Petral Ltd: Analysis of Costing Methods for Products W and Z-2018

VerifiedAdded on 2023/06/14

|5

|1272

|147

Report

AI Summary

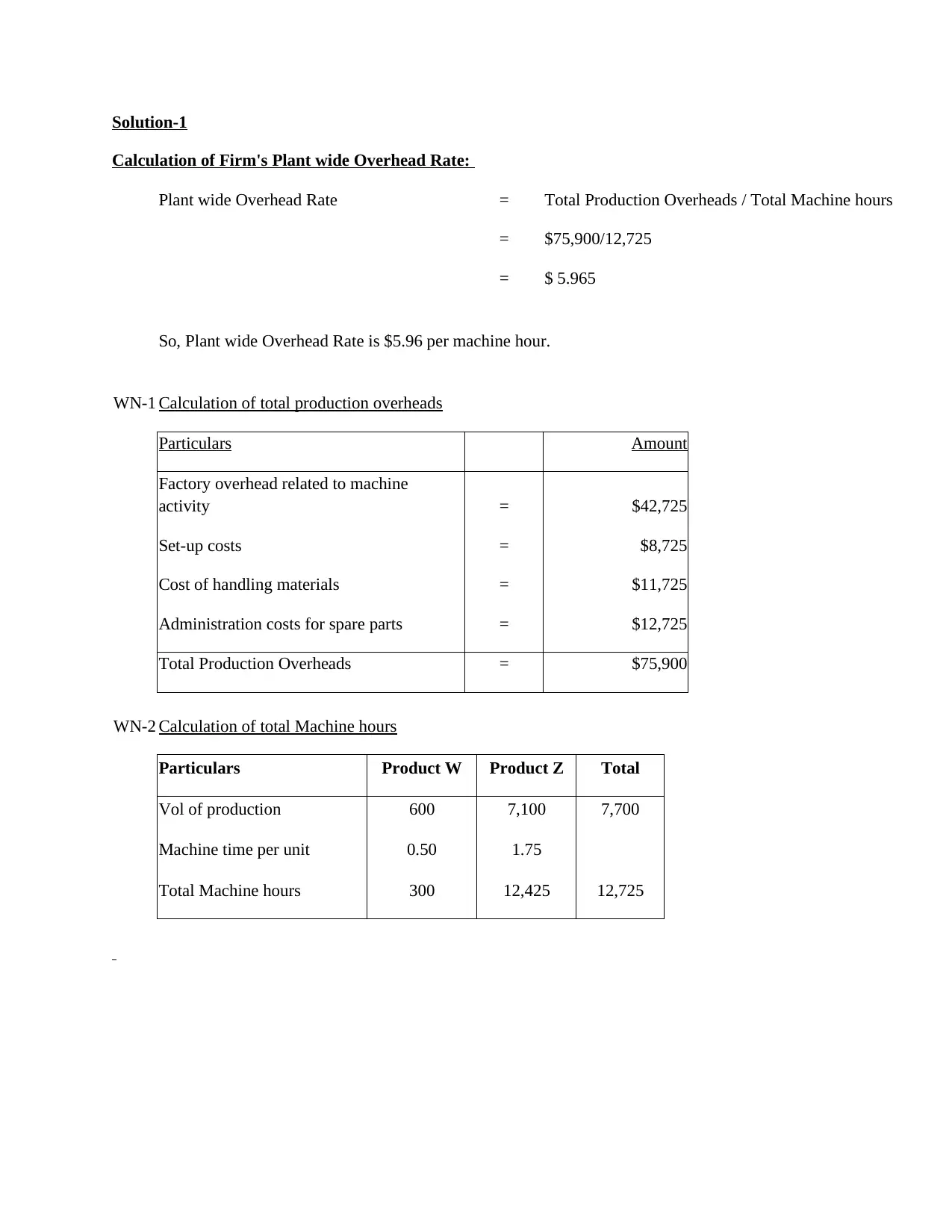

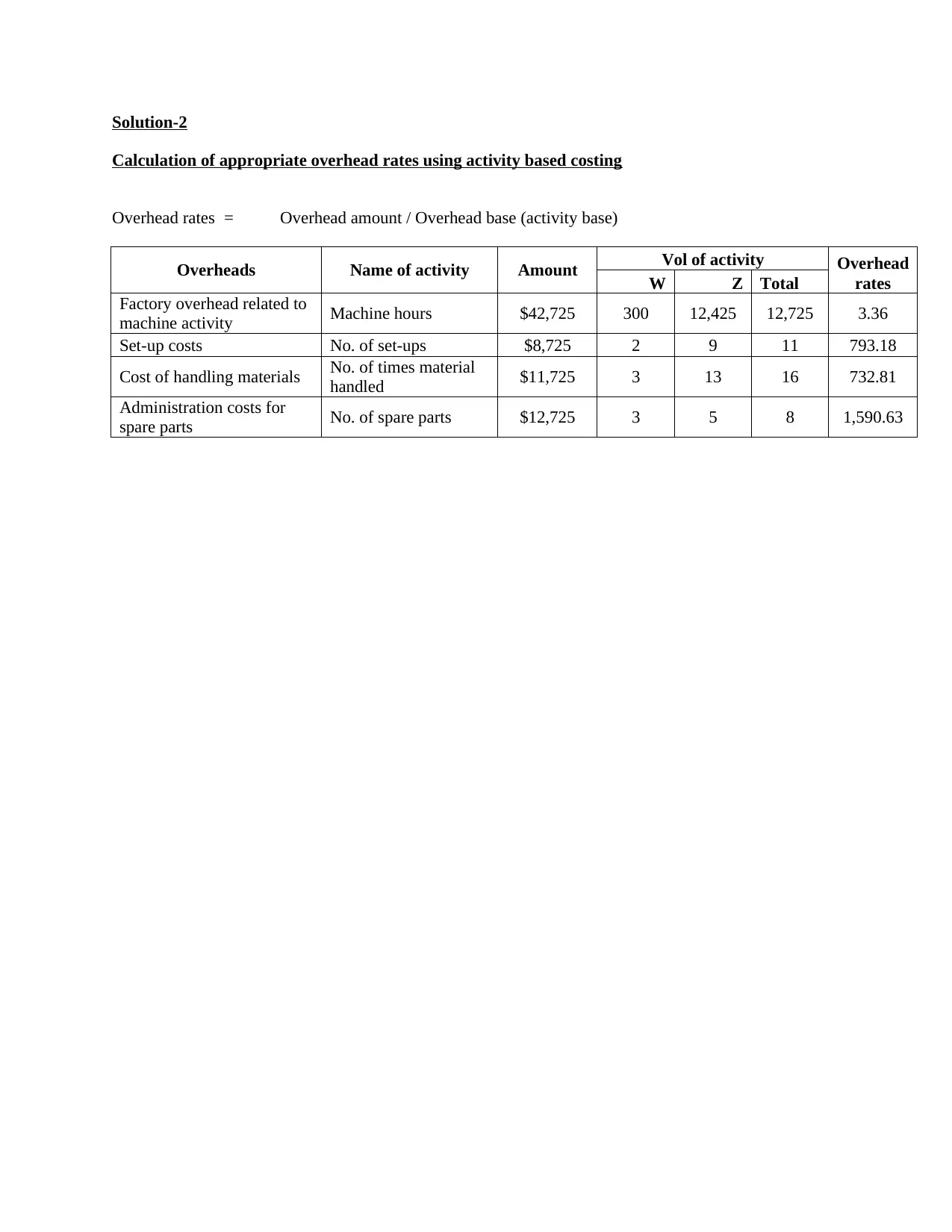

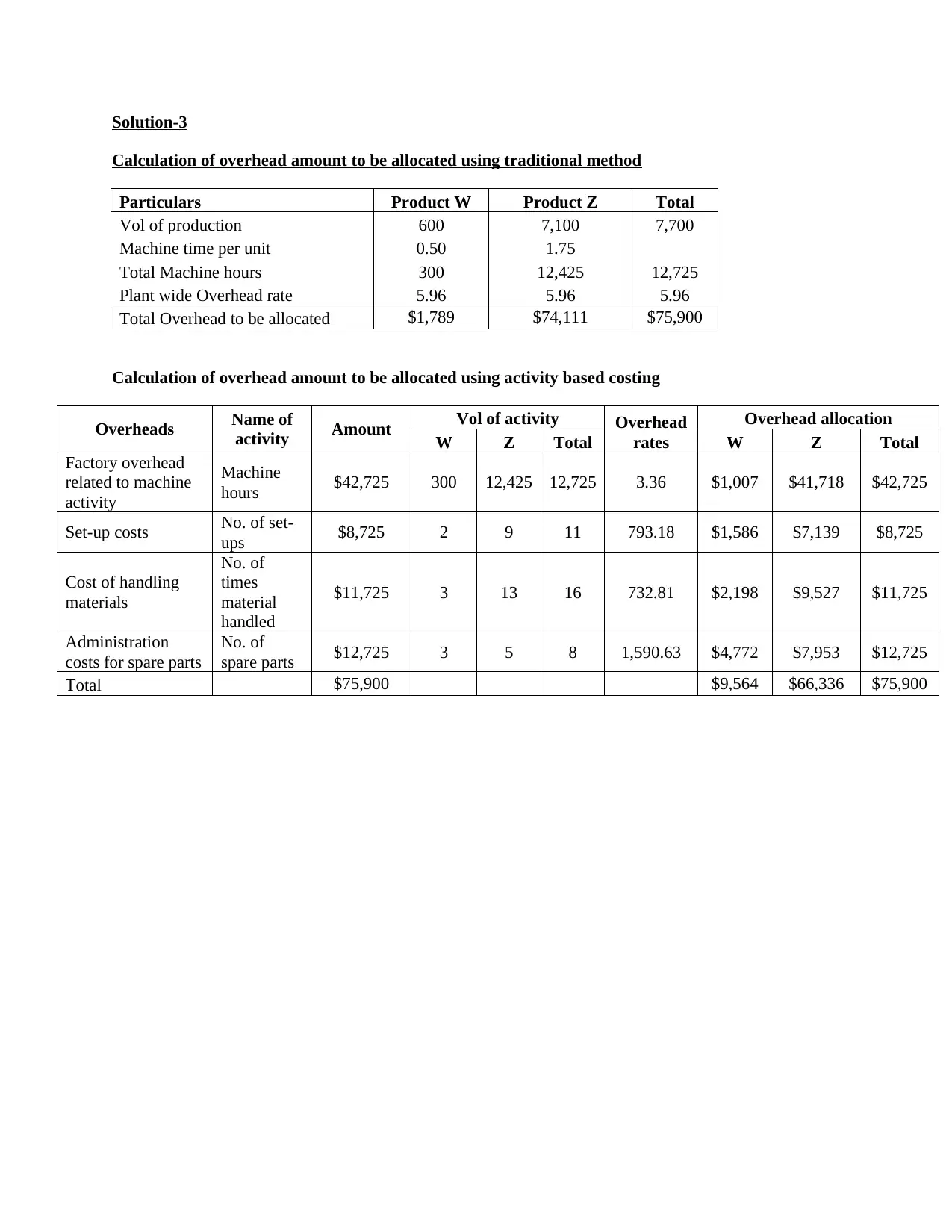

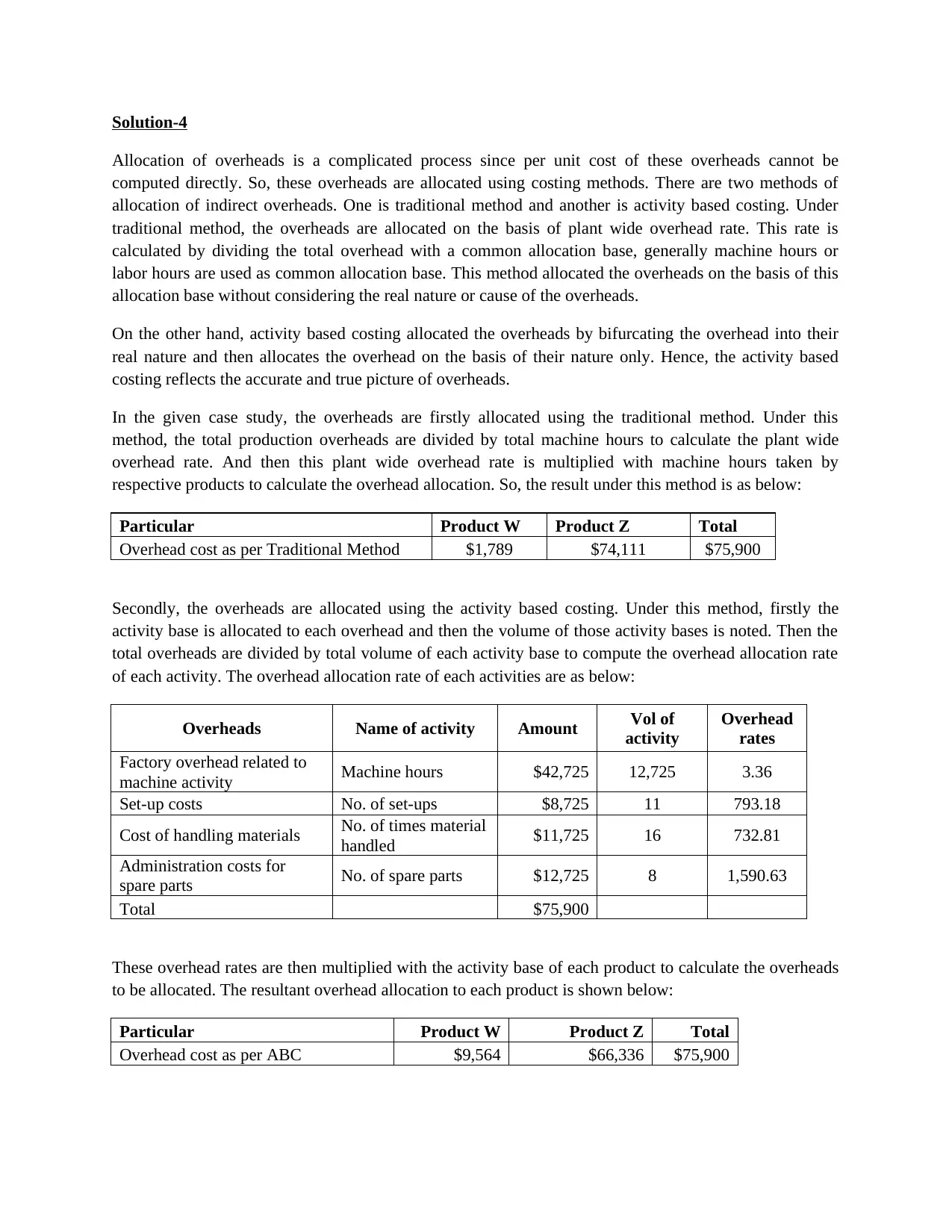

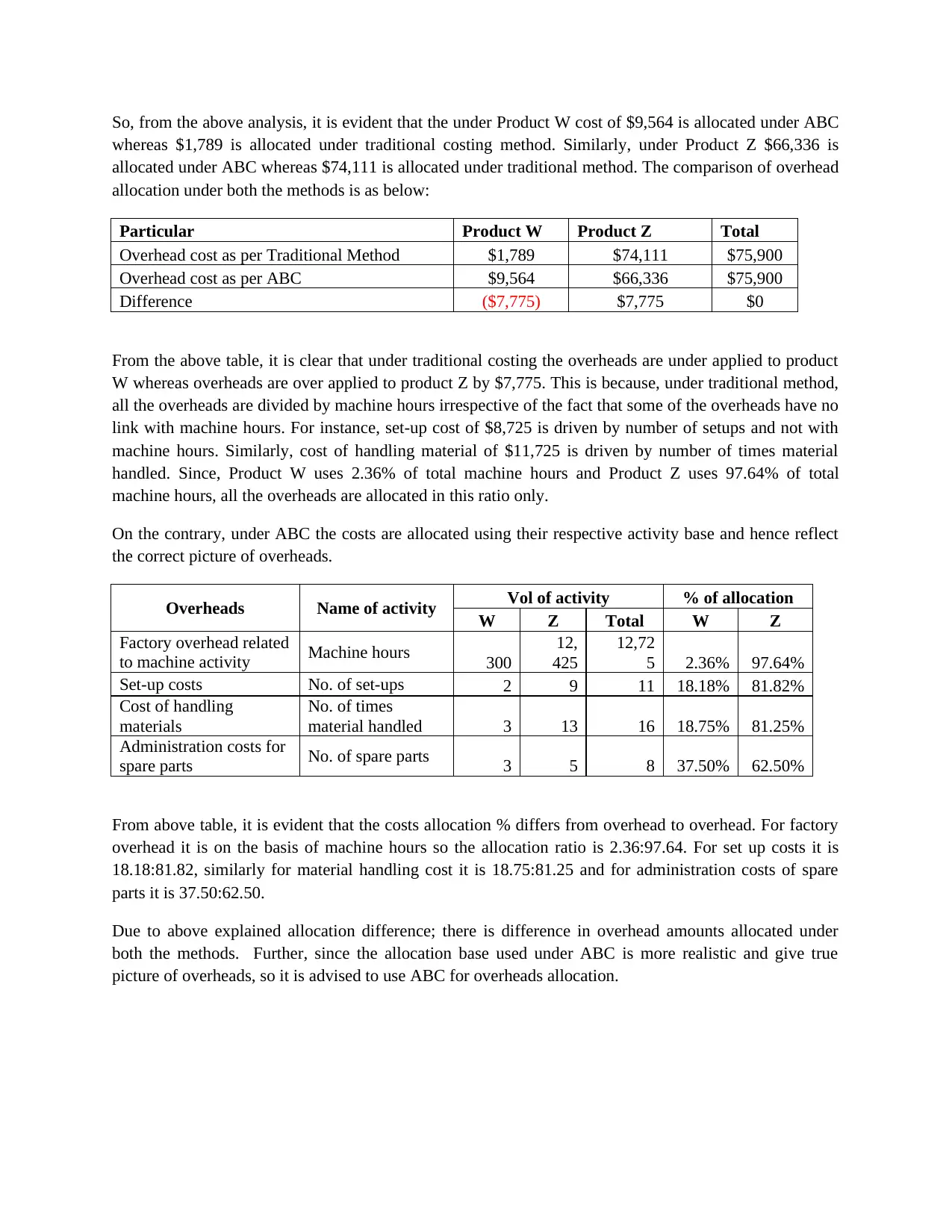

This report analyzes Petral Ltd's overhead allocation using both traditional and activity-based costing (ABC) methods. The traditional method calculates a plant-wide overhead rate based on total machine hours, while ABC allocates overheads based on specific activities and their respective drivers. The analysis reveals significant differences in overhead allocation between the two methods, particularly for Products W and Z. Under the traditional method, overheads are under-applied to Product W and over-applied to Product Z. ABC provides a more accurate picture of overhead costs by considering the specific activities that drive those costs, such as machine hours, set-up costs, material handling, and spare parts administration. The report concludes that ABC is a more realistic and reliable method for overhead allocation, as it reflects the true nature of overhead costs and provides a more accurate cost picture for each product. Desklib provides access to solved assignments and study tools to help students understand these concepts better.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.