of

diagnostic and other pathology services. It is a leading private healthcare provider in the

country having leading pathology operations across Malaysia, Singapore and Newzealand.

Discussion:

Review of literature:

In this section, analysis of literature review concerning the methods used for the

computation of pay performance is demonstrated. In addition to this, the guideline and

position of shareholder association of Australia on remuneration executive is also

demonstrated. The relationship between the organization strategy and human resource

management is increasingly identified in the report. There are two common approaches

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

MANAGERIAL ACCOUNTING

involved in the making payment for individual performance. As reviewed from literature,

there is increase in merit salary popularity and there is decline in popularity of incentive pay.

Incentive pays are the incentive plans that are based on bonus payment of employees

depending on their productivity at work. It is the most direct way employed by organization

for creating link between performance and pay structure and it is evident that individual

behaviour at workplace would be motivated by structure of incentive payment. The reason is

attributable to the fact that deserving employees end up being paid more as this plan helps in

attracting and selecting good performers (Adams 2017). In literature, a detailed description is

provided regarding the plans of incentive pays of the counterproductive behaviours.

There some issues that is associated with the incentive plans such as maintenance

cost, diversified workforce, organization culture and small group’s incentive plans. The

approach of incentive pay is not adopted by several organizations because the negative

impacts of the plan and maintenance cost outweighs the increase in performance by

performance incentives. In some situation, incentive pay is considered as the best fit for

organizations where it is possible to measure the work comprehensively and they are

repetitive, simple and designed for individual. Incentive plan is associated with the

management control approach and it would involve oriented management style that would

stress fairness, due process and participation pay of incentives (Ahmed et al. 2015).

Under this system, there are two types of incentive pay that has been designed and

this involves long term incentive plans (LTI) and short term incentive plans (STI).

LTI are the scheme that helps in establishing relationship between overall long term

performance and bonus schemes as the main focus of such plan is to focus on long term

performance. Some of the plans under this scheme are based on options and stocks. Under

this plan, executives are able to achieve target value for certain measure of performance, they

MANAGERIAL ACCOUNTING

involved in the making payment for individual performance. As reviewed from literature,

there is increase in merit salary popularity and there is decline in popularity of incentive pay.

Incentive pays are the incentive plans that are based on bonus payment of employees

depending on their productivity at work. It is the most direct way employed by organization

for creating link between performance and pay structure and it is evident that individual

behaviour at workplace would be motivated by structure of incentive payment. The reason is

attributable to the fact that deserving employees end up being paid more as this plan helps in

attracting and selecting good performers (Adams 2017). In literature, a detailed description is

provided regarding the plans of incentive pays of the counterproductive behaviours.

There some issues that is associated with the incentive plans such as maintenance

cost, diversified workforce, organization culture and small group’s incentive plans. The

approach of incentive pay is not adopted by several organizations because the negative

impacts of the plan and maintenance cost outweighs the increase in performance by

performance incentives. In some situation, incentive pay is considered as the best fit for

organizations where it is possible to measure the work comprehensively and they are

repetitive, simple and designed for individual. Incentive plan is associated with the

management control approach and it would involve oriented management style that would

stress fairness, due process and participation pay of incentives (Ahmed et al. 2015).

Under this system, there are two types of incentive pay that has been designed and

this involves long term incentive plans (LTI) and short term incentive plans (STI).

LTI are the scheme that helps in establishing relationship between overall long term

performance and bonus schemes as the main focus of such plan is to focus on long term

performance. Some of the plans under this scheme are based on options and stocks. Under

this plan, executives are able to achieve target value for certain measure of performance, they

6

MANAGERIAL ACCOUNTING

are granted with the options or stocks and enabling organization to lower the amount of fixed

costs. LTI intends to create alignment between long term objectives and interest of

shareholder and executives of company. However, this particular approach of scheme comes

with the drawback as employee perceives that performance is associated with reward level.

This is so because such approach is confined towards higher level of executives who directly

impacts the overall performance of company. Employee under such benefits scheme is not

able to derive direct benefits as it creates restriction on liquidity of company (Gitman et al.

2015).

STI are the schemes where the period of performance measurement is usually one

year and employees are paid in cash such as gain share, share of profit, bonus scheme and

commission. The performance criteria under such scheme incorporates qualitative, non

qualitative and some non financial measures. Employees are able to prioritize bottom line and

become well acquainted with the profit margin under the method of profit sharing (Pickering

2017).

It is viewed by the association of Australian shareholder that incentive schemes are

not properly aligned with shareholder returns and they are too often made for less than the

superior performance. The guidelines advocated by the Australian association for LTI plans

are as follows:

LTI involves two components that help in improving the performance of company in

long run. The progress of long term cycle is reflected across business cycle that make

hurdle based on pre set and superior level of increase in company earnings. Making

use of relative total shareholder return against the suitable group of comparator is

another component that is vested at a maximum of 10%.

LTI should be provided to senior executives for creation of shareholder value.

MANAGERIAL ACCOUNTING

are granted with the options or stocks and enabling organization to lower the amount of fixed

costs. LTI intends to create alignment between long term objectives and interest of

shareholder and executives of company. However, this particular approach of scheme comes

with the drawback as employee perceives that performance is associated with reward level.

This is so because such approach is confined towards higher level of executives who directly

impacts the overall performance of company. Employee under such benefits scheme is not

able to derive direct benefits as it creates restriction on liquidity of company (Gitman et al.

2015).

STI are the schemes where the period of performance measurement is usually one

year and employees are paid in cash such as gain share, share of profit, bonus scheme and

commission. The performance criteria under such scheme incorporates qualitative, non

qualitative and some non financial measures. Employees are able to prioritize bottom line and

become well acquainted with the profit margin under the method of profit sharing (Pickering

2017).

It is viewed by the association of Australian shareholder that incentive schemes are

not properly aligned with shareholder returns and they are too often made for less than the

superior performance. The guidelines advocated by the Australian association for LTI plans

are as follows:

LTI involves two components that help in improving the performance of company in

long run. The progress of long term cycle is reflected across business cycle that make

hurdle based on pre set and superior level of increase in company earnings. Making

use of relative total shareholder return against the suitable group of comparator is

another component that is vested at a maximum of 10%.

LTI should be provided to senior executives for creation of shareholder value.

7

MANAGERIAL ACCOUNTING

The guidelines advocated by ASA for STI plans are as follows:

Financial performance metrics forms the basis of 50% of STI that is verified by

company in area of responsibility and is based on quantifiable performance indicators.

Equity forms the basis of 50% of STI awards are provided to executives that is

regardless of whether the executives are in the same position.

Company review:

The remuneration structure of Healthscope group is based on performance with the

objective of recognizing and encouraging high performance in a manner that helps in aligning

the long term interests of shareholders and organization as a whole. Outcome of remuneration

is reflecting in the performance when the financial or non financial targets are exceeded or

achieved. It is recognized by the board that it is important to ensure continuous alignment

between shareholder and senior executives. Remuneration arrangement of key management

personnel of Healthscope is detailed in the annual report. It is the responsibility of board to

ensure that structure of remuneration is equitable and well aligned with the long term interest

of stakeholders and organization. Board is further responsible for establishment of

remuneration committee that provides recommendation to the board about incentive

arrangements and fixed remuneration for senior executive and other executives reporting to

CEO. Any major change and development in the incentive plans of employees is also

recommended by the remuneration committee. The incentive plans of organization were

affected in the current year because the financial performance was below target.

STI- The outcome of STI was reduced for participants in corporate roles and such

discretion was exercised by the board. Outcome was reduced to a maximum of 40% of the

target of individual regarding STI opportunity. Such decision was taken by management after

MANAGERIAL ACCOUNTING

The guidelines advocated by ASA for STI plans are as follows:

Financial performance metrics forms the basis of 50% of STI that is verified by

company in area of responsibility and is based on quantifiable performance indicators.

Equity forms the basis of 50% of STI awards are provided to executives that is

regardless of whether the executives are in the same position.

Company review:

The remuneration structure of Healthscope group is based on performance with the

objective of recognizing and encouraging high performance in a manner that helps in aligning

the long term interests of shareholders and organization as a whole. Outcome of remuneration

is reflecting in the performance when the financial or non financial targets are exceeded or

achieved. It is recognized by the board that it is important to ensure continuous alignment

between shareholder and senior executives. Remuneration arrangement of key management

personnel of Healthscope is detailed in the annual report. It is the responsibility of board to

ensure that structure of remuneration is equitable and well aligned with the long term interest

of stakeholders and organization. Board is further responsible for establishment of

remuneration committee that provides recommendation to the board about incentive

arrangements and fixed remuneration for senior executive and other executives reporting to

CEO. Any major change and development in the incentive plans of employees is also

recommended by the remuneration committee. The incentive plans of organization were

affected in the current year because the financial performance was below target.

STI- The outcome of STI was reduced for participants in corporate roles and such

discretion was exercised by the board. Outcome was reduced to a maximum of 40% of the

target of individual regarding STI opportunity. Such decision was taken by management after

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

MANAGERIAL ACCOUNTING

accounting for a range of factors that included the financial performance of group lower than

it is anticipated (Boer et al. 2017).

LTI- The two performance conditions following the testing of performance for the

financial year 2015 of the performance rights of LTI that is earning per share and return to

shareholder return (Leong et al. 2015).

An appropriate focus on internal and external performance was continued to be

provided due to hurdles created by current dual performance. In financial year 2018, the

weighting of measures will be adjusted so that equal weight age will be provided to

performance measure. There is likelihood that such re weighting will help in aligning the

interest of shareholders. Under the LTI plan, there will also be revision of future grants

regarding the EPS target setting practice. This will have three year target for replacing current

approach of cumulative annual target setting. The commitment of Healthscope remained to

providing a retrospective performance disclosure against the metrics of EPS at the end of

each performance period (Maas and Rosendaal 2016).

Remuneration policy of Healthscope intends to ensure that the organization has the

capability of attracting and retaining suitably experienced and qualified personnel.

Summary of findings:

The above section details literature review analysis on the framework of

remuneration and importance of disclosing remuneration in the annual report of organization.

It also elucidates the discussion on the remuneration framework and structure of Healthscope

group. According to review of literature, it can be inferred that computation of incentives are

done using several methods and accordingly it helps in determining the measure of

performance. Nevertheless, there are some considerable differences between the methods of

MANAGERIAL ACCOUNTING

accounting for a range of factors that included the financial performance of group lower than

it is anticipated (Boer et al. 2017).

LTI- The two performance conditions following the testing of performance for the

financial year 2015 of the performance rights of LTI that is earning per share and return to

shareholder return (Leong et al. 2015).

An appropriate focus on internal and external performance was continued to be

provided due to hurdles created by current dual performance. In financial year 2018, the

weighting of measures will be adjusted so that equal weight age will be provided to

performance measure. There is likelihood that such re weighting will help in aligning the

interest of shareholders. Under the LTI plan, there will also be revision of future grants

regarding the EPS target setting practice. This will have three year target for replacing current

approach of cumulative annual target setting. The commitment of Healthscope remained to

providing a retrospective performance disclosure against the metrics of EPS at the end of

each performance period (Maas and Rosendaal 2016).

Remuneration policy of Healthscope intends to ensure that the organization has the

capability of attracting and retaining suitably experienced and qualified personnel.

Summary of findings:

The above section details literature review analysis on the framework of

remuneration and importance of disclosing remuneration in the annual report of organization.

It also elucidates the discussion on the remuneration framework and structure of Healthscope

group. According to review of literature, it can be inferred that computation of incentives are

done using several methods and accordingly it helps in determining the measure of

performance. Nevertheless, there are some considerable differences between the methods of

9

MANAGERIAL ACCOUNTING

computing performance pay that are used practically and those discussed in the literature.

This is so because such methods take into account some realistic and market related factors

impacting the structure of remuneration (Qu et al. 2016). In addition to this, such factors need

to be well aligned with the performance of organization. This will help in strategizing the

remuneration in line with goals and objectives of organization. From the analysis of

remuneration report of Helathscope group, it is depicted that remuneration is structured

through an engaging and equitable rewarding framework.

Analysis of remuneration method used:

Details of remuneration committee and its membership:

The remuneration committee is composed of majority of independent directors who

have the responsibility of conducting review of key aspects of remuneration structure and

arrangements of Healthscope. During the process of developing framework of remuneration,

the committee consults with other key external shareholders. Such external independent

advice is sought by the committee when required that will help in guiding the informed

decision making. The function of remuneration committee is to make arrangement for

remuneration to non executive directors, make major development and changes in the

employee incentive plans and make recommendations for incentive arrangement and fixed

remuneration for senior and other executives reporting to chief executive officer (Rao et al.

2015).

Allocation of executive remuneration:

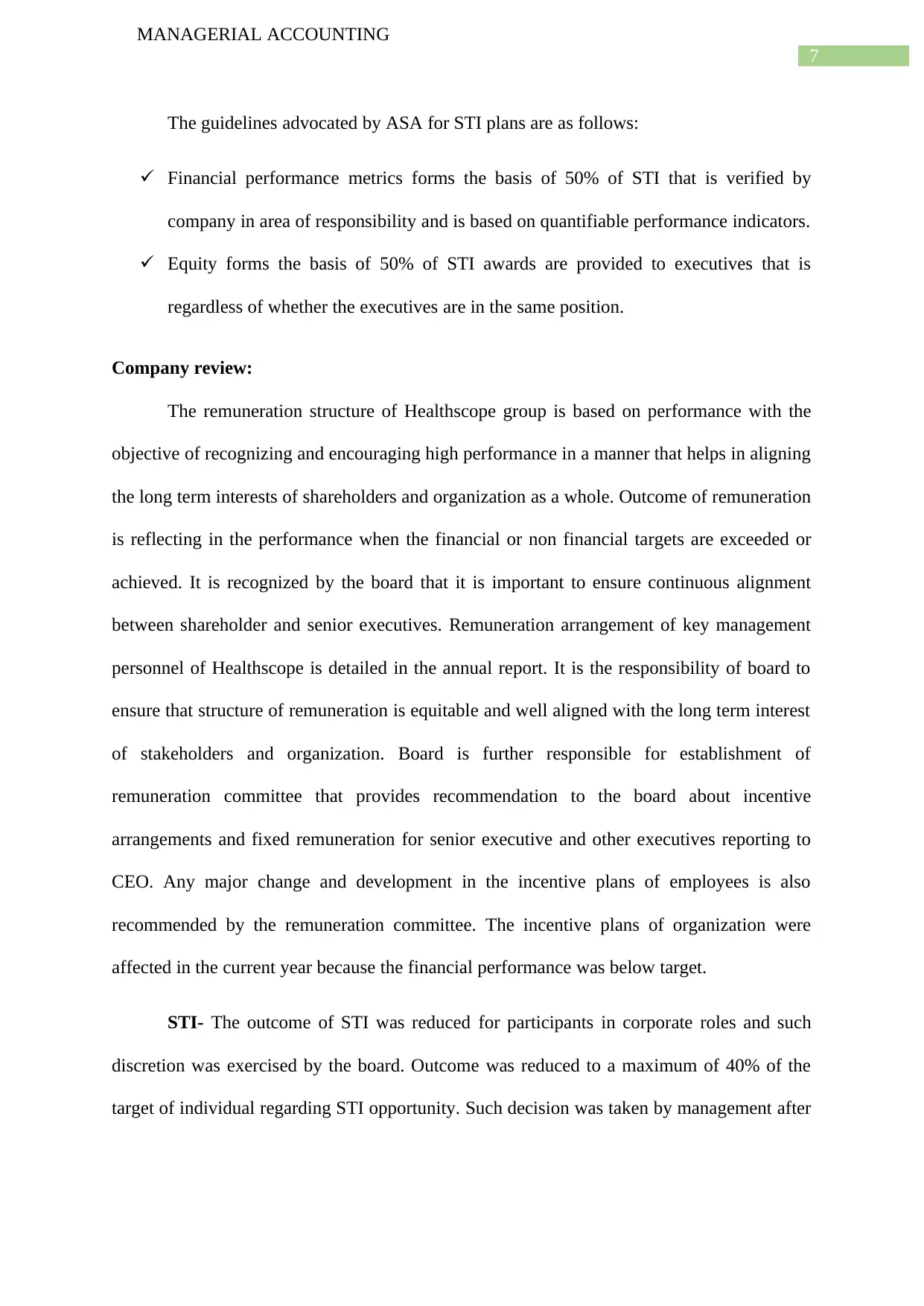

The plan of STI is designed for rewarding performance and increasing focus against

those areas that considerably drives the strategic initiatives of Healthscope. For senior

executives, targets of STI were aligned with the approach of balance scorecard and the STI

MANAGERIAL ACCOUNTING

computing performance pay that are used practically and those discussed in the literature.

This is so because such methods take into account some realistic and market related factors

impacting the structure of remuneration (Qu et al. 2016). In addition to this, such factors need

to be well aligned with the performance of organization. This will help in strategizing the

remuneration in line with goals and objectives of organization. From the analysis of

remuneration report of Helathscope group, it is depicted that remuneration is structured

through an engaging and equitable rewarding framework.

Analysis of remuneration method used:

Details of remuneration committee and its membership:

The remuneration committee is composed of majority of independent directors who

have the responsibility of conducting review of key aspects of remuneration structure and

arrangements of Healthscope. During the process of developing framework of remuneration,

the committee consults with other key external shareholders. Such external independent

advice is sought by the committee when required that will help in guiding the informed

decision making. The function of remuneration committee is to make arrangement for

remuneration to non executive directors, make major development and changes in the

employee incentive plans and make recommendations for incentive arrangement and fixed

remuneration for senior and other executives reporting to chief executive officer (Rao et al.

2015).

Allocation of executive remuneration:

The plan of STI is designed for rewarding performance and increasing focus against

those areas that considerably drives the strategic initiatives of Healthscope. For senior

executives, targets of STI were aligned with the approach of balance scorecard and the STI

10

MANAGERIAL ACCOUNTING

measures of CEO and CFO is based on operating net profit after tax and it does not involve

non operating items that are not related to business in their usual operations. Balanced

scorecard makes use of financial and non financial measure for measuring the performance.

Using the scorecard at organizational level helps in providing the information by aligning the

goals and performance plan of employees. For senior executives, financial targets are based

on operating earnings before interest and tax. On other hand, there are some non financial

measures involves goals and setting specific targets in relation to quality. The key to positive

outcome of Healthscope is related with area of safety, culture and people

(Healthscope.com.au 2018).

STI awards based on financial and non financial measures:

(Source: Healthscope.com.au 2018)

LTI plan on other hand is designed for aligning the shareholder interest and providing

them with equity interest by way of granting performance rights and it is subjected to the

achievement of dual performance conditions. There are dual performance hurdles under this

particular approach that involves relative total shareholder return and earnings per share. This

performance measures are indicative of the fact that organization utilize both lag and lead

MANAGERIAL ACCOUNTING

measures of CEO and CFO is based on operating net profit after tax and it does not involve

non operating items that are not related to business in their usual operations. Balanced

scorecard makes use of financial and non financial measure for measuring the performance.

Using the scorecard at organizational level helps in providing the information by aligning the

goals and performance plan of employees. For senior executives, financial targets are based

on operating earnings before interest and tax. On other hand, there are some non financial

measures involves goals and setting specific targets in relation to quality. The key to positive

outcome of Healthscope is related with area of safety, culture and people

(Healthscope.com.au 2018).

STI awards based on financial and non financial measures:

(Source: Healthscope.com.au 2018)

LTI plan on other hand is designed for aligning the shareholder interest and providing

them with equity interest by way of granting performance rights and it is subjected to the

achievement of dual performance conditions. There are dual performance hurdles under this

particular approach that involves relative total shareholder return and earnings per share. This

performance measures are indicative of the fact that organization utilize both lag and lead

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

MANAGERIAL ACCOUNTING

indicators. Measure of EPS was chosen because it has lower susceptibility to volatility of

short term share price and correlation with long term return of shareholder

(Healthscope.com.au 2018). The performance of ordinary shares of Helathscope is measured

under relative total shareholder return against the performance of comparator group of

companies. It is believed by the board that this particular measure is an appropriate hurdle as

it helps in creating linkage between relative share performance of company and senior

executive reward. Assessment of performance of RTSR is done independently over the

performance period against the constituents of S&P ASX 100 index. Computation of EPS on

other hand is done by dividing operating net profit after tax by weighted average number of

shares (Healthscope.com.au 2018). Furthermore, it is believed by the board of company that

such methods of assessing the performance are considered as the most appropriate way of

assessing true financial performance and accordingly determining the outcome of

remuneration.

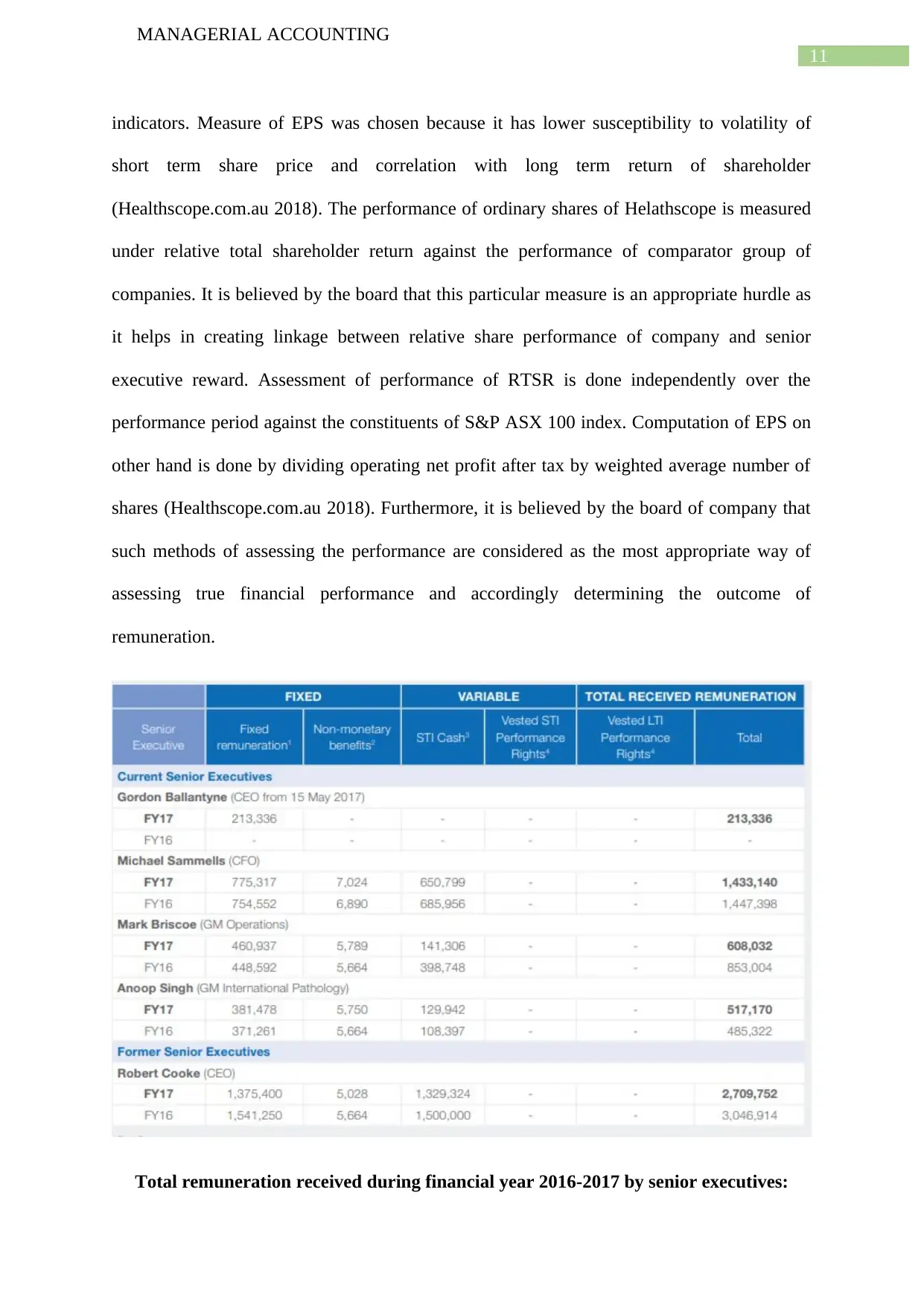

Total remuneration received during financial year 2016-2017 by senior executives:

MANAGERIAL ACCOUNTING

indicators. Measure of EPS was chosen because it has lower susceptibility to volatility of

short term share price and correlation with long term return of shareholder

(Healthscope.com.au 2018). The performance of ordinary shares of Helathscope is measured

under relative total shareholder return against the performance of comparator group of

companies. It is believed by the board that this particular measure is an appropriate hurdle as

it helps in creating linkage between relative share performance of company and senior

executive reward. Assessment of performance of RTSR is done independently over the

performance period against the constituents of S&P ASX 100 index. Computation of EPS on

other hand is done by dividing operating net profit after tax by weighted average number of

shares (Healthscope.com.au 2018). Furthermore, it is believed by the board of company that

such methods of assessing the performance are considered as the most appropriate way of

assessing true financial performance and accordingly determining the outcome of

remuneration.

Total remuneration received during financial year 2016-2017 by senior executives:

12

MANAGERIAL ACCOUNTING

(Source: Healthscope.com.au 2018)

The financial and operational performance of company is considered as critical

indicator of share value driver and performance. Remuneration outcome of senior executives

and CEO is reflected in performance measure outcome of country (Riaz et al. 2015).

Reporting any changes in executive remuneration reporting-2016 versus 2017:

A comprehensive review of remuneration framework of Health scope was conducted

during year 2017 that involved short as well as ling term incentive plan. It was declared in the

annual report that an appropriate focus on internal and external focus is provided by hurdles

of current dual performance. In financial year 2018, it is sought by the board that there will

be adjustment in weighing of measures for brining equal weight age of earning per share and

return to shareholder. Such re weighting intends to align the interest of shareholders.

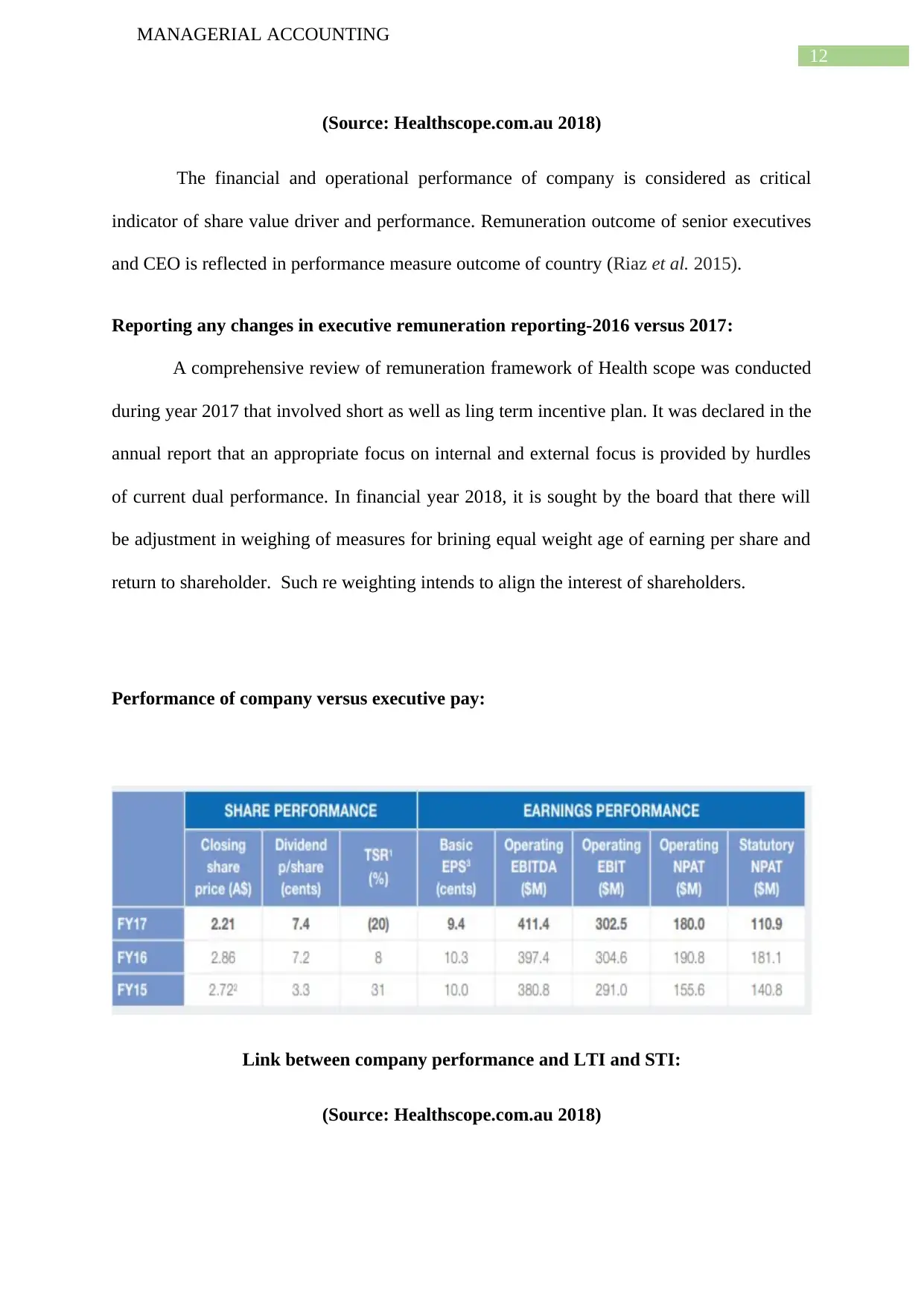

Performance of company versus executive pay:

Link between company performance and LTI and STI:

(Source: Healthscope.com.au 2018)

MANAGERIAL ACCOUNTING

(Source: Healthscope.com.au 2018)

The financial and operational performance of company is considered as critical

indicator of share value driver and performance. Remuneration outcome of senior executives

and CEO is reflected in performance measure outcome of country (Riaz et al. 2015).

Reporting any changes in executive remuneration reporting-2016 versus 2017:

A comprehensive review of remuneration framework of Health scope was conducted

during year 2017 that involved short as well as ling term incentive plan. It was declared in the

annual report that an appropriate focus on internal and external focus is provided by hurdles

of current dual performance. In financial year 2018, it is sought by the board that there will

be adjustment in weighing of measures for brining equal weight age of earning per share and

return to shareholder. Such re weighting intends to align the interest of shareholders.

Performance of company versus executive pay:

Link between company performance and LTI and STI:

(Source: Healthscope.com.au 2018)

13

MANAGERIAL ACCOUNTING

Recommendation:

From the analysis of remuneration structure of Healthscope group, it has been viewed

that the remuneration strategy is based on ownership that provided senior management with

the opportunity of receiving equity instruments as a component of long and short term

remuneration. Organization has made use of financial and non financial measures for

determining the performance pay. The remuneration framework for year 2017 was weighted

towards at risk remuneration. A clear link has been noticed between the performance of

company and outcomes of its incentive schemes for its senior executives. Remuneration of

executives is also determined by performing benchmarking exercise. However, it is required

on part of management of Healthscope to look at overall interaction when incorporating

shareholder engagement in determining the executive’s remuneration. Since, shareholder

engagement in determining remuneration of executives is regarded as essential to the good

corporate governance practices; there should be considerable involvement of shareholder

(Kanapathippillai et al. 2015). Furthermore, there should be well alignment between overall

performance and objective of remuneration reporting framework.

Conclusion:

The above discussed paper demonstrates the comparison and analysis of methods that

are used paying for performance by reviewing the annual report of Healthcsope and literature.

It is illustrated from reviewing the literature that computation of performance pay is done by

using various methods. It is depicted from annual report analysis of Healthscope that

disclosure relating to executive of remuneration is done according to applicable regulations

and legislations. Moreover, the incentive plan that is short term and long term incentive plan

and its outcome reflects the performance of organization. There is adequate amount of

disclosure regarding the measures of such incentive schemes. On contrary to this, the

methodology of allocation of executive remuneration is not disclosed properly. Some of the

MANAGERIAL ACCOUNTING

Recommendation:

From the analysis of remuneration structure of Healthscope group, it has been viewed

that the remuneration strategy is based on ownership that provided senior management with

the opportunity of receiving equity instruments as a component of long and short term

remuneration. Organization has made use of financial and non financial measures for

determining the performance pay. The remuneration framework for year 2017 was weighted

towards at risk remuneration. A clear link has been noticed between the performance of

company and outcomes of its incentive schemes for its senior executives. Remuneration of

executives is also determined by performing benchmarking exercise. However, it is required

on part of management of Healthscope to look at overall interaction when incorporating

shareholder engagement in determining the executive’s remuneration. Since, shareholder

engagement in determining remuneration of executives is regarded as essential to the good

corporate governance practices; there should be considerable involvement of shareholder

(Kanapathippillai et al. 2015). Furthermore, there should be well alignment between overall

performance and objective of remuneration reporting framework.

Conclusion:

The above discussed paper demonstrates the comparison and analysis of methods that

are used paying for performance by reviewing the annual report of Healthcsope and literature.

It is illustrated from reviewing the literature that computation of performance pay is done by

using various methods. It is depicted from annual report analysis of Healthscope that

disclosure relating to executive of remuneration is done according to applicable regulations

and legislations. Moreover, the incentive plan that is short term and long term incentive plan

and its outcome reflects the performance of organization. There is adequate amount of

disclosure regarding the measures of such incentive schemes. On contrary to this, the

methodology of allocation of executive remuneration is not disclosed properly. Some of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

MANAGERIAL ACCOUNTING

changes have been brought in current year regarding the weight age of schemes plan. From

the analysis, further conclusion can be drawn regarding the methods used for computing the

pay performance that there is considerable difference between the computation methods of

pay performance used by Healthscope and those discussed in literature. Hence, there is

difference between the theoretical and practical implications of the methods used for

performance pay due to the factors such as market data and other important factors.

MANAGERIAL ACCOUNTING

changes have been brought in current year regarding the weight age of schemes plan. From

the analysis, further conclusion can be drawn regarding the methods used for computing the

pay performance that there is considerable difference between the computation methods of

pay performance used by Healthscope and those discussed in literature. Hence, there is

difference between the theoretical and practical implications of the methods used for

performance pay due to the factors such as market data and other important factors.

15

MANAGERIAL ACCOUNTING

Reference list:

Adams, C.A., 2017. Conceptualising the contemporary corporate value creation

process. Accounting, Auditing & Accountability Journal, 30(4), pp.906-931.

Ahmed, A., Ng, C. and Delaney, D., 2015. Women on corporate boards and the incidence of

receiving a ‘strike’on the remuneration report. Corporate Ownership & Control, 12(4),

pp.261-272.

Bartram, T., Boyle, B., Stanton, P., Sablok, G. and Burgess, J., 2015. Performance and

reward practices of multinational corporations operating in Australia. Journal of Industrial

Relations, 57(2), pp.210-231.

Boer, H., Berger, A., Chapman, R. and Gertsen, F. eds., 2017. CI Changes from Suggestion

Box to Organisational Learning: Continuous Improvement in Europe and Australia:

Continuous Improvement in Europe and Australia. Routledge.

Chen, Y. and Jermias, J., 2014. Business strategy, executive compensation and firm

performance. Accounting & Finance, 54(1), pp.113-134.

Dumay, J., Frost, G. and Beck, C., 2015. Material legitimacy: blending organisational and

stakeholder concerns through non-financial information disclosures. Journal of Accounting &

Organizational Change, 11(1), pp.2-23.

Duong, L. and Evans, J., 2015. CFO compensation: Evidence from Australia. Pacific-Basin

Finance Journal, 35, pp.425-443.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

MANAGERIAL ACCOUNTING

Reference list:

Adams, C.A., 2017. Conceptualising the contemporary corporate value creation

process. Accounting, Auditing & Accountability Journal, 30(4), pp.906-931.

Ahmed, A., Ng, C. and Delaney, D., 2015. Women on corporate boards and the incidence of

receiving a ‘strike’on the remuneration report. Corporate Ownership & Control, 12(4),

pp.261-272.

Bartram, T., Boyle, B., Stanton, P., Sablok, G. and Burgess, J., 2015. Performance and

reward practices of multinational corporations operating in Australia. Journal of Industrial

Relations, 57(2), pp.210-231.

Boer, H., Berger, A., Chapman, R. and Gertsen, F. eds., 2017. CI Changes from Suggestion

Box to Organisational Learning: Continuous Improvement in Europe and Australia:

Continuous Improvement in Europe and Australia. Routledge.

Chen, Y. and Jermias, J., 2014. Business strategy, executive compensation and firm

performance. Accounting & Finance, 54(1), pp.113-134.

Dumay, J., Frost, G. and Beck, C., 2015. Material legitimacy: blending organisational and

stakeholder concerns through non-financial information disclosures. Journal of Accounting &

Organizational Change, 11(1), pp.2-23.

Duong, L. and Evans, J., 2015. CFO compensation: Evidence from Australia. Pacific-Basin

Finance Journal, 35, pp.425-443.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

16

MANAGERIAL ACCOUNTING

Healthscope.com.au. (2018). [online] Available at:

http://healthscope.com.au/application/files/3715/0344/5418/HS_Annual%20Report

%20FY17_v15_FA_low.pdf [Accessed 14 May 2018].

Kanapathippillai, S., Johl, S.K. and Wines, G., 2016. Remuneration committee effectiveness

and narrative remuneration disclosure. Pacific-Basin finance journal, 40, pp.384-402.

Leong, M.S.W., Paramasivam, A., Sundarasen, S. and Rajagopalan, U., 2015. Board

Composition and Companies’ Performance: Does Political Affiliation Moderate the

Relationship?. International Journal of Business and Management, 10(10), p.216.

Maas, K. and Rosendaal, S., 2016. Sustainability targets in executive remuneration: Targets,

time frame, country and sector specification. Business Strategy and the Environment, 25(6),

pp.390-401.

Moriarty, R., 2018. Asic highlights the importance of annual general meetings and recent

trends in corporate governance. Governance Directions, 70(2), p.77

Ndayisaba, G. and Ahmed, A., 2015. CEO remuneration, board composition and firm

performance: Empirical evidence from Australian listed companies. Corporate Ownership

and Control, 13(1), pp.534-552.

Pickering, M.E., 2017. Strategic decision making in publicly traded professional service

companies: an exploration of senior professional participation in acquisition decision

processes. Journal of Professions and Organization, 4(2), pp.179-202.

Qu, X., Percy, M., Stewart, J. and Hu, F., 2016. Executive stock option vesting conditions,

corporate governance and CEO attributes: evidence from Australia. Accounting & Finance.

Rao, K. and Tilt, C., 2015, November. Board Diversity and CSR Reporting: Australian

Evidence. In A-CSEAR 2015-Proceedings of the 14th Australasian Centre on Social and

MANAGERIAL ACCOUNTING

Healthscope.com.au. (2018). [online] Available at:

http://healthscope.com.au/application/files/3715/0344/5418/HS_Annual%20Report

%20FY17_v15_FA_low.pdf [Accessed 14 May 2018].

Kanapathippillai, S., Johl, S.K. and Wines, G., 2016. Remuneration committee effectiveness

and narrative remuneration disclosure. Pacific-Basin finance journal, 40, pp.384-402.

Leong, M.S.W., Paramasivam, A., Sundarasen, S. and Rajagopalan, U., 2015. Board

Composition and Companies’ Performance: Does Political Affiliation Moderate the

Relationship?. International Journal of Business and Management, 10(10), p.216.

Maas, K. and Rosendaal, S., 2016. Sustainability targets in executive remuneration: Targets,

time frame, country and sector specification. Business Strategy and the Environment, 25(6),

pp.390-401.

Moriarty, R., 2018. Asic highlights the importance of annual general meetings and recent

trends in corporate governance. Governance Directions, 70(2), p.77

Ndayisaba, G. and Ahmed, A., 2015. CEO remuneration, board composition and firm

performance: Empirical evidence from Australian listed companies. Corporate Ownership

and Control, 13(1), pp.534-552.

Pickering, M.E., 2017. Strategic decision making in publicly traded professional service

companies: an exploration of senior professional participation in acquisition decision

processes. Journal of Professions and Organization, 4(2), pp.179-202.

Qu, X., Percy, M., Stewart, J. and Hu, F., 2016. Executive stock option vesting conditions,

corporate governance and CEO attributes: evidence from Australia. Accounting & Finance.

Rao, K. and Tilt, C., 2015, November. Board Diversity and CSR Reporting: Australian

Evidence. In A-CSEAR 2015-Proceedings of the 14th Australasian Centre on Social and

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17

MANAGERIAL ACCOUNTING

Environmental Accounting Research Conference: A-CSEAR 2015 (p. 116). Academic

Conferences and publishing limited.

Riaz, Z., Ray, S. and Ray, P.K., 2015. Collibration as an alternative regulatory mechanism to

govern the disclosure of director and executive remuneration in Australia. International

Journal of Corporate Governance, 6(2-4), pp.241-274.

Safari, M., Cooper, B.J. and Dellaportas, S., 2016. The influence of remuneration structures

on financial reporting quality: evidence from Australia. Australian Accounting Review, 26(1),

pp.66-75.

Shamsabadi, H.A., Min, B.S. and Chung, R., 2016. Corporate governance and dividend

strategy: lessons from Australia. International Journal of Managerial Finance, 12(5), pp.583-

610.

Swan, P.L., 2016. Mandated divorce: company boards, incentives and performance.

MANAGERIAL ACCOUNTING

Environmental Accounting Research Conference: A-CSEAR 2015 (p. 116). Academic

Conferences and publishing limited.

Riaz, Z., Ray, S. and Ray, P.K., 2015. Collibration as an alternative regulatory mechanism to

govern the disclosure of director and executive remuneration in Australia. International

Journal of Corporate Governance, 6(2-4), pp.241-274.

Safari, M., Cooper, B.J. and Dellaportas, S., 2016. The influence of remuneration structures

on financial reporting quality: evidence from Australia. Australian Accounting Review, 26(1),

pp.66-75.

Shamsabadi, H.A., Min, B.S. and Chung, R., 2016. Corporate governance and dividend

strategy: lessons from Australia. International Journal of Managerial Finance, 12(5), pp.583-

610.

Swan, P.L., 2016. Mandated divorce: company boards, incentives and performance.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.