Nestle Company Financial Analysis Report: AC4410 Assignment 2

VerifiedAdded on 2023/06/03

|10

|1966

|482

Report

AI Summary

This report provides a comprehensive financial analysis of Nestle SA from 2013 to 2016, focusing on key financial ratios. The analysis begins with a company overview, highlighting Nestle's position as a global leader in the food and beverage industry, its diverse product portfolio, and its global presence...

Assignment 2 Nestle group

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AC4410 Accounting and Finance

Contents

Company overview....................................................................................................................3

Ratio and analysis......................................................................................................................4

Nestle financial statement analysis from year 2013 to 2016.....................................................5

Profitability Ratios....................................................................................................................5

Liquidity Ratios.........................................................................................................................6

Activity Ratios...........................................................................................................................7

Conclusion.................................................................................................................................9

Bibliography............................................................................................................................10

Appendix.................................................................................................................................11

2

Contents

Company overview....................................................................................................................3

Ratio and analysis......................................................................................................................4

Nestle financial statement analysis from year 2013 to 2016.....................................................5

Profitability Ratios....................................................................................................................5

Liquidity Ratios.........................................................................................................................6

Activity Ratios...........................................................................................................................7

Conclusion.................................................................................................................................9

Bibliography............................................................................................................................10

Appendix.................................................................................................................................11

2

AC4410 Accounting and Finance

Company overview

Nestlé SA is a Swiss multinational food and beverage company based in Vevey

Switzerland. It is currently considered as the largest food company in the world according to

the revenue realised within the financial years 2014-2016. It has obtained 72nd rank in

Fortune Global 500 in 2014 and also got 33rd place in the 2016 edition of Forbes Global

2000. This list was developed for recognition of the largest public companies in the world (J.

Chris Leach, 2016).

Nestlé's products include baby food, medical food, bottled water, breakfast cereals,

coffee and tea, confectionery, dairy products, ice cream, frozen foods, pet food and snacks.

Twenty-nine of Nestlé's brands have annual sales of over 1 billion Swiss francs (about $ 1.1

billion). The list of most popular Nestle brands includes Maggi, Nescafe, Kit Kat,

Smarties,Nesquik, Stouffer's, Vittel and Nespresso. Nestlé is currently operating in 194

countries with 447 factories.It is currently employing about 339,000 people. It is also one of

the major shareholders of L'Oréal, the largest cosmetics company in the world.

3

Company overview

Nestlé SA is a Swiss multinational food and beverage company based in Vevey

Switzerland. It is currently considered as the largest food company in the world according to

the revenue realised within the financial years 2014-2016. It has obtained 72nd rank in

Fortune Global 500 in 2014 and also got 33rd place in the 2016 edition of Forbes Global

2000. This list was developed for recognition of the largest public companies in the world (J.

Chris Leach, 2016).

Nestlé's products include baby food, medical food, bottled water, breakfast cereals,

coffee and tea, confectionery, dairy products, ice cream, frozen foods, pet food and snacks.

Twenty-nine of Nestlé's brands have annual sales of over 1 billion Swiss francs (about $ 1.1

billion). The list of most popular Nestle brands includes Maggi, Nescafe, Kit Kat,

Smarties,Nesquik, Stouffer's, Vittel and Nespresso. Nestlé is currently operating in 194

countries with 447 factories.It is currently employing about 339,000 people. It is also one of

the major shareholders of L'Oréal, the largest cosmetics company in the world.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AC4410 Accounting and Finance

Ratio and analysis

The main aim of ratio and analysis

In accounting, a ratio is a coefficient or a percentage usually calculated through two

functional masses of the balance sheet or the income statement. The ratios are used to

measure profitability, the structure of costs, productivity, solvency, liquidity and the

financial stability.(Timothy R. Mayes, 2016).

Benefits of ratio analysis

There are more than a hundred ratios used by companies all over the world. These

ratios are very beneficial as they make it possible to evaluate the financial situation of a

company. It aids management in evaluating the financial progress from one year to another.

Moreover, it also aids in comparing with other companies in the same sector (Stephen A.

Ross, 2016).Methods such as DuPont analysis can formalize these estimates. Ratios can also

be integrated into different discriminate analysis approaches.These approaches are mostly

combined to calculate a single indicator called a score. These scores are very important for

assessing the risks and bankruptcy of an institution (Tracy, 2012).

Limitations of ratio analysis

Ratio analysis is mostly based on the historical facts and figures which is not so helpful

for predicting the future of any company. This is beacuse the current business

environment is very unpredictable and dynamic.

The financial information presented in the balance sheet may not be accurate as the value

of financial assets or liabilities will be lowered on account of inflation

It cannot be regarded as adequate method for comparing the financial results of a

company with that of another as the entities tend to adopt the use of different accounting

practices. Thus, the use of this technique will not prove to be highly effective in

comparing the financial results across different entities.

4

Ratio and analysis

The main aim of ratio and analysis

In accounting, a ratio is a coefficient or a percentage usually calculated through two

functional masses of the balance sheet or the income statement. The ratios are used to

measure profitability, the structure of costs, productivity, solvency, liquidity and the

financial stability.(Timothy R. Mayes, 2016).

Benefits of ratio analysis

There are more than a hundred ratios used by companies all over the world. These

ratios are very beneficial as they make it possible to evaluate the financial situation of a

company. It aids management in evaluating the financial progress from one year to another.

Moreover, it also aids in comparing with other companies in the same sector (Stephen A.

Ross, 2016).Methods such as DuPont analysis can formalize these estimates. Ratios can also

be integrated into different discriminate analysis approaches.These approaches are mostly

combined to calculate a single indicator called a score. These scores are very important for

assessing the risks and bankruptcy of an institution (Tracy, 2012).

Limitations of ratio analysis

Ratio analysis is mostly based on the historical facts and figures which is not so helpful

for predicting the future of any company. This is beacuse the current business

environment is very unpredictable and dynamic.

The financial information presented in the balance sheet may not be accurate as the value

of financial assets or liabilities will be lowered on account of inflation

It cannot be regarded as adequate method for comparing the financial results of a

company with that of another as the entities tend to adopt the use of different accounting

practices. Thus, the use of this technique will not prove to be highly effective in

comparing the financial results across different entities.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AC4410 Accounting and Finance

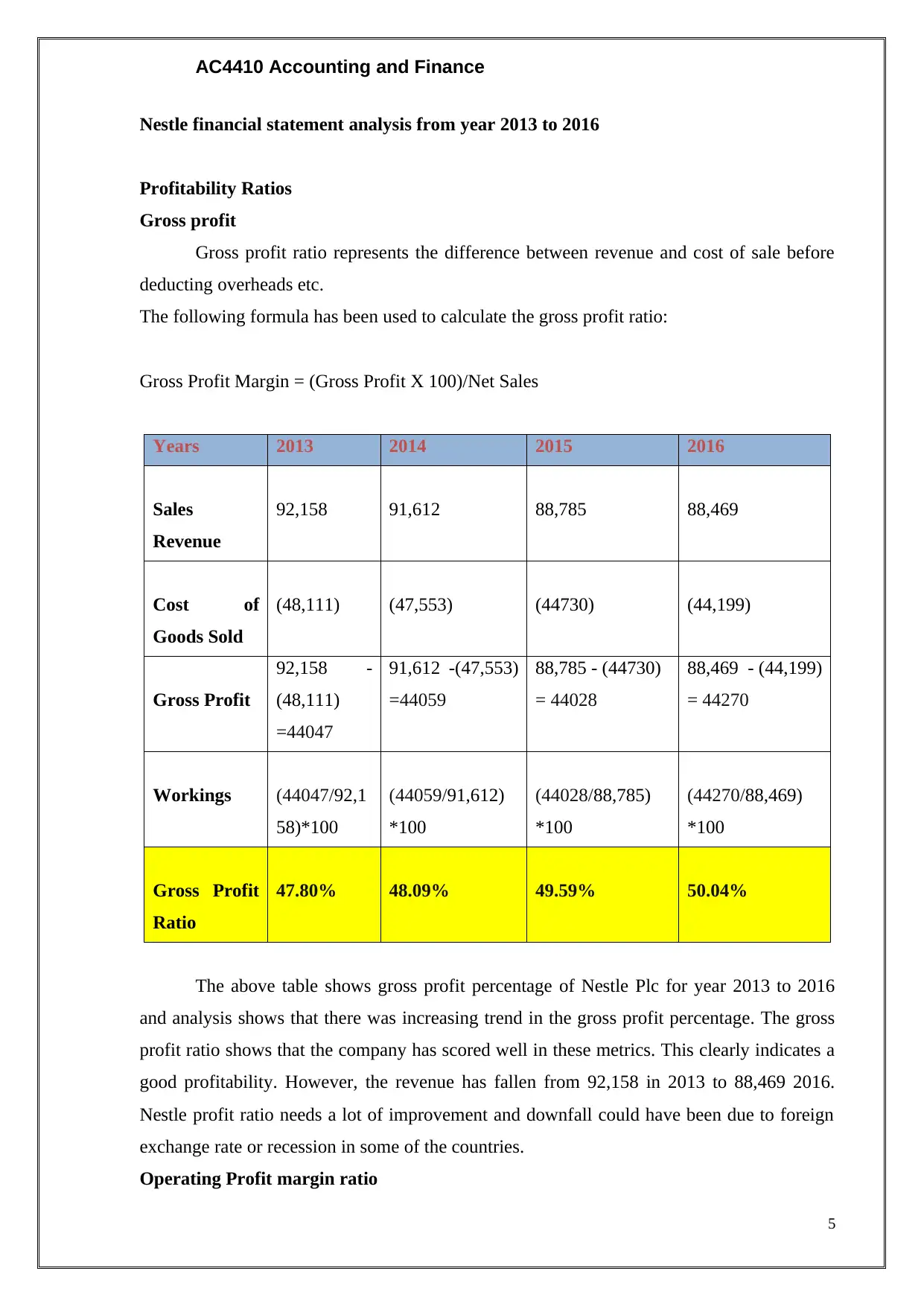

Nestle financial statement analysis from year 2013 to 2016

Profitability Ratios

Gross profit

Gross profit ratio represents the difference between revenue and cost of sale before

deducting overheads etc.

The following formula has been used to calculate the gross profit ratio:

Gross Profit Margin = (Gross Profit X 100)/Net Sales

Years 2013 2014 2015 2016

Sales

Revenue

92,158 91,612 88,785 88,469

Cost of

Goods Sold

(48,111) (47,553) (44730) (44,199)

Gross Profit

92,158 -

(48,111)

=44047

91,612 -(47,553)

=44059

88,785 - (44730)

= 44028

88,469 - (44,199)

= 44270

Workings (44047/92,1

58)*100

(44059/91,612)

*100

(44028/88,785)

*100

(44270/88,469)

*100

Gross Profit

Ratio

47.80% 48.09% 49.59% 50.04%

The above table shows gross profit percentage of Nestle Plc for year 2013 to 2016

and analysis shows that there was increasing trend in the gross profit percentage. The gross

profit ratio shows that the company has scored well in these metrics. This clearly indicates a

good profitability. However, the revenue has fallen from 92,158 in 2013 to 88,469 2016.

Nestle profit ratio needs a lot of improvement and downfall could have been due to foreign

exchange rate or recession in some of the countries.

Operating Profit margin ratio

5

Nestle financial statement analysis from year 2013 to 2016

Profitability Ratios

Gross profit

Gross profit ratio represents the difference between revenue and cost of sale before

deducting overheads etc.

The following formula has been used to calculate the gross profit ratio:

Gross Profit Margin = (Gross Profit X 100)/Net Sales

Years 2013 2014 2015 2016

Sales

Revenue

92,158 91,612 88,785 88,469

Cost of

Goods Sold

(48,111) (47,553) (44730) (44,199)

Gross Profit

92,158 -

(48,111)

=44047

91,612 -(47,553)

=44059

88,785 - (44730)

= 44028

88,469 - (44,199)

= 44270

Workings (44047/92,1

58)*100

(44059/91,612)

*100

(44028/88,785)

*100

(44270/88,469)

*100

Gross Profit

Ratio

47.80% 48.09% 49.59% 50.04%

The above table shows gross profit percentage of Nestle Plc for year 2013 to 2016

and analysis shows that there was increasing trend in the gross profit percentage. The gross

profit ratio shows that the company has scored well in these metrics. This clearly indicates a

good profitability. However, the revenue has fallen from 92,158 in 2013 to 88,469 2016.

Nestle profit ratio needs a lot of improvement and downfall could have been due to foreign

exchange rate or recession in some of the countries.

Operating Profit margin ratio

5

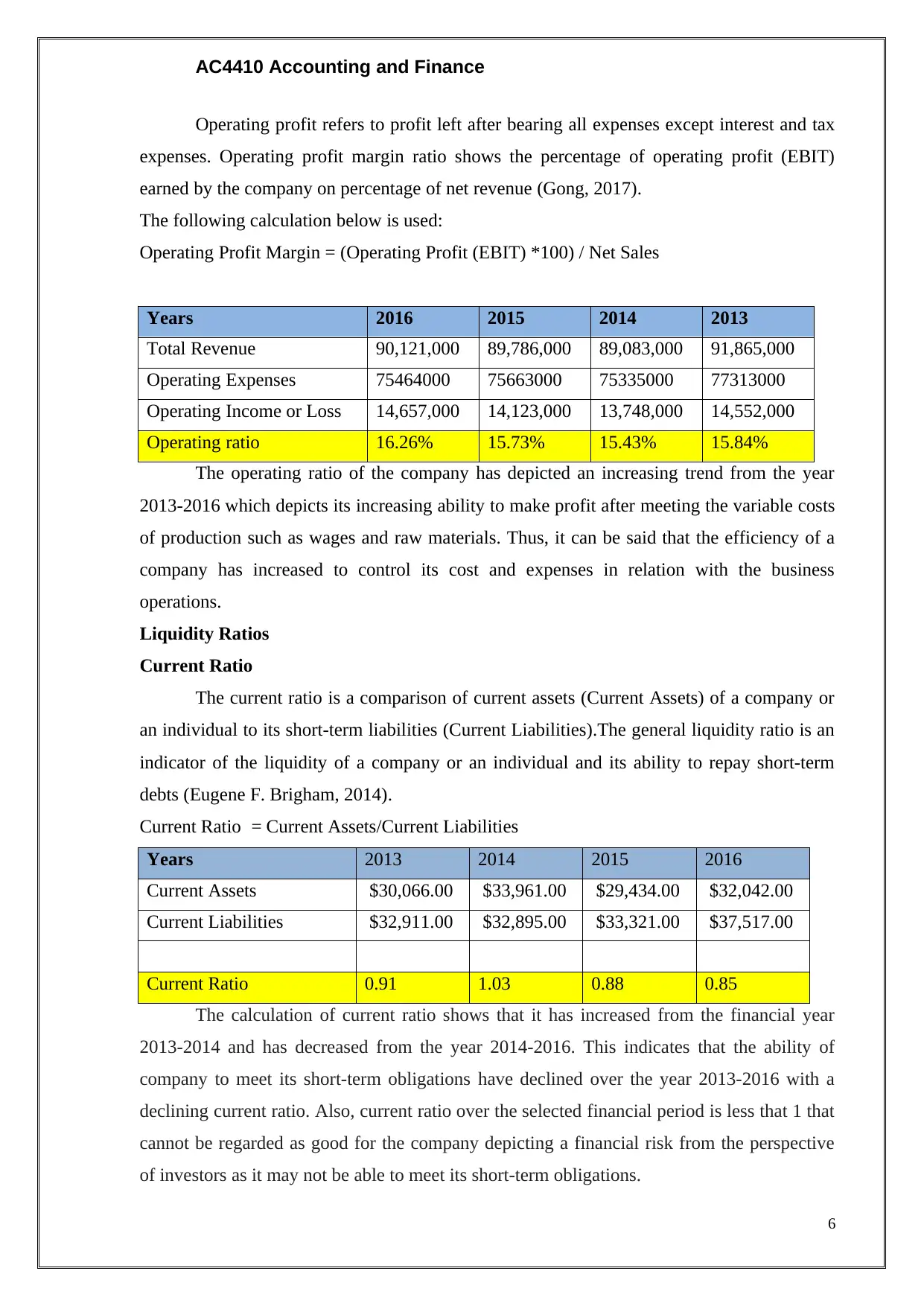

AC4410 Accounting and Finance

Operating profit refers to profit left after bearing all expenses except interest and tax

expenses. Operating profit margin ratio shows the percentage of operating profit (EBIT)

earned by the company on percentage of net revenue (Gong, 2017).

The following calculation below is used:

Operating Profit Margin = (Operating Profit (EBIT) *100) / Net Sales

Years 2016 2015 2014 2013

Total Revenue 90,121,000 89,786,000 89,083,000 91,865,000

Operating Expenses 75464000 75663000 75335000 77313000

Operating Income or Loss 14,657,000 14,123,000 13,748,000 14,552,000

Operating ratio 16.26% 15.73% 15.43% 15.84%

The operating ratio of the company has depicted an increasing trend from the year

2013-2016 which depicts its increasing ability to make profit after meeting the variable costs

of production such as wages and raw materials. Thus, it can be said that the efficiency of a

company has increased to control its cost and expenses in relation with the business

operations.

Liquidity Ratios

Current Ratio

The current ratio is a comparison of current assets (Current Assets) of a company or

an individual to its short-term liabilities (Current Liabilities).The general liquidity ratio is an

indicator of the liquidity of a company or an individual and its ability to repay short-term

debts (Eugene F. Brigham, 2014).

Current Ratio = Current Assets/Current Liabilities

Years 2013 2014 2015 2016

Current Assets $30,066.00 $33,961.00 $29,434.00 $32,042.00

Current Liabilities $32,911.00 $32,895.00 $33,321.00 $37,517.00

Current Ratio 0.91 1.03 0.88 0.85

The calculation of current ratio shows that it has increased from the financial year

2013-2014 and has decreased from the year 2014-2016. This indicates that the ability of

company to meet its short-term obligations have declined over the year 2013-2016 with a

declining current ratio. Also, current ratio over the selected financial period is less that 1 that

cannot be regarded as good for the company depicting a financial risk from the perspective

of investors as it may not be able to meet its short-term obligations.

6

Operating profit refers to profit left after bearing all expenses except interest and tax

expenses. Operating profit margin ratio shows the percentage of operating profit (EBIT)

earned by the company on percentage of net revenue (Gong, 2017).

The following calculation below is used:

Operating Profit Margin = (Operating Profit (EBIT) *100) / Net Sales

Years 2016 2015 2014 2013

Total Revenue 90,121,000 89,786,000 89,083,000 91,865,000

Operating Expenses 75464000 75663000 75335000 77313000

Operating Income or Loss 14,657,000 14,123,000 13,748,000 14,552,000

Operating ratio 16.26% 15.73% 15.43% 15.84%

The operating ratio of the company has depicted an increasing trend from the year

2013-2016 which depicts its increasing ability to make profit after meeting the variable costs

of production such as wages and raw materials. Thus, it can be said that the efficiency of a

company has increased to control its cost and expenses in relation with the business

operations.

Liquidity Ratios

Current Ratio

The current ratio is a comparison of current assets (Current Assets) of a company or

an individual to its short-term liabilities (Current Liabilities).The general liquidity ratio is an

indicator of the liquidity of a company or an individual and its ability to repay short-term

debts (Eugene F. Brigham, 2014).

Current Ratio = Current Assets/Current Liabilities

Years 2013 2014 2015 2016

Current Assets $30,066.00 $33,961.00 $29,434.00 $32,042.00

Current Liabilities $32,911.00 $32,895.00 $33,321.00 $37,517.00

Current Ratio 0.91 1.03 0.88 0.85

The calculation of current ratio shows that it has increased from the financial year

2013-2014 and has decreased from the year 2014-2016. This indicates that the ability of

company to meet its short-term obligations have declined over the year 2013-2016 with a

declining current ratio. Also, current ratio over the selected financial period is less that 1 that

cannot be regarded as good for the company depicting a financial risk from the perspective

of investors as it may not be able to meet its short-term obligations.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AC4410 Accounting and Finance

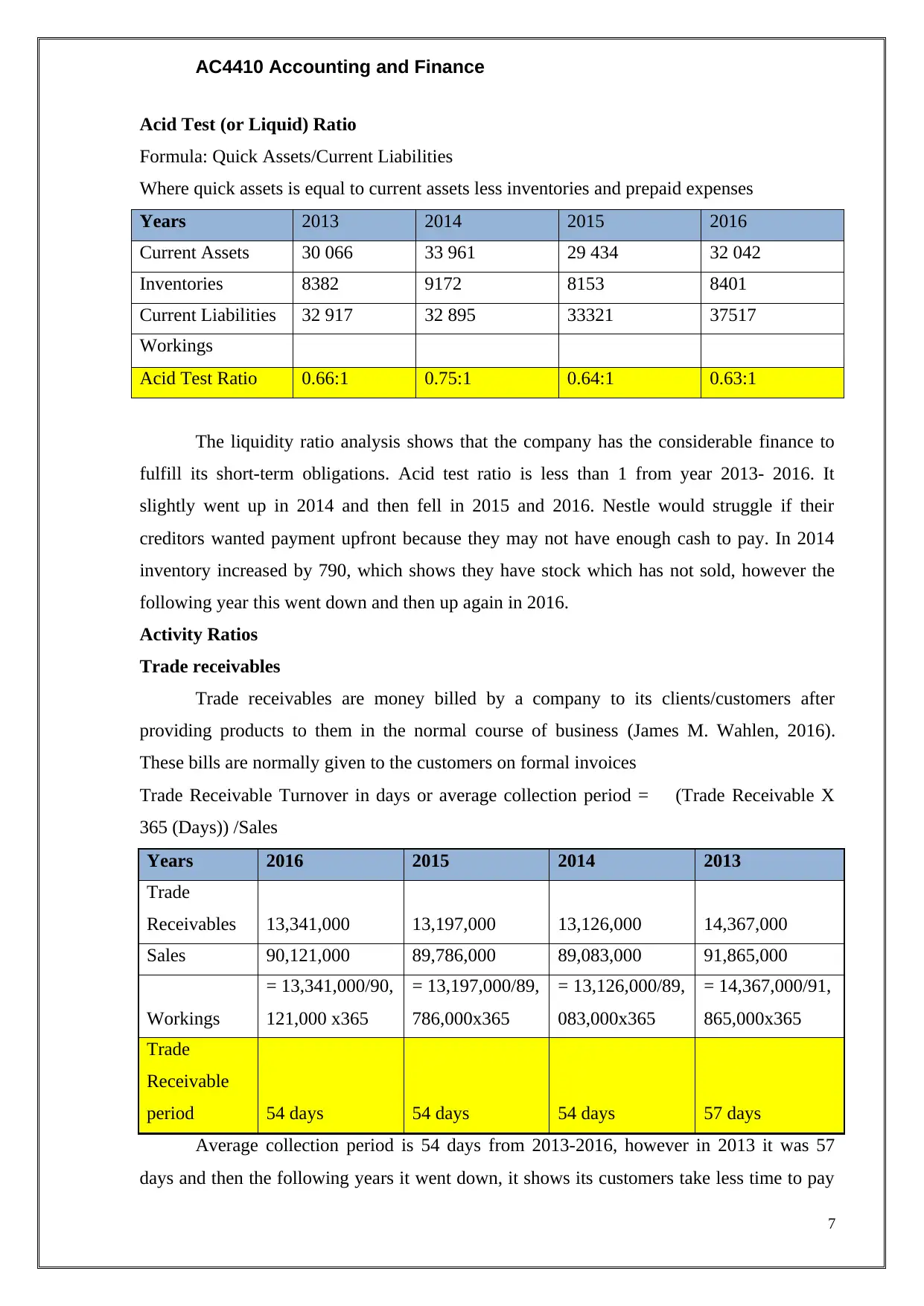

Acid Test (or Liquid) Ratio

Formula: Quick Assets/Current Liabilities

Where quick assets is equal to current assets less inventories and prepaid expenses

Years 2013 2014 2015 2016

Current Assets 30 066 33 961 29 434 32 042

Inventories 8382 9172 8153 8401

Current Liabilities 32 917 32 895 33321 37517

Workings

Acid Test Ratio 0.66:1 0.75:1 0.64:1 0.63:1

The liquidity ratio analysis shows that the company has the considerable finance to

fulfill its short-term obligations. Acid test ratio is less than 1 from year 2013- 2016. It

slightly went up in 2014 and then fell in 2015 and 2016. Nestle would struggle if their

creditors wanted payment upfront because they may not have enough cash to pay. In 2014

inventory increased by 790, which shows they have stock which has not sold, however the

following year this went down and then up again in 2016.

Activity Ratios

Trade receivables

Trade receivables are money billed by a company to its clients/customers after

providing products to them in the normal course of business (James M. Wahlen, 2016).

These bills are normally given to the customers on formal invoices

Trade Receivable Turnover in days or average collection period = (Trade Receivable X

365 (Days)) /Sales

Years 2016 2015 2014 2013

Trade

Receivables 13,341,000 13,197,000 13,126,000 14,367,000

Sales 90,121,000 89,786,000 89,083,000 91,865,000

Workings

= 13,341,000/90,

121,000 x365

= 13,197,000/89,

786,000x365

= 13,126,000/89,

083,000x365

= 14,367,000/91,

865,000x365

Trade

Receivable

period 54 days 54 days 54 days 57 days

Average collection period is 54 days from 2013-2016, however in 2013 it was 57

days and then the following years it went down, it shows its customers take less time to pay

7

Acid Test (or Liquid) Ratio

Formula: Quick Assets/Current Liabilities

Where quick assets is equal to current assets less inventories and prepaid expenses

Years 2013 2014 2015 2016

Current Assets 30 066 33 961 29 434 32 042

Inventories 8382 9172 8153 8401

Current Liabilities 32 917 32 895 33321 37517

Workings

Acid Test Ratio 0.66:1 0.75:1 0.64:1 0.63:1

The liquidity ratio analysis shows that the company has the considerable finance to

fulfill its short-term obligations. Acid test ratio is less than 1 from year 2013- 2016. It

slightly went up in 2014 and then fell in 2015 and 2016. Nestle would struggle if their

creditors wanted payment upfront because they may not have enough cash to pay. In 2014

inventory increased by 790, which shows they have stock which has not sold, however the

following year this went down and then up again in 2016.

Activity Ratios

Trade receivables

Trade receivables are money billed by a company to its clients/customers after

providing products to them in the normal course of business (James M. Wahlen, 2016).

These bills are normally given to the customers on formal invoices

Trade Receivable Turnover in days or average collection period = (Trade Receivable X

365 (Days)) /Sales

Years 2016 2015 2014 2013

Trade

Receivables 13,341,000 13,197,000 13,126,000 14,367,000

Sales 90,121,000 89,786,000 89,083,000 91,865,000

Workings

= 13,341,000/90,

121,000 x365

= 13,197,000/89,

786,000x365

= 13,126,000/89,

083,000x365

= 14,367,000/91,

865,000x365

Trade

Receivable

period 54 days 54 days 54 days 57 days

Average collection period is 54 days from 2013-2016, however in 2013 it was 57

days and then the following years it went down, it shows its customers take less time to pay

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AC4410 Accounting and Finance

back compared to 2013. Another reason for longer time frame in 2013 is because trade

receivable was higher than the other three years.

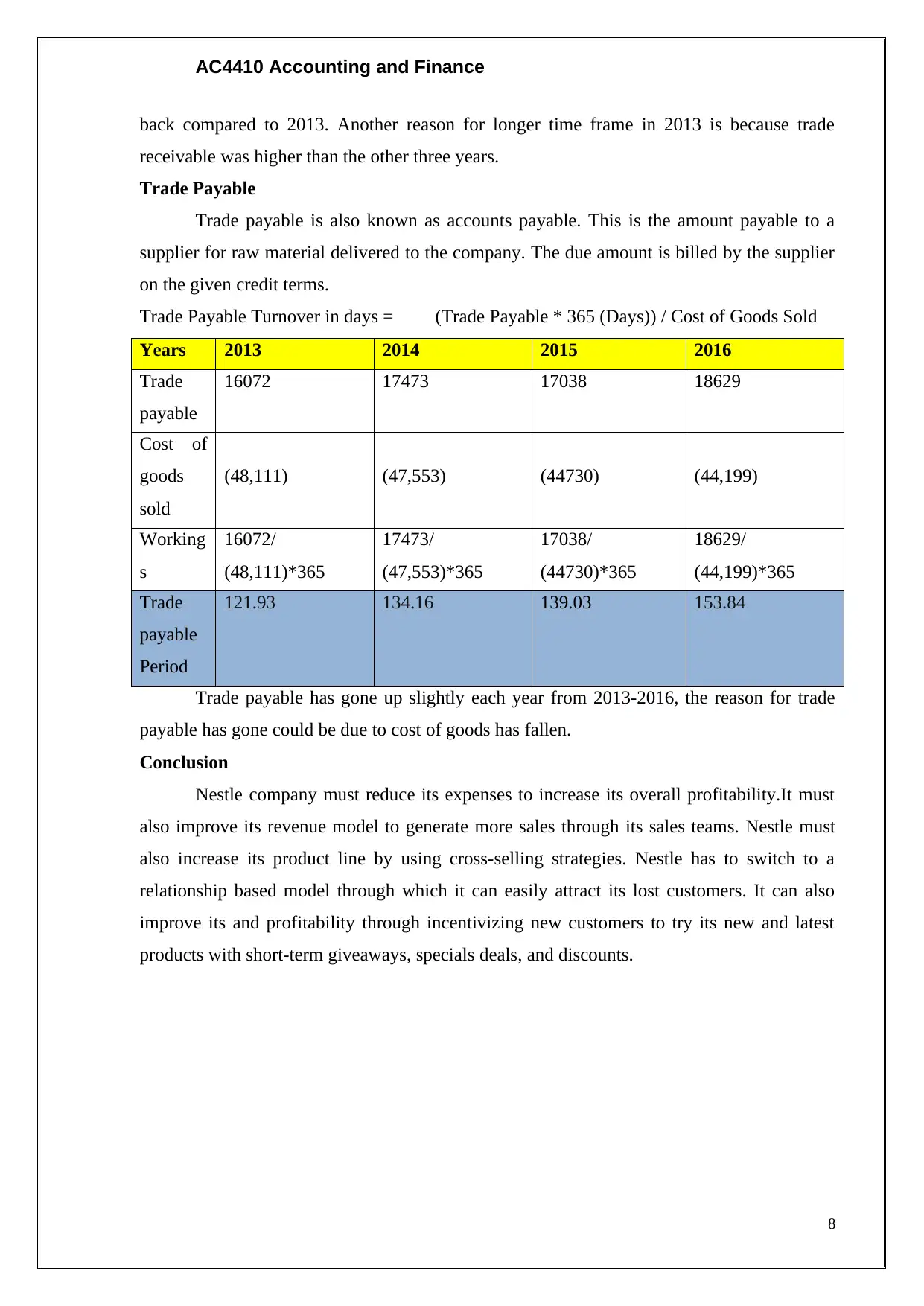

Trade Payable

Trade payable is also known as accounts payable. This is the amount payable to a

supplier for raw material delivered to the company. The due amount is billed by the supplier

on the given credit terms.

Trade Payable Turnover in days = (Trade Payable * 365 (Days)) / Cost of Goods Sold

Years 2013 2014 2015 2016

Trade

payable

16072 17473 17038 18629

Cost of

goods

sold

(48,111) (47,553) (44730) (44,199)

Working

s

16072/

(48,111)*365

17473/

(47,553)*365

17038/

(44730)*365

18629/

(44,199)*365

Trade

payable

Period

121.93 134.16 139.03 153.84

Trade payable has gone up slightly each year from 2013-2016, the reason for trade

payable has gone could be due to cost of goods has fallen.

Conclusion

Nestle company must reduce its expenses to increase its overall profitability.It must

also improve its revenue model to generate more sales through its sales teams. Nestle must

also increase its product line by using cross-selling strategies. Nestle has to switch to a

relationship based model through which it can easily attract its lost customers. It can also

improve its and profitability through incentivizing new customers to try its new and latest

products with short-term giveaways, specials deals, and discounts.

8

back compared to 2013. Another reason for longer time frame in 2013 is because trade

receivable was higher than the other three years.

Trade Payable

Trade payable is also known as accounts payable. This is the amount payable to a

supplier for raw material delivered to the company. The due amount is billed by the supplier

on the given credit terms.

Trade Payable Turnover in days = (Trade Payable * 365 (Days)) / Cost of Goods Sold

Years 2013 2014 2015 2016

Trade

payable

16072 17473 17038 18629

Cost of

goods

sold

(48,111) (47,553) (44730) (44,199)

Working

s

16072/

(48,111)*365

17473/

(47,553)*365

17038/

(44730)*365

18629/

(44,199)*365

Trade

payable

Period

121.93 134.16 139.03 153.84

Trade payable has gone up slightly each year from 2013-2016, the reason for trade

payable has gone could be due to cost of goods has fallen.

Conclusion

Nestle company must reduce its expenses to increase its overall profitability.It must

also improve its revenue model to generate more sales through its sales teams. Nestle must

also increase its product line by using cross-selling strategies. Nestle has to switch to a

relationship based model through which it can easily attract its lost customers. It can also

improve its and profitability through incentivizing new customers to try its new and latest

products with short-term giveaways, specials deals, and discounts.

8

AC4410 Accounting and Finance

Bibliography

Eugene F. Brigham, J. F. (2014). Fundamentals of Financial Management. Cengage

Learning.

Gong, Z. (2017). Comparing the development of two communication technology companies

using financial statement analysis. GRIN Verlag.

J. Chris Leach, R. W. (2016). Entrepreneurial Finance. Cengage Learning.

James M. Wahlen, J. P. (2016). Intermediate Accounting: Reporting and Analysis. Cengage

Learning.

McGowan, C. (2014). The Fundamentals of Financial Statement Analysis as Applied to the

Coca-Cola Company. Business Expert Press.

Stephen A. Ross, R. M. (2016). Essentials of Corporate Finance, Fourth Edition. McGraw-

Hill Education Australia.

Timothy R. Mayes, T. M. (2016). Financial Analysis with Microsoft Excel 2016. Cengage

Learning.

Tracy, A. (2012). Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to

Analyse Any Business on the Planet. Ratio Analysis.

9

Bibliography

Eugene F. Brigham, J. F. (2014). Fundamentals of Financial Management. Cengage

Learning.

Gong, Z. (2017). Comparing the development of two communication technology companies

using financial statement analysis. GRIN Verlag.

J. Chris Leach, R. W. (2016). Entrepreneurial Finance. Cengage Learning.

James M. Wahlen, J. P. (2016). Intermediate Accounting: Reporting and Analysis. Cengage

Learning.

McGowan, C. (2014). The Fundamentals of Financial Statement Analysis as Applied to the

Coca-Cola Company. Business Expert Press.

Stephen A. Ross, R. M. (2016). Essentials of Corporate Finance, Fourth Edition. McGraw-

Hill Education Australia.

Timothy R. Mayes, T. M. (2016). Financial Analysis with Microsoft Excel 2016. Cengage

Learning.

Tracy, A. (2012). Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to

Analyse Any Business on the Planet. Ratio Analysis.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AC4410 Accounting and Finance

Appendix

http://www.nestle.com/asset-library/Documents/Library/Documents/Financial_Statements/

2013-Financial-Statements-EN.pdf

http://www.nestle.com/asset-library/Documents/Library/Documents/Financial_Statements/

2014-Financial-Statements-EN.pdf

http://www.nestle.com/asset-library/Documents/Library/Documents/Financial_Statements/

2015-Financial-Statements-EN.pdf

http://www.nestle.com/asset-library/Documents/Library/Documents/Financial_Statements/

2016-Financial-Statements-EN.pdf

.

10

Appendix

http://www.nestle.com/asset-library/Documents/Library/Documents/Financial_Statements/

2013-Financial-Statements-EN.pdf

http://www.nestle.com/asset-library/Documents/Library/Documents/Financial_Statements/

2014-Financial-Statements-EN.pdf

http://www.nestle.com/asset-library/Documents/Library/Documents/Financial_Statements/

2015-Financial-Statements-EN.pdf

http://www.nestle.com/asset-library/Documents/Library/Documents/Financial_Statements/

2016-Financial-Statements-EN.pdf

.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.