Management Accounting Report: Cost Analysis for Smart Looks Ltd

VerifiedAdded on 2020/02/17

|23

|4865

|64

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Smart Looks Limited, a textile company. It begins by classifying costs based on various criteria, including fixed, variable, and semi-variable costs, and computes total and per-unit production costs. The report then explores different stock valuation methods (FIFO, LIFO, and weighted average) and their impact on the cost of goods sold. Key Performance Indicators (KPIs) are used to analyze business performance, and strategies for reducing expenses and enhancing quality are discussed. The report further delves into budgeting, including different techniques and budget statements, such as a cash budget. Finally, it applies marginal costing to determine selling prices and calculates estimated and actual margins, culminating in a report to the board of directors based on the budget.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Separation of expenses on the basis of different criteria..................................................1

1.2 Computation of total and per unit cost of production.......................................................2

1.3 Analysis of cost data.........................................................................................................3

1.4 Stock valuation methods for costing................................................................................5

1. FIFO...................................................................................................................................5

2. LIFO...................................................................................................................................5

3. Weighted Average Method.................................................................................................6

TASK 2............................................................................................................................................6

2.1 Report of COGS using three stock valuation methods.....................................................6

2.2 Use of KPI for analysing business performance..............................................................8

2.3 Strategies which are helpful for reduce expenses and enhance quality..........................10

TASK 3..........................................................................................................................................10

3.1 Budget and its importance for Smart Looks Limited.....................................................10

3.2 Different techniques for preparing budget.....................................................................11

3.3 Various budget statements for Smart Looks Limited.....................................................12

3.4 Cash budget for chosen firm...........................................................................................14

TASK 4..........................................................................................................................................15

4.1 and 4.2 Use of marginal costing method to compute selling price and Calculating

estimated as well as actual margin.......................................................................................15

4.3 Report to board of directors on the basis of budget........................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Separation of expenses on the basis of different criteria..................................................1

1.2 Computation of total and per unit cost of production.......................................................2

1.3 Analysis of cost data.........................................................................................................3

1.4 Stock valuation methods for costing................................................................................5

1. FIFO...................................................................................................................................5

2. LIFO...................................................................................................................................5

3. Weighted Average Method.................................................................................................6

TASK 2............................................................................................................................................6

2.1 Report of COGS using three stock valuation methods.....................................................6

2.2 Use of KPI for analysing business performance..............................................................8

2.3 Strategies which are helpful for reduce expenses and enhance quality..........................10

TASK 3..........................................................................................................................................10

3.1 Budget and its importance for Smart Looks Limited.....................................................10

3.2 Different techniques for preparing budget.....................................................................11

3.3 Various budget statements for Smart Looks Limited.....................................................12

3.4 Cash budget for chosen firm...........................................................................................14

TASK 4..........................................................................................................................................15

4.1 and 4.2 Use of marginal costing method to compute selling price and Calculating

estimated as well as actual margin.......................................................................................15

4.3 Report to board of directors on the basis of budget........................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................20

INTRODUCTION

In the firm management plays an integral role whether it is related to financial or non

financial aspects. By using different management techniques the company able to achieve its

various numbers of goals and objectives in very effectual and smooth way. In the current study

there is Smart Looks Limited firm is selected which operates and run its business in the textile

industry. It produces and prepare cloths and garments for the retail stores and shops. The present

study describes about the different criteria of costing which helps to segregate number of

expenses. It shows about the budget and its significant in the firm for estimating future data and

taking highly effectual business decisions. On the basis of current report, the reader is able to

know different budget statements of Smart Looks Limited.

TASK 1

1.1 Separation of expenses on the basis of different criteria

Fixed cost Variable costs Semi-variable costs

Factory rent Material for cloths Factory supervisor's wages

Office rates Power for sewing machinery Telephone

Factory heating Packaging material Delivery drivers pay

Fixed costs- Cost incurred in an entity which is unaffected with the changes in the sales units of

an entity as this will not increase or decreases with the time (Bowling, 2014). Fixed costs is

always remained constant throughout the making of product as it is occurred in the business.

Variable costs- This cost is fluctuating in nature as this gets changed with a minute changes

takes places in the overall sales unit of an entity like smart Looks Ltd. It has parallel relationship

between sales unit of an entity and the variable cost incurred. Material cost is variable costs

which gets changes with various sales units included in the business.

Semi-variable costs- It is that kind of costs which has both characteristics of variable and fixed

nature of costs in order to give the status of semi-variable costs in the business enterprise.

Delivery dealer's pay comes under this particular category as fixed amount of dealer's rates along

with changes takes places in the future in the rates. Factory bill fall under this stream in which

amount is fixed but the units used by the firm will increases the utility bill of the factory.

1

In the firm management plays an integral role whether it is related to financial or non

financial aspects. By using different management techniques the company able to achieve its

various numbers of goals and objectives in very effectual and smooth way. In the current study

there is Smart Looks Limited firm is selected which operates and run its business in the textile

industry. It produces and prepare cloths and garments for the retail stores and shops. The present

study describes about the different criteria of costing which helps to segregate number of

expenses. It shows about the budget and its significant in the firm for estimating future data and

taking highly effectual business decisions. On the basis of current report, the reader is able to

know different budget statements of Smart Looks Limited.

TASK 1

1.1 Separation of expenses on the basis of different criteria

Fixed cost Variable costs Semi-variable costs

Factory rent Material for cloths Factory supervisor's wages

Office rates Power for sewing machinery Telephone

Factory heating Packaging material Delivery drivers pay

Fixed costs- Cost incurred in an entity which is unaffected with the changes in the sales units of

an entity as this will not increase or decreases with the time (Bowling, 2014). Fixed costs is

always remained constant throughout the making of product as it is occurred in the business.

Variable costs- This cost is fluctuating in nature as this gets changed with a minute changes

takes places in the overall sales unit of an entity like smart Looks Ltd. It has parallel relationship

between sales unit of an entity and the variable cost incurred. Material cost is variable costs

which gets changes with various sales units included in the business.

Semi-variable costs- It is that kind of costs which has both characteristics of variable and fixed

nature of costs in order to give the status of semi-variable costs in the business enterprise.

Delivery dealer's pay comes under this particular category as fixed amount of dealer's rates along

with changes takes places in the future in the rates. Factory bill fall under this stream in which

amount is fixed but the units used by the firm will increases the utility bill of the factory.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Other ways to classify costs

Direct costs- It is regarded as that type of costs which is directly attributable to a product as this

costs is included in the making of a product. For example raw material required for

manufacturing different products.

Indirect costs- Costs spend by an individual are indirectly related to a specific product will

contribute indirectly in a product. For instance, maintenance costs incurred in an entity such as

oiling and lubricating used in improving the current conditions of machines. Indirect costs will

include maintenance of oil which helps in boosting the current machinery in order to generate

higher outcomes in the near future as this is beneficial for an enterprise.

Opportunity costs- It is that type of costs incurred in an entity which states that one alternative

sacrificed for taking the next best alternative in an enterprise It is incurred in the firm which is

incurred in a firm where an entity owner sacrificed one cost for next best alternative are regarded

as the opportunity costs for the business.

1.2 Computation of total and per unit cost of production

In the total cost those all the expenses used and added which incur in the firm in direct or

indirect manner. Furthermore, unit cost helps to the firm to analyse that for producing each cloth

how many expenses are comes into consideration. On the basis of various expenses total and unit

cost computed as below:

2

Direct costs- It is regarded as that type of costs which is directly attributable to a product as this

costs is included in the making of a product. For example raw material required for

manufacturing different products.

Indirect costs- Costs spend by an individual are indirectly related to a specific product will

contribute indirectly in a product. For instance, maintenance costs incurred in an entity such as

oiling and lubricating used in improving the current conditions of machines. Indirect costs will

include maintenance of oil which helps in boosting the current machinery in order to generate

higher outcomes in the near future as this is beneficial for an enterprise.

Opportunity costs- It is that type of costs incurred in an entity which states that one alternative

sacrificed for taking the next best alternative in an enterprise It is incurred in the firm which is

incurred in a firm where an entity owner sacrificed one cost for next best alternative are regarded

as the opportunity costs for the business.

1.2 Computation of total and per unit cost of production

In the total cost those all the expenses used and added which incur in the firm in direct or

indirect manner. Furthermore, unit cost helps to the firm to analyse that for producing each cloth

how many expenses are comes into consideration. On the basis of various expenses total and unit

cost computed as below:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

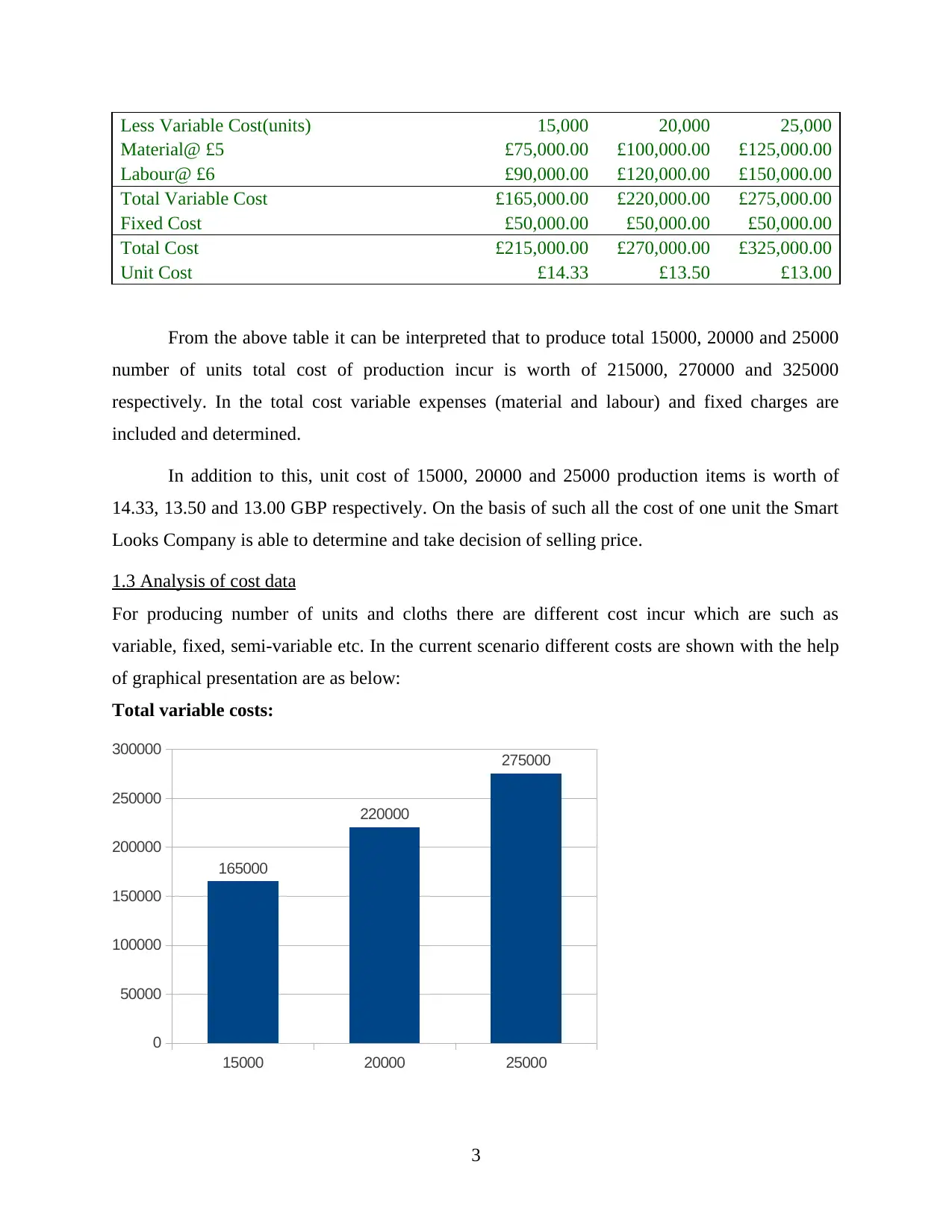

Less Variable Cost(units) 15,000 20,000 25,000

Material@ £5 £75,000.00 £100,000.00 £125,000.00

Labour@ £6 £90,000.00 £120,000.00 £150,000.00

Total Variable Cost £165,000.00 £220,000.00 £275,000.00

Fixed Cost £50,000.00 £50,000.00 £50,000.00

Total Cost £215,000.00 £270,000.00 £325,000.00

Unit Cost £14.33 £13.50 £13.00

From the above table it can be interpreted that to produce total 15000, 20000 and 25000

number of units total cost of production incur is worth of 215000, 270000 and 325000

respectively. In the total cost variable expenses (material and labour) and fixed charges are

included and determined.

In addition to this, unit cost of 15000, 20000 and 25000 production items is worth of

14.33, 13.50 and 13.00 GBP respectively. On the basis of such all the cost of one unit the Smart

Looks Company is able to determine and take decision of selling price.

1.3 Analysis of cost data

For producing number of units and cloths there are different cost incur which are such as

variable, fixed, semi-variable etc. In the current scenario different costs are shown with the help

of graphical presentation are as below:

Total variable costs:

15000 20000 25000

0

50000

100000

150000

200000

250000

300000

165000

220000

275000

3

Material@ £5 £75,000.00 £100,000.00 £125,000.00

Labour@ £6 £90,000.00 £120,000.00 £150,000.00

Total Variable Cost £165,000.00 £220,000.00 £275,000.00

Fixed Cost £50,000.00 £50,000.00 £50,000.00

Total Cost £215,000.00 £270,000.00 £325,000.00

Unit Cost £14.33 £13.50 £13.00

From the above table it can be interpreted that to produce total 15000, 20000 and 25000

number of units total cost of production incur is worth of 215000, 270000 and 325000

respectively. In the total cost variable expenses (material and labour) and fixed charges are

included and determined.

In addition to this, unit cost of 15000, 20000 and 25000 production items is worth of

14.33, 13.50 and 13.00 GBP respectively. On the basis of such all the cost of one unit the Smart

Looks Company is able to determine and take decision of selling price.

1.3 Analysis of cost data

For producing number of units and cloths there are different cost incur which are such as

variable, fixed, semi-variable etc. In the current scenario different costs are shown with the help

of graphical presentation are as below:

Total variable costs:

15000 20000 25000

0

50000

100000

150000

200000

250000

300000

165000

220000

275000

3

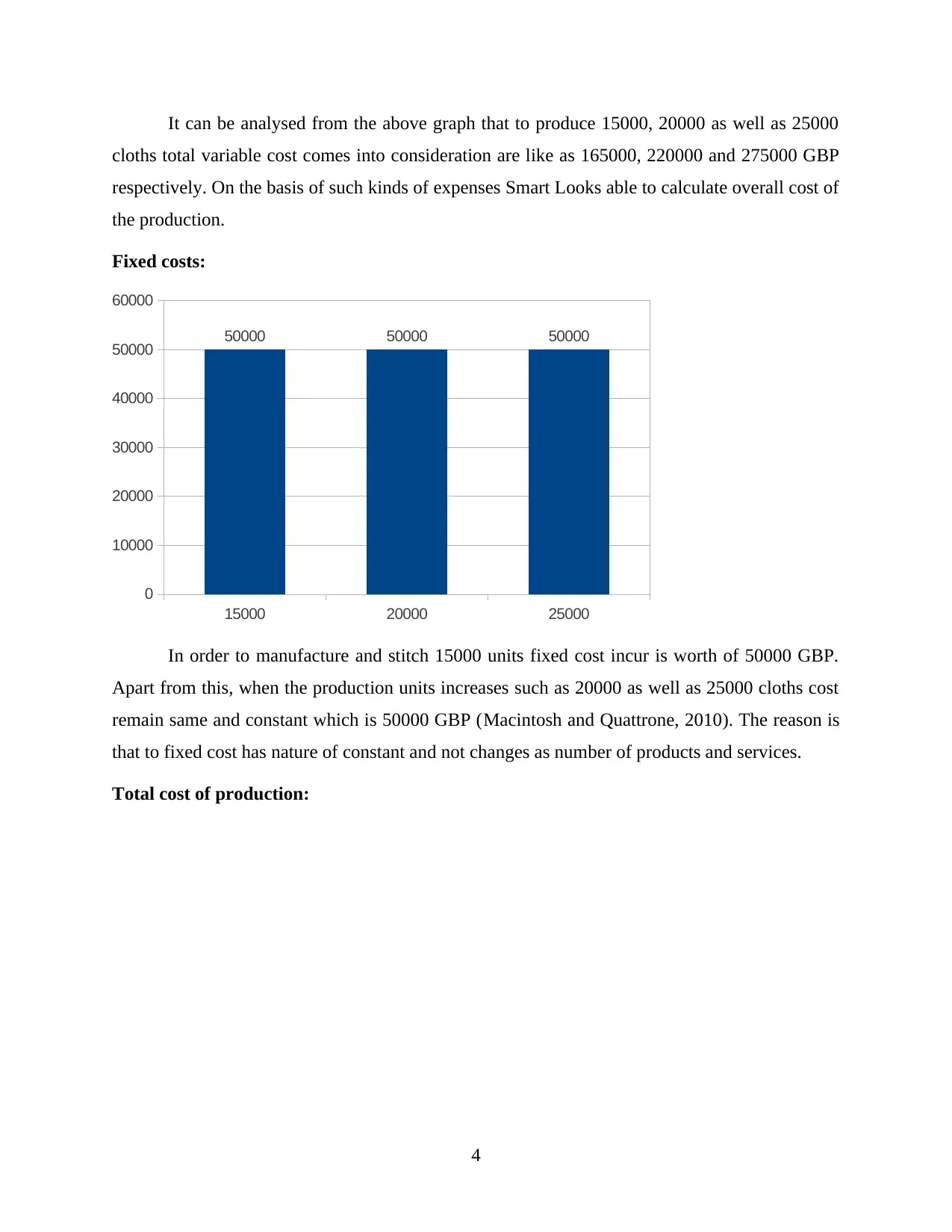

It can be analysed from the above graph that to produce 15000, 20000 as well as 25000

cloths total variable cost comes into consideration are like as 165000, 220000 and 275000 GBP

respectively. On the basis of such kinds of expenses Smart Looks able to calculate overall cost of

the production.

Fixed costs:

15000 20000 25000

0

10000

20000

30000

40000

50000

60000

50000 50000 50000

In order to manufacture and stitch 15000 units fixed cost incur is worth of 50000 GBP.

Apart from this, when the production units increases such as 20000 as well as 25000 cloths cost

remain same and constant which is 50000 GBP (Macintosh and Quattrone, 2010). The reason is

that to fixed cost has nature of constant and not changes as number of products and services.

Total cost of production:

4

cloths total variable cost comes into consideration are like as 165000, 220000 and 275000 GBP

respectively. On the basis of such kinds of expenses Smart Looks able to calculate overall cost of

the production.

Fixed costs:

15000 20000 25000

0

10000

20000

30000

40000

50000

60000

50000 50000 50000

In order to manufacture and stitch 15000 units fixed cost incur is worth of 50000 GBP.

Apart from this, when the production units increases such as 20000 as well as 25000 cloths cost

remain same and constant which is 50000 GBP (Macintosh and Quattrone, 2010). The reason is

that to fixed cost has nature of constant and not changes as number of products and services.

Total cost of production:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15000 20000 25000

0

50000

100000

150000

200000

250000

300000

350000

215000

270000

325000

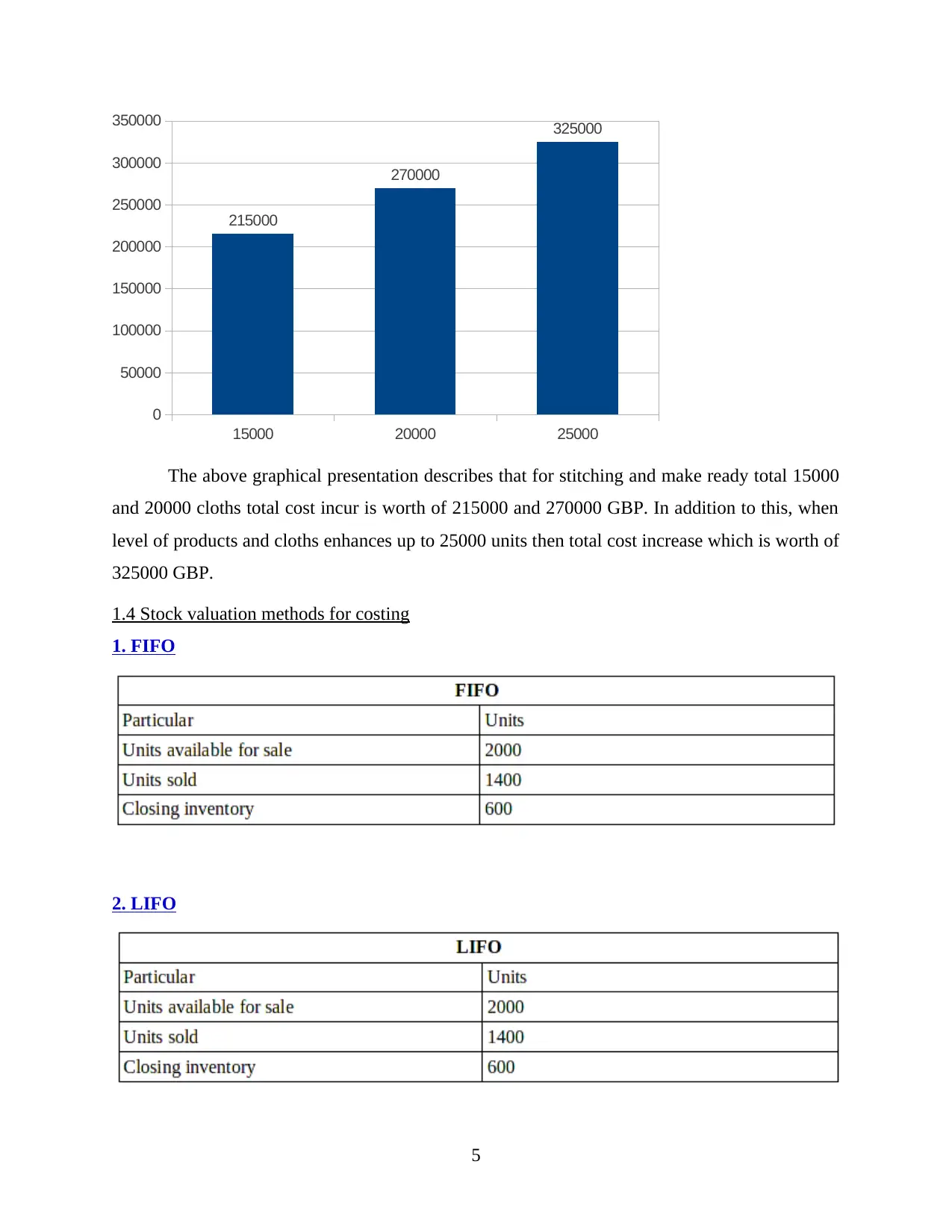

The above graphical presentation describes that for stitching and make ready total 15000

and 20000 cloths total cost incur is worth of 215000 and 270000 GBP. In addition to this, when

level of products and cloths enhances up to 25000 units then total cost increase which is worth of

325000 GBP.

1.4 Stock valuation methods for costing

1. FIFO

2. LIFO

5

0

50000

100000

150000

200000

250000

300000

350000

215000

270000

325000

The above graphical presentation describes that for stitching and make ready total 15000

and 20000 cloths total cost incur is worth of 215000 and 270000 GBP. In addition to this, when

level of products and cloths enhances up to 25000 units then total cost increase which is worth of

325000 GBP.

1.4 Stock valuation methods for costing

1. FIFO

2. LIFO

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Weighted Average Method

TASK 2

2.1 Report of COGS using three stock valuation methods

6

TASK 2

2.1 Report of COGS using three stock valuation methods

6

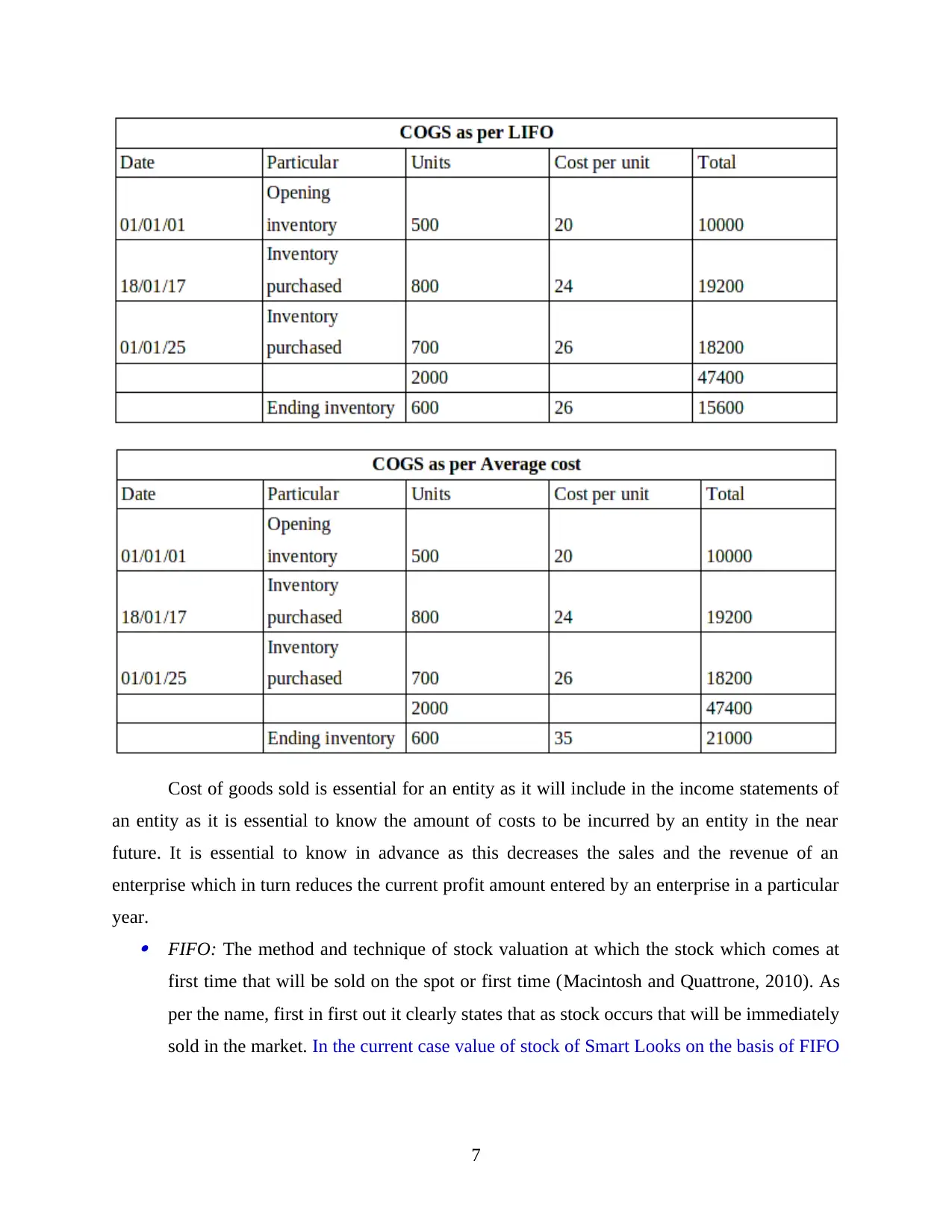

Cost of goods sold is essential for an entity as it will include in the income statements of

an entity as it is essential to know the amount of costs to be incurred by an entity in the near

future. It is essential to know in advance as this decreases the sales and the revenue of an

enterprise which in turn reduces the current profit amount entered by an enterprise in a particular

year. FIFO: The method and technique of stock valuation at which the stock which comes at

first time that will be sold on the spot or first time (Macintosh and Quattrone, 2010). As

per the name, first in first out it clearly states that as stock occurs that will be immediately

sold in the market. In the current case value of stock of Smart Looks on the basis of FIFO

7

an entity as it is essential to know the amount of costs to be incurred by an entity in the near

future. It is essential to know in advance as this decreases the sales and the revenue of an

enterprise which in turn reduces the current profit amount entered by an enterprise in a particular

year. FIFO: The method and technique of stock valuation at which the stock which comes at

first time that will be sold on the spot or first time (Macintosh and Quattrone, 2010). As

per the name, first in first out it clearly states that as stock occurs that will be immediately

sold in the market. In the current case value of stock of Smart Looks on the basis of FIFO

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is worth of 12000 GBP at which production and unit cost is such as 500, 800, 700 units

and 20, 24, 26 GBP respectively. LIFO: The other technique of stock valuation is last in first out at where the firm sell

those inventory which is comes at last time. Due to this nature most of the companies are

not using he method because of not giving clear and actual value of the whole inventory.

In the current scenarios on the basis of LIFO method value of overall stock is worth of

15600 GBP.

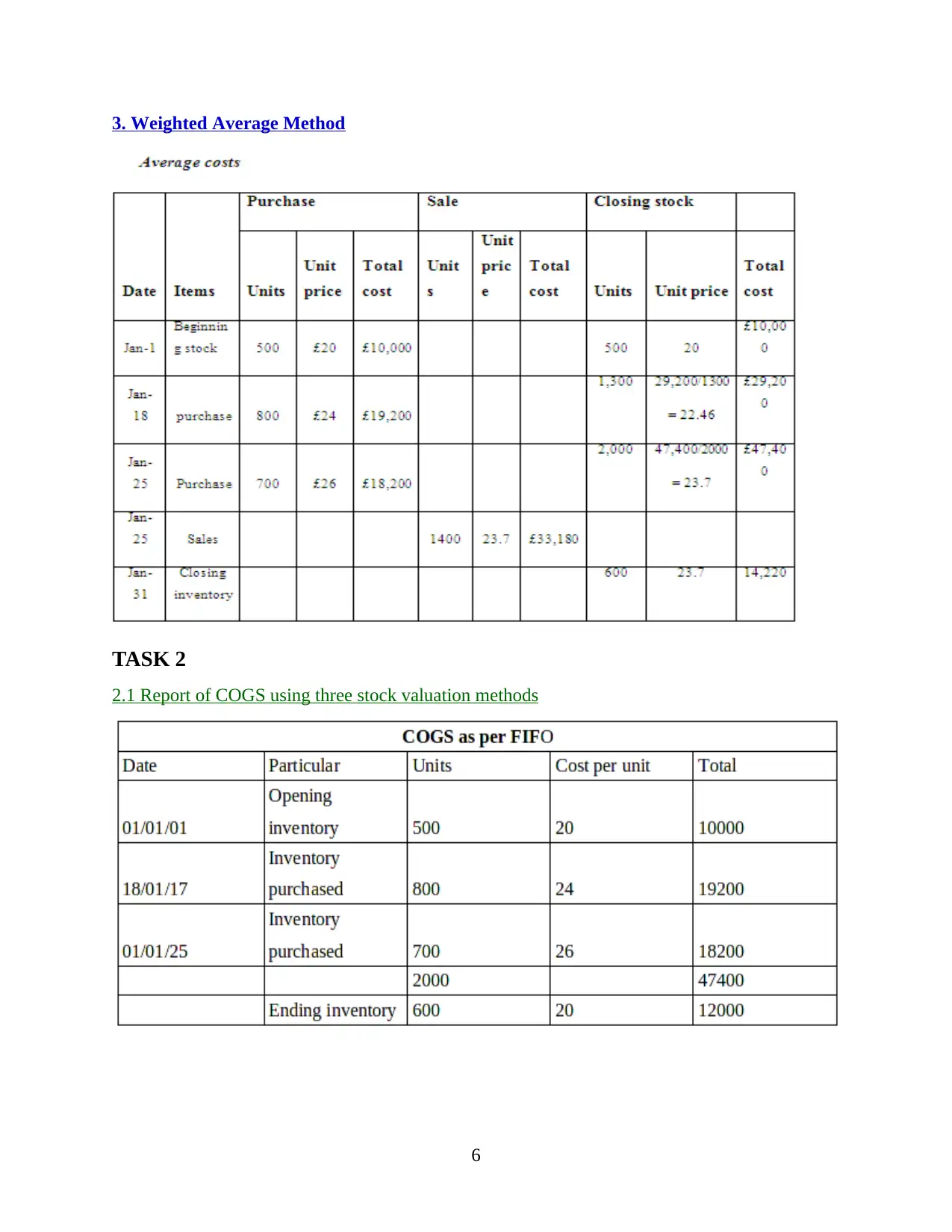

Weighted average method: According to the respective method of stock valuation the

company determine average value which is helpful to take better decisions. From the

above table it can be assessed that average stock value of Smart Looks Limited is 21000

GBP where ending stock level is such as 600 units. Stock of the ending is 600 units only

because among total 2000 units of production there are 1400 sold up the year end.

2.2 Use of KPI for analysing business performance

When the company and firm going to analyse that in which direction and trend its

business is performing there are different ways and indicators used by it. On the basis of various

types of key performance indicators the management able to assess that firm has increasing trend

or decreasing in the overall industry where it operating. The KPIs are such as quality, balanced

scorecard, satisfaction level of users, benchmarking etc. Apart from this, on the basis of different

kinds of financial informations the Smart Looks able to assess it business performance which are

such as variance analysis, cost, profit level etc (Kaplan and Atkinson, 2015). In the firm when

profitability ratios increases consistently then it can be said that firm is able to attract more

number of buyers and generate higher profit. By using quality aspect, when there are quality of

the cloths and products is better and higher as compare to previous year then it can be clearly

said that Smart Looks is performing well. In addition to this, the balanced scorecard is one of the

effectual tool because it helps to analyse performance in terms of four aspects which are such as

customer, internal business process, financial as well as learning and growth.

Customer Experience- The success factor such as customer experience helps to know that

whether business performance of Smart Looks is better and in the profitable ways or not. If it

able to provide higher quality of the cloths and products as compare to previous year then it can

be clearly said that Smart Looks is performing well and customers having more interest towards

8

and 20, 24, 26 GBP respectively. LIFO: The other technique of stock valuation is last in first out at where the firm sell

those inventory which is comes at last time. Due to this nature most of the companies are

not using he method because of not giving clear and actual value of the whole inventory.

In the current scenarios on the basis of LIFO method value of overall stock is worth of

15600 GBP.

Weighted average method: According to the respective method of stock valuation the

company determine average value which is helpful to take better decisions. From the

above table it can be assessed that average stock value of Smart Looks Limited is 21000

GBP where ending stock level is such as 600 units. Stock of the ending is 600 units only

because among total 2000 units of production there are 1400 sold up the year end.

2.2 Use of KPI for analysing business performance

When the company and firm going to analyse that in which direction and trend its

business is performing there are different ways and indicators used by it. On the basis of various

types of key performance indicators the management able to assess that firm has increasing trend

or decreasing in the overall industry where it operating. The KPIs are such as quality, balanced

scorecard, satisfaction level of users, benchmarking etc. Apart from this, on the basis of different

kinds of financial informations the Smart Looks able to assess it business performance which are

such as variance analysis, cost, profit level etc (Kaplan and Atkinson, 2015). In the firm when

profitability ratios increases consistently then it can be said that firm is able to attract more

number of buyers and generate higher profit. By using quality aspect, when there are quality of

the cloths and products is better and higher as compare to previous year then it can be clearly

said that Smart Looks is performing well. In addition to this, the balanced scorecard is one of the

effectual tool because it helps to analyse performance in terms of four aspects which are such as

customer, internal business process, financial as well as learning and growth.

Customer Experience- The success factor such as customer experience helps to know that

whether business performance of Smart Looks is better and in the profitable ways or not. If it

able to provide higher quality of the cloths and products as compare to previous year then it can

be clearly said that Smart Looks is performing well and customers having more interest towards

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

it. Apart from this, if the potential and new customer's level of loyalty raise towards the Smart

Looks entity improve then assessed that it performs well. The two critical success factors under

the customer experience are like as increasing satisfaction level of consumers along with the

quality of product. Moreover, the key performance indicators are such as sales and turnover of

the Smart Looks. If these both the factors improve then management determine that company

growing and performing well in the industry.

Suppliers and products quality- In this if the suppliers provide higher and the bets quality of

products as well as services to the Smart Looks then able to perform well in the industry of

cloths and garments. Here on the basis of quality of raw materials provided by suppliers business

performance is to be measured in the better ways. CSFs are such as improve quality of the cloth

and garments as well as attract more number of suppliers. The KPIs in the suppliers and quality

aspect are such as attract more of customers and increase the revenue with the help of higher

quality of cloths.

Operational efficiency- Apart from this, another critical success factors is like as operational

efficiency where it has been measured that for producing and manufacturing cloths management

is up to which extent producing as well as efficient. Higher the level and extent of productivity

and efficiency of the operational department lead to improve the business performance of Smart

Looks Limited. Improve the production process and reduce number of the damage products

which are the critical success factors. Furthermore, the performance will be measure in form of

declining the total production cost and enhance the efficiency of individuals and production

employees.

Reducing maintenance spending- In order to reach up to goals and become success the

management needs to reduce and decrease the level of costs which comes under the maintenance

of various equipments and other associated things. Lower the maintenance charges helps to

Smart Looks for enhancing level of success and business performance both. Mainly two kinds of

the CSFs in this current element are such as optimum utilisation of production equipments by

reducing extra load on them and eliminate damaged products. In addition to this, key

performance indicators at there are like as increase the production level using same quantity of

raw fabrics and increase quality of the products by eliminating the damaged items.

9

Looks entity improve then assessed that it performs well. The two critical success factors under

the customer experience are like as increasing satisfaction level of consumers along with the

quality of product. Moreover, the key performance indicators are such as sales and turnover of

the Smart Looks. If these both the factors improve then management determine that company

growing and performing well in the industry.

Suppliers and products quality- In this if the suppliers provide higher and the bets quality of

products as well as services to the Smart Looks then able to perform well in the industry of

cloths and garments. Here on the basis of quality of raw materials provided by suppliers business

performance is to be measured in the better ways. CSFs are such as improve quality of the cloth

and garments as well as attract more number of suppliers. The KPIs in the suppliers and quality

aspect are such as attract more of customers and increase the revenue with the help of higher

quality of cloths.

Operational efficiency- Apart from this, another critical success factors is like as operational

efficiency where it has been measured that for producing and manufacturing cloths management

is up to which extent producing as well as efficient. Higher the level and extent of productivity

and efficiency of the operational department lead to improve the business performance of Smart

Looks Limited. Improve the production process and reduce number of the damage products

which are the critical success factors. Furthermore, the performance will be measure in form of

declining the total production cost and enhance the efficiency of individuals and production

employees.

Reducing maintenance spending- In order to reach up to goals and become success the

management needs to reduce and decrease the level of costs which comes under the maintenance

of various equipments and other associated things. Lower the maintenance charges helps to

Smart Looks for enhancing level of success and business performance both. Mainly two kinds of

the CSFs in this current element are such as optimum utilisation of production equipments by

reducing extra load on them and eliminate damaged products. In addition to this, key

performance indicators at there are like as increase the production level using same quantity of

raw fabrics and increase quality of the products by eliminating the damaged items.

9

Cost reduction and profitability increase- Decreasing the costs and different number of

expenses helps to the management in order to become success because lower the costs lead to

improve the profitability in the industry. The critical success factors by which respective aspect

will be achieve are like as use the strategies for controlling over expenses and marketing cloths

for attracting higher consumers. Apart from this, KPIs to measure such factors are such as extent

of total cost of production and revenue generation.

2.3 Strategies which are helpful for reduce expenses and enhance quality

In the firm level of expenses are sometimes increases and at that position it is necessary

to reduce it. In addition to this, to improve level of quality is also one of the important aspect for

firm which helps to enhance consumer's attraction and generate more sales and profit. By using

cost management and risk management strategies Smart Looks able to reduce those costs which

are incurred in production and hamper profitability ratios (Islam and Hu, 2012). To improve

quality of the products and cloths effective strategies are like as use of innovative techniques, six

sigma, total quality management, lean production etc. By using and applying such kinds of

techniques and strategies Smart Looks Limited able to determine wastage products and eliminate

them from operation process. Along with this with the help of new and innovative techniques the

management able to make the production process effective by which cost reduce and quality

become highly better. The six sigma is also one of the best method for enhancing the production

quality by which cost ultimately reduces. When the manager of Smart Looks Limited apply the

six sigma then level or proportion of defective products will be comes up to 0.06% behind total

10000 units.

TASK 3

3.1 Budget and its importance for Smart Looks Limited

The statement and account which highly helpful for the selected company to assess and

identify those informations which will be occur in current and further financial period. By using

budget the management can know future data in terms of different aspects like as sales, cost,

incomes, expenditures, profit etc. In the corporate world, most of the companies are use budget

for identify future performance of business (10 Benefits of Budgeting Your Money, 2013). It has

key importances for the company which are expressed as below:

10

expenses helps to the management in order to become success because lower the costs lead to

improve the profitability in the industry. The critical success factors by which respective aspect

will be achieve are like as use the strategies for controlling over expenses and marketing cloths

for attracting higher consumers. Apart from this, KPIs to measure such factors are such as extent

of total cost of production and revenue generation.

2.3 Strategies which are helpful for reduce expenses and enhance quality

In the firm level of expenses are sometimes increases and at that position it is necessary

to reduce it. In addition to this, to improve level of quality is also one of the important aspect for

firm which helps to enhance consumer's attraction and generate more sales and profit. By using

cost management and risk management strategies Smart Looks able to reduce those costs which

are incurred in production and hamper profitability ratios (Islam and Hu, 2012). To improve

quality of the products and cloths effective strategies are like as use of innovative techniques, six

sigma, total quality management, lean production etc. By using and applying such kinds of

techniques and strategies Smart Looks Limited able to determine wastage products and eliminate

them from operation process. Along with this with the help of new and innovative techniques the

management able to make the production process effective by which cost reduce and quality

become highly better. The six sigma is also one of the best method for enhancing the production

quality by which cost ultimately reduces. When the manager of Smart Looks Limited apply the

six sigma then level or proportion of defective products will be comes up to 0.06% behind total

10000 units.

TASK 3

3.1 Budget and its importance for Smart Looks Limited

The statement and account which highly helpful for the selected company to assess and

identify those informations which will be occur in current and further financial period. By using

budget the management can know future data in terms of different aspects like as sales, cost,

incomes, expenditures, profit etc. In the corporate world, most of the companies are use budget

for identify future performance of business (10 Benefits of Budgeting Your Money, 2013). It has

key importances for the company which are expressed as below:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.