Financial Accounting, Investment Appraisal, and Ratio Analysis Report

VerifiedAdded on 2023/01/16

|12

|2540

|28

Report

AI Summary

This report comprehensively analyzes financial resource management, starting with a comparison of management and financial accounting, highlighting their distinct objectives, users, and regulatory compliance. The report then delves into investment appraisal techniques, such as payback period,...

Managing Financial Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

QUESTION 1.............................................................................................................................3

Explaining management and financial accounting................................................................3

Presenting difference between management and financial accounting..................................4

QUESTION 2.............................................................................................................................5

Assessing viability of options available referring investment appraisal techniques..............5

QUESTION 3.............................................................................................................................8

Analyzing financial statements of firm using ratio analysis technique..................................8

CONCLUSION........................................................................................................................10

RECOMMENDATIONS.........................................................................................................11

REFERENCES.........................................................................................................................12

INTRODUCTION......................................................................................................................3

QUESTION 1.............................................................................................................................3

Explaining management and financial accounting................................................................3

Presenting difference between management and financial accounting..................................4

QUESTION 2.............................................................................................................................5

Assessing viability of options available referring investment appraisal techniques..............5

QUESTION 3.............................................................................................................................8

Analyzing financial statements of firm using ratio analysis technique..................................8

CONCLUSION........................................................................................................................10

RECOMMENDATIONS.........................................................................................................11

REFERENCES.........................................................................................................................12

INTRODUCTION

In the recent times, business units lay more emphasis on undertaking competent

strategic and policy framework with the motive to make optimum use of funds. Moreover,

without having wide framework business unit faces difficulty in getting desired level of

outcome or success. Now, several tools & techniques are available which firm can use before

taking decision pertaining to investment and financing decision. The present report is based

on different case situation which will develop understanding about the concept of

management and financial accounting. Further, it will shed light on the aspects on the basis of

which management accounting differs from financial. Along with this, report will exhibit

how concept pertaining to ratio analysis and capital budgeting aid in decision making.

QUESTION 1

Explaining management and financial accounting

Management accounting: It refers to the presentation of accounting information

which in turn used by management team for the formulation of policy framework regarding

day to day activities. MA assists management team in performing functions related to

planning, organizing, staffing, directing and controlling. In other words, the main function of

MA is to make appropriate forecast about production and selling aspects, cash inflow &

outflow (Eldenburg and et.al., 2019). In addition to this, aspects of MA also focus on

identifying specific cost centre and delegation of roles and responsibilities which in turn

helps in achieving success.

Financial accounting: It implies for the collection, summarization and presentation

of monetary information that resulted from business transactions. FA reports furnish

information about operating profit and business value to the concerned stakeholders

(Steccolini, 2019). Hence, financial accounting technique is undertaken by businesses with

the motive to serve information to all the stakeholders in an acceptable and standardized

format. In this way, it can be stated that financial accounting process is employed by the firm

for showing financial position and performance to both internal and external stakeholders

(Weetman, 2019). There are several functions which in turn associated with financial

accounting aspects. This in turn includes recording of systematic records, communicating

results to the stakeholders, budget preparation and cost control. It is highly significant which

In the recent times, business units lay more emphasis on undertaking competent

strategic and policy framework with the motive to make optimum use of funds. Moreover,

without having wide framework business unit faces difficulty in getting desired level of

outcome or success. Now, several tools & techniques are available which firm can use before

taking decision pertaining to investment and financing decision. The present report is based

on different case situation which will develop understanding about the concept of

management and financial accounting. Further, it will shed light on the aspects on the basis of

which management accounting differs from financial. Along with this, report will exhibit

how concept pertaining to ratio analysis and capital budgeting aid in decision making.

QUESTION 1

Explaining management and financial accounting

Management accounting: It refers to the presentation of accounting information

which in turn used by management team for the formulation of policy framework regarding

day to day activities. MA assists management team in performing functions related to

planning, organizing, staffing, directing and controlling. In other words, the main function of

MA is to make appropriate forecast about production and selling aspects, cash inflow &

outflow (Eldenburg and et.al., 2019). In addition to this, aspects of MA also focus on

identifying specific cost centre and delegation of roles and responsibilities which in turn

helps in achieving success.

Financial accounting: It implies for the collection, summarization and presentation

of monetary information that resulted from business transactions. FA reports furnish

information about operating profit and business value to the concerned stakeholders

(Steccolini, 2019). Hence, financial accounting technique is undertaken by businesses with

the motive to serve information to all the stakeholders in an acceptable and standardized

format. In this way, it can be stated that financial accounting process is employed by the firm

for showing financial position and performance to both internal and external stakeholders

(Weetman, 2019). There are several functions which in turn associated with financial

accounting aspects. This in turn includes recording of systematic records, communicating

results to the stakeholders, budget preparation and cost control. It is highly significant which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps in analyzing areas where improvements are needed. In addition to this, by analyzing

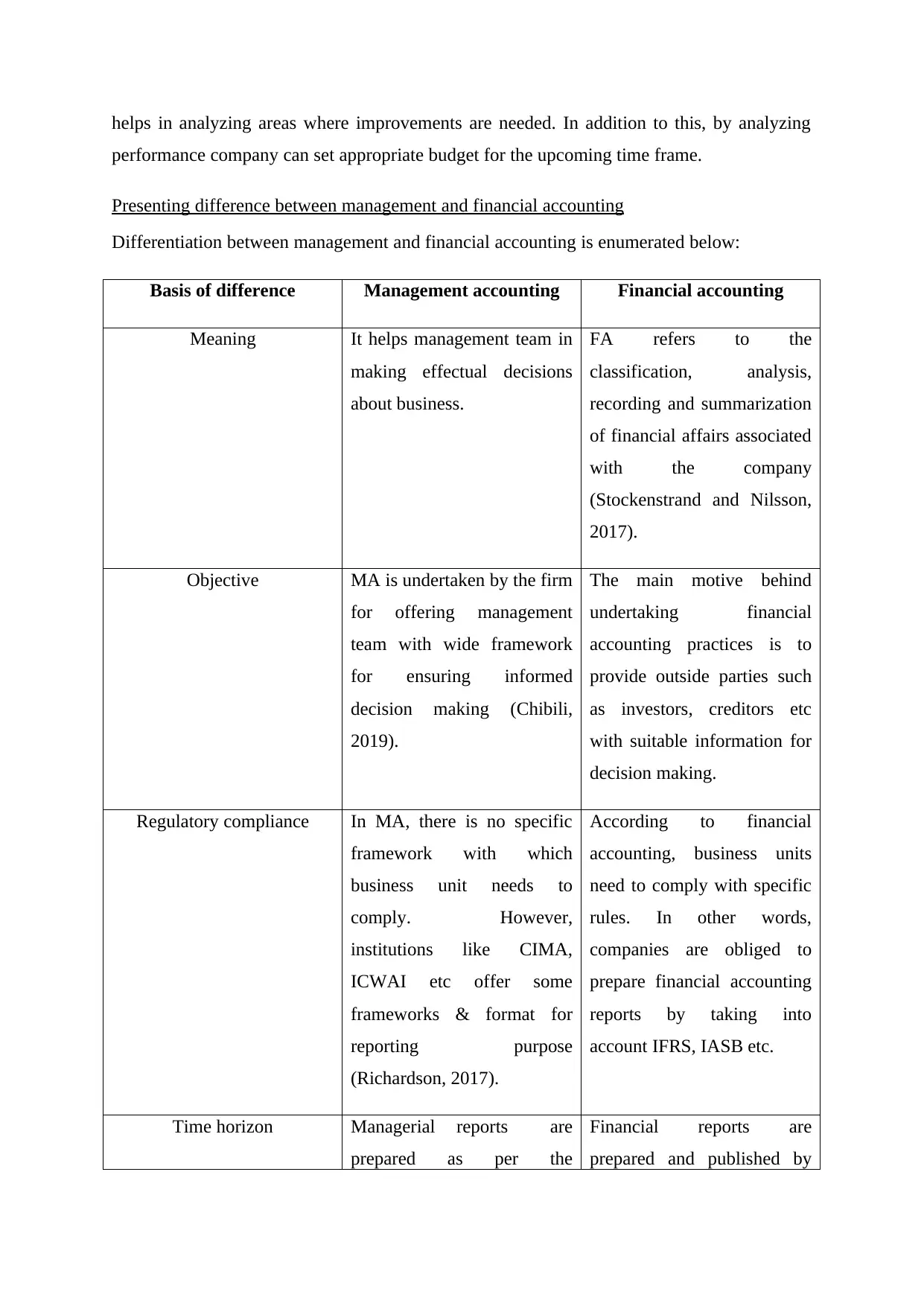

performance company can set appropriate budget for the upcoming time frame.

Presenting difference between management and financial accounting

Differentiation between management and financial accounting is enumerated below:

Basis of difference Management accounting Financial accounting

Meaning It helps management team in

making effectual decisions

about business.

FA refers to the

classification, analysis,

recording and summarization

of financial affairs associated

with the company

(Stockenstrand and Nilsson,

2017).

Objective MA is undertaken by the firm

for offering management

team with wide framework

for ensuring informed

decision making (Chibili,

2019).

The main motive behind

undertaking financial

accounting practices is to

provide outside parties such

as investors, creditors etc

with suitable information for

decision making.

Regulatory compliance In MA, there is no specific

framework with which

business unit needs to

comply. However,

institutions like CIMA,

ICWAI etc offer some

frameworks & format for

reporting purpose

(Richardson, 2017).

According to financial

accounting, business units

need to comply with specific

rules. In other words,

companies are obliged to

prepare financial accounting

reports by taking into

account IFRS, IASB etc.

Time horizon Managerial reports are

prepared as per the

Financial reports are

prepared and published by

performance company can set appropriate budget for the upcoming time frame.

Presenting difference between management and financial accounting

Differentiation between management and financial accounting is enumerated below:

Basis of difference Management accounting Financial accounting

Meaning It helps management team in

making effectual decisions

about business.

FA refers to the

classification, analysis,

recording and summarization

of financial affairs associated

with the company

(Stockenstrand and Nilsson,

2017).

Objective MA is undertaken by the firm

for offering management

team with wide framework

for ensuring informed

decision making (Chibili,

2019).

The main motive behind

undertaking financial

accounting practices is to

provide outside parties such

as investors, creditors etc

with suitable information for

decision making.

Regulatory compliance In MA, there is no specific

framework with which

business unit needs to

comply. However,

institutions like CIMA,

ICWAI etc offer some

frameworks & format for

reporting purpose

(Richardson, 2017).

According to financial

accounting, business units

need to comply with specific

rules. In other words,

companies are obliged to

prepare financial accounting

reports by taking into

account IFRS, IASB etc.

Time horizon Managerial reports are

prepared as per the

Financial reports are

prepared and published by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

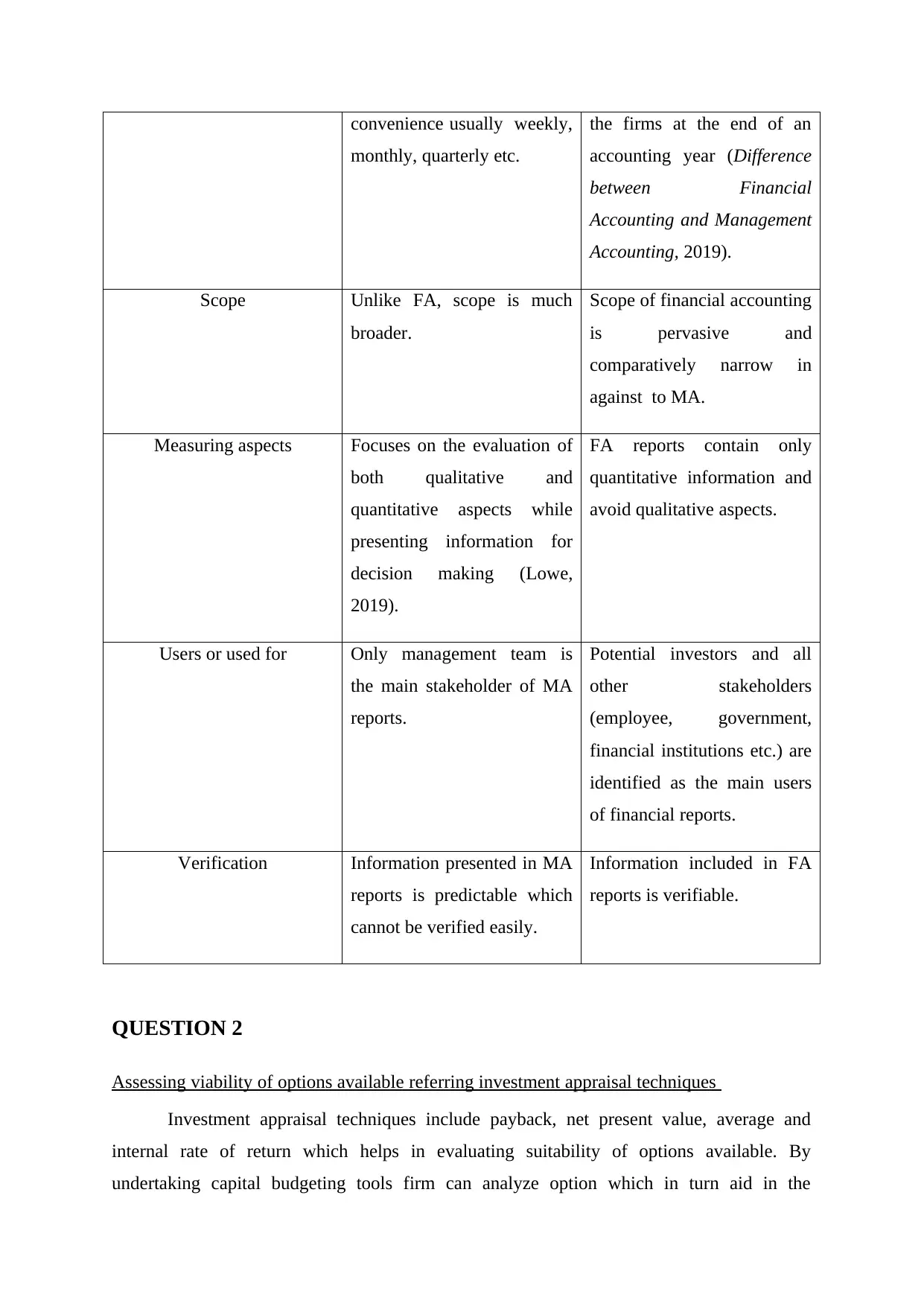

convenience usually weekly,

monthly, quarterly etc.

the firms at the end of an

accounting year (Difference

between Financial

Accounting and Management

Accounting, 2019).

Scope Unlike FA, scope is much

broader.

Scope of financial accounting

is pervasive and

comparatively narrow in

against to MA.

Measuring aspects Focuses on the evaluation of

both qualitative and

quantitative aspects while

presenting information for

decision making (Lowe,

2019).

FA reports contain only

quantitative information and

avoid qualitative aspects.

Users or used for Only management team is

the main stakeholder of MA

reports.

Potential investors and all

other stakeholders

(employee, government,

financial institutions etc.) are

identified as the main users

of financial reports.

Verification Information presented in MA

reports is predictable which

cannot be verified easily.

Information included in FA

reports is verifiable.

QUESTION 2

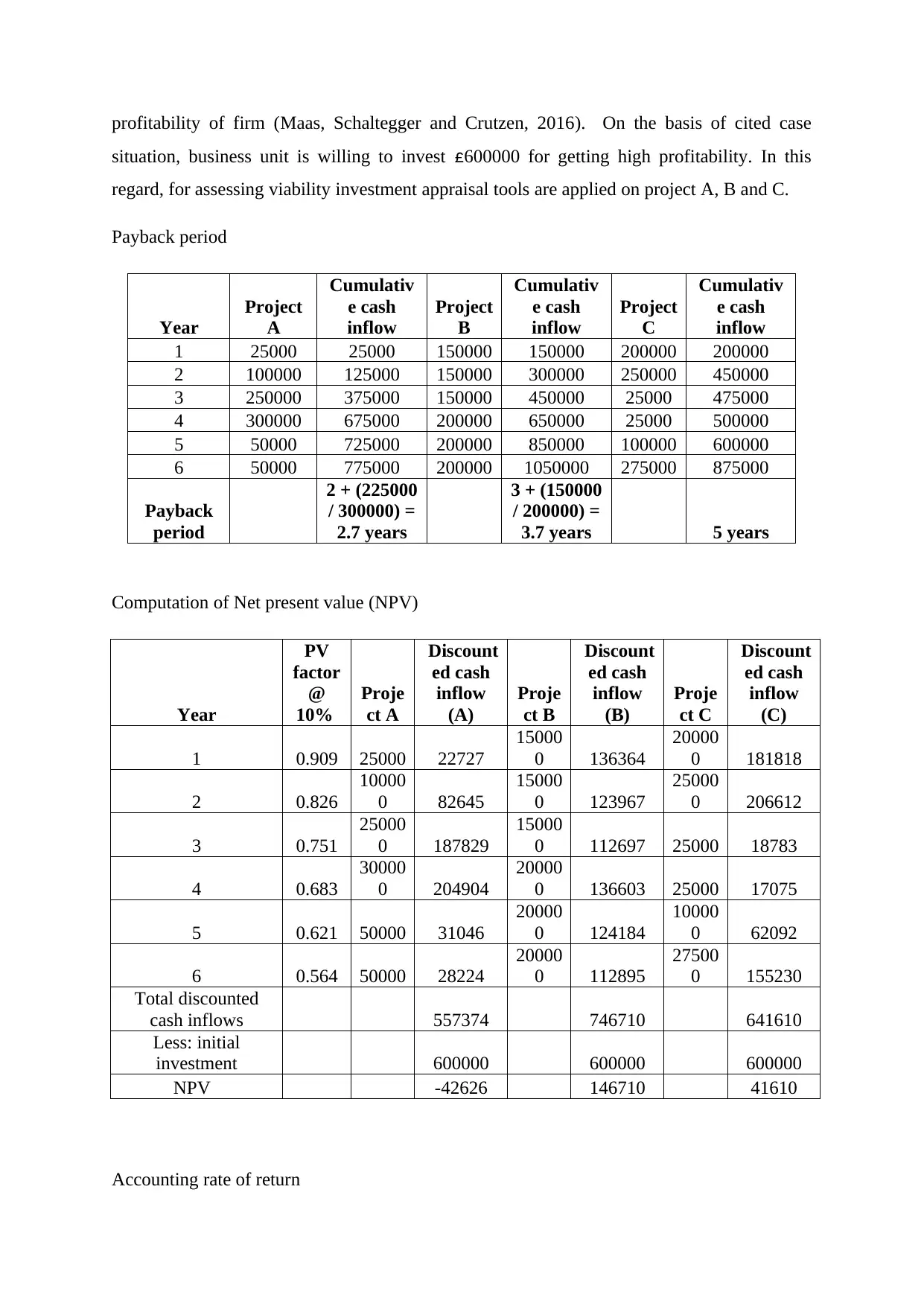

Assessing viability of options available referring investment appraisal techniques

Investment appraisal techniques include payback, net present value, average and

internal rate of return which helps in evaluating suitability of options available. By

undertaking capital budgeting tools firm can analyze option which in turn aid in the

monthly, quarterly etc.

the firms at the end of an

accounting year (Difference

between Financial

Accounting and Management

Accounting, 2019).

Scope Unlike FA, scope is much

broader.

Scope of financial accounting

is pervasive and

comparatively narrow in

against to MA.

Measuring aspects Focuses on the evaluation of

both qualitative and

quantitative aspects while

presenting information for

decision making (Lowe,

2019).

FA reports contain only

quantitative information and

avoid qualitative aspects.

Users or used for Only management team is

the main stakeholder of MA

reports.

Potential investors and all

other stakeholders

(employee, government,

financial institutions etc.) are

identified as the main users

of financial reports.

Verification Information presented in MA

reports is predictable which

cannot be verified easily.

Information included in FA

reports is verifiable.

QUESTION 2

Assessing viability of options available referring investment appraisal techniques

Investment appraisal techniques include payback, net present value, average and

internal rate of return which helps in evaluating suitability of options available. By

undertaking capital budgeting tools firm can analyze option which in turn aid in the

profitability of firm (Maas, Schaltegger and Crutzen, 2016). On the basis of cited case

situation, business unit is willing to invest £600000 for getting high profitability. In this

regard, for assessing viability investment appraisal tools are applied on project A, B and C.

Payback period

Year

Project

A

Cumulativ

e cash

inflow

Project

B

Cumulativ

e cash

inflow

Project

C

Cumulativ

e cash

inflow

1 25000 25000 150000 150000 200000 200000

2 100000 125000 150000 300000 250000 450000

3 250000 375000 150000 450000 25000 475000

4 300000 675000 200000 650000 25000 500000

5 50000 725000 200000 850000 100000 600000

6 50000 775000 200000 1050000 275000 875000

Payback

period

2 + (225000

/ 300000) =

2.7 years

3 + (150000

/ 200000) =

3.7 years 5 years

Computation of Net present value (NPV)

Year

PV

factor

@

10%

Proje

ct A

Discount

ed cash

inflow

(A)

Proje

ct B

Discount

ed cash

inflow

(B)

Proje

ct C

Discount

ed cash

inflow

(C)

1 0.909 25000 22727

15000

0 136364

20000

0 181818

2 0.826

10000

0 82645

15000

0 123967

25000

0 206612

3 0.751

25000

0 187829

15000

0 112697 25000 18783

4 0.683

30000

0 204904

20000

0 136603 25000 17075

5 0.621 50000 31046

20000

0 124184

10000

0 62092

6 0.564 50000 28224

20000

0 112895

27500

0 155230

Total discounted

cash inflows 557374 746710 641610

Less: initial

investment 600000 600000 600000

NPV -42626 146710 41610

Accounting rate of return

situation, business unit is willing to invest £600000 for getting high profitability. In this

regard, for assessing viability investment appraisal tools are applied on project A, B and C.

Payback period

Year

Project

A

Cumulativ

e cash

inflow

Project

B

Cumulativ

e cash

inflow

Project

C

Cumulativ

e cash

inflow

1 25000 25000 150000 150000 200000 200000

2 100000 125000 150000 300000 250000 450000

3 250000 375000 150000 450000 25000 475000

4 300000 675000 200000 650000 25000 500000

5 50000 725000 200000 850000 100000 600000

6 50000 775000 200000 1050000 275000 875000

Payback

period

2 + (225000

/ 300000) =

2.7 years

3 + (150000

/ 200000) =

3.7 years 5 years

Computation of Net present value (NPV)

Year

PV

factor

@

10%

Proje

ct A

Discount

ed cash

inflow

(A)

Proje

ct B

Discount

ed cash

inflow

(B)

Proje

ct C

Discount

ed cash

inflow

(C)

1 0.909 25000 22727

15000

0 136364

20000

0 181818

2 0.826

10000

0 82645

15000

0 123967

25000

0 206612

3 0.751

25000

0 187829

15000

0 112697 25000 18783

4 0.683

30000

0 204904

20000

0 136603 25000 17075

5 0.621 50000 31046

20000

0 124184

10000

0 62092

6 0.564 50000 28224

20000

0 112895

27500

0 155230

Total discounted

cash inflows 557374 746710 641610

Less: initial

investment 600000 600000 600000

NPV -42626 146710 41610

Accounting rate of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year

Project

A

Project

B

Project

C

1 25000 150000 200000

2 100000 150000 250000

3 250000 150000 25000

4 300000 200000 25000

5 50000 200000 100000

6 50000 200000 275000

Average cash

inflow 129167 175000 145833

Average

investment 600000 600000 600000

ARR 22% 29% 24%

Internal rate of return

Year

Project

A

Project

B

Project

C

0 (600000) (600000) (600000)

1 25000 150000 200000

2 100000 150000 250000

3 250000 150000 25000

4 300000 200000 25000

5 50000 200000 100000

6 50000 200000 275000

IRR 8% 17% 12%

By applying investment appraisal tools on given cash flows it has identified that

payback period pertaining to project B & C implies for 3.7 and 5 years. Referring this, it can

be entailed that by investing money in project b business entity will recoup initial investment

within the period of 3 years and 8 months. Along with this, ARR and IRR of project B

accounts for 29% & 17% respectively. This in turn shows that project B will offers higher

returns after the period of 6 years over other options available. In addition to this, NPV of

project B is also higher over other alternatives. As per the selection criteria, company should

give priority to the projects having lower payback period and higher NPV, ARR & IRR.

Accordingly, project B falls in the category of viable option as compared to A & C. The

rationale behind this, NPV of project A is negative and C having lower return. Further, ARR

and IRR of other options are less in comparison to project B. Considering all these aspects, it

Project

A

Project

B

Project

C

1 25000 150000 200000

2 100000 150000 250000

3 250000 150000 25000

4 300000 200000 25000

5 50000 200000 100000

6 50000 200000 275000

Average cash

inflow 129167 175000 145833

Average

investment 600000 600000 600000

ARR 22% 29% 24%

Internal rate of return

Year

Project

A

Project

B

Project

C

0 (600000) (600000) (600000)

1 25000 150000 200000

2 100000 150000 250000

3 250000 150000 25000

4 300000 200000 25000

5 50000 200000 100000

6 50000 200000 275000

IRR 8% 17% 12%

By applying investment appraisal tools on given cash flows it has identified that

payback period pertaining to project B & C implies for 3.7 and 5 years. Referring this, it can

be entailed that by investing money in project b business entity will recoup initial investment

within the period of 3 years and 8 months. Along with this, ARR and IRR of project B

accounts for 29% & 17% respectively. This in turn shows that project B will offers higher

returns after the period of 6 years over other options available. In addition to this, NPV of

project B is also higher over other alternatives. As per the selection criteria, company should

give priority to the projects having lower payback period and higher NPV, ARR & IRR.

Accordingly, project B falls in the category of viable option as compared to A & C. The

rationale behind this, NPV of project A is negative and C having lower return. Further, ARR

and IRR of other options are less in comparison to project B. Considering all these aspects, it

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can be said that project B will help in increasing company’s profitability and assists in getting

desired level of outcome or success.

QUESTION 3

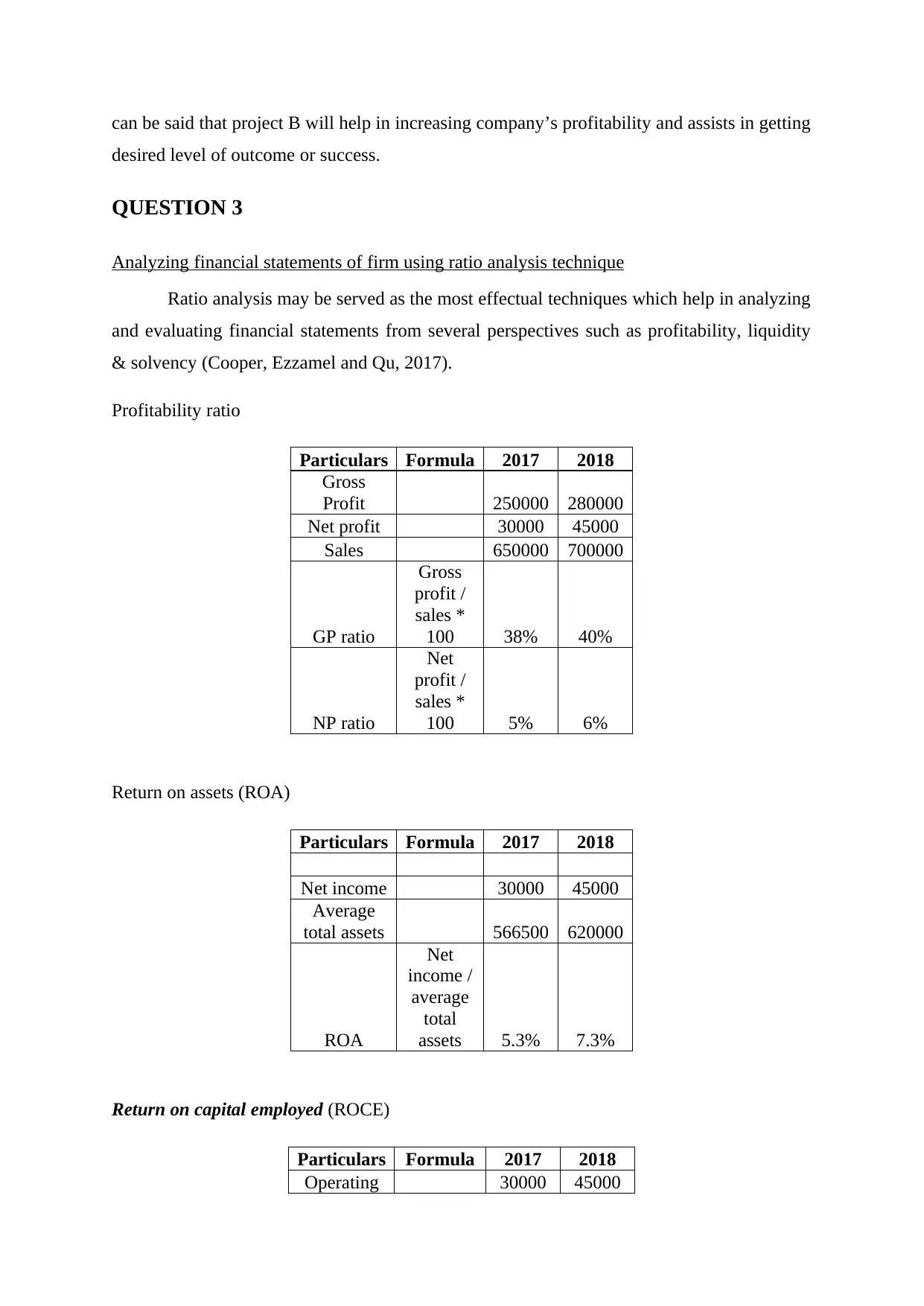

Analyzing financial statements of firm using ratio analysis technique

Ratio analysis may be served as the most effectual techniques which help in analyzing

and evaluating financial statements from several perspectives such as profitability, liquidity

& solvency (Cooper, Ezzamel and Qu, 2017).

Profitability ratio

Particulars Formula 2017 2018

Gross

Profit 250000 280000

Net profit 30000 45000

Sales 650000 700000

GP ratio

Gross

profit /

sales *

100 38% 40%

NP ratio

Net

profit /

sales *

100 5% 6%

Return on assets (ROA)

Particulars Formula 2017 2018

Net income 30000 45000

Average

total assets 566500 620000

ROA

Net

income /

average

total

assets 5.3% 7.3%

Return on capital employed (ROCE)

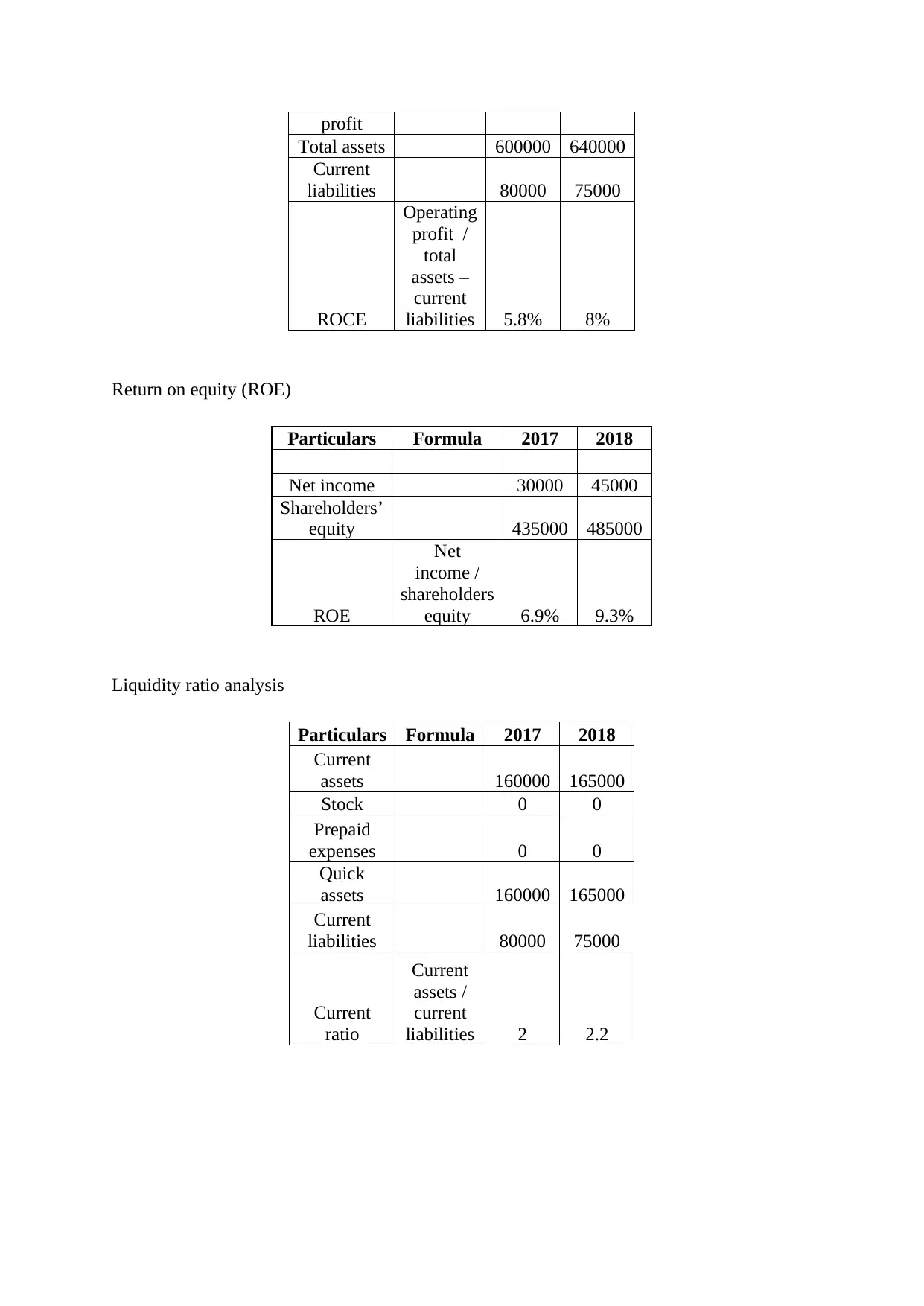

Particulars Formula 2017 2018

Operating 30000 45000

desired level of outcome or success.

QUESTION 3

Analyzing financial statements of firm using ratio analysis technique

Ratio analysis may be served as the most effectual techniques which help in analyzing

and evaluating financial statements from several perspectives such as profitability, liquidity

& solvency (Cooper, Ezzamel and Qu, 2017).

Profitability ratio

Particulars Formula 2017 2018

Gross

Profit 250000 280000

Net profit 30000 45000

Sales 650000 700000

GP ratio

Gross

profit /

sales *

100 38% 40%

NP ratio

Net

profit /

sales *

100 5% 6%

Return on assets (ROA)

Particulars Formula 2017 2018

Net income 30000 45000

Average

total assets 566500 620000

ROA

Net

income /

average

total

assets 5.3% 7.3%

Return on capital employed (ROCE)

Particulars Formula 2017 2018

Operating 30000 45000

profit

Total assets 600000 640000

Current

liabilities 80000 75000

ROCE

Operating

profit /

total

assets –

current

liabilities 5.8% 8%

Return on equity (ROE)

Particulars Formula 2017 2018

Net income 30000 45000

Shareholders’

equity 435000 485000

ROE

Net

income /

shareholders

equity 6.9% 9.3%

Liquidity ratio analysis

Particulars Formula 2017 2018

Current

assets 160000 165000

Stock 0 0

Prepaid

expenses 0 0

Quick

assets 160000 165000

Current

liabilities 80000 75000

Current

ratio

Current

assets /

current

liabilities 2 2.2

Total assets 600000 640000

Current

liabilities 80000 75000

ROCE

Operating

profit /

total

assets –

current

liabilities 5.8% 8%

Return on equity (ROE)

Particulars Formula 2017 2018

Net income 30000 45000

Shareholders’

equity 435000 485000

ROE

Net

income /

shareholders

equity 6.9% 9.3%

Liquidity ratio analysis

Particulars Formula 2017 2018

Current

assets 160000 165000

Stock 0 0

Prepaid

expenses 0 0

Quick

assets 160000 165000

Current

liabilities 80000 75000

Current

ratio

Current

assets /

current

liabilities 2 2.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

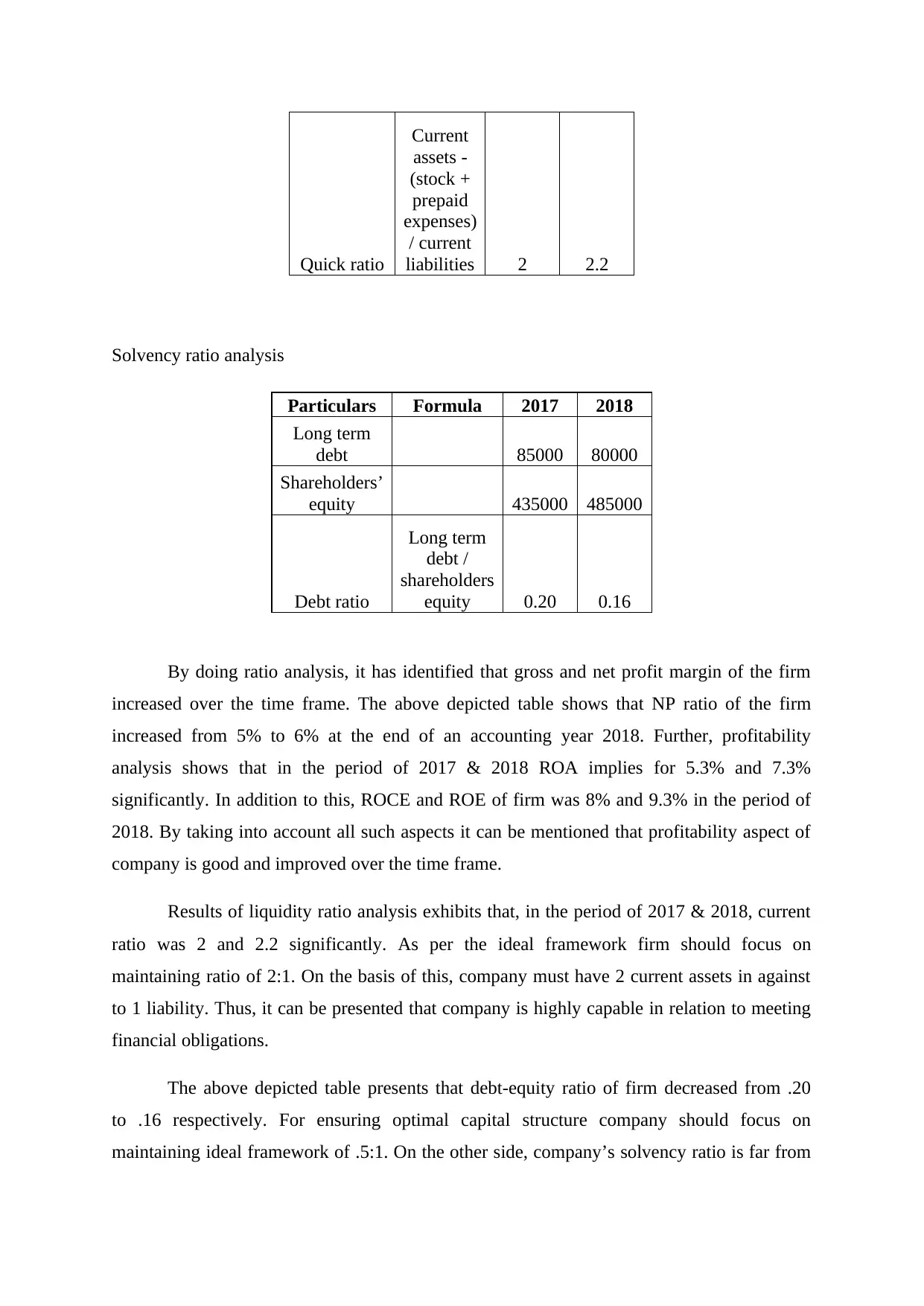

Quick ratio

Current

assets -

(stock +

prepaid

expenses)

/ current

liabilities 2 2.2

Solvency ratio analysis

Particulars Formula 2017 2018

Long term

debt 85000 80000

Shareholders’

equity 435000 485000

Debt ratio

Long term

debt /

shareholders

equity 0.20 0.16

By doing ratio analysis, it has identified that gross and net profit margin of the firm

increased over the time frame. The above depicted table shows that NP ratio of the firm

increased from 5% to 6% at the end of an accounting year 2018. Further, profitability

analysis shows that in the period of 2017 & 2018 ROA implies for 5.3% and 7.3%

significantly. In addition to this, ROCE and ROE of firm was 8% and 9.3% in the period of

2018. By taking into account all such aspects it can be mentioned that profitability aspect of

company is good and improved over the time frame.

Results of liquidity ratio analysis exhibits that, in the period of 2017 & 2018, current

ratio was 2 and 2.2 significantly. As per the ideal framework firm should focus on

maintaining ratio of 2:1. On the basis of this, company must have 2 current assets in against

to 1 liability. Thus, it can be presented that company is highly capable in relation to meeting

financial obligations.

The above depicted table presents that debt-equity ratio of firm decreased from .20

to .16 respectively. For ensuring optimal capital structure company should focus on

maintaining ideal framework of .5:1. On the other side, company’s solvency ratio is far from

Current

assets -

(stock +

prepaid

expenses)

/ current

liabilities 2 2.2

Solvency ratio analysis

Particulars Formula 2017 2018

Long term

debt 85000 80000

Shareholders’

equity 435000 485000

Debt ratio

Long term

debt /

shareholders

equity 0.20 0.16

By doing ratio analysis, it has identified that gross and net profit margin of the firm

increased over the time frame. The above depicted table shows that NP ratio of the firm

increased from 5% to 6% at the end of an accounting year 2018. Further, profitability

analysis shows that in the period of 2017 & 2018 ROA implies for 5.3% and 7.3%

significantly. In addition to this, ROCE and ROE of firm was 8% and 9.3% in the period of

2018. By taking into account all such aspects it can be mentioned that profitability aspect of

company is good and improved over the time frame.

Results of liquidity ratio analysis exhibits that, in the period of 2017 & 2018, current

ratio was 2 and 2.2 significantly. As per the ideal framework firm should focus on

maintaining ratio of 2:1. On the basis of this, company must have 2 current assets in against

to 1 liability. Thus, it can be presented that company is highly capable in relation to meeting

financial obligations.

The above depicted table presents that debt-equity ratio of firm decreased from .20

to .16 respectively. For ensuring optimal capital structure company should focus on

maintaining ideal framework of .5:1. On the other side, company’s solvency ratio is far from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the ideal framework. Thus, at the time of raising funds firm should keep in mind ideal ratio.

Accordingly, business organization should issue 2 equities in against to 1 debt instrument.

CONCLUSION

By summing up this report, it can be concluded that significant difference take place

between management and financial accounting. Moreover, such accounting systems differ on

the basis of several aspects namely stakeholders, period, reporting format etc. Besides this, it

can be inferred that investment appraisal techniques are highly significant which facilitates

selection of appropriate project out of several options available. It can be summarized from

the evaluation that project B will prove to be more beneficial for the firm. Further, it has been

articulated that financial position and performance of firm has improved over the time period.

This in turn recognized as good indicator for the firm which shows that strategic framework

undertaken is competent.

RECOMMENDATIONS

In the context of outcome derived through capital budgeting, company should focus

on investing £600000 in project B over A & C. Moreover, NPV, IRR and ARR of

project B are positive and higher in comparison to other alternatives.

As per the results of ratio analysis business organization is advised in relation to

employing budgetary control and promotional tools. Moreover, through employing

such tools business unit can exert control on undesirable expenses. Further,

promotional tools also help in raising sales and thereby profitability as well.

Further, at the time of developing framework regarding working capital and financial

structure firm should keep in mind ideal ratio.

Accordingly, business organization should issue 2 equities in against to 1 debt instrument.

CONCLUSION

By summing up this report, it can be concluded that significant difference take place

between management and financial accounting. Moreover, such accounting systems differ on

the basis of several aspects namely stakeholders, period, reporting format etc. Besides this, it

can be inferred that investment appraisal techniques are highly significant which facilitates

selection of appropriate project out of several options available. It can be summarized from

the evaluation that project B will prove to be more beneficial for the firm. Further, it has been

articulated that financial position and performance of firm has improved over the time period.

This in turn recognized as good indicator for the firm which shows that strategic framework

undertaken is competent.

RECOMMENDATIONS

In the context of outcome derived through capital budgeting, company should focus

on investing £600000 in project B over A & C. Moreover, NPV, IRR and ARR of

project B are positive and higher in comparison to other alternatives.

As per the results of ratio analysis business organization is advised in relation to

employing budgetary control and promotional tools. Moreover, through employing

such tools business unit can exert control on undesirable expenses. Further,

promotional tools also help in raising sales and thereby profitability as well.

Further, at the time of developing framework regarding working capital and financial

structure firm should keep in mind ideal ratio.

REFERENCES

Books and Journals

Chibili, M., 2019. Basic management accounting for the hospitality industry. Routledge.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-

1025.

Eldenburg, L. G. and et.al., 2019. Management accounting. John Wiley & Sons.

Lowe, E. A., 2019. On the idea of a management control system: integrating accounting and

management control. Management Control Theory. p.63.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production. 136. pp.237-248.

Richardson, A. J., 2017. The relationship between management and financial accounting as

professions and technologies of practice. In The Role of the Management Accountant (pp.

246-261). Routledge.

Steccolini, I., 2019. Accounting and the post-new public management: Re-considering

publicness in accounting research. Accounting, Auditing & Accountability Journal. 32(1).

pp.255-279.

Stockenstrand, A. K. and Nilsson, F. eds., 2017. Bank Regulation: Effects on Strategy,

Financial Accounting and Management Control. Taylor & Francis.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Online

Difference between Financial Accounting and Management Accounting. 2019. Online.

Available through: < https://keydifferences.com/difference-between-financial-accounting-

and-management-accounting.html >.

Books and Journals

Chibili, M., 2019. Basic management accounting for the hospitality industry. Routledge.

Cooper, D. J., Ezzamel, M. and Qu, S. Q., 2017. Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research. 34(2). pp.991-

1025.

Eldenburg, L. G. and et.al., 2019. Management accounting. John Wiley & Sons.

Lowe, E. A., 2019. On the idea of a management control system: integrating accounting and

management control. Management Control Theory. p.63.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability

assessment, management accounting, control, and reporting. Journal of Cleaner

Production. 136. pp.237-248.

Richardson, A. J., 2017. The relationship between management and financial accounting as

professions and technologies of practice. In The Role of the Management Accountant (pp.

246-261). Routledge.

Steccolini, I., 2019. Accounting and the post-new public management: Re-considering

publicness in accounting research. Accounting, Auditing & Accountability Journal. 32(1).

pp.255-279.

Stockenstrand, A. K. and Nilsson, F. eds., 2017. Bank Regulation: Effects on Strategy,

Financial Accounting and Management Control. Taylor & Francis.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

Online

Difference between Financial Accounting and Management Accounting. 2019. Online.

Available through: < https://keydifferences.com/difference-between-financial-accounting-

and-management-accounting.html >.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.