Genesis Energy Limited: Comprehensive Financial Analysis Report

VerifiedAdded on 2020/05/16

|15

|2983

|27

Project

AI Summary

This project report provides a comprehensive financial analysis of Genesis Energy Limited, an Australian company operating in the electricity industry. The report examines the company's description, ownership structure, and governance, highlighting key stakeholders and board members. It delves into performance ratios such as Return on Assets (ROA), Return on Equity (ROE), and debt ratios, offering insights into the company's financial health. The analysis includes calculations of Capital Asset Pricing Model (CAPM) and Weighted Average Cost of Capital (WACC) to assess investment proposals. The report also covers debt ratios and dividend policies, providing recommendations for investors. The financial statements of the company have been analyzed to evaluate the actual position and performance of the company. The stock price of the company has been compared with the Australian stock prices and additionally, the total cost of capital has been evaluated to identify the best investment proposal of the company. The report concludes with recommendations for investment, emphasizing the company's potential for short-term and long-term returns. The report is aimed at providing a better understanding of the company's position to make informed decisions.

Running Head: Finance For Business

1

Project Report: Finance for business

1

Project Report: Finance for business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance For Business

2

Contents

Introduction.......................................................................................................................3

1. Company description...............................................................................................3

2. Ownership structure governance.............................................................................3

3. Performance ratios...................................................................................................4

4. Changes in stock price.............................................................................................6

5. Significant factors....................................................................................................7

6. Calculation of CAPM and beta values.....................................................................7

7. WACC calculations.................................................................................................8

8. Debt ratios................................................................................................................9

9. Dividend policy......................................................................................................10

10. Recommendation and Conclusion.........................................................................10

References.......................................................................................................................11

Appendix.........................................................................................................................12

2

Contents

Introduction.......................................................................................................................3

1. Company description...............................................................................................3

2. Ownership structure governance.............................................................................3

3. Performance ratios...................................................................................................4

4. Changes in stock price.............................................................................................6

5. Significant factors....................................................................................................7

6. Calculation of CAPM and beta values.....................................................................7

7. WACC calculations.................................................................................................8

8. Debt ratios................................................................................................................9

9. Dividend policy......................................................................................................10

10. Recommendation and Conclusion.........................................................................10

References.......................................................................................................................11

Appendix.........................................................................................................................12

Finance For Business

3

Introduction:

Finance for business report explains about the various tools through which the

performance, actual position, activities, changes into the stock performance etc could be

evaluated easily. This report has been prepared on Genesis Energy Limited. It is an

Australian company which is managing its operations and business into electricity industry.

For evaluating the actual position and performance of the company, financial statement of the

company has been analyzed. Further, the stock price of the company has been compared with

the Australian stock prices and additionally, the total cost of capital has been evaluated to

identify the best investment proposal of the company. This report assists the company and the

investors to evaluate the position of the company so that a better conclusion could be get.

1. Company description:

Genesis Energy Limited is basically a New Zealand company which has been listed in

the industry of electricity generation and LPG and electricity natural gas. This company has

also been registered in the ASX by the name of GNE.AX. This company is one of the largest

electricity and LPG and natural gas retailers in the Australian market. The market share of the

company is increasing continuously and currently the 39% of electricity market of Australia

is owned by the company (Home, 2018). The company is currently employed 860 people.

Further, the total assets and total equity of the company has been enhanced.

2. Ownership structure governance:

Ownership governance structure is an important part of corporate governance of an

organization. It manages the elements of finance of the company through merging various

theory of agency. The ownership structure of the company has been analyzed and the

following data has been found:

Substantial stakeholders:

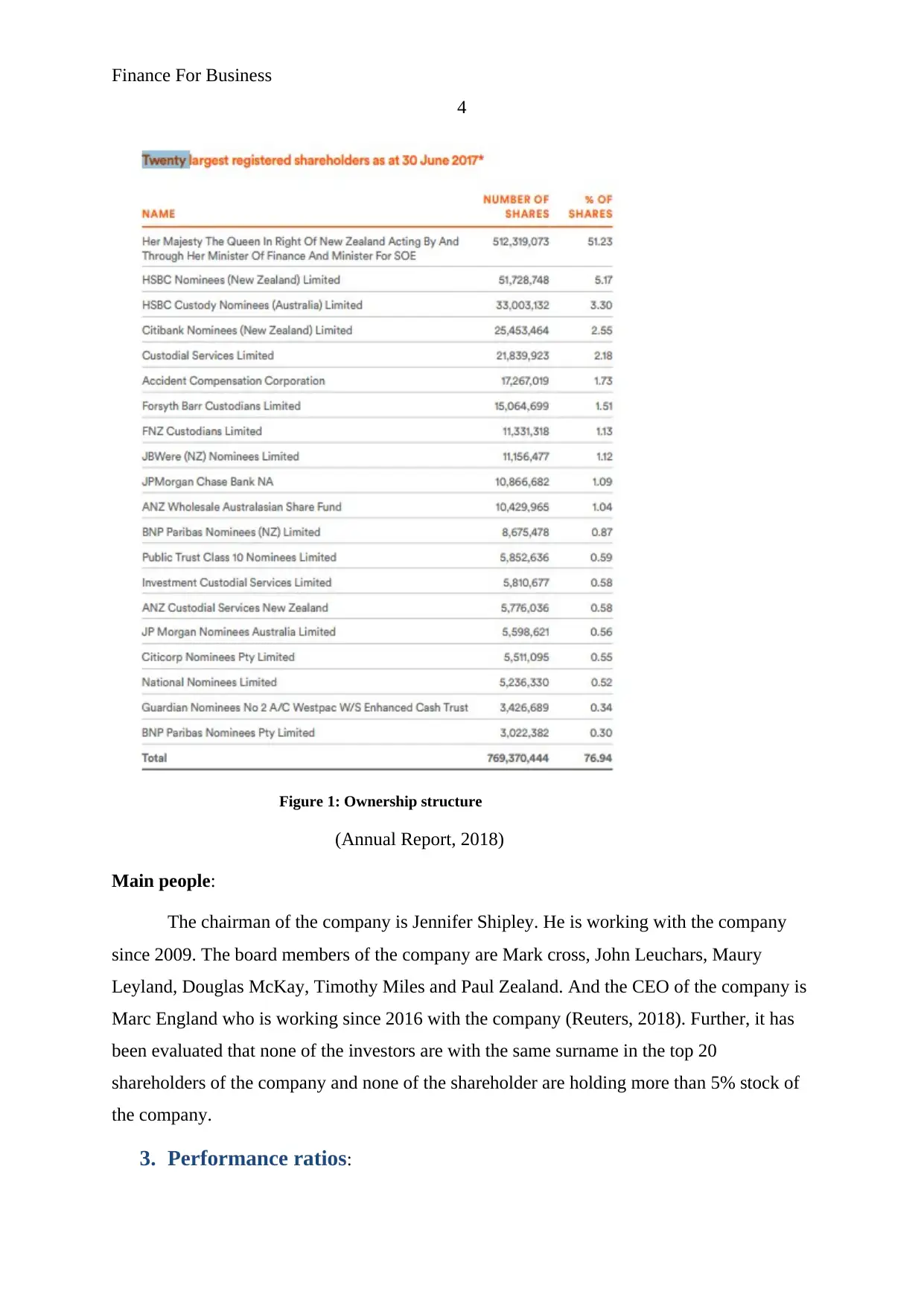

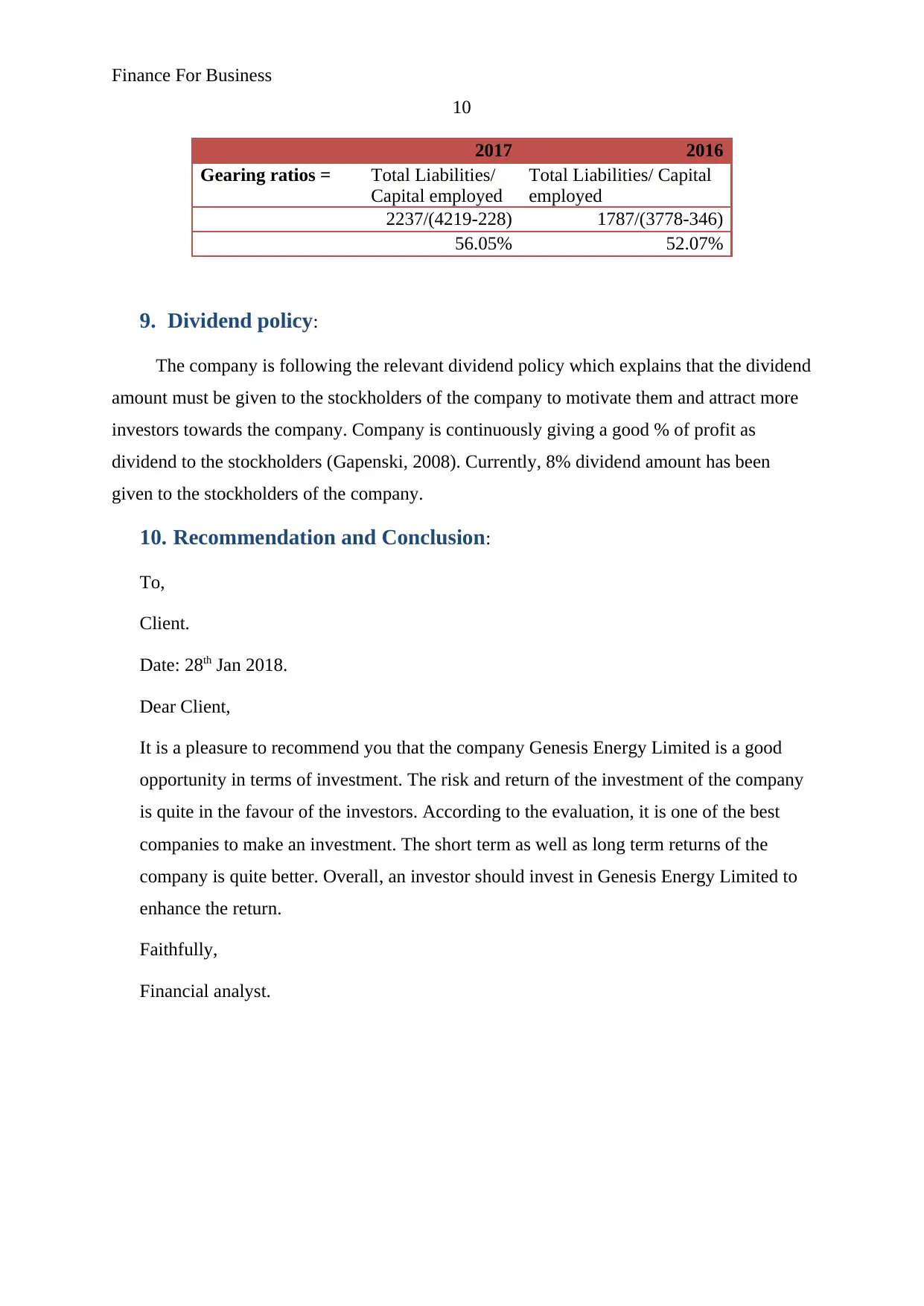

The figure 1 explains that the people with higher than 20% shareholding is only one

which name is Her Majesty. This is holding 51.23% share of the company. In addition, there

are only 2 investors who are holding more than 5% stock of the company. The name of the

holder is HSBC Nominees (New Zealand) Limited and the total ownership is 5.17%

(Annual Report, 2018).

3

Introduction:

Finance for business report explains about the various tools through which the

performance, actual position, activities, changes into the stock performance etc could be

evaluated easily. This report has been prepared on Genesis Energy Limited. It is an

Australian company which is managing its operations and business into electricity industry.

For evaluating the actual position and performance of the company, financial statement of the

company has been analyzed. Further, the stock price of the company has been compared with

the Australian stock prices and additionally, the total cost of capital has been evaluated to

identify the best investment proposal of the company. This report assists the company and the

investors to evaluate the position of the company so that a better conclusion could be get.

1. Company description:

Genesis Energy Limited is basically a New Zealand company which has been listed in

the industry of electricity generation and LPG and electricity natural gas. This company has

also been registered in the ASX by the name of GNE.AX. This company is one of the largest

electricity and LPG and natural gas retailers in the Australian market. The market share of the

company is increasing continuously and currently the 39% of electricity market of Australia

is owned by the company (Home, 2018). The company is currently employed 860 people.

Further, the total assets and total equity of the company has been enhanced.

2. Ownership structure governance:

Ownership governance structure is an important part of corporate governance of an

organization. It manages the elements of finance of the company through merging various

theory of agency. The ownership structure of the company has been analyzed and the

following data has been found:

Substantial stakeholders:

The figure 1 explains that the people with higher than 20% shareholding is only one

which name is Her Majesty. This is holding 51.23% share of the company. In addition, there

are only 2 investors who are holding more than 5% stock of the company. The name of the

holder is HSBC Nominees (New Zealand) Limited and the total ownership is 5.17%

(Annual Report, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance For Business

4

Figure 1: Ownership structure

(Annual Report, 2018)

Main people:

The chairman of the company is Jennifer Shipley. He is working with the company

since 2009. The board members of the company are Mark cross, John Leuchars, Maury

Leyland, Douglas McKay, Timothy Miles and Paul Zealand. And the CEO of the company is

Marc England who is working since 2016 with the company (Reuters, 2018). Further, it has

been evaluated that none of the investors are with the same surname in the top 20

shareholders of the company and none of the shareholder are holding more than 5% stock of

the company.

3. Performance ratios:

4

Figure 1: Ownership structure

(Annual Report, 2018)

Main people:

The chairman of the company is Jennifer Shipley. He is working with the company

since 2009. The board members of the company are Mark cross, John Leuchars, Maury

Leyland, Douglas McKay, Timothy Miles and Paul Zealand. And the CEO of the company is

Marc England who is working since 2016 with the company (Reuters, 2018). Further, it has

been evaluated that none of the investors are with the same surname in the top 20

shareholders of the company and none of the shareholder are holding more than 5% stock of

the company.

3. Performance ratios:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance For Business

5

Performance ratios are the part of ratio analysis study. This ratio includes various ratios

which are used by the professionals to manage and administer the financial changes and the

performance of the company. Following are the study few performance ratios of the

company:

Return on assets (ROA):

Return on assets ratio explains about the total profit of company which has been

earned in context with the total assets of the company. The return on assets calculations of the

company explains that the return on assets is 2.82% which is expressing about moderate

performance of the company (Morningstar, 2018).

Return on assets= NPAT/ total Assets

119/4219

2.82%

(Gapenski, 2008)

Return on equity (ROE):

Return on equity ratio explains about the total profit of company which has been

earned in context with the total equity of the company. The return on equity calculations of

the company explains that the return on equity is 6.00% which is expressing about moderate

performance of the company.

Return on Equity= Net profit after tax/

ordinary equity

119/1982

6.00%

(Morningstar, 2018)

Debt ratios:

Debt ratio explains about the total liability of company which has been managed in

context with the total assets of the company. The debt ratio calculations of the company

explain that the capital structure of the company is 53.02% which is expressing about huge

liabilities of the company in context with the total assets of the company.

Debt Ratios = Total Liabilities/

total assets

2237/4219

53.02%

5

Performance ratios are the part of ratio analysis study. This ratio includes various ratios

which are used by the professionals to manage and administer the financial changes and the

performance of the company. Following are the study few performance ratios of the

company:

Return on assets (ROA):

Return on assets ratio explains about the total profit of company which has been

earned in context with the total assets of the company. The return on assets calculations of the

company explains that the return on assets is 2.82% which is expressing about moderate

performance of the company (Morningstar, 2018).

Return on assets= NPAT/ total Assets

119/4219

2.82%

(Gapenski, 2008)

Return on equity (ROE):

Return on equity ratio explains about the total profit of company which has been

earned in context with the total equity of the company. The return on equity calculations of

the company explains that the return on equity is 6.00% which is expressing about moderate

performance of the company.

Return on Equity= Net profit after tax/

ordinary equity

119/1982

6.00%

(Morningstar, 2018)

Debt ratios:

Debt ratio explains about the total liability of company which has been managed in

context with the total assets of the company. The debt ratio calculations of the company

explain that the capital structure of the company is 53.02% which is expressing about huge

liabilities of the company in context with the total assets of the company.

Debt Ratios = Total Liabilities/

total assets

2237/4219

53.02%

Finance For Business

6

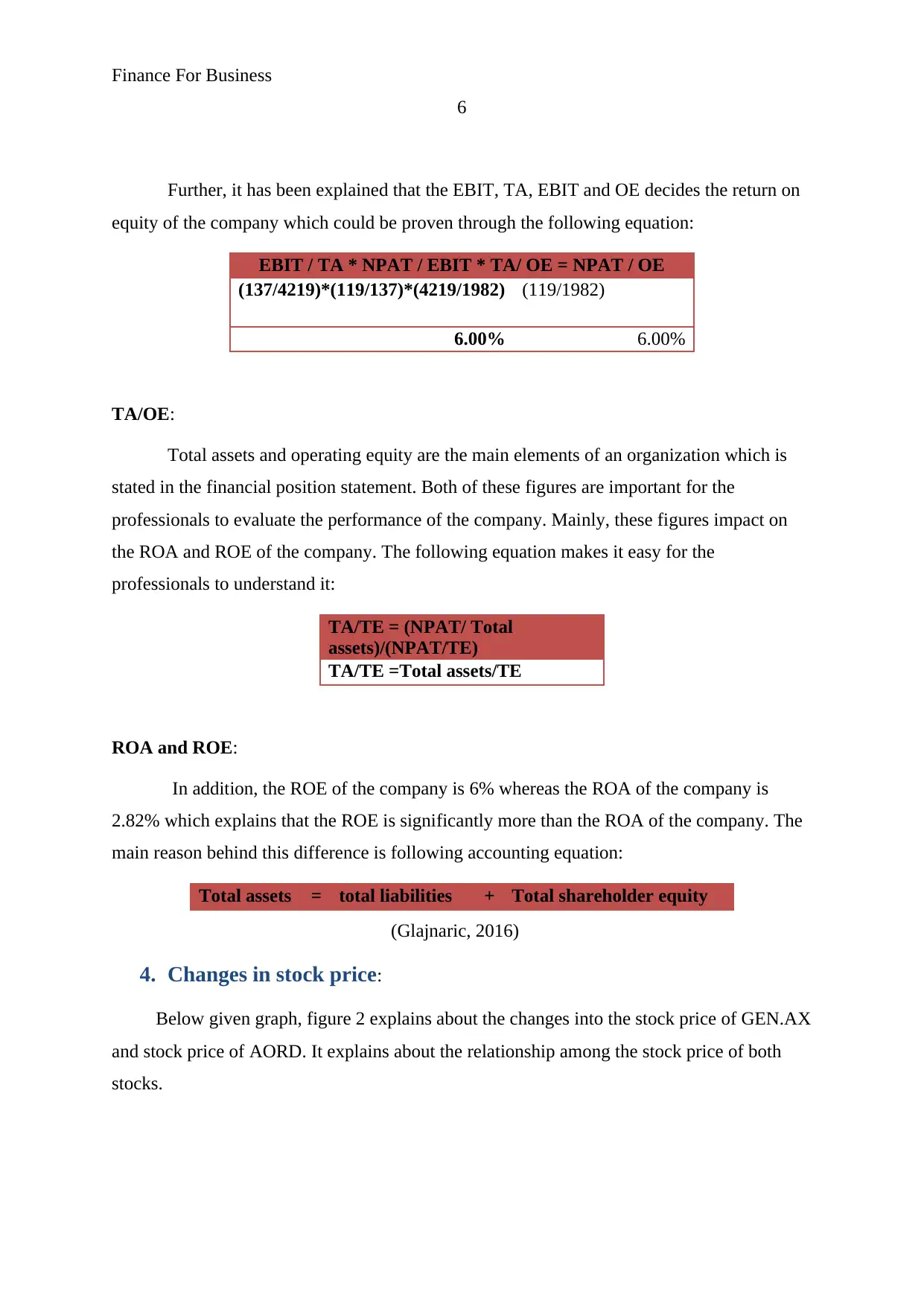

Further, it has been explained that the EBIT, TA, EBIT and OE decides the return on

equity of the company which could be proven through the following equation:

EBIT / TA * NPAT / EBIT * TA/ OE = NPAT / OE

(137/4219)*(119/137)*(4219/1982) (119/1982)

6.00% 6.00%

TA/OE:

Total assets and operating equity are the main elements of an organization which is

stated in the financial position statement. Both of these figures are important for the

professionals to evaluate the performance of the company. Mainly, these figures impact on

the ROA and ROE of the company. The following equation makes it easy for the

professionals to understand it:

TA/TE = (NPAT/ Total

assets)/(NPAT/TE)

TA/TE =Total assets/TE

ROA and ROE:

In addition, the ROE of the company is 6% whereas the ROA of the company is

2.82% which explains that the ROE is significantly more than the ROA of the company. The

main reason behind this difference is following accounting equation:

Total assets = total liabilities + Total shareholder equity

(Glajnaric, 2016)

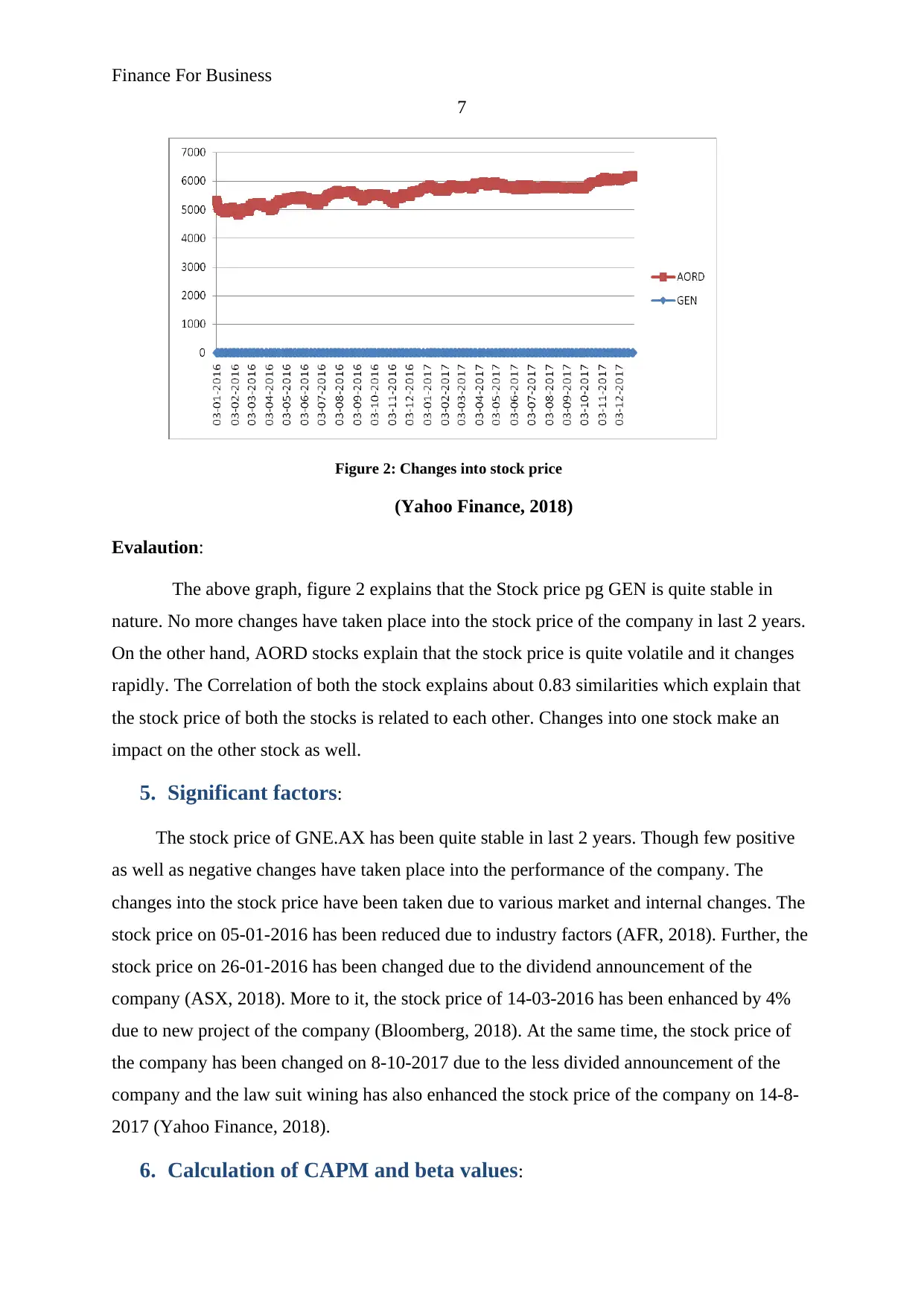

4. Changes in stock price:

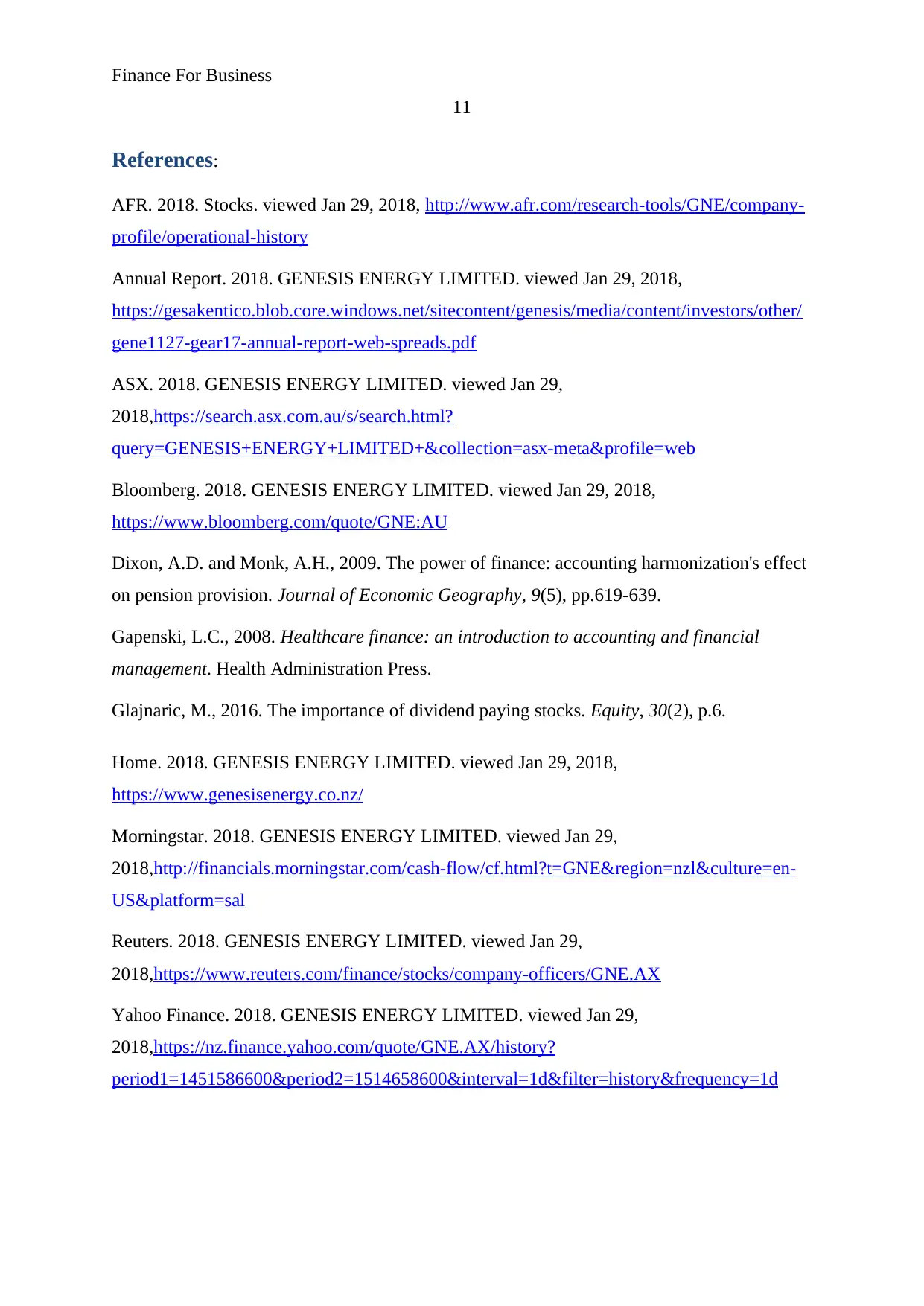

Below given graph, figure 2 explains about the changes into the stock price of GEN.AX

and stock price of AORD. It explains about the relationship among the stock price of both

stocks.

6

Further, it has been explained that the EBIT, TA, EBIT and OE decides the return on

equity of the company which could be proven through the following equation:

EBIT / TA * NPAT / EBIT * TA/ OE = NPAT / OE

(137/4219)*(119/137)*(4219/1982) (119/1982)

6.00% 6.00%

TA/OE:

Total assets and operating equity are the main elements of an organization which is

stated in the financial position statement. Both of these figures are important for the

professionals to evaluate the performance of the company. Mainly, these figures impact on

the ROA and ROE of the company. The following equation makes it easy for the

professionals to understand it:

TA/TE = (NPAT/ Total

assets)/(NPAT/TE)

TA/TE =Total assets/TE

ROA and ROE:

In addition, the ROE of the company is 6% whereas the ROA of the company is

2.82% which explains that the ROE is significantly more than the ROA of the company. The

main reason behind this difference is following accounting equation:

Total assets = total liabilities + Total shareholder equity

(Glajnaric, 2016)

4. Changes in stock price:

Below given graph, figure 2 explains about the changes into the stock price of GEN.AX

and stock price of AORD. It explains about the relationship among the stock price of both

stocks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance For Business

7

Figure 2: Changes into stock price

(Yahoo Finance, 2018)

Evalaution:

The above graph, figure 2 explains that the Stock price pg GEN is quite stable in

nature. No more changes have taken place into the stock price of the company in last 2 years.

On the other hand, AORD stocks explain that the stock price is quite volatile and it changes

rapidly. The Correlation of both the stock explains about 0.83 similarities which explain that

the stock price of both the stocks is related to each other. Changes into one stock make an

impact on the other stock as well.

5. Significant factors:

The stock price of GNE.AX has been quite stable in last 2 years. Though few positive

as well as negative changes have taken place into the performance of the company. The

changes into the stock price have been taken due to various market and internal changes. The

stock price on 05-01-2016 has been reduced due to industry factors (AFR, 2018). Further, the

stock price on 26-01-2016 has been changed due to the dividend announcement of the

company (ASX, 2018). More to it, the stock price of 14-03-2016 has been enhanced by 4%

due to new project of the company (Bloomberg, 2018). At the same time, the stock price of

the company has been changed on 8-10-2017 due to the less divided announcement of the

company and the law suit wining has also enhanced the stock price of the company on 14-8-

2017 (Yahoo Finance, 2018).

6. Calculation of CAPM and beta values:

7

Figure 2: Changes into stock price

(Yahoo Finance, 2018)

Evalaution:

The above graph, figure 2 explains that the Stock price pg GEN is quite stable in

nature. No more changes have taken place into the stock price of the company in last 2 years.

On the other hand, AORD stocks explain that the stock price is quite volatile and it changes

rapidly. The Correlation of both the stock explains about 0.83 similarities which explain that

the stock price of both the stocks is related to each other. Changes into one stock make an

impact on the other stock as well.

5. Significant factors:

The stock price of GNE.AX has been quite stable in last 2 years. Though few positive

as well as negative changes have taken place into the performance of the company. The

changes into the stock price have been taken due to various market and internal changes. The

stock price on 05-01-2016 has been reduced due to industry factors (AFR, 2018). Further, the

stock price on 26-01-2016 has been changed due to the dividend announcement of the

company (ASX, 2018). More to it, the stock price of 14-03-2016 has been enhanced by 4%

due to new project of the company (Bloomberg, 2018). At the same time, the stock price of

the company has been changed on 8-10-2017 due to the less divided announcement of the

company and the law suit wining has also enhanced the stock price of the company on 14-8-

2017 (Yahoo Finance, 2018).

6. Calculation of CAPM and beta values:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance For Business

8

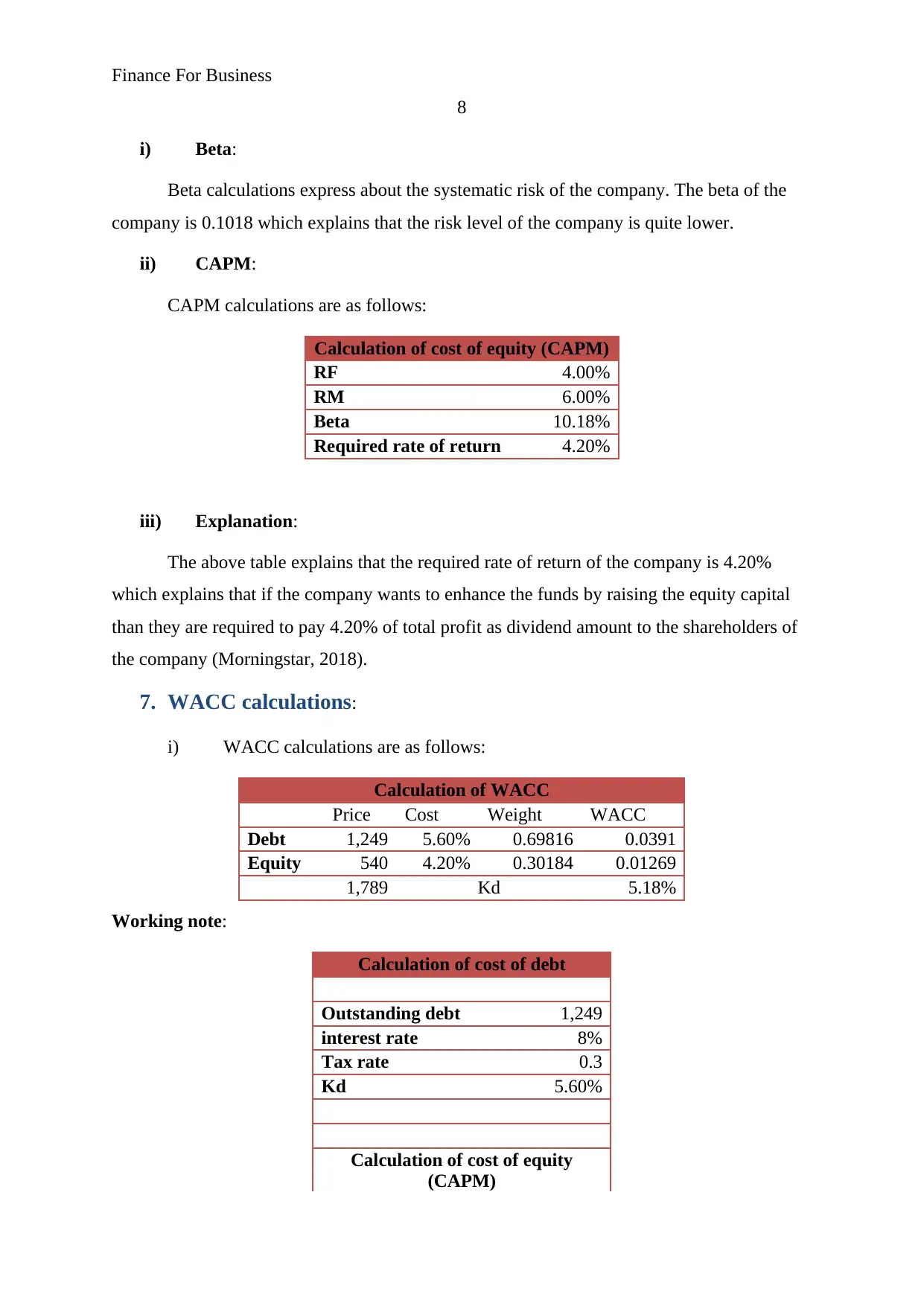

i) Beta:

Beta calculations express about the systematic risk of the company. The beta of the

company is 0.1018 which explains that the risk level of the company is quite lower.

ii) CAPM:

CAPM calculations are as follows:

Calculation of cost of equity (CAPM)

RF 4.00%

RM 6.00%

Beta 10.18%

Required rate of return 4.20%

iii) Explanation:

The above table explains that the required rate of return of the company is 4.20%

which explains that if the company wants to enhance the funds by raising the equity capital

than they are required to pay 4.20% of total profit as dividend amount to the shareholders of

the company (Morningstar, 2018).

7. WACC calculations:

i) WACC calculations are as follows:

Calculation of WACC

Price Cost Weight WACC

Debt 1,249 5.60% 0.69816 0.0391

Equity 540 4.20% 0.30184 0.01269

1,789 Kd 5.18%

Working note:

Calculation of cost of debt

Outstanding debt 1,249

interest rate 8%

Tax rate 0.3

Kd 5.60%

Calculation of cost of equity

(CAPM)

8

i) Beta:

Beta calculations express about the systematic risk of the company. The beta of the

company is 0.1018 which explains that the risk level of the company is quite lower.

ii) CAPM:

CAPM calculations are as follows:

Calculation of cost of equity (CAPM)

RF 4.00%

RM 6.00%

Beta 10.18%

Required rate of return 4.20%

iii) Explanation:

The above table explains that the required rate of return of the company is 4.20%

which explains that if the company wants to enhance the funds by raising the equity capital

than they are required to pay 4.20% of total profit as dividend amount to the shareholders of

the company (Morningstar, 2018).

7. WACC calculations:

i) WACC calculations are as follows:

Calculation of WACC

Price Cost Weight WACC

Debt 1,249 5.60% 0.69816 0.0391

Equity 540 4.20% 0.30184 0.01269

1,789 Kd 5.18%

Working note:

Calculation of cost of debt

Outstanding debt 1,249

interest rate 8%

Tax rate 0.3

Kd 5.60%

Calculation of cost of equity

(CAPM)

Finance For Business

9

RF 4.00%

RM 6.00%

Beta 10.18%

Required rate of return 4.20%

(Reuters, 2018)

ii) Evaluation:

The above table explains that the cost of equity of the company is 4.20% and cost of

debt of the company is 5.6% which explains that if the company wants to enhance the funds

through equity capital than they are required to pay 4.20% as dividend to the shareholders of

the company and at the same time, for raising the funds through debt, company has to pay

5.6% of total profit as interest amount to debt holders. The current cost of capital of the

company is 5.18% which is quite moderate. If the company would raise the debt more than

equity than the total cost of the company would be more.

8. Debt ratios:

i) Optimal capital structure:

Optimal capital structure is a level of debt and equity of the company where the risk

of the company and the cost of the company are lower. The following calculation of debt

ratio explains that the company is required to reduce the level of debt and must enhance the

equity to manage the optimal capital structure.

2017 2016

Debt Ratios = Total Liabilities/ total

assets

Total Liabilities/

total assets

2237/4219 1787/3778

53.02% 47.30%

ii) Gearing ratios:

Further, the gearing ratio of the company has been evaluated and it has been found that

the gearing position of the company has been enhanced. The company has lowered the short

term liabilities and the total liabilities have been enhanced by the company. Due to it, the

gearing ratio of the company has been enhanced (Dixon and Monk, 2009). Director has not

mentioned anything about it in their annual report.

9

RF 4.00%

RM 6.00%

Beta 10.18%

Required rate of return 4.20%

(Reuters, 2018)

ii) Evaluation:

The above table explains that the cost of equity of the company is 4.20% and cost of

debt of the company is 5.6% which explains that if the company wants to enhance the funds

through equity capital than they are required to pay 4.20% as dividend to the shareholders of

the company and at the same time, for raising the funds through debt, company has to pay

5.6% of total profit as interest amount to debt holders. The current cost of capital of the

company is 5.18% which is quite moderate. If the company would raise the debt more than

equity than the total cost of the company would be more.

8. Debt ratios:

i) Optimal capital structure:

Optimal capital structure is a level of debt and equity of the company where the risk

of the company and the cost of the company are lower. The following calculation of debt

ratio explains that the company is required to reduce the level of debt and must enhance the

equity to manage the optimal capital structure.

2017 2016

Debt Ratios = Total Liabilities/ total

assets

Total Liabilities/

total assets

2237/4219 1787/3778

53.02% 47.30%

ii) Gearing ratios:

Further, the gearing ratio of the company has been evaluated and it has been found that

the gearing position of the company has been enhanced. The company has lowered the short

term liabilities and the total liabilities have been enhanced by the company. Due to it, the

gearing ratio of the company has been enhanced (Dixon and Monk, 2009). Director has not

mentioned anything about it in their annual report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance For Business

10

2017 2016

Gearing ratios = Total Liabilities/

Capital employed

Total Liabilities/ Capital

employed

2237/(4219-228) 1787/(3778-346)

56.05% 52.07%

9. Dividend policy:

The company is following the relevant dividend policy which explains that the dividend

amount must be given to the stockholders of the company to motivate them and attract more

investors towards the company. Company is continuously giving a good % of profit as

dividend to the stockholders (Gapenski, 2008). Currently, 8% dividend amount has been

given to the stockholders of the company.

10. Recommendation and Conclusion:

To,

Client.

Date: 28th Jan 2018.

Dear Client,

It is a pleasure to recommend you that the company Genesis Energy Limited is a good

opportunity in terms of investment. The risk and return of the investment of the company

is quite in the favour of the investors. According to the evaluation, it is one of the best

companies to make an investment. The short term as well as long term returns of the

company is quite better. Overall, an investor should invest in Genesis Energy Limited to

enhance the return.

Faithfully,

Financial analyst.

10

2017 2016

Gearing ratios = Total Liabilities/

Capital employed

Total Liabilities/ Capital

employed

2237/(4219-228) 1787/(3778-346)

56.05% 52.07%

9. Dividend policy:

The company is following the relevant dividend policy which explains that the dividend

amount must be given to the stockholders of the company to motivate them and attract more

investors towards the company. Company is continuously giving a good % of profit as

dividend to the stockholders (Gapenski, 2008). Currently, 8% dividend amount has been

given to the stockholders of the company.

10. Recommendation and Conclusion:

To,

Client.

Date: 28th Jan 2018.

Dear Client,

It is a pleasure to recommend you that the company Genesis Energy Limited is a good

opportunity in terms of investment. The risk and return of the investment of the company

is quite in the favour of the investors. According to the evaluation, it is one of the best

companies to make an investment. The short term as well as long term returns of the

company is quite better. Overall, an investor should invest in Genesis Energy Limited to

enhance the return.

Faithfully,

Financial analyst.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance For Business

11

References:

AFR. 2018. Stocks. viewed Jan 29, 2018, http://www.afr.com/research-tools/GNE/company-

profile/operational-history

Annual Report. 2018. GENESIS ENERGY LIMITED. viewed Jan 29, 2018,

https://gesakentico.blob.core.windows.net/sitecontent/genesis/media/content/investors/other/

gene1127-gear17-annual-report-web-spreads.pdf

ASX. 2018. GENESIS ENERGY LIMITED. viewed Jan 29,

2018,https://search.asx.com.au/s/search.html?

query=GENESIS+ENERGY+LIMITED+&collection=asx-meta&profile=web

Bloomberg. 2018. GENESIS ENERGY LIMITED. viewed Jan 29, 2018,

https://www.bloomberg.com/quote/GNE:AU

Dixon, A.D. and Monk, A.H., 2009. The power of finance: accounting harmonization's effect

on pension provision. Journal of Economic Geography, 9(5), pp.619-639.

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Glajnaric, M., 2016. The importance of dividend paying stocks. Equity, 30(2), p.6.

Home. 2018. GENESIS ENERGY LIMITED. viewed Jan 29, 2018,

https://www.genesisenergy.co.nz/

Morningstar. 2018. GENESIS ENERGY LIMITED. viewed Jan 29,

2018,http://financials.morningstar.com/cash-flow/cf.html?t=GNE®ion=nzl&culture=en-

US&platform=sal

Reuters. 2018. GENESIS ENERGY LIMITED. viewed Jan 29,

2018,https://www.reuters.com/finance/stocks/company-officers/GNE.AX

Yahoo Finance. 2018. GENESIS ENERGY LIMITED. viewed Jan 29,

2018,https://nz.finance.yahoo.com/quote/GNE.AX/history?

period1=1451586600&period2=1514658600&interval=1d&filter=history&frequency=1d

11

References:

AFR. 2018. Stocks. viewed Jan 29, 2018, http://www.afr.com/research-tools/GNE/company-

profile/operational-history

Annual Report. 2018. GENESIS ENERGY LIMITED. viewed Jan 29, 2018,

https://gesakentico.blob.core.windows.net/sitecontent/genesis/media/content/investors/other/

gene1127-gear17-annual-report-web-spreads.pdf

ASX. 2018. GENESIS ENERGY LIMITED. viewed Jan 29,

2018,https://search.asx.com.au/s/search.html?

query=GENESIS+ENERGY+LIMITED+&collection=asx-meta&profile=web

Bloomberg. 2018. GENESIS ENERGY LIMITED. viewed Jan 29, 2018,

https://www.bloomberg.com/quote/GNE:AU

Dixon, A.D. and Monk, A.H., 2009. The power of finance: accounting harmonization's effect

on pension provision. Journal of Economic Geography, 9(5), pp.619-639.

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Glajnaric, M., 2016. The importance of dividend paying stocks. Equity, 30(2), p.6.

Home. 2018. GENESIS ENERGY LIMITED. viewed Jan 29, 2018,

https://www.genesisenergy.co.nz/

Morningstar. 2018. GENESIS ENERGY LIMITED. viewed Jan 29,

2018,http://financials.morningstar.com/cash-flow/cf.html?t=GNE®ion=nzl&culture=en-

US&platform=sal

Reuters. 2018. GENESIS ENERGY LIMITED. viewed Jan 29,

2018,https://www.reuters.com/finance/stocks/company-officers/GNE.AX

Yahoo Finance. 2018. GENESIS ENERGY LIMITED. viewed Jan 29,

2018,https://nz.finance.yahoo.com/quote/GNE.AX/history?

period1=1451586600&period2=1514658600&interval=1d&filter=history&frequency=1d

Finance For Business

12

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.