Besto Company Case Study: Financial Analysis of Costing Systems

VerifiedAdded on 2022/11/25

|6

|1868

|199

Case Study

AI Summary

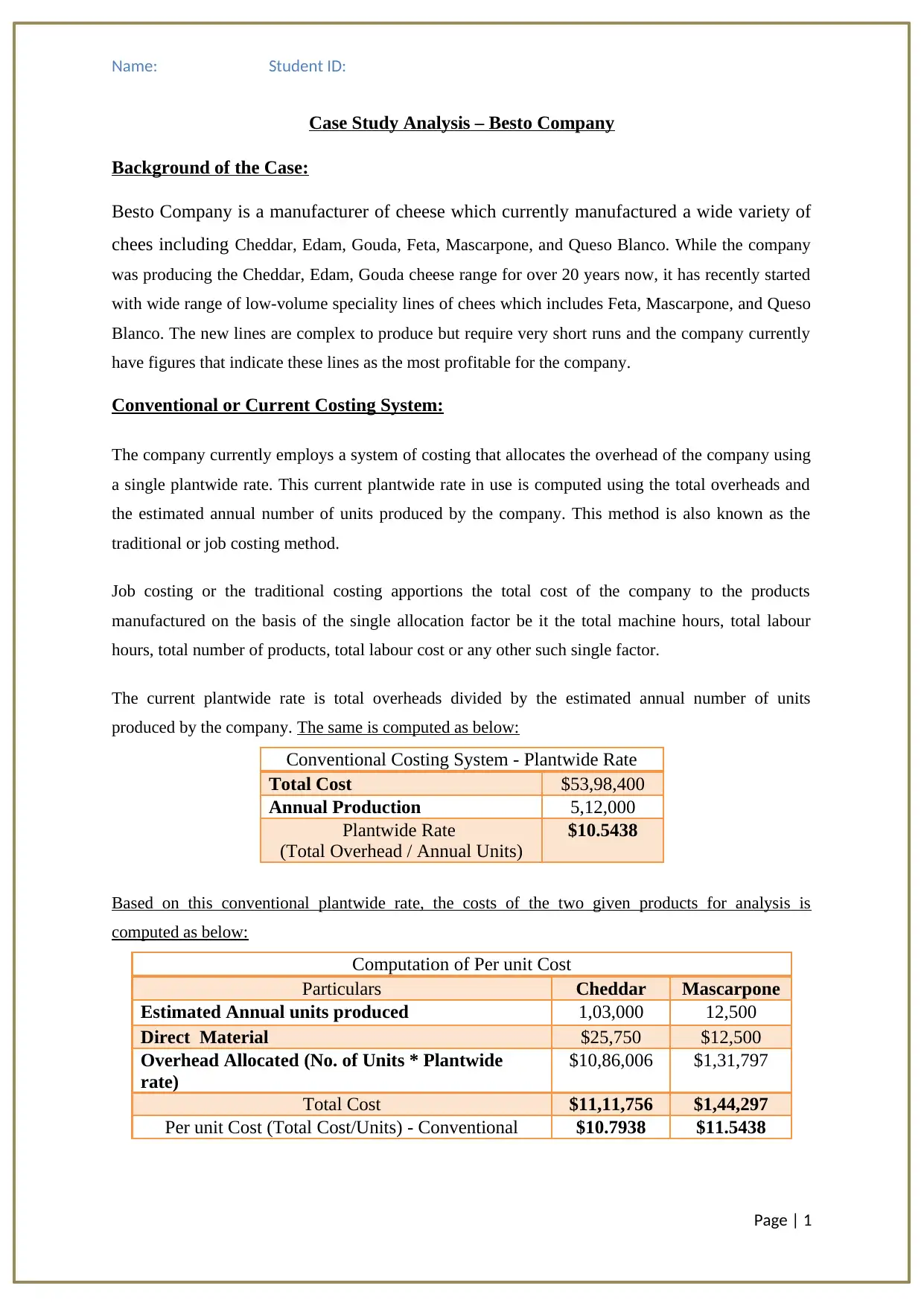

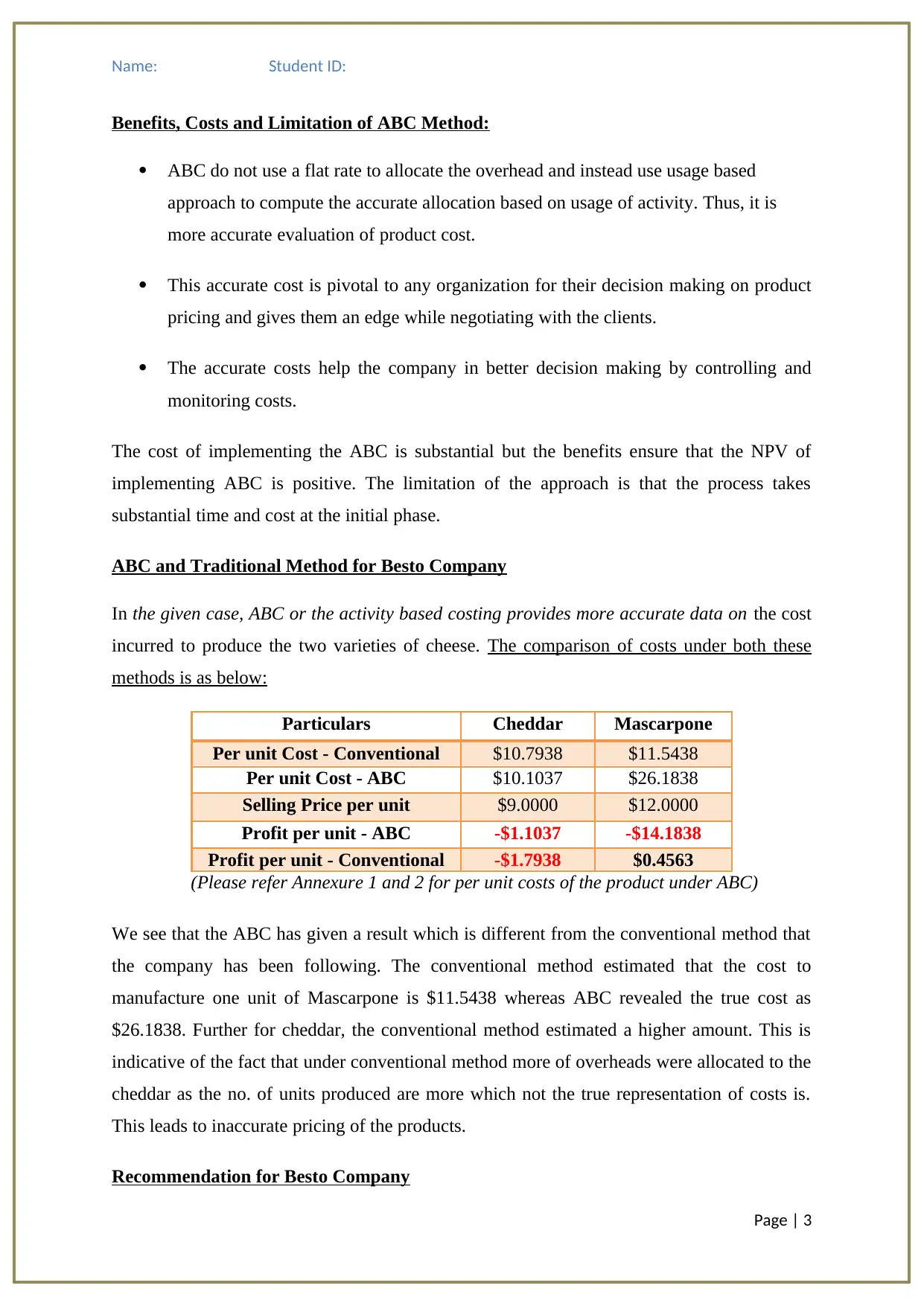

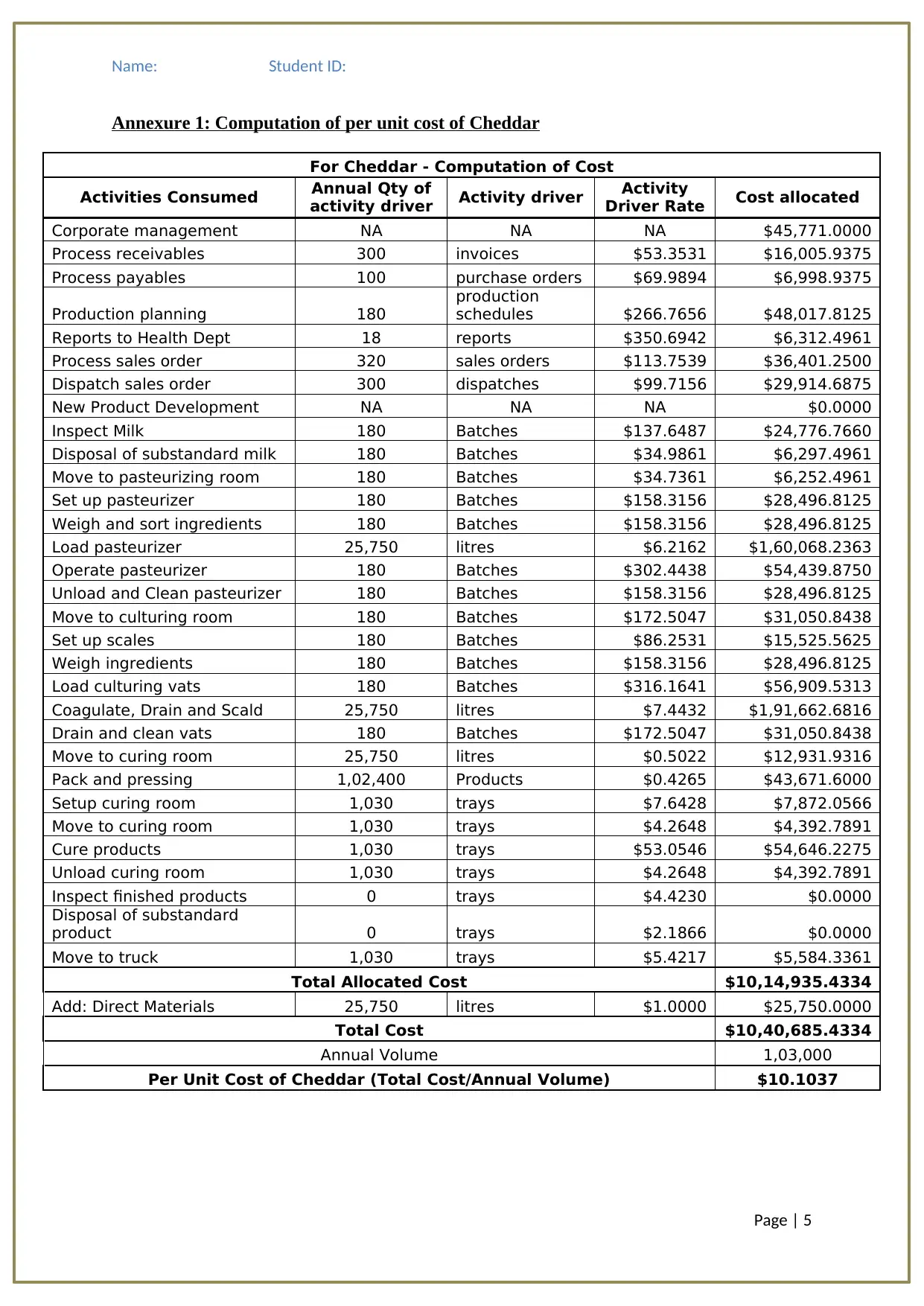

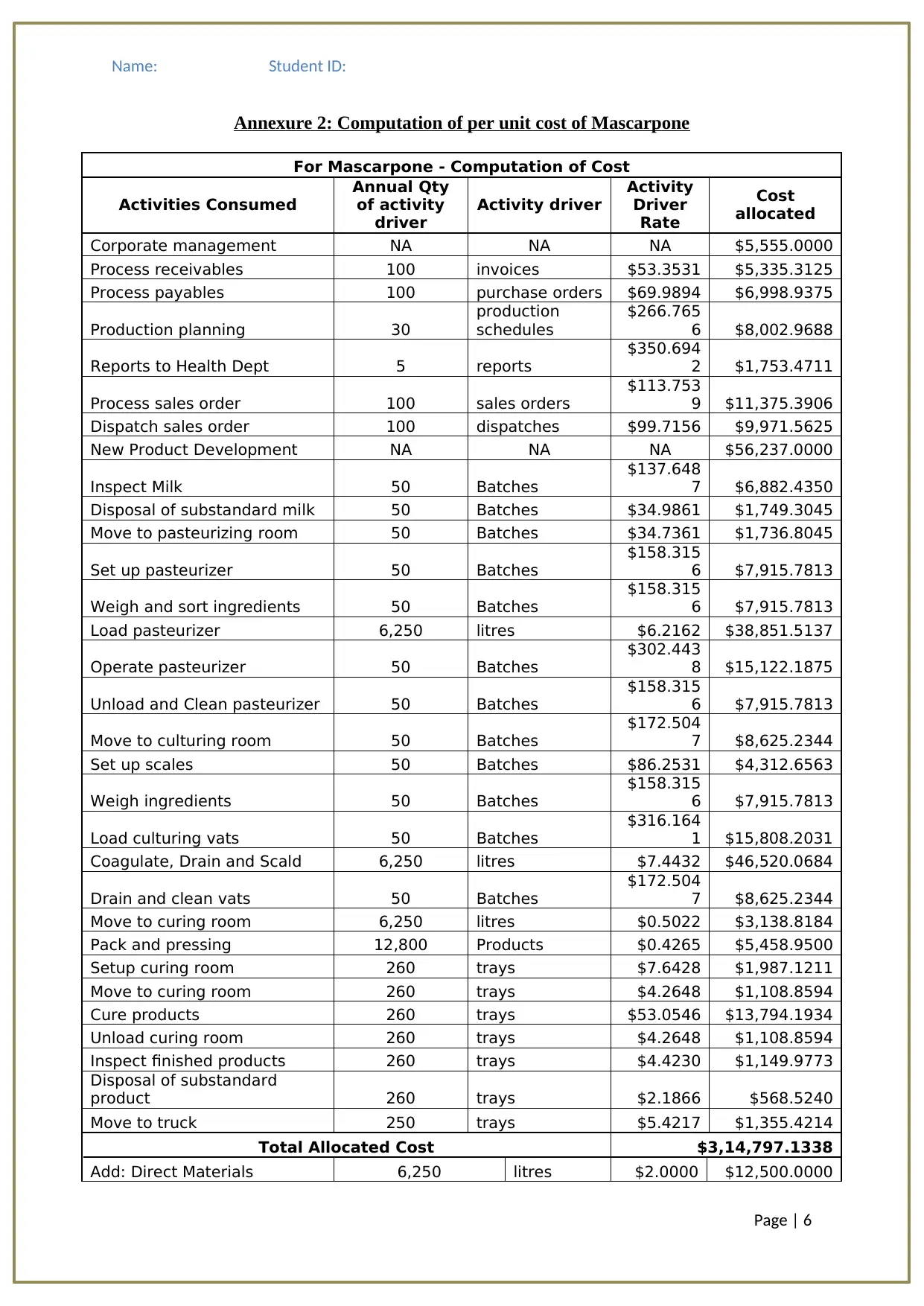

This case study analyzes Besto Company, a cheese manufacturer, and its costing methods. The company currently uses a traditional plantwide costing system, which allocates overhead based on the number of units produced. The analysis compares this to activity-based costing (ABC), a more modern approach that allocates costs based on the activities consuming resources. The study reveals that the traditional method misrepresents the true costs of different cheese varieties, leading to inaccurate pricing and declining profits. Using ABC, the study calculates per-unit costs for Cheddar and Mascarpone, highlighting the significant differences between the two costing methods. The analysis concludes with a recommendation for Besto Company to adopt ABC for more accurate, realistic, and reliable cost information, which is crucial for informed decision-making regarding pricing, cost control, and overall profitability. The annexures provide detailed calculations of per-unit costs under both costing methods, supporting the analysis and recommendations.

1 out of 6

Related Documents

![Management Accounting: Costing Analysis of Office Desks - [Company]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fjv%2Fc197923795a34b81bdce50f667d18d4c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.