Multinational Companies are known to create wealth

VerifiedAdded on 2022/09/18

|18

|4093

|22

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: INTERNATIONAL FINANCE

International Finance

Name of the Student:

Name of the University:

Author’s Note:

International Finance

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1INTERNATIONAL FINANCE

Table of Contents

Part A...............................................................................................................................................2

Question 1........................................................................................................................................2

Question 2........................................................................................................................................4

Question 3........................................................................................................................................9

Question 5......................................................................................................................................11

References......................................................................................................................................13

Table of Contents

Part A...............................................................................................................................................2

Question 1........................................................................................................................................2

Question 2........................................................................................................................................4

Question 3........................................................................................................................................9

Question 5......................................................................................................................................11

References......................................................................................................................................13

2INTERNATIONAL FINANCE

Part A

Question 1

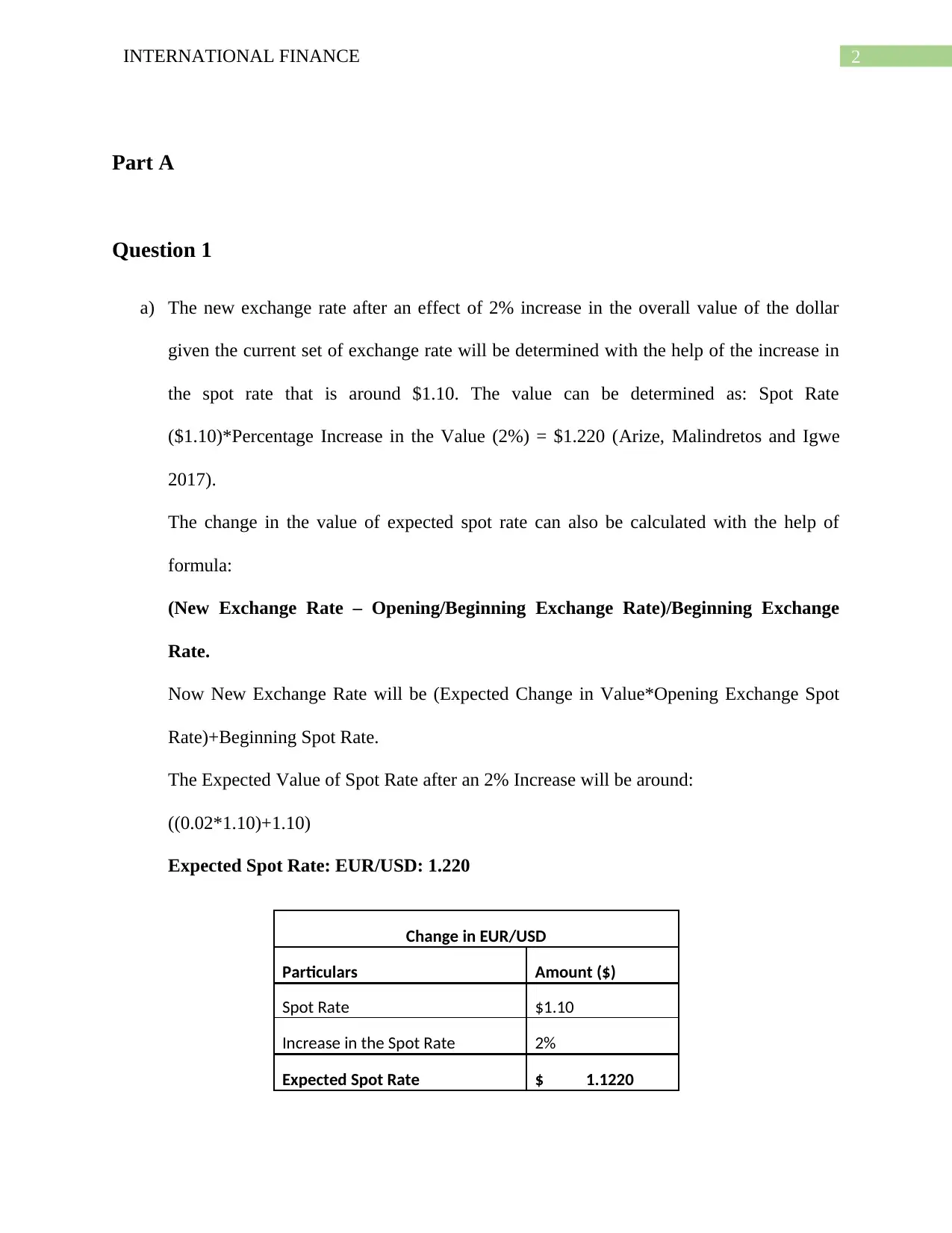

a) The new exchange rate after an effect of 2% increase in the overall value of the dollar

given the current set of exchange rate will be determined with the help of the increase in

the spot rate that is around $1.10. The value can be determined as: Spot Rate

($1.10)*Percentage Increase in the Value (2%) = $1.220 (Arize, Malindretos and Igwe

2017).

The change in the value of expected spot rate can also be calculated with the help of

formula:

(New Exchange Rate – Opening/Beginning Exchange Rate)/Beginning Exchange

Rate.

Now New Exchange Rate will be (Expected Change in Value*Opening Exchange Spot

Rate)+Beginning Spot Rate.

The Expected Value of Spot Rate after an 2% Increase will be around:

((0.02*1.10)+1.10)

Expected Spot Rate: EUR/USD: 1.220

Change in EUR/USD

Particulars Amount ($)

Spot Rate $1.10

Increase in the Spot Rate 2%

Expected Spot Rate $ 1.1220

Part A

Question 1

a) The new exchange rate after an effect of 2% increase in the overall value of the dollar

given the current set of exchange rate will be determined with the help of the increase in

the spot rate that is around $1.10. The value can be determined as: Spot Rate

($1.10)*Percentage Increase in the Value (2%) = $1.220 (Arize, Malindretos and Igwe

2017).

The change in the value of expected spot rate can also be calculated with the help of

formula:

(New Exchange Rate – Opening/Beginning Exchange Rate)/Beginning Exchange

Rate.

Now New Exchange Rate will be (Expected Change in Value*Opening Exchange Spot

Rate)+Beginning Spot Rate.

The Expected Value of Spot Rate after an 2% Increase will be around:

((0.02*1.10)+1.10)

Expected Spot Rate: EUR/USD: 1.220

Change in EUR/USD

Particulars Amount ($)

Spot Rate $1.10

Increase in the Spot Rate 2%

Expected Spot Rate $ 1.1220

3INTERNATIONAL FINANCE

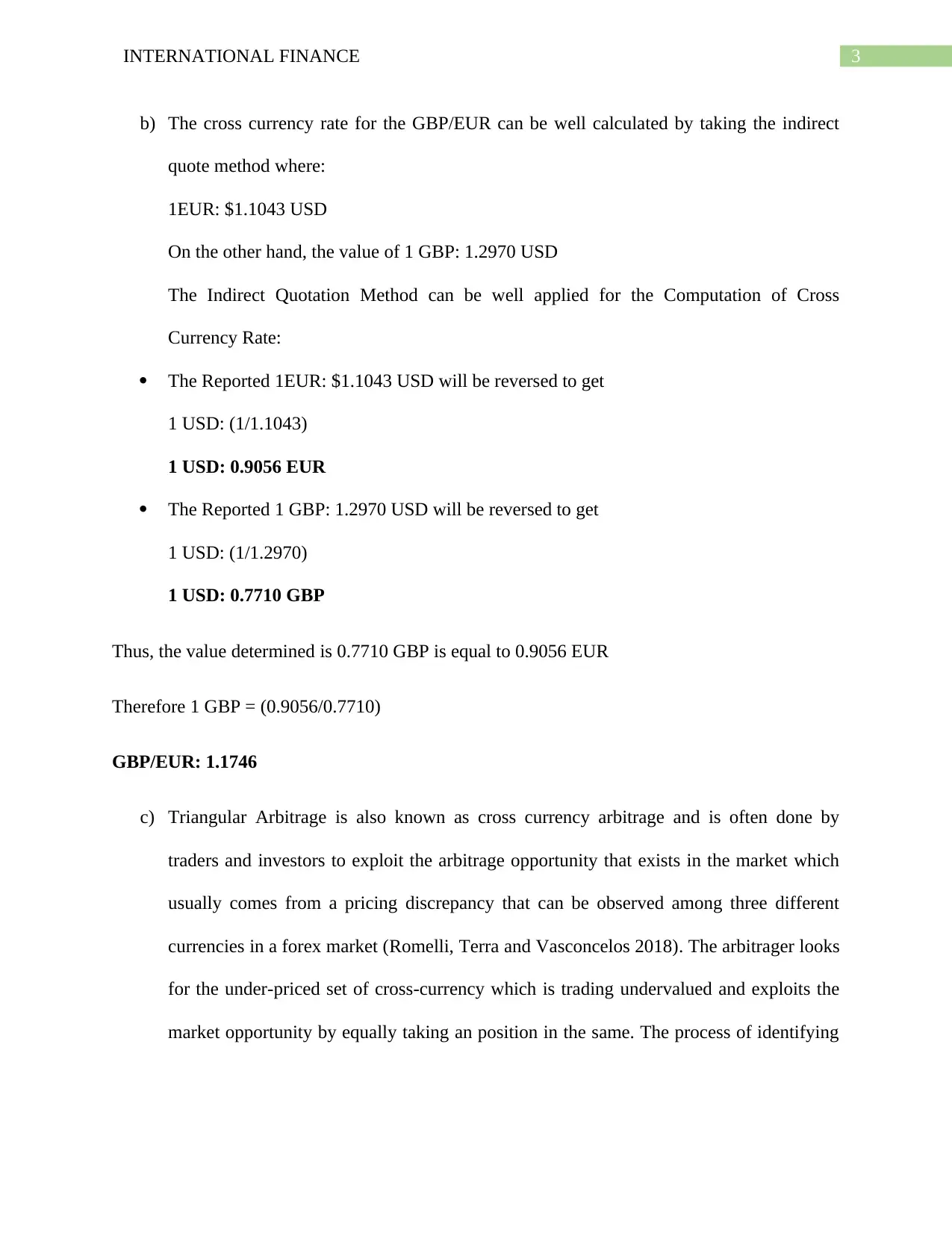

b) The cross currency rate for the GBP/EUR can be well calculated by taking the indirect

quote method where:

1EUR: $1.1043 USD

On the other hand, the value of 1 GBP: 1.2970 USD

The Indirect Quotation Method can be well applied for the Computation of Cross

Currency Rate:

The Reported 1EUR: $1.1043 USD will be reversed to get

1 USD: (1/1.1043)

1 USD: 0.9056 EUR

The Reported 1 GBP: 1.2970 USD will be reversed to get

1 USD: (1/1.2970)

1 USD: 0.7710 GBP

Thus, the value determined is 0.7710 GBP is equal to 0.9056 EUR

Therefore 1 GBP = (0.9056/0.7710)

GBP/EUR: 1.1746

c) Triangular Arbitrage is also known as cross currency arbitrage and is often done by

traders and investors to exploit the arbitrage opportunity that exists in the market which

usually comes from a pricing discrepancy that can be observed among three different

currencies in a forex market (Romelli, Terra and Vasconcelos 2018). The arbitrager looks

for the under-priced set of cross-currency which is trading undervalued and exploits the

market opportunity by equally taking an position in the same. The process of identifying

b) The cross currency rate for the GBP/EUR can be well calculated by taking the indirect

quote method where:

1EUR: $1.1043 USD

On the other hand, the value of 1 GBP: 1.2970 USD

The Indirect Quotation Method can be well applied for the Computation of Cross

Currency Rate:

The Reported 1EUR: $1.1043 USD will be reversed to get

1 USD: (1/1.1043)

1 USD: 0.9056 EUR

The Reported 1 GBP: 1.2970 USD will be reversed to get

1 USD: (1/1.2970)

1 USD: 0.7710 GBP

Thus, the value determined is 0.7710 GBP is equal to 0.9056 EUR

Therefore 1 GBP = (0.9056/0.7710)

GBP/EUR: 1.1746

c) Triangular Arbitrage is also known as cross currency arbitrage and is often done by

traders and investors to exploit the arbitrage opportunity that exists in the market which

usually comes from a pricing discrepancy that can be observed among three different

currencies in a forex market (Romelli, Terra and Vasconcelos 2018). The arbitrager looks

for the under-priced set of cross-currency which is trading undervalued and exploits the

market opportunity by equally taking an position in the same. The process of identifying

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4INTERNATIONAL FINANCE

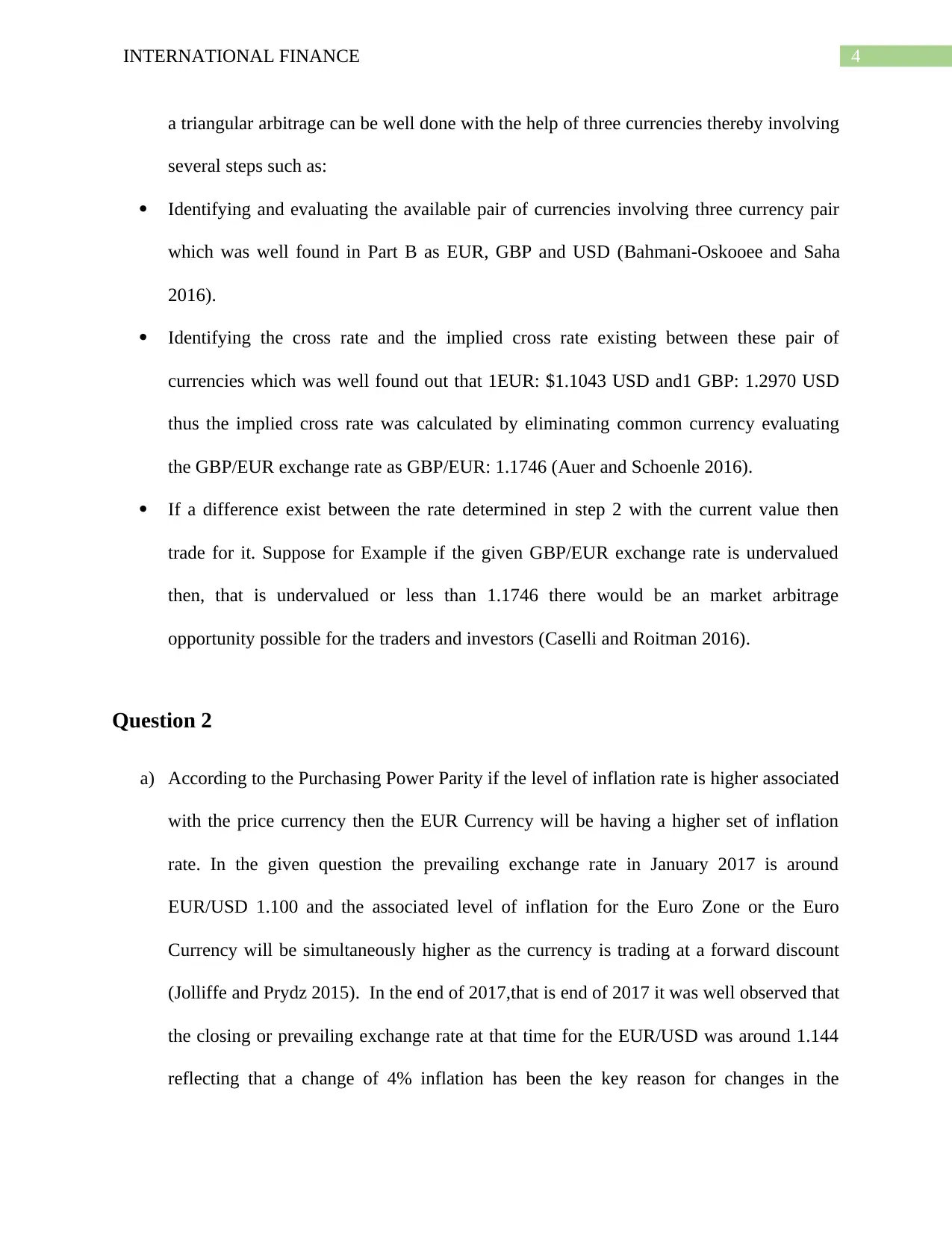

a triangular arbitrage can be well done with the help of three currencies thereby involving

several steps such as:

Identifying and evaluating the available pair of currencies involving three currency pair

which was well found in Part B as EUR, GBP and USD (Bahmani-Oskooee and Saha

2016).

Identifying the cross rate and the implied cross rate existing between these pair of

currencies which was well found out that 1EUR: $1.1043 USD and1 GBP: 1.2970 USD

thus the implied cross rate was calculated by eliminating common currency evaluating

the GBP/EUR exchange rate as GBP/EUR: 1.1746 (Auer and Schoenle 2016).

If a difference exist between the rate determined in step 2 with the current value then

trade for it. Suppose for Example if the given GBP/EUR exchange rate is undervalued

then, that is undervalued or less than 1.1746 there would be an market arbitrage

opportunity possible for the traders and investors (Caselli and Roitman 2016).

Question 2

a) According to the Purchasing Power Parity if the level of inflation rate is higher associated

with the price currency then the EUR Currency will be having a higher set of inflation

rate. In the given question the prevailing exchange rate in January 2017 is around

EUR/USD 1.100 and the associated level of inflation for the Euro Zone or the Euro

Currency will be simultaneously higher as the currency is trading at a forward discount

(Jolliffe and Prydz 2015). In the end of 2017,that is end of 2017 it was well observed that

the closing or prevailing exchange rate at that time for the EUR/USD was around 1.144

reflecting that a change of 4% inflation has been the key reason for changes in the

a triangular arbitrage can be well done with the help of three currencies thereby involving

several steps such as:

Identifying and evaluating the available pair of currencies involving three currency pair

which was well found in Part B as EUR, GBP and USD (Bahmani-Oskooee and Saha

2016).

Identifying the cross rate and the implied cross rate existing between these pair of

currencies which was well found out that 1EUR: $1.1043 USD and1 GBP: 1.2970 USD

thus the implied cross rate was calculated by eliminating common currency evaluating

the GBP/EUR exchange rate as GBP/EUR: 1.1746 (Auer and Schoenle 2016).

If a difference exist between the rate determined in step 2 with the current value then

trade for it. Suppose for Example if the given GBP/EUR exchange rate is undervalued

then, that is undervalued or less than 1.1746 there would be an market arbitrage

opportunity possible for the traders and investors (Caselli and Roitman 2016).

Question 2

a) According to the Purchasing Power Parity if the level of inflation rate is higher associated

with the price currency then the EUR Currency will be having a higher set of inflation

rate. In the given question the prevailing exchange rate in January 2017 is around

EUR/USD 1.100 and the associated level of inflation for the Euro Zone or the Euro

Currency will be simultaneously higher as the currency is trading at a forward discount

(Jolliffe and Prydz 2015). In the end of 2017,that is end of 2017 it was well observed that

the closing or prevailing exchange rate at that time for the EUR/USD was around 1.144

reflecting that a change of 4% inflation has been the key reason for changes in the

5INTERNATIONAL FINANCE

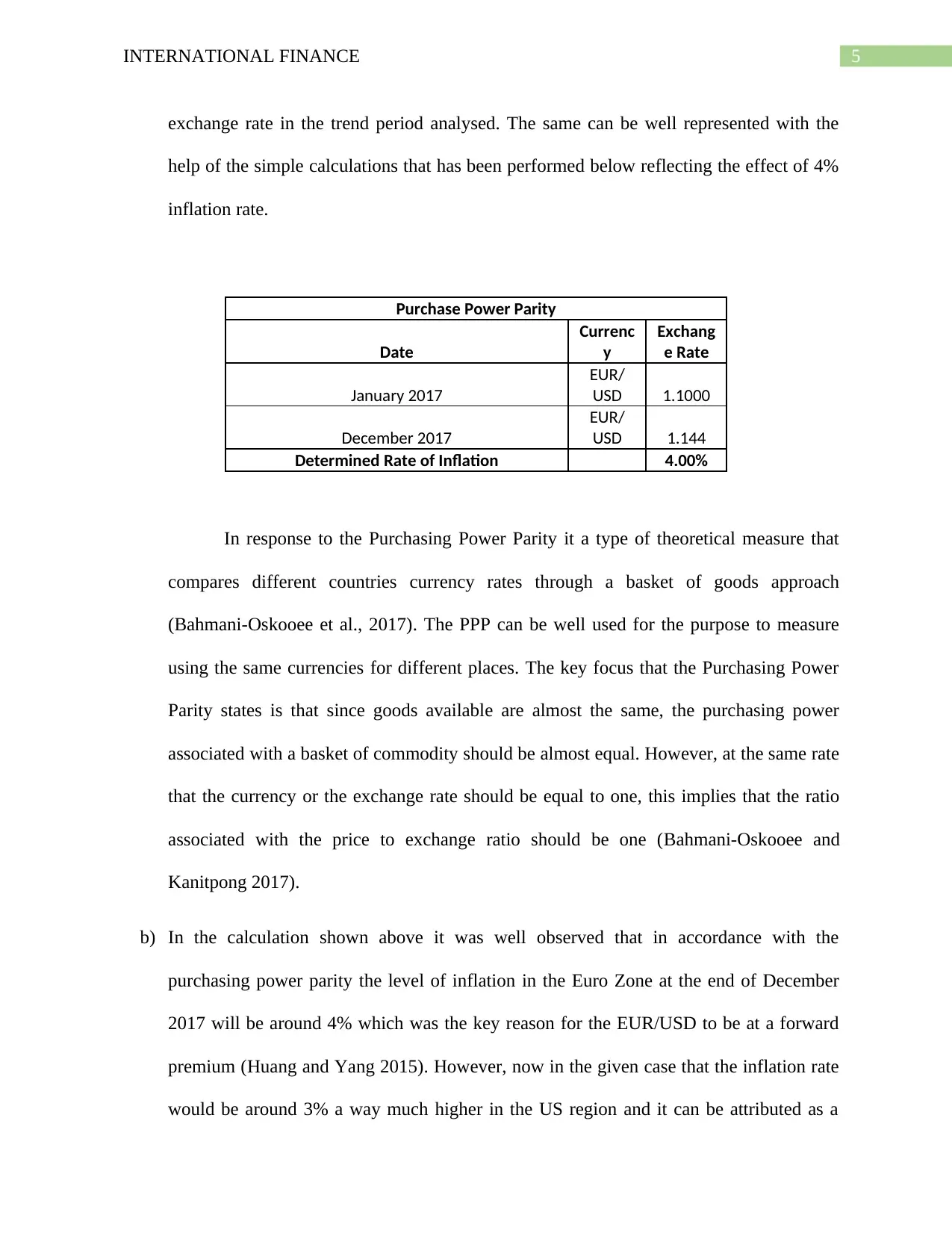

exchange rate in the trend period analysed. The same can be well represented with the

help of the simple calculations that has been performed below reflecting the effect of 4%

inflation rate.

Purchase Power Parity

Date

Currenc

y

Exchang

e Rate

January 2017

EUR/

USD 1.1000

December 2017

EUR/

USD 1.144

Determined Rate of Inflation 4.00%

In response to the Purchasing Power Parity it a type of theoretical measure that

compares different countries currency rates through a basket of goods approach

(Bahmani-Oskooee et al., 2017). The PPP can be well used for the purpose to measure

using the same currencies for different places. The key focus that the Purchasing Power

Parity states is that since goods available are almost the same, the purchasing power

associated with a basket of commodity should be almost equal. However, at the same rate

that the currency or the exchange rate should be equal to one, this implies that the ratio

associated with the price to exchange ratio should be one (Bahmani-Oskooee and

Kanitpong 2017).

b) In the calculation shown above it was well observed that in accordance with the

purchasing power parity the level of inflation in the Euro Zone at the end of December

2017 will be around 4% which was the key reason for the EUR/USD to be at a forward

premium (Huang and Yang 2015). However, now in the given case that the inflation rate

would be around 3% a way much higher in the US region and it can be attributed as a

exchange rate in the trend period analysed. The same can be well represented with the

help of the simple calculations that has been performed below reflecting the effect of 4%

inflation rate.

Purchase Power Parity

Date

Currenc

y

Exchang

e Rate

January 2017

EUR/

USD 1.1000

December 2017

EUR/

USD 1.144

Determined Rate of Inflation 4.00%

In response to the Purchasing Power Parity it a type of theoretical measure that

compares different countries currency rates through a basket of goods approach

(Bahmani-Oskooee et al., 2017). The PPP can be well used for the purpose to measure

using the same currencies for different places. The key focus that the Purchasing Power

Parity states is that since goods available are almost the same, the purchasing power

associated with a basket of commodity should be almost equal. However, at the same rate

that the currency or the exchange rate should be equal to one, this implies that the ratio

associated with the price to exchange ratio should be one (Bahmani-Oskooee and

Kanitpong 2017).

b) In the calculation shown above it was well observed that in accordance with the

purchasing power parity the level of inflation in the Euro Zone at the end of December

2017 will be around 4% which was the key reason for the EUR/USD to be at a forward

premium (Huang and Yang 2015). However, now in the given case that the inflation rate

would be around 3% a way much higher in the US region and it can be attributed as a

6INTERNATIONAL FINANCE

excess inflation in the US zone which would ultimately make the prices of goods and

services much more expensive in the US region (Kakwani and Son 2016). The same can

also be taken in the form of analysis where the 3% inflation rate would be discounted in

the EUR/USD currency exchange rate as follows:

Expected Rise in Inflation in the US Zone: 3% Increase

EUR /USD

Inflation Adjustment of 3% higher means: 1.1*0.97: 1.067

In January 2017, the value of the EUR/USD will be around 1.067.

The expected rise in the level of inflation level would be affecting the prices of the goods

and services in the US Region thereby it would also affect the value of the US dollar making the

US Dollar Depreciate where previously we could easily get $1.1 for 1 Euro however due to the

increase in the inflation rate by around 3% we could only get now $1.067 for 1Euro (Jiang,

Bahmani-Oskooee and Chang 2015). The change in the value of dollar is by around ($1.10-

$1.067): $0.033. In the given set of quotation observed for the EUR/USD Currency Exchange

rate it could be well observed that the Euro Currency is at a forward premium due to which the

higher rate of inflation expected. Thus, it is very important that the inflation rate in the US would

be much higher for contradicting the interest rate in the Euro Zone.

c) The changes in the exchange rate could be well implied with the help of the given macro-

economic factors such as the interest rate changes and change in the inflation rate of the

economy. The exchange rate plays a vital role in the country’s level of trade that is

crucial to most every free market economy in the world. This has been the key reason

which changes in the exchange rate has also been given a prior priority. The changes in

demand currency can be well described with help of given graph below:

excess inflation in the US zone which would ultimately make the prices of goods and

services much more expensive in the US region (Kakwani and Son 2016). The same can

also be taken in the form of analysis where the 3% inflation rate would be discounted in

the EUR/USD currency exchange rate as follows:

Expected Rise in Inflation in the US Zone: 3% Increase

EUR /USD

Inflation Adjustment of 3% higher means: 1.1*0.97: 1.067

In January 2017, the value of the EUR/USD will be around 1.067.

The expected rise in the level of inflation level would be affecting the prices of the goods

and services in the US Region thereby it would also affect the value of the US dollar making the

US Dollar Depreciate where previously we could easily get $1.1 for 1 Euro however due to the

increase in the inflation rate by around 3% we could only get now $1.067 for 1Euro (Jiang,

Bahmani-Oskooee and Chang 2015). The change in the value of dollar is by around ($1.10-

$1.067): $0.033. In the given set of quotation observed for the EUR/USD Currency Exchange

rate it could be well observed that the Euro Currency is at a forward premium due to which the

higher rate of inflation expected. Thus, it is very important that the inflation rate in the US would

be much higher for contradicting the interest rate in the Euro Zone.

c) The changes in the exchange rate could be well implied with the help of the given macro-

economic factors such as the interest rate changes and change in the inflation rate of the

economy. The exchange rate plays a vital role in the country’s level of trade that is

crucial to most every free market economy in the world. This has been the key reason

which changes in the exchange rate has also been given a prior priority. The changes in

demand currency can be well described with help of given graph below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL FINANCE

Currency fluctuation are natural outcome of the ongoing floating exchange rate

system that otherwise impact the overall value of the currency rate. There are numerous

fundamental and technical factors that influences the overall exchange rate of an currency

when viewed from the other aspect of currency. The key impact of changing real-

exchange rate can be well explained with the help of given factors:

Merchandise Trade: The trade refers to the nation’s international trade activity that is

carried out. It can also be said out that the a weaker or depreciating currency will be

stimulating the overall export level and make the import more expensive for the

economy, thereby it could result in a large trade deficit over a period of time. On the othe

hand, a appreciating or a stronger currency can decrease the export competitiveness

thereby making the imports cheaper which can cause further deficit in the trade deficit

thereby ultimately making the currency weakening with currency appreciation.

Economic Growth: The economic growth for the economy GDP can be well evaluated

with the help of changes in various factors like the change in the net export activity, or

changes in capital investment which is also affected by the variability in the exchange

Currency fluctuation are natural outcome of the ongoing floating exchange rate

system that otherwise impact the overall value of the currency rate. There are numerous

fundamental and technical factors that influences the overall exchange rate of an currency

when viewed from the other aspect of currency. The key impact of changing real-

exchange rate can be well explained with the help of given factors:

Merchandise Trade: The trade refers to the nation’s international trade activity that is

carried out. It can also be said out that the a weaker or depreciating currency will be

stimulating the overall export level and make the import more expensive for the

economy, thereby it could result in a large trade deficit over a period of time. On the othe

hand, a appreciating or a stronger currency can decrease the export competitiveness

thereby making the imports cheaper which can cause further deficit in the trade deficit

thereby ultimately making the currency weakening with currency appreciation.

Economic Growth: The economic growth for the economy GDP can be well evaluated

with the help of changes in various factors like the change in the net export activity, or

changes in capital investment which is also affected by the variability in the exchange

8INTERNATIONAL FINANCE

rate. The key equation that shown below shows that the higher value in net exports could

result in a higher GDP value.

GDP=C+I+G+(X−M)

where:C=Consumption or consumer spending, the biggest component of economy

I=Capital investment by businesses and households

G=Government Expense

(X−M) = Exports−Imports, or net export activity carried out by the economy.

Capital Flows: Foreign capital generally flows to the countries where currency exchange

rate have strong and a stable government, that are alongside having a dynamic economies

and a alongside stable currencies. It is relatively very important that the currency of an

economy stays stable so that the foreign investors are attracted to the economies business

activity.

d) The expected interest rate in the US would be comparatively higher than in the Euro Rate

for contradicting the higher rate of inflation prevailing in the Euro Zone. In accordance

with the given theory of interest rate parity when seen from a real term basis the

prevailing interest rate should be equal across the globe. In the given set of quotation

observed for the EUR/USD Currency Exchange rate it could be well observed that the

Euro Currency is at a forward premium due to which the higher rate of inflation expected.

Thus, it is very important that the inflation rate in the US would be much higher for

contradicting the interest rate in the Euro Zone.

e) It is expected that the interest rate would be remaining the same in the Euro Zone

however at the same time it is crucial to note that the changes in the factors like the

changes in the inflation rate, liquidity risk and credit risk are some of the key concepts

rate. The key equation that shown below shows that the higher value in net exports could

result in a higher GDP value.

GDP=C+I+G+(X−M)

where:C=Consumption or consumer spending, the biggest component of economy

I=Capital investment by businesses and households

G=Government Expense

(X−M) = Exports−Imports, or net export activity carried out by the economy.

Capital Flows: Foreign capital generally flows to the countries where currency exchange

rate have strong and a stable government, that are alongside having a dynamic economies

and a alongside stable currencies. It is relatively very important that the currency of an

economy stays stable so that the foreign investors are attracted to the economies business

activity.

d) The expected interest rate in the US would be comparatively higher than in the Euro Rate

for contradicting the higher rate of inflation prevailing in the Euro Zone. In accordance

with the given theory of interest rate parity when seen from a real term basis the

prevailing interest rate should be equal across the globe. In the given set of quotation

observed for the EUR/USD Currency Exchange rate it could be well observed that the

Euro Currency is at a forward premium due to which the higher rate of inflation expected.

Thus, it is very important that the inflation rate in the US would be much higher for

contradicting the interest rate in the Euro Zone.

e) It is expected that the interest rate would be remaining the same in the Euro Zone

however at the same time it is crucial to note that the changes in the factors like the

changes in the inflation rate, liquidity risk and credit risk are some of the key concepts

9INTERNATIONAL FINANCE

that would be affecting the various bond prices. Although the prevailing exchange rate in

the economy would not be affecting the overall value of the government bonds but in

practice the same may get materially affected due to the factors mentioned above.

Changes in the above mentioned prices affect the variability in the bond prices due to

changing risk factors and the associated return factors that would be demanded by the

investors. The key component of required rate of return can be well divided into several

key factors as shown below:

Required Rate of Return: Real Risk Free Rate of Return + Inflation Rate+ Market

Risk Premium.

In Accordance with the various factors stated above the real risk free rate in

accordance with the theory of Interest Rate Parity may remain the same however the

other key factors that helps in determining the value of bonds may materially affect the

overall price or value of the bonds (McKinnon and Ohno 2016).

Question 3

Country Risk relates to the overall risk associated with the investment made by a foreign

investors when investing into a foreign country. The risk premium demanded by the investors is

generally due to the fact that the investor will be exposed to various macro-economic, political

and business factors of the economy that would be affecting the prevailing exchange rate and the

overall investment return that is associated with the investor (Kim, Park and Kim 2017). If the

exchange rate volatility increases in an economy where the investor or institution has invested it

would ultimately be affecting the overall performance of the economy. Country risk analysis can

be better done with the help of the Political risk associated in an economy (Della Corte,

that would be affecting the various bond prices. Although the prevailing exchange rate in

the economy would not be affecting the overall value of the government bonds but in

practice the same may get materially affected due to the factors mentioned above.

Changes in the above mentioned prices affect the variability in the bond prices due to

changing risk factors and the associated return factors that would be demanded by the

investors. The key component of required rate of return can be well divided into several

key factors as shown below:

Required Rate of Return: Real Risk Free Rate of Return + Inflation Rate+ Market

Risk Premium.

In Accordance with the various factors stated above the real risk free rate in

accordance with the theory of Interest Rate Parity may remain the same however the

other key factors that helps in determining the value of bonds may materially affect the

overall price or value of the bonds (McKinnon and Ohno 2016).

Question 3

Country Risk relates to the overall risk associated with the investment made by a foreign

investors when investing into a foreign country. The risk premium demanded by the investors is

generally due to the fact that the investor will be exposed to various macro-economic, political

and business factors of the economy that would be affecting the prevailing exchange rate and the

overall investment return that is associated with the investor (Kim, Park and Kim 2017). If the

exchange rate volatility increases in an economy where the investor or institution has invested it

would ultimately be affecting the overall performance of the economy. Country risk analysis can

be better done with the help of the Political risk associated in an economy (Della Corte,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10INTERNATIONAL FINANCE

Ramadorai and Sarno 2016). Changes in the government policies and actions and rules and

regulation can affect the operations of the business organisations and entities on an individual

basis. On the other hand changes in the macro-economic risks like the prevailing rate of

inflation, interest rate and business cycle under which the economy is currently undergoing are

also some of the important factors affecting the overall country risk involved in this scenario.

There are times when it is quite often observed that the country’s economy may be strong, but if

the political climate is unfriendly to foreign investors, the country may not be an attractive point

for the purpose of investment (Asteriou, Masatci and Pılbeam 2016). The analyzed Political risks

would include regulations imposed, restrictions on foreign investment and government

expropriation. In most countries political risk has been reduced by acceptance of new markets

and change of perception into beliefs that investment and trade across nations are one of the

ways for economic growth (Beckmann and Stix 2015). From the point of view of an investor, it

is imperative to conduct country risk analysis so that any factor which can affect the new project

or undertaking needs to be considered in decision making process of the business (Chkili and

Nguyen 2014). The exchange rate of a country is affected by different factors and the degree to

which such exchange rates varies is known as the volatility of the exchange rate. The exchange

rate is often affected by the debt which is taken by the country from other nations and even

political turmoil in the country can impact the exchange rate. Investors and MNCs needs to

consider such aspects before making any investments in the country as the same can impact the

profitability and even in extreme circumstances incur significant losses to the business or the

investor. There are different tools available with the help of which analysis can be conducted in

regarding the country risks and exchange rate volatility. These tools are both qualitative and

quantitative in nature. Therefore, it can be said that there are lot of challenges in terms of

Ramadorai and Sarno 2016). Changes in the government policies and actions and rules and

regulation can affect the operations of the business organisations and entities on an individual

basis. On the other hand changes in the macro-economic risks like the prevailing rate of

inflation, interest rate and business cycle under which the economy is currently undergoing are

also some of the important factors affecting the overall country risk involved in this scenario.

There are times when it is quite often observed that the country’s economy may be strong, but if

the political climate is unfriendly to foreign investors, the country may not be an attractive point

for the purpose of investment (Asteriou, Masatci and Pılbeam 2016). The analyzed Political risks

would include regulations imposed, restrictions on foreign investment and government

expropriation. In most countries political risk has been reduced by acceptance of new markets

and change of perception into beliefs that investment and trade across nations are one of the

ways for economic growth (Beckmann and Stix 2015). From the point of view of an investor, it

is imperative to conduct country risk analysis so that any factor which can affect the new project

or undertaking needs to be considered in decision making process of the business (Chkili and

Nguyen 2014). The exchange rate of a country is affected by different factors and the degree to

which such exchange rates varies is known as the volatility of the exchange rate. The exchange

rate is often affected by the debt which is taken by the country from other nations and even

political turmoil in the country can impact the exchange rate. Investors and MNCs needs to

consider such aspects before making any investments in the country as the same can impact the

profitability and even in extreme circumstances incur significant losses to the business or the

investor. There are different tools available with the help of which analysis can be conducted in

regarding the country risks and exchange rate volatility. These tools are both qualitative and

quantitative in nature. Therefore, it can be said that there are lot of challenges in terms of

11INTERNATIONAL FINANCE

exchange rate volatility and country risks which the MNCs and foreign investors needs to be

aware of before making any investments in the country.

It is accordingly important for the investors and institutional investors to consider various

risks and factors that are associated with the investment so that the implication of the country

risk that is faced by investors can be better assessed and can be better hedged with the help of

financial derivatives or financial instruments. There are various and wide range of financial

instruments like options, swaps, futures and forward contracts that allow the foreign investors

and institutions to mitigate or reduce the associated risk with international or foreign

investments.

Question 5

Multinational Companies play an important role in an economy as they are considered to

be the catalysts to bring about globalization in an economy. Globalization has facilitated the

growth of Multinational companies and has increased trade, communication and workforce

mobility in a business environment. Most of the Multinational Companies are significantly

achieving growth and has also led to better revenue generation and employment generation in a

business (Williamson 2002). As per viewpoints of different researchers, there is often a mixed

reaction relating to whether the growth of Multinational Companies have a positive or negative

impact on the economies in which the companies are operating. However, it can be clearly seen

that the positive impact of the growth out weights the negative impacts and the reasons for

considering the same are discussed in details in paragraph below.

Multinational Companies are known to create wealth and more job opportunities around

the globe. It is a fact that Multinational companies help in meeting the employment requirement

exchange rate volatility and country risks which the MNCs and foreign investors needs to be

aware of before making any investments in the country.

It is accordingly important for the investors and institutional investors to consider various

risks and factors that are associated with the investment so that the implication of the country

risk that is faced by investors can be better assessed and can be better hedged with the help of

financial derivatives or financial instruments. There are various and wide range of financial

instruments like options, swaps, futures and forward contracts that allow the foreign investors

and institutions to mitigate or reduce the associated risk with international or foreign

investments.

Question 5

Multinational Companies play an important role in an economy as they are considered to

be the catalysts to bring about globalization in an economy. Globalization has facilitated the

growth of Multinational companies and has increased trade, communication and workforce

mobility in a business environment. Most of the Multinational Companies are significantly

achieving growth and has also led to better revenue generation and employment generation in a

business (Williamson 2002). As per viewpoints of different researchers, there is often a mixed

reaction relating to whether the growth of Multinational Companies have a positive or negative

impact on the economies in which the companies are operating. However, it can be clearly seen

that the positive impact of the growth out weights the negative impacts and the reasons for

considering the same are discussed in details in paragraph below.

Multinational Companies are known to create wealth and more job opportunities around

the globe. It is a fact that Multinational companies help in meeting the employment requirement

12INTERNATIONAL FINANCE

of a business and thereby contributes to an economy in the most effective manner. Investments

which are made in a multinational corporation creates foreign currency which is very useful for

maintain trade relations with other nations (Pettinger 2017). Another positive impact of

Multinational Companies is the prices at which they offer quality products which is quite lower

than normal businesses. The reason for such lower cost is the economies of scale factor which is

enjoyed by Multinational Companies (Holmes et al. 2016). This enables the business to lower the

average costs and thereby also the prices of the commodities are reduced. This situation is much

more applicable on industries which have high fixed costs such as airlines industry. Another

positive impact of such Multinational Companies is that they tend to make large profits and a

major portion of the profits are used for commencing research and development activities so that

there is further expansion of the business (Meyer 2014). This allows the business to reach out to

more customers and provide quality products which is their major tool against competition.

Furthermore, it is often seen that people or consumers tend to go for those products which are

properly branded and have a set standard for quality. These sorts of products are offered by the

Multinational companies and thereby are also popular among the consumers of the business.

Examples can be given of brands like Coca-Cola and Apple which are known for their quality

and brand nature. Another major advantage of growth of Multinational Companies in the

economy is that there would be significant flow of Foreign direct investments which would help

in the economic growth of the country (Temiz and Gökmen 2014). It would also help in

enhancing the foreign exchange reserve which the country has and also make the foreign trade

process much simpler in nature.

The above discussion clearly shows that growth of Multinational Companies helps in

development of the economy as a whole and also creates job opportunities in the country. It is for

of a business and thereby contributes to an economy in the most effective manner. Investments

which are made in a multinational corporation creates foreign currency which is very useful for

maintain trade relations with other nations (Pettinger 2017). Another positive impact of

Multinational Companies is the prices at which they offer quality products which is quite lower

than normal businesses. The reason for such lower cost is the economies of scale factor which is

enjoyed by Multinational Companies (Holmes et al. 2016). This enables the business to lower the

average costs and thereby also the prices of the commodities are reduced. This situation is much

more applicable on industries which have high fixed costs such as airlines industry. Another

positive impact of such Multinational Companies is that they tend to make large profits and a

major portion of the profits are used for commencing research and development activities so that

there is further expansion of the business (Meyer 2014). This allows the business to reach out to

more customers and provide quality products which is their major tool against competition.

Furthermore, it is often seen that people or consumers tend to go for those products which are

properly branded and have a set standard for quality. These sorts of products are offered by the

Multinational companies and thereby are also popular among the consumers of the business.

Examples can be given of brands like Coca-Cola and Apple which are known for their quality

and brand nature. Another major advantage of growth of Multinational Companies in the

economy is that there would be significant flow of Foreign direct investments which would help

in the economic growth of the country (Temiz and Gökmen 2014). It would also help in

enhancing the foreign exchange reserve which the country has and also make the foreign trade

process much simpler in nature.

The above discussion clearly shows that growth of Multinational Companies helps in

development of the economy as a whole and also creates job opportunities in the country. It is for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13INTERNATIONAL FINANCE

such reasons that, growth of a Multinational Companies can be considered to be good for the

economy.

such reasons that, growth of a Multinational Companies can be considered to be good for the

economy.

14INTERNATIONAL FINANCE

References

Arize, A.C., Malindretos, J. and Igwe, E.U., 2017. Do exchange rate changes improve the trade

balance: An asymmetric nonlinear cointegration approach. International Review of Economics &

Finance, 49, pp.313-326.

Asteriou, D., Masatci, K. and Pılbeam, K., 2016. Exchange rate volatility and international trade:

International evidence from the MINT countries. Economic Modelling, 58, pp.133-140.

Auer, R.A. and Schoenle, R.S., 2016. Market structure and exchange rate pass-through. Journal

of International Economics, 98, pp.60-77.

Bahmani-Oskooee, M. and Kanitpong, T., 2017. Do exchange rate changes have symmetric or

asymmetric effects on the trade balances of Asian countries?. Applied Economics, 49(46),

pp.4668-4678.

Bahmani-Oskooee, M. and Saha, S., 2016. Do exchange rate changes have symmetric or

asymmetric effects on stock prices?. Global Finance Journal, 31, pp.57-72.

Bahmani-Oskooee, M., Chang, T., Chen, T.H. and Tzeng, H.W., 2017. Revisiting purchasing

power parity in Eastern European countries: quantile unit root tests. Empirical Economics, 52(2),

pp.463-483.

Beckmann, E. and Stix, H., 2015. Foreign currency borrowing and knowledge about exchange

rate risk. Journal of Economic Behavior & Organization, 112, pp.1-16.

Caselli, F.G. and Roitman, A., 2016. Nonlinear exchange‐rate pass‐through in emerging

markets. International Finance.

References

Arize, A.C., Malindretos, J. and Igwe, E.U., 2017. Do exchange rate changes improve the trade

balance: An asymmetric nonlinear cointegration approach. International Review of Economics &

Finance, 49, pp.313-326.

Asteriou, D., Masatci, K. and Pılbeam, K., 2016. Exchange rate volatility and international trade:

International evidence from the MINT countries. Economic Modelling, 58, pp.133-140.

Auer, R.A. and Schoenle, R.S., 2016. Market structure and exchange rate pass-through. Journal

of International Economics, 98, pp.60-77.

Bahmani-Oskooee, M. and Kanitpong, T., 2017. Do exchange rate changes have symmetric or

asymmetric effects on the trade balances of Asian countries?. Applied Economics, 49(46),

pp.4668-4678.

Bahmani-Oskooee, M. and Saha, S., 2016. Do exchange rate changes have symmetric or

asymmetric effects on stock prices?. Global Finance Journal, 31, pp.57-72.

Bahmani-Oskooee, M., Chang, T., Chen, T.H. and Tzeng, H.W., 2017. Revisiting purchasing

power parity in Eastern European countries: quantile unit root tests. Empirical Economics, 52(2),

pp.463-483.

Beckmann, E. and Stix, H., 2015. Foreign currency borrowing and knowledge about exchange

rate risk. Journal of Economic Behavior & Organization, 112, pp.1-16.

Caselli, F.G. and Roitman, A., 2016. Nonlinear exchange‐rate pass‐through in emerging

markets. International Finance.

15INTERNATIONAL FINANCE

Chkili, W. and Nguyen, D.K., 2014. Exchange rate movements and stock market returns in a

regime-switching environment: Evidence for BRICS countries. Research in International

Business and Finance, 31, pp.46-56.

Della Corte, P., Ramadorai, T. and Sarno, L., 2016. Volatility risk premia and exchange rate

predictability. Journal of Financial Economics, 120(1), pp.21-40.

Demir, F., 2013. Growth under exchange rate volatility: Does access to foreign or domestic

equity markets matter?. Journal of Development Economics, 100(1), pp.74-88.

Engel, C., 2016. Exchange rates, interest rates, and the risk premium. American Economic

Review, 106(2), pp.436-74.

Holmes Jr, R.M., Li, H., Hitt, M.A., DeGhetto, K. and Sutton, T., 2016. The Effects of Location

and MNC Attributes on MNCs' Establishment of Foreign R&D Centers: Evidence from

China. Long Range Planning, 49(5), pp.594-613.

Huang, C.H. and Yang, C.Y., 2015. European exchange rate regimes and purchasing power

parity: An empirical study on eleven eurozone countries. International Review of Economics &

Finance, 35, pp.100-109.

Jiang, C., Bahmani-Oskooee, M. and Chang, T., 2015. Revisiting purchasing power parity in

OECD. Applied Economics, 47(40), pp.4323-4334.

Jolliffe, D. and Prydz, E.B., 2015. Global poverty goals and prices: how purchasing power parity

matters. The World Bank.

Chkili, W. and Nguyen, D.K., 2014. Exchange rate movements and stock market returns in a

regime-switching environment: Evidence for BRICS countries. Research in International

Business and Finance, 31, pp.46-56.

Della Corte, P., Ramadorai, T. and Sarno, L., 2016. Volatility risk premia and exchange rate

predictability. Journal of Financial Economics, 120(1), pp.21-40.

Demir, F., 2013. Growth under exchange rate volatility: Does access to foreign or domestic

equity markets matter?. Journal of Development Economics, 100(1), pp.74-88.

Engel, C., 2016. Exchange rates, interest rates, and the risk premium. American Economic

Review, 106(2), pp.436-74.

Holmes Jr, R.M., Li, H., Hitt, M.A., DeGhetto, K. and Sutton, T., 2016. The Effects of Location

and MNC Attributes on MNCs' Establishment of Foreign R&D Centers: Evidence from

China. Long Range Planning, 49(5), pp.594-613.

Huang, C.H. and Yang, C.Y., 2015. European exchange rate regimes and purchasing power

parity: An empirical study on eleven eurozone countries. International Review of Economics &

Finance, 35, pp.100-109.

Jiang, C., Bahmani-Oskooee, M. and Chang, T., 2015. Revisiting purchasing power parity in

OECD. Applied Economics, 47(40), pp.4323-4334.

Jolliffe, D. and Prydz, E.B., 2015. Global poverty goals and prices: how purchasing power parity

matters. The World Bank.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16INTERNATIONAL FINANCE

Kakwani, N. and Son, H.H., 2016. Global poverty estimates based on 2011 purchasing power

parity: where should the new poverty line be drawn?. The Journal of Economic Inequality, 14(2),

pp.173-184.

Kim, K., Park, H. and Kim, H., 2017. Real options analysis for renewable energy investment

decisions in developing countries. Renewable and Sustainable Energy Reviews, 75, pp.918-926.

McKinnon, R.I. and Ohno, K., 2016. 7 Purchasing power parity as a monetary. The Future of the

International Monetary System: Change, Coordination of Instability?: Change, Coordination of

Instability?, p.42.

Meyer, K.E., 2014. Process perspectives on the growth of emerging economy

multinationals. Understanding multinationals from emerging markets, pp.169-194.

Pettinger, T. (2017). Multinational Corporations: Good or Bad? | Economics Help. [online]

Economicshelp.org. Available at:

https://www.economicshelp.org/blog/538/economics/multinational-corporations-good-or-bad/

[Accessed 28 Aug. 2019].

Romelli, D., Terra, C. and Vasconcelos, E., 2018. Current account and real exchange rate

changes: The impact of trade openness. European Economic Review, 105, pp.135-158.

Temiz, D. and Gökmen, A., 2014. FDI inflow as an international business operation by MNCs

and economic growth: An empirical study on Turkey. International Business Review, 23(1),

pp.145-154.

Kakwani, N. and Son, H.H., 2016. Global poverty estimates based on 2011 purchasing power

parity: where should the new poverty line be drawn?. The Journal of Economic Inequality, 14(2),

pp.173-184.

Kim, K., Park, H. and Kim, H., 2017. Real options analysis for renewable energy investment

decisions in developing countries. Renewable and Sustainable Energy Reviews, 75, pp.918-926.

McKinnon, R.I. and Ohno, K., 2016. 7 Purchasing power parity as a monetary. The Future of the

International Monetary System: Change, Coordination of Instability?: Change, Coordination of

Instability?, p.42.

Meyer, K.E., 2014. Process perspectives on the growth of emerging economy

multinationals. Understanding multinationals from emerging markets, pp.169-194.

Pettinger, T. (2017). Multinational Corporations: Good or Bad? | Economics Help. [online]

Economicshelp.org. Available at:

https://www.economicshelp.org/blog/538/economics/multinational-corporations-good-or-bad/

[Accessed 28 Aug. 2019].

Romelli, D., Terra, C. and Vasconcelos, E., 2018. Current account and real exchange rate

changes: The impact of trade openness. European Economic Review, 105, pp.135-158.

Temiz, D. and Gökmen, A., 2014. FDI inflow as an international business operation by MNCs

and economic growth: An empirical study on Turkey. International Business Review, 23(1),

pp.145-154.

17INTERNATIONAL FINANCE

Williamson, L. (2002). Globalisation: good or bad?. [online] the Guardian. Available at:

https://www.theguardian.com/world/2002/oct/31/globalisation.lewiswilliamson [Accessed 28

Aug. 2019].

Williamson, L. (2002). Globalisation: good or bad?. [online] the Guardian. Available at:

https://www.theguardian.com/world/2002/oct/31/globalisation.lewiswilliamson [Accessed 28

Aug. 2019].

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.