Managing Business Performance: Marginal and Standard Costing Analysis

VerifiedAdded on 2023/01/13

|13

|3360

|44

Report

AI Summary

This report analyzes the business performance of "Spark Footwear" using various performance management techniques. It begins with an application of marginal costing, calculating profit margins, break-even points, and margin of safety under different scenarios of selling price and variable cost changes. The report then transitions to standard costing, explaining its concept, procedures, and the importance of variance analysis. It details factors influencing both favorable and adverse material and labor variances, offering insights into how these variances impact a business. The report highlights the significance of standard costing as a control tool, emphasizing the importance of analyzing variances to improve operational efficiency and decision-making. The analysis provides valuable insights into the financial performance of the business and offers recommendations for improvement.

Managing Business

Performance

Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Statement of marginal costing showing 20 % profit on selling price..........................................1

2. and 3. Statement of marginal costing showing various changes in selling price and variable

cost...................................................................................................................................................2

4. Explanation of results and limitations of the exercise:......................................................6

PART 2............................................................................................................................................6

Explain the term of standard costing and procedure for standard costs.................................6

Different factors that lead in both adverse and favourable materials.....................................8

Critically analyse standard costing as a tool for control.........................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Statement of marginal costing showing 20 % profit on selling price..........................................1

2. and 3. Statement of marginal costing showing various changes in selling price and variable

cost...................................................................................................................................................2

4. Explanation of results and limitations of the exercise:......................................................6

PART 2............................................................................................................................................6

Explain the term of standard costing and procedure for standard costs.................................6

Different factors that lead in both adverse and favourable materials.....................................8

Critically analyse standard costing as a tool for control.........................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

A business management approach focuses on the operations as a whole rather than a

division level. The business performance management review on the overall business activities

and analysis of how to meet with organisational goals & objectives. To manage the performance

of business requirements it is required to apply different techniques of performance management.

It is essential for different activities in order to enhance sustainability and get success for a long

period of time. This assignment is based on the new footwear business which is “Spark

Footwear”. For performance management of new business application of different techniques

such as marginal costing, Break-even point and margin of safety is covered in this project

PART 1

1. Statement of marginal costing showing 20 % profit on selling price

Statement of marginal costing

1

A business management approach focuses on the operations as a whole rather than a

division level. The business performance management review on the overall business activities

and analysis of how to meet with organisational goals & objectives. To manage the performance

of business requirements it is required to apply different techniques of performance management.

It is essential for different activities in order to enhance sustainability and get success for a long

period of time. This assignment is based on the new footwear business which is “Spark

Footwear”. For performance management of new business application of different techniques

such as marginal costing, Break-even point and margin of safety is covered in this project

PART 1

1. Statement of marginal costing showing 20 % profit on selling price

Statement of marginal costing

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

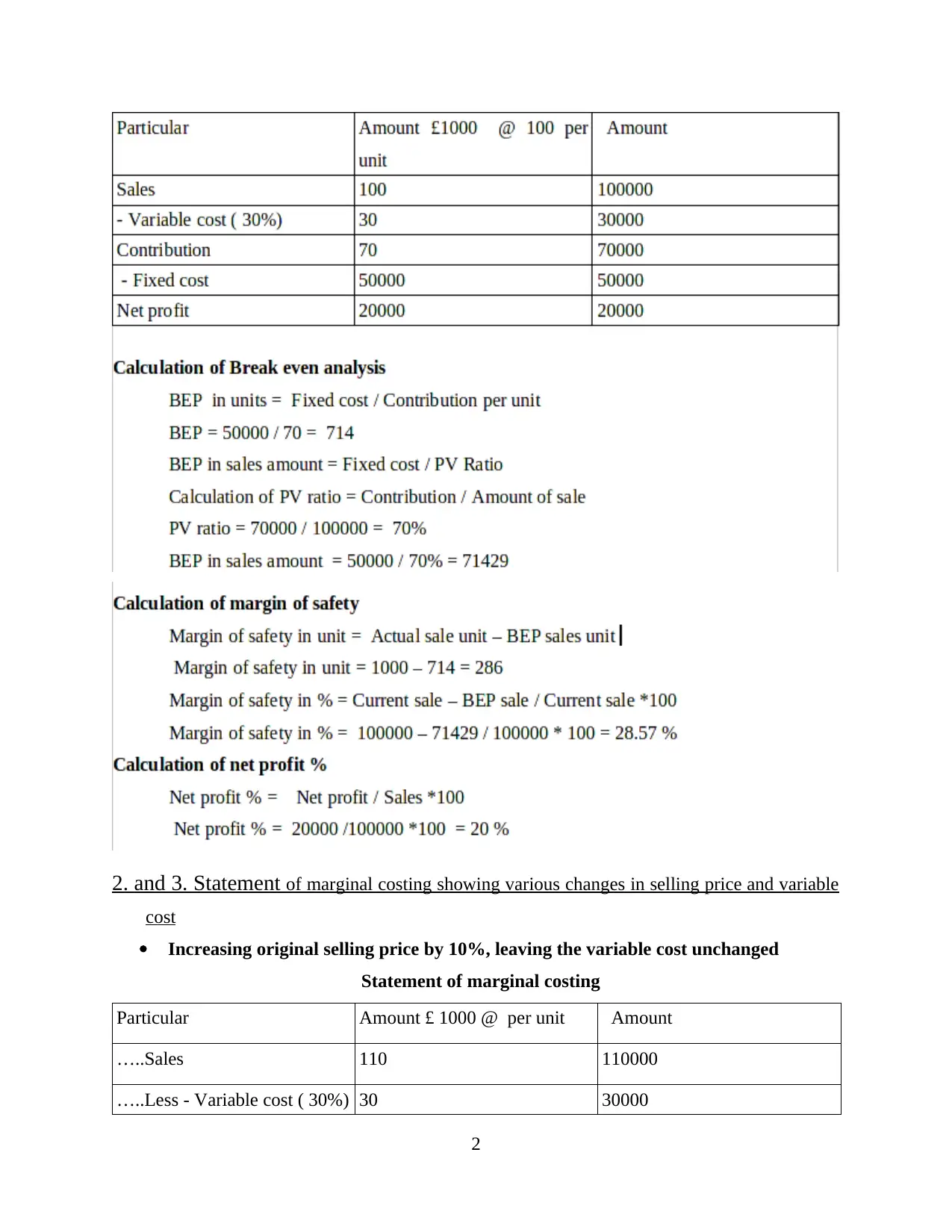

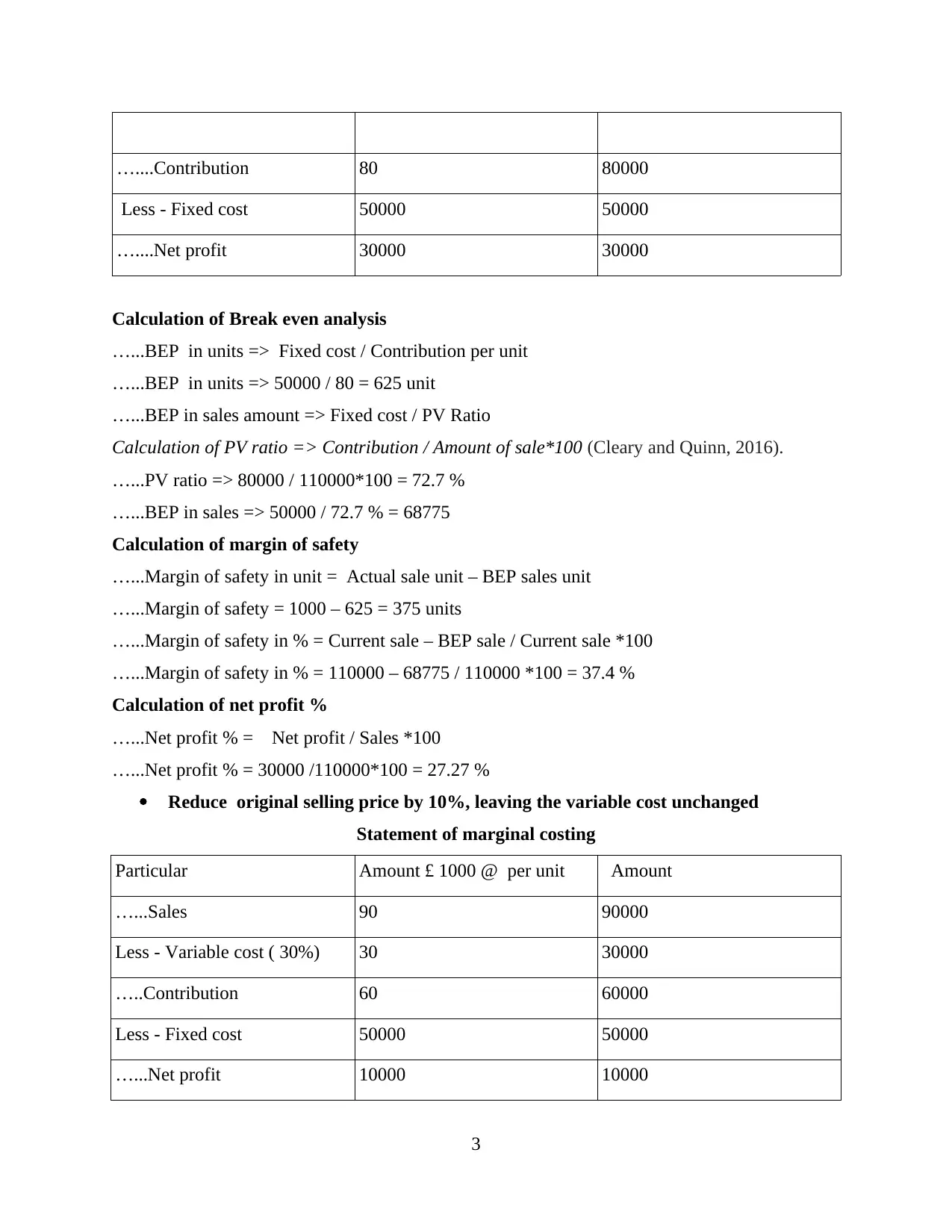

2. and 3. Statement of marginal costing showing various changes in selling price and variable

cost

Increasing original selling price by 10%, leaving the variable cost unchanged

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

…..Sales 110 110000

…..Less - Variable cost ( 30%) 30 30000

2

cost

Increasing original selling price by 10%, leaving the variable cost unchanged

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

…..Sales 110 110000

…..Less - Variable cost ( 30%) 30 30000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

…....Contribution 80 80000

Less - Fixed cost 50000 50000

…....Net profit 30000 30000

Calculation of Break even analysis

…...BEP in units => Fixed cost / Contribution per unit

…...BEP in units => 50000 / 80 = 625 unit

…...BEP in sales amount => Fixed cost / PV Ratio

Calculation of PV ratio => Contribution / Amount of sale*100 (Cleary and Quinn, 2016).

…...PV ratio => 80000 / 110000*100 = 72.7 %

…...BEP in sales => 50000 / 72.7 % = 68775

Calculation of margin of safety

…...Margin of safety in unit = Actual sale unit – BEP sales unit

…...Margin of safety = 1000 – 625 = 375 units

…...Margin of safety in % = Current sale – BEP sale / Current sale *100

…...Margin of safety in % = 110000 – 68775 / 110000 *100 = 37.4 %

Calculation of net profit %

…...Net profit % = Net profit / Sales *100

…...Net profit % = 30000 /110000*100 = 27.27 %

Reduce original selling price by 10%, leaving the variable cost unchanged

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

…...Sales 90 90000

Less - Variable cost ( 30%) 30 30000

…..Contribution 60 60000

Less - Fixed cost 50000 50000

…...Net profit 10000 10000

3

Less - Fixed cost 50000 50000

…....Net profit 30000 30000

Calculation of Break even analysis

…...BEP in units => Fixed cost / Contribution per unit

…...BEP in units => 50000 / 80 = 625 unit

…...BEP in sales amount => Fixed cost / PV Ratio

Calculation of PV ratio => Contribution / Amount of sale*100 (Cleary and Quinn, 2016).

…...PV ratio => 80000 / 110000*100 = 72.7 %

…...BEP in sales => 50000 / 72.7 % = 68775

Calculation of margin of safety

…...Margin of safety in unit = Actual sale unit – BEP sales unit

…...Margin of safety = 1000 – 625 = 375 units

…...Margin of safety in % = Current sale – BEP sale / Current sale *100

…...Margin of safety in % = 110000 – 68775 / 110000 *100 = 37.4 %

Calculation of net profit %

…...Net profit % = Net profit / Sales *100

…...Net profit % = 30000 /110000*100 = 27.27 %

Reduce original selling price by 10%, leaving the variable cost unchanged

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

…...Sales 90 90000

Less - Variable cost ( 30%) 30 30000

…..Contribution 60 60000

Less - Fixed cost 50000 50000

…...Net profit 10000 10000

3

Calculation of Break even analysis

…....BEP in units => Fixed cost / Contribution per unit

…....BEP in units => 50000 / 60 = 833 units

…....BEP in sales amount => Fixed cost / PV Ratio

…....Calculation of PV ratio => Contribution / Amount of sale*100

…....PV ratio = 60000 /90000*100 = 66.66 %

…....BEP in sales amount => 50000 / 66.66 % => 75000

Calculation of margin of safety

….....Margin of safety in unit => Actual sale unit – BEP sales unit ((Fasone Kofler and Scuderi,

2016).

….....Margin of safety => 1000 – 833 = 167 unit

…....Margin of safety in % => Current sale – BEP sale / Current sale *100

…....Margin of safety => 90000 – 75000 /90000*100 = 16.66 %

Calculation of net profit %

…..Net profit % => Net profit / Sales *100

…..Net profit % => 10000 / 90000*100 => 11.11 %

Using original selling price, reduce variable costs to 25% of the selling price

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

…..Sales 100 100000

Less - Variable cost ( 25 %) 25 25000

…...Contribution 75 75000

Less - Fixed cost 50000 50000

…...Net profit 25000 25000

Calculation of Break even analysis

BEP in units => Fixed cost / Contribution per unit

BEP in units => 50000 / 75 => 667 unit

BEP in sales amount => Fixed cost / PV Ratio (Haseeb and et.al., 2019).

Calculation of PV ratio => Contribution / Amount of sale*100

4

…....BEP in units => Fixed cost / Contribution per unit

…....BEP in units => 50000 / 60 = 833 units

…....BEP in sales amount => Fixed cost / PV Ratio

…....Calculation of PV ratio => Contribution / Amount of sale*100

…....PV ratio = 60000 /90000*100 = 66.66 %

…....BEP in sales amount => 50000 / 66.66 % => 75000

Calculation of margin of safety

….....Margin of safety in unit => Actual sale unit – BEP sales unit ((Fasone Kofler and Scuderi,

2016).

….....Margin of safety => 1000 – 833 = 167 unit

…....Margin of safety in % => Current sale – BEP sale / Current sale *100

…....Margin of safety => 90000 – 75000 /90000*100 = 16.66 %

Calculation of net profit %

…..Net profit % => Net profit / Sales *100

…..Net profit % => 10000 / 90000*100 => 11.11 %

Using original selling price, reduce variable costs to 25% of the selling price

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

…..Sales 100 100000

Less - Variable cost ( 25 %) 25 25000

…...Contribution 75 75000

Less - Fixed cost 50000 50000

…...Net profit 25000 25000

Calculation of Break even analysis

BEP in units => Fixed cost / Contribution per unit

BEP in units => 50000 / 75 => 667 unit

BEP in sales amount => Fixed cost / PV Ratio (Haseeb and et.al., 2019).

Calculation of PV ratio => Contribution / Amount of sale*100

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

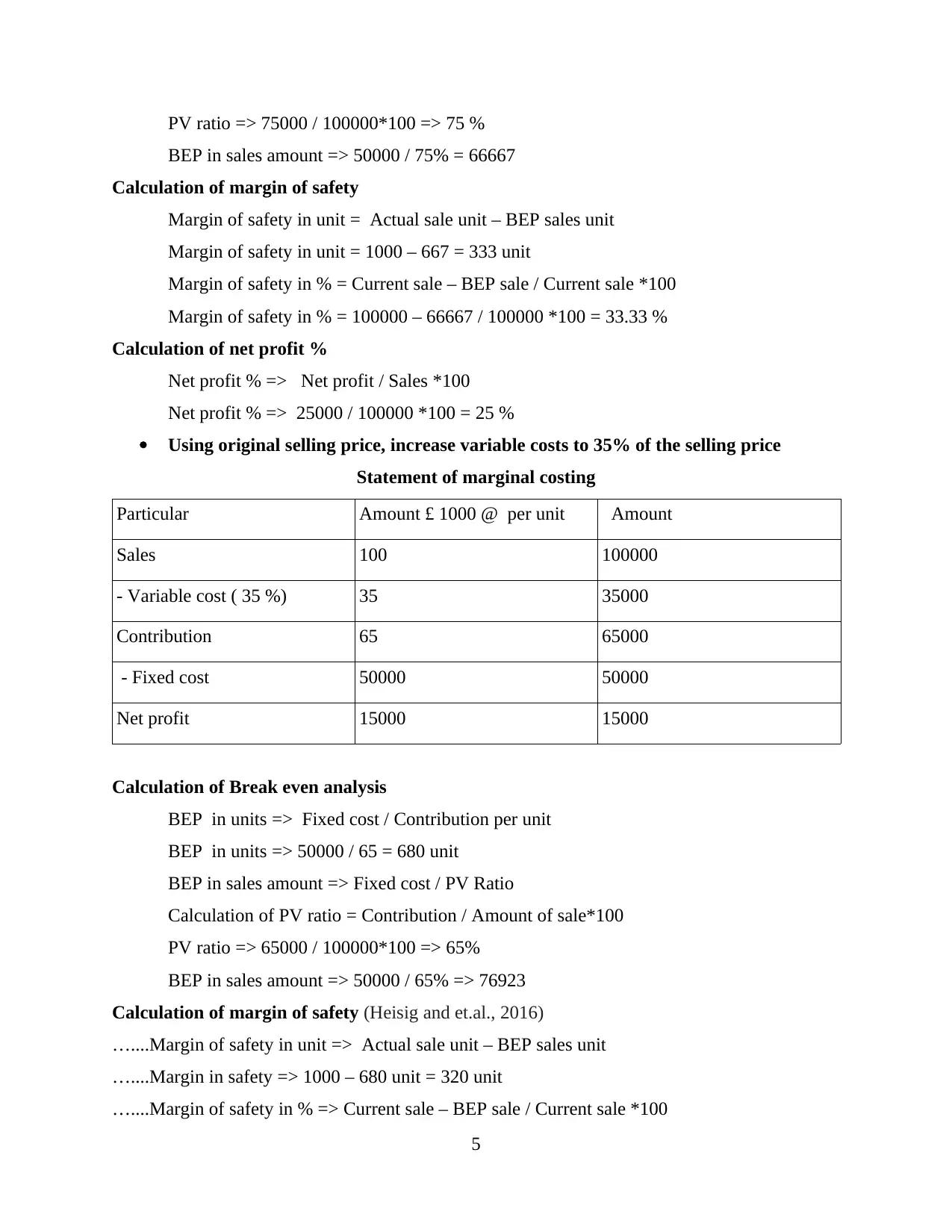

PV ratio => 75000 / 100000*100 => 75 %

BEP in sales amount => 50000 / 75% = 66667

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit

Margin of safety in unit = 1000 – 667 = 333 unit

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 100000 – 66667 / 100000 *100 = 33.33 %

Calculation of net profit %

Net profit % => Net profit / Sales *100

Net profit % => 25000 / 100000 *100 = 25 %

Using original selling price, increase variable costs to 35% of the selling price

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 100 100000

- Variable cost ( 35 %) 35 35000

Contribution 65 65000

- Fixed cost 50000 50000

Net profit 15000 15000

Calculation of Break even analysis

BEP in units => Fixed cost / Contribution per unit

BEP in units => 50000 / 65 = 680 unit

BEP in sales amount => Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale*100

PV ratio => 65000 / 100000*100 => 65%

BEP in sales amount => 50000 / 65% => 76923

Calculation of margin of safety (Heisig and et.al., 2016)

…....Margin of safety in unit => Actual sale unit – BEP sales unit

…....Margin in safety => 1000 – 680 unit = 320 unit

…....Margin of safety in % => Current sale – BEP sale / Current sale *100

5

BEP in sales amount => 50000 / 75% = 66667

Calculation of margin of safety

Margin of safety in unit = Actual sale unit – BEP sales unit

Margin of safety in unit = 1000 – 667 = 333 unit

Margin of safety in % = Current sale – BEP sale / Current sale *100

Margin of safety in % = 100000 – 66667 / 100000 *100 = 33.33 %

Calculation of net profit %

Net profit % => Net profit / Sales *100

Net profit % => 25000 / 100000 *100 = 25 %

Using original selling price, increase variable costs to 35% of the selling price

Statement of marginal costing

Particular Amount £ 1000 @ per unit Amount

Sales 100 100000

- Variable cost ( 35 %) 35 35000

Contribution 65 65000

- Fixed cost 50000 50000

Net profit 15000 15000

Calculation of Break even analysis

BEP in units => Fixed cost / Contribution per unit

BEP in units => 50000 / 65 = 680 unit

BEP in sales amount => Fixed cost / PV Ratio

Calculation of PV ratio = Contribution / Amount of sale*100

PV ratio => 65000 / 100000*100 => 65%

BEP in sales amount => 50000 / 65% => 76923

Calculation of margin of safety (Heisig and et.al., 2016)

…....Margin of safety in unit => Actual sale unit – BEP sales unit

…....Margin in safety => 1000 – 680 unit = 320 unit

…....Margin of safety in % => Current sale – BEP sale / Current sale *100

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

…....Margin of safety in % = 100000 – 76923 / 100000 *100 = 23.07 %

Calculation of net profit %

Net profit % => Net profit / Sales *100

Net profit % => 15000 / 100000 * 100 = 15%

4. Explanation of results and limitations of the exercise:

The marginal costing technique is part of costing that supports a business to recognise the

changes in profits with increment or decrease in production units. Such as, Spark footwear sale

out about 1000 units wit effective profit margin of 20% as a result they get BEP is 71429 and

margin of safety 28.57%. When selling price enhance so it is direct impact on the profitability

and increase PV ratio and net profit. The manager of company decide to increase variables cost

so it shows negative impact on PV ratio as well as margin ratio. After overall analysis there is

identified some limitation such as:

In this exercise does not consider factors during to calculation of profit margins.

Results are not using of short time period.

PART 2

Explain the term of standard costing and procedure for standard costs

Standard costing is a costing method which is applied by the business to compare

standard costs and revenues with actual outcomes. In case of succeeding at the variances with a

reason of informing the administration in regard of fluctuation and take right measures for the

development. It is related to the different variances which are important for management of

operational activities. When variances occur in business then at that time management became

aware of the manufacturing costs that have varied from the standard costs. It is applied by the

Spark Footwear to find out differences between actual and budgeted cost unit.

The term, standard cost mainly defines about the expected cost per unit to manufacture

footwear in particular period of time. The main purpose of this cost is to measure the

performance, control the fluctuations, analyse the value of stock and set up the selling price of

each product to prepare a quotation.

Establishment of standards: It is a first step in which managers establish standards as per

the reason for comparison with actual costs. For this system, a standard can be set by

administration on estimation basis. To set up these costs managers require more weight

6

Calculation of net profit %

Net profit % => Net profit / Sales *100

Net profit % => 15000 / 100000 * 100 = 15%

4. Explanation of results and limitations of the exercise:

The marginal costing technique is part of costing that supports a business to recognise the

changes in profits with increment or decrease in production units. Such as, Spark footwear sale

out about 1000 units wit effective profit margin of 20% as a result they get BEP is 71429 and

margin of safety 28.57%. When selling price enhance so it is direct impact on the profitability

and increase PV ratio and net profit. The manager of company decide to increase variables cost

so it shows negative impact on PV ratio as well as margin ratio. After overall analysis there is

identified some limitation such as:

In this exercise does not consider factors during to calculation of profit margins.

Results are not using of short time period.

PART 2

Explain the term of standard costing and procedure for standard costs

Standard costing is a costing method which is applied by the business to compare

standard costs and revenues with actual outcomes. In case of succeeding at the variances with a

reason of informing the administration in regard of fluctuation and take right measures for the

development. It is related to the different variances which are important for management of

operational activities. When variances occur in business then at that time management became

aware of the manufacturing costs that have varied from the standard costs. It is applied by the

Spark Footwear to find out differences between actual and budgeted cost unit.

The term, standard cost mainly defines about the expected cost per unit to manufacture

footwear in particular period of time. The main purpose of this cost is to measure the

performance, control the fluctuations, analyse the value of stock and set up the selling price of

each product to prepare a quotation.

Establishment of standards: It is a first step in which managers establish standards as per

the reason for comparison with actual costs. For this system, a standard can be set by

administration on estimation basis. To set up these costs managers require more weight

6

which is mainly based on the past data, the current plan and future trends, Moreover,

these standards are fixed in both costs and quantity. The Spark Footwear also set up

standards for standard cost in order to compare the actual and budgeted cost. It may be

traced from the average direction of the footwear industry.

Determination of actual cost: After setting the standard it is required to conduct an

analysis of each element like material, labours and overheads. For determination of them

it is required to use wages sheets, invoices, account book and many more. With the help

of it, Spark Footwear get aware of all the production cost that is categorised into the

material, labour and overheads.

Comparison of actual cost with a standard cost: In next step manager requires to

compare actual cost with the standard cost to analyse the differences. Through this

variance analysis, the actual performance of a business could be determined and

according to that effective decisions could be made. If these variances are favourable then

these are good for the company adverse variance shows weak estimation power of

organisation. Like, Spark Footwear has equivalenced the actual costs with budgeted cost

to get the result of favourable and adverse variances.

Determination of causes: After the examination, in the next step it is required to find out

the causes for the variances to take the right action. Managers apply all the modifications

to analyse the overall performance of business. Spark Footwear faces the problem of

differences and at that time managers search reason and take the right action to enhance

the performance of business.

Disposition of variances: At the end of this procedure management take decision of

disposition of variances by moving the costing profit and loss account. The Spark

footwear is required to be assured about the disposition of variances.

The term of standard costing can help to determine the profit margin of business at

different phases of production. Moreover, it is useful in practical management functions like

planning as well as controlling.

7

these standards are fixed in both costs and quantity. The Spark Footwear also set up

standards for standard cost in order to compare the actual and budgeted cost. It may be

traced from the average direction of the footwear industry.

Determination of actual cost: After setting the standard it is required to conduct an

analysis of each element like material, labours and overheads. For determination of them

it is required to use wages sheets, invoices, account book and many more. With the help

of it, Spark Footwear get aware of all the production cost that is categorised into the

material, labour and overheads.

Comparison of actual cost with a standard cost: In next step manager requires to

compare actual cost with the standard cost to analyse the differences. Through this

variance analysis, the actual performance of a business could be determined and

according to that effective decisions could be made. If these variances are favourable then

these are good for the company adverse variance shows weak estimation power of

organisation. Like, Spark Footwear has equivalenced the actual costs with budgeted cost

to get the result of favourable and adverse variances.

Determination of causes: After the examination, in the next step it is required to find out

the causes for the variances to take the right action. Managers apply all the modifications

to analyse the overall performance of business. Spark Footwear faces the problem of

differences and at that time managers search reason and take the right action to enhance

the performance of business.

Disposition of variances: At the end of this procedure management take decision of

disposition of variances by moving the costing profit and loss account. The Spark

footwear is required to be assured about the disposition of variances.

The term of standard costing can help to determine the profit margin of business at

different phases of production. Moreover, it is useful in practical management functions like

planning as well as controlling.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

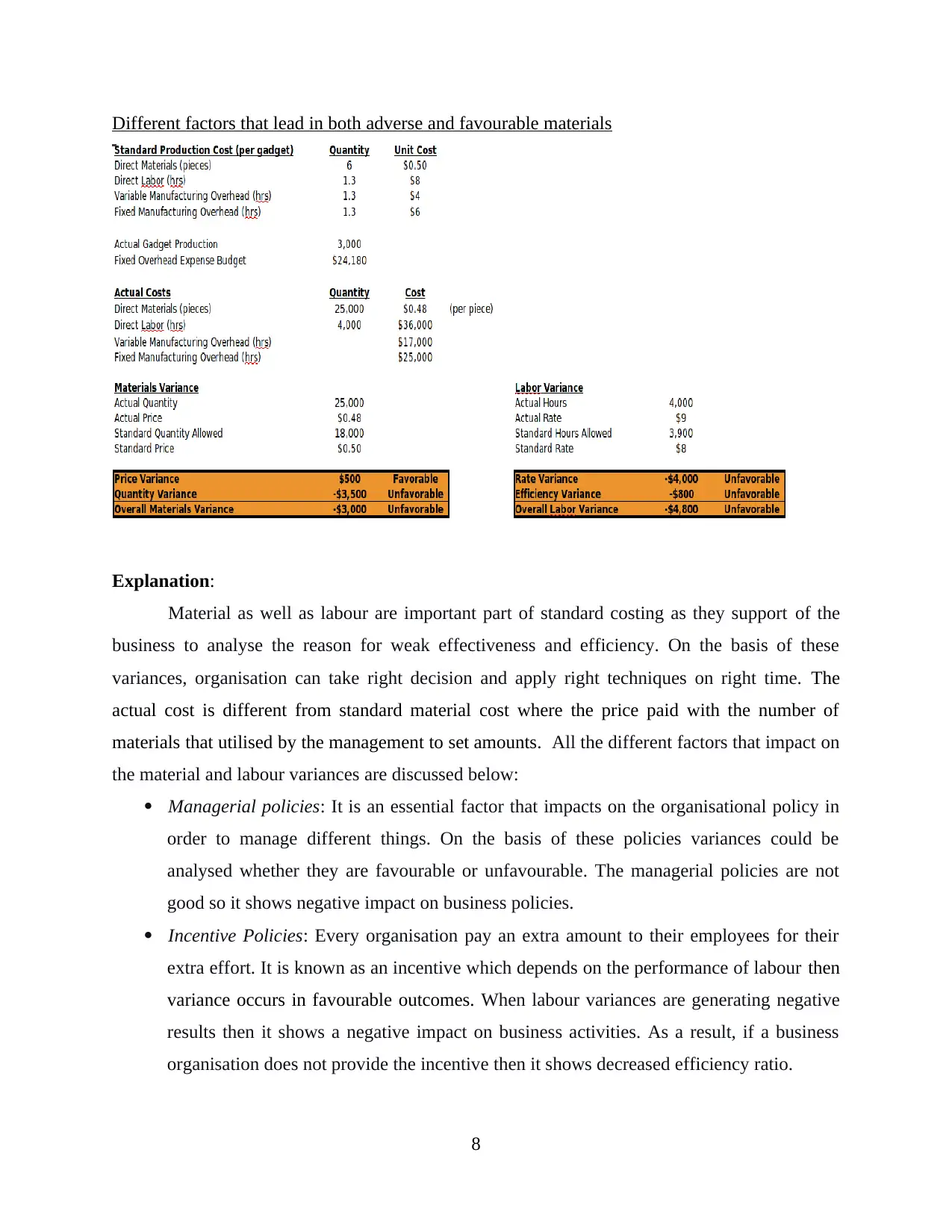

Different factors that lead in both adverse and favourable materials

Explanation:

Material as well as labour are important part of standard costing as they support of the

business to analyse the reason for weak effectiveness and efficiency. On the basis of these

variances, organisation can take right decision and apply right techniques on right time. The

actual cost is different from standard material cost where the price paid with the number of

materials that utilised by the management to set amounts. All the different factors that impact on

the material and labour variances are discussed below:

Managerial policies: It is an essential factor that impacts on the organisational policy in

order to manage different things. On the basis of these policies variances could be

analysed whether they are favourable or unfavourable. The managerial policies are not

good so it shows negative impact on business policies.

Incentive Policies: Every organisation pay an extra amount to their employees for their

extra effort. It is known as an incentive which depends on the performance of labour then

variance occurs in favourable outcomes. When labour variances are generating negative

results then it shows a negative impact on business activities. As a result, if a business

organisation does not provide the incentive then it shows decreased efficiency ratio.

8

Explanation:

Material as well as labour are important part of standard costing as they support of the

business to analyse the reason for weak effectiveness and efficiency. On the basis of these

variances, organisation can take right decision and apply right techniques on right time. The

actual cost is different from standard material cost where the price paid with the number of

materials that utilised by the management to set amounts. All the different factors that impact on

the material and labour variances are discussed below:

Managerial policies: It is an essential factor that impacts on the organisational policy in

order to manage different things. On the basis of these policies variances could be

analysed whether they are favourable or unfavourable. The managerial policies are not

good so it shows negative impact on business policies.

Incentive Policies: Every organisation pay an extra amount to their employees for their

extra effort. It is known as an incentive which depends on the performance of labour then

variance occurs in favourable outcomes. When labour variances are generating negative

results then it shows a negative impact on business activities. As a result, if a business

organisation does not provide the incentive then it shows decreased efficiency ratio.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quality of raw material: The material variances are based on the quality of raw material

in which quality ratio is calculated which helps to determine that operations are

generating positive outcomes in favour of business activities. When Spark Footwear will

use the low quality of material then it will show a negative impact on organisation

occurrence.

Effective operating cycle period: To circulate the procedure of operating cycle period is

short so present effect variances in a positive manner. On the other side, it takes a long

time in this cycle so it presents a negative impact on business activities. As per this

example, it is analysed that there are material as well as labour variances and both are

unfavourable that means operating life cycle takes more time for a particular procedure.

Critically analyse standard costing as a tool for control

Standard costing is an effective tool which is applied by administration in certain period

of time. This tool is helping an organisation in planning, controlling and decision making in the

operation of a business. It is analysed that standard costing technique is applied in business

because it acts as an instrument of encouraging the staff, preventing wastages and increasing

productivity. As a result standard costing is applied by Spark Footwear in adequate manner

which will help the managers to determine deduction in unplanned cost and enhance profitability

level of organisation. With the help of this term a business take right decision on time. Along

with that control all those activities which are not appropriate for a business.

When an organisation apply standard costing technique the at that time managers

compare standard cost with actual cost and get variances in positive as well as negative manner.

If negative results are analysed then managers must take action and control the cost. In positive

manner follow the particular cost structure. So it is understood that standard costing is working

as a controlling tool which control all business activities in appropriate manner. There are

different advantages using standard costing as management tool and all of them are as follows: Fixing of standard price: The standard price is fixed for stock as raw material and

finished goods which are keeping for sale. Furthermore, profit planning is also finished

with the support of standard costing. Comparison and analysis of data: When standard are set that time standards can be

compared with actual to find the variances. The reason of occur these variances that

9

in which quality ratio is calculated which helps to determine that operations are

generating positive outcomes in favour of business activities. When Spark Footwear will

use the low quality of material then it will show a negative impact on organisation

occurrence.

Effective operating cycle period: To circulate the procedure of operating cycle period is

short so present effect variances in a positive manner. On the other side, it takes a long

time in this cycle so it presents a negative impact on business activities. As per this

example, it is analysed that there are material as well as labour variances and both are

unfavourable that means operating life cycle takes more time for a particular procedure.

Critically analyse standard costing as a tool for control

Standard costing is an effective tool which is applied by administration in certain period

of time. This tool is helping an organisation in planning, controlling and decision making in the

operation of a business. It is analysed that standard costing technique is applied in business

because it acts as an instrument of encouraging the staff, preventing wastages and increasing

productivity. As a result standard costing is applied by Spark Footwear in adequate manner

which will help the managers to determine deduction in unplanned cost and enhance profitability

level of organisation. With the help of this term a business take right decision on time. Along

with that control all those activities which are not appropriate for a business.

When an organisation apply standard costing technique the at that time managers

compare standard cost with actual cost and get variances in positive as well as negative manner.

If negative results are analysed then managers must take action and control the cost. In positive

manner follow the particular cost structure. So it is understood that standard costing is working

as a controlling tool which control all business activities in appropriate manner. There are

different advantages using standard costing as management tool and all of them are as follows: Fixing of standard price: The standard price is fixed for stock as raw material and

finished goods which are keeping for sale. Furthermore, profit planning is also finished

with the support of standard costing. Comparison and analysis of data: When standard are set that time standards can be

compared with actual to find the variances. The reason of occur these variances that

9

internal as well as external factors impact on the business performance. So according to

that business take right decision on right time. Emphasis on cost: The behaviour of people impact on the management, staff members

and workers in order to change cost. Besides, this time incentive scheme is working

properly on basis of standard technique. Better forecasting: The main reason of probable variances are interpreted in the

circumstance to develop effective budget. This budget can supports in better forecasting

of sales be made very effectively.

Reduce the costs: For the raw standard price is fixed and standard rate is fixed for labour.

Standards are fixed where variable overhead as well as fixed variable separately. It is a

good way to control cost effectively.

CONCLUSION

As per the above report it has been articulated that to manage the performance of

business in proper manner to apply effective techniques that compare the actual and standard

cost. Through comparison get the result as variances that occur in business with reason of

internal and external factors that impact on the business performance. The standard costing

technique working as a controlling tool which is analysed all the cost of material and labour and

according to that company take appropriate action.

10

that business take right decision on right time. Emphasis on cost: The behaviour of people impact on the management, staff members

and workers in order to change cost. Besides, this time incentive scheme is working

properly on basis of standard technique. Better forecasting: The main reason of probable variances are interpreted in the

circumstance to develop effective budget. This budget can supports in better forecasting

of sales be made very effectively.

Reduce the costs: For the raw standard price is fixed and standard rate is fixed for labour.

Standards are fixed where variable overhead as well as fixed variable separately. It is a

good way to control cost effectively.

CONCLUSION

As per the above report it has been articulated that to manage the performance of

business in proper manner to apply effective techniques that compare the actual and standard

cost. Through comparison get the result as variances that occur in business with reason of

internal and external factors that impact on the business performance. The standard costing

technique working as a controlling tool which is analysed all the cost of material and labour and

according to that company take appropriate action.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.