Improving Cash Budget for CooperWorld

VerifiedAdded on 2021/04/17

|14

|3189

|23

AI Summary

This report aims to provide a comprehensive solution to CooperWorld's cash flow problems by implementing strategies such as making cash sales, reducing debtors' time, leasing equipment, and providing discounts on loans. By adopting these methods, CooperWorld can improve its cash budget, meet financial obligations easily, and contribute to a strong liquidity position.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RUNNING HEAD: PERFORMANCE MANAGEMENT

Budgeting

Budgeting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Performance management 1

Contents

Introduction...........................................................................................................................................2

Requirement 1.......................................................................................................................................2

Requirement 2.......................................................................................................................................5

Requirement 3.......................................................................................................................................6

Requirement 4.......................................................................................................................................6

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

Contents

Introduction...........................................................................................................................................2

Requirement 1.......................................................................................................................................2

Requirement 2.......................................................................................................................................5

Requirement 3.......................................................................................................................................6

Requirement 4.......................................................................................................................................6

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

Performance management 2

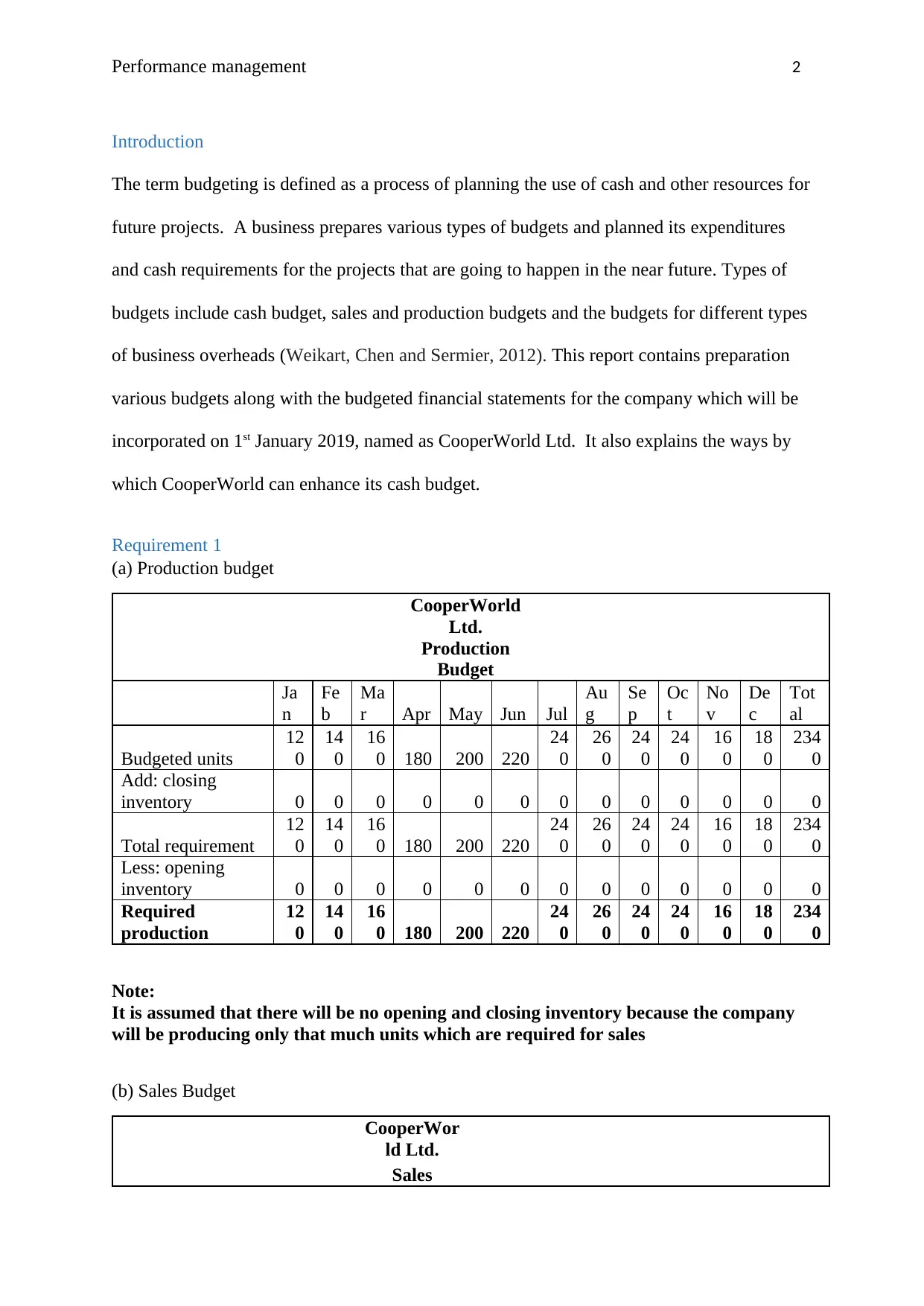

Introduction

The term budgeting is defined as a process of planning the use of cash and other resources for

future projects. A business prepares various types of budgets and planned its expenditures

and cash requirements for the projects that are going to happen in the near future. Types of

budgets include cash budget, sales and production budgets and the budgets for different types

of business overheads (Weikart, Chen and Sermier, 2012). This report contains preparation

various budgets along with the budgeted financial statements for the company which will be

incorporated on 1st January 2019, named as CooperWorld Ltd. It also explains the ways by

which CooperWorld can enhance its cash budget.

Requirement 1

(a) Production budget

CooperWorld

Ltd.

Production

Budget

Ja

n

Fe

b

Ma

r Apr May Jun Jul

Au

g

Se

p

Oc

t

No

v

De

c

Tot

al

Budgeted units

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Add: closing

inventory 0 0 0 0 0 0 0 0 0 0 0 0 0

Total requirement

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Less: opening

inventory 0 0 0 0 0 0 0 0 0 0 0 0 0

Required

production

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Note:

It is assumed that there will be no opening and closing inventory because the company

will be producing only that much units which are required for sales

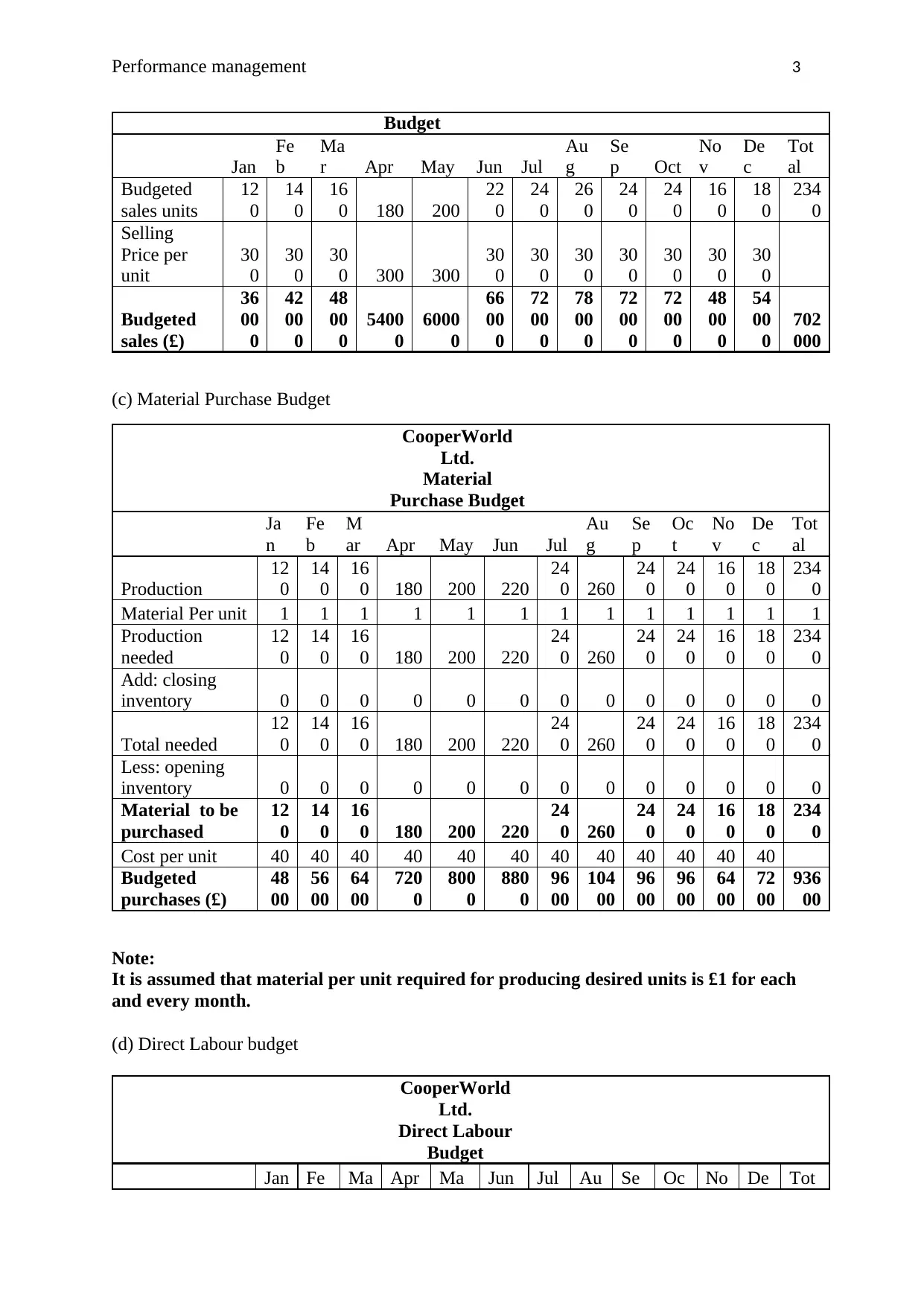

(b) Sales Budget

CooperWor

ld Ltd.

Sales

Introduction

The term budgeting is defined as a process of planning the use of cash and other resources for

future projects. A business prepares various types of budgets and planned its expenditures

and cash requirements for the projects that are going to happen in the near future. Types of

budgets include cash budget, sales and production budgets and the budgets for different types

of business overheads (Weikart, Chen and Sermier, 2012). This report contains preparation

various budgets along with the budgeted financial statements for the company which will be

incorporated on 1st January 2019, named as CooperWorld Ltd. It also explains the ways by

which CooperWorld can enhance its cash budget.

Requirement 1

(a) Production budget

CooperWorld

Ltd.

Production

Budget

Ja

n

Fe

b

Ma

r Apr May Jun Jul

Au

g

Se

p

Oc

t

No

v

De

c

Tot

al

Budgeted units

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Add: closing

inventory 0 0 0 0 0 0 0 0 0 0 0 0 0

Total requirement

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Less: opening

inventory 0 0 0 0 0 0 0 0 0 0 0 0 0

Required

production

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Note:

It is assumed that there will be no opening and closing inventory because the company

will be producing only that much units which are required for sales

(b) Sales Budget

CooperWor

ld Ltd.

Sales

Performance management 3

Budget

Jan

Fe

b

Ma

r Apr May Jun Jul

Au

g

Se

p Oct

No

v

De

c

Tot

al

Budgeted

sales units

12

0

14

0

16

0 180 200

22

0

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Selling

Price per

unit

30

0

30

0

30

0 300 300

30

0

30

0

30

0

30

0

30

0

30

0

30

0

Budgeted

sales (£)

36

00

0

42

00

0

48

00

0

5400

0

6000

0

66

00

0

72

00

0

78

00

0

72

00

0

72

00

0

48

00

0

54

00

0

702

000

(c) Material Purchase Budget

CooperWorld

Ltd.

Material

Purchase Budget

Ja

n

Fe

b

M

ar Apr May Jun Jul

Au

g

Se

p

Oc

t

No

v

De

c

Tot

al

Production

12

0

14

0

16

0 180 200 220

24

0 260

24

0

24

0

16

0

18

0

234

0

Material Per unit 1 1 1 1 1 1 1 1 1 1 1 1 1

Production

needed

12

0

14

0

16

0 180 200 220

24

0 260

24

0

24

0

16

0

18

0

234

0

Add: closing

inventory 0 0 0 0 0 0 0 0 0 0 0 0 0

Total needed

12

0

14

0

16

0 180 200 220

24

0 260

24

0

24

0

16

0

18

0

234

0

Less: opening

inventory 0 0 0 0 0 0 0 0 0 0 0 0 0

Material to be

purchased

12

0

14

0

16

0 180 200 220

24

0 260

24

0

24

0

16

0

18

0

234

0

Cost per unit 40 40 40 40 40 40 40 40 40 40 40 40

Budgeted

purchases (£)

48

00

56

00

64

00

720

0

800

0

880

0

96

00

104

00

96

00

96

00

64

00

72

00

936

00

Note:

It is assumed that material per unit required for producing desired units is £1 for each

and every month.

(d) Direct Labour budget

CooperWorld

Ltd.

Direct Labour

Budget

Jan Fe Ma Apr Ma Jun Jul Au Se Oc No De Tot

Budget

Jan

Fe

b

Ma

r Apr May Jun Jul

Au

g

Se

p Oct

No

v

De

c

Tot

al

Budgeted

sales units

12

0

14

0

16

0 180 200

22

0

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Selling

Price per

unit

30

0

30

0

30

0 300 300

30

0

30

0

30

0

30

0

30

0

30

0

30

0

Budgeted

sales (£)

36

00

0

42

00

0

48

00

0

5400

0

6000

0

66

00

0

72

00

0

78

00

0

72

00

0

72

00

0

48

00

0

54

00

0

702

000

(c) Material Purchase Budget

CooperWorld

Ltd.

Material

Purchase Budget

Ja

n

Fe

b

M

ar Apr May Jun Jul

Au

g

Se

p

Oc

t

No

v

De

c

Tot

al

Production

12

0

14

0

16

0 180 200 220

24

0 260

24

0

24

0

16

0

18

0

234

0

Material Per unit 1 1 1 1 1 1 1 1 1 1 1 1 1

Production

needed

12

0

14

0

16

0 180 200 220

24

0 260

24

0

24

0

16

0

18

0

234

0

Add: closing

inventory 0 0 0 0 0 0 0 0 0 0 0 0 0

Total needed

12

0

14

0

16

0 180 200 220

24

0 260

24

0

24

0

16

0

18

0

234

0

Less: opening

inventory 0 0 0 0 0 0 0 0 0 0 0 0 0

Material to be

purchased

12

0

14

0

16

0 180 200 220

24

0 260

24

0

24

0

16

0

18

0

234

0

Cost per unit 40 40 40 40 40 40 40 40 40 40 40 40

Budgeted

purchases (£)

48

00

56

00

64

00

720

0

800

0

880

0

96

00

104

00

96

00

96

00

64

00

72

00

936

00

Note:

It is assumed that material per unit required for producing desired units is £1 for each

and every month.

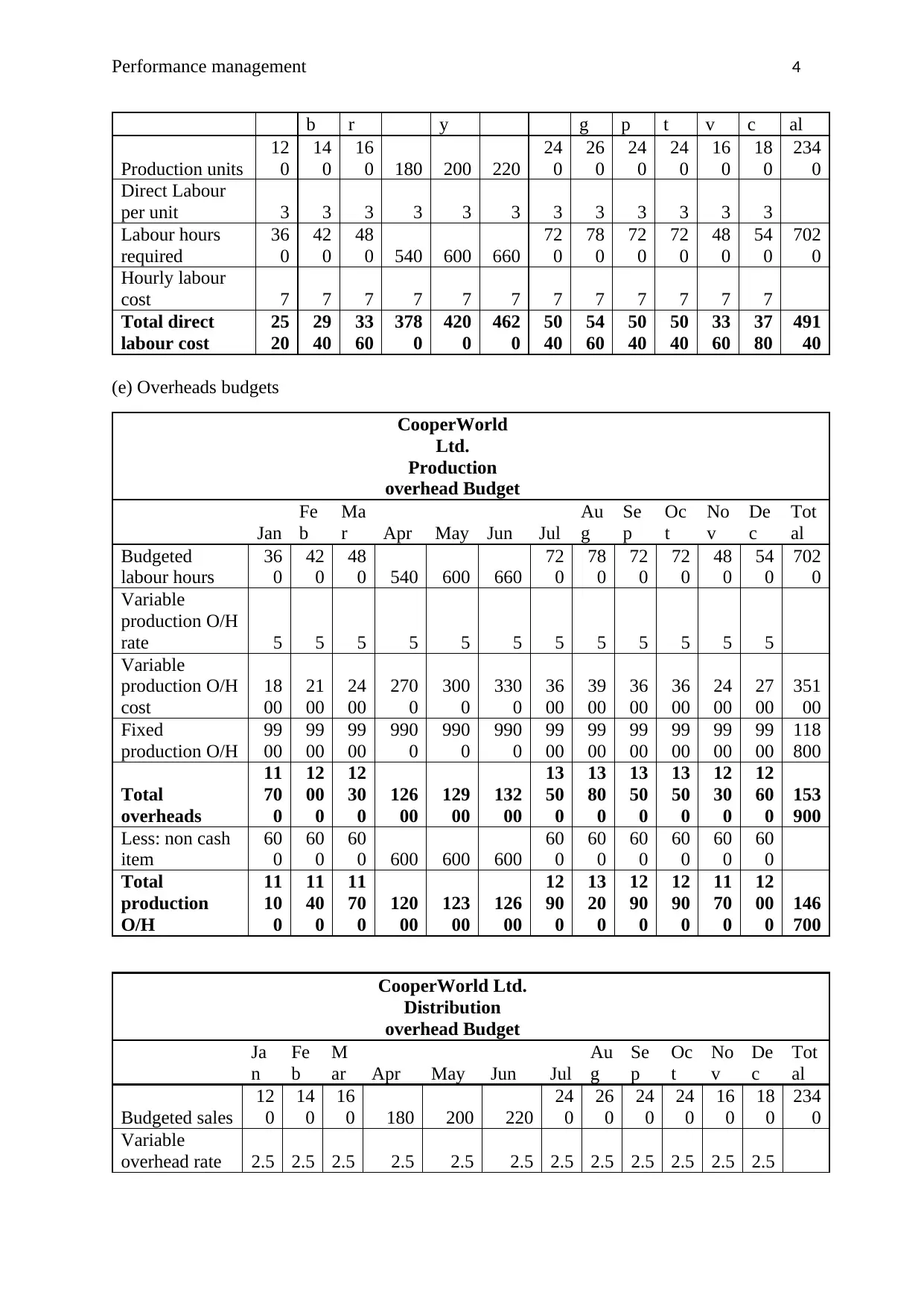

(d) Direct Labour budget

CooperWorld

Ltd.

Direct Labour

Budget

Jan Fe Ma Apr Ma Jun Jul Au Se Oc No De Tot

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Performance management 4

b r y g p t v c al

Production units

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Direct Labour

per unit 3 3 3 3 3 3 3 3 3 3 3 3

Labour hours

required

36

0

42

0

48

0 540 600 660

72

0

78

0

72

0

72

0

48

0

54

0

702

0

Hourly labour

cost 7 7 7 7 7 7 7 7 7 7 7 7

Total direct

labour cost

25

20

29

40

33

60

378

0

420

0

462

0

50

40

54

60

50

40

50

40

33

60

37

80

491

40

(e) Overheads budgets

CooperWorld

Ltd.

Production

overhead Budget

Jan

Fe

b

Ma

r Apr May Jun Jul

Au

g

Se

p

Oc

t

No

v

De

c

Tot

al

Budgeted

labour hours

36

0

42

0

48

0 540 600 660

72

0

78

0

72

0

72

0

48

0

54

0

702

0

Variable

production O/H

rate 5 5 5 5 5 5 5 5 5 5 5 5

Variable

production O/H

cost

18

00

21

00

24

00

270

0

300

0

330

0

36

00

39

00

36

00

36

00

24

00

27

00

351

00

Fixed

production O/H

99

00

99

00

99

00

990

0

990

0

990

0

99

00

99

00

99

00

99

00

99

00

99

00

118

800

Total

overheads

11

70

0

12

00

0

12

30

0

126

00

129

00

132

00

13

50

0

13

80

0

13

50

0

13

50

0

12

30

0

12

60

0

153

900

Less: non cash

item

60

0

60

0

60

0 600 600 600

60

0

60

0

60

0

60

0

60

0

60

0

Total

production

O/H

11

10

0

11

40

0

11

70

0

120

00

123

00

126

00

12

90

0

13

20

0

12

90

0

12

90

0

11

70

0

12

00

0

146

700

CooperWorld Ltd.

Distribution

overhead Budget

Ja

n

Fe

b

M

ar Apr May Jun Jul

Au

g

Se

p

Oc

t

No

v

De

c

Tot

al

Budgeted sales

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Variable

overhead rate 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5

b r y g p t v c al

Production units

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Direct Labour

per unit 3 3 3 3 3 3 3 3 3 3 3 3

Labour hours

required

36

0

42

0

48

0 540 600 660

72

0

78

0

72

0

72

0

48

0

54

0

702

0

Hourly labour

cost 7 7 7 7 7 7 7 7 7 7 7 7

Total direct

labour cost

25

20

29

40

33

60

378

0

420

0

462

0

50

40

54

60

50

40

50

40

33

60

37

80

491

40

(e) Overheads budgets

CooperWorld

Ltd.

Production

overhead Budget

Jan

Fe

b

Ma

r Apr May Jun Jul

Au

g

Se

p

Oc

t

No

v

De

c

Tot

al

Budgeted

labour hours

36

0

42

0

48

0 540 600 660

72

0

78

0

72

0

72

0

48

0

54

0

702

0

Variable

production O/H

rate 5 5 5 5 5 5 5 5 5 5 5 5

Variable

production O/H

cost

18

00

21

00

24

00

270

0

300

0

330

0

36

00

39

00

36

00

36

00

24

00

27

00

351

00

Fixed

production O/H

99

00

99

00

99

00

990

0

990

0

990

0

99

00

99

00

99

00

99

00

99

00

99

00

118

800

Total

overheads

11

70

0

12

00

0

12

30

0

126

00

129

00

132

00

13

50

0

13

80

0

13

50

0

13

50

0

12

30

0

12

60

0

153

900

Less: non cash

item

60

0

60

0

60

0 600 600 600

60

0

60

0

60

0

60

0

60

0

60

0

Total

production

O/H

11

10

0

11

40

0

11

70

0

120

00

123

00

126

00

12

90

0

13

20

0

12

90

0

12

90

0

11

70

0

12

00

0

146

700

CooperWorld Ltd.

Distribution

overhead Budget

Ja

n

Fe

b

M

ar Apr May Jun Jul

Au

g

Se

p

Oc

t

No

v

De

c

Tot

al

Budgeted sales

12

0

14

0

16

0 180 200 220

24

0

26

0

24

0

24

0

16

0

18

0

234

0

Variable

overhead rate 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5 2.5

Performance management 5

Variable

expenses (£)

30

0

35

0

40

0 450 500 550

60

0

65

0

60

0

60

0

40

0

45

0

585

0

Fixed

expenses

39

00

39

00

39

00 3900 3900 3900

39

00

39

00

39

00

39

00

39

00

39

00

468

00

Total

distribution

O/H

42

00

42

50

43

00 4350 4400 4450

45

00

45

50

45

00

45

00

43

00

43

50

526

50

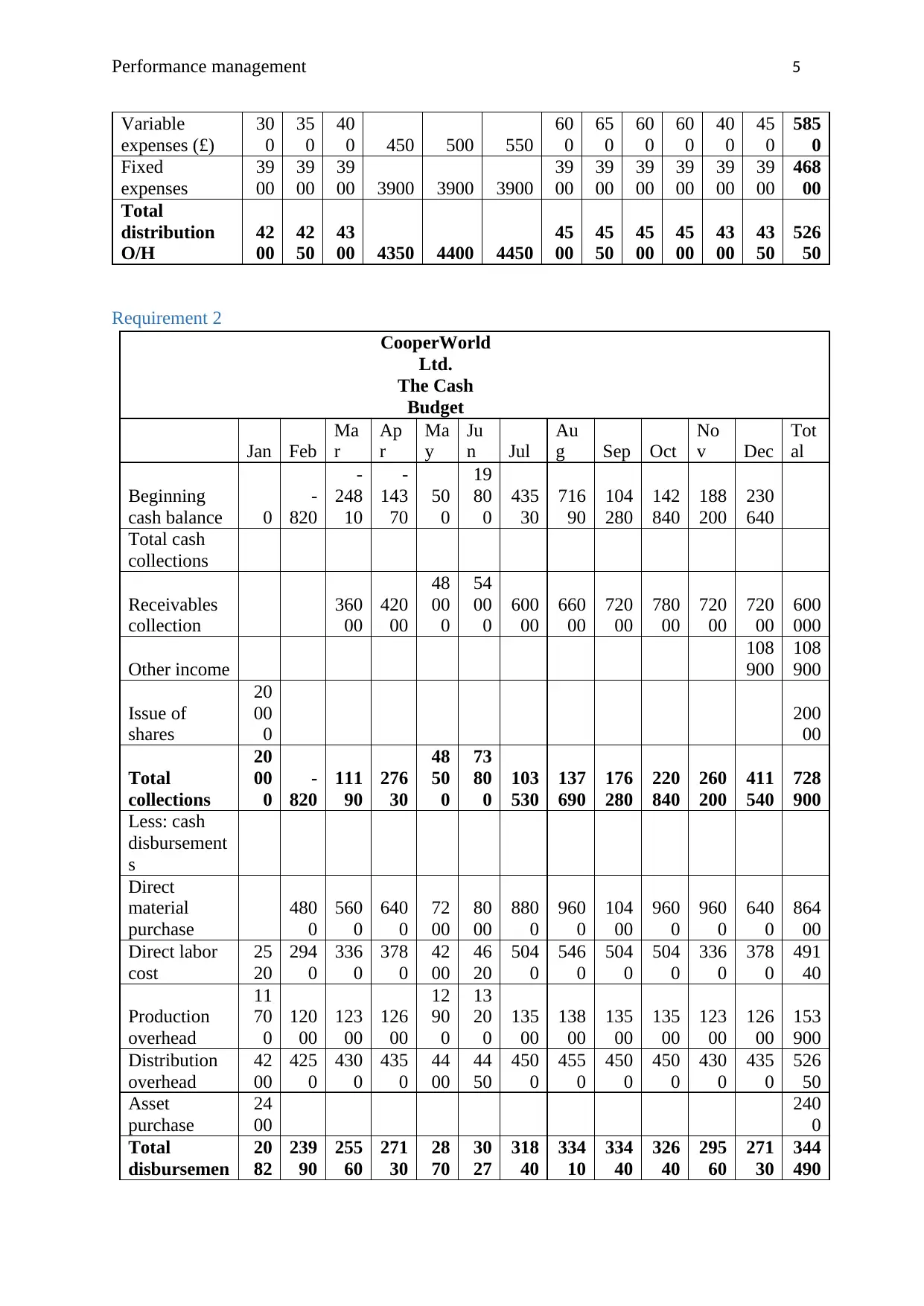

Requirement 2

CooperWorld

Ltd.

The Cash

Budget

Jan Feb

Ma

r

Ap

r

Ma

y

Ju

n Jul

Au

g Sep Oct

No

v Dec

Tot

al

Beginning

cash balance 0

-

820

-

248

10

-

143

70

50

0

19

80

0

435

30

716

90

104

280

142

840

188

200

230

640

Total cash

collections

Receivables

collection

360

00

420

00

48

00

0

54

00

0

600

00

660

00

720

00

780

00

720

00

720

00

600

000

Other income

108

900

108

900

Issue of

shares

20

00

0

200

00

Total

collections

20

00

0

-

820

111

90

276

30

48

50

0

73

80

0

103

530

137

690

176

280

220

840

260

200

411

540

728

900

Less: cash

disbursement

s

Direct

material

purchase

480

0

560

0

640

0

72

00

80

00

880

0

960

0

104

00

960

0

960

0

640

0

864

00

Direct labor

cost

25

20

294

0

336

0

378

0

42

00

46

20

504

0

546

0

504

0

504

0

336

0

378

0

491

40

Production

overhead

11

70

0

120

00

123

00

126

00

12

90

0

13

20

0

135

00

138

00

135

00

135

00

123

00

126

00

153

900

Distribution

overhead

42

00

425

0

430

0

435

0

44

00

44

50

450

0

455

0

450

0

450

0

430

0

435

0

526

50

Asset

purchase

24

00

240

0

Total

disbursemen

20

82

239

90

255

60

271

30

28

70

30

27

318

40

334

10

334

40

326

40

295

60

271

30

344

490

Variable

expenses (£)

30

0

35

0

40

0 450 500 550

60

0

65

0

60

0

60

0

40

0

45

0

585

0

Fixed

expenses

39

00

39

00

39

00 3900 3900 3900

39

00

39

00

39

00

39

00

39

00

39

00

468

00

Total

distribution

O/H

42

00

42

50

43

00 4350 4400 4450

45

00

45

50

45

00

45

00

43

00

43

50

526

50

Requirement 2

CooperWorld

Ltd.

The Cash

Budget

Jan Feb

Ma

r

Ap

r

Ma

y

Ju

n Jul

Au

g Sep Oct

No

v Dec

Tot

al

Beginning

cash balance 0

-

820

-

248

10

-

143

70

50

0

19

80

0

435

30

716

90

104

280

142

840

188

200

230

640

Total cash

collections

Receivables

collection

360

00

420

00

48

00

0

54

00

0

600

00

660

00

720

00

780

00

720

00

720

00

600

000

Other income

108

900

108

900

Issue of

shares

20

00

0

200

00

Total

collections

20

00

0

-

820

111

90

276

30

48

50

0

73

80

0

103

530

137

690

176

280

220

840

260

200

411

540

728

900

Less: cash

disbursement

s

Direct

material

purchase

480

0

560

0

640

0

72

00

80

00

880

0

960

0

104

00

960

0

960

0

640

0

864

00

Direct labor

cost

25

20

294

0

336

0

378

0

42

00

46

20

504

0

546

0

504

0

504

0

336

0

378

0

491

40

Production

overhead

11

70

0

120

00

123

00

126

00

12

90

0

13

20

0

135

00

138

00

135

00

135

00

123

00

126

00

153

900

Distribution

overhead

42

00

425

0

430

0

435

0

44

00

44

50

450

0

455

0

450

0

450

0

430

0

435

0

526

50

Asset

purchase

24

00

240

0

Total

disbursemen

20

82

239

90

255

60

271

30

28

70

30

27

318

40

334

10

334

40

326

40

295

60

271

30

344

490

Performance management 6

ts 0 0 0

Excess

(deficiency)

-

82

0

-

248

10

-

143

70 500

19

80

0

43

53

0

716

90

104

280

142

840

188

200

230

640

384

410

384

410

Ending cash

balance

-

82

0

-

248

10

-

143

70 500

19

80

0

43

53

0

716

90

104

280

142

840

188

200

230

640

384

410

384

410

Requirement 3

CooperWorld Ltd.

Income statement

Particulars

Amoun

t

Sales (2340*300) 702000

Less: cost of goods sold (2340*76) 187740

Gross profit 514260

Distribution and administration expenses 52650

Depreciation 600

Net income 461010

CooperWorld Ltd.

Balance sheet as on December 2019

Particulars Amount

Assets

Cash 384410

Accounts receivables 102000

Property and Equipment 1800

Total assets 488210

Liabilities

Accounts payable 7200

Issued capital 20000

Net income 461010

Total Liabilities 488210

Requirement 4

(A) Budgeting is a considered as a very important function of a business. Companies that

does not prepare budgets for themselves, faces number of financial problems. It the most

commonly used management accounting tool and has many uses in the modern business

world. The key uses which are been stated in the academic literature are planning and

ts 0 0 0

Excess

(deficiency)

-

82

0

-

248

10

-

143

70 500

19

80

0

43

53

0

716

90

104

280

142

840

188

200

230

640

384

410

384

410

Ending cash

balance

-

82

0

-

248

10

-

143

70 500

19

80

0

43

53

0

716

90

104

280

142

840

188

200

230

640

384

410

384

410

Requirement 3

CooperWorld Ltd.

Income statement

Particulars

Amoun

t

Sales (2340*300) 702000

Less: cost of goods sold (2340*76) 187740

Gross profit 514260

Distribution and administration expenses 52650

Depreciation 600

Net income 461010

CooperWorld Ltd.

Balance sheet as on December 2019

Particulars Amount

Assets

Cash 384410

Accounts receivables 102000

Property and Equipment 1800

Total assets 488210

Liabilities

Accounts payable 7200

Issued capital 20000

Net income 461010

Total Liabilities 488210

Requirement 4

(A) Budgeting is a considered as a very important function of a business. Companies that

does not prepare budgets for themselves, faces number of financial problems. It the most

commonly used management accounting tool and has many uses in the modern business

world. The key uses which are been stated in the academic literature are planning and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance management 7

controlling. Apart from these, use of budgets also produce some other benefits to the

business, in today’s era (Edey, 2014). Following are:

Budgets are mostly used for the purpose of planning, which provides directions to the

business. They help the organization to collect the information required for making a

plan, including all the related items and expenses. By preparing a budget,

management comes to know about the cost and expenses which are to be incurred in

implementing the plan. Such planning helps in estimating the future business

conditions and avoiding the uncertainties (Dugdale and Lyne, 2010).

They also help in establishing control within the organization and is used a tool for

measuring performance against the set and predetermined targets. The actual

performance of the business can easily be compared with the budgeted one by

preparing suitable and appropriate budgets. Such comparison helps in better

management and control of business activities (Dlabay and Burrow, 2007).

Budgets are also used as a medium of communication and interaction between the

various departments and employees of an organization. As the departments are

interdependent of each other, budgets stimulates coordination in their activities. Every

division of the organization prepared a budget for itself which communicate the

financial plans across the different parts of the firm. Thus, reflecting how the different

units of the business are properly managed and are working together towards the

integrated plan of the organization, in order to achieve the set targets (Horner, 2017).

If budgets are prepared correctly and appropriately, it may results into enhancing the

motivation among the employees and managers of the organization. Knowing the

predetermined target will motivate the employees to work in a correct direction and

also to increase their performance (Atrill, McLaney and Harvey, 2014).

controlling. Apart from these, use of budgets also produce some other benefits to the

business, in today’s era (Edey, 2014). Following are:

Budgets are mostly used for the purpose of planning, which provides directions to the

business. They help the organization to collect the information required for making a

plan, including all the related items and expenses. By preparing a budget,

management comes to know about the cost and expenses which are to be incurred in

implementing the plan. Such planning helps in estimating the future business

conditions and avoiding the uncertainties (Dugdale and Lyne, 2010).

They also help in establishing control within the organization and is used a tool for

measuring performance against the set and predetermined targets. The actual

performance of the business can easily be compared with the budgeted one by

preparing suitable and appropriate budgets. Such comparison helps in better

management and control of business activities (Dlabay and Burrow, 2007).

Budgets are also used as a medium of communication and interaction between the

various departments and employees of an organization. As the departments are

interdependent of each other, budgets stimulates coordination in their activities. Every

division of the organization prepared a budget for itself which communicate the

financial plans across the different parts of the firm. Thus, reflecting how the different

units of the business are properly managed and are working together towards the

integrated plan of the organization, in order to achieve the set targets (Horner, 2017).

If budgets are prepared correctly and appropriately, it may results into enhancing the

motivation among the employees and managers of the organization. Knowing the

predetermined target will motivate the employees to work in a correct direction and

also to increase their performance (Atrill, McLaney and Harvey, 2014).

Performance management 8

Thus, it can be said that, preparation of budgets is very necessary for the companies in

today’s business world. Reason being, they guide the business in correct direction and

help in achieving greater success. CooperWorld Ltd., being a new company, prepared

sales, cash production and overheads budgets. This will help the company to know about

their expected cash inflow and outflow along with the expenses and purchases required

for the purpose of production.

(B) Cash budget is basically a plan of expected cash receipts and cash payments made during

a specific period of time. The inflow of cash include items like cash collected from

receivables, cash receipts, sales made on cash basis and other income. On the other side, cash

outflow or disbursement include expenses related to inventory, selling and administrative

expenses, distribution expenses and other payments. The net effect is denoted by excess and

deficiency (Crosson and Needles, 2013). Figures included in the cash budget of CooperWorld

Ltd. are:

Total cash collections: This item include figures related to the cash collected by

the business during a financial year. It consists of cash collection made from the

receivables and shares issued.

Receivable collection: It includes the figures of payments made by the debtors of the

company. In the coming year, CooperWorld will make credit sales and 2 month credit period

is been allowed to debtors. The sales of January will be collected in March and of February in

April. The series continues till the end of the year (Weil, Schipper and Francis, 2013).

Share issued: It includes 20000 ordinary shares issued by the company at par of £1 each. This

shows the inflow of cash and hence is recorded under the head ‘cash collections’ (Needles,

Powers and Crosson, 2013).

Thus, it can be said that, preparation of budgets is very necessary for the companies in

today’s business world. Reason being, they guide the business in correct direction and

help in achieving greater success. CooperWorld Ltd., being a new company, prepared

sales, cash production and overheads budgets. This will help the company to know about

their expected cash inflow and outflow along with the expenses and purchases required

for the purpose of production.

(B) Cash budget is basically a plan of expected cash receipts and cash payments made during

a specific period of time. The inflow of cash include items like cash collected from

receivables, cash receipts, sales made on cash basis and other income. On the other side, cash

outflow or disbursement include expenses related to inventory, selling and administrative

expenses, distribution expenses and other payments. The net effect is denoted by excess and

deficiency (Crosson and Needles, 2013). Figures included in the cash budget of CooperWorld

Ltd. are:

Total cash collections: This item include figures related to the cash collected by

the business during a financial year. It consists of cash collection made from the

receivables and shares issued.

Receivable collection: It includes the figures of payments made by the debtors of the

company. In the coming year, CooperWorld will make credit sales and 2 month credit period

is been allowed to debtors. The sales of January will be collected in March and of February in

April. The series continues till the end of the year (Weil, Schipper and Francis, 2013).

Share issued: It includes 20000 ordinary shares issued by the company at par of £1 each. This

shows the inflow of cash and hence is recorded under the head ‘cash collections’ (Needles,

Powers and Crosson, 2013).

Performance management 9

Apart from these two, another item which is included is the beginning cash balance. It shows

the balance of cash at the starting of each month. In January, February and March

CooperWorld has negative cash balance in the starting which turns positive later on. Other

income is also there.

Total Cash Disbursements: Under this head, all the payments made in cash are

included. It consists of material purchase, labour, distribution and production

overheads and the asset purchase. It basically shows the outflow of cash from the

business (Davis and Davis, 2011).

Direct material purchase: The figures of this item shows the payment made regarding the

material purchase by the company for the purpose of production. CooperWorld will be

purchasing the material in the year when production is been done and the payment regarding

the same will be made in the following month. In January, a purchase amount to £4800 is

been made which was paid in February and the amount of material purchase in February will

be paid out in March. This will continue till end of the year (DRURY, 2013).

Direct Labour cost: It shows the cost incurred on hiring labour for the purpose of producing

the required production units. The units produced in each month will require labour for 3

hours at the cost of £7 per hour. Through proper calculation and provided information, the

total direct labour cost for month of January is expected to be £2520 and of February is

£2940. Similarly, the cost is been calculated for other months also (Lal, 2009).

Production overhead: It include the amounts of variable and fixed expenditure incurred on the

production. The variable overhead consists of an absorption rate of £5 per hour for each

month and the fixed expense amounted to £9900. The variable production overhead cost

amounted to £1800 in month of January and £2100 in February and so on. Fixed cost remain

same for every month. The total production of overhead is expected to be £11700 in January,

Apart from these two, another item which is included is the beginning cash balance. It shows

the balance of cash at the starting of each month. In January, February and March

CooperWorld has negative cash balance in the starting which turns positive later on. Other

income is also there.

Total Cash Disbursements: Under this head, all the payments made in cash are

included. It consists of material purchase, labour, distribution and production

overheads and the asset purchase. It basically shows the outflow of cash from the

business (Davis and Davis, 2011).

Direct material purchase: The figures of this item shows the payment made regarding the

material purchase by the company for the purpose of production. CooperWorld will be

purchasing the material in the year when production is been done and the payment regarding

the same will be made in the following month. In January, a purchase amount to £4800 is

been made which was paid in February and the amount of material purchase in February will

be paid out in March. This will continue till end of the year (DRURY, 2013).

Direct Labour cost: It shows the cost incurred on hiring labour for the purpose of producing

the required production units. The units produced in each month will require labour for 3

hours at the cost of £7 per hour. Through proper calculation and provided information, the

total direct labour cost for month of January is expected to be £2520 and of February is

£2940. Similarly, the cost is been calculated for other months also (Lal, 2009).

Production overhead: It include the amounts of variable and fixed expenditure incurred on the

production. The variable overhead consists of an absorption rate of £5 per hour for each

month and the fixed expense amounted to £9900. The variable production overhead cost

amounted to £1800 in month of January and £2100 in February and so on. Fixed cost remain

same for every month. The total production of overhead is expected to be £11700 in January,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Performance management 10

£12000 in February and so on. This expense has to be paid in the same month, when it has

occurred.

Distribution overhead: It also include the fixed and variable distribution expenses incurred

during the year. The variable distribution overhead is £2.5 per unit sold and fixed cost is

£3900. Total variable cost occurred in starting is 300 and then it continues to increase till

October. After that the cost reduces but fixed cost remains same. The total distribution

overhead reported in January is £4200 and is to be paid in the same month.

Asset purchase: CooperWorld will be purchasing an office equipment in January 2019 worth

£2400. The asset will depreciated at 25% per annum. This purchase shows the outflow of

cash.

(C) For a company, it is very necessary to have an appropriate cash budget which shows the

strong position company’s cash flow. It is very essential for the companies to timely review

their cash budget and should take necessary measures to improve the same. The cash budget

of CoopWorld Ltd. shows that company has negative cash balance in the starting three

months of the year 2019. There can be various reasons for such negative figure. But, the thing

which is taken into consideration is that it is important for the CoopWorld to take certain

steps for improving the position of cash. It can be done in following ways:

First of all, company should make cash sales along with the credit sales. The

amount of cash sales will be treated as a cash inflow in the business and will also

increase the cash balance.

The time given to debtors for making payments should be less than the time taken

by the company from creditors. Reason being, if payables got due before

receivables, then the company will have to face cash flow problems. Early and

timely collection of receivables will definitely improve the position of cash budget

£12000 in February and so on. This expense has to be paid in the same month, when it has

occurred.

Distribution overhead: It also include the fixed and variable distribution expenses incurred

during the year. The variable distribution overhead is £2.5 per unit sold and fixed cost is

£3900. Total variable cost occurred in starting is 300 and then it continues to increase till

October. After that the cost reduces but fixed cost remains same. The total distribution

overhead reported in January is £4200 and is to be paid in the same month.

Asset purchase: CooperWorld will be purchasing an office equipment in January 2019 worth

£2400. The asset will depreciated at 25% per annum. This purchase shows the outflow of

cash.

(C) For a company, it is very necessary to have an appropriate cash budget which shows the

strong position company’s cash flow. It is very essential for the companies to timely review

their cash budget and should take necessary measures to improve the same. The cash budget

of CoopWorld Ltd. shows that company has negative cash balance in the starting three

months of the year 2019. There can be various reasons for such negative figure. But, the thing

which is taken into consideration is that it is important for the CoopWorld to take certain

steps for improving the position of cash. It can be done in following ways:

First of all, company should make cash sales along with the credit sales. The

amount of cash sales will be treated as a cash inflow in the business and will also

increase the cash balance.

The time given to debtors for making payments should be less than the time taken

by the company from creditors. Reason being, if payables got due before

receivables, then the company will have to face cash flow problems. Early and

timely collection of receivables will definitely improve the position of cash budget

Performance management 11

and also turns the negative figures into positive ones (Brigham and Houston,

2012).

Another way is that instead of buying the equipment, CooperWorld should take

the same on lease. Leasing allows the company to pay the required amount in

small instalments which eventually improve its cash balance. Moreover, lease

payments are treated as business expense and hence, can be written off.

Before selling goods on credit, company should do a credit check of its customers,

so as to know about their creditworthiness. Similarly, company should make early

payments to its suppliers and creditors and should maintain a healthy relationship

with them. All these efforts will directly and indirectly improve the cash budget

(Brigham and Houston, 2012).

Apart from the above steps, inventory management, providing discounts on loan can also

enhance the cash budget of the organization.

Conclusion

The above report concludes that budgets are very necessary for an organization to prepare.

Also by taking corrective steps, a company can improve its cash budget (Swain and Reed,

2014). CooperWorld should adopt the mentioned ways in order to increase and improve its

cash position. A suitable and appropriate cash budget can help in meeting the financial

obligation easily and also contributes in the strong position of liquidity.

and also turns the negative figures into positive ones (Brigham and Houston,

2012).

Another way is that instead of buying the equipment, CooperWorld should take

the same on lease. Leasing allows the company to pay the required amount in

small instalments which eventually improve its cash balance. Moreover, lease

payments are treated as business expense and hence, can be written off.

Before selling goods on credit, company should do a credit check of its customers,

so as to know about their creditworthiness. Similarly, company should make early

payments to its suppliers and creditors and should maintain a healthy relationship

with them. All these efforts will directly and indirectly improve the cash budget

(Brigham and Houston, 2012).

Apart from the above steps, inventory management, providing discounts on loan can also

enhance the cash budget of the organization.

Conclusion

The above report concludes that budgets are very necessary for an organization to prepare.

Also by taking corrective steps, a company can improve its cash budget (Swain and Reed,

2014). CooperWorld should adopt the mentioned ways in order to increase and improve its

cash position. A suitable and appropriate cash budget can help in meeting the financial

obligation easily and also contributes in the strong position of liquidity.

Performance management 12

References

Atrill, P., McLaney, E. and Harvey, D., (2014). Accounting: An Introduction, 6/E (Vol. 6).

Australia: Pearson Higher Education AU.

Brigham, E.F. and Houston, J.F., (2012). Fundamentals of financial management. 13th ed.

USA: Cengage Learning.

Crosson, S.V. and Needles, B.E., (2013). Managerial accounting. 11th ed. USA: Cengage

Learning.

Davis, C.E. and Davis, E., (2011). Managerial accounting. Hoboken: John Wiley & Sons.

Dlabay, L. and Burrow, J.L., (2007). Business finance. USA: Cengage Learning.

DRURY, C.M., (2013). Management and cost accounting. 7th ed. London: Springer.

Dugdale, D. and Lyne, S., (2010). Budgeting practice and organisational structure. Oxford:

Elsevier.

Edey, H.C., (2014). Business Budgets and Accounts (RLE Accounting). New York:

Routledge.

Horner, D., (2017). Accounting for Non-accountants. 10th ed. United Kingdom: Kogan Page

Publishers.

Lal, J., (2009). Cost Accounting 4E. New Delhi: Tata McGraw-Hill Education.

Needles, B.E., Powers, M. and Crosson, S.V., (2013). Principles of accounting. 11th ed. USA:

Cengage Learning.

Swain, J.W. and Reed, B.J., (2014). Budgeting for public managers. New York: Routledge.

Weil, R.L., Schipper, K. and Francis, J.,( 2013). Financial accounting: an introduction to

concepts, methods and uses. 14th ed. USA: Cengage Learning.

References

Atrill, P., McLaney, E. and Harvey, D., (2014). Accounting: An Introduction, 6/E (Vol. 6).

Australia: Pearson Higher Education AU.

Brigham, E.F. and Houston, J.F., (2012). Fundamentals of financial management. 13th ed.

USA: Cengage Learning.

Crosson, S.V. and Needles, B.E., (2013). Managerial accounting. 11th ed. USA: Cengage

Learning.

Davis, C.E. and Davis, E., (2011). Managerial accounting. Hoboken: John Wiley & Sons.

Dlabay, L. and Burrow, J.L., (2007). Business finance. USA: Cengage Learning.

DRURY, C.M., (2013). Management and cost accounting. 7th ed. London: Springer.

Dugdale, D. and Lyne, S., (2010). Budgeting practice and organisational structure. Oxford:

Elsevier.

Edey, H.C., (2014). Business Budgets and Accounts (RLE Accounting). New York:

Routledge.

Horner, D., (2017). Accounting for Non-accountants. 10th ed. United Kingdom: Kogan Page

Publishers.

Lal, J., (2009). Cost Accounting 4E. New Delhi: Tata McGraw-Hill Education.

Needles, B.E., Powers, M. and Crosson, S.V., (2013). Principles of accounting. 11th ed. USA:

Cengage Learning.

Swain, J.W. and Reed, B.J., (2014). Budgeting for public managers. New York: Routledge.

Weil, R.L., Schipper, K. and Francis, J.,( 2013). Financial accounting: an introduction to

concepts, methods and uses. 14th ed. USA: Cengage Learning.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance management 13

Weikart, L.A., Chen, G.G. and Sermier, E., (2012). Budgeting and financial management for

nonprofit organizations. California: CQ Press

Weikart, L.A., Chen, G.G. and Sermier, E., (2012). Budgeting and financial management for

nonprofit organizations. California: CQ Press

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.