Portfolio Management and Financial Analysis of Sainsbury and Tesco

VerifiedAdded on 2023/01/04

|20

|4221

|83

Report

AI Summary

This report delves into portfolio management, focusing on the financial performance of Sainsbury and Tesco. It begins with an introduction to portfolio management and then proceeds to a detailed financial ratio analysis, including current ratio, quick ratio, net profit margin, gearing ratio, and others, for both companies over two years. The analysis evaluates their performance, financial positions, and investment potential, followed by recommendations based on the financial data. The report also explores capital investment appraisal techniques, discusses their limitations in long-term decision-making, and concludes with a summary of the findings. The analysis uses data from 2018 and 2019 to compare the financial health and investment prospects of the two major retail companies. The report provides insights into the companies' efficiency, profitability, and financial stability, offering a comprehensive view of their performance in the market.

Portfolio Managerial

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PORTOFOLIO 1..............................................................................................................................3

a. Financial ratio analysis of Sainsbury as well as Tesco: ..........................................................3

b. Analysis of performance, financial position as well as investment potential in relevance to

both companies: ..........................................................................................................................5

c. Recommendations on the basis of financial performance of business:..................................12

d. Limitations of reliability of financial ratios in context to performance of company:............12

PORTOFOLIO 2............................................................................................................................13

a. Evaluating capital investment appraisals for identifying suitable project:............................13

b. Discussing limitations associated with investment appraisal techniques for the purpose of

decision-making in long run:.....................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

PORTOFOLIO 1..............................................................................................................................3

a. Financial ratio analysis of Sainsbury as well as Tesco: ..........................................................3

b. Analysis of performance, financial position as well as investment potential in relevance to

both companies: ..........................................................................................................................5

c. Recommendations on the basis of financial performance of business:..................................12

d. Limitations of reliability of financial ratios in context to performance of company:............12

PORTOFOLIO 2............................................................................................................................13

a. Evaluating capital investment appraisals for identifying suitable project:............................13

b. Discussing limitations associated with investment appraisal techniques for the purpose of

decision-making in long run:.....................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Portfolio management refers to a technique of analysing or overviewing various

investment options that company attains and selecting group of profitable investment alternatives

(Chen and Demirer, 2018). This report is based on evaluation of portfolio management in

Sainsbury and Tesco. Former organization was founded in 1869 by John James Sainsbury and is

based in London. While, later company is situated in England and was founded by Jack Cohen in

1919.

This repost consist ratio analysis of both the companies along with its interpretation.

Further, recommendations are provided on the basis of financial performance along with it

limitations of financial ratios are also discussed. Additionally, investment appraisal techniques

are studied and its results are interpreted with the intention of choosing appropriate project for

investment. Further, limitations of techniques regarding investment appraisal is discussed on the

basis of its result of long term decision-making.

PORTOFOLIO 1

a. Financial ratio analysis of Sainsbury as well as Tesco:

CURRENT RATIO Current assets / current liabilities

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Current assets 7581 7857 12570 13600

Current liabilities 11417 10302 20680 19233

Results 0.66 0.76 0.61 0.71

QUICK RATIO Quick assets / current liabilities

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Quick assets 5652 6047 9953 11336

Current liabilities 11417 10302 20680 19233

Results 0.5 0.59 0.48 0.59

NET PROFIT MARGIN Net profit / revenues * 100

Portfolio management refers to a technique of analysing or overviewing various

investment options that company attains and selecting group of profitable investment alternatives

(Chen and Demirer, 2018). This report is based on evaluation of portfolio management in

Sainsbury and Tesco. Former organization was founded in 1869 by John James Sainsbury and is

based in London. While, later company is situated in England and was founded by Jack Cohen in

1919.

This repost consist ratio analysis of both the companies along with its interpretation.

Further, recommendations are provided on the basis of financial performance along with it

limitations of financial ratios are also discussed. Additionally, investment appraisal techniques

are studied and its results are interpreted with the intention of choosing appropriate project for

investment. Further, limitations of techniques regarding investment appraisal is discussed on the

basis of its result of long term decision-making.

PORTOFOLIO 1

a. Financial ratio analysis of Sainsbury as well as Tesco:

CURRENT RATIO Current assets / current liabilities

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Current assets 7581 7857 12570 13600

Current liabilities 11417 10302 20680 19233

Results 0.66 0.76 0.61 0.71

QUICK RATIO Quick assets / current liabilities

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Quick assets 5652 6047 9953 11336

Current liabilities 11417 10302 20680 19233

Results 0.5 0.59 0.48 0.59

NET PROFIT MARGIN Net profit / revenues * 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Net profit 219 309 1320 1210

Revenues 29007 28456 63911 57493

Results 0.75 1.09 2.07 2.1

GROSS PROFIT

MARGIN Gross profit / Revenues * 100

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Gross profit 2007 1882 4144 3352

Revenues 29007 28456 63911 57493

Results 6.92 6.61 6.48 5.83

GEARING RATIO Debts / Equity

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Debts 15085 14590 34213 34404

Equity 8456 7411 14834 10480

Results 1.78 1.97 2.31 3.28

EARNING PER SHARE Total earnings / outstanding shares

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Total earnings 219 309 1320 1210

Outstanding shares 54 65 215 244

Results 4.06 4.75 6.14 4.96

PRICE EARNING RATIO Share price / EPS

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

PARTICULARS 2019 2018 2019 2018

Net profit 219 309 1320 1210

Revenues 29007 28456 63911 57493

Results 0.75 1.09 2.07 2.1

GROSS PROFIT

MARGIN Gross profit / Revenues * 100

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Gross profit 2007 1882 4144 3352

Revenues 29007 28456 63911 57493

Results 6.92 6.61 6.48 5.83

GEARING RATIO Debts / Equity

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Debts 15085 14590 34213 34404

Equity 8456 7411 14834 10480

Results 1.78 1.97 2.31 3.28

EARNING PER SHARE Total earnings / outstanding shares

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Total earnings 219 309 1320 1210

Outstanding shares 54 65 215 244

Results 4.06 4.75 6.14 4.96

PRICE EARNING RATIO Share price / EPS

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Share price 229.9 264.9 255.2 189.55

Earnings per share 1.86 2.49 6.14 4.96

Results 123.6 106.39 41.56 38.22

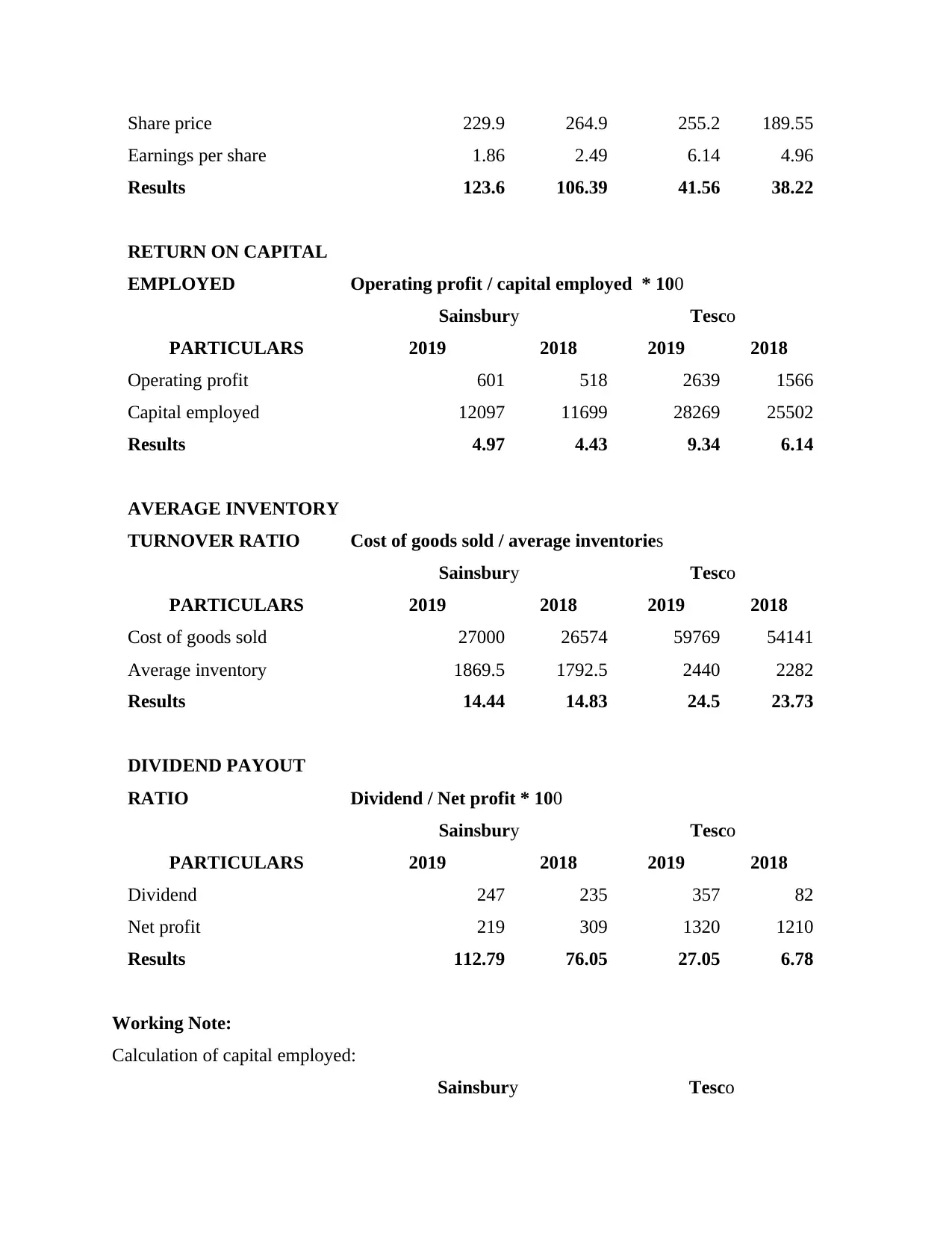

RETURN ON CAPITAL

EMPLOYED Operating profit / capital employed * 100

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Operating profit 601 518 2639 1566

Capital employed 12097 11699 28269 25502

Results 4.97 4.43 9.34 6.14

AVERAGE INVENTORY

TURNOVER RATIO Cost of goods sold / average inventories

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Cost of goods sold 27000 26574 59769 54141

Average inventory 1869.5 1792.5 2440 2282

Results 14.44 14.83 24.5 23.73

DIVIDEND PAYOUT

RATIO Dividend / Net profit * 100

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Dividend 247 235 357 82

Net profit 219 309 1320 1210

Results 112.79 76.05 27.05 6.78

Working Note:

Calculation of capital employed:

Sainsbury Tesco

Earnings per share 1.86 2.49 6.14 4.96

Results 123.6 106.39 41.56 38.22

RETURN ON CAPITAL

EMPLOYED Operating profit / capital employed * 100

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Operating profit 601 518 2639 1566

Capital employed 12097 11699 28269 25502

Results 4.97 4.43 9.34 6.14

AVERAGE INVENTORY

TURNOVER RATIO Cost of goods sold / average inventories

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Cost of goods sold 27000 26574 59769 54141

Average inventory 1869.5 1792.5 2440 2282

Results 14.44 14.83 24.5 23.73

DIVIDEND PAYOUT

RATIO Dividend / Net profit * 100

Sainsbury Tesco

PARTICULARS 2019 2018 2019 2018

Dividend 247 235 357 82

Net profit 219 309 1320 1210

Results 112.79 76.05 27.05 6.78

Working Note:

Calculation of capital employed:

Sainsbury Tesco

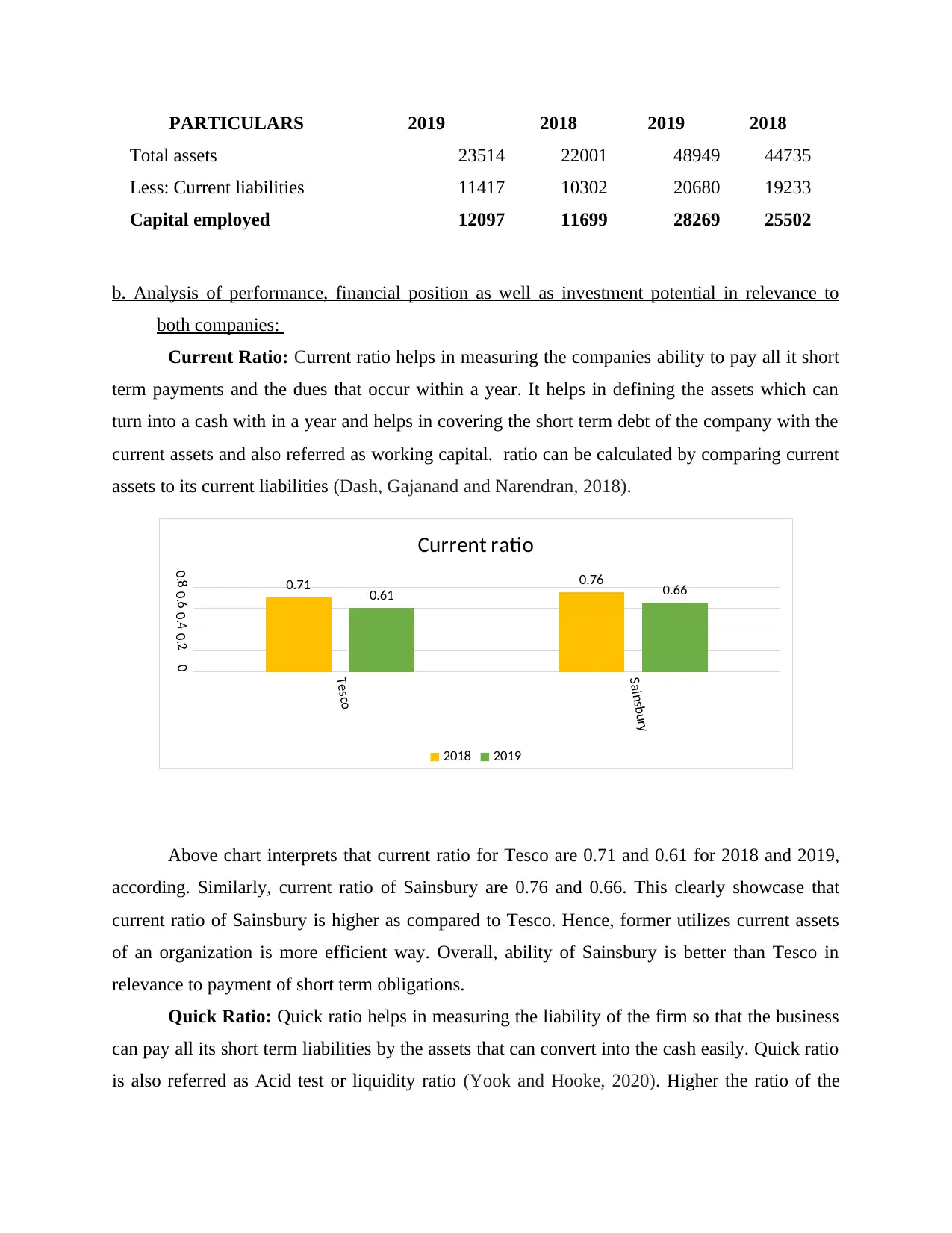

PARTICULARS 2019 2018 2019 2018

Total assets 23514 22001 48949 44735

Less: Current liabilities 11417 10302 20680 19233

Capital employed 12097 11699 28269 25502

b. Analysis of performance, financial position as well as investment potential in relevance to

both companies:

Current Ratio: Current ratio helps in measuring the companies ability to pay all it short

term payments and the dues that occur within a year. It helps in defining the assets which can

turn into a cash with in a year and helps in covering the short term debt of the company with the

current assets and also referred as working capital. ratio can be calculated by comparing current

assets to its current liabilities (Dash, Gajanand and Narendran, 2018).

Above chart interprets that current ratio for Tesco are 0.71 and 0.61 for 2018 and 2019,

according. Similarly, current ratio of Sainsbury are 0.76 and 0.66. This clearly showcase that

current ratio of Sainsbury is higher as compared to Tesco. Hence, former utilizes current assets

of an organization is more efficient way. Overall, ability of Sainsbury is better than Tesco in

relevance to payment of short term obligations.

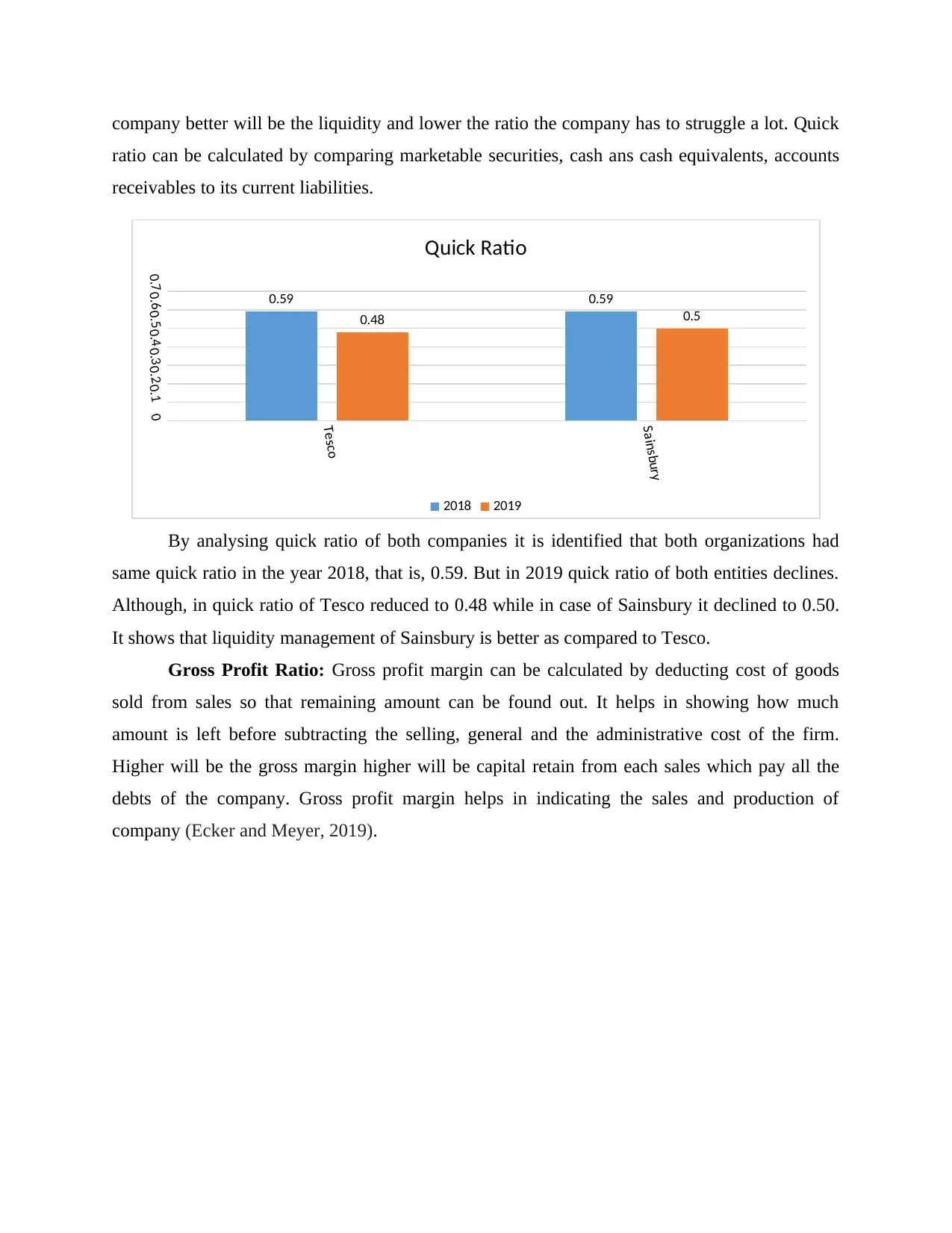

Quick Ratio: Quick ratio helps in measuring the liability of the firm so that the business

can pay all its short term liabilities by the assets that can convert into the cash easily. Quick ratio

is also referred as Acid test or liquidity ratio (Yook and Hooke, 2020). Higher the ratio of the

Tesco

Sainsbury

00.20.40.60.8 0.71 0.76

0.61 0.66

Current ratio

2018 2019

Total assets 23514 22001 48949 44735

Less: Current liabilities 11417 10302 20680 19233

Capital employed 12097 11699 28269 25502

b. Analysis of performance, financial position as well as investment potential in relevance to

both companies:

Current Ratio: Current ratio helps in measuring the companies ability to pay all it short

term payments and the dues that occur within a year. It helps in defining the assets which can

turn into a cash with in a year and helps in covering the short term debt of the company with the

current assets and also referred as working capital. ratio can be calculated by comparing current

assets to its current liabilities (Dash, Gajanand and Narendran, 2018).

Above chart interprets that current ratio for Tesco are 0.71 and 0.61 for 2018 and 2019,

according. Similarly, current ratio of Sainsbury are 0.76 and 0.66. This clearly showcase that

current ratio of Sainsbury is higher as compared to Tesco. Hence, former utilizes current assets

of an organization is more efficient way. Overall, ability of Sainsbury is better than Tesco in

relevance to payment of short term obligations.

Quick Ratio: Quick ratio helps in measuring the liability of the firm so that the business

can pay all its short term liabilities by the assets that can convert into the cash easily. Quick ratio

is also referred as Acid test or liquidity ratio (Yook and Hooke, 2020). Higher the ratio of the

Tesco

Sainsbury

00.20.40.60.8 0.71 0.76

0.61 0.66

Current ratio

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company better will be the liquidity and lower the ratio the company has to struggle a lot. Quick

ratio can be calculated by comparing marketable securities, cash ans cash equivalents, accounts

receivables to its current liabilities.

By analysing quick ratio of both companies it is identified that both organizations had

same quick ratio in the year 2018, that is, 0.59. But in 2019 quick ratio of both entities declines.

Although, in quick ratio of Tesco reduced to 0.48 while in case of Sainsbury it declined to 0.50.

It shows that liquidity management of Sainsbury is better as compared to Tesco.

Gross Profit Ratio: Gross profit margin can be calculated by deducting cost of goods

sold from sales so that remaining amount can be found out. It helps in showing how much

amount is left before subtracting the selling, general and the administrative cost of the firm.

Higher will be the gross margin higher will be capital retain from each sales which pay all the

debts of the company. Gross profit margin helps in indicating the sales and production of

company (Ecker and Meyer, 2019).

Tesco

Sainsbury

00.10.20.30.40.50.60.7 0.59 0.59

0.48 0.5

Quick Ratio

2018 2019

ratio can be calculated by comparing marketable securities, cash ans cash equivalents, accounts

receivables to its current liabilities.

By analysing quick ratio of both companies it is identified that both organizations had

same quick ratio in the year 2018, that is, 0.59. But in 2019 quick ratio of both entities declines.

Although, in quick ratio of Tesco reduced to 0.48 while in case of Sainsbury it declined to 0.50.

It shows that liquidity management of Sainsbury is better as compared to Tesco.

Gross Profit Ratio: Gross profit margin can be calculated by deducting cost of goods

sold from sales so that remaining amount can be found out. It helps in showing how much

amount is left before subtracting the selling, general and the administrative cost of the firm.

Higher will be the gross margin higher will be capital retain from each sales which pay all the

debts of the company. Gross profit margin helps in indicating the sales and production of

company (Ecker and Meyer, 2019).

Tesco

Sainsbury

00.10.20.30.40.50.60.7 0.59 0.59

0.48 0.5

Quick Ratio

2018 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

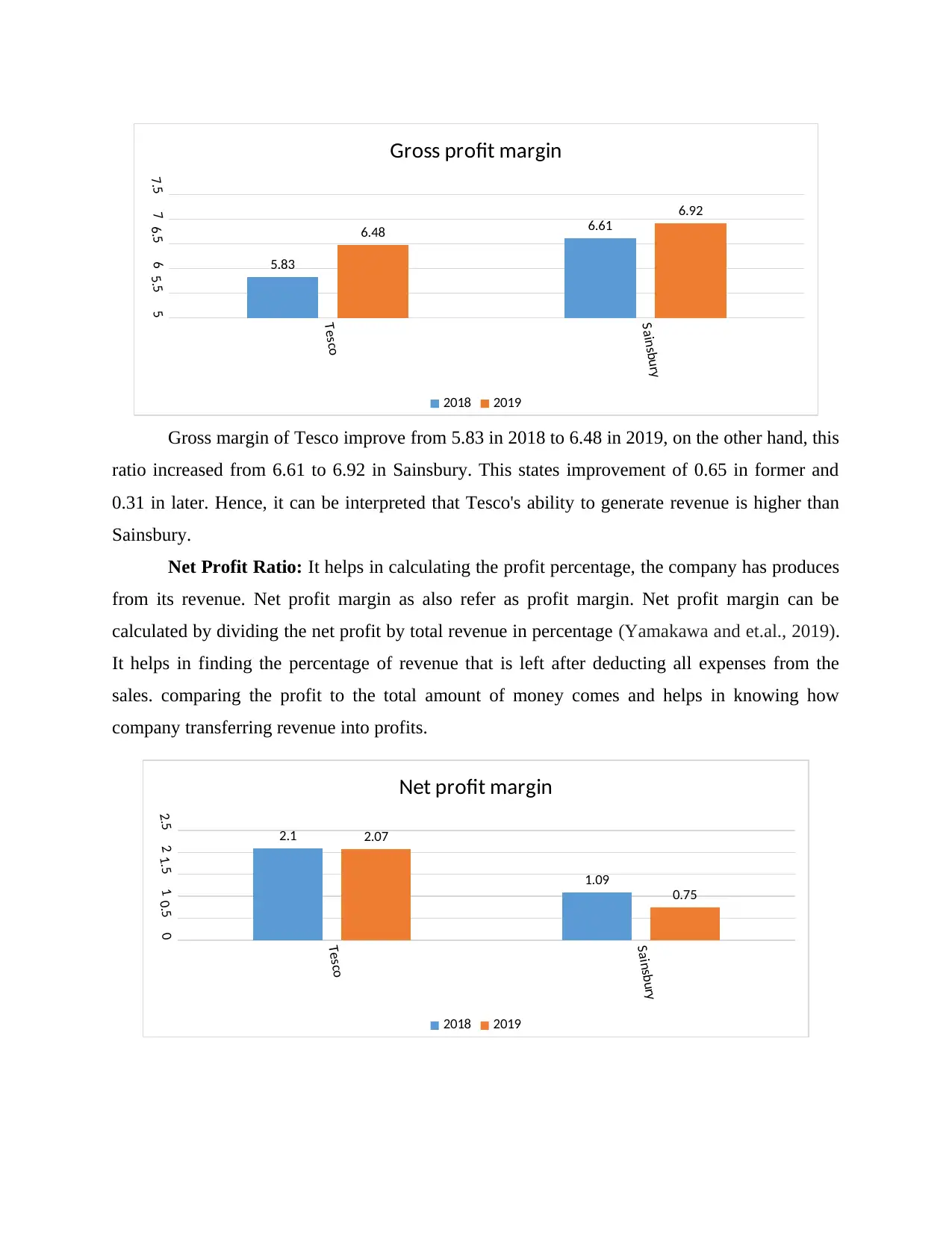

Gross margin of Tesco improve from 5.83 in 2018 to 6.48 in 2019, on the other hand, this

ratio increased from 6.61 to 6.92 in Sainsbury. This states improvement of 0.65 in former and

0.31 in later. Hence, it can be interpreted that Tesco's ability to generate revenue is higher than

Sainsbury.

Net Profit Ratio: It helps in calculating the profit percentage, the company has produces

from its revenue. Net profit margin as also refer as profit margin. Net profit margin can be

calculated by dividing the net profit by total revenue in percentage (Yamakawa and et.al., 2019).

It helps in finding the percentage of revenue that is left after deducting all expenses from the

sales. comparing the profit to the total amount of money comes and helps in knowing how

company transferring revenue into profits.

Tesco

Sainsbury

55.566.577.5

5.83

6.616.48

6.92

Gross profit margin

2018 2019

Tesco

Sainsbury

00.511.522.5 2.1

1.09

2.07

0.75

Net profit margin

2018 2019

ratio increased from 6.61 to 6.92 in Sainsbury. This states improvement of 0.65 in former and

0.31 in later. Hence, it can be interpreted that Tesco's ability to generate revenue is higher than

Sainsbury.

Net Profit Ratio: It helps in calculating the profit percentage, the company has produces

from its revenue. Net profit margin as also refer as profit margin. Net profit margin can be

calculated by dividing the net profit by total revenue in percentage (Yamakawa and et.al., 2019).

It helps in finding the percentage of revenue that is left after deducting all expenses from the

sales. comparing the profit to the total amount of money comes and helps in knowing how

company transferring revenue into profits.

Tesco

Sainsbury

55.566.577.5

5.83

6.616.48

6.92

Gross profit margin

2018 2019

Tesco

Sainsbury

00.511.522.5 2.1

1.09

2.07

0.75

Net profit margin

2018 2019

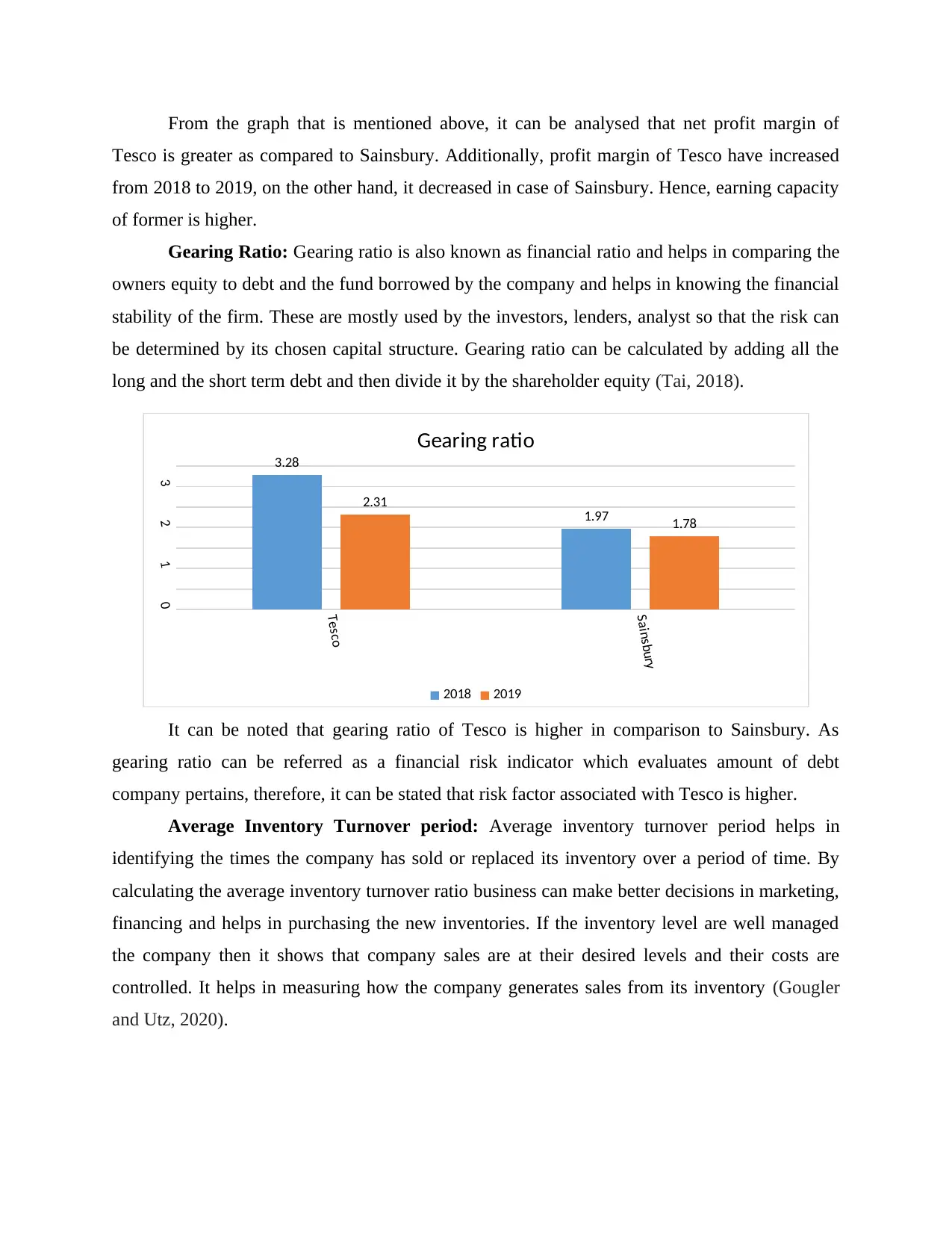

From the graph that is mentioned above, it can be analysed that net profit margin of

Tesco is greater as compared to Sainsbury. Additionally, profit margin of Tesco have increased

from 2018 to 2019, on the other hand, it decreased in case of Sainsbury. Hence, earning capacity

of former is higher.

Gearing Ratio: Gearing ratio is also known as financial ratio and helps in comparing the

owners equity to debt and the fund borrowed by the company and helps in knowing the financial

stability of the firm. These are mostly used by the investors, lenders, analyst so that the risk can

be determined by its chosen capital structure. Gearing ratio can be calculated by adding all the

long and the short term debt and then divide it by the shareholder equity (Tai, 2018).

It can be noted that gearing ratio of Tesco is higher in comparison to Sainsbury. As

gearing ratio can be referred as a financial risk indicator which evaluates amount of debt

company pertains, therefore, it can be stated that risk factor associated with Tesco is higher.

Average Inventory Turnover period: Average inventory turnover period helps in

identifying the times the company has sold or replaced its inventory over a period of time. By

calculating the average inventory turnover ratio business can make better decisions in marketing,

financing and helps in purchasing the new inventories. If the inventory level are well managed

the company then it shows that company sales are at their desired levels and their costs are

controlled. It helps in measuring how the company generates sales from its inventory (Gougler

and Utz, 2020).

Tesco

Sainsbury

0

1

2

3

3.28

1.97

2.31

1.78

Gearing ratio

2018 2019

Tesco is greater as compared to Sainsbury. Additionally, profit margin of Tesco have increased

from 2018 to 2019, on the other hand, it decreased in case of Sainsbury. Hence, earning capacity

of former is higher.

Gearing Ratio: Gearing ratio is also known as financial ratio and helps in comparing the

owners equity to debt and the fund borrowed by the company and helps in knowing the financial

stability of the firm. These are mostly used by the investors, lenders, analyst so that the risk can

be determined by its chosen capital structure. Gearing ratio can be calculated by adding all the

long and the short term debt and then divide it by the shareholder equity (Tai, 2018).

It can be noted that gearing ratio of Tesco is higher in comparison to Sainsbury. As

gearing ratio can be referred as a financial risk indicator which evaluates amount of debt

company pertains, therefore, it can be stated that risk factor associated with Tesco is higher.

Average Inventory Turnover period: Average inventory turnover period helps in

identifying the times the company has sold or replaced its inventory over a period of time. By

calculating the average inventory turnover ratio business can make better decisions in marketing,

financing and helps in purchasing the new inventories. If the inventory level are well managed

the company then it shows that company sales are at their desired levels and their costs are

controlled. It helps in measuring how the company generates sales from its inventory (Gougler

and Utz, 2020).

Tesco

Sainsbury

0

1

2

3

3.28

1.97

2.31

1.78

Gearing ratio

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

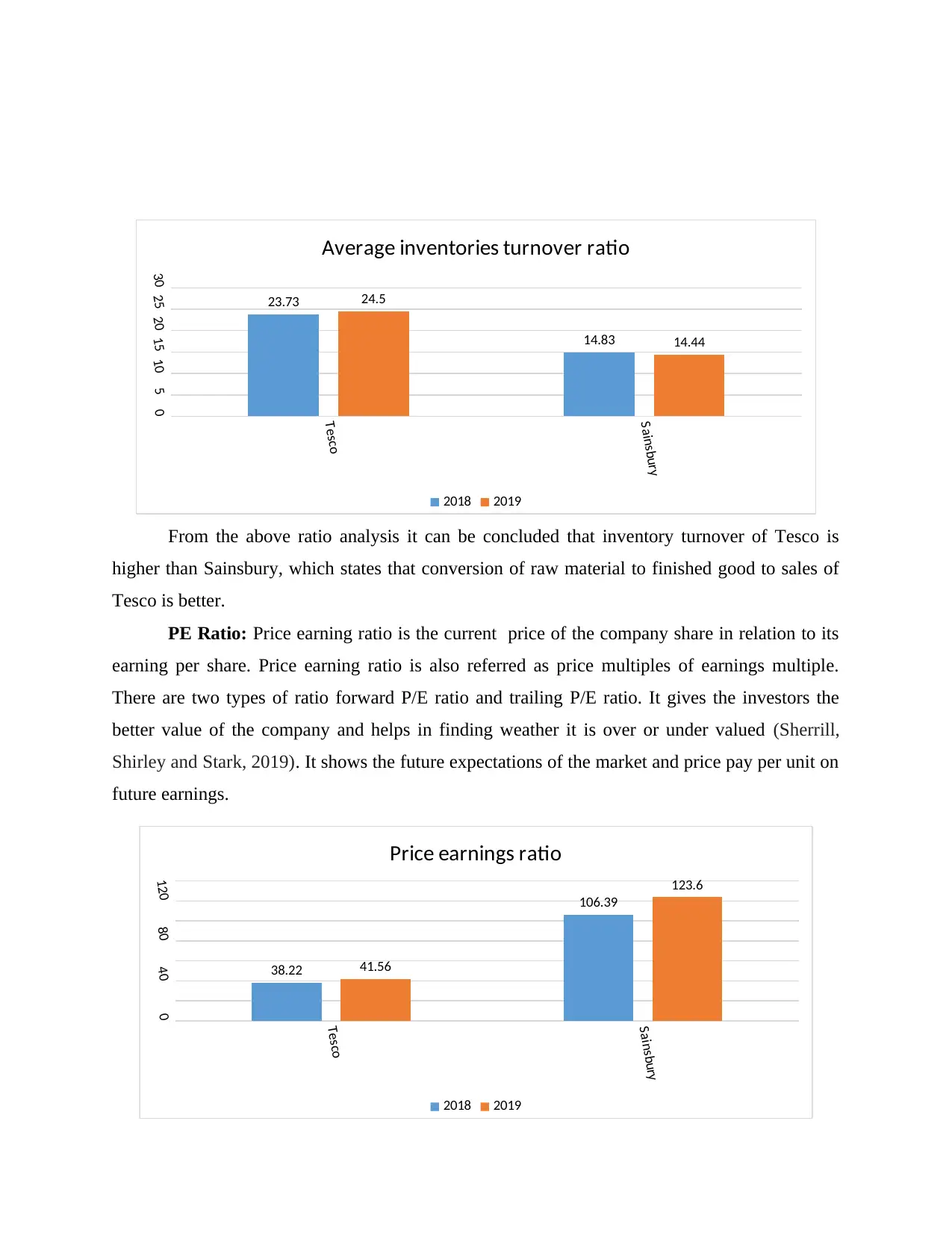

From the above ratio analysis it can be concluded that inventory turnover of Tesco is

higher than Sainsbury, which states that conversion of raw material to finished good to sales of

Tesco is better.

PE Ratio: Price earning ratio is the current price of the company share in relation to its

earning per share. Price earning ratio is also referred as price multiples of earnings multiple.

There are two types of ratio forward P/E ratio and trailing P/E ratio. It gives the investors the

better value of the company and helps in finding weather it is over or under valued (Sherrill,

Shirley and Stark, 2019). It shows the future expectations of the market and price pay per unit on

future earnings.

Tesco

Sainsbury

051015202530

23.73

14.83

24.5

14.44

Average inventories turnover ratio

2018 2019

Tesco

Sainsbury

0

40

80

120

38.22

106.39

41.56

123.6

Price earnings ratio

2018 2019

higher than Sainsbury, which states that conversion of raw material to finished good to sales of

Tesco is better.

PE Ratio: Price earning ratio is the current price of the company share in relation to its

earning per share. Price earning ratio is also referred as price multiples of earnings multiple.

There are two types of ratio forward P/E ratio and trailing P/E ratio. It gives the investors the

better value of the company and helps in finding weather it is over or under valued (Sherrill,

Shirley and Stark, 2019). It shows the future expectations of the market and price pay per unit on

future earnings.

Tesco

Sainsbury

051015202530

23.73

14.83

24.5

14.44

Average inventories turnover ratio

2018 2019

Tesco

Sainsbury

0

40

80

120

38.22

106.39

41.56

123.6

Price earnings ratio

2018 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Higher price earning ratio denotes higher amount is paid by investors in context to their

earnings. As, PE ratio of Sainsbury if higher than Tesco in both years it can be said that

investors of Sainsbury are paying excessive price as compared to their earnings.

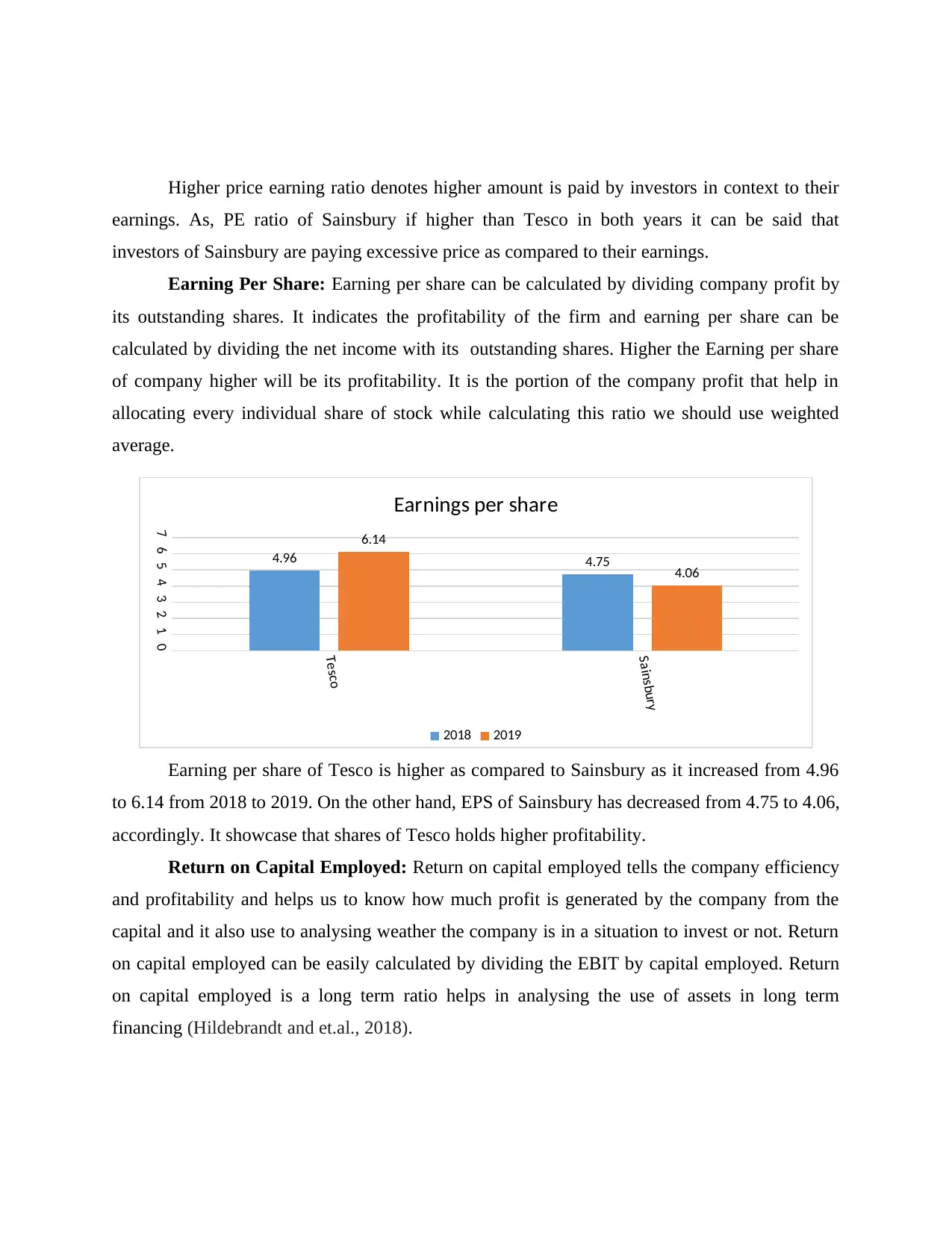

Earning Per Share: Earning per share can be calculated by dividing company profit by

its outstanding shares. It indicates the profitability of the firm and earning per share can be

calculated by dividing the net income with its outstanding shares. Higher the Earning per share

of company higher will be its profitability. It is the portion of the company profit that help in

allocating every individual share of stock while calculating this ratio we should use weighted

average.

Earning per share of Tesco is higher as compared to Sainsbury as it increased from 4.96

to 6.14 from 2018 to 2019. On the other hand, EPS of Sainsbury has decreased from 4.75 to 4.06,

accordingly. It showcase that shares of Tesco holds higher profitability.

Return on Capital Employed: Return on capital employed tells the company efficiency

and profitability and helps us to know how much profit is generated by the company from the

capital and it also use to analysing weather the company is in a situation to invest or not. Return

on capital employed can be easily calculated by dividing the EBIT by capital employed. Return

on capital employed is a long term ratio helps in analysing the use of assets in long term

financing (Hildebrandt and et.al., 2018).

Tesco

Sainsbury

01234567

4.96 4.75

6.14

4.06

Earnings per share

2018 2019

earnings. As, PE ratio of Sainsbury if higher than Tesco in both years it can be said that

investors of Sainsbury are paying excessive price as compared to their earnings.

Earning Per Share: Earning per share can be calculated by dividing company profit by

its outstanding shares. It indicates the profitability of the firm and earning per share can be

calculated by dividing the net income with its outstanding shares. Higher the Earning per share

of company higher will be its profitability. It is the portion of the company profit that help in

allocating every individual share of stock while calculating this ratio we should use weighted

average.

Earning per share of Tesco is higher as compared to Sainsbury as it increased from 4.96

to 6.14 from 2018 to 2019. On the other hand, EPS of Sainsbury has decreased from 4.75 to 4.06,

accordingly. It showcase that shares of Tesco holds higher profitability.

Return on Capital Employed: Return on capital employed tells the company efficiency

and profitability and helps us to know how much profit is generated by the company from the

capital and it also use to analysing weather the company is in a situation to invest or not. Return

on capital employed can be easily calculated by dividing the EBIT by capital employed. Return

on capital employed is a long term ratio helps in analysing the use of assets in long term

financing (Hildebrandt and et.al., 2018).

Tesco

Sainsbury

01234567

4.96 4.75

6.14

4.06

Earnings per share

2018 2019

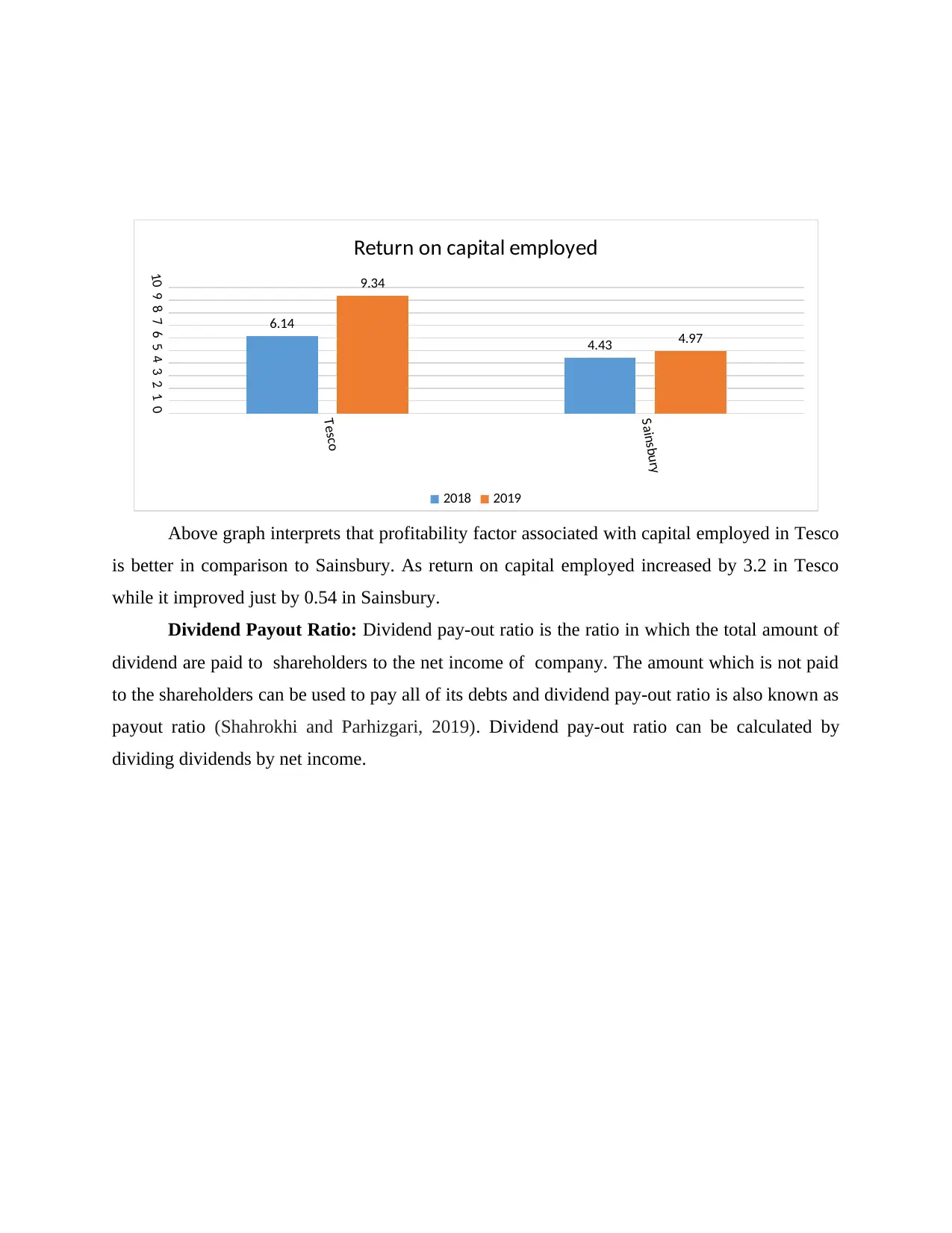

Above graph interprets that profitability factor associated with capital employed in Tesco

is better in comparison to Sainsbury. As return on capital employed increased by 3.2 in Tesco

while it improved just by 0.54 in Sainsbury.

Dividend Payout Ratio: Dividend pay-out ratio is the ratio in which the total amount of

dividend are paid to shareholders to the net income of company. The amount which is not paid

to the shareholders can be used to pay all of its debts and dividend pay-out ratio is also known as

payout ratio (Shahrokhi and Parhizgari, 2019). Dividend pay-out ratio can be calculated by

dividing dividends by net income.Tesco

Sainsbury

012345678910

6.14

4.43

9.34

4.97

Return on capital employed

2018 2019

is better in comparison to Sainsbury. As return on capital employed increased by 3.2 in Tesco

while it improved just by 0.54 in Sainsbury.

Dividend Payout Ratio: Dividend pay-out ratio is the ratio in which the total amount of

dividend are paid to shareholders to the net income of company. The amount which is not paid

to the shareholders can be used to pay all of its debts and dividend pay-out ratio is also known as

payout ratio (Shahrokhi and Parhizgari, 2019). Dividend pay-out ratio can be calculated by

dividing dividends by net income.Tesco

Sainsbury

012345678910

6.14

4.43

9.34

4.97

Return on capital employed

2018 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.