Efficient Portfolio Management: Impact on Investors and Financial Market

VerifiedAdded on 2023/04/22

|18

|2516

|198

AI Summary

This report analyzes the impact of efficient portfolio management on investors and the financial market. It discusses the concept of efficient frontier, Harry Markowitz and William Sharpe models, and the use of trend lines and separation property in portfolio construction. The report also evaluates the performance of optimal portfolios using Sharpe ratio and compares the Markowitz and Sharpe models.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Finance portfolio management

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction

The efficient portfolio offers various benefits to the investors and also the financial market.

Selection of optimal portfolio offers the maximum return to the investors and also helps them to

diversify or set off the risk with other security return. This report will represent that how optimal

portfolio impact positively to the investors and also states that how efficient portfolio frontier

provides an expected return. This report also states that Harry Markowitz and William Sharpe

model helps to the investor in measuring the performance of optimal portfolio and also helps in

creating the optimal portfolio for the future growth and development of an investor in various

manners.

2

The efficient portfolio offers various benefits to the investors and also the financial market.

Selection of optimal portfolio offers the maximum return to the investors and also helps them to

diversify or set off the risk with other security return. This report will represent that how optimal

portfolio impact positively to the investors and also states that how efficient portfolio frontier

provides an expected return. This report also states that Harry Markowitz and William Sharpe

model helps to the investor in measuring the performance of optimal portfolio and also helps in

creating the optimal portfolio for the future growth and development of an investor in various

manners.

2

Analysis of an efficient portfolio in Australia

A selection of an efficient portfolio provides a source of income to the investors. The process of

selection a portfolio may be divided into two parts. The first part commences with experience

and observation and completes with beliefs about the future performances of available securities.

The second part commences with the appropriate beliefs about future performances and

completes with the optimal selection of portfolio. The investors can use various techniques of

portfolio selection to measure the expected returns and level of risk (Pavlou, Doumpos, &

Zopounidis, 2018).

Efficient Frontier

The efficient frontier is the set of ideal or optimal portfolios which provides maximum expected

return to the investors with defined level of risk. This concept is basically introduced by “Harry

Markowitz” and it is easily to understand. Efficient frontier is a graphical representation of all

optimal securities. It is basically shows the risk and returns trade- off of a portfolio and help to

the investors in imagine the efficient portfolios (Chandra, 2017).

Harry Markowitz’s modern portfolio theory described efficient frontier in an appropriate manner.

Efficient portfolio frontier is related to the Markowitz’s portfolio theory which are discussed

below and represented in a diagram.

3

A selection of an efficient portfolio provides a source of income to the investors. The process of

selection a portfolio may be divided into two parts. The first part commences with experience

and observation and completes with beliefs about the future performances of available securities.

The second part commences with the appropriate beliefs about future performances and

completes with the optimal selection of portfolio. The investors can use various techniques of

portfolio selection to measure the expected returns and level of risk (Pavlou, Doumpos, &

Zopounidis, 2018).

Efficient Frontier

The efficient frontier is the set of ideal or optimal portfolios which provides maximum expected

return to the investors with defined level of risk. This concept is basically introduced by “Harry

Markowitz” and it is easily to understand. Efficient frontier is a graphical representation of all

optimal securities. It is basically shows the risk and returns trade- off of a portfolio and help to

the investors in imagine the efficient portfolios (Chandra, 2017).

Harry Markowitz’s modern portfolio theory described efficient frontier in an appropriate manner.

Efficient portfolio frontier is related to the Markowitz’s portfolio theory which are discussed

below and represented in a diagram.

3

Figure 1: Efficient Frontier

By Author, 2019

The above graph shows all the results of various portfolio combinations of risky assets. In the

graph standard deviation is lie on the X-axis and return is lie on the Y-axis.

Tangency Portfolio is the point where the portfolio of only risk- free securities meets the

combination of risky securities.

The Capital allocation line or straight line shows a portfolio of all the risk-free securities and

risky securities, which is generally a government bond.

Lower section of the hyperbole of portfolio will have poor return and ultimately maximum risk

to the investors. Portfolios to the right will have maximum returns but also maximum risk.

Markowitz Portfolio Concept is the base idea of the “Ways to Wealth Concept”

Efficient portfolio importance for the last two decades in Australia

An efficient portfolio helps to the investors to earn more return from the market. The purpose of

efficient frontier is to maximize returns while minimizing volatility. A risk-opposed investor’s

aim is to find out the combination of investment which harvests the maximum return with little

bit risk which is affordable by him. The efficient frontier plot portfolio that gives the identical

4

By Author, 2019

The above graph shows all the results of various portfolio combinations of risky assets. In the

graph standard deviation is lie on the X-axis and return is lie on the Y-axis.

Tangency Portfolio is the point where the portfolio of only risk- free securities meets the

combination of risky securities.

The Capital allocation line or straight line shows a portfolio of all the risk-free securities and

risky securities, which is generally a government bond.

Lower section of the hyperbole of portfolio will have poor return and ultimately maximum risk

to the investors. Portfolios to the right will have maximum returns but also maximum risk.

Markowitz Portfolio Concept is the base idea of the “Ways to Wealth Concept”

Efficient portfolio importance for the last two decades in Australia

An efficient portfolio helps to the investors to earn more return from the market. The purpose of

efficient frontier is to maximize returns while minimizing volatility. A risk-opposed investor’s

aim is to find out the combination of investment which harvests the maximum return with little

bit risk which is affordable by him. The efficient frontier plot portfolio that gives the identical

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

risk- returns trade-off. The last two decades in Australia, the investors use the efficient portfolio

frontier to find out each investment returns and the level of risk associated with them (Clarke, De

Silva, & Thorley, 2016).

For example:

Mr. A has two securities, Security A and Security B, for investment. The following table

shows Mr. A expectation for expected return and standard deviation:

Securities Expected return (Er) Standard Deviation

A 12% 6%

B 8% 4%

The correlation coefficient between returns on both assets is estimated to be 0.6

Following table represents Mr. A portfolio’s standard deviation and expected return at different

mix of A and B

Security A Weight Security B Weight Portfolio Standard

Deviation

Portfolio Standard

Deviation

100% 0% 6% 12%

80% 20% 4.87% 11.20%

60% 40% 3.94% 10.4%

5

frontier to find out each investment returns and the level of risk associated with them (Clarke, De

Silva, & Thorley, 2016).

For example:

Mr. A has two securities, Security A and Security B, for investment. The following table

shows Mr. A expectation for expected return and standard deviation:

Securities Expected return (Er) Standard Deviation

A 12% 6%

B 8% 4%

The correlation coefficient between returns on both assets is estimated to be 0.6

Following table represents Mr. A portfolio’s standard deviation and expected return at different

mix of A and B

Security A Weight Security B Weight Portfolio Standard

Deviation

Portfolio Standard

Deviation

100% 0% 6% 12%

80% 20% 4.87% 11.20%

60% 40% 3.94% 10.4%

5

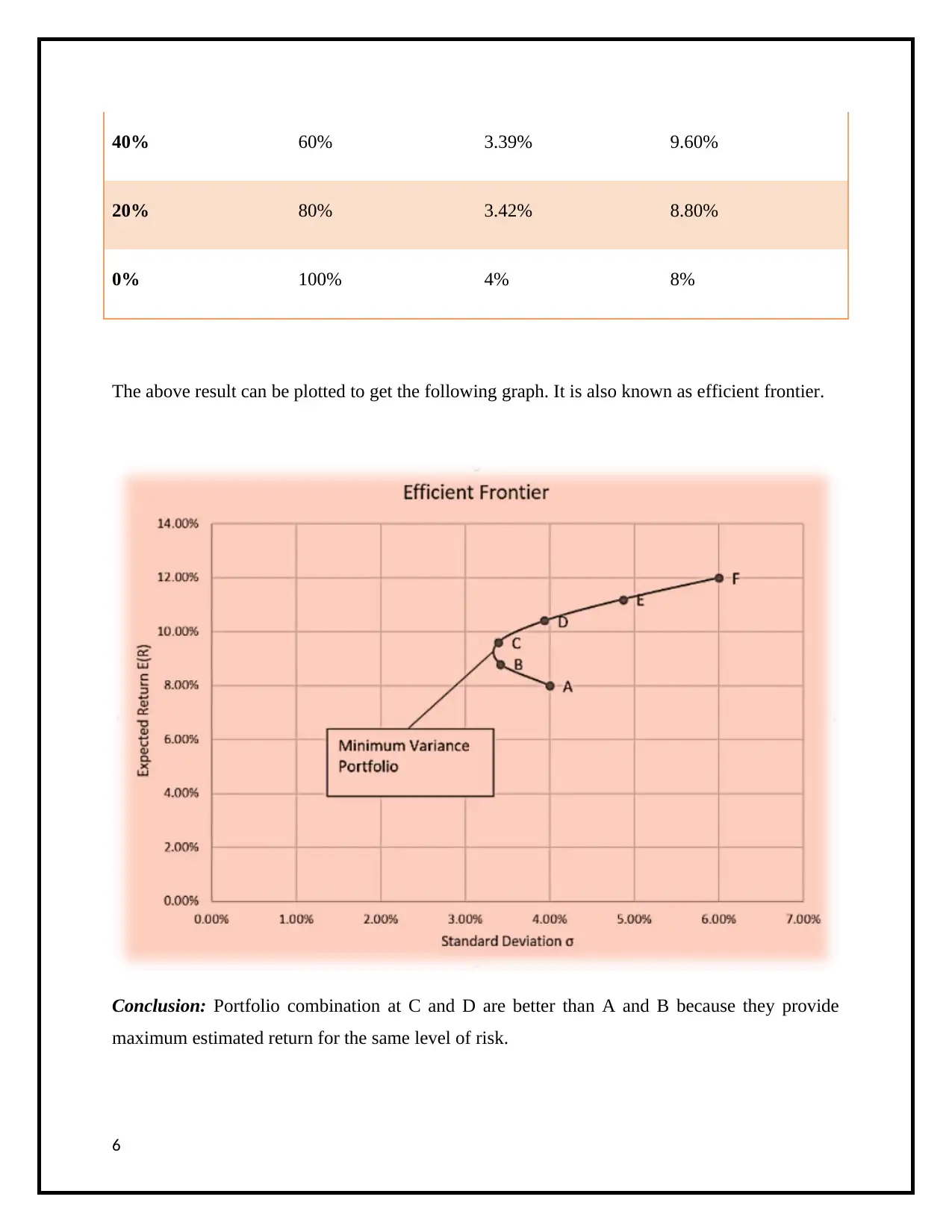

40% 60% 3.39% 9.60%

20% 80% 3.42% 8.80%

0% 100% 4% 8%

The above result can be plotted to get the following graph. It is also known as efficient frontier.

Conclusion: Portfolio combination at C and D are better than A and B because they provide

maximum estimated return for the same level of risk.

6

20% 80% 3.42% 8.80%

0% 100% 4% 8%

The above result can be plotted to get the following graph. It is also known as efficient frontier.

Conclusion: Portfolio combination at C and D are better than A and B because they provide

maximum estimated return for the same level of risk.

6

With the help of this the investor can know level of risk associate with the investment and also

find out the highest level of return from the investment.

Trend line

In a technical analysis, a trend lines are important tool for both trend identification and

confirmation in the capital market. Trend analysis is a straight line that joins two or more price

point and then spreads into the upcoming period to act as a support line and resistance (Edwards,

Magee, & Bassetti, 2018).

7

find out the highest level of return from the investment.

Trend line

In a technical analysis, a trend lines are important tool for both trend identification and

confirmation in the capital market. Trend analysis is a straight line that joins two or more price

point and then spreads into the upcoming period to act as a support line and resistance (Edwards,

Magee, & Bassetti, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Uptrend market is selected for the creation of portfolio:

Figure 2: Uptrend Line

By Author, 2018

This trend line shows a positive slope in the graph to the investors and is formed by connecting

two or more low points. It is also support and shows that net- demand is growing up even as the

rise price. The uptrend line is also considered as compact and integral. A growing price

associated with rising demand is very bullish and indicates a strong fortitude on the part of the

purchasers.

8

Figure 2: Uptrend Line

By Author, 2018

This trend line shows a positive slope in the graph to the investors and is formed by connecting

two or more low points. It is also support and shows that net- demand is growing up even as the

rise price. The uptrend line is also considered as compact and integral. A growing price

associated with rising demand is very bullish and indicates a strong fortitude on the part of the

purchasers.

8

Daily Data of Equity for the period January 2015-December 2018.

2015

2016

9

2015

2016

9

2017

2018

10

2018

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

Construction of portfolio (four stocks)

Aristocrat Leisure Limited

Type of Company: Consumer Discretionary

Manufactures, designs, develops and markets a different variety of products and services

comprising electronic gaming machines, casino, digital social games and management systems.

CSL Limited

Type of Company: Health Care

Expansion, marketing and manufacturing of pharmaceutical and investigative products, human

plasma fractions and cell culture media.

WOW (WOOLWORTHS GROUP LIMITED)

Type of Company: Consumer Staples

General merchandise, food and specialty retailing through chain store operations.

WES (WESFARMERS LIMITED)

Type of Company: Consumer Discretionary

Expanded industrial with benefits comprising operations of retail covering general merchandise,

supermarkets and specialty divisions stores, liquor and fuel outlets and office supplies and home

12

Aristocrat Leisure Limited

Type of Company: Consumer Discretionary

Manufactures, designs, develops and markets a different variety of products and services

comprising electronic gaming machines, casino, digital social games and management systems.

CSL Limited

Type of Company: Health Care

Expansion, marketing and manufacturing of pharmaceutical and investigative products, human

plasma fractions and cell culture media.

WOW (WOOLWORTHS GROUP LIMITED)

Type of Company: Consumer Staples

General merchandise, food and specialty retailing through chain store operations.

WES (WESFARMERS LIMITED)

Type of Company: Consumer Discretionary

Expanded industrial with benefits comprising operations of retail covering general merchandise,

supermarkets and specialty divisions stores, liquor and fuel outlets and office supplies and home

12

improvement; gas processing, coal mining and distribution; insurance; fertilizers and chemicals;

and safety product and industrial distribution.

Analysis and Evaluation

The efficient frontier represents all the dominant portfolios in risk or return space. Efficient limit

is the combination of best or ideal portfolios that gives the maximum estimated return to the

investors for a defined level of risk. The portfolio of securities that shown underneath to the

efficient frontier are sub- ideal because they do not give expected profit to the investors whereas

portfolios that lie to the efficient limit are ideal or optimal to the investors and also provides

expected or more returns to the investors (Heaton, Polson, & Witte, 2016).

For example: The risk-free rate is 6% p.a. which include 3 months T-bill rate as a risk free rate

and the expected return on the stock market is 10% with a standard deviation of 20%. The ABC

LTD. common stock’s returns are 40% correlated with the stock market return and has a standard

deviation of 80%. What is the expected return for ABC LTD stock?

Ans. E (Ri) = Rf + βi (Rm – Rf)

If βi = COVi,M / M2

βi = 0.40/0.80

= 0.50

Rf = 6%/12*3 = 1.5%

Note: Beta is less than one means that the stock is less volatile than the market as a whole or

vice-versa.

E(Ri) = 1.5% + 0.50 ( 10%- 6%)

= 2*4

13

and safety product and industrial distribution.

Analysis and Evaluation

The efficient frontier represents all the dominant portfolios in risk or return space. Efficient limit

is the combination of best or ideal portfolios that gives the maximum estimated return to the

investors for a defined level of risk. The portfolio of securities that shown underneath to the

efficient frontier are sub- ideal because they do not give expected profit to the investors whereas

portfolios that lie to the efficient limit are ideal or optimal to the investors and also provides

expected or more returns to the investors (Heaton, Polson, & Witte, 2016).

For example: The risk-free rate is 6% p.a. which include 3 months T-bill rate as a risk free rate

and the expected return on the stock market is 10% with a standard deviation of 20%. The ABC

LTD. common stock’s returns are 40% correlated with the stock market return and has a standard

deviation of 80%. What is the expected return for ABC LTD stock?

Ans. E (Ri) = Rf + βi (Rm – Rf)

If βi = COVi,M / M2

βi = 0.40/0.80

= 0.50

Rf = 6%/12*3 = 1.5%

Note: Beta is less than one means that the stock is less volatile than the market as a whole or

vice-versa.

E(Ri) = 1.5% + 0.50 ( 10%- 6%)

= 2*4

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 8%

Application of Separation property to the portfolio

A separation property is an important part of modern portfolio theory that provides a portfolio

manager to detach the satisfaction process into two distinct portions:

The first portion of separation property is the determination of the “optimal risky portfolio”

whereas the second portion is modifying the use of that portfolio to the risk-aversive wants of

each individual user (Lorig & Sircar, 2016).

Sharpe performance measure of the optimal portfolio

Sharpe ratio helps to the investor to measure the performance of optimal portfolio. Sharper ratio

is the portion of risk- adjusted return of a portfolio. A portfolio which has a highest Sharpe ratio

is considered as good and optimal to the investors (Dhrymes, 2017).

Sharpe ratio is calculated by following formula:

= {R (p) – R (f)} /s (p)

Where R (p): Portfolio Return

S (p): Standard deviation of the portfolio

R (f): Risk free rate of return

The Sharpe ratio is a measure of return that is always used to compare the investment

performance managers by constructing an adjustment for risk.

If the risk-free rate is changed by +1% and -1% then the Sharpe fluctuate and the estimated rate

of return and level of risk associated is also changed.

If the risk-free rate of return is +1% then the security performed better in the financial market

whereas if the risk-free rate of return is -1% then the security performed worse in the market.

Risk premium or reward of Sharpe Ratio to the variability of risk or return as measured by the

standard deviation of return (Padma & Rambabu, 2017).

14

Application of Separation property to the portfolio

A separation property is an important part of modern portfolio theory that provides a portfolio

manager to detach the satisfaction process into two distinct portions:

The first portion of separation property is the determination of the “optimal risky portfolio”

whereas the second portion is modifying the use of that portfolio to the risk-aversive wants of

each individual user (Lorig & Sircar, 2016).

Sharpe performance measure of the optimal portfolio

Sharpe ratio helps to the investor to measure the performance of optimal portfolio. Sharper ratio

is the portion of risk- adjusted return of a portfolio. A portfolio which has a highest Sharpe ratio

is considered as good and optimal to the investors (Dhrymes, 2017).

Sharpe ratio is calculated by following formula:

= {R (p) – R (f)} /s (p)

Where R (p): Portfolio Return

S (p): Standard deviation of the portfolio

R (f): Risk free rate of return

The Sharpe ratio is a measure of return that is always used to compare the investment

performance managers by constructing an adjustment for risk.

If the risk-free rate is changed by +1% and -1% then the Sharpe fluctuate and the estimated rate

of return and level of risk associated is also changed.

If the risk-free rate of return is +1% then the security performed better in the financial market

whereas if the risk-free rate of return is -1% then the security performed worse in the market.

Risk premium or reward of Sharpe Ratio to the variability of risk or return as measured by the

standard deviation of return (Padma & Rambabu, 2017).

14

The use of the Markowitz portfolio model in the construction of the optimal portfolio

compared with the single index model.

William Sharpe simplifies the Markowitz Model by decreasing the data in a substantive manner.

Sharpe has improved the method of Markowitz but he also introduced some inputs in his model.

Harry Markowitz suggested that the investors were mainly focused on assessing the risk and

return of individual securities when construction of an optimal portfolio. Markowitz offers an

approach that is called diversification, where the portfolio construction is made after evaluation

of the overall risk portfolio. The diversification idea of Harry Markowitz is subject to fact that

with increasing number of assets or securities in the optimal portfolios, the risk can be diversified

or set- off with the other assets or securities by an investor (Way, et. al., 2019). It is a simple

method for the investors and provides an idea to use diversification technique to diversify the

level of risk with other securities. Expected return and risk as used by investors are measured by

the first two probability moments i.e., expected variance and value of the security. This model

also said that there is no transaction cost or taxes on the security or asset which are purchased by

the investors to form an optimal portfolio to earn return. The financial or capital markets are

frictionless and not give any harm to the investors (Chandra, 2017).

But the Sharpe model is just opposite to the Markowitz model because it measure portfolio

performance by giving risk premium per unit of total risk which is calculated by the portfolio

standard deviation of return (Kellner & Utz, 2019).

15

compared with the single index model.

William Sharpe simplifies the Markowitz Model by decreasing the data in a substantive manner.

Sharpe has improved the method of Markowitz but he also introduced some inputs in his model.

Harry Markowitz suggested that the investors were mainly focused on assessing the risk and

return of individual securities when construction of an optimal portfolio. Markowitz offers an

approach that is called diversification, where the portfolio construction is made after evaluation

of the overall risk portfolio. The diversification idea of Harry Markowitz is subject to fact that

with increasing number of assets or securities in the optimal portfolios, the risk can be diversified

or set- off with the other assets or securities by an investor (Way, et. al., 2019). It is a simple

method for the investors and provides an idea to use diversification technique to diversify the

level of risk with other securities. Expected return and risk as used by investors are measured by

the first two probability moments i.e., expected variance and value of the security. This model

also said that there is no transaction cost or taxes on the security or asset which are purchased by

the investors to form an optimal portfolio to earn return. The financial or capital markets are

frictionless and not give any harm to the investors (Chandra, 2017).

But the Sharpe model is just opposite to the Markowitz model because it measure portfolio

performance by giving risk premium per unit of total risk which is calculated by the portfolio

standard deviation of return (Kellner & Utz, 2019).

15

Conclusion

This report concluded that the efficient portfolio provides an expected or more return to the

investors from the financial market. By using the various models, an investor can create an

optimal portfolio for increasing the wealth and investment. In this report the efficient portfolio

frontier provides an optimal or ideal level of return or more return to the investors. Harry

Markowitz and William Sharpe is best model which provides an idea to the investors while

creating an optimal portfolio for their future growth and development. The Sharpe model helps

to the investors to check the performance level of the ideal or optimal portfolio by comparing the

past trend of the financial market.

16

This report concluded that the efficient portfolio provides an expected or more return to the

investors from the financial market. By using the various models, an investor can create an

optimal portfolio for increasing the wealth and investment. In this report the efficient portfolio

frontier provides an optimal or ideal level of return or more return to the investors. Harry

Markowitz and William Sharpe is best model which provides an idea to the investors while

creating an optimal portfolio for their future growth and development. The Sharpe model helps

to the investors to check the performance level of the ideal or optimal portfolio by comparing the

past trend of the financial market.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

References

Chandra, P. (2017). Investment analysis and portfolio management. McGraw-Hill Education,

2017.

Clarke, R., De Silva, H., & Thorley, S. (2016). Fundamentals of Efficient Factor Investing.

Dhrymes, P. J. (2017). Portfolio theory: origins, Markowitz and CAPM based selection.

In Portfolio Construction, Measurement, and Efficiency (pp. 39-48). Springer, Cham.

Edwards, R. D., Magee, J., & Bassetti, W. C. (2018). Technical analysis of stock trends. CRC

press. (corrected May 2017). Financial Analysts Journal, 72(6), 9-26.

Heaton, J. B., Polson, N. G., & Witte, J. H. (2016). Deep portfolio theory. arXiv preprint

arXiv:1605.07230.

Kellner, F., & Utz, S. (2019). Sustainability in supplier selection and order allocation: combining

integer variables with Markowitz portfolio theory. Journal of Cleaner Production, 214,

462-474.

Lorig, M., & Sircar, R. (2016). Portfolio optimization under local-stochastic volatility:

Coefficient taylor series approximations and implied Sharpe ratio. SIAM Journal on

Financial Mathematics, 7(1), 418-447.

Padma, A., & Rambabu, G. (2017). Optimal Portfolio Construction by Using Sharpe Single

Index Model. Sumedha Journal of Management, 6(4), 57-65.

Pavlou, A., Doumpos, M., & Zopounidis, C. (2018). The Robustness of Portfolio Optimization

Models: An Empirical Comparative Analysis. In Perspectives, Trends, and Applications

in Corporate Finance and Accounting (pp. 210-229). IGI Global.

Way, R., Lafond, F., Lillo, F., Panchenko, V., & Farmer, J. D. (2019). Wright meets Markowitz:

How standard portfolio theory changes when assets are technologies following

experience curves. Journal of Economic Dynamics and Control.

17

Chandra, P. (2017). Investment analysis and portfolio management. McGraw-Hill Education,

2017.

Clarke, R., De Silva, H., & Thorley, S. (2016). Fundamentals of Efficient Factor Investing.

Dhrymes, P. J. (2017). Portfolio theory: origins, Markowitz and CAPM based selection.

In Portfolio Construction, Measurement, and Efficiency (pp. 39-48). Springer, Cham.

Edwards, R. D., Magee, J., & Bassetti, W. C. (2018). Technical analysis of stock trends. CRC

press. (corrected May 2017). Financial Analysts Journal, 72(6), 9-26.

Heaton, J. B., Polson, N. G., & Witte, J. H. (2016). Deep portfolio theory. arXiv preprint

arXiv:1605.07230.

Kellner, F., & Utz, S. (2019). Sustainability in supplier selection and order allocation: combining

integer variables with Markowitz portfolio theory. Journal of Cleaner Production, 214,

462-474.

Lorig, M., & Sircar, R. (2016). Portfolio optimization under local-stochastic volatility:

Coefficient taylor series approximations and implied Sharpe ratio. SIAM Journal on

Financial Mathematics, 7(1), 418-447.

Padma, A., & Rambabu, G. (2017). Optimal Portfolio Construction by Using Sharpe Single

Index Model. Sumedha Journal of Management, 6(4), 57-65.

Pavlou, A., Doumpos, M., & Zopounidis, C. (2018). The Robustness of Portfolio Optimization

Models: An Empirical Comparative Analysis. In Perspectives, Trends, and Applications

in Corporate Finance and Accounting (pp. 210-229). IGI Global.

Way, R., Lafond, F., Lillo, F., Panchenko, V., & Farmer, J. D. (2019). Wright meets Markowitz:

How standard portfolio theory changes when assets are technologies following

experience curves. Journal of Economic Dynamics and Control.

17

18

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.