Financial Analysis: Metropolis Health System Prosthetic Department

VerifiedAdded on 2022/08/12

|8

|1993

|439

Case Study

AI Summary

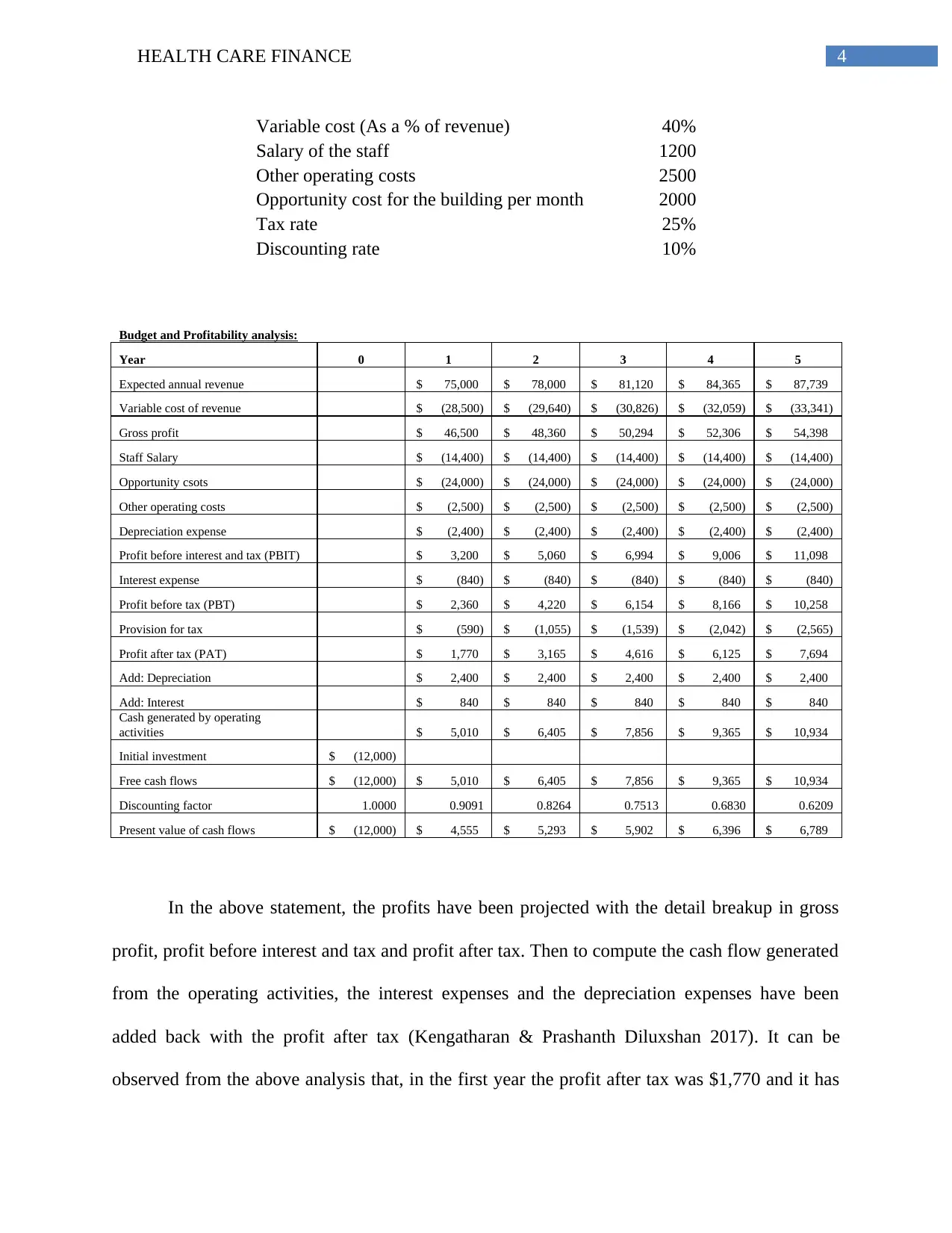

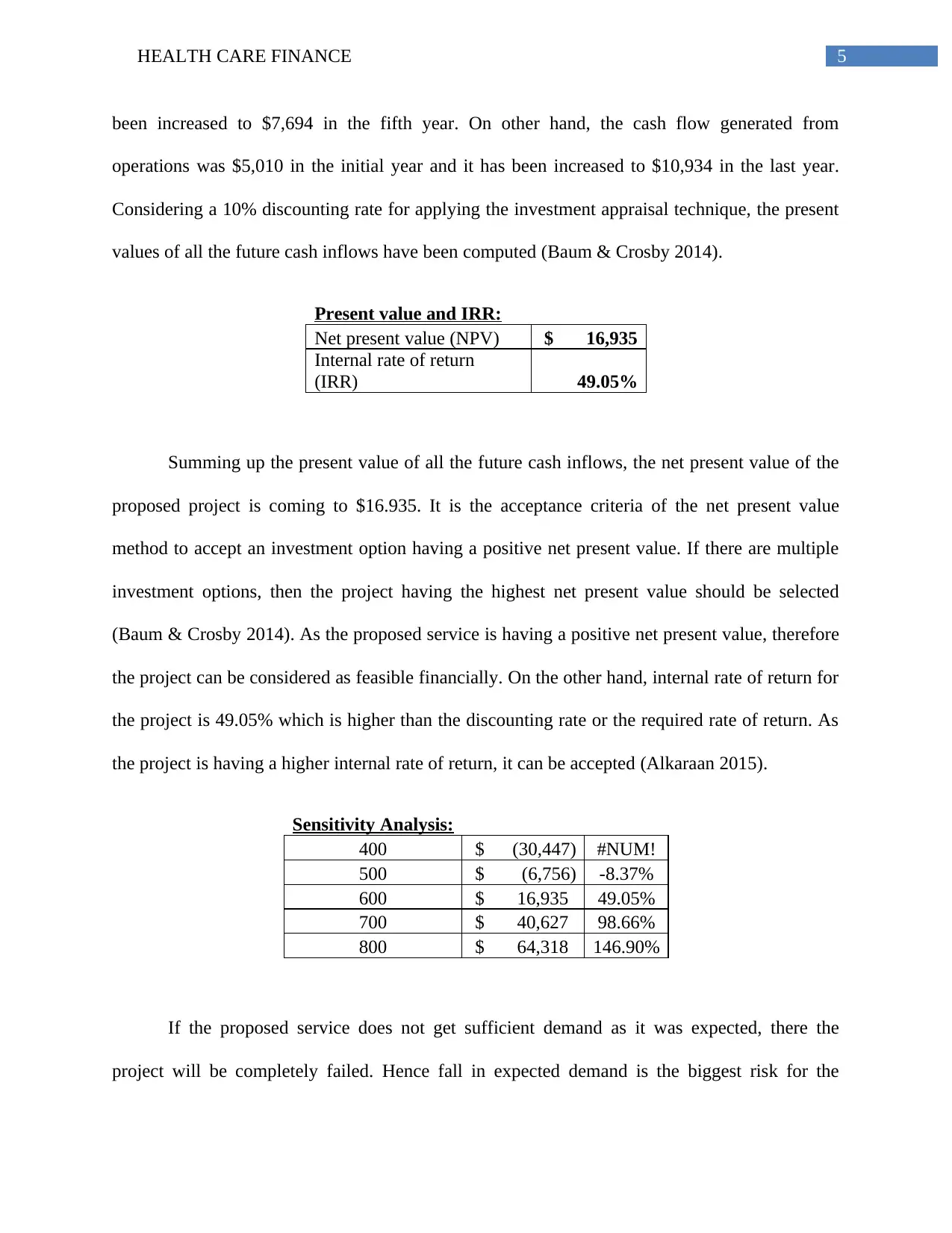

This case study analyzes the financial feasibility of establishing a prosthetic and assisted equipment department within the Metropolis Health System (MHS). The study begins by outlining the goals of the project, which aims to enhance MHS's service offerings and expand its business. It then details the costs associated with the project, including equipment purchases, room costs, and initial expenses. A comprehensive budget and financial analysis is presented, projecting revenue, expenses, and profitability over five years. Key assumptions such as service price, demand growth, and financing terms are clearly stated. The analysis calculates profit after tax, cash flow, Net Present Value (NPV), and Internal Rate of Return (IRR) to assess the project's financial viability. A sensitivity analysis is also conducted to evaluate the impact of changes in demand on the project's profitability. The study concludes that the project is financially feasible, recommending its implementation as a business expansion strategy for MHS. References and bibliography are included.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.