Management Accounting Project Report

VerifiedAdded on 2022/11/14

|14

|3359

|120

AI Summary

This Management Accounting Project Report includes schedules, activities, and resource drivers used. It covers traditional and activity-based costing systems, management accounting factors, benefits, and limitations of ABC costing. The report also provides information on corporate management, process receivables, process payables, production planning, reports to health dept, process sales order, dispatch sales order, new product development, inspect filling ingredients, disposal of substandard ingredients, move to mixing room, set up mixer, weigh and sort ingredients, load mixer, operate mixer, unload and clean mixer, move to filling room, set up pastry cases, stack cases on filling machine, fill pastry cases, clean hopper, move to baking, stack cases on baking trays, setup ovens, move to ovens, bake products, unload oven, inspect finished products, and disposal of substandard products.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Management Accounting

1

Project Report: Management Accounting

1

Project Report: Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

2

Contents

Answer 1, 2, 3 and 4.........................................................................................................3

Schedule 1.....................................................................................................................3

Schedule 2.....................................................................................................................3

Schedule 3.....................................................................................................................4

Schedule 4.....................................................................................................................4

Schedule 5.....................................................................................................................6

Schedule 6.....................................................................................................................7

Answer 5...........................................................................................................................8

Answer 6...........................................................................................................................8

Answer 7...........................................................................................................................9

Answer 8 and 9.................................................................................................................9

Introduction...................................................................................................................9

Traditional costing system............................................................................................9

Activity based costing system....................................................................................10

Management accounting factor...................................................................................11

Benefit of ABC costing..............................................................................................11

Cost and limitation of ABC costing:..........................................................................12

Conclusion..................................................................................................................12

References.......................................................................................................................13

2

Contents

Answer 1, 2, 3 and 4.........................................................................................................3

Schedule 1.....................................................................................................................3

Schedule 2.....................................................................................................................3

Schedule 3.....................................................................................................................4

Schedule 4.....................................................................................................................4

Schedule 5.....................................................................................................................6

Schedule 6.....................................................................................................................7

Answer 5...........................................................................................................................8

Answer 6...........................................................................................................................8

Answer 7...........................................................................................................................9

Answer 8 and 9.................................................................................................................9

Introduction...................................................................................................................9

Traditional costing system............................................................................................9

Activity based costing system....................................................................................10

Management accounting factor...................................................................................11

Benefit of ABC costing..............................................................................................11

Cost and limitation of ABC costing:..........................................................................12

Conclusion..................................................................................................................12

References.......................................................................................................................13

Management Accounting

3

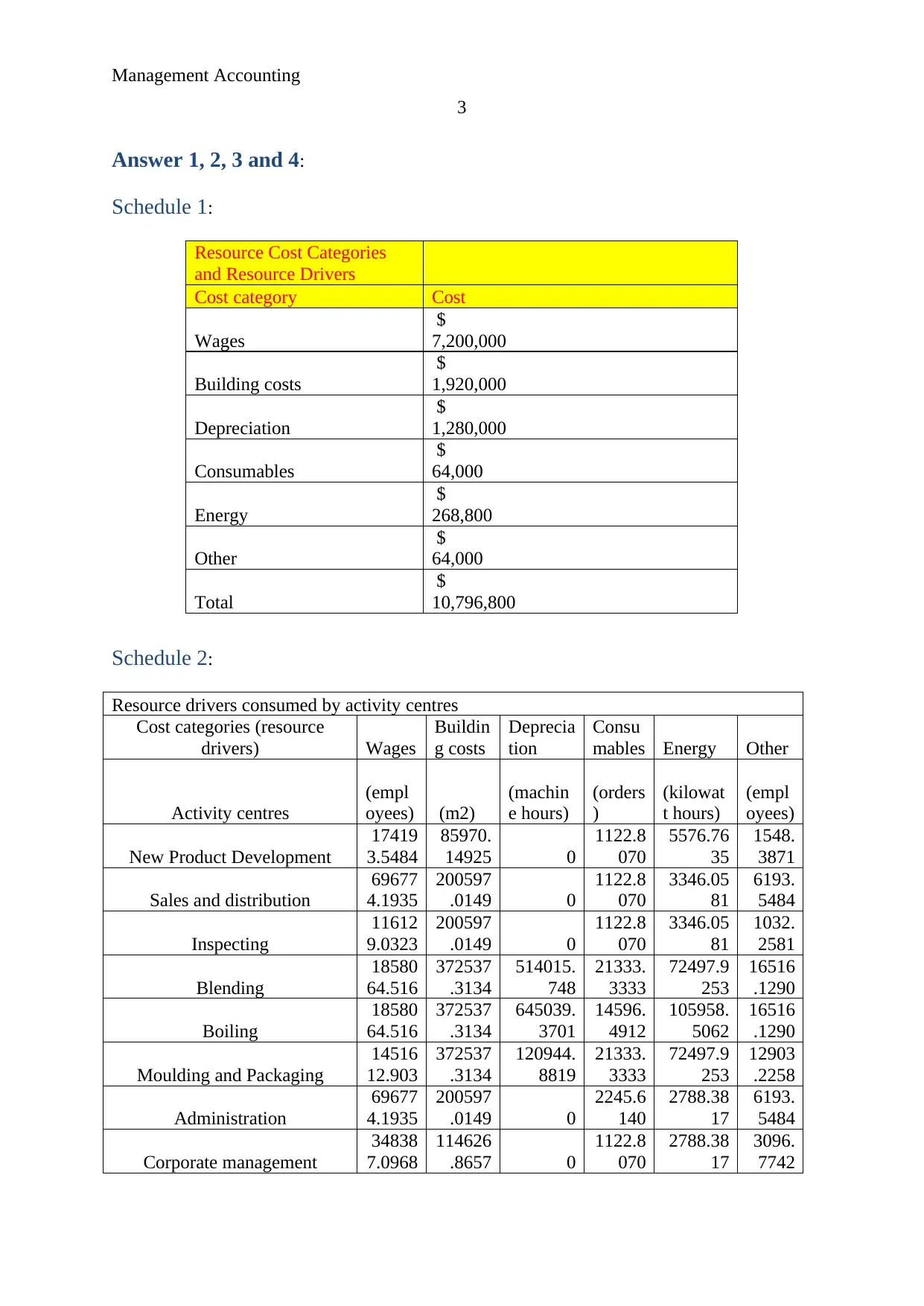

Answer 1, 2, 3 and 4:

Schedule 1:

Resource Cost Categories

and Resource Drivers

Cost category Cost

Wages

$

7,200,000

Building costs

$

1,920,000

Depreciation

$

1,280,000

Consumables

$

64,000

Energy

$

268,800

Other

$

64,000

Total

$

10,796,800

Schedule 2:

Resource drivers consumed by activity centres

Cost categories (resource

drivers) Wages

Buildin

g costs

Deprecia

tion

Consu

mables Energy Other

Activity centres

(empl

oyees) (m2)

(machin

e hours)

(orders

)

(kilowat

t hours)

(empl

oyees)

New Product Development

17419

3.5484

85970.

14925 0

1122.8

070

5576.76

35

1548.

3871

Sales and distribution

69677

4.1935

200597

.0149 0

1122.8

070

3346.05

81

6193.

5484

Inspecting

11612

9.0323

200597

.0149 0

1122.8

070

3346.05

81

1032.

2581

Blending

18580

64.516

372537

.3134

514015.

748

21333.

3333

72497.9

253

16516

.1290

Boiling

18580

64.516

372537

.3134

645039.

3701

14596.

4912

105958.

5062

16516

.1290

Moulding and Packaging

14516

12.903

372537

.3134

120944.

8819

21333.

3333

72497.9

253

12903

.2258

Administration

69677

4.1935

200597

.0149 0

2245.6

140

2788.38

17

6193.

5484

Corporate management

34838

7.0968

114626

.8657 0

1122.8

070

2788.38

17

3096.

7742

3

Answer 1, 2, 3 and 4:

Schedule 1:

Resource Cost Categories

and Resource Drivers

Cost category Cost

Wages

$

7,200,000

Building costs

$

1,920,000

Depreciation

$

1,280,000

Consumables

$

64,000

Energy

$

268,800

Other

$

64,000

Total

$

10,796,800

Schedule 2:

Resource drivers consumed by activity centres

Cost categories (resource

drivers) Wages

Buildin

g costs

Deprecia

tion

Consu

mables Energy Other

Activity centres

(empl

oyees) (m2)

(machin

e hours)

(orders

)

(kilowat

t hours)

(empl

oyees)

New Product Development

17419

3.5484

85970.

14925 0

1122.8

070

5576.76

35

1548.

3871

Sales and distribution

69677

4.1935

200597

.0149 0

1122.8

070

3346.05

81

6193.

5484

Inspecting

11612

9.0323

200597

.0149 0

1122.8

070

3346.05

81

1032.

2581

Blending

18580

64.516

372537

.3134

514015.

748

21333.

3333

72497.9

253

16516

.1290

Boiling

18580

64.516

372537

.3134

645039.

3701

14596.

4912

105958.

5062

16516

.1290

Moulding and Packaging

14516

12.903

372537

.3134

120944.

8819

21333.

3333

72497.9

253

12903

.2258

Administration

69677

4.1935

200597

.0149 0

2245.6

140

2788.38

17

6193.

5484

Corporate management

34838

7.0968

114626

.8657 0

1122.8

070

2788.38

17

3096.

7742

Management Accounting

4

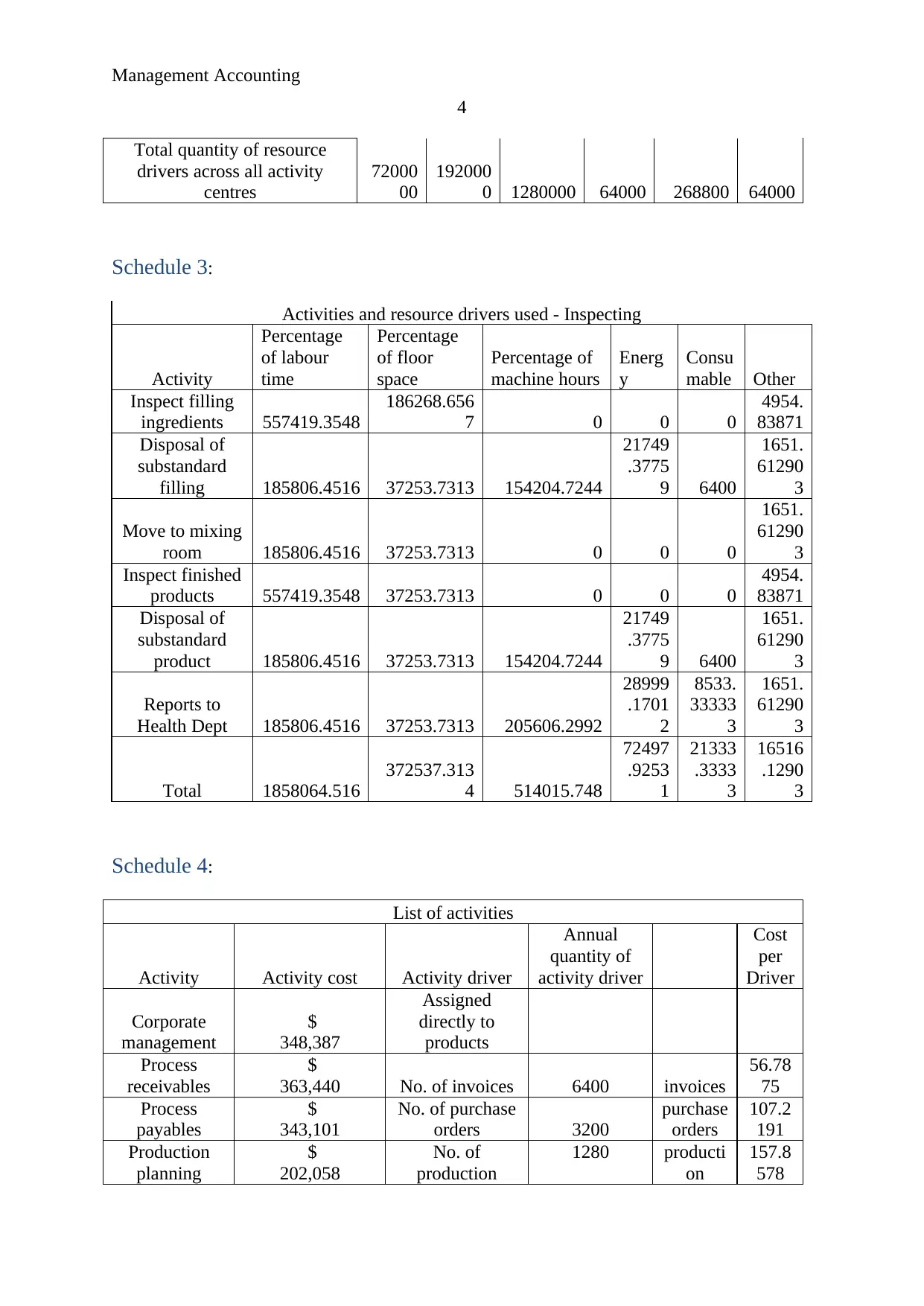

Total quantity of resource

drivers across all activity

centres

72000

00

192000

0 1280000 64000 268800 64000

Schedule 3:

Activities and resource drivers used - Inspecting

Activity

Percentage

of labour

time

Percentage

of floor

space

Percentage of

machine hours

Energ

y

Consu

mable Other

Inspect filling

ingredients 557419.3548

186268.656

7 0 0 0

4954.

83871

Disposal of

substandard

filling 185806.4516 37253.7313 154204.7244

21749

.3775

9 6400

1651.

61290

3

Move to mixing

room 185806.4516 37253.7313 0 0 0

1651.

61290

3

Inspect finished

products 557419.3548 37253.7313 0 0 0

4954.

83871

Disposal of

substandard

product 185806.4516 37253.7313 154204.7244

21749

.3775

9 6400

1651.

61290

3

Reports to

Health Dept 185806.4516 37253.7313 205606.2992

28999

.1701

2

8533.

33333

3

1651.

61290

3

Total 1858064.516

372537.313

4 514015.748

72497

.9253

1

21333

.3333

3

16516

.1290

3

Schedule 4:

List of activities

Activity Activity cost Activity driver

Annual

quantity of

activity driver

Cost

per

Driver

Corporate

management

$

348,387

Assigned

directly to

products

Process

receivables

$

363,440 No. of invoices 6400 invoices

56.78

75

Process

payables

$

343,101

No. of purchase

orders 3200

purchase

orders

107.2

191

Production

planning

$

202,058

No. of

production

1280 producti

on

157.8

578

4

Total quantity of resource

drivers across all activity

centres

72000

00

192000

0 1280000 64000 268800 64000

Schedule 3:

Activities and resource drivers used - Inspecting

Activity

Percentage

of labour

time

Percentage

of floor

space

Percentage of

machine hours

Energ

y

Consu

mable Other

Inspect filling

ingredients 557419.3548

186268.656

7 0 0 0

4954.

83871

Disposal of

substandard

filling 185806.4516 37253.7313 154204.7244

21749

.3775

9 6400

1651.

61290

3

Move to mixing

room 185806.4516 37253.7313 0 0 0

1651.

61290

3

Inspect finished

products 557419.3548 37253.7313 0 0 0

4954.

83871

Disposal of

substandard

product 185806.4516 37253.7313 154204.7244

21749

.3775

9 6400

1651.

61290

3

Reports to

Health Dept 185806.4516 37253.7313 205606.2992

28999

.1701

2

8533.

33333

3

1651.

61290

3

Total 1858064.516

372537.313

4 514015.748

72497

.9253

1

21333

.3333

3

16516

.1290

3

Schedule 4:

List of activities

Activity Activity cost Activity driver

Annual

quantity of

activity driver

Cost

per

Driver

Corporate

management

$

348,387

Assigned

directly to

products

Process

receivables

$

363,440 No. of invoices 6400 invoices

56.78

75

Process

payables

$

343,101

No. of purchase

orders 3200

purchase

orders

107.2

191

Production

planning

$

202,058

No. of

production

1280 producti

on

157.8

578

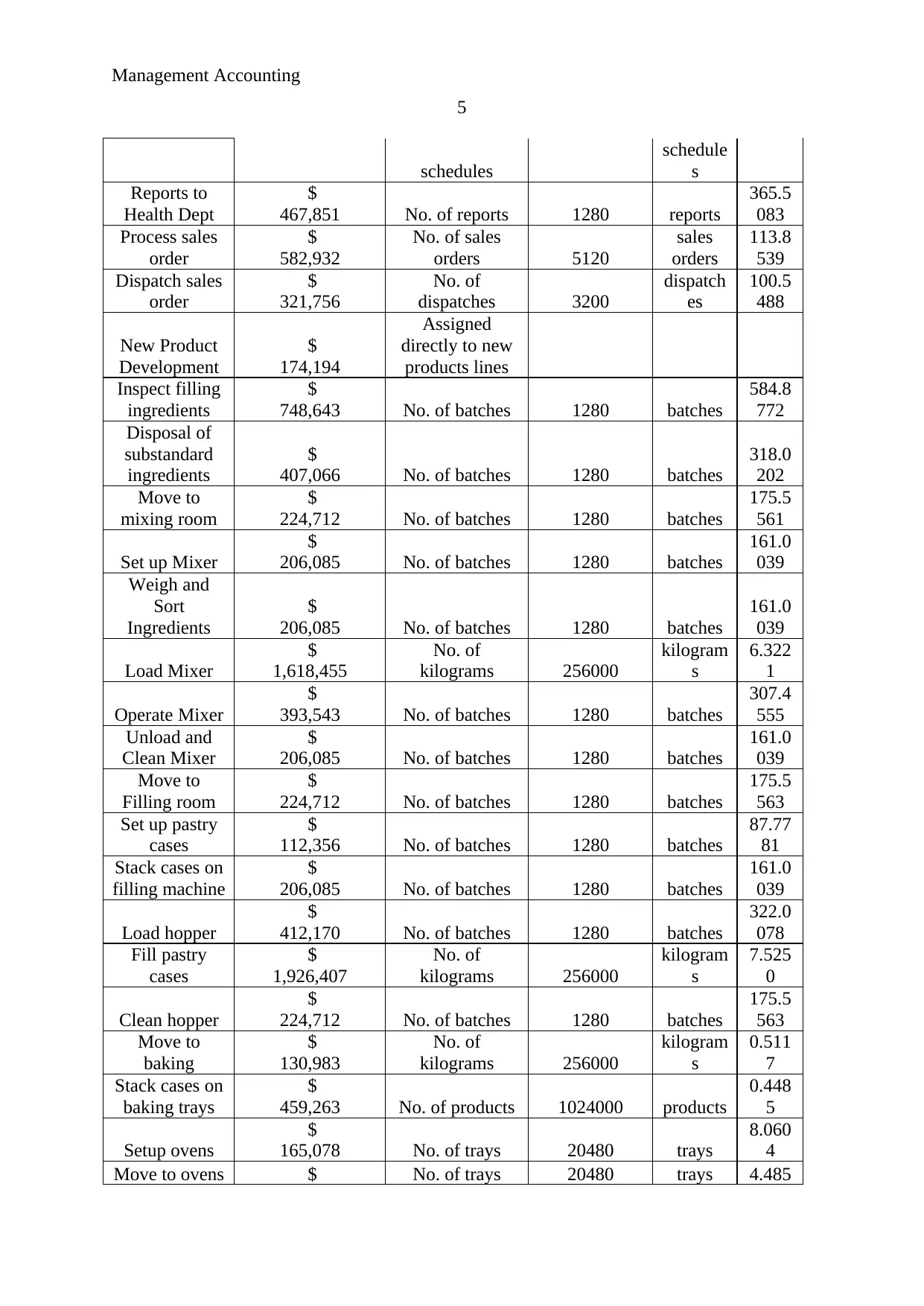

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

5

schedules

schedule

s

Reports to

Health Dept

$

467,851 No. of reports 1280 reports

365.5

083

Process sales

order

$

582,932

No. of sales

orders 5120

sales

orders

113.8

539

Dispatch sales

order

$

321,756

No. of

dispatches 3200

dispatch

es

100.5

488

New Product

Development

$

174,194

Assigned

directly to new

products lines

Inspect filling

ingredients

$

748,643 No. of batches 1280 batches

584.8

772

Disposal of

substandard

ingredients

$

407,066 No. of batches 1280 batches

318.0

202

Move to

mixing room

$

224,712 No. of batches 1280 batches

175.5

561

Set up Mixer

$

206,085 No. of batches 1280 batches

161.0

039

Weigh and

Sort

Ingredients

$

206,085 No. of batches 1280 batches

161.0

039

Load Mixer

$

1,618,455

No. of

kilograms 256000

kilogram

s

6.322

1

Operate Mixer

$

393,543 No. of batches 1280 batches

307.4

555

Unload and

Clean Mixer

$

206,085 No. of batches 1280 batches

161.0

039

Move to

Filling room

$

224,712 No. of batches 1280 batches

175.5

563

Set up pastry

cases

$

112,356 No. of batches 1280 batches

87.77

81

Stack cases on

filling machine

$

206,085 No. of batches 1280 batches

161.0

039

Load hopper

$

412,170 No. of batches 1280 batches

322.0

078

Fill pastry

cases

$

1,926,407

No. of

kilograms 256000

kilogram

s

7.525

0

Clean hopper

$

224,712 No. of batches 1280 batches

175.5

563

Move to

baking

$

130,983

No. of

kilograms 256000

kilogram

s

0.511

7

Stack cases on

baking trays

$

459,263 No. of products 1024000 products

0.448

5

Setup ovens

$

165,078 No. of trays 20480 trays

8.060

4

Move to ovens $ No. of trays 20480 trays 4.485

5

schedules

schedule

s

Reports to

Health Dept

$

467,851 No. of reports 1280 reports

365.5

083

Process sales

order

$

582,932

No. of sales

orders 5120

sales

orders

113.8

539

Dispatch sales

order

$

321,756

No. of

dispatches 3200

dispatch

es

100.5

488

New Product

Development

$

174,194

Assigned

directly to new

products lines

Inspect filling

ingredients

$

748,643 No. of batches 1280 batches

584.8

772

Disposal of

substandard

ingredients

$

407,066 No. of batches 1280 batches

318.0

202

Move to

mixing room

$

224,712 No. of batches 1280 batches

175.5

561

Set up Mixer

$

206,085 No. of batches 1280 batches

161.0

039

Weigh and

Sort

Ingredients

$

206,085 No. of batches 1280 batches

161.0

039

Load Mixer

$

1,618,455

No. of

kilograms 256000

kilogram

s

6.322

1

Operate Mixer

$

393,543 No. of batches 1280 batches

307.4

555

Unload and

Clean Mixer

$

206,085 No. of batches 1280 batches

161.0

039

Move to

Filling room

$

224,712 No. of batches 1280 batches

175.5

563

Set up pastry

cases

$

112,356 No. of batches 1280 batches

87.77

81

Stack cases on

filling machine

$

206,085 No. of batches 1280 batches

161.0

039

Load hopper

$

412,170 No. of batches 1280 batches

322.0

078

Fill pastry

cases

$

1,926,407

No. of

kilograms 256000

kilogram

s

7.525

0

Clean hopper

$

224,712 No. of batches 1280 batches

175.5

563

Move to

baking

$

130,983

No. of

kilograms 256000

kilogram

s

0.511

7

Stack cases on

baking trays

$

459,263 No. of products 1024000 products

0.448

5

Setup ovens

$

165,078 No. of trays 20480 trays

8.060

4

Move to ovens $ No. of trays 20480 trays 4.485

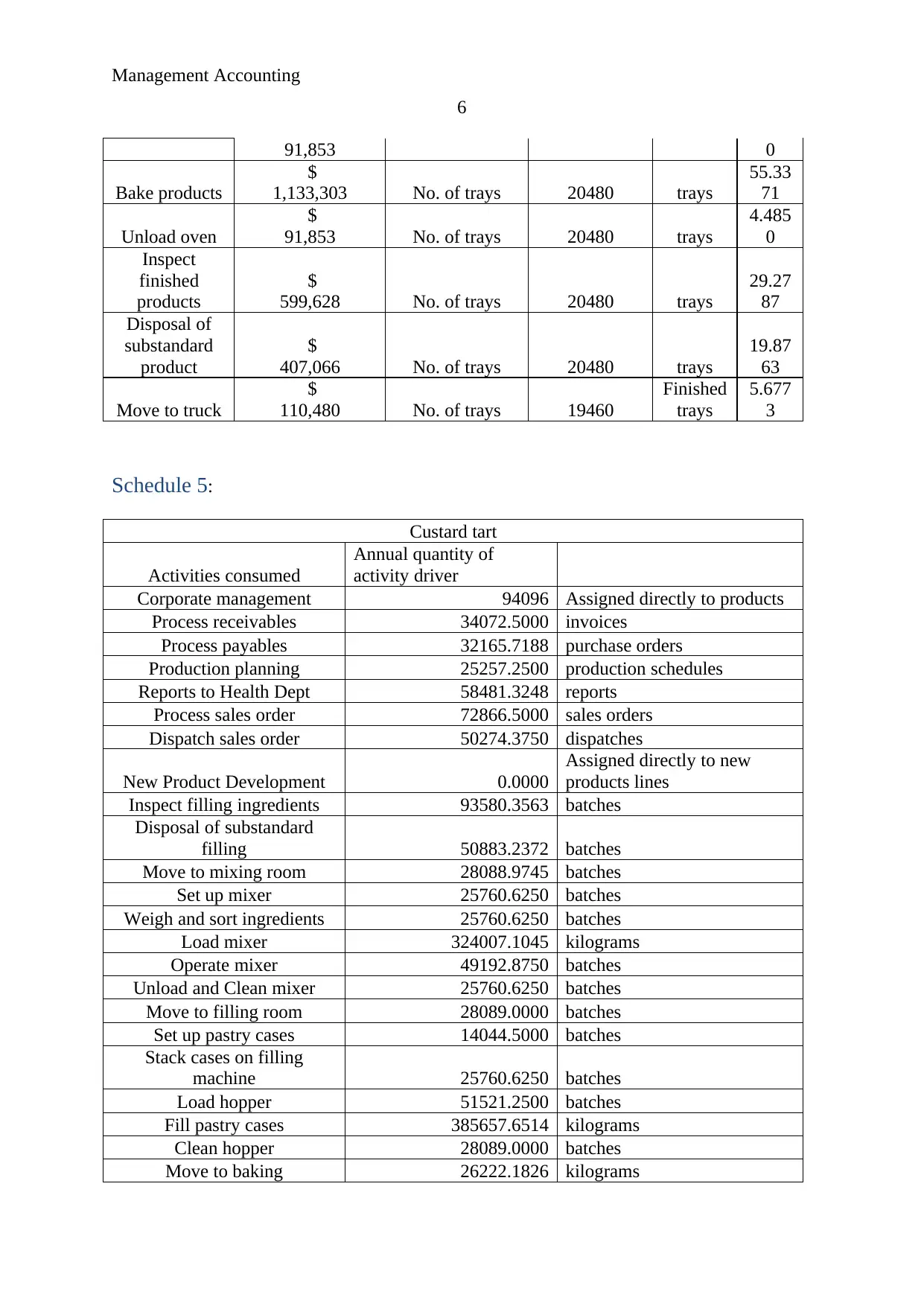

Management Accounting

6

91,853 0

Bake products

$

1,133,303 No. of trays 20480 trays

55.33

71

Unload oven

$

91,853 No. of trays 20480 trays

4.485

0

Inspect

finished

products

$

599,628 No. of trays 20480 trays

29.27

87

Disposal of

substandard

product

$

407,066 No. of trays 20480 trays

19.87

63

Move to truck

$

110,480 No. of trays 19460

Finished

trays

5.677

3

Schedule 5:

Custard tart

Activities consumed

Annual quantity of

activity driver

Corporate management 94096 Assigned directly to products

Process receivables 34072.5000 invoices

Process payables 32165.7188 purchase orders

Production planning 25257.2500 production schedules

Reports to Health Dept 58481.3248 reports

Process sales order 72866.5000 sales orders

Dispatch sales order 50274.3750 dispatches

New Product Development 0.0000

Assigned directly to new

products lines

Inspect filling ingredients 93580.3563 batches

Disposal of substandard

filling 50883.2372 batches

Move to mixing room 28088.9745 batches

Set up mixer 25760.6250 batches

Weigh and sort ingredients 25760.6250 batches

Load mixer 324007.1045 kilograms

Operate mixer 49192.8750 batches

Unload and Clean mixer 25760.6250 batches

Move to filling room 28089.0000 batches

Set up pastry cases 14044.5000 batches

Stack cases on filling

machine 25760.6250 batches

Load hopper 51521.2500 batches

Fill pastry cases 385657.6514 kilograms

Clean hopper 28089.0000 batches

Move to baking 26222.1826 kilograms

6

91,853 0

Bake products

$

1,133,303 No. of trays 20480 trays

55.33

71

Unload oven

$

91,853 No. of trays 20480 trays

4.485

0

Inspect

finished

products

$

599,628 No. of trays 20480 trays

29.27

87

Disposal of

substandard

product

$

407,066 No. of trays 20480 trays

19.87

63

Move to truck

$

110,480 No. of trays 19460

Finished

trays

5.677

3

Schedule 5:

Custard tart

Activities consumed

Annual quantity of

activity driver

Corporate management 94096 Assigned directly to products

Process receivables 34072.5000 invoices

Process payables 32165.7188 purchase orders

Production planning 25257.2500 production schedules

Reports to Health Dept 58481.3248 reports

Process sales order 72866.5000 sales orders

Dispatch sales order 50274.3750 dispatches

New Product Development 0.0000

Assigned directly to new

products lines

Inspect filling ingredients 93580.3563 batches

Disposal of substandard

filling 50883.2372 batches

Move to mixing room 28088.9745 batches

Set up mixer 25760.6250 batches

Weigh and sort ingredients 25760.6250 batches

Load mixer 324007.1045 kilograms

Operate mixer 49192.8750 batches

Unload and Clean mixer 25760.6250 batches

Move to filling room 28089.0000 batches

Set up pastry cases 14044.5000 batches

Stack cases on filling

machine 25760.6250 batches

Load hopper 51521.2500 batches

Fill pastry cases 385657.6514 kilograms

Clean hopper 28089.0000 batches

Move to baking 26222.1826 kilograms

Management Accounting

7

Stack cases on baking trays 91852.6000 products

Setup ovens 16523.9209 trays

Move to ovens 9194.2700 trays

Bake products 113440.9741 trays

Unload oven 9194.2700 trays

Inspect finished products 0.0000 trays

Disposal of substandard

product 0.0000 trays

Move to truck 11638.4378 Finished trays

Direct Materials 3

per kilogram

Assigned directly to products

Current Market Selling Price 9 per unit of product

Batch size 1300

Annual Volume 205000

* All Calculations to 4

decimal places

Total Indirect Cost 1801476.773

Per Unit Indirect cost 8.7877

Schedule 6:

Apple and Cinnamon Danish

Activities consumed

Annual quantity of

activity driver

Corporate management 11475 Assigned directly to products

Process receivables 11357.5000 invoices

Process payables 10721.9063 purchase orders

Production planning 9471.4688 production schedules

Reports to Health Dept 21930.4968 reports

Process sales order 21632.2422 sales orders

Dispatch sales order 10054.8750 dispatches

New Product Development 88576.0000

Assigned directly to new

products lines

Inspect filling ingredients 29243.8613 batches

Disposal of substandard

filling 15901.0116 batches

Move to mixing room 8777.8045 batches

Set up mixer 8050.1953 batches

Weigh and sort ingredients 8050.1953 batches

Load mixer 79026.1230 kilograms

Operate mixer 15372.7734 batches

Unload and Clean mixer 8050.1953 batches

Move to filling room 8777.8125 batches

Set up pastry cases 4388.9063 batches

7

Stack cases on baking trays 91852.6000 products

Setup ovens 16523.9209 trays

Move to ovens 9194.2700 trays

Bake products 113440.9741 trays

Unload oven 9194.2700 trays

Inspect finished products 0.0000 trays

Disposal of substandard

product 0.0000 trays

Move to truck 11638.4378 Finished trays

Direct Materials 3

per kilogram

Assigned directly to products

Current Market Selling Price 9 per unit of product

Batch size 1300

Annual Volume 205000

* All Calculations to 4

decimal places

Total Indirect Cost 1801476.773

Per Unit Indirect cost 8.7877

Schedule 6:

Apple and Cinnamon Danish

Activities consumed

Annual quantity of

activity driver

Corporate management 11475 Assigned directly to products

Process receivables 11357.5000 invoices

Process payables 10721.9063 purchase orders

Production planning 9471.4688 production schedules

Reports to Health Dept 21930.4968 reports

Process sales order 21632.2422 sales orders

Dispatch sales order 10054.8750 dispatches

New Product Development 88576.0000

Assigned directly to new

products lines

Inspect filling ingredients 29243.8613 batches

Disposal of substandard

filling 15901.0116 batches

Move to mixing room 8777.8045 batches

Set up mixer 8050.1953 batches

Weigh and sort ingredients 8050.1953 batches

Load mixer 79026.1230 kilograms

Operate mixer 15372.7734 batches

Unload and Clean mixer 8050.1953 batches

Move to filling room 8777.8125 batches

Set up pastry cases 4388.9063 batches

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

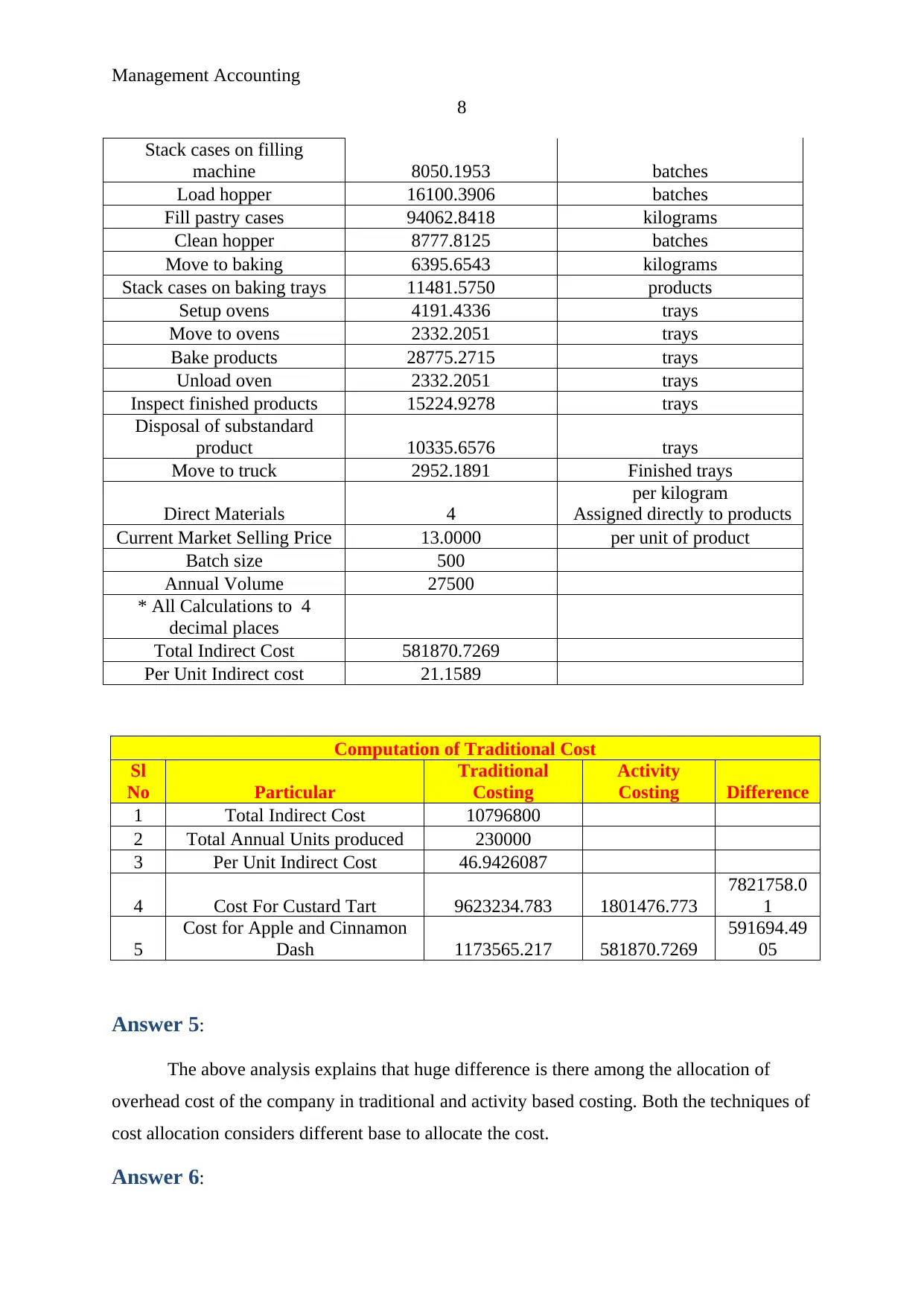

Management Accounting

8

Stack cases on filling

machine 8050.1953 batches

Load hopper 16100.3906 batches

Fill pastry cases 94062.8418 kilograms

Clean hopper 8777.8125 batches

Move to baking 6395.6543 kilograms

Stack cases on baking trays 11481.5750 products

Setup ovens 4191.4336 trays

Move to ovens 2332.2051 trays

Bake products 28775.2715 trays

Unload oven 2332.2051 trays

Inspect finished products 15224.9278 trays

Disposal of substandard

product 10335.6576 trays

Move to truck 2952.1891 Finished trays

Direct Materials 4

per kilogram

Assigned directly to products

Current Market Selling Price 13.0000 per unit of product

Batch size 500

Annual Volume 27500

* All Calculations to 4

decimal places

Total Indirect Cost 581870.7269

Per Unit Indirect cost 21.1589

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 10796800

2 Total Annual Units produced 230000

3 Per Unit Indirect Cost 46.9426087

4 Cost For Custard Tart 9623234.783 1801476.773

7821758.0

1

5

Cost for Apple and Cinnamon

Dash 1173565.217 581870.7269

591694.49

05

Answer 5:

The above analysis explains that huge difference is there among the allocation of

overhead cost of the company in traditional and activity based costing. Both the techniques of

cost allocation considers different base to allocate the cost.

Answer 6:

8

Stack cases on filling

machine 8050.1953 batches

Load hopper 16100.3906 batches

Fill pastry cases 94062.8418 kilograms

Clean hopper 8777.8125 batches

Move to baking 6395.6543 kilograms

Stack cases on baking trays 11481.5750 products

Setup ovens 4191.4336 trays

Move to ovens 2332.2051 trays

Bake products 28775.2715 trays

Unload oven 2332.2051 trays

Inspect finished products 15224.9278 trays

Disposal of substandard

product 10335.6576 trays

Move to truck 2952.1891 Finished trays

Direct Materials 4

per kilogram

Assigned directly to products

Current Market Selling Price 13.0000 per unit of product

Batch size 500

Annual Volume 27500

* All Calculations to 4

decimal places

Total Indirect Cost 581870.7269

Per Unit Indirect cost 21.1589

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 10796800

2 Total Annual Units produced 230000

3 Per Unit Indirect Cost 46.9426087

4 Cost For Custard Tart 9623234.783 1801476.773

7821758.0

1

5

Cost for Apple and Cinnamon

Dash 1173565.217 581870.7269

591694.49

05

Answer 5:

The above analysis explains that huge difference is there among the allocation of

overhead cost of the company in traditional and activity based costing. Both the techniques of

cost allocation considers different base to allocate the cost.

Answer 6:

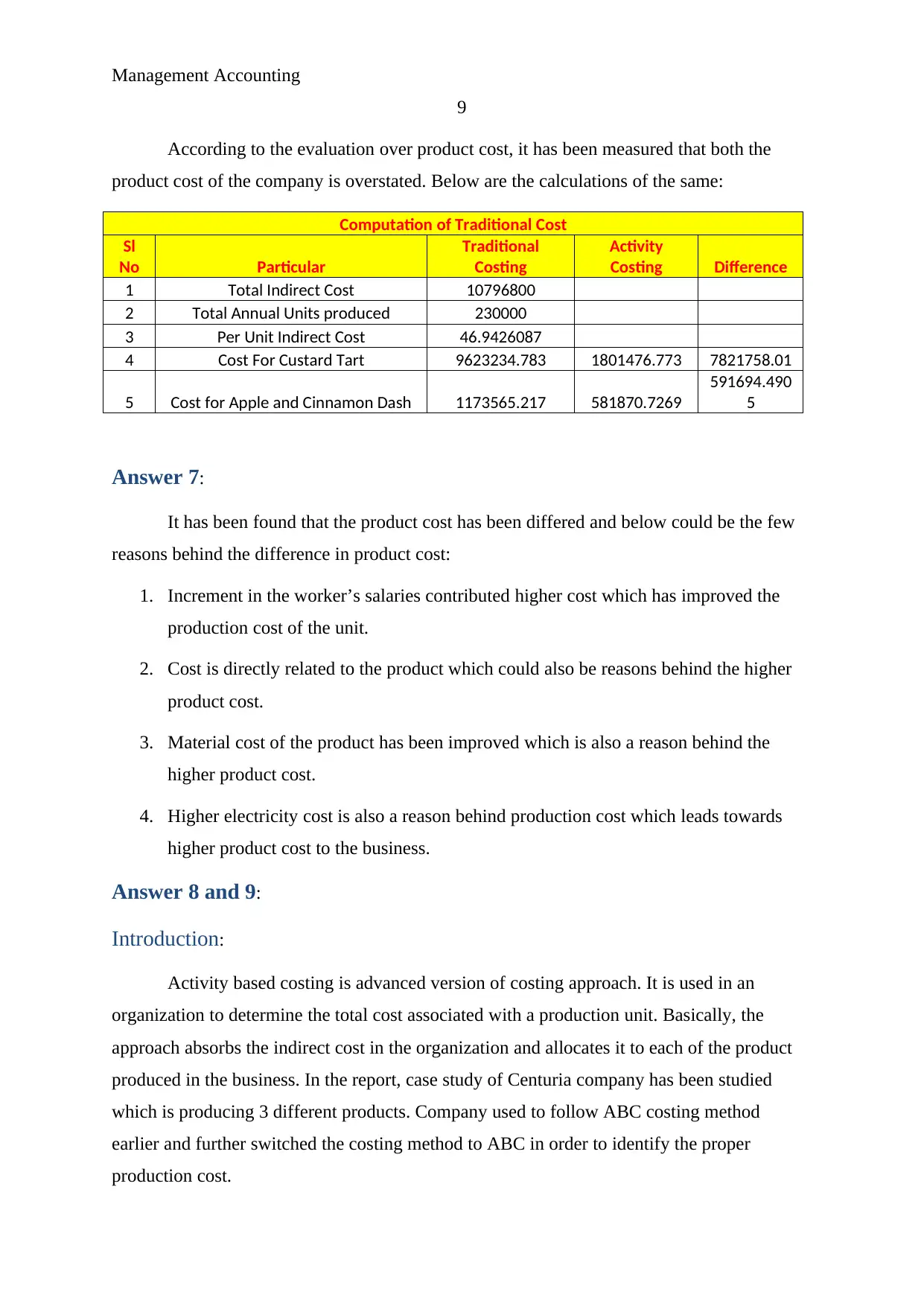

Management Accounting

9

According to the evaluation over product cost, it has been measured that both the

product cost of the company is overstated. Below are the calculations of the same:

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 10796800

2 Total Annual Units produced 230000

3 Per Unit Indirect Cost 46.9426087

4 Cost For Custard Tart 9623234.783 1801476.773 7821758.01

5 Cost for Apple and Cinnamon Dash 1173565.217 581870.7269

591694.490

5

Answer 7:

It has been found that the product cost has been differed and below could be the few

reasons behind the difference in product cost:

1. Increment in the worker’s salaries contributed higher cost which has improved the

production cost of the unit.

2. Cost is directly related to the product which could also be reasons behind the higher

product cost.

3. Material cost of the product has been improved which is also a reason behind the

higher product cost.

4. Higher electricity cost is also a reason behind production cost which leads towards

higher product cost to the business.

Answer 8 and 9:

Introduction:

Activity based costing is advanced version of costing approach. It is used in an

organization to determine the total cost associated with a production unit. Basically, the

approach absorbs the indirect cost in the organization and allocates it to each of the product

produced in the business. In the report, case study of Centuria company has been studied

which is producing 3 different products. Company used to follow ABC costing method

earlier and further switched the costing method to ABC in order to identify the proper

production cost.

9

According to the evaluation over product cost, it has been measured that both the

product cost of the company is overstated. Below are the calculations of the same:

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 10796800

2 Total Annual Units produced 230000

3 Per Unit Indirect Cost 46.9426087

4 Cost For Custard Tart 9623234.783 1801476.773 7821758.01

5 Cost for Apple and Cinnamon Dash 1173565.217 581870.7269

591694.490

5

Answer 7:

It has been found that the product cost has been differed and below could be the few

reasons behind the difference in product cost:

1. Increment in the worker’s salaries contributed higher cost which has improved the

production cost of the unit.

2. Cost is directly related to the product which could also be reasons behind the higher

product cost.

3. Material cost of the product has been improved which is also a reason behind the

higher product cost.

4. Higher electricity cost is also a reason behind production cost which leads towards

higher product cost to the business.

Answer 8 and 9:

Introduction:

Activity based costing is advanced version of costing approach. It is used in an

organization to determine the total cost associated with a production unit. Basically, the

approach absorbs the indirect cost in the organization and allocates it to each of the product

produced in the business. In the report, case study of Centuria company has been studied

which is producing 3 different products. Company used to follow ABC costing method

earlier and further switched the costing method to ABC in order to identify the proper

production cost.

Management Accounting

10

Traditional costing system:

Traditional costing system is one of the oldest techniques in cost accounting. In this

cost accounting method, cost of production house is collected and allocated to each of cost

driver in proportion basis. Average rate of overhead is used in this method to assign the cost

to each of the production cost. This method assists an organization to draw all the indirect

and there overhead cost in the production department of the company (Drury, 2013).

The main deficiency of this method is cost assignment process. The total indirect

production cost of the company is assigned to production department on the basis of overhead

cost. It directly impact over the management decision (Garrison, Noreen, Brewer and

McGowan, 2010). However, in case of ABC costing, cost is assigned to each of the

production house on the basis of their cost centre.

In case of Centuria, traditional costing system has not played a vital role. This costing

system has manipulated the decision of management through discovering the wrong product

cost. Low maintained reduction in product and various other issues have been faced by the

company because of it. To conclude, this method is not a good one to make decisions and

calculate the product cost of the company.

Activity based costing system:

Activity based costing system is new method in cost accounting. In this cost

accounting method, cost of production house is collected and allocated to each of cost driver

on the basis of their cost centre. Cost centre and relevant base of production house is used in

this method to assign the cost to each of the production cost (Hansen, Mowen and Guan,

2009). This method assists an organization to draw all the indirect and there overhead cost in

the production department of the company.

10

Traditional costing system:

Traditional costing system is one of the oldest techniques in cost accounting. In this

cost accounting method, cost of production house is collected and allocated to each of cost

driver in proportion basis. Average rate of overhead is used in this method to assign the cost

to each of the production cost. This method assists an organization to draw all the indirect

and there overhead cost in the production department of the company (Drury, 2013).

The main deficiency of this method is cost assignment process. The total indirect

production cost of the company is assigned to production department on the basis of overhead

cost. It directly impact over the management decision (Garrison, Noreen, Brewer and

McGowan, 2010). However, in case of ABC costing, cost is assigned to each of the

production house on the basis of their cost centre.

In case of Centuria, traditional costing system has not played a vital role. This costing

system has manipulated the decision of management through discovering the wrong product

cost. Low maintained reduction in product and various other issues have been faced by the

company because of it. To conclude, this method is not a good one to make decisions and

calculate the product cost of the company.

Activity based costing system:

Activity based costing system is new method in cost accounting. In this cost

accounting method, cost of production house is collected and allocated to each of cost driver

on the basis of their cost centre. Cost centre and relevant base of production house is used in

this method to assign the cost to each of the production cost (Hansen, Mowen and Guan,

2009). This method assists an organization to draw all the indirect and there overhead cost in

the production department of the company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

11

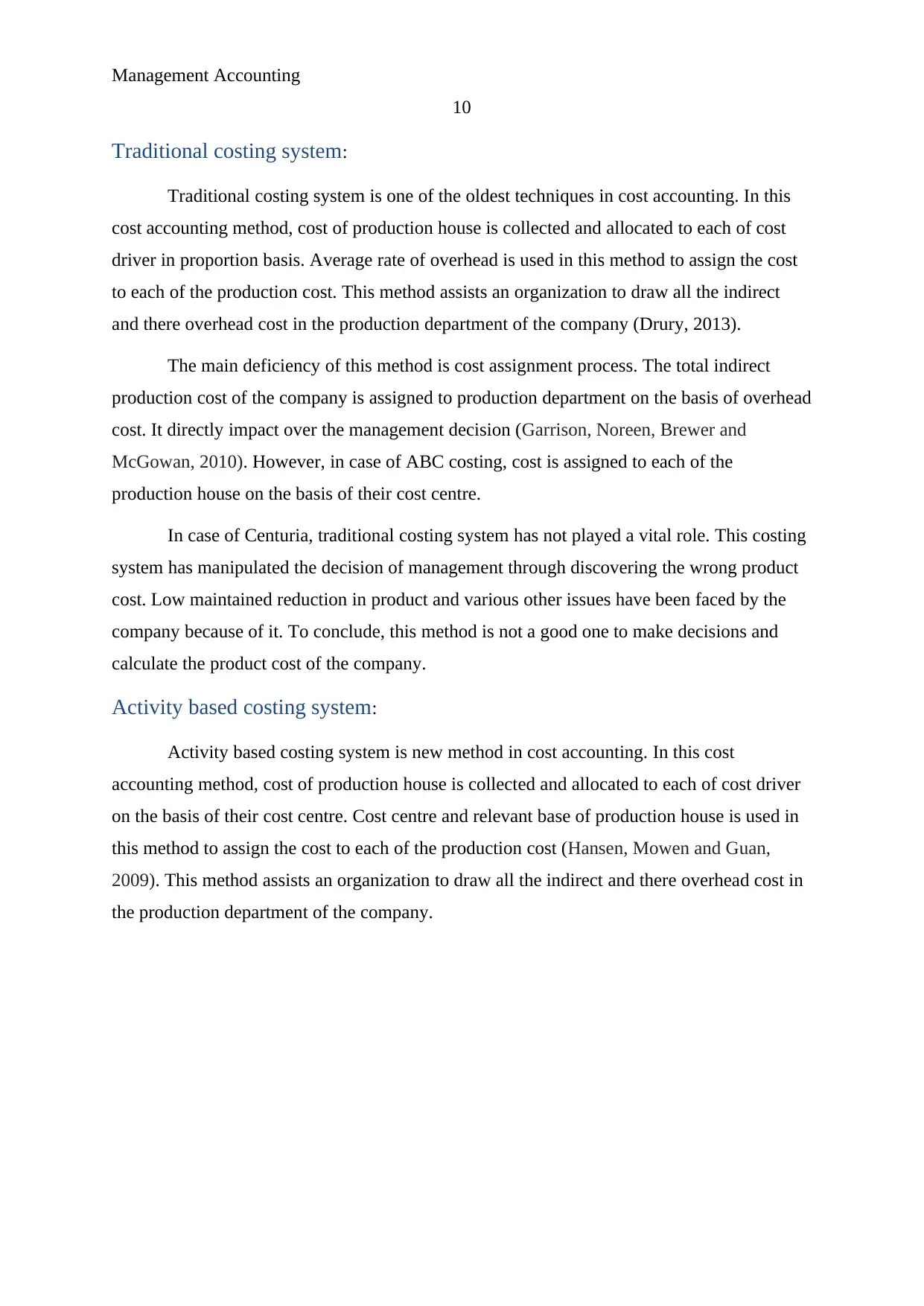

(Marshall, McManus and Viele, 2011)

The main deficiency of this method is complexity in cost assignment process. The

total indirect production cost of the company is assigned to production department through

evaluating and conducting depth analysis on each of the indirect cost. Unlike traditional

costing system, cost is assigned to each of the production house on the basis of their cost

centre (Hopper, Northcott and Scapens, 2009).

In case of Centuria, activity based costing system has played a vital role. This costing

system has improved the decision of management through discovering the correct product

cost. Various issues of the company have been resolved because of this method. To conclude,

this method is a good one to make decisions and calculate the product cost of the company.

Management accounting factor:

Centuria company could put a concern on the below points in order to evaluate

whether the company should adopt the ABC system over traditional costing system:

Nature:

In case of Centuria, the company is totally based on production. Hence it becomes

important for the business to measure production cost correctly. ABC costing would help the

company to find the same (Horngren, 2009).

11

(Marshall, McManus and Viele, 2011)

The main deficiency of this method is complexity in cost assignment process. The

total indirect production cost of the company is assigned to production department through

evaluating and conducting depth analysis on each of the indirect cost. Unlike traditional

costing system, cost is assigned to each of the production house on the basis of their cost

centre (Hopper, Northcott and Scapens, 2009).

In case of Centuria, activity based costing system has played a vital role. This costing

system has improved the decision of management through discovering the correct product

cost. Various issues of the company have been resolved because of this method. To conclude,

this method is a good one to make decisions and calculate the product cost of the company.

Management accounting factor:

Centuria company could put a concern on the below points in order to evaluate

whether the company should adopt the ABC system over traditional costing system:

Nature:

In case of Centuria, the company is totally based on production. Hence it becomes

important for the business to measure production cost correctly. ABC costing would help the

company to find the same (Horngren, 2009).

Management Accounting

12

Amount:

In case of Centuria, it is important for the company to calculated exact amount of

production for each of the product. Hence, it becomes important for the business to measure

production cost correctly. ABC costing would help the company to find the same.

Rigidness of employees:

Company is using traditional costing system from last 15 years. Hence, it would be bit

tough for the employees of the company to shift to ABC. A proper discussion must be done

by the company before making any decision (Silvi, Bartolini and Hines, 2017).

Total number of product:

In case of Centuria, the company is producing 2 products. Hence, it becomes

important for the business to measure production cost of each of the product correctly. ABC

costing would help the company to find the same.

Benefit of ABC costing:

More to it, the ABC costing would help the business in below manner:

classify the correct cost on the basis of associated product and services

ABC technique is recognized concerned and appreciated in practice life.

It improves the profit and prosperity of a production house.

Differentiate in services and products of a manufacturing house (Kaplan and

Anderson, 2013).

Cost and limitation of ABC costing:

The analysis explains that huge difference is there among the allocation of overhead

cost of the company in traditional and activity based costing. Both the techniques of cost

allocation considers different base to allocate the cost.

Further, it has been measured that the outcome from ABC method is not always

reliable. It also contains few error which could affect over the management decision of the

company.

Conclusion:

12

Amount:

In case of Centuria, it is important for the company to calculated exact amount of

production for each of the product. Hence, it becomes important for the business to measure

production cost correctly. ABC costing would help the company to find the same.

Rigidness of employees:

Company is using traditional costing system from last 15 years. Hence, it would be bit

tough for the employees of the company to shift to ABC. A proper discussion must be done

by the company before making any decision (Silvi, Bartolini and Hines, 2017).

Total number of product:

In case of Centuria, the company is producing 2 products. Hence, it becomes

important for the business to measure production cost of each of the product correctly. ABC

costing would help the company to find the same.

Benefit of ABC costing:

More to it, the ABC costing would help the business in below manner:

classify the correct cost on the basis of associated product and services

ABC technique is recognized concerned and appreciated in practice life.

It improves the profit and prosperity of a production house.

Differentiate in services and products of a manufacturing house (Kaplan and

Anderson, 2013).

Cost and limitation of ABC costing:

The analysis explains that huge difference is there among the allocation of overhead

cost of the company in traditional and activity based costing. Both the techniques of cost

allocation considers different base to allocate the cost.

Further, it has been measured that the outcome from ABC method is not always

reliable. It also contains few error which could affect over the management decision of the

company.

Conclusion:

Management Accounting

13

On the basis of calculations over company, a huge difference has been found among

the ABC costing and traditional costing method. The study brief that ABC costing method

would make it easier for the business to reach over better conclusion and ait would also help

the management to make further decisions accordingly for the betterment of the company.

Centuria Company is recommended to use ABC costing method to improve overall process

of the business.

13

On the basis of calculations over company, a huge difference has been found among

the ABC costing and traditional costing method. The study brief that ABC costing method

would make it easier for the business to reach over better conclusion and ait would also help

the management to make further decisions accordingly for the betterment of the company.

Centuria Company is recommended to use ABC costing method to improve overall process

of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

14

References:

DRURY, C. M. (2013). Management and cost accounting. Springer.

Garrison, R. H., Noreen, E. W., Brewer, P. C., and McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Hansen, D., Mowen, M., and Guan, L. (2009). Cost management: accounting and control.

Cengage Learning.

Hopper, T., Northcott, D., and Scapens, R. (2009). Issues in management accounting.

Pearson education.

Horngren, C. T. (2009). Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Kaplan, R., and Anderson, S. R. (2013). Time-driven activity-based costing: a simpler and

more powerful path to higher profits. Harvard business press.

Marshall, D. H., McManus, W. W., and Viele, D. F. (2011). Accounting. McGraw-Hill

Irwin,.

Silvi, R., Bartolini, M., and Hines, P. (2017). Strategic cost management and lean thinking: A

framework for management accounting. Issues in management accounting. Pearson

education.

14

References:

DRURY, C. M. (2013). Management and cost accounting. Springer.

Garrison, R. H., Noreen, E. W., Brewer, P. C., and McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Hansen, D., Mowen, M., and Guan, L. (2009). Cost management: accounting and control.

Cengage Learning.

Hopper, T., Northcott, D., and Scapens, R. (2009). Issues in management accounting.

Pearson education.

Horngren, C. T. (2009). Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Kaplan, R., and Anderson, S. R. (2013). Time-driven activity-based costing: a simpler and

more powerful path to higher profits. Harvard business press.

Marshall, D. H., McManus, W. W., and Viele, D. F. (2011). Accounting. McGraw-Hill

Irwin,.

Silvi, R., Bartolini, M., and Hines, P. (2017). Strategic cost management and lean thinking: A

framework for management accounting. Issues in management accounting. Pearson

education.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.