Healthcare Finance Project: All-Care Health Agency Financial Analysis

VerifiedAdded on 2019/09/20

|8

|1100

|137

Report

AI Summary

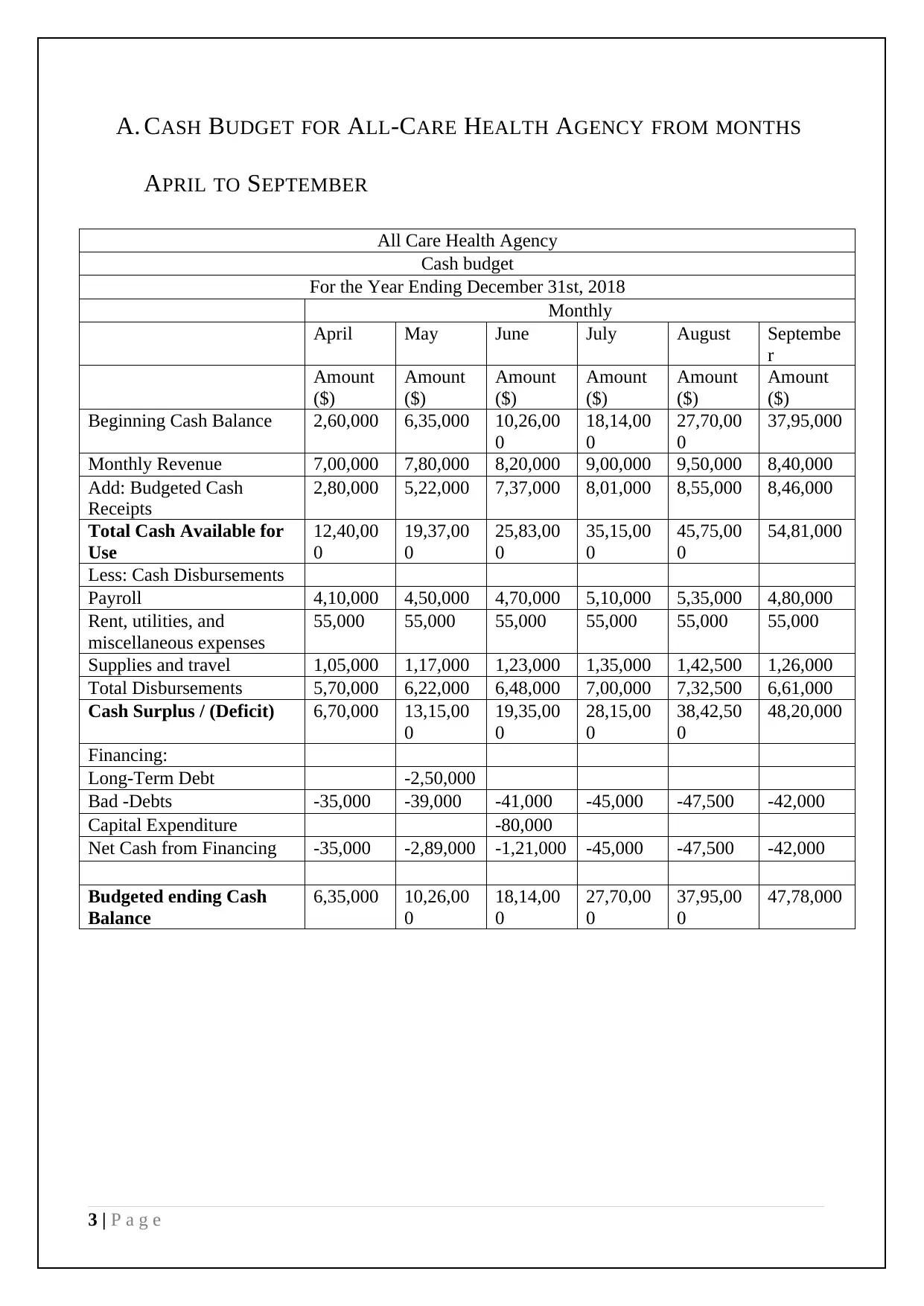

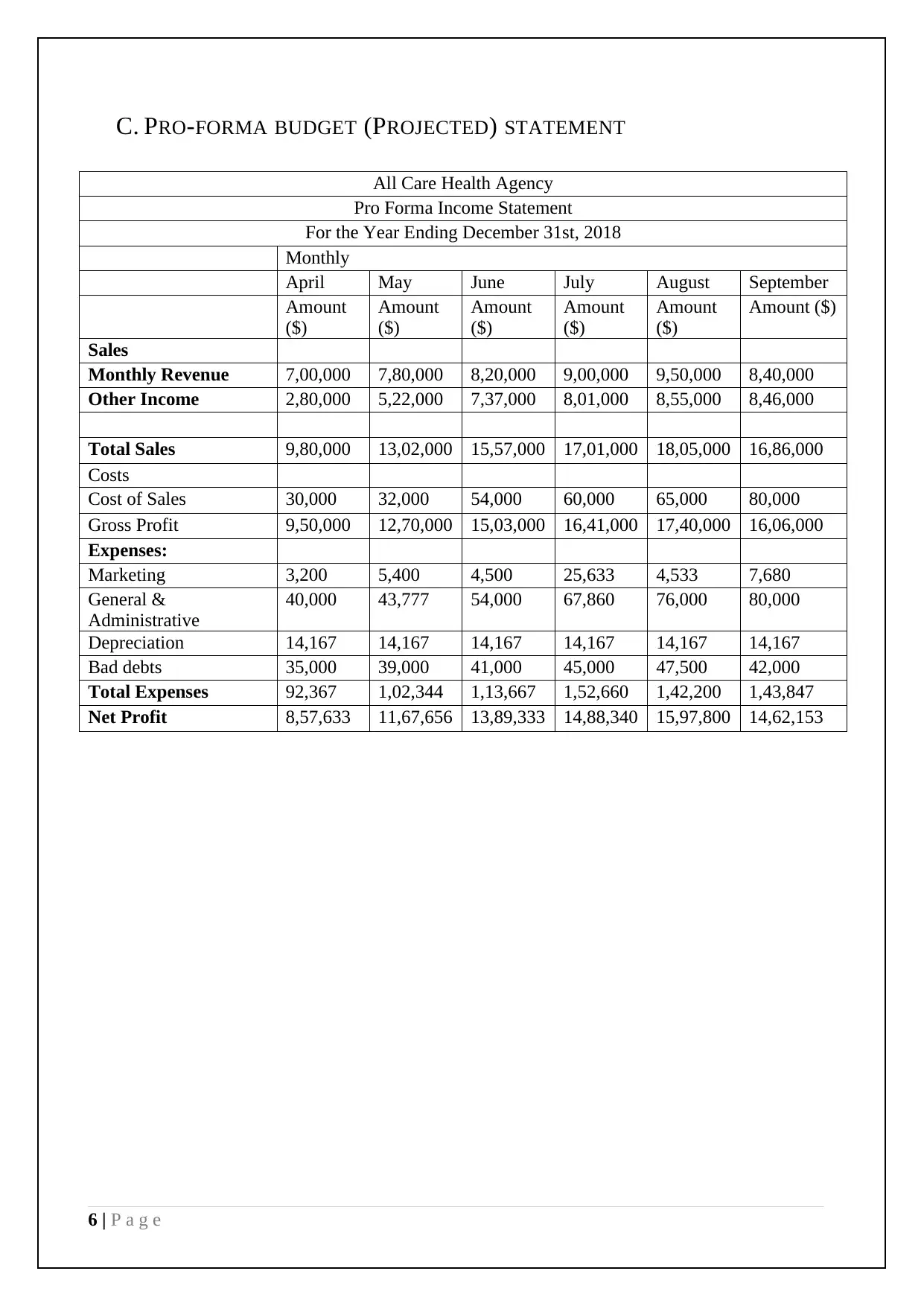

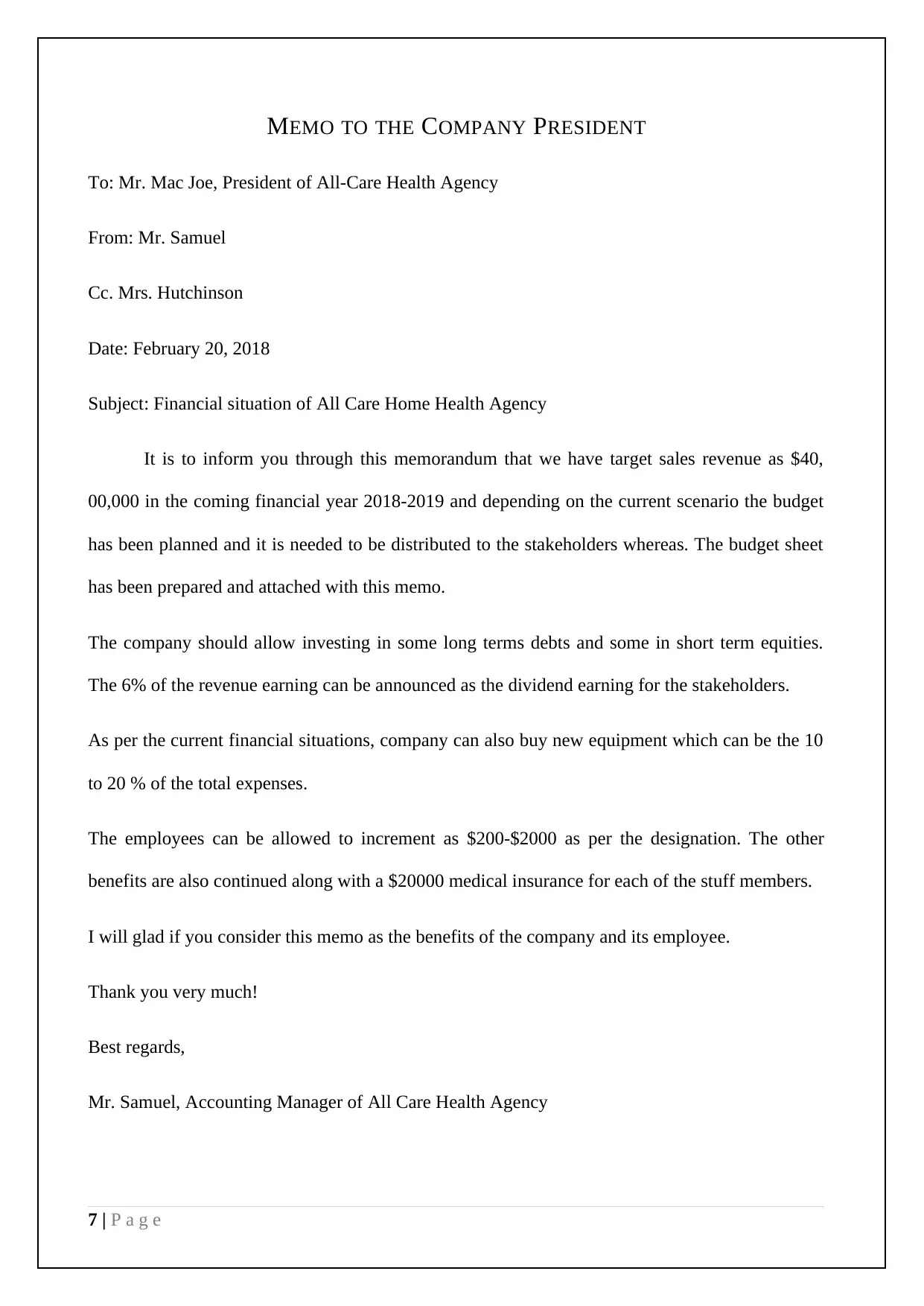

This report presents a comprehensive financial analysis of the All-Care Health Agency, focusing on its cash budget and pro-forma income statement for the year ending December 31st, 2018. The assignment includes a detailed cash budget from April to September, outlining beginning cash balances, monthly revenue, cash receipts, disbursements, and financing activities, culminating in an ending cash balance. The report provides a rationale for the budget, emphasizing the importance of planning, budgeting, and financing capital projects. It highlights factors such as high stakes, long-term implications, and the cyclical nature of spending. Furthermore, a pro-forma income statement projects sales, other income, costs, expenses, and net profit. A memo to the company president summarizes key financial recommendations, including revenue targets, investment strategies, dividend announcements, capital expenditure plans, and employee benefits. The report concludes with a works cited section, referencing relevant sources on capital budgeting and finance.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.