Managing Financial Resources and Performance

VerifiedAdded on 2023/03/17

|12

|3096

|20

AI Summary

This report analyzes the financial performance of Vodafone for the years 2016 and 2017, comparing it with its competitor Deutsche Telekom. It examines various financial ratios and highlights the areas of concern for Vodafone. The report also discusses the reasons behind the difference in performance and suggests that Vodafone should be concerned about Deutsche Telekom's performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGING FINANCIAL RESOURCES AND PERFORMANCE

Managing financial resources and performance

Name of the student

Name of the university

Student ID

Author note

Managing financial resources and performance

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGING FINANCIAL RESOURCES AND PERFORMANCE

Table of Contents

Introduction......................................................................................................................................2

Task 1 – Finding financial performance..........................................................................................2

Task 2 – financial analysis...............................................................................................................4

Performance of Vodafone................................................................................................................4

Performance of Deutsche Telekom.................................................................................................6

Reason of difference in performance...............................................................................................6

Vodafone to be concerned about Deutsche Telekom......................................................................8

Conclusion.......................................................................................................................................8

Reference.......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................2

Task 1 – Finding financial performance..........................................................................................2

Task 2 – financial analysis...............................................................................................................4

Performance of Vodafone................................................................................................................4

Performance of Deutsche Telekom.................................................................................................6

Reason of difference in performance...............................................................................................6

Vodafone to be concerned about Deutsche Telekom......................................................................8

Conclusion.......................................................................................................................................8

Reference.......................................................................................................................................10

2MANAGING FINANCIAL RESOURCES AND PERFORMANCE

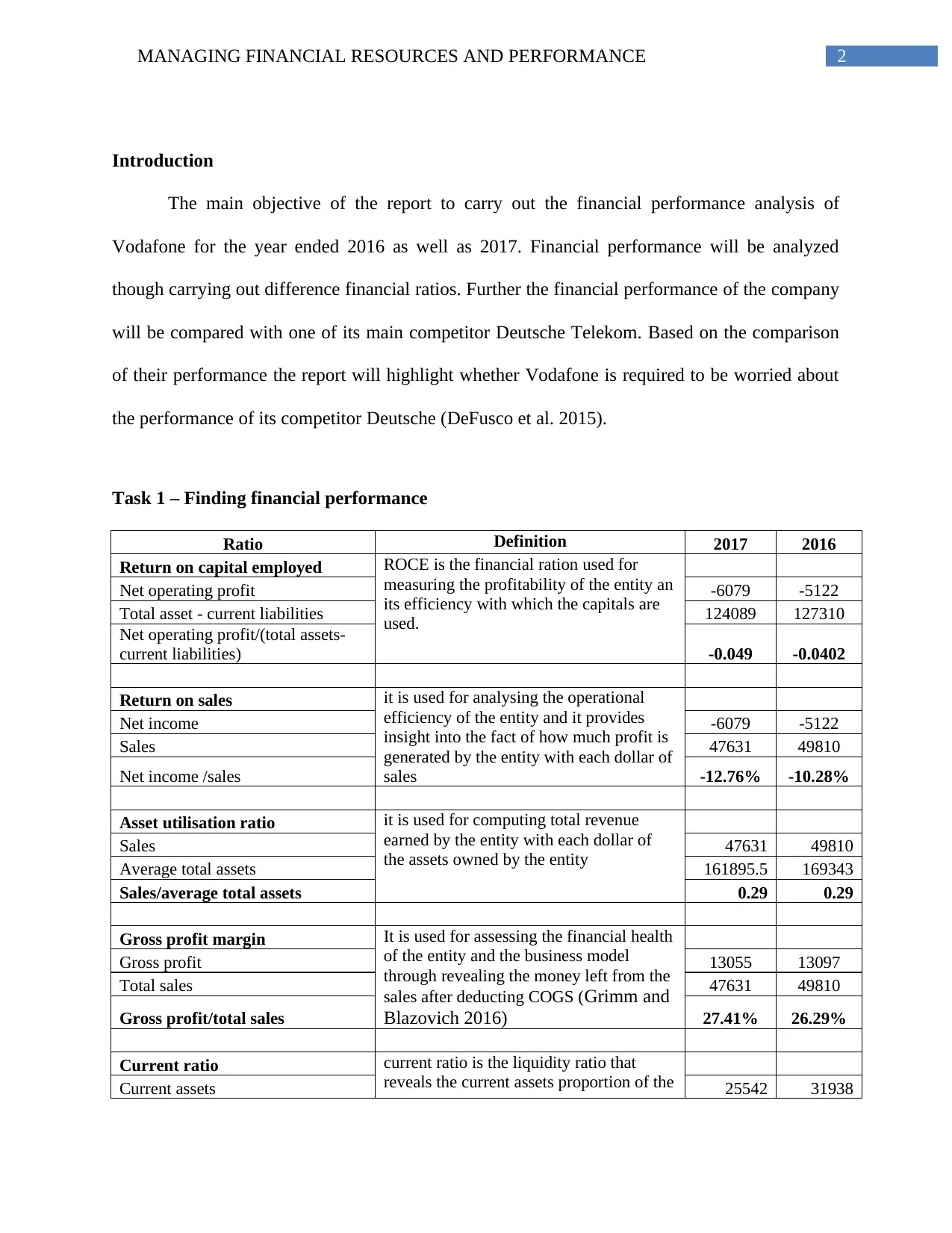

Introduction

The main objective of the report to carry out the financial performance analysis of

Vodafone for the year ended 2016 as well as 2017. Financial performance will be analyzed

though carrying out difference financial ratios. Further the financial performance of the company

will be compared with one of its main competitor Deutsche Telekom. Based on the comparison

of their performance the report will highlight whether Vodafone is required to be worried about

the performance of its competitor Deutsche (DeFusco et al. 2015).

Task 1 – Finding financial performance

Ratio Definition 2017 2016

Return on capital employed ROCE is the financial ration used for

measuring the profitability of the entity an

its efficiency with which the capitals are

used.

Net operating profit -6079 -5122

Total asset - current liabilities 124089 127310

Net operating profit/(total assets-

current liabilities) -0.049 -0.0402

Return on sales it is used for analysing the operational

efficiency of the entity and it provides

insight into the fact of how much profit is

generated by the entity with each dollar of

sales

Net income -6079 -5122

Sales 47631 49810

Net income /sales -12.76% -10.28%

Asset utilisation ratio it is used for computing total revenue

earned by the entity with each dollar of

the assets owned by the entity

Sales 47631 49810

Average total assets 161895.5 169343

Sales/average total assets 0.29 0.29

Gross profit margin It is used for assessing the financial health

of the entity and the business model

through revealing the money left from the

sales after deducting COGS (Grimm and

Blazovich 2016)

Gross profit 13055 13097

Total sales 47631 49810

Gross profit/total sales 27.41% 26.29%

Current ratio current ratio is the liquidity ratio that

reveals the current assets proportion of theCurrent assets 25542 31938

Introduction

The main objective of the report to carry out the financial performance analysis of

Vodafone for the year ended 2016 as well as 2017. Financial performance will be analyzed

though carrying out difference financial ratios. Further the financial performance of the company

will be compared with one of its main competitor Deutsche Telekom. Based on the comparison

of their performance the report will highlight whether Vodafone is required to be worried about

the performance of its competitor Deutsche (DeFusco et al. 2015).

Task 1 – Finding financial performance

Ratio Definition 2017 2016

Return on capital employed ROCE is the financial ration used for

measuring the profitability of the entity an

its efficiency with which the capitals are

used.

Net operating profit -6079 -5122

Total asset - current liabilities 124089 127310

Net operating profit/(total assets-

current liabilities) -0.049 -0.0402

Return on sales it is used for analysing the operational

efficiency of the entity and it provides

insight into the fact of how much profit is

generated by the entity with each dollar of

sales

Net income -6079 -5122

Sales 47631 49810

Net income /sales -12.76% -10.28%

Asset utilisation ratio it is used for computing total revenue

earned by the entity with each dollar of

the assets owned by the entity

Sales 47631 49810

Average total assets 161895.5 169343

Sales/average total assets 0.29 0.29

Gross profit margin It is used for assessing the financial health

of the entity and the business model

through revealing the money left from the

sales after deducting COGS (Grimm and

Blazovich 2016)

Gross profit 13055 13097

Total sales 47631 49810

Gross profit/total sales 27.41% 26.29%

Current ratio current ratio is the liquidity ratio that

reveals the current assets proportion of theCurrent assets 25542 31938

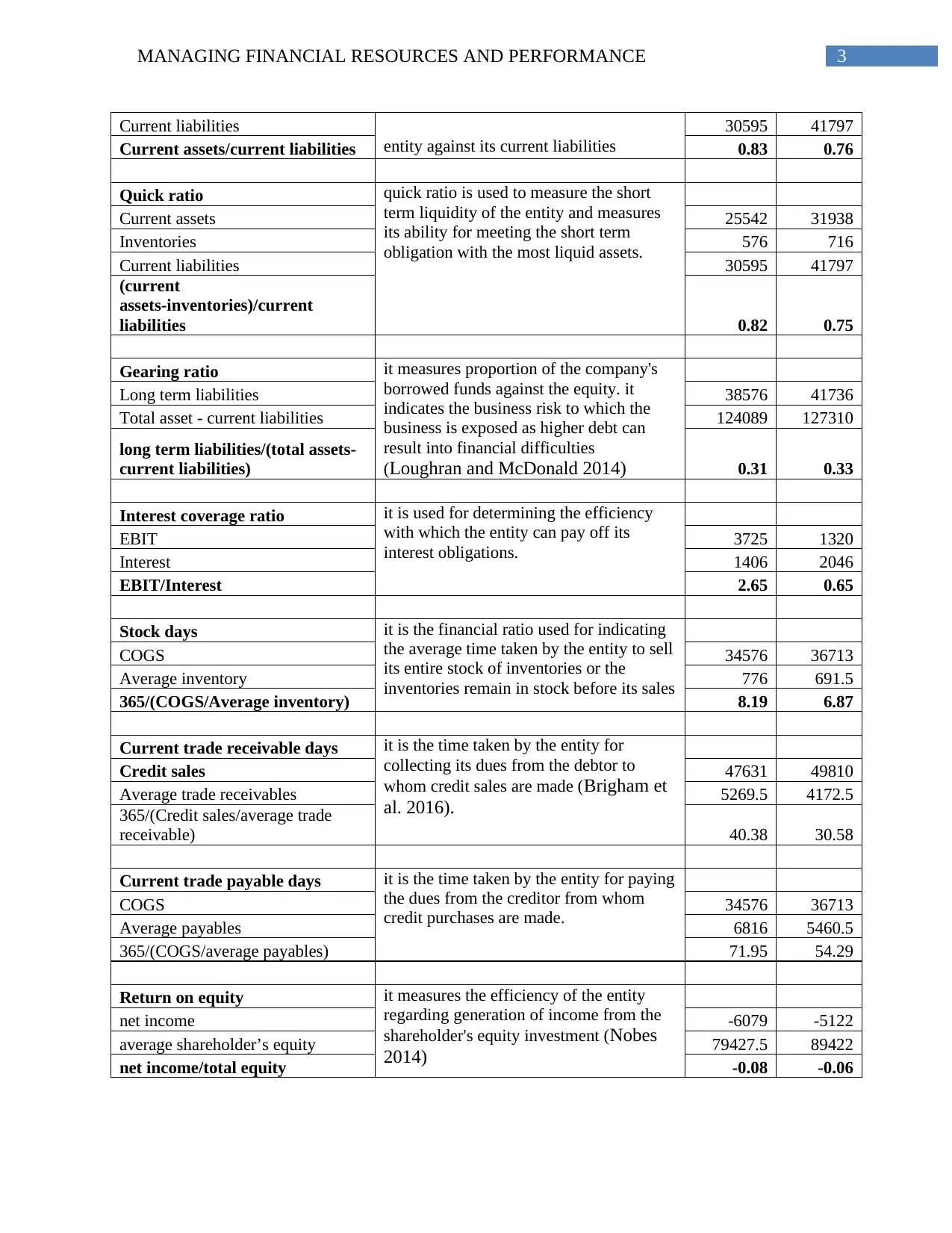

3MANAGING FINANCIAL RESOURCES AND PERFORMANCE

entity against its current liabilities

Current liabilities 30595 41797

Current assets/current liabilities 0.83 0.76

Quick ratio quick ratio is used to measure the short

term liquidity of the entity and measures

its ability for meeting the short term

obligation with the most liquid assets.

Current assets 25542 31938

Inventories 576 716

Current liabilities 30595 41797

(current

assets-inventories)/current

liabilities 0.82 0.75

Gearing ratio it measures proportion of the company's

borrowed funds against the equity. it

indicates the business risk to which the

business is exposed as higher debt can

result into financial difficulties

(Loughran and McDonald 2014)

Long term liabilities 38576 41736

Total asset - current liabilities 124089 127310

long term liabilities/(total assets-

current liabilities) 0.31 0.33

Interest coverage ratio it is used for determining the efficiency

with which the entity can pay off its

interest obligations.

EBIT 3725 1320

Interest 1406 2046

EBIT/Interest 2.65 0.65

Stock days it is the financial ratio used for indicating

the average time taken by the entity to sell

its entire stock of inventories or the

inventories remain in stock before its sales

COGS 34576 36713

Average inventory 776 691.5

365/(COGS/Average inventory) 8.19 6.87

Current trade receivable days it is the time taken by the entity for

collecting its dues from the debtor to

whom credit sales are made (Brigham et

al. 2016).

Credit sales 47631 49810

Average trade receivables 5269.5 4172.5

365/(Credit sales/average trade

receivable) 40.38 30.58

Current trade payable days it is the time taken by the entity for paying

the dues from the creditor from whom

credit purchases are made.

COGS 34576 36713

Average payables 6816 5460.5

365/(COGS/average payables) 71.95 54.29

Return on equity it measures the efficiency of the entity

regarding generation of income from the

shareholder's equity investment (Nobes

2014)

net income -6079 -5122

average shareholder’s equity 79427.5 89422

net income/total equity -0.08 -0.06

entity against its current liabilities

Current liabilities 30595 41797

Current assets/current liabilities 0.83 0.76

Quick ratio quick ratio is used to measure the short

term liquidity of the entity and measures

its ability for meeting the short term

obligation with the most liquid assets.

Current assets 25542 31938

Inventories 576 716

Current liabilities 30595 41797

(current

assets-inventories)/current

liabilities 0.82 0.75

Gearing ratio it measures proportion of the company's

borrowed funds against the equity. it

indicates the business risk to which the

business is exposed as higher debt can

result into financial difficulties

(Loughran and McDonald 2014)

Long term liabilities 38576 41736

Total asset - current liabilities 124089 127310

long term liabilities/(total assets-

current liabilities) 0.31 0.33

Interest coverage ratio it is used for determining the efficiency

with which the entity can pay off its

interest obligations.

EBIT 3725 1320

Interest 1406 2046

EBIT/Interest 2.65 0.65

Stock days it is the financial ratio used for indicating

the average time taken by the entity to sell

its entire stock of inventories or the

inventories remain in stock before its sales

COGS 34576 36713

Average inventory 776 691.5

365/(COGS/Average inventory) 8.19 6.87

Current trade receivable days it is the time taken by the entity for

collecting its dues from the debtor to

whom credit sales are made (Brigham et

al. 2016).

Credit sales 47631 49810

Average trade receivables 5269.5 4172.5

365/(Credit sales/average trade

receivable) 40.38 30.58

Current trade payable days it is the time taken by the entity for paying

the dues from the creditor from whom

credit purchases are made.

COGS 34576 36713

Average payables 6816 5460.5

365/(COGS/average payables) 71.95 54.29

Return on equity it measures the efficiency of the entity

regarding generation of income from the

shareholder's equity investment (Nobes

2014)

net income -6079 -5122

average shareholder’s equity 79427.5 89422

net income/total equity -0.08 -0.06

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGING FINANCIAL RESOURCES AND PERFORMANCE

Task 2 – financial analysis

Performance of Vodafone

2017 was a solid year for the company in context of financial performance as it was able

to deliver commercial momentum with the underlying sustained growth. With recovery of the

European revenues and strong continuous growth in Middle East and African operations the

entity was able to meet the financial guidance and was able to increase the dividend per share by

2%. Further, if the cash generation is consideration it is viewed as the key for delivering strong

return to the shareholders. It was able to deliver € 4.1 billion amount of free cash flow during the

year 2017 that was significantly higher as compared to € 1.3 billion of 2016 (Vodafone.com

2019)

Looking into the results of ratio computed in part 1, it can be identified that the company

was not able to generate profits for both 2016 as well as 2017 and hence, it was not able to create

return on its capital employed. Further, the return on capital employed of the company has been

further deteriorated in 2017 as compared to the year 2016. Further, the net of the company for

the years led to negative margin o n sales (Rohman and Bohlin 2014). Further the notable fact is

that the net loss margin has increased to 12/76% in 2017 as compared to 10.28% in 2016. It is

signifying that the company could not make any improvement to its performance for earning

profits from sales. Asset utilization ratio of the company has been same in 2017 as it was in

2016. Asset utilization is crucial to any entity as the success of the entity is generally tied with

the ability for managing the leveraging the assets. Optimal asset utilization ratio signifies that the

entity is more efficient with each dollar of the asset held by it (Robinson et al. 2015). However,

Vodafone was not able to improve its asset utilization ability and it was maintained at the same

Task 2 – financial analysis

Performance of Vodafone

2017 was a solid year for the company in context of financial performance as it was able

to deliver commercial momentum with the underlying sustained growth. With recovery of the

European revenues and strong continuous growth in Middle East and African operations the

entity was able to meet the financial guidance and was able to increase the dividend per share by

2%. Further, if the cash generation is consideration it is viewed as the key for delivering strong

return to the shareholders. It was able to deliver € 4.1 billion amount of free cash flow during the

year 2017 that was significantly higher as compared to € 1.3 billion of 2016 (Vodafone.com

2019)

Looking into the results of ratio computed in part 1, it can be identified that the company

was not able to generate profits for both 2016 as well as 2017 and hence, it was not able to create

return on its capital employed. Further, the return on capital employed of the company has been

further deteriorated in 2017 as compared to the year 2016. Further, the net of the company for

the years led to negative margin o n sales (Rohman and Bohlin 2014). Further the notable fact is

that the net loss margin has increased to 12/76% in 2017 as compared to 10.28% in 2016. It is

signifying that the company could not make any improvement to its performance for earning

profits from sales. Asset utilization ratio of the company has been same in 2017 as it was in

2016. Asset utilization is crucial to any entity as the success of the entity is generally tied with

the ability for managing the leveraging the assets. Optimal asset utilization ratio signifies that the

entity is more efficient with each dollar of the asset held by it (Robinson et al. 2015). However,

Vodafone was not able to improve its asset utilization ability and it was maintained at the same

5MANAGING FINANCIAL RESOURCES AND PERFORMANCE

rate in 2017 too. Gross profit margin of the entity is satisfactory and moreover the company was

able to enhance the same in 2017 as compared to 2016. It is identified that the gross profit

margin has been improved as the entity was able to reduce the cost of sales. Looking into the

liquidity ratio it can be stated that the liquidity ratios of at least more than 1 signifies that the

current assets of the company are sufficient to pay off the short term obligation upon becoming

due (Easton and Sommers 2018). However, the current ratio and quick ratio of the company for

both the years that is 2016 as well as 2017 is below 1 that is indicating that the company is not

able to pay off its short term obligations when they will become due. Gearing ratio that is used

for measuring the equity of the owners as compared to debt or borrowed funds indicating that the

company is lower leveraged as the same for the entity in 2016 is 0.33 and further improved to

0.31 in the year 2017. If the efficiency level of the company is taken into consideration it can be

identified that during 2016 the entity was taking on an average 6.87 days for selling or replacing

the entire stock of its inventories (Wahlen, Baginski and Bradshaw 2014). However, in 2017 the

same duration is increased to 8.19 days that is indicating that the efficiency of the company

regarding selling of its stock has been deteriorated. If the receivable days are analyzed it can be

found that during 2016 the entity was taking on an average 30.58 days for collecting the dues

from the debtors to whom it has made credit sales. However, in 2017 the same duration is

increased to 40.38 days that is indicating that the efficiency of the company regarding collection

of the dues has been deteriorated (Vodafone.com 2019). On the other hand, if the trade payable

days are considered it can be found that during 2016 the entity was taking on an average 54.29

days for paying the dues to the creditors from whom it has made credit purchases. However, in

2017 the same duration is increased to 71.95 days that is indicating that the efficiency of the

company regarding payment of the dues has been deteriorated (Vodafone.com 2019). Lastly, if

rate in 2017 too. Gross profit margin of the entity is satisfactory and moreover the company was

able to enhance the same in 2017 as compared to 2016. It is identified that the gross profit

margin has been improved as the entity was able to reduce the cost of sales. Looking into the

liquidity ratio it can be stated that the liquidity ratios of at least more than 1 signifies that the

current assets of the company are sufficient to pay off the short term obligation upon becoming

due (Easton and Sommers 2018). However, the current ratio and quick ratio of the company for

both the years that is 2016 as well as 2017 is below 1 that is indicating that the company is not

able to pay off its short term obligations when they will become due. Gearing ratio that is used

for measuring the equity of the owners as compared to debt or borrowed funds indicating that the

company is lower leveraged as the same for the entity in 2016 is 0.33 and further improved to

0.31 in the year 2017. If the efficiency level of the company is taken into consideration it can be

identified that during 2016 the entity was taking on an average 6.87 days for selling or replacing

the entire stock of its inventories (Wahlen, Baginski and Bradshaw 2014). However, in 2017 the

same duration is increased to 8.19 days that is indicating that the efficiency of the company

regarding selling of its stock has been deteriorated. If the receivable days are analyzed it can be

found that during 2016 the entity was taking on an average 30.58 days for collecting the dues

from the debtors to whom it has made credit sales. However, in 2017 the same duration is

increased to 40.38 days that is indicating that the efficiency of the company regarding collection

of the dues has been deteriorated (Vodafone.com 2019). On the other hand, if the trade payable

days are considered it can be found that during 2016 the entity was taking on an average 54.29

days for paying the dues to the creditors from whom it has made credit purchases. However, in

2017 the same duration is increased to 71.95 days that is indicating that the efficiency of the

company regarding payment of the dues has been deteriorated (Vodafone.com 2019). Lastly, if

6MANAGING FINANCIAL RESOURCES AND PERFORMANCE

the return on equity is considered it can be identified that as the company was not able to

generate profit from sales for both 2016 as well as 2017, it was not able to provide any return on

shareholder’s equity. Hence it can be stated that the overall financial performance of Vodafone

for the year 2016 was not at all good. It is notable that the performance of the entity further

deteriorated in the year 2017 (Vodafone.com 2019)

Performance of Deutsche Telekom

On the other hand, if the performance of its main competitor Deutsche Telekom over the

same period is considered it can be identified that whereas the Vodafone could not generate

profit for both 2016 as well as 2017, Deutsche was able to generate profit from its sales and the

profit was amounted to € 5,551 and the same has been improved from € 3104 million during

2017 (AG 2019). It was found that the liquidity position of the company was not sufficient to

meet the short term obligation as the amount of current assets was not enough to cover up the

amount of short term obligation. However, it was found that the liquidity position of Deutsche

Telekom is significantly better as compared to Vodafone. Further, looking into the leverage

position of the entity it can be identified that the amount of debt is more than double the amount

of the equity. Hence, it can be stated that the entity is highly leveraged that will raise question on

its long term sustainability (AG 2019)

Reason of difference in performance

However, it is notable that whereas the profit of Deutsche Telekom has been improved,

Vodafone could not generate any profit for both the years. Moreover, the liquidity position of the

company is significantly low to meet the short term obligation. It can be identified that during

the past years European telecom sector did not perform as per the expectation. The main reason

the return on equity is considered it can be identified that as the company was not able to

generate profit from sales for both 2016 as well as 2017, it was not able to provide any return on

shareholder’s equity. Hence it can be stated that the overall financial performance of Vodafone

for the year 2016 was not at all good. It is notable that the performance of the entity further

deteriorated in the year 2017 (Vodafone.com 2019)

Performance of Deutsche Telekom

On the other hand, if the performance of its main competitor Deutsche Telekom over the

same period is considered it can be identified that whereas the Vodafone could not generate

profit for both 2016 as well as 2017, Deutsche was able to generate profit from its sales and the

profit was amounted to € 5,551 and the same has been improved from € 3104 million during

2017 (AG 2019). It was found that the liquidity position of the company was not sufficient to

meet the short term obligation as the amount of current assets was not enough to cover up the

amount of short term obligation. However, it was found that the liquidity position of Deutsche

Telekom is significantly better as compared to Vodafone. Further, looking into the leverage

position of the entity it can be identified that the amount of debt is more than double the amount

of the equity. Hence, it can be stated that the entity is highly leveraged that will raise question on

its long term sustainability (AG 2019)

Reason of difference in performance

However, it is notable that whereas the profit of Deutsche Telekom has been improved,

Vodafone could not generate any profit for both the years. Moreover, the liquidity position of the

company is significantly low to meet the short term obligation. It can be identified that during

the past years European telecom sector did not perform as per the expectation. The main reason

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGING FINANCIAL RESOURCES AND PERFORMANCE

behind that is there are improvement in the financial and customer’s trends in Italy and the strong

growth in Germany’s retail sector that reduced the churn in Spain and the consistent performance

over UK (Mariniello and Salemi 2015). Vodafone was required the regulatory clearance for 18.4

billion purchase of the Liberty Global Purchase Plc’s assets in the central Europe so that the

entity can compete with Deutsche in better way. It will further put the telecom tower in separate

business that will make easier for the entity for cutting the costs and sharing with the other

carriers. However, due to acquisition of Liberty Global Plc, Vodafone invested huge amount that

is € 18.4 billion which has a large impact on its performance (Mariniello and Salemi 2015)

However, owing to fall in the industry conditions both are performing to the downside.

Further, Vodafone has largest geographical diversification if it is compared with Deutsche

Telekom. It has exposure to US through 45% share in the Verizon Wireless that represents near

about 42% of adjusted operating profit of the entity. Further, it has lowest exposure to the

domestic market and can be expected that in near future it will improve its financial

performances (Sutherland 2014). Apart from that, high geographical diversification is the clear

positive factor for the company as the entity is not dependent overly on any particular market.

On the other hand, Deutsche Telekom is highly dependent on domestic market and is facing

fierce competition in the domestic market. Further, owing to the weak microeconomic situation

the competition is quite high. Even in the emerging market like Poland, it revealed poor

performance with the decrease in sales as well as lower margins (Pina, Torres and Bachiller

2014)

behind that is there are improvement in the financial and customer’s trends in Italy and the strong

growth in Germany’s retail sector that reduced the churn in Spain and the consistent performance

over UK (Mariniello and Salemi 2015). Vodafone was required the regulatory clearance for 18.4

billion purchase of the Liberty Global Purchase Plc’s assets in the central Europe so that the

entity can compete with Deutsche in better way. It will further put the telecom tower in separate

business that will make easier for the entity for cutting the costs and sharing with the other

carriers. However, due to acquisition of Liberty Global Plc, Vodafone invested huge amount that

is € 18.4 billion which has a large impact on its performance (Mariniello and Salemi 2015)

However, owing to fall in the industry conditions both are performing to the downside.

Further, Vodafone has largest geographical diversification if it is compared with Deutsche

Telekom. It has exposure to US through 45% share in the Verizon Wireless that represents near

about 42% of adjusted operating profit of the entity. Further, it has lowest exposure to the

domestic market and can be expected that in near future it will improve its financial

performances (Sutherland 2014). Apart from that, high geographical diversification is the clear

positive factor for the company as the entity is not dependent overly on any particular market.

On the other hand, Deutsche Telekom is highly dependent on domestic market and is facing

fierce competition in the domestic market. Further, owing to the weak microeconomic situation

the competition is quite high. Even in the emerging market like Poland, it revealed poor

performance with the decrease in sales as well as lower margins (Pina, Torres and Bachiller

2014)

8MANAGING FINANCIAL RESOURCES AND PERFORMANCE

Vodafone to be concerned about Deutsche Telekom

However, Vodafone is required to be concerned about the performance of Deutsche

Telekom as the Deutsche Telekom is able to provide better return to its shareholders and better

return on its capital employed. Further, owing to its ability to generate profits during the year

2016 as well as 2017 it was able to generate return on its sales and provide return on

shareholder’s equity. Further, from the annual report of the entity it is observed that the trade

receivables of the company have increased at lower rates as compared to the rate of increase in

sales. Hence, it is signifying that the company is efficient is collecting its dues from the debtors.

Further, negligible increase in accounts payable is signifying that the company is making

payments for its dues on time (Mariniello and Salemi 2015). Whereas the efficiency of Vodafone

has been reduced in context of accounts receivable and accounts payable, Deutsche Telekom is

efficient in collecting its debts and making payments for its dues. Hence, the financial

performance of the entity has been improved whereas the performance of Vodafone is

significantly deteriorated over the years. Investors are generally concerned about the return on

their investment and that is confirmed through the better performance of the company. Hence,

likelihood is there that owing to bad financial performance of Vodafone; investors will withdraw

their holdings from the company and may move to Deutsche Telekom (Forsgren 2017).

Conclusion

From the above discussion it is concluded that over the years financial performance of

Vodafone is deteriorated in all aspects including profitability, liquidity and efficiencies. On the

other hand, it is found for its main competitor Deutsche Telekom was able to generate return on

its sales and provide return on shareholder’s equity. Further, it is observed that the trade

receivables of Deutsche Telekom have increased at lower rates as compared to the rate of

Vodafone to be concerned about Deutsche Telekom

However, Vodafone is required to be concerned about the performance of Deutsche

Telekom as the Deutsche Telekom is able to provide better return to its shareholders and better

return on its capital employed. Further, owing to its ability to generate profits during the year

2016 as well as 2017 it was able to generate return on its sales and provide return on

shareholder’s equity. Further, from the annual report of the entity it is observed that the trade

receivables of the company have increased at lower rates as compared to the rate of increase in

sales. Hence, it is signifying that the company is efficient is collecting its dues from the debtors.

Further, negligible increase in accounts payable is signifying that the company is making

payments for its dues on time (Mariniello and Salemi 2015). Whereas the efficiency of Vodafone

has been reduced in context of accounts receivable and accounts payable, Deutsche Telekom is

efficient in collecting its debts and making payments for its dues. Hence, the financial

performance of the entity has been improved whereas the performance of Vodafone is

significantly deteriorated over the years. Investors are generally concerned about the return on

their investment and that is confirmed through the better performance of the company. Hence,

likelihood is there that owing to bad financial performance of Vodafone; investors will withdraw

their holdings from the company and may move to Deutsche Telekom (Forsgren 2017).

Conclusion

From the above discussion it is concluded that over the years financial performance of

Vodafone is deteriorated in all aspects including profitability, liquidity and efficiencies. On the

other hand, it is found for its main competitor Deutsche Telekom was able to generate return on

its sales and provide return on shareholder’s equity. Further, it is observed that the trade

receivables of Deutsche Telekom have increased at lower rates as compared to the rate of

9MANAGING FINANCIAL RESOURCES AND PERFORMANCE

increase in sales. Hence, it is signifying that the company is efficient is collecting its dues from

the debtors. Further, negligible increase in accounts payable is signifying that the company is

making payments for its dues on time. Hence, it is stated that Vodafone is required to be

concerned about the performance of Deutsche Telekom as the investors are generally concerned

about the return on their investment and likelihood is there that owing to bad financial

performance of Vodafone investors will withdraw their holdings from the company and may

move to Deutsche Telekom.

increase in sales. Hence, it is signifying that the company is efficient is collecting its dues from

the debtors. Further, negligible increase in accounts payable is signifying that the company is

making payments for its dues on time. Hence, it is stated that Vodafone is required to be

concerned about the performance of Deutsche Telekom as the investors are generally concerned

about the return on their investment and likelihood is there that owing to bad financial

performance of Vodafone investors will withdraw their holdings from the company and may

move to Deutsche Telekom.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGING FINANCIAL RESOURCES AND PERFORMANCE

Reference

AG, D., 2019. Company. [online] Telekom.com. Available at:

https://www.telekom.com/en/company [Accessed 8 May 2019].

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E., 2015. Quantitative

investment analysis. John Wiley & Sons.

Easton, M. and Sommers, Z., 2018. Financial Statement Analysis & Valuation, 5e.

Forsgren, M., 2017. Theories of the multinational firm: A multidimensional creature in the

global economy. Edward Elgar Publishing.

Grimm, S.D. and Blazovich, J.L., 2016. Developing student competencies: An integrated

approach to a financial statement analysis project. Journal of Accounting Education, 35, pp.69-

101.

Loughran, T. and McDonald, B., 2014. Measuring readability in financial disclosures. The

Journal of Finance, 69(4), pp.1643-1671.

Mariniello, M. and Salemi, F., 2015. Addressing fragmentation in EU mobile telecom

markets (No. 2015/13). Bruegel Policy Contribution.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Reference

AG, D., 2019. Company. [online] Telekom.com. Available at:

https://www.telekom.com/en/company [Accessed 8 May 2019].

Brigham, E.F., Ehrhardt, M.C., Nason, R.R. and Gessaroli, J., 2016. Financial Managment:

Theory And Practice, Canadian Edition. Nelson Education.

DeFusco, R.A., McLeavey, D.W., Pinto, J.E., Anson, M.J. and Runkle, D.E., 2015. Quantitative

investment analysis. John Wiley & Sons.

Easton, M. and Sommers, Z., 2018. Financial Statement Analysis & Valuation, 5e.

Forsgren, M., 2017. Theories of the multinational firm: A multidimensional creature in the

global economy. Edward Elgar Publishing.

Grimm, S.D. and Blazovich, J.L., 2016. Developing student competencies: An integrated

approach to a financial statement analysis project. Journal of Accounting Education, 35, pp.69-

101.

Loughran, T. and McDonald, B., 2014. Measuring readability in financial disclosures. The

Journal of Finance, 69(4), pp.1643-1671.

Mariniello, M. and Salemi, F., 2015. Addressing fragmentation in EU mobile telecom

markets (No. 2015/13). Bruegel Policy Contribution.

Nobes, C., 2014. International classification of financial reporting. Routledge.

11MANAGING FINANCIAL RESOURCES AND PERFORMANCE

Pina, V., Torres, L. and Bachiller, P., 2014. Service quality in utility industries: the European

telecommunications sector. Managing Service Quality: An International Journal, 24(1), pp.2-22.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Rohman, I.K. and Bohlin, E., 2014. Decomposition analysis of the telecommunications sector in

Indonesia: What does the cellular era shed light on?. Telecommunications Policy, 38(3), pp.248-

263.

Sutherland, E., 2014. Lobbying and litigation in telecommunications markets–reapplying

Porter’s five forces. info, 16(5), pp.1-18.

Vodafone.com., 2019. Vodafone in Europe. [online] Available at:

https://www.vodafone.com/content/index/about/policy/eu.html [Accessed 8 May 2019].

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

Pina, V., Torres, L. and Bachiller, P., 2014. Service quality in utility industries: the European

telecommunications sector. Managing Service Quality: An International Journal, 24(1), pp.2-22.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Rohman, I.K. and Bohlin, E., 2014. Decomposition analysis of the telecommunications sector in

Indonesia: What does the cellular era shed light on?. Telecommunications Policy, 38(3), pp.248-

263.

Sutherland, E., 2014. Lobbying and litigation in telecommunications markets–reapplying

Porter’s five forces. info, 16(5), pp.1-18.

Vodafone.com., 2019. Vodafone in Europe. [online] Available at:

https://www.vodafone.com/content/index/about/policy/eu.html [Accessed 8 May 2019].

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.