ACCT20075 Auditing & Ethics: Company Accounts and Audit Report

VerifiedAdded on 2023/06/07

|15

|3791

|310

Report

AI Summary

This report provides a detailed analysis of company accounts, focusing on materiality and audit scope. It includes an analytical review of financial statements, examining liquidity, profitability, and solvency ratios over a four-year period. The report also analyzes the cash flow statement and reviews the auditor's report, highlighting key disclosures and draft notes that could affect the audit process. The analysis considers the financial performance of Met Cash Limited from 2014 to 2017, assessing key financial ratios and indicators to determine the overall health and stability of the business. Desklib is a platform where students can find similar solved assignments and study resources.

Running head: COMPANY ACCOUNTS

Company Accounts

Name of the Student:

Name of the University:

Author’s Note

Company Accounts

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

COMPANY ACCOUNTS

Table of Contents

Section 1..........................................................................................................................................2

Materiality and Scope of Audit....................................................................................................2

Key Disclosures and Draft Notes................................................................................................3

Section 2..........................................................................................................................................4

Analytical Review of the Financial statements...........................................................................4

Section 3..........................................................................................................................................9

Analysis of Cash Flow Statement................................................................................................9

Review of the Auditor’s Report.................................................................................................11

Reference.......................................................................................................................................12

COMPANY ACCOUNTS

Table of Contents

Section 1..........................................................................................................................................2

Materiality and Scope of Audit....................................................................................................2

Key Disclosures and Draft Notes................................................................................................3

Section 2..........................................................................................................................................4

Analytical Review of the Financial statements...........................................................................4

Section 3..........................................................................................................................................9

Analysis of Cash Flow Statement................................................................................................9

Review of the Auditor’s Report.................................................................................................11

Reference.......................................................................................................................................12

2

COMPANY ACCOUNTS

Section 1

Materiality and Scope of Audit

The objectives of this assignment is to conduct audit procedures for the purpose of

ascertaining the materiality level of the financial statements of a company in order to review

whether the financial statements are free from misstatements. The materiality concept is

fundamental to the scope of audit as the auditors determine whether the financial statements are

showing true and fair view on the basis of judgement of the auditor. The company which is

considered for this assessment is Met Cash Limited (Mars-metcdn-com., 2018).

The concept of materiality states that the auditor needs to considers items which forms a

major part of the financial statements and also affects the decision-making capabilities of the

investors. In order to estimate materiality of an item of a financial statement, the auditor needs to

apply his expertise skills and judgements. Materiality is determined on the basis of qualitative

and quantitative aspects of financial statements (Legoria, Melendrez & Reynolds, 2013). The

auditor considers qualitative aspects such as net profits, changes in accounting principles, assets

of the business. As per quantitative aspect of materiality, the auditor considers a percentage

which is used for the purpose of computing the materiality of the business. Normally this is done

at the planning stage for the audit process and planning materiality is computed (Vîlsănoiu &

Buzenche, 2014). Generally qualitative materiality for an item is considered for items which has

a significance in the business or the items which are complex in nature.

During the planning stage of audit, planning materiality and performance materiality is to

be computed. In the calculation of planning materiality, a particular base is considered which is

an item present in the financial statements of the company (Elder et al., 2013). It is normally the

COMPANY ACCOUNTS

Section 1

Materiality and Scope of Audit

The objectives of this assignment is to conduct audit procedures for the purpose of

ascertaining the materiality level of the financial statements of a company in order to review

whether the financial statements are free from misstatements. The materiality concept is

fundamental to the scope of audit as the auditors determine whether the financial statements are

showing true and fair view on the basis of judgement of the auditor. The company which is

considered for this assessment is Met Cash Limited (Mars-metcdn-com., 2018).

The concept of materiality states that the auditor needs to considers items which forms a

major part of the financial statements and also affects the decision-making capabilities of the

investors. In order to estimate materiality of an item of a financial statement, the auditor needs to

apply his expertise skills and judgements. Materiality is determined on the basis of qualitative

and quantitative aspects of financial statements (Legoria, Melendrez & Reynolds, 2013). The

auditor considers qualitative aspects such as net profits, changes in accounting principles, assets

of the business. As per quantitative aspect of materiality, the auditor considers a percentage

which is used for the purpose of computing the materiality of the business. Normally this is done

at the planning stage for the audit process and planning materiality is computed (Vîlsănoiu &

Buzenche, 2014). Generally qualitative materiality for an item is considered for items which has

a significance in the business or the items which are complex in nature.

During the planning stage of audit, planning materiality and performance materiality is to

be computed. In the calculation of planning materiality, a particular base is considered which is

an item present in the financial statements of the company (Elder et al., 2013). It is normally the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

COMPANY ACCOUNTS

policy of most of the auditing firms to take the item which has the highest value for the

computation of planning materiality of a business (Eilifsen & Messier Jr, 2014). On the basis of

planning materiality, performance materiality of a business is computed.

The annual report of Metcash ltd shows the financial performance of the business for the

year 2018. The figure of total assets which is shown in the balance sheet of the company is

shown to be $ 3,719 million which is considered for the purpose of calculating the planning

materiality of a business. In addition to this, the calculations of planning materiality require the

auditor to assume a percentage on the basis of which the planning materiality figure is to be

derived. The computation of planning materiality is shown below:

Planning Materiality=Total Assets of the Business × Percentage considered

¿ $ 3,719 million ×5 %

¿ $ 185.95 million

The planning materiality comes to about $ 185.95 million which will be used by the

auditor to identify performance materiality which is ultimately used for ascertaining if there are

any material misstatements in the financial statements of the company (Jacoby & Levy, 2016).

Key Disclosures and Draft Notes

The key disclosures which are shown in the annual reports of Met Cash ltd which can

affect the audit process are listed below in details:

Commitment, Contingencies and other financial exposures: The operating lease

commitments of the business which is related to warehouses and retail stores is shown to

have decreased significantly from $ 1491.7 million to about $ 1373.1 million in 2018.

COMPANY ACCOUNTS

policy of most of the auditing firms to take the item which has the highest value for the

computation of planning materiality of a business (Eilifsen & Messier Jr, 2014). On the basis of

planning materiality, performance materiality of a business is computed.

The annual report of Metcash ltd shows the financial performance of the business for the

year 2018. The figure of total assets which is shown in the balance sheet of the company is

shown to be $ 3,719 million which is considered for the purpose of calculating the planning

materiality of a business. In addition to this, the calculations of planning materiality require the

auditor to assume a percentage on the basis of which the planning materiality figure is to be

derived. The computation of planning materiality is shown below:

Planning Materiality=Total Assets of the Business × Percentage considered

¿ $ 3,719 million ×5 %

¿ $ 185.95 million

The planning materiality comes to about $ 185.95 million which will be used by the

auditor to identify performance materiality which is ultimately used for ascertaining if there are

any material misstatements in the financial statements of the company (Jacoby & Levy, 2016).

Key Disclosures and Draft Notes

The key disclosures which are shown in the annual reports of Met Cash ltd which can

affect the audit process are listed below in details:

Commitment, Contingencies and other financial exposures: The operating lease

commitments of the business which is related to warehouses and retail stores is shown to

have decreased significantly from $ 1491.7 million to about $ 1373.1 million in 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

COMPANY ACCOUNTS

This is a material disclosure and therefore the auditor needs to verify the same as the

same can affect the financial statements of the business (Lewis, 2013).

Tax: The items of tax which is shown in the financial statements of Met cash ltd shows

current tax expenses of the business, deferred tax expenses. The disclosures which is

shown in the annual reports of the business for tax shows that the company has complex

tax treatments and has introduced a tax funding program. This needs to considered by the

auditor as the complexity of the treatments makes the situation more material in nature

from the perspective of audit.

Interest Bearing Borrowings: The financial statements which is prepared by the

company shows that the business has taken interest bearing borrowings during the year.

The interest-bearing borrowings of the business shows that it comprises of Financial

leases, US private placements, Bilateral loans and also bank loans. The borrowings of the

business are shown in the balance sheet of the company and has the capability of

affecting the entire financial statements of the business. The borrowings of the business

represent a material amount and therefore has the capacity of affecting the financial

statements of the company.

Section 2

Analytical Review of the Financial statements

Analytical procedures are one of the practices which is used in auditing which considers

significant financial ratios to get an overview of the financial performance of the business.

Analytical procedures require the auditor to consider key financial ratios which are indicators of

the health of the business (Sharma & Panigrahi, 2013). Some of the ratios which are considered

are profitability ratios, liquidity ratios, solvency ratios and capital structure ratios.

COMPANY ACCOUNTS

This is a material disclosure and therefore the auditor needs to verify the same as the

same can affect the financial statements of the business (Lewis, 2013).

Tax: The items of tax which is shown in the financial statements of Met cash ltd shows

current tax expenses of the business, deferred tax expenses. The disclosures which is

shown in the annual reports of the business for tax shows that the company has complex

tax treatments and has introduced a tax funding program. This needs to considered by the

auditor as the complexity of the treatments makes the situation more material in nature

from the perspective of audit.

Interest Bearing Borrowings: The financial statements which is prepared by the

company shows that the business has taken interest bearing borrowings during the year.

The interest-bearing borrowings of the business shows that it comprises of Financial

leases, US private placements, Bilateral loans and also bank loans. The borrowings of the

business are shown in the balance sheet of the company and has the capability of

affecting the entire financial statements of the business. The borrowings of the business

represent a material amount and therefore has the capacity of affecting the financial

statements of the company.

Section 2

Analytical Review of the Financial statements

Analytical procedures are one of the practices which is used in auditing which considers

significant financial ratios to get an overview of the financial performance of the business.

Analytical procedures require the auditor to consider key financial ratios which are indicators of

the health of the business (Sharma & Panigrahi, 2013). Some of the ratios which are considered

are profitability ratios, liquidity ratios, solvency ratios and capital structure ratios.

5

COMPANY ACCOUNTS

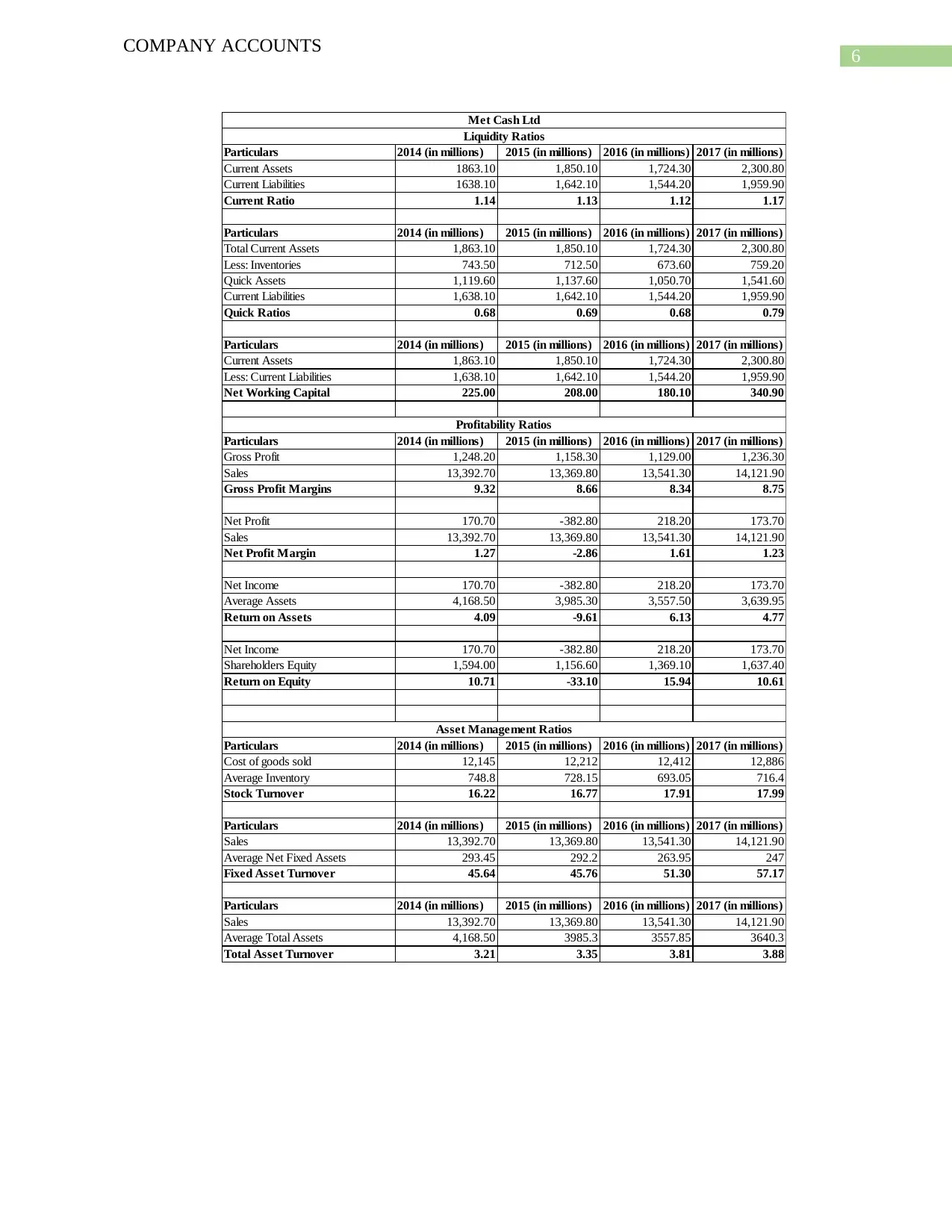

In this case, in order to apply analytical procedures for the business of Met Cash Limited,

financial statements are considered for a period of 4 years starting from 2014 to 2017. The table

below shows the computation of key financial ratios of Met Cash Limited for the four years

period.

COMPANY ACCOUNTS

In this case, in order to apply analytical procedures for the business of Met Cash Limited,

financial statements are considered for a period of 4 years starting from 2014 to 2017. The table

below shows the computation of key financial ratios of Met Cash Limited for the four years

period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

COMPANY ACCOUNTS

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Current Assets 1863.10 1,850.10 1,724.30 2,300.80

Current Liabilities 1638.10 1,642.10 1,544.20 1,959.90

Current Ratio 1.14 1.13 1.12 1.17

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Total Current Assets 1,863.10 1,850.10 1,724.30 2,300.80

Less: Inventories 743.50 712.50 673.60 759.20

Quick Assets 1,119.60 1,137.60 1,050.70 1,541.60

Current Liabilities 1,638.10 1,642.10 1,544.20 1,959.90

Quick Ratios 0.68 0.69 0.68 0.79

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Current Assets 1,863.10 1,850.10 1,724.30 2,300.80

Less: Current Liabilities 1,638.10 1,642.10 1,544.20 1,959.90

Net Working Capital 225.00 208.00 180.10 340.90

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Gross Profit 1,248.20 1,158.30 1,129.00 1,236.30

Sales 13,392.70 13,369.80 13,541.30 14,121.90

Gross Profit Margins 9.32 8.66 8.34 8.75

Net Profit 170.70 -382.80 218.20 173.70

Sales 13,392.70 13,369.80 13,541.30 14,121.90

Net Profit Margin 1.27 -2.86 1.61 1.23

Net Income 170.70 -382.80 218.20 173.70

Average Assets 4,168.50 3,985.30 3,557.50 3,639.95

Return on Assets 4.09 -9.61 6.13 4.77

Net Income 170.70 -382.80 218.20 173.70

Shareholders Equity 1,594.00 1,156.60 1,369.10 1,637.40

Return on Equity 10.71 -33.10 15.94 10.61

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Cost of goods sold 12,145 12,212 12,412 12,886

Average Inventory 748.8 728.15 693.05 716.4

Stock Turnover 16.22 16.77 17.91 17.99

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Sales 13,392.70 13,369.80 13,541.30 14,121.90

Average Net Fixed Assets 293.45 292.2 263.95 247

Fixed Asset Turnover 45.64 45.76 51.30 57.17

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Sales 13,392.70 13,369.80 13,541.30 14,121.90

Average Total Assets 4,168.50 3985.3 3557.85 3640.3

Total Asset Turnover 3.21 3.35 3.81 3.88

Met Cash Ltd

Liquidity Ratios

Profitability Ratios

Asset Management Ratios

COMPANY ACCOUNTS

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Current Assets 1863.10 1,850.10 1,724.30 2,300.80

Current Liabilities 1638.10 1,642.10 1,544.20 1,959.90

Current Ratio 1.14 1.13 1.12 1.17

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Total Current Assets 1,863.10 1,850.10 1,724.30 2,300.80

Less: Inventories 743.50 712.50 673.60 759.20

Quick Assets 1,119.60 1,137.60 1,050.70 1,541.60

Current Liabilities 1,638.10 1,642.10 1,544.20 1,959.90

Quick Ratios 0.68 0.69 0.68 0.79

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Current Assets 1,863.10 1,850.10 1,724.30 2,300.80

Less: Current Liabilities 1,638.10 1,642.10 1,544.20 1,959.90

Net Working Capital 225.00 208.00 180.10 340.90

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Gross Profit 1,248.20 1,158.30 1,129.00 1,236.30

Sales 13,392.70 13,369.80 13,541.30 14,121.90

Gross Profit Margins 9.32 8.66 8.34 8.75

Net Profit 170.70 -382.80 218.20 173.70

Sales 13,392.70 13,369.80 13,541.30 14,121.90

Net Profit Margin 1.27 -2.86 1.61 1.23

Net Income 170.70 -382.80 218.20 173.70

Average Assets 4,168.50 3,985.30 3,557.50 3,639.95

Return on Assets 4.09 -9.61 6.13 4.77

Net Income 170.70 -382.80 218.20 173.70

Shareholders Equity 1,594.00 1,156.60 1,369.10 1,637.40

Return on Equity 10.71 -33.10 15.94 10.61

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Cost of goods sold 12,145 12,212 12,412 12,886

Average Inventory 748.8 728.15 693.05 716.4

Stock Turnover 16.22 16.77 17.91 17.99

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Sales 13,392.70 13,369.80 13,541.30 14,121.90

Average Net Fixed Assets 293.45 292.2 263.95 247

Fixed Asset Turnover 45.64 45.76 51.30 57.17

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Sales 13,392.70 13,369.80 13,541.30 14,121.90

Average Total Assets 4,168.50 3985.3 3557.85 3640.3

Total Asset Turnover 3.21 3.35 3.81 3.88

Met Cash Ltd

Liquidity Ratios

Profitability Ratios

Asset Management Ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

COMPANY ACCOUNTS

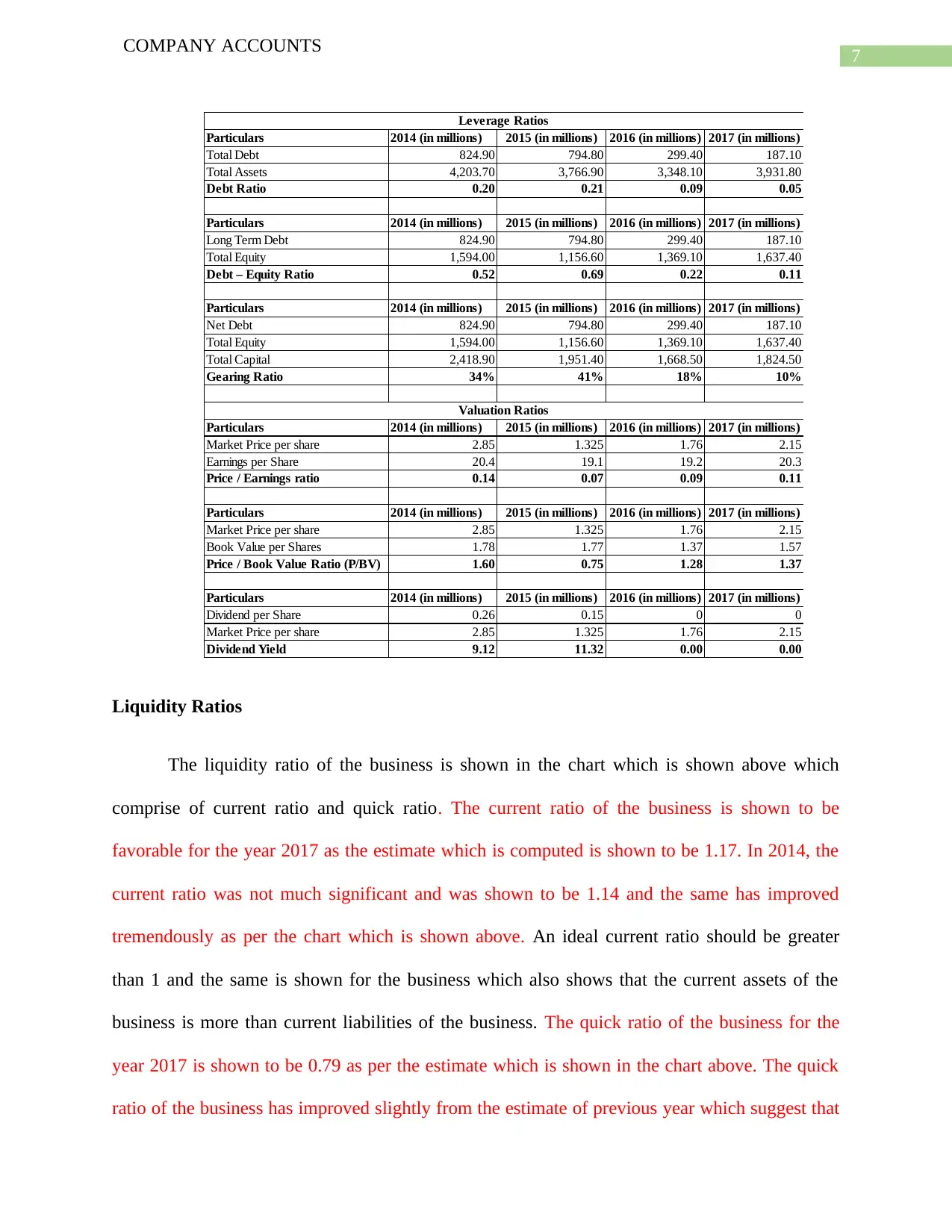

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Total Debt 824.90 794.80 299.40 187.10

Total Assets 4,203.70 3,766.90 3,348.10 3,931.80

Debt Ratio 0.20 0.21 0.09 0.05

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Long Term Debt 824.90 794.80 299.40 187.10

Total Equity 1,594.00 1,156.60 1,369.10 1,637.40

Debt – Equity Ratio 0.52 0.69 0.22 0.11

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Net Debt 824.90 794.80 299.40 187.10

Total Equity 1,594.00 1,156.60 1,369.10 1,637.40

Total Capital 2,418.90 1,951.40 1,668.50 1,824.50

Gearing Ratio 34% 41% 18% 10%

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Market Price per share 2.85 1.325 1.76 2.15

Earnings per Share 20.4 19.1 19.2 20.3

Price / Earnings ratio 0.14 0.07 0.09 0.11

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Market Price per share 2.85 1.325 1.76 2.15

Book Value per Shares 1.78 1.77 1.37 1.57

Price / Book Value Ratio (P/BV) 1.60 0.75 1.28 1.37

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Dividend per Share 0.26 0.15 0 0

Market Price per share 2.85 1.325 1.76 2.15

Dividend Yield 9.12 11.32 0.00 0.00

Valuation Ratios

Leverage Ratios

Liquidity Ratios

The liquidity ratio of the business is shown in the chart which is shown above which

comprise of current ratio and quick ratio. The current ratio of the business is shown to be

favorable for the year 2017 as the estimate which is computed is shown to be 1.17. In 2014, the

current ratio was not much significant and was shown to be 1.14 and the same has improved

tremendously as per the chart which is shown above. An ideal current ratio should be greater

than 1 and the same is shown for the business which also shows that the current assets of the

business is more than current liabilities of the business. The quick ratio of the business for the

year 2017 is shown to be 0.79 as per the estimate which is shown in the chart above. The quick

ratio of the business has improved slightly from the estimate of previous year which suggest that

COMPANY ACCOUNTS

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Total Debt 824.90 794.80 299.40 187.10

Total Assets 4,203.70 3,766.90 3,348.10 3,931.80

Debt Ratio 0.20 0.21 0.09 0.05

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Long Term Debt 824.90 794.80 299.40 187.10

Total Equity 1,594.00 1,156.60 1,369.10 1,637.40

Debt – Equity Ratio 0.52 0.69 0.22 0.11

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Net Debt 824.90 794.80 299.40 187.10

Total Equity 1,594.00 1,156.60 1,369.10 1,637.40

Total Capital 2,418.90 1,951.40 1,668.50 1,824.50

Gearing Ratio 34% 41% 18% 10%

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Market Price per share 2.85 1.325 1.76 2.15

Earnings per Share 20.4 19.1 19.2 20.3

Price / Earnings ratio 0.14 0.07 0.09 0.11

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Market Price per share 2.85 1.325 1.76 2.15

Book Value per Shares 1.78 1.77 1.37 1.57

Price / Book Value Ratio (P/BV) 1.60 0.75 1.28 1.37

Particulars 2014 (in millions) 2015 (in millions) 2016 (in millions) 2017 (in millions)

Dividend per Share 0.26 0.15 0 0

Market Price per share 2.85 1.325 1.76 2.15

Dividend Yield 9.12 11.32 0.00 0.00

Valuation Ratios

Leverage Ratios

Liquidity Ratios

The liquidity ratio of the business is shown in the chart which is shown above which

comprise of current ratio and quick ratio. The current ratio of the business is shown to be

favorable for the year 2017 as the estimate which is computed is shown to be 1.17. In 2014, the

current ratio was not much significant and was shown to be 1.14 and the same has improved

tremendously as per the chart which is shown above. An ideal current ratio should be greater

than 1 and the same is shown for the business which also shows that the current assets of the

business is more than current liabilities of the business. The quick ratio of the business for the

year 2017 is shown to be 0.79 as per the estimate which is shown in the chart above. The quick

ratio of the business has improved slightly from the estimate of previous year which suggest that

8

COMPANY ACCOUNTS

the liquidity position of the business is favorable. The quick ratio considers assets which are

more liquid in nature and does not include stock in the category of current assets (Khidmat &

Rehman, 2014). The quick asset of the business has also increased during the period in

comparison to previous year estimate which is computed. This shows that the business has an

efficient liquidity structure which can meet the current obligations of the business effectively.

The auditor needs to assess whether the current assets and current liabilities of the business are

showing true and fair view or not. The net working capital of the business shows there is an

increase in the same which is a positive sign for the business. The auditor needs to assess the

liquidity position of the business considering the financial statements of the company.

Profitability Ratios

The profitability ratios form an important part of the analysis which is conducted by the

auditor as most of the manipulations are generally in this area. The ratios which are computed

considering this area are gross profit margin, net profit margin, return on equity, return on assets.

The gross margin shows that there has been an increase in the gross profits of the business from

previous year estimates which shows operational efficiency of the business. The net profit

margin of the business is shown to have declined which suggest that there has been an increase

in the costs of the business. The estimate of net profit as calculated for the year 2017 is shown to

be 1.23 which was 1.61 in 2016 as computed in the table above. This can be due to the increase

amount of costs which are incurred by the business during the year (Al Nimer, Warrad & Al

Omari, 2015). The return on assets and return on equity of the business are key financial

indicators of the business and therefore should be considered by the auditor. The return on equity

and return on assets of the business is showed to be on a declining verge which can be attributed

to the fall in the profitability of the business. The auditor needs to apply audit procedures in order

COMPANY ACCOUNTS

the liquidity position of the business is favorable. The quick ratio considers assets which are

more liquid in nature and does not include stock in the category of current assets (Khidmat &

Rehman, 2014). The quick asset of the business has also increased during the period in

comparison to previous year estimate which is computed. This shows that the business has an

efficient liquidity structure which can meet the current obligations of the business effectively.

The auditor needs to assess whether the current assets and current liabilities of the business are

showing true and fair view or not. The net working capital of the business shows there is an

increase in the same which is a positive sign for the business. The auditor needs to assess the

liquidity position of the business considering the financial statements of the company.

Profitability Ratios

The profitability ratios form an important part of the analysis which is conducted by the

auditor as most of the manipulations are generally in this area. The ratios which are computed

considering this area are gross profit margin, net profit margin, return on equity, return on assets.

The gross margin shows that there has been an increase in the gross profits of the business from

previous year estimates which shows operational efficiency of the business. The net profit

margin of the business is shown to have declined which suggest that there has been an increase

in the costs of the business. The estimate of net profit as calculated for the year 2017 is shown to

be 1.23 which was 1.61 in 2016 as computed in the table above. This can be due to the increase

amount of costs which are incurred by the business during the year (Al Nimer, Warrad & Al

Omari, 2015). The return on assets and return on equity of the business are key financial

indicators of the business and therefore should be considered by the auditor. The return on equity

and return on assets of the business is showed to be on a declining verge which can be attributed

to the fall in the profitability of the business. The auditor needs to apply audit procedures in order

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

COMPANY ACCOUNTS

to check the viability of expenses which is incurred by the business during the period. This is to

be done in order to ensure that the profits or losses which are shown in the financial statements

are not vague in nature. In order to obtain a clear understanding of the expenses and sales figures

which the management of the company has shown in the financial statements, the auditor needs

to apply vouching procedures in order to justify the sales and different expenses figures which

are shown in the annual reports of the company.

Asset Management Ratios

The asset management ratios of a business comprise of stock turnover ratio, asset

turnover ratio which is related to the business. These ratios show how efficiently the

management utilizes the assets of the business for the purpose of generating revenues of the

business. The inventories of the business are always considered to be integral part of the

financial statements and are most vulnerable to material misstatement.

The auditor of business needs to verify the balances which are shown for inventories and

assets of the business in order to ensure that the same are fairly represented. The auditor can also

check the balances of inventory by conducting a physical take of the stock in order to value the

same. In case of valuation of assets of the business, the auditor can take the help of an expert in

the field in order to confirm the valuation of the assets of the business.

Leverage Ratios

The leverage ratios of the business are generally associated with the capital structure

which is used by businesses and the capital includes both equity capital and debt capital of a

business. The ratios which are considered in case of such a business are related to debt ratio, debt

to equity ratios and gearing ratio. The debt ratio shows that the level of borrowings of the

COMPANY ACCOUNTS

to check the viability of expenses which is incurred by the business during the period. This is to

be done in order to ensure that the profits or losses which are shown in the financial statements

are not vague in nature. In order to obtain a clear understanding of the expenses and sales figures

which the management of the company has shown in the financial statements, the auditor needs

to apply vouching procedures in order to justify the sales and different expenses figures which

are shown in the annual reports of the company.

Asset Management Ratios

The asset management ratios of a business comprise of stock turnover ratio, asset

turnover ratio which is related to the business. These ratios show how efficiently the

management utilizes the assets of the business for the purpose of generating revenues of the

business. The inventories of the business are always considered to be integral part of the

financial statements and are most vulnerable to material misstatement.

The auditor of business needs to verify the balances which are shown for inventories and

assets of the business in order to ensure that the same are fairly represented. The auditor can also

check the balances of inventory by conducting a physical take of the stock in order to value the

same. In case of valuation of assets of the business, the auditor can take the help of an expert in

the field in order to confirm the valuation of the assets of the business.

Leverage Ratios

The leverage ratios of the business are generally associated with the capital structure

which is used by businesses and the capital includes both equity capital and debt capital of a

business. The ratios which are considered in case of such a business are related to debt ratio, debt

to equity ratios and gearing ratio. The debt ratio shows that the level of borrowings of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

COMPANY ACCOUNTS

company has decreased significantly which shows that the company is relying more on equity

capital of the business. The debt to equity ratio also shows a similar figure during the year and

the estimate for 2017 is shown to be 0.11.

The auditor needs to assess the capital structure of the business and identify any risks

which can affect the business and overall audit process of the business. The figure of borrowings

of the business has decreased and this is the reason due to which the for the fall in the debt ratio

of the business. The auditor needs to check the repayment schedule for the company and also

check whether the business has taken any additional loan for the business.

Valuation Ratios

The valuation ratio of the business comprises of price-earnings ratio, price to book value

ratio which are considered important from the perspective of a business. The price earning ratio

of the company is shown to have increased and the same is shown to be 0.11 for the year 2017.

The price to book value ratio has also increased. The auditor needs to consider the earning per

shares which is shown by the business and ensure that that figure is correct. EPS is considered by

investors before taking investment decisions and therefore the auditor needs to check the same.

Section 3

Analysis of Cash Flow Statement

Cash flow statement is a part of the financial statements of a business and statement

reveals the cash position of the business. The statements show the various sources from which

cash comes in to the business and also the sources of cash outflows of the business. The cash

flow statement of Metcash ltd is effectively shown in the annual reports for 2018 classifying the

activities as operating, financing and investing activities.

COMPANY ACCOUNTS

company has decreased significantly which shows that the company is relying more on equity

capital of the business. The debt to equity ratio also shows a similar figure during the year and

the estimate for 2017 is shown to be 0.11.

The auditor needs to assess the capital structure of the business and identify any risks

which can affect the business and overall audit process of the business. The figure of borrowings

of the business has decreased and this is the reason due to which the for the fall in the debt ratio

of the business. The auditor needs to check the repayment schedule for the company and also

check whether the business has taken any additional loan for the business.

Valuation Ratios

The valuation ratio of the business comprises of price-earnings ratio, price to book value

ratio which are considered important from the perspective of a business. The price earning ratio

of the company is shown to have increased and the same is shown to be 0.11 for the year 2017.

The price to book value ratio has also increased. The auditor needs to consider the earning per

shares which is shown by the business and ensure that that figure is correct. EPS is considered by

investors before taking investment decisions and therefore the auditor needs to check the same.

Section 3

Analysis of Cash Flow Statement

Cash flow statement is a part of the financial statements of a business and statement

reveals the cash position of the business. The statements show the various sources from which

cash comes in to the business and also the sources of cash outflows of the business. The cash

flow statement of Metcash ltd is effectively shown in the annual reports for 2018 classifying the

activities as operating, financing and investing activities.

11

COMPANY ACCOUNTS

The cash inflows from operating activities of the business shows the maximum cash

inflows of the business which is receipts from the customers and the same is shown to be $

15,765.9 million. The category of cash activities which has the greatest cash outflow is shown in

cash from operating activities and the same is cash paid to employees and suppliers (Bhandari &

Iyer, 2013). The primary cash receipts and cash payments which are shown in the annual reports

of the business are cash received from customers and cash payments made to suppliers which are

shown in the cash from operating activities of the business.

The main cash flows which are related to investing activities of the business are shown to

be payments which are made by the business towards acquisition of assets and in case of

financing activities the major cash flows which is shown in cash flow statement of the business is

shown to be payments of dividends which are made to owners of parent companies.

The going concern principle is considered to a fundamental principle in accounting and

therefore the auditor needs to ensure that this principle of the business is not affected. As per the

significant ratios which are computed for Met Cash Ltd, the liquidity ratio of the business is

shown to be favorable which shows that the company is not facing any liquidity problems. The

business has incurred a loss in the current year but that is due to the increase in the expenses of

the business. The management has made dividend payments during the year which suggest that

the business has adequate reserves. Thus, only on the basis of the loss, it cannot be judged

whether the going concern principle of the business is in jeopardy or not. However, the auditor

needs to identify the negative financial indicators which are a sign that the going concern

principle is affected.

COMPANY ACCOUNTS

The cash inflows from operating activities of the business shows the maximum cash

inflows of the business which is receipts from the customers and the same is shown to be $

15,765.9 million. The category of cash activities which has the greatest cash outflow is shown in

cash from operating activities and the same is cash paid to employees and suppliers (Bhandari &

Iyer, 2013). The primary cash receipts and cash payments which are shown in the annual reports

of the business are cash received from customers and cash payments made to suppliers which are

shown in the cash from operating activities of the business.

The main cash flows which are related to investing activities of the business are shown to

be payments which are made by the business towards acquisition of assets and in case of

financing activities the major cash flows which is shown in cash flow statement of the business is

shown to be payments of dividends which are made to owners of parent companies.

The going concern principle is considered to a fundamental principle in accounting and

therefore the auditor needs to ensure that this principle of the business is not affected. As per the

significant ratios which are computed for Met Cash Ltd, the liquidity ratio of the business is

shown to be favorable which shows that the company is not facing any liquidity problems. The

business has incurred a loss in the current year but that is due to the increase in the expenses of

the business. The management has made dividend payments during the year which suggest that

the business has adequate reserves. Thus, only on the basis of the loss, it cannot be judged

whether the going concern principle of the business is in jeopardy or not. However, the auditor

needs to identify the negative financial indicators which are a sign that the going concern

principle is affected.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.