Accounting Report: Financial, Management Accounting and Analysis

VerifiedAdded on 2023/01/16

|14

|2710

|56

Report

AI Summary

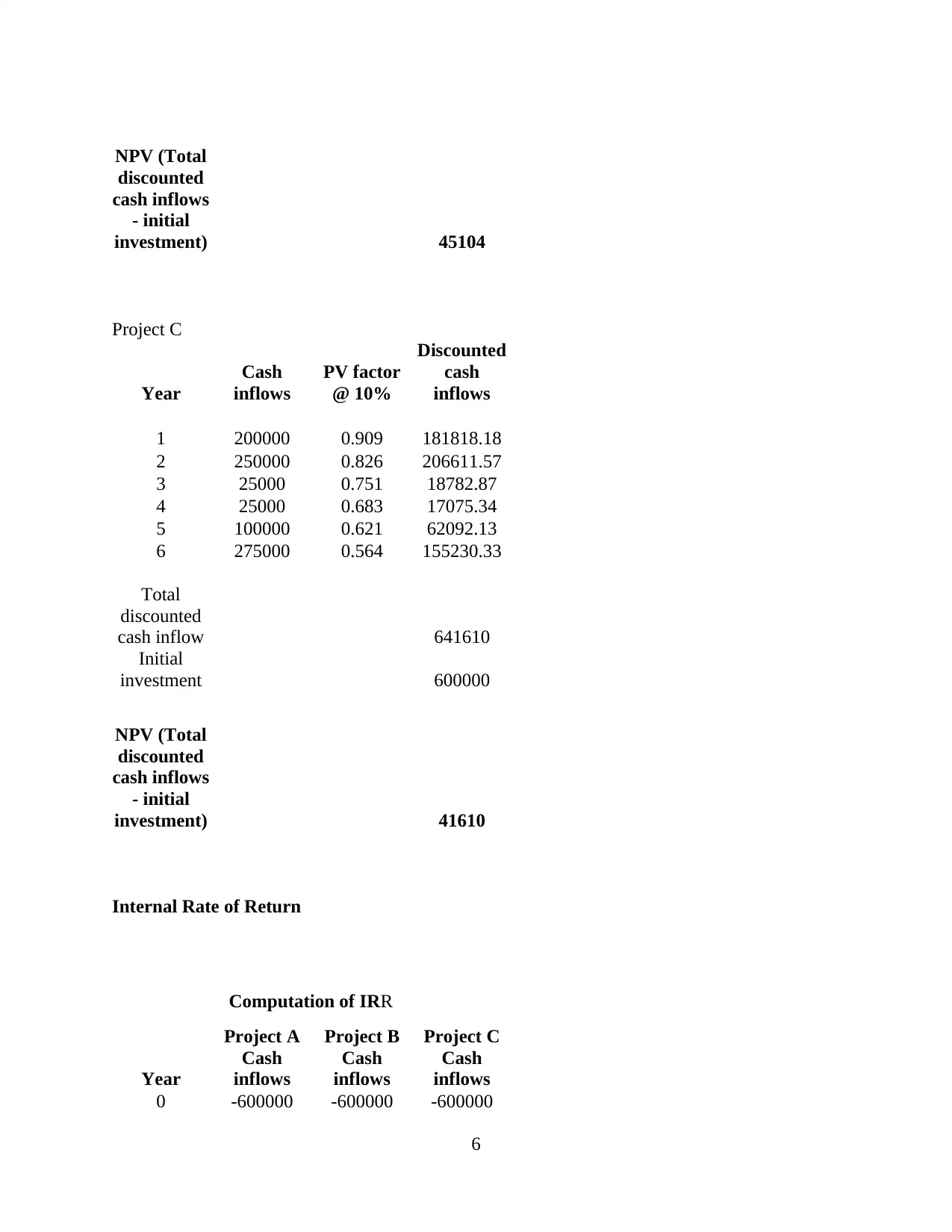

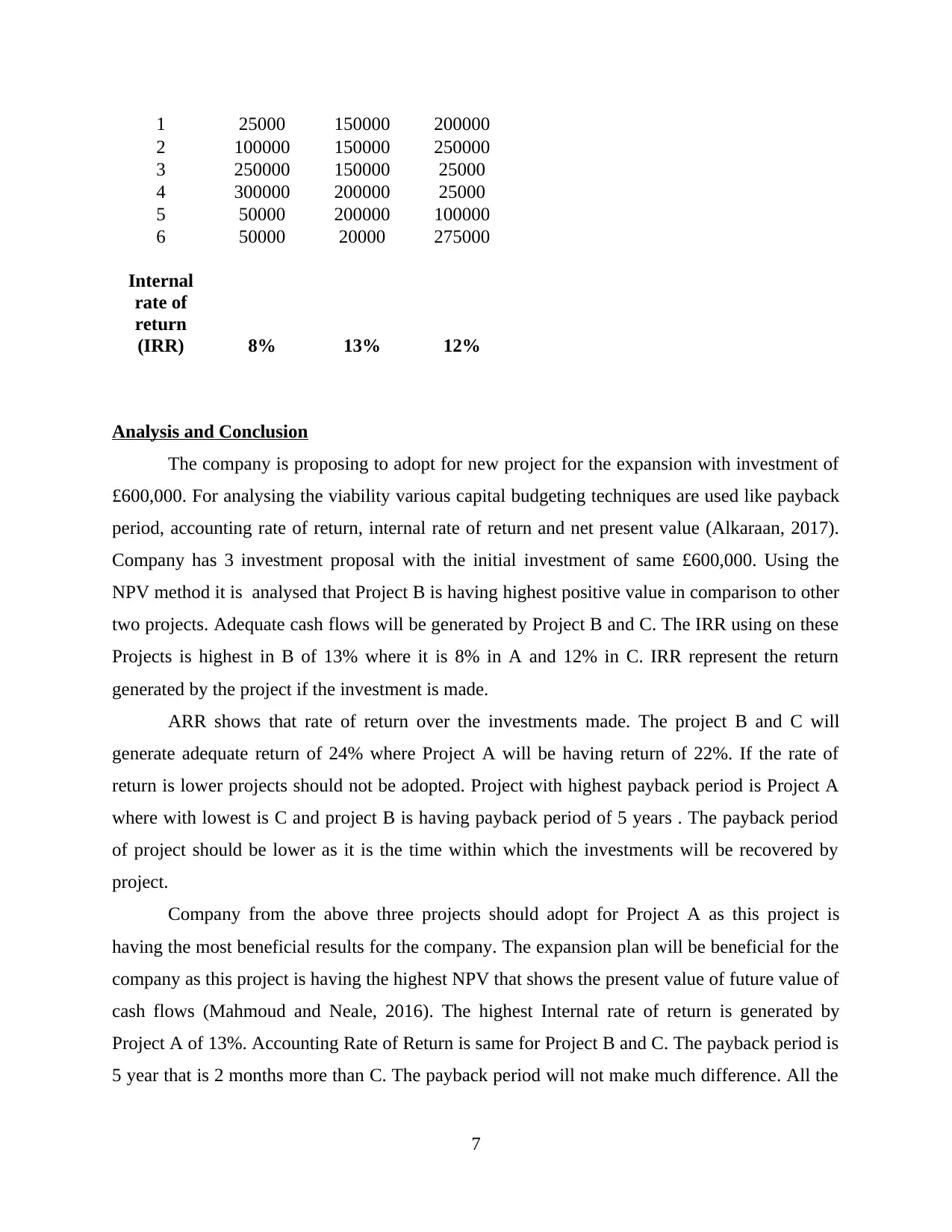

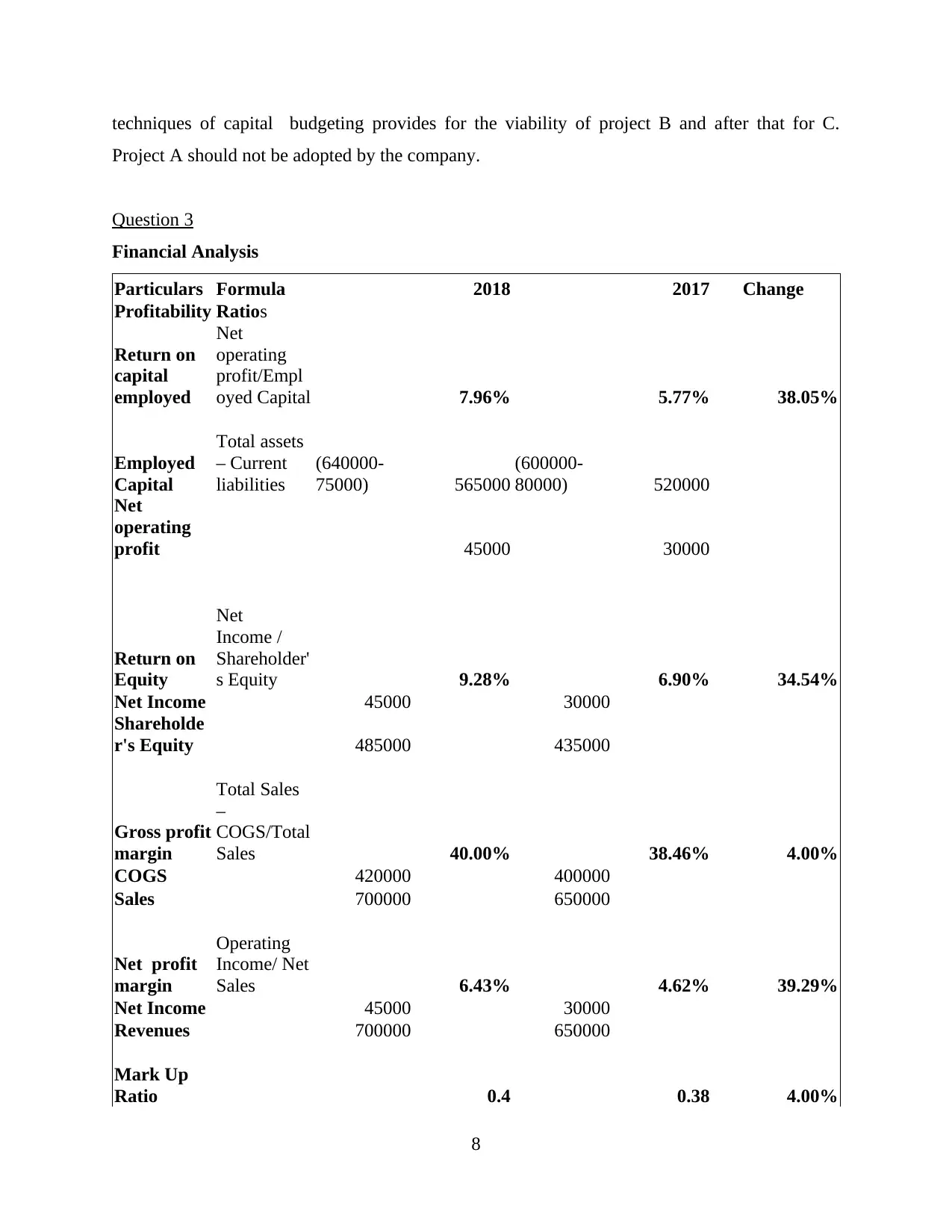

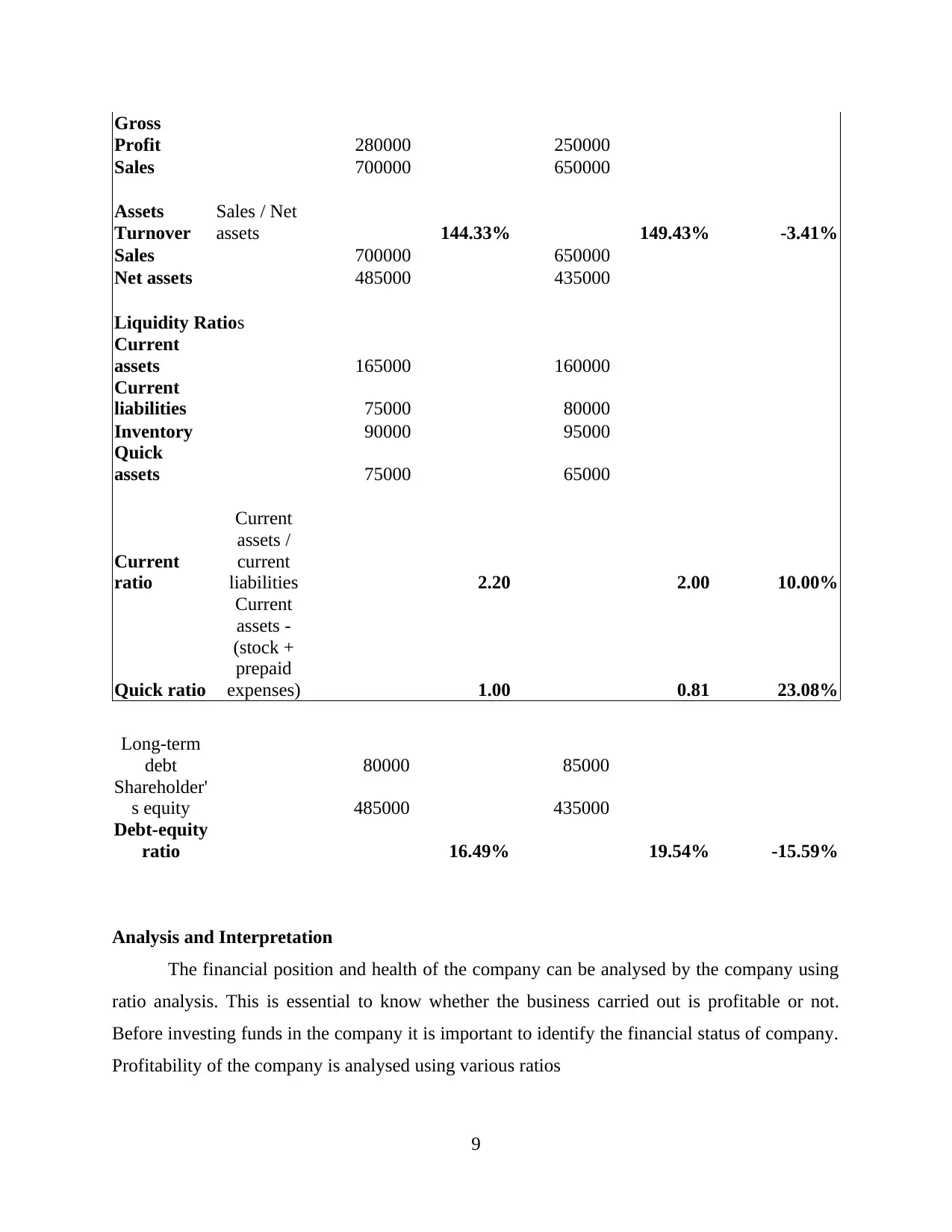

This report provides a comprehensive overview of accounting, focusing on both financial and management accounting. It begins with an executive summary and an introduction to accounting, emphasizing its role in communicating business results. The report then delves into the distinctions between financial and management accounting, outlining their respective functions and the types of information they provide. Financial accounting is presented as a specialized branch that tracks financial transactions, prepares financial statements, and communicates results to external stakeholders. Management accounting, on the other hand, is described as providing financial information to internal managers for decision-making, cost control, and business development. The report includes detailed analysis of investment appraisal techniques, such as payback period, accounting rate of return, net present value, and internal rate of return, to evaluate the viability of three different projects. Finally, the report presents a financial analysis using ratio analysis to assess the company's profitability, liquidity, and efficiency, providing insights into the company's financial health and performance.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.