Management Accounting Costing and Budgeting

22 Pages4424 Words319 Views

Added on 2023-04-04

About This Document

This report discusses the concepts of management accounting, different types of costs and expenses, methods of cost segregation, inventory management, cost of goods sold, key performance indicators, and strategies to control costs and improve product quality. The case study focuses on Smart Looks Limited, a clothing company. The report provides insights into the company's financial data, cost analysis, budgeting methods, and inventory valuation techniques.

Management Accounting Costing and Budgeting

Added on 2023-04-04

ShareRelated Documents

MANAGEMENT

ACCOUNTING COSTING

AND BUDGETING

1

ACCOUNTING COSTING

AND BUDGETING

1

2

INTRODUCTION

The accounting process under which financial data are recorded, analysed and reviewed

by the managers of the company able to take internal business decisions is known as

management accounting. It considers in the business entity for manage the overall financials as

well as forecast for the upcoming times. In the current report Smart Looks Limited company is to

be taken into account for analsye and explain different concepts of the management accounting.

In this report, different kinds of costs are to be classified as per their criteria of segregation.

Different kinds of budgets like as sales, production, cash, overhead etc. are prepared and

reviewed here for the Smart Looks firm. In addition to this, at the current study there are

different kinds of budgeting methods such as zero based, flexible and fixed are to be explained

which supports to frame the budget statements. Moreover costs such as variable, fixed and semi

variable are analysed and after adding such all cost of total production and units expenses both

determined.

TASK 1

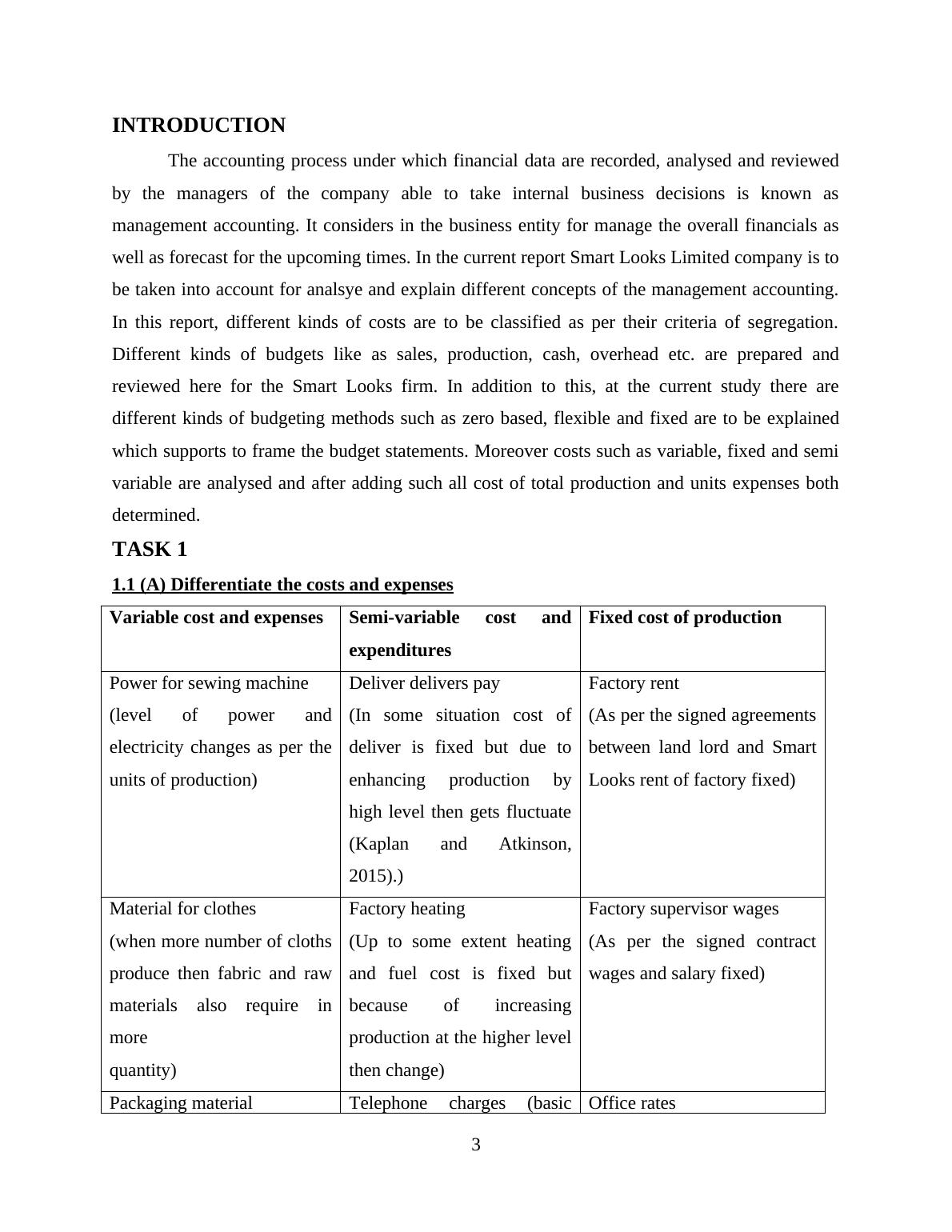

1.1 (A) Differentiate the costs and expenses

Variable cost and expenses Semi-variable cost and

expenditures

Fixed cost of production

Power for sewing machine

(level of power and

electricity changes as per the

units of production)

Deliver delivers pay

(In some situation cost of

deliver is fixed but due to

enhancing production by

high level then gets fluctuate

(Kaplan and Atkinson,

2015).)

Factory rent

(As per the signed agreements

between land lord and Smart

Looks rent of factory fixed)

Material for clothes

(when more number of cloths

produce then fabric and raw

materials also require in

more

quantity)

Factory heating

(Up to some extent heating

and fuel cost is fixed but

because of increasing

production at the higher level

then change)

Factory supervisor wages

(As per the signed contract

wages and salary fixed)

Packaging material Telephone charges (basic Office rates

3

The accounting process under which financial data are recorded, analysed and reviewed

by the managers of the company able to take internal business decisions is known as

management accounting. It considers in the business entity for manage the overall financials as

well as forecast for the upcoming times. In the current report Smart Looks Limited company is to

be taken into account for analsye and explain different concepts of the management accounting.

In this report, different kinds of costs are to be classified as per their criteria of segregation.

Different kinds of budgets like as sales, production, cash, overhead etc. are prepared and

reviewed here for the Smart Looks firm. In addition to this, at the current study there are

different kinds of budgeting methods such as zero based, flexible and fixed are to be explained

which supports to frame the budget statements. Moreover costs such as variable, fixed and semi

variable are analysed and after adding such all cost of total production and units expenses both

determined.

TASK 1

1.1 (A) Differentiate the costs and expenses

Variable cost and expenses Semi-variable cost and

expenditures

Fixed cost of production

Power for sewing machine

(level of power and

electricity changes as per the

units of production)

Deliver delivers pay

(In some situation cost of

deliver is fixed but due to

enhancing production by

high level then gets fluctuate

(Kaplan and Atkinson,

2015).)

Factory rent

(As per the signed agreements

between land lord and Smart

Looks rent of factory fixed)

Material for clothes

(when more number of cloths

produce then fabric and raw

materials also require in

more

quantity)

Factory heating

(Up to some extent heating

and fuel cost is fixed but

because of increasing

production at the higher level

then change)

Factory supervisor wages

(As per the signed contract

wages and salary fixed)

Packaging material Telephone charges (basic Office rates

3

(Higher the number of cloths

lead to increase costs of

packaging and fewer units

incur low cost of packaging

the products)

cost and bills of the

telephone are fixed for each

month but as higher and

lower consuming lead to

increase and decline

respectively (Islam and Hu,

2012).)

(It is not related to the

production level and due to

this it remains same and not

varied)

1.1 (B) Other methods to segregate costs of the production

In the above section there are costs are to be segregated in basically three concepts which

are such fixed, variable as well as semi-variable expenses. Apart from this all there are other

ways on the basis of total expenses associated in the Smart Looks Limited. Varieties of the other

costs as well as expenses on the basis of which number of expenditures are classified are like as

prime costs, opportunity costs, sunk costs, conversion expenses etc. Furthermore, by considering

the direct as well as indirect costs and overheads expenses also total costs are classified at the

workplace. In addition to this, among the overheads also there are different expense comes which

are such as manufacturing, fixed as well as variable overheads (Hammad, Jusoh and Yen Nee

Oon, 2010).

1.2 Calculating the total expenses along with the unit cost

At the current task there are different kinds and varieties of costs comes under the

production and manufacturing process. After adding all types of expenses the company able to

assess the total cost of products which are stitched and manufactured in the firm of Smart Looks

Limited. Further, after consider the total cost as well as level of outputs the managers able to

assess cost and expense of every unit. Moreover, total and unit expenditure of the firm are stated

as below:

4

lead to increase costs of

packaging and fewer units

incur low cost of packaging

the products)

cost and bills of the

telephone are fixed for each

month but as higher and

lower consuming lead to

increase and decline

respectively (Islam and Hu,

2012).)

(It is not related to the

production level and due to

this it remains same and not

varied)

1.1 (B) Other methods to segregate costs of the production

In the above section there are costs are to be segregated in basically three concepts which

are such fixed, variable as well as semi-variable expenses. Apart from this all there are other

ways on the basis of total expenses associated in the Smart Looks Limited. Varieties of the other

costs as well as expenses on the basis of which number of expenditures are classified are like as

prime costs, opportunity costs, sunk costs, conversion expenses etc. Furthermore, by considering

the direct as well as indirect costs and overheads expenses also total costs are classified at the

workplace. In addition to this, among the overheads also there are different expense comes which

are such as manufacturing, fixed as well as variable overheads (Hammad, Jusoh and Yen Nee

Oon, 2010).

1.2 Calculating the total expenses along with the unit cost

At the current task there are different kinds and varieties of costs comes under the

production and manufacturing process. After adding all types of expenses the company able to

assess the total cost of products which are stitched and manufactured in the firm of Smart Looks

Limited. Further, after consider the total cost as well as level of outputs the managers able to

assess cost and expense of every unit. Moreover, total and unit expenditure of the firm are stated

as below:

4

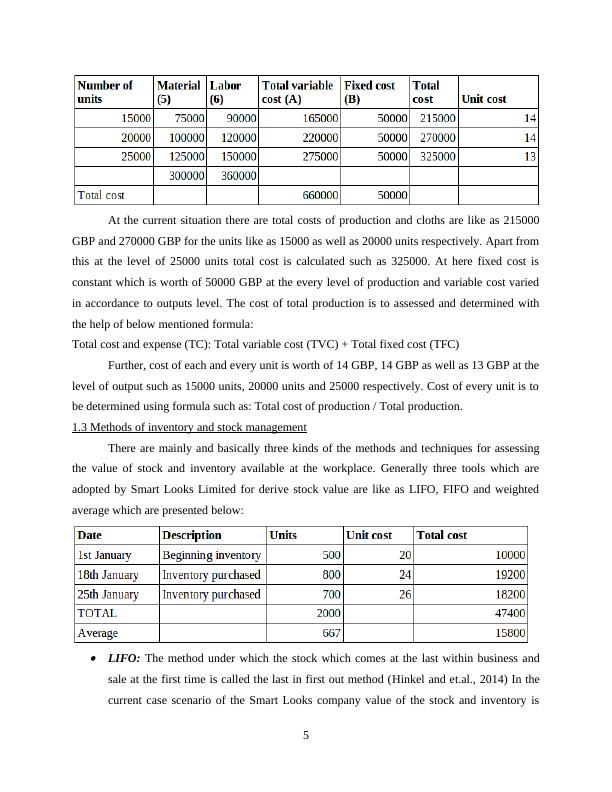

At the current situation there are total costs of production and cloths are like as 215000

GBP and 270000 GBP for the units like as 15000 as well as 20000 units respectively. Apart from

this at the level of 25000 units total cost is calculated such as 325000. At here fixed cost is

constant which is worth of 50000 GBP at the every level of production and variable cost varied

in accordance to outputs level. The cost of total production is to assessed and determined with

the help of below mentioned formula:

Total cost and expense (TC): Total variable cost (TVC) + Total fixed cost (TFC)

Further, cost of each and every unit is worth of 14 GBP, 14 GBP as well as 13 GBP at the

level of output such as 15000 units, 20000 units and 25000 respectively. Cost of every unit is to

be determined using formula such as: Total cost of production / Total production.

1.3 Methods of inventory and stock management

There are mainly and basically three kinds of the methods and techniques for assessing

the value of stock and inventory available at the workplace. Generally three tools which are

adopted by Smart Looks Limited for derive stock value are like as LIFO, FIFO and weighted

average which are presented below:

LIFO: The method under which the stock which comes at the last within business and

sale at the first time is called the last in first out method (Hinkel and et.al., 2014) In the

current case scenario of the Smart Looks company value of the stock and inventory is

5

GBP and 270000 GBP for the units like as 15000 as well as 20000 units respectively. Apart from

this at the level of 25000 units total cost is calculated such as 325000. At here fixed cost is

constant which is worth of 50000 GBP at the every level of production and variable cost varied

in accordance to outputs level. The cost of total production is to assessed and determined with

the help of below mentioned formula:

Total cost and expense (TC): Total variable cost (TVC) + Total fixed cost (TFC)

Further, cost of each and every unit is worth of 14 GBP, 14 GBP as well as 13 GBP at the

level of output such as 15000 units, 20000 units and 25000 respectively. Cost of every unit is to

be determined using formula such as: Total cost of production / Total production.

1.3 Methods of inventory and stock management

There are mainly and basically three kinds of the methods and techniques for assessing

the value of stock and inventory available at the workplace. Generally three tools which are

adopted by Smart Looks Limited for derive stock value are like as LIFO, FIFO and weighted

average which are presented below:

LIFO: The method under which the stock which comes at the last within business and

sale at the first time is called the last in first out method (Hinkel and et.al., 2014) In the

current case scenario of the Smart Looks company value of the stock and inventory is

5

worth of 10000 GBP as well as 19200 GBP which is for the units of 500 and 800

respectively. On the basis of current stock valuation technique the business able to

determine effectual and proper value and takes the business decisions in the proper way.

Further, old and higher inventory lead to reduce productivity and liquidity of the firm due

to which LIFO method is better. FIFO: Another method for valuing the level of inventory and stock is such as first in first

out under which beginning stock is to be sold at the earlier and preference to the new and

current inventory is to be given (Clinton and White, 2012). At this technique stock value

of the Smart Looks company is such as 18200 GBP which is lower as compare to above

mentioned method. Higher the value of stock is better and due to which cause the above

discussed method is more effectual. Apart from this, after adopting the existing stock

valuation way the company able cannot sale the old stock which lead to decrease its

efficiency for generating revenue in the textile industry.

Weighted Average: Combination as well as mixture of LIFO and FIFO both the methods

is known as weighted average technique where the firm can assess average value of the

overall stock (Eichfelder and Schorn, 2012). In the business entity Smart Looks average

value of the available stock comes worth of 15800 GBP which is lower from both the

tools. Hence, due to this overall stock valuation fall down this is not good for the firm as

compare to others. At this level of the stock value average production units are such as

667 units at the end of the financial year.

1.4 Analyse as well as interpret the costs using graphical representation

In the Smart Looks firm there are variable as well as fixed both kinds of costs associated

under stitching and producing cloths. After adding such both expenses total cost is to be

determined which shows and presented using the graphs stated below:

Total variable costs:

6

respectively. On the basis of current stock valuation technique the business able to

determine effectual and proper value and takes the business decisions in the proper way.

Further, old and higher inventory lead to reduce productivity and liquidity of the firm due

to which LIFO method is better. FIFO: Another method for valuing the level of inventory and stock is such as first in first

out under which beginning stock is to be sold at the earlier and preference to the new and

current inventory is to be given (Clinton and White, 2012). At this technique stock value

of the Smart Looks company is such as 18200 GBP which is lower as compare to above

mentioned method. Higher the value of stock is better and due to which cause the above

discussed method is more effectual. Apart from this, after adopting the existing stock

valuation way the company able cannot sale the old stock which lead to decrease its

efficiency for generating revenue in the textile industry.

Weighted Average: Combination as well as mixture of LIFO and FIFO both the methods

is known as weighted average technique where the firm can assess average value of the

overall stock (Eichfelder and Schorn, 2012). In the business entity Smart Looks average

value of the available stock comes worth of 15800 GBP which is lower from both the

tools. Hence, due to this overall stock valuation fall down this is not good for the firm as

compare to others. At this level of the stock value average production units are such as

667 units at the end of the financial year.

1.4 Analyse as well as interpret the costs using graphical representation

In the Smart Looks firm there are variable as well as fixed both kinds of costs associated

under stitching and producing cloths. After adding such both expenses total cost is to be

determined which shows and presented using the graphs stated below:

Total variable costs:

6

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Various Type of Costs of the Cited Firm | Assignmentlg...

|15

|3452

|96

Management Accounting Assignment tasklg...

|20

|4773

|101

Management Accounting Report For Smart Looks Limitedlg...

|18

|4938

|121

MANAGEMENT ACCOUNTING TABLE OF CONTENTS INTRODUCTION 5 Q1.5 a) Classification of cost 5 Q2.7 b) Analysis of inventory 7 Q3. Method 8lg...

|18

|3165

|106

MANAGEMENT ACCOUNTING AND COGS Reportlg...

|24

|5191

|500

Budget Statements of Smart Looks Limited- Reportlg...

|23

|4865

|64